breaking the deadlock: unifying our federal student loan programs paul combe, president &ceo...

TRANSCRIPT

Breaking the Deadlock: Unifying Our Federal Student Loan Programs

Paul Combe, President &CEOAmerican Student Assistance

PESC 6th Annual Conference on Technology & Standards

April 7, 2009

Change is in the Air

• New presidential administration and new Congress

• Drumbeat within Congress and industry for federal aid simplification

• Student debt has become a social issue

2ASA Confidential and Proprietary Information

A Growing Social Issue

3ASA Confidential and Proprietary Information

• Rare opportunity to take advantage of broad consensus for reform

• If we could rebuild the federal college loan program, what would it look like?

4ASA Confidential and Proprietary Information

FFELP vs. DL

• Debate has missed the bigger issue – Education Debt is now the problem

• The major focus of the debate has been about delivery systems and which program costs government less

• Loan processing systems have become a market tool that can be used to restrict the range of consumer choice

• Competition between FFELP and DL has produced many positives that should not be lost in the future

5ASA Confidential and Proprietary Information

Break the Deadlock

• Time to move past FFELP versus DL

• Combine the best of both programs to create a single unified program that breaks the gridlock

• Create a single loan program with one delivery system that incorporates private and federal funding

• Greater focus on education debt management for ALL and a refocused role for GA’s…guaranteeing the borrowers’ success, not the lenders’

6ASA Confidential and Proprietary Information

Rebuilding with a Consumer Focus

• America has chosen debt as the primary method for funding higher education and therefore has a responsibility to help students manage their debt

• Federal student loan program should focus on borrower as “consumer”

– Consumer rights including:

• Real Open Choice

• Effective Competition

• Debt Management Services

• Education Debt Management = Entitlement

7ASA Confidential and Proprietary Information

ASA Confidential and Proprietary Information

Building a Market-Based Future

• Loan programs should use public and private capital

• Federal capital used as benchmark or “ceiling” on loan rate

• Benchmark rate set by an analogous market rate…FHA mortgage rates

• Federal guarantee only / No SAP

• Price / rate competition below benchmark

• Post Graduation Borrower Subsidies

• New GSC Under-treasury?

8

Single System

• Borrower should be able to choose any lender, at any school, with any guarantor, and have it processed just as efficiently

• DL mandatory on all schools’ lender list

• Low cost of entry … more competitors

• Federal System (COD)?

9ASA Confidential and Proprietary Information

ASA Confidential and Proprietary Information

What is Education Debt Management?

• Effective education debt management is not just due diligence with a prescribed amount of letters and phone calls

• It’s about using federal college loans as “teachable moments”:

– Use continuum of intervention / education activity (proactive and reactive) to target, engage, and impact the borrower’s financial wellness

– It is proactive and focused on getting the right information to the right borrower at the right time

– It is individualized and personalized

– Uses CRM tools

10

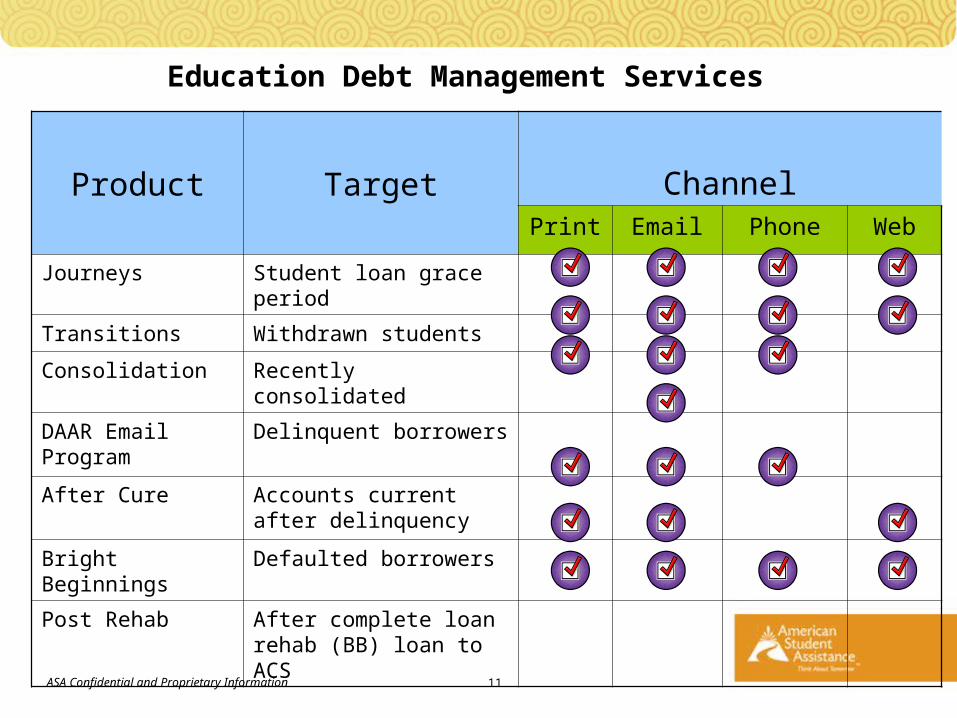

Education Debt Management Services

Product Target ChannelPrint Email Phone Web

Journeys Student loan grace period

Transitions Withdrawn students

Consolidation Recently consolidated

DAAR Email Program

Delinquent borrowers

After Cure Accounts current after delinquency

Bright Beginnings Defaulted borrowers

Post Rehab After complete loan rehab (BB) loan to ACS

11ASA Confidential and Proprietary Information

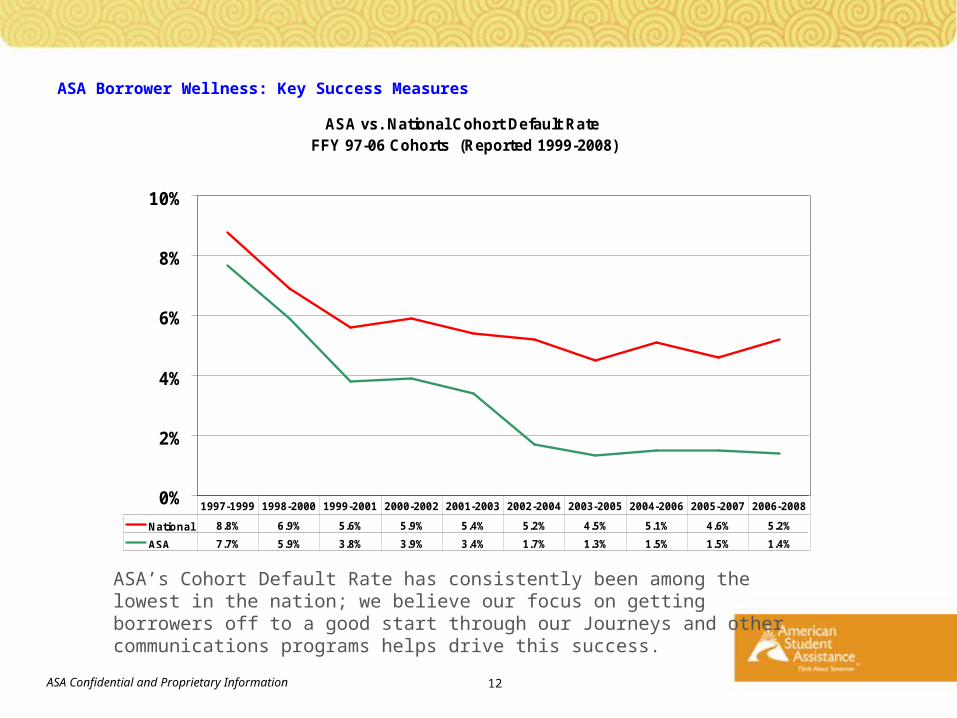

ASA vs. National Cohort Default Rate FFY 97-06 Cohorts (Reported 1999-2008)

0%

2%

4%

6%

8%

10%

National 8.8% 6.9% 5.6% 5.9% 5.4% 5.2% 4.5% 5.1% 4.6% 5.2%

ASA 7.7% 5.9% 3.8% 3.9% 3.4% 1.7% 1.3% 1.5% 1.5% 1.4%

1997-1999 1998-2000 1999-2001 2000-2002 2001-2003 2002-2004 2003-2005 2004-2006 2005-2007 2006-2008

ASA Borrower Wellness: Key Success Measures

ASA Confidential and Proprietary Information 12

ASA’s Cohort Default Rate has consistently been among the lowest in the nation; we believe our focus on getting borrowers off to a good start through our Journeys and other communications programs helps drive this success.

ASA Confidential and Proprietary Information 13

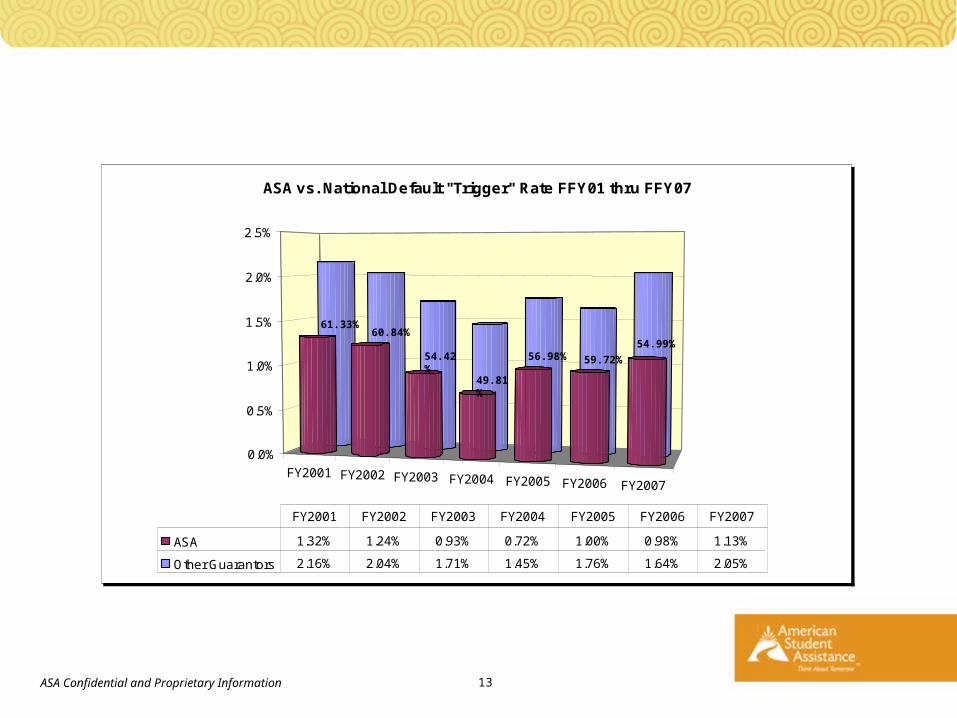

FY2001 FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

ASA vs. National Default "Trigger" Rate FFY01 thru FFY07

ASA 1.32% 1.24% 0.93% 0.72% 1.00% 0.98% 1.13%

Other Guarantors 2.16% 2.04% 1.71% 1.45% 1.76% 1.64% 2.05%

FY2001 FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

61.33%60.84%

54.42%

49.81%

56.98% 59.72%

54.99%

ASA Confidential and Proprietary Information

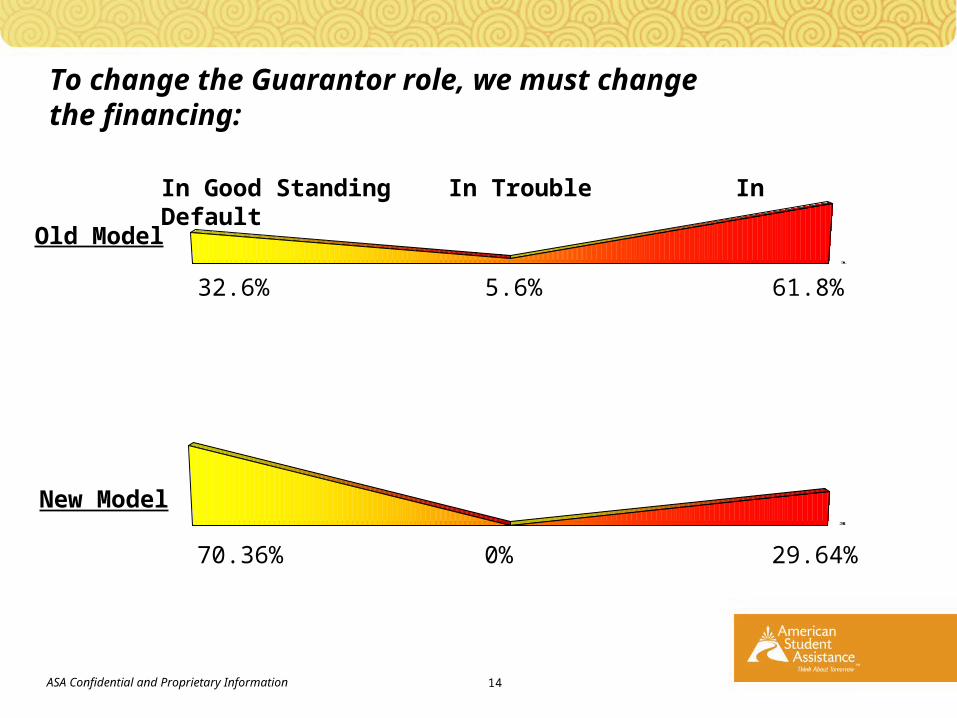

32.6% 5.6% 61.8%

Old Model

New Model

1

3

70.36% 0% 29.64%

In Good Standing In Trouble In Default

To change the Guarantor role, we must change the financing:

14

ASA Confidential and Proprietary Information

Questions? Suggestions? More Information?

• We want to hear from you!

• Join the discussion on ASA’s Policy Perspectives Blog: http://www.amsa.com/blogs/policyperspectives

• Please contact me with questions, suggestions and feedback:

15

American Student Assistance®

100 Cambridge Street, Suite 1600Boston, MA 02114

(800) 999-9080(617) 728-4670 F A X(800) 999-0923 T D D

www.amsa.com