brent saunders

TRANSCRIPT

Plenary Keynote

Eye Disease Remains a Significant and Growing Problem

Glaucoma is the second leading cause of blindness globally, according to WHO. Affecting 80 million by 2020.

Persistence rates are generally under 50% as early as the first year of treatment

As many as 80% of patients fail to use their drops regularly~3

Sources: Varma et al. Am J Ophthalmol 2012. CDC Statistics 2010 & 1995. WHO Statistics 2013 & 2015. Cowen and Company Ophthalmology 2015. Evaluate Pharma Glaucoma Report: published Aug 2015Source: 2007 DEWS guidelines. CDC 2014. NEI 2010.

Glaucoma

Dry eye is one the most prevalent ophthalmology disease in the general population with an estimated 15-18%

Dry eye is estimated to affect approximately 30 million patients in the U.S. There are two types of Dry Eye: aqueous-deficient and evaporative 30

million patients

in the US

Dry Eye

13.13.13 2.48 2.15 0.31 0.135

DiabeticNeuropathies

Wet AMD Dry AMD Retinal VeinOcclusion

OpticNeuritis

RetinitisPigmentosa

21million

patients in the US

US Prevalence (Millions)Retinal Disease

million patients

in the US

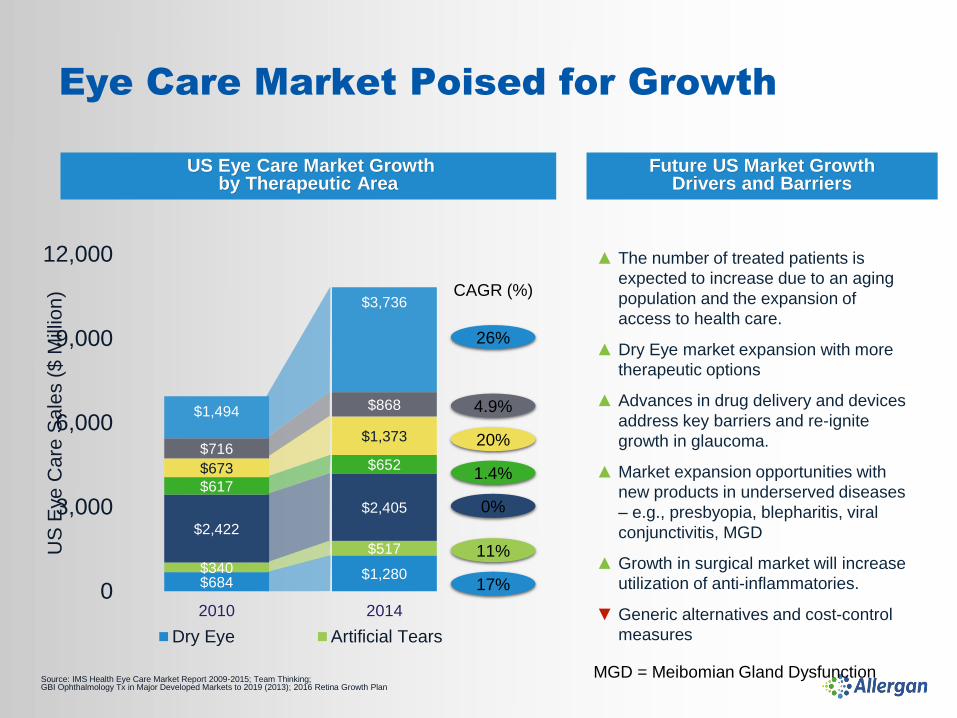

$684 $1,280$340$517

$2,422

$2,405$617

$652$673

$1,373$716

$868$1,494

$3,736

0

3,000

6,000

9,000

12,000

2010 2014

US

Eye

Car

e S

ales

($

Mill

ion)

Dry Eye Artificial Tears

Source: IMS Health Eye Care Market Report 2009-2015; Team Thinking; GBI Ophthalmology Tx in Major Developed Markets to 2019 (2013); 2016 Retina Growth Plan

Eye Care Market Poised for Growth

▲ The number of treated patients is expected to increase due to an aging population and the expansion of access to health care.

▲ Dry Eye market expansion with more therapeutic options

▲ Advances in drug delivery and devices address key barriers and re-ignite growth in glaucoma.

▲ Market expansion opportunities with new products in underserved diseases – e.g., presbyopia, blepharitis, viral conjunctivitis, MGD

▲ Growth in surgical market will increase utilization of anti-inflammatories.

▼ Generic alternatives and cost-control measures

MGD = Meibomian Gland Dysfunction

CAGR (%)

0%

11%

17%

1.4%

20%

4.9%

26%

Future US Market GrowthDrivers and Barriers

US Eye Care Market Growth by Therapeutic Area

Eye Care Ecosystem is Vibrant

Mynosys

Octata

SOURCE: Thomson Reuters, PitchBook database

A New Pharmaceutical Innovation Ecosystem

Fueled by Significant Investments

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

0.6

1.2

1.8

2.4

3.0

3.5

4.1

4.7

5.3

5.9

6.5

Ven

ture

cap

ital i

nves

ted,

$B

Num

ber

of b

iote

ch s

tart

ups

2010

2000

2005

19952014

Number of biotech startups

Venture capital invested, $B

• Continued VC funding

• Scientific creativity

• Professional management

Sustainability

Revenues of all NME-grade compounds launched in a given year cumulated for 7-8 years. Includes all innovative compounds classified as NME or BLA, excluding generics, biosimilars and NDA products (new derivatives, new formulations etc.)SOURCE: Evaluate 2014

14%Biotech & Start-up Companies

24%Regional PharmaNon-profit Academia Specialty

academia

Specialty

GLOBALPHARMA

Biotech & start-ups

Regional Pharma62%

Global Pharma

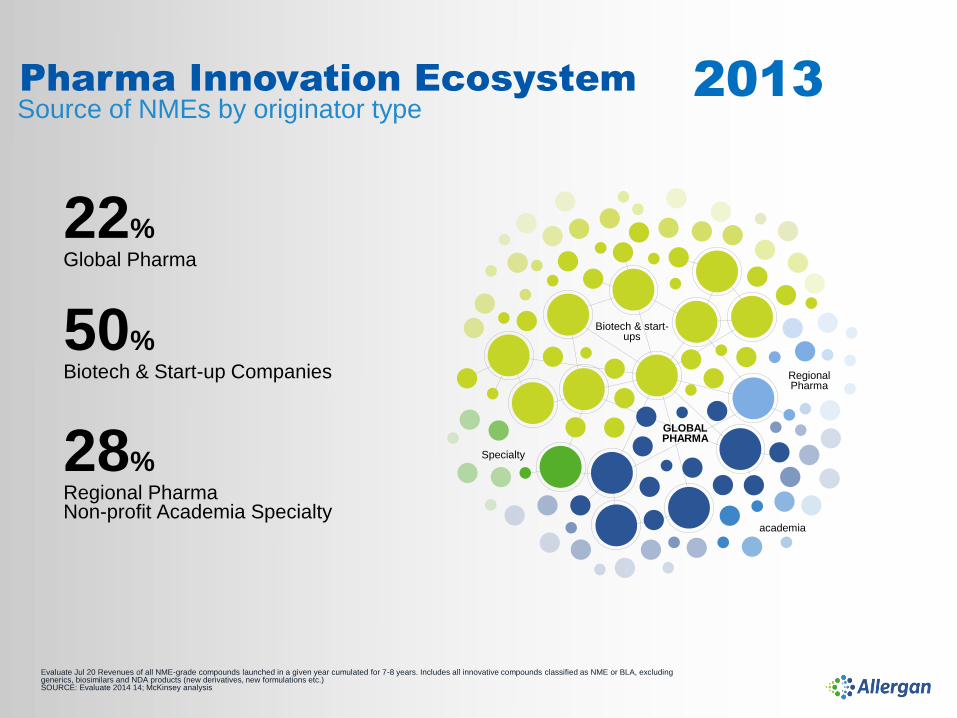

1998Source of NMEs by originator typePharma Innovation Ecosystem

Evaluate Jul 20 Revenues of all NME-grade compounds launched in a given year cumulated for 7-8 years. Includes all innovative compounds classified as NME or BLA, excluding generics, biosimilars and NDA products (new derivatives, new formulations etc.)SOURCE: Evaluate 2014 14; McKinsey analysis

academia

Specialty

GLOBALPHARMA

Biotech & start-ups

Regional Pharma

2013

50%Biotech & Start-up Companies

28%Regional PharmaNon-profit Academia Specialty

22%Global Pharma

Pharma Innovation Ecosystem

Source of NMEs by originator type

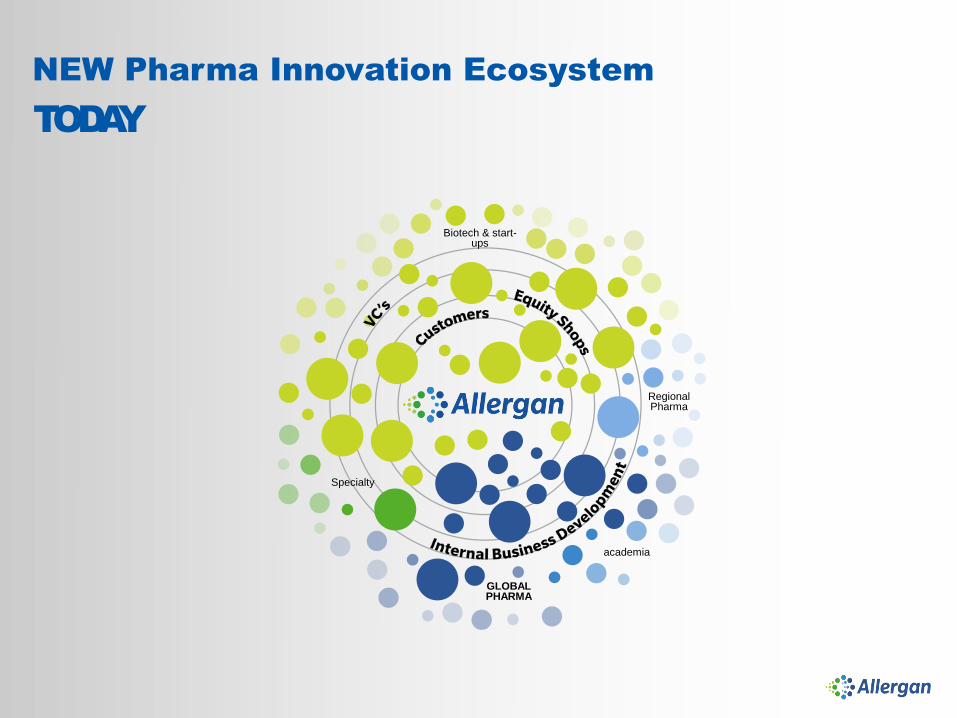

academia

GLOBALPHARMA

Biotech & start-ups

Regional Pharma

Specialty

TODAY

NEW Pharma Innovation Ecosystem

Customer

PRIVATE COMPANIES VENTURE

CAPITAL

REGIONAL PLAYERS

PRIVATE EQUITY

Start-ups

Ideas

PATIENTS

DEVELOPMENT POWERHOUSE

COMMERCIAL MACHINE

BUSINESS DEVELOPMENT

THERAPEUTIC AREA

LEADER

Customer Intimacy is Critical

We discover, acquire, partner and collaborate on compounds at all stages of R&D with a strong preference for validated targets or compounds with proof of concept.

CGRPs

Ozurdex

Latisse

Avycaz

Linzess

Kybella

XEN45

Bimatoprost SR

Restasis X

Abicipar

Relamoralin

KYTH-105

Juvederm Botox

AGN-241660

Rapastinel

SER 120

Esmya

Nebivolol

VraylarBystolic/Vals

artan

Viberzi

Dalvance

OD-01

customer

Teflaro

Combigan

CommercializationDEVELOPMENT

DISCOVERY

Allergan Model

SOURCE: Evaluate; Capital IQ1 Based on 2014 R&D spend/revenue and % of clinical non-generic NME, NDA, and biologic pipeline assets that are non-organic

Low High% pipeline externally sourced1

Low

High

R&

D /

Sal

es1

OPEN SCIENCE

LOW-COST

TRADITIONAL

Allergan is a Forerunner in

Use Open Science Model to Sustain Leadership

Underlying Logic Behind Eye Care Strategy

Leading Therapies In:

Dry Eye

Glaucoma

Retina

in Eye Care

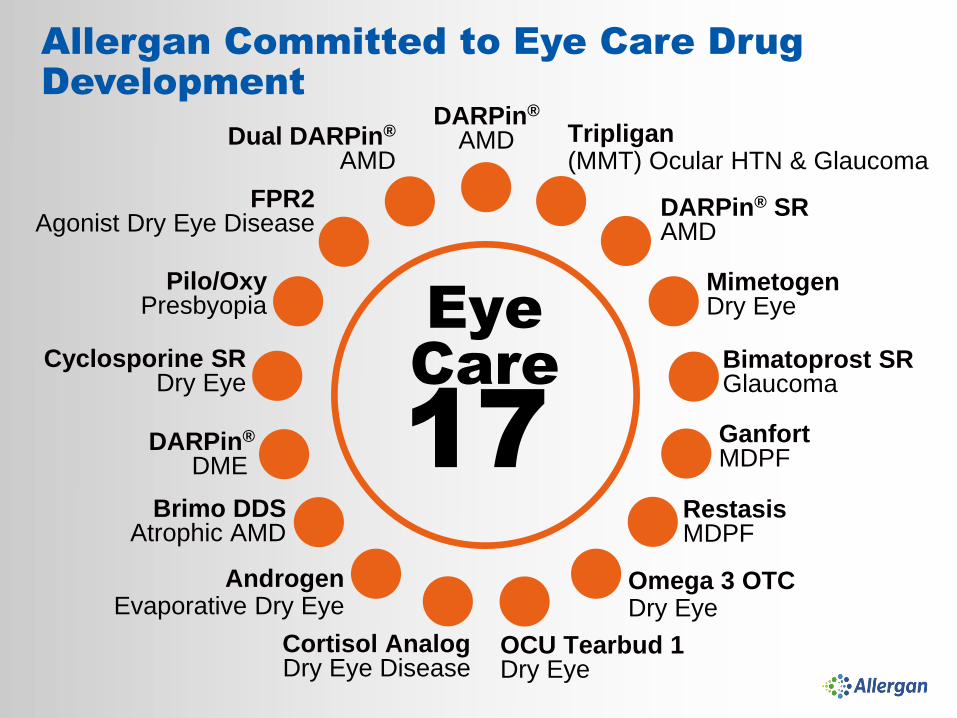

17

Eye

Care

Tripligan (MMT) Ocular HTN & Glaucoma

FPR2Agonist Dry Eye Disease

MimetogenDry Eye

Bimatoprost SR Glaucoma

Ganfort MDPF

Restasis MDPF

Omega 3 OTC Dry Eye

Pilo/Oxy Presbyopia

Cortisol Analog Dry Eye Disease

Brimo DDS Atrophic AMD

Androgen Evaporative Dry Eye

Cyclosporine SR Dry Eye

DARPin®

DME

Dual DARPin®

AMD

DARPin® SR AMD

OCU Tearbud 1 Dry Eye

DARPin®

AMD

Allergan Committed to Eye Care Drug

Development

Growth pharma