brico international

DESCRIPTION

The italian trade magazine for the DIY market.TRANSCRIPT

The italian trade magazine for the DIY market

BricoMagazineBricoMagazineInternational Edition - June 2013 www.bricomagazine.com

International Edition

Interview2013 brings re-vampedassortment and new developments for Self

Expo&ForumBricoDay, the n°1 event in Italy for the Diy marketis back on september 26

Market dataGfK Retail: the growthof private labels inItaly’s Diy superstores

DIY in Italy: the market strugglesbut holds up

1 1 14:07

FITT, THE SPECIALISTIN GARDEN HOSE MANUFACTURINGHigh quality and efficient serviceunder the Made in Italy trademark

Innovation, design, high-quality products and comprehen-sive service. Guided by these values, FITT® strives daily to satisfy its retail clients as well as consumers. Capitalizing on a highly flexible production organization and a wide range of technological solutions, FITT® -next to a standard range of garden hoses- offers clients the ability to fully customize its products, combining different types of textile reinforce-ments, materials and aesthetic finishes. This allows each client to create and market a distinctive, customized range of garden hoses.

NTS® patent, an international success

The commitment to innovation, brought FITT® to develop

the revolutionary NTS® technology, the patent recognized

by the market as the new standard in garden hoses.

During use, ordinary hoses tend to form knots and twists

that obstruct water flow and make the task of watering

difficult and irritating. The NTS® anti-knot patent eliminates

standard hose defects, preventing folds and erratic beha-

viour and ensuring extraordinary manageability. The exclu-

sive helicoidal mesh enables the hose to absorb the

torsion forces generated by water pressure and eliminate

them.

Thanks to this innovative technology, the NTS® hose is

handy and docile, easy to roll and unroll on the hose reel

without any kink.

Worldwide presence and service

FITT expertise in PVC hose manufacturing is supported by

an established commercial presence on every continent:

thanks to a well structured network of subsidiaries in

Europe (France, Spain, Poland) and to commercial agree-

ments and technological partnerships -from North Ameri-

ca, to Brazil, South Africa, Australia and Japan- FITT® is

able to provide a targeted service to clients all over the

world. Thanks to the international presence, FITT® boasts

a deep knowledge of different markets that enables the

Company to develop products aimed to meet specific

requirements worldwide delivered through a highly efficient

logistic service.

PATENT

NO FOLD NO TWIST EASY

Editorial .............................................................................. 5

News

Retail trade ....................................................................... 9

Current affairs ................................................................. 16

Self joins Bricoalliance and looks towards Europe .............................................................. 18

BricolaRge doubles up ............................................... 19

Buyers enjoy better organized National Hardware Show in 2013 .......................... 22

Bricofer unveils its “Reality Shop” experience for DIY enthusiasts ................................. 24

INTERVIEW

2013 brings re-vamped assortment and new developments for Self ......................................... 28by Giulia Arrigoni

A SURVEY OF DIY CHAINS

A negative year for the DIY retail network ............... 36by Giulia Arrigoni

MISTERY CLIENT

Visiting the Bricoman outlet in Carate Brianza ............................................................ 44in collaboration with Interactive Market Research

EXPO&FORUM

BricoDay 2012: brands and private labels in DIY ................................................................................... 50by Monica Renna

VISUAL MERCHANDISING

Put out... the outdoor range ........................................ 56by Dora Binnella

VISITED FOR YOU

La Prealpina, Carmagnola ............................................. 62by Giulia Arrigoni

MARKETS

The wood sector: the crisis and a changing approach to the market .............................. 66by Raffaella Pozzetti

MARKETS

The paints and coatings sector: partnerships and training are the key ................................................. 70by Raffaella Pozzetti

STUDIES AND RESEARCHES

The growth of private labels in Italy ........................ 74by GfK Retail and Technology Italia

MARKETS

The mass merchandisers’ approach to private label DIY ......................................................... 56by Raffaella Pozzetti

INTERVIEW

Brichome, one company and a common business strategy .............................. 82by Giulia Arrigoni

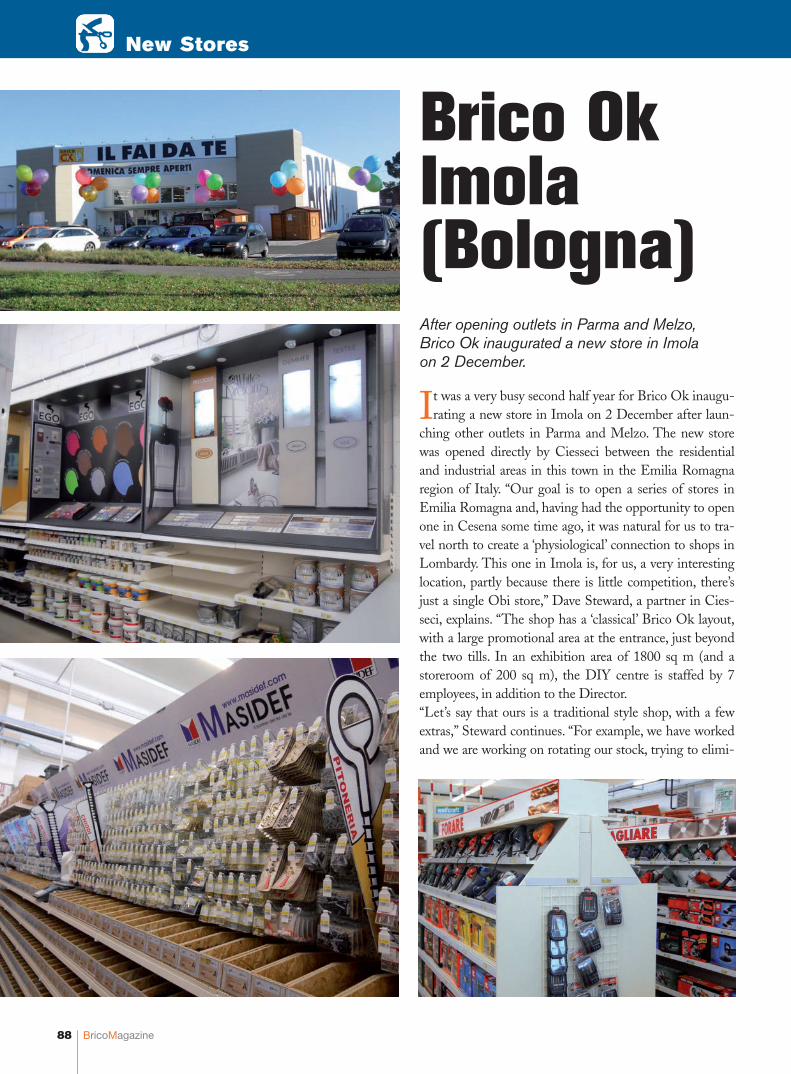

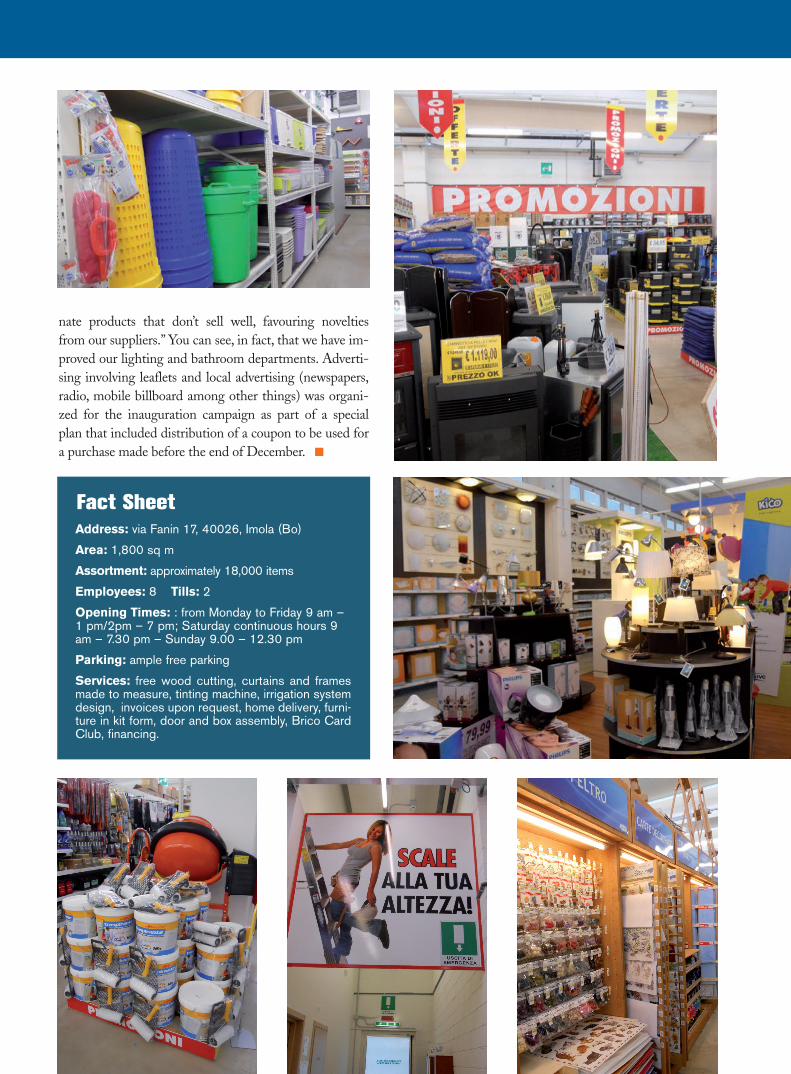

New Stores ....................................................................... 86

The showcase ..................................................................92

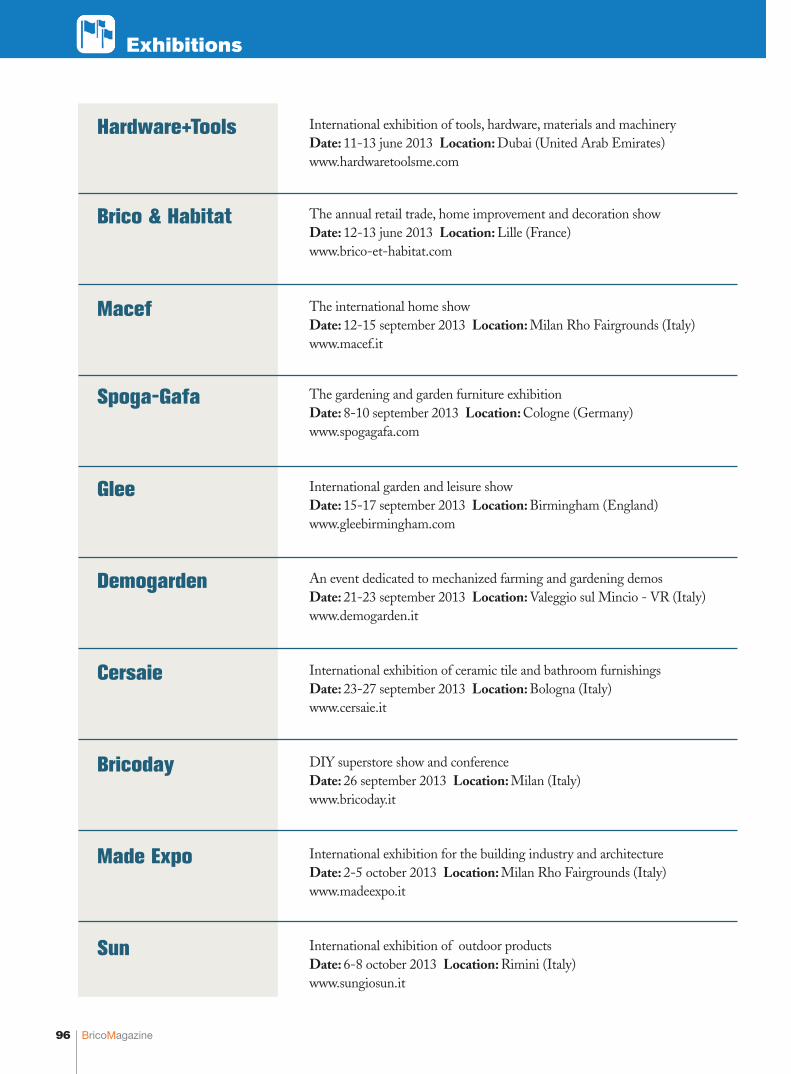

Exhibitions ........................................................................ 96

Contents BricoMagazine International Edition - June 2013

BricoMagazine 1

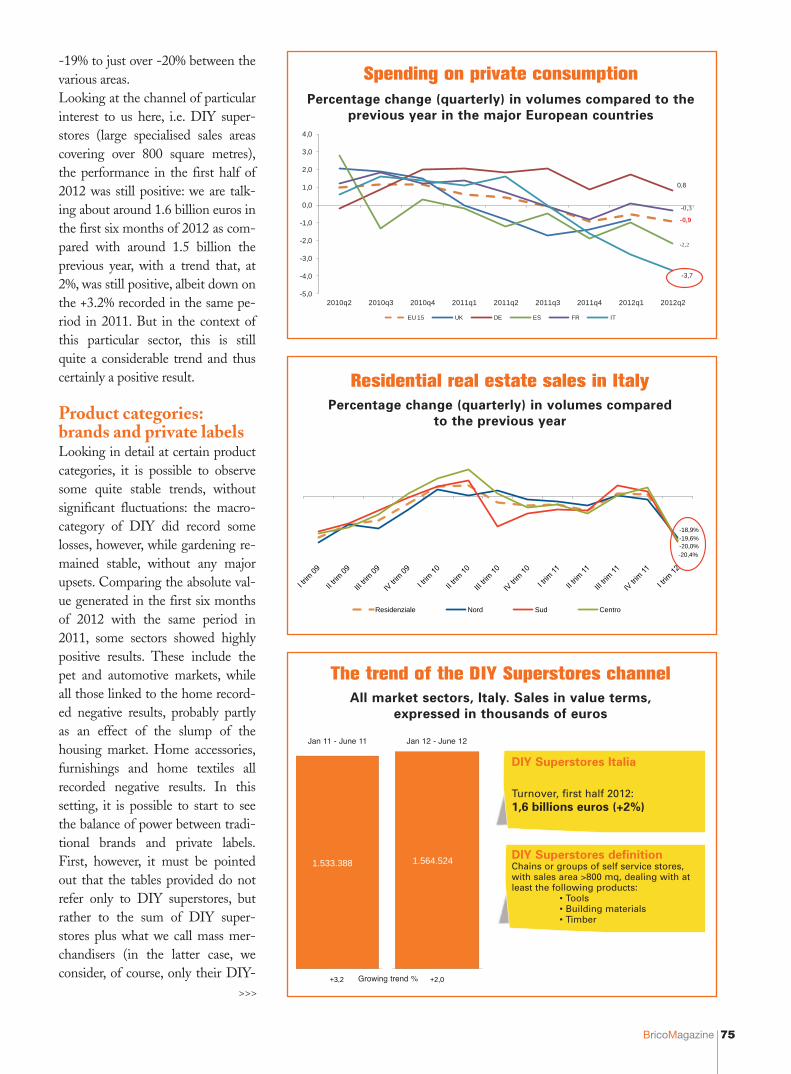

Focus onA negative year for the DIY retailnetwork in ItalyAs 2012 came to a close, theDIY network was still sufferingthe effects of the economiccrisis, with the number of ou-tlets down. Conversely, increa-ses were recorded both in totaldisplay space and in the avera-ge size of Italian DIY centres.

PAGE36

SPONSORED BY

6th

EDITIO

N

Expo&Forum

The n°1 eventfor the DIY

market in Italy

Over 100 exhibitors

Come and meet the best Italian companiesand retailers in a marketplace environment.BricoDay is held in Milan at MiCo, the largestcongress center in Italy (part of Fiera MilanoGroup). Participation is free of charge.Special assistance for foreign visitors. Sendyour requests to: [email protected]

luceQuadraw w w . c f g . i t

™

Thursday, September 26, 2013

®

Register for free at

www.bricoday.it

Top italian andinternationalspeakers

Via Gattamelata, 5 Fiera Milano CityMilan - Italy

For info www.bricoday.it Find out more on the 2012 edition at page 50

BricoDay 2012 clip

EnglishBrochure

It is with great pleasure that we intro-duce to international readers Brico-Magazine, the Italian magazine dedi-

cated to the modern DIY retail world. We took this opportunity on the basis ofdifferent yet equally important reasons:the 10-year anniversary of the magazine;the arrival, for the first time in Italy, ofthe Global DIY Summit, organized bythe European associations EDRA/Fedy-ma, of which BricoMagazine is mediapartner; the growing importance of in-ternational markets for Italian compa-nies, not only the traditional European ones, but also theemerging areas of the world. After having reported onthe evolution of the Italian DIY market for a decade – asector that is currently going through its first year of ac-tual recession – the magazine’s publisher decided to sub-mit an all-round view of Italian DIY retailers and sup-pliers to all major DIY operators in the world. As manyas 4,500 copies of BricoMagazine will be circulated, of-fering the possibility to get closer to a market that hasalways recorded good growth rates, consisting of majorsuppliers as well as a highly complex and diversified re-tail network. We publish this international issue of Bri-

coMagazine with the aim to offer readersthe widest possible picture of the Italianmarket, with news, interviews and specialfeatures on the current situation and the fu-ture development of DIY retail stores inItaly. For example, on page ... you can readan interesting interview with the representa-tives of Self, the main Italian DIY retailchain, running directly a network of totallyowned stores. And again, always in the retailfield, the "Visited for you" series of articlesdevoted to new openings with detailedanalyses of the point of sale, as well as the

reception and the service reserved to our mystery shop-per visiting a DIY shop. Readers will also find specificarticles devoted to visual merchandising and, of course,to the world of suppliers with a detailed analysis of thecurrent situation. Finally, in order to better understandItaly’s DIY retail network, two interesting articles areworth a special mention. The first one describes a DIYindependent (Brichome) and the second an "unusual"hardware store, which will undoubtedly offer plenty offood for thought. We hope that you will like this publi-cation, we are at your disposal if you want to contact usfor more information. Happy reading!

BricoMagazine is published by EpE Edizioni S.r.l - Via Spezia, 33 20142 Milan - Tel +39 02 8950 1830 - Fax +39 02 8950 1604Email: [email protected] - Web: www.bricomagazine.com

Managing director: Massimo Casolaro [email protected]

Editorial manager: Giulia Arrigoni [email protected]

Editors: Claudia Perolari [email protected]ée Duca [email protected]

Editorial assistant: Silvia Mariani [email protected]

Contributors: Dora Binnella, Raffaella Còndina, Ferdinando Crespi, Mauro Milani, Daniela Ostidich, Raffaella Pozzetti, Andrea Prete, Monica Renna, Anna Rucci, Lena Scotti, Bob Vereen

Paging up: Claudia Bellelli [email protected]

Photography: Andrea Lavaria [email protected]

Printed by: Ingraph - Seregno (Mi)

Advertising office: EPE Edizioni - Via Spezia, 33 - 20142 Milano Tel. +39 02 8950 1830 - Fax +39 02 8950 1604

Sales manager: Maurizio Casolaro [email protected]

Giulia Arrigonieditorial manager.

BricoMagazine 5

Editorial BricoMagazine International Edition - June 2013

ColophonALFER www.alfer.com III cover

ALUBOX www.alubox.it Page 4

ARCANSAS www.arcansas.it Page 17

ARIETE www.ariete-group.it Pages 31-33-65

BOLIS www.bolisitalia.com Page 11

BRICOLIFE www.bricolife.it Page 8

C&C www.cecarredi.com Page 43

CAM www.extremasealants.com Page 13

CFG www.cfg.it Page 15

COMFERUT www.comferut.it Page 61

ELEA www.eleaspa.it Pages 20-21

FITT www.fitt.it II cover

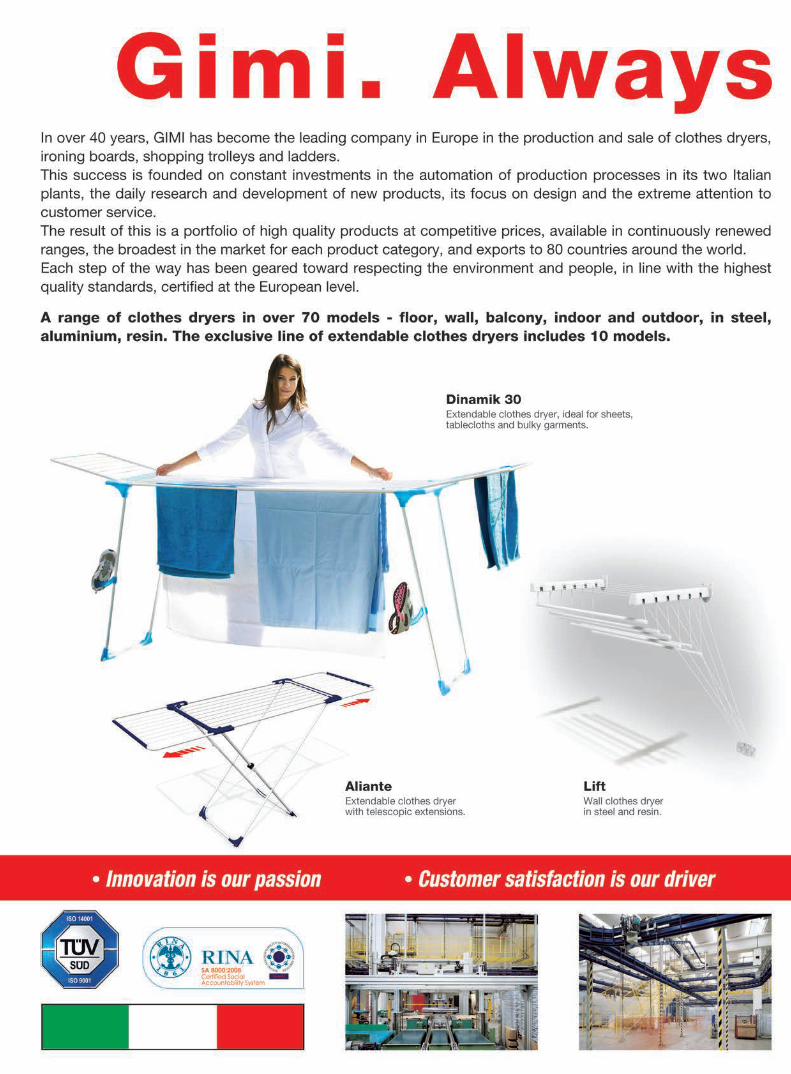

GIMI www.gimi.eu Page 26-27

Global DIY Summit Page 73

KIMONO www.kimono-spa.com IV cover

KRINO www.krino.it Page 41

MADE4DIY Page 69

MOBIL PLASTIC www.mobilplastic.it Page 49

POLIMARK www.polimarksrl.com Page 55

SODIFER www.sodifer.it Page 6-7 / 34-35

VEGA www.vega-pika.it Page 25

Advertisers

13:39:36

BricoMagazine 9

Ikea Italia, purchases exceed 1 billion euros. And that’s not all!

The Ikea Italia annual press conference, held recently in Milan,presented its annual report on social, environmental and humanresources. The social and economic activity of the Swedishgroup involves over 2,500 Italian enterprises. In the furniture in-dustry alone purchases reached more than 1 billion euro, and in-volved 53 manufacturing operations for a total of 2,500 jobs.Furthermore food purchases totalled twenty and a half millioneuros and 7.2 million kg of merchandise was purchased; about200 million euros was spent on goods and services and jobs crea-ted numbered 1,110 in the transport sector and 1,600 in outsourcing. The construction and maintenance of exi-sting Ikea stores originated a total turnover of 18 million euro for 80 Italian companies, including professionals,builders and other suppliers.

Retail trade news

Self debuts on TV soap opera style

For the first time ever Self has decided to advertise via a nation-wide campaign on TV. The commercial uses a retro 1980s setting for a “soap opera” featuring a clueless 50-something coupletrying to cope with a series of unfortunate, yet commonplace hitches resulting from poor home maintenan-ce. The TV spots were broadcast on major Italian networks RAI and Mediaset in various time slotsbetween late March and early April. The campaign plays around with the typical soap format and dialogue,which highlights the ridiculousness of the situation and supplies tongue in cheek solutions to the problems

of the two protagonists. Self resolves the various situations thatoccur thanks to its wide variety of DIY products. In the com-mercials Self contrasts comedy with drama - emphasized by thecharacters -, in a simple and practical way that any of us couldapply for ourselves in our own homes. A solution is always athand thanks to the wide variety of high quality products selectedin the commercial to decorate for example the floor, paint thewalls, renovate the interior and tend the garden.

A new entry for the FDT Group

The FDT consortium has added a new affiliate to itsgroup. On 4th March this year Papeschi srl joined theconsortium with two outlets – one 2500 square meterstore in Lucca and another (1,200 sq.m) in Gallicano(near Lucca). The company has more than 50 years ex-perience in the flooring and interior decoration market

and has also developed DIY and outdoor furnishing departments – first at the Lucca outlet and then in its Gallicano sto-re, which is dedicated entirely to DIY. The stores also offer a key-cutting service and, above all, a paint and colouring de-partment that also targets professionals.

BricoMagazine10

OBI Italy’s "Master in Retail Management" course has ended and the first young graduates have entered its sales network

The Master in Retail Management course, organized by OBI in collaboration with the E-ducation.it Trai-ning School, offered a new format that aimed to increase the students’ potential and get them started on aprofessional career in the chain’s stores. Lasting from May to November 2012, for a total of 752 hours, thestudents of the three courses held in Milan, Florence and Rome, alternated between classroom lectures

and two internships at OBI stores. During the lectures varioussubjects were covered, such as economic management of the salesoutlet, marketing, purchasing and supplier relationships, managingcustomer service, the organization of human resources in DIY su-perstores, as well as leadership and management skills. During theinternship, however, those participating also followed a trainingprogramme developed by the Human Resources Department, whi-ch allowed them to get an all-round overview of how the storeswork, starting from the receipt of goods to the sale, the checkout

area and information box, and then moving onto administration. Fifty-two people were involved in theOBI sponsored training course, 46 of whom completed the course and gained their diploma. More than50% of the participants are currently working in OBI. At the end of the Master course the best candidatefrom each of the three courses was awarded a scholarship.

Retail trade news

Student discounts at CFadda

The students’ discount card campaign is part of a project that will, fromtime to time, involve different categories of customers. The discount is ex-pected to be 8% on all items and card holders must sign up for the CFad-da Advantages Card. At the time of signing you will need to hand in acopy of your identity document and proof of payment of tuition fees forthe academic year 2012-13. The request to activate the 8% special di-scount must be submitted no later than 30 June 2013. The discount willbe valid until 31 July 2013 on merchandise from all departments, exclu-ding items already part of other promotional offers. The card-holder’s na-me is embossed on the card and whenever it is used, the user must show avalid identity document. The campaign will not only be announced via theusual channels, but will also be publicized both in stores and at places nor-mally frequented by students (university canteens, sports clubs, studentunion, etc.).

Bricolife becomes a member of EDRA

Following Self ’s example, the Bricolife Consortium has also decided to join EDRA. This brings the total numberof European members of the association to 113 - either directly or via membership of affiliated trade associa-tions. John Herbert, General Secretary of EDRA said "We are delighted to have Bricolife as a new member ofEDRA. Bricolife is happy too welcome the type of smaller, family-run enterprise that occupies such an impor-tant role in the Italian market. "

BOLIS ITALIA srlVia F.lli Kennedy23881 Airuno (LC) - ItalyTel: +39 0399271126Fax: +39 0399271133 e-mail [email protected]

www.bolisitalia.com

Fixing Design

� �

���

�����

��

����

�����

���

����

���

�

��� �����������

Retail trade news

Bricolife plays "Twice” the newmake a purchase and win 2 ti-mes competition

The new contest created by the Bricolife consor-tium, which began on 15th March and lasteduntil 15th May, had three main objectives: to en-courage the use of the Loyalty Card, promotethe activation of new cards and encourage con-sumer spending via customer rewards; for every25 euro spent, customers received a scratch card(2 for 50 euros, 3 for 75 euros, etc.). Customerscould find out immediately if they had won one

of the shop-ping vouchersup for grabs (atotal of 3,250vouchers withvalues startingfrom 5 euroswere availa-ble), and couldalso continue

the game on-line. In fact, all the cards have a re-movable strip concealing an entry code foranother competition at the Bricolife site. Oncehe or she entered the code and compiled an onli-ne form with their personal data the recipientwere included in the final draw. Once the com-petition ends a company official will extract thenames of the lucky winners who will take home“Superprizes” including a Fiat Panda, 5 electricbicycles and 100 Samsung tablets).

Leroy Merlin returns to the Bollate correctional facility

Leroy Merlin and the administration of the Bol-late correctional facility are working togetheronce again, this time the Leroy Merlin staffworked directly with Block Two inmates on aproject to soundproof the institution’s multi-functional meeting room, auditorium, cinemawhich is used for meditation, interviews andgroup discussions. Gianluca and Giovanni fromthe Baranzate store of Leroy Merlin are expertsin the construction industry and got to workwith 13 inmates starting with the theory and te-chnical characteristics of sound-proofing mate-rials before moving on to the practical applica-tion of completing the project together. BlockTwo inmates have a single room, which is usedas a venue for meetings with social workers aswell as an auditorium. Before they were carriedout the work the reinforced concrete and ironwalls afforded no privacy and did nothing to de-crease acoustic fall-out. For this reason a groupof inmates and volunteers mobilised to resolve asituation that has been creating considerable in-convenience over the years. The working part-nership between Leroy Merlin and the correc-tional house happened almost by accident: thestore, situated nearby, was organising its usualcraft and DIY courses for the public and contac-ted the Bollate facility asking the warden if theycould hold some of these courses inside the pri-son so that inmates could learn helpful skills forthe future. The warden considered with interestthis proposal and the value of the competenciesinvolved and immediately gave the go ahead.

New entries in Bricolife

The Bricolife Consortium has welcomed anothertwo members. The first is Unipam srl, the companyowner of the Centro Acquisti Orizzonte retail outlets(using the traditional department store model withfood hall) which has decided to increase the storearea dedicated to DIY. Unipam operates in Laziowhere it has 11 outlets; the most recent opening wasin Cisterna di Latina. The second new member isFree Time srl, with one 2,000 sq.m store in Foggia.

BricoMagazine12

www.extremasealants.com

is a brand by CAM International,an extremely innovative company for every kind of market and necessity

DIY AND PROFESSIONAL

SEALANTS - ADHESIVES - SERVICE PRODUCTS - CAR CARE

alte

rego

stud

io.it

via f.lli Cervi, 48 - 20023 Cantalupo di Cerro Maggiore (MI) ItalyTel. +39 0331 533538/9 Fax +39 0331 533540

BricoMagazine14

Retail trade news

On 6th and 7th March Pomezia hosted the ninth Bricofer BusinessMeeting "To Do Together"

Against the backdrop of the Hotel Selene CongressCentre the ninth edition of the Bricofer Business Mee-ting "To Do Together" took place in Pomezia (near Ro-me), where suppliers met affiliates and brand represen-tatives. The event, which takes place three times a year,offers fast track access to business contacts in order toincrease efficiency. This philosophy of ‘chasing business’identifies in the supplier a true partner that should beintegrated into the network and sees the store as the fir-st interface with customer demand. Via a system of oneto one appointments, in just two days 26 partner sup-pliers in the group made approximately 540 orders tothe tune of 980,000 euros. This was an important op-portunity for suppliers to submit tenders created specifi-cally for the event and proved fundamentally importantin creating active participation between suppliers anddistributors. The gala dinner at the conclusion of thefirst day saw affiliates, suppliers and Bricofer staff enjoya moment of relaxation and fun. During the evening aspecial token of appreciation was given to German sup-plier Alfer Aluminium GmbH which received the Spe-

cial Bricofer Partnersprize for the on-goingdedication and coope-ration with which it isalways ready to followsales and marketinginitiatives thus de-monstrating its relia-bility and confidencein Bricofer.

� � � � � � � � � � � � � � � � � � �

�

� � � � � � � � � � � �� � � � � � � � � � � � �� � � � � � � � � � � � � � � �

� � � � � � � � � � � � � � � � � � � �

� � � �

� � � � � � � � � � � � � � �� � � � � � � � � �

� � � � � � � � � � � � � � �� � � � � � � � � � � � �� � � � � �

� � � � � � � � � � � � � � � �

Self HappyBox: a box full of surprises

Self wants to reward the loyalty of existingcustomers and attract new ones with this in-novative proposal: participating in the BigSelf Happy Box Contest. This toolbox con-tains a wide range of products for the home,leisure and not to be missed offers for just €9.90. Customers reserved their boxes from25th March to 25th April at www.selfitalia.itand picked them up later at selected stores.This gave them the right to participate in theBig prize draw which gave away fantastic HPnotebooks and printers, Vergnano coffeemakers and much, much more – in total 84prizes were up for grabs. With a few clicks ofthe mouse, customers could purchase the SelfHappy Box directly on-line by filling in andprinting the reservation form; the boxes wereavailable for collection from 2nd to 5th May.The competition was promoted via on-lineadvertising, flyers and brochures distributedat all the Group’s stores.

From Bricocenter to Italbrico

Three former Bricocenter members have swit-ched allegiance to Italbrico. As of last January,CIB Brico Valenza S.r.l. based in Valenza (nearAlessandria) with a 1000 sq.m outlet, BricoPietrasanta Srl with a store of 900 sq.m in Pie-trasanta (near Lucca) and Fastred Srl based inNocera Inferiore (near Salerno) where it opera-tes a 1,400 sq.m DIY store have, in fact, beco-me part of the latter consortium.

CFG, since 1961, distributes all over Italy chemicals for

Professional and DIY maintenanceUp to today, CFG range is the widest on the market and at the same time available from a single

source.

In 2011, the CFG Srl has acquired the brands LuceQuadra and Emmeci specialized into electrical

equipment (fan, heater, lighting, plugs, torches, etc.) thus entering into the segment of electrical

equipment with more than 350 new part numbers and with two brands present in Italy since 50

years.

In 2012, the CFG Srl became the official national distribution in Italy for Duracell, Ambi Pur Car,Ambi Pur Home, Gillette, Braun for wholesalers and retailer belonging to Hardware, Electrical,

Garden, Marine and Brico Groups.

From owned warehouse in Livorno, orders are given to couriers within 24 hours from order receipt

and delivered by courier to retailers in the next 48 hours.

Several thousands of Retailers are supplied by CFG in Italy. Employees, area managers and a wide

network of sales agents regularly visit stores offering technical support and commercial training and

verifying proper product presence on the shelf.

As far as the large-scale distribution Brico (Non-Food), CFG is present in the most important Italian chains.

CFG Srl - Via Fraschetti, 5 - 57128 Livorno Ph. +39 0586 580066 - Fax +39 0586 580731 - E-mail [email protected]

www.cfg.it

The new logistic center of CFG. CFG headquarter, located in an historic villa.

BricoMagazine16

Current affairs

Elettrocanali expands its headquarters and logistics centre

Operating in the production and sale of electrical equipment,Elettrocanali a company situated in Scanzorosciate (near Ber-gamo), recently inaugurated its new logistics centre and officebuilding. The industrial complex covers an area of about 20,000sq.m, 13,000 sq.m of which is undercover. The make-over hastransformed the premises both in terms of space and design tofit in with the needs of a company that has continued to growfor over forty years. Together with the adjoining plant in Pe-drengo, the two production sites in the province of Bergamooccupy a covered area of 16,000 square meters; if we take intoaccount the production sites in Osimo, near Ancona, and thatin Avellino, the four Italian plants total over 20,000 sq.m. Out-side Italian borders meanwhile Elettrocanali is present in Fran-ce and Spain with two subsidiaries dedicated to sales andmarketing near Lyon in France and Barcelona in Spain. Thisexpansion has also effected logistics: the majority of exports (toover 70 countries, accounting for 50% of sales) and distributionin Northern Italy leave from the Scanzorosciate depot. SinceElettrocanali’s trading policy is committed to immediate, in-stock availability for all the items in its catalogue, there is a clearneed for adequate space to prepare and ship orders, given thesteadily increasing volume of business the company handles.

C.&C.'s new online catalogue

C. & C. Arre-damenti Metal-lici srl has aneye on the futu-re, but is notforgetting thepast. Its com-prehensive cata-logue of equip-ment for allmanufacturingand commercial needs has now gone online.Indeed, the DIY world is not C. & C.’s onlytarget market. Its aim, with this simple, illu-strated catalogue, is to remind all its clients ofits production flexibility, which allows it to of-fer a wide range of complementary products.Its aim, in short, is to be, more and more, anall-inclusive supplier, offering turnkey solu-tions. The catalogue is full of articles that areclearly presented with photographs, technicaldescriptions and all the necessary measure-ments. All users have to do is visit the websitewww.cecarredi.com and click on SCARICACATALOGO PRODOTTI (download ca-talogue). By entering a few essential details,which will remain in our archive and in the li-st of newsletter subscribers, users can receivethe full catalogue or the section or sections ofinterest (Shelving – Drum storage – Work-shop furnishings – Community furnishings –Office furnishings).

Bosch Power Tools reaches the 4 billion euro milestone

Despite unfavourable market conditions, the Power Tools division of the Bo-sch Group has recorded a 6% growth in sales for the year 2012. The companyhit the target of € 4 billion in sales for the very first time and in doing so ack-nowledged the contribution made by its 19,000 employees. In 2012, the ove-rall market growth was 4% with a turnover of 24.5 billion euro. Particularlypositive results were recorded in Asia, despite the market performing belowexpectations. The main cause can be found in the effects of the economicslowdown in China. Good progress was achieved in North America, wheregrowth was 6%. One of the reasons for the positive development of sales isthe great market success of the measuring instruments business. Good news

from Europe too; despite a stagnant market, Bosch Power Tools managed to strengthen its position with a +3%.

Ind.i.a. are shopping in Germany

Among the many sad stories about Italian companies stepping out ofbusiness, fortunately something good happens occasionally. This isthe case for Ind.ia Vicenza, a company specializing in iron accesso-ries, which has just finalised the acquisition of Triebenbacher, a Ger-man company with 9 branches and 91 employees, a reference pointin Germany for iron and steel accessories. Ind.ia, led by founder Bru-no Gonzato and his children, today employs more than 700 peopleworldwide with 120 in the company headquarters in Malo.

Idro-Bric acquires Acquasanit

Idro-Bric SpA recently took over Aquasanit, the commercial arm of Inda Ltd, a company that is stepping out ofthe DIY market to concentrate on the professional retail market as its core business. With the acquisition of Ac-quasanit, Idro-Bric completes its range of products as a global supplier for plumbing installation, taps, hydrothe-rapy, sanitary ware, water heaters, boilers, furniture, shower cubicles, bathtubs and bathroom accessories. Fromthe point of view of logistics the Acquasanit warehouse has been integrated into Idro-Bric’s Casirate d'Adda de-pot and storage operations, and the company is in the process of building a new 600 sq.m warehouse to improvedistribution logistics. Inda currently supplies Idro-Bric with an assortment of shower cubicles and bathroom fur-niture. Revenue forecasts for 2013 predict post-takeover sales of 45 million euro.

BricoMagazine18

Self joins Bricoalliance and looks towards Europe The Self group continues to grow and as it does it is taking inspiration from what is happe-ning outside Italy by joining European consortiums and trade associations.

Following its recent adhesion toEdra, Self has also decided tojoin Bricoalliance, a purchase centresupported by nine European chains.We asked Enrico Gardino somequestions about the reasons behindthis move and what objectives Selfplans to pursue. First the obvious question: Why?First and foremost to expandoutside Italy so we can im-prove our purchasing powerand then to compare our per-formance with other chains’.The first reason is, as you say,obvious; everyone knows. Butthis is the kind of move thatbreaths life into a business.The second reason, which isjust as important for us, is im-proving our performance andthe best way to do it is to com-pare ourselves to other chainsthat work in the same sector;not our direct competition,that would be impossible, butwith the reality of how thingswork in other countries Do you think that your expe-rience of markets outsideItaly will help power futuredevelopments for your brand?It’s certainly becoming moreand more important to look atwhat’s happening elsewhereand we believe that this kindof exchange of information –

perhaps with Bricoalliance – couldbe a stepping stone towards the fu-ture for Self. This is the same moti-vation that lies behind our member-ship of Edra and it was that decisionwhich led to us joining Bricoal-liance.Have you been to any meetingsyet? What was your impression?

Yes, I’ve been to meetings withEdra and Bricoalliance. More thananything else the consortium hasbeen working swiftly to try to as-similate common developmentstrategies for the future. Further-more, in a few months – the datehas yet to be decided – we will beholding our first meetings withsuppliers as Bricoalliance. Theidea isn’t to enter into negoti-ations immediately, but topresent the consortium, ex-plain what it is and what itwants to do and outline ourfuture projects. Our intentionis to build a reality that will gobeyond a simple exchange oforders and contracts: at leastthat what we hope to achieve. You have set yourselves anambitious task: nine brandsin nine countries...You’re right, but I believe thiscould be a great opportunityfor us. There’s a great deal ofwork that still has to be done -there’s no doubt about that –not only problems connectedto the different languages wespeak but also different men-talities, customs and marketdemand. We will all need tobe flexible and committed tothis project if we want to makethe best choices that will ben-efit everyone. �

Current affairs by Giulia Arrigoni

EnricoGardino,Self’s CEO

BricoMagazine 19

BricolaRge doubles up BricolaRge has decided to invest a significant amount ofmoney over the course of 2013, according to a plan thatwill revolutionise the company’s communications with itscustomer base and independent dealers.

With 12 outlets, a modern un-mistakeable brand and, de-

spite the current economic down-turn, thriving business, BricolaRgeclosed 2012 in the black thanks to itspolicy of presenting itself to suppliersas a potential partner, but also thanksto its appeal to a customer base thatleans heavily towards DIYers. Based on its success and followingthe logic of its strategy, BricolaRgehas drawn up an ambitious invest-ment plan for 2013 that will revolu-tionise the company’s communica-tions with its customer base and withindependent dealers that want to bepart of a consortium that will allowthem to improve their market shareand, of course, their sales and profitmargins. “When deciding how to deal withthe problems in the franchising sec-tor that emerged during BricoDay2012” – says Carlo Basciani, head ofmarketing at BricolaRge – “we optedfor the consortium model as a likelyalternative; all our members sharethe decision-making and the benefitsequally and the benefits can be ma-jor, above all during a recession likethe present one.”BricolaRge was developed based onthe experience gained with Con-sorzio Punto Legno, which was oneof the first of its kind in the ItalianDIY sector, but which went on tohave some serious issues. Howmuch of Punto Legno is thereBricolaRge?

“It’s certainly true that when we talkabout Punto Legno we are talkingabout the history of DIY in Italy.The sector has come a long way andhas left industry professionals –manufacturers and distributors –with a wealth of valid experience andknow-how”, continues Mr. Basciani.Personally I feel very attached to ourpast, but at the same time, as some-one who has yet to celebrate his 40thbirthday, I think the present and thefuture are there for the taking andshould be fully mapped out. I havebeen with BricolaRge since 2009and in these last few years we haveworked hard to improve our organi-sation and the open and honest rela-tionship we have with our suppliers,whom we see as our partners in thisventure. All of this benefits ourmembers. There is still a great dealto do and 2013 will be an importantyear for our consortium. What can we expect from Brico-laRge?At present being part of the Brico-laRge consortium is an opportunityand we hope it will become a sourceof pride with time. We are workingon projects that will bring a breath offresh air to the market and take it in-to the new century. Of course wecan’t give too much away, but thenew frontier is in communications,media and the internet - all aspectsthat will carry a great deal of weight.But whatever the medium, I believethe kind of reputation your brand

has with suppliers and consumers isparamount and I think our reputa-tion is solid. We have worked hard toachieve this and now we have to putit out there and you can be sure wewill be doing our utmost in order tosucceed. Is there anything more you can tellDIY enthusiasts?We aim to give the consumer thegreatest possible satisfaction. Untilrecently that usually meant gainingthe customers’ trust and encouragingtheir loyalty, but that is no longer thecase. Marketing experts talk about“conversational marketing” and re-tailers that “listen” (says PhilipKotler) because today the customerreally is King: the customer com-ments, has opinions, interacts withthe retailer and with other con-sumers. We want to be part of thatflow of information because it is ofvalue to us and, and I cannot stressthis enough, to our customers. InItaly in particular, and not just in oursector, it’s very difficult for the con-sumer to be heard. We’d like to seethat change. We want to listen, workwith the customer and, hopefullygrow with them too. �

Carlo Basciani.

BricoMagazine22

Current affairs by Bob Vereen

Buyers enjoy betterorganized NationalHardware Show in 2013

Just as retailers realize they mustkeep improving to satisfy cus-

tomer needs, this year's NationalHardware Show, held in earlyMay, offered buyers a number ofmajor improvements designed tomake it easier to shop, easier tofind new items or explore othermarket opportunities and with theadded advantage of a series of edu-cational seminars, several of themfocusing on the rapidly evolvingworld of social media and mobiledevices and their impact on retail-

ing and marketing.While there are other exhibitions forthe kinds of products sold in hard-ware stores, home centers and spe-cialty retailers, there is none quitelike the National Hardware Show,which blends a huge exhibition witheducational seminars, and that iswhy it attracts wholesale and retailbuyers from around the world, fromas far away as Australia, Europe,South America and Asia, in addi-tion to full line and specialty whole-salers and distributors, as well as in-

A report from the National

Hardware Show 2013, 7-9

may Las Vegas.

BricoMagazine 23

dividual retailers and chain store re-tailers of all kinds from throughoutNorth and Central America.Because buyers are always lookingfor “something new”, this year theshow featured three segments em-phasizing new items in a New Prod-ucts section, making it easy for buy-ers to concentrate on such items,another area called Innovation Sec-tion also introduced new items, andthis year show management also set

aside an area for New Exhibitors,whose products, in most cases,would be new to most attendees. A Packaging Exposition, rewardingfirms with outstanding packaging,also helped buyers focus on sales-making products and effectivepoint-of-sale merchanding aids.For american buyers who realize thatconsumer interest in American-madeproducts is growing at a remarkablepace, special recognition was givento firms whose products are Made inAmerica so they could concentratetheir buying on those items.But perhaps the most importantchange in the show this year was theimproved organization of the showby merchandise category, making itmuch easier for buyers to concen-trate their product reviews of theitems of most importance to them.And because the show consisted ofmore than 2,700 exhibitors, such adepartmental organization was mosthelpful. Recognizing overall mer-chandising trends, two new cate-gories were offered building prod-ucts and farm & ranch. Management said the show alsoallowed manufacturers to connectwith inventors and find new prod-ucts for their portfolio. For inven-tors, it was their way of gettingtheir products into the distribution

channel. “Of the new products weshowcased at the National Hard-ware Show this year, three of themwere from products we discoveredat the show last year. One of themwas a winner of the Retailer’sChoice award,” said Corey Talbot,vice president of marketing andnew product development atHyde. “The National HardwareShow is the best place to find greattalent—inventors that need some-one to help them move their prod-uct along the distribution channel.Those inventors typically have anew product 80% of the way de-veloped, but need someone to takeit the rest of the way.”The Retailer's Choice mentionedabove is a recognition program ofHardware Retailing magazine, inwhich a group of retailers prowl theshow and pick items they think willbe winners in their stores. Theproducts and producers are recog-nized during the show's final stagesand also in the magazine's July is-sue, reaching more than 30,000wholesale and retail readers. Themagazine has used retailers tosearch for products they like at thisshow for more than 40 years.Next year's show will be held inLas Vegas May 6-8, 2014. www.nationalhardwareshow.com �

In all, here are the 11 categoriesin which the show's 2,700 exhi-bitors were organized:• Building Products• Farm & Ranch• Hardware & Tools• Homewares• International Sources, whichincluded suppliers from morethan a dozen countries• Inventor's Spotlight (anotherplace to find new products)• Lawn, Garden & Outdoor living• Paint & Accessories• Plumbing and Electrical• Storage and Organization• Outdoors, Tailgate and Re-creation an outdoors display ofitems like barbecue grills,

Exhibitors categories

BricoMagazine24

Bricofer unveils its “Reali experience for DIY enthus

Current affairs by Giulia Arrigoni

BricoMagazine24

Not so much a reality

show as a reality shop,

where several couples

will be getting to grips

with DIY projects.

A 14-stop tour covering

the length and breadth

of Italy.

The retail chain Bricofer haslaunched its “Reality Shop”, a

reality show-type shopping expe-rience for couples. The competitorswill be filmed as they try their handat DIY, having been given a specificassignment: to construct an objectwithin a time limit of 20 minutes.The winning couple will becomethe faces of a Bricofer advertising

campaign and will take hometwo Dacia Dokker Vans. To

take part, the would-becompetitors were re-

quired to submit aphoto showing

themselves doingDIY or in

which they appear together with so-me object related to the world ofDIY. The individuals in the photosdeemed most appropriate, selectedat the sole discretion of the judgingcommittee, took part in a castingprocess which led to the final selec-tion of the Reality Shop conte-stants. In particular, the committeeselected, on the basis of the photos,the individuals who will be takingpart and matched them in couples;the list of contestants can be consul-ted on the retailer’s website,www.bricofer.it.

The contestants, the stops,and the challengeThe contestants will be pitted

against each other on a total of14 stages. The tour opened

on May 18 at the RomaCapena store and will end

with the final on July 20,again in Rome. The challenge

facing these DIYers is broken downinto four different stages. On arri-ving at the Bricofer store, each com-peting couple is given a sealed enve-lope containing a photo of theobject that they are required to re-produce, together with some sugge-stions as to the products they mightbuy and the total amount they canspend; after opening the envelope,the contestants have two minutes inwhich to jot down a list of thethings they need to buy, remaining

within their budget. Then, thecompeting couples are given15 minutes to race round

lity Shop” usiasts

the store, filling their trolley before going to the cash desk tocheck that they have not spent too much. Once the cashierhas given them the go-ahead, the contestants have just 20minutes to leave the store, load their purchases into a DaciaDokker Van put at their disposal, and make their way to aspecial venue located somewhere nearby, where they willconstruct the specified object. Throughout the entire dura-tion of the challenge, the competitors will be filmed bySPACE TV cameras and the resulting videos will be shownin the Reality Shop area of the Bricofer website and also onBricofer’s various social media pages. The 10 couples recei-ving the highest number of votes will qualify for the final.

The finalThe Reality Shop final will be the focus of a major event tobe held in Rome on 20 July. The final will take the form of achallenge against the clock: the couple who complete the re-quested object in the quickest time will be the winners andwill become the faces of a Bricofer advertising campaign.What is more, each member of the couple will go home atthe wheel of a spanking Dacia Dokker Van! What is moreall those who voted for the competing couples will be ente-red in a special draw for three great prizes: a Blue-Expressflight for two people to Moscow from Blue Panorama, aweekend in Tuscany courtesy of UNA Hotels & Resorts (attheir UNA Poggio dei Medici venue), and a €300 voucherto spend at Bricofer.

And for Bricofer’s customers… “Look & Win”As well as its Reality Shop, Bricofer has also launchedanother initiative, this time open to all its customers: until 6July, anyone spending more than €50 will be given a “Scopri& Vinci” (“Look & Win”) scratchcard and thus have thechance to win, immediately, one of a range of fantastic prizes(Blue-Express flights from Blue Panorama, weekends atUNA Hotels & Resorts, and much more besides*). Further-more, if even if you don’t win, your “Scopri & Vinci” cardswill be “put in hat” and one will be drawn at the RealityShop final in Rome: the lucky winner will receive a DaciaDokker Van. �

BricoMagazine28

Self is Italy’s biggest DIY retailer,not only in terms of its size, butabove all, for the range of innovativeproducts it offers. And now the com-pany has started a new brand – Dot-torbrico. In this interview KristosBasimas, head of purchasing andoverseas markets at Self, and thecompany’s communications directorRiccardo Baldi tell us about the cur-rent situation on the Italian marketand how the company is dealing withthe current recession.How did the Italian market per-form in 2012 and how are thingslooking in the first few months of2013?In 2012 the DIY market in Italy fellfor the first time ever – a drop of 2%.Of course when we look at the fig-ures for other markets - Spain for ex-ample fell by 9% - the reduction wasminimal. However we mustn’t forgetthat in other areas, such as Russia,there was an increase of 12%. Theseare examples of the two extremes andthere are other realities, France forone, where business remained stableat a level with 2011. However this isthe first time we’ve seen a decrease inturnover and it’s something we needto take into account when consider-ing new store openings. And the situation for Self?We are making progress in develop-ment, but in terms of breaking even

by Giulia ArrigoniInterview

2013 brings re-vampedassortment and newdevelopments for Self

Self is Italy’s biggest DIY retailer, not only in terms of its size, but above all, for the range of innovative products it offers. In this interview with KristosBasimas, head of purchasing and overseas markets at Self, and the company’s communications directorRiccardo Baldi, we talk about the current situation onthe Italian market and what Self is doing to deal withthe current recession.

BricoMagazine 29

we are in line with the rest of themarket, which means we need to becareful. Although we have strength-ened our market share, putting usahead on performance, we must con-tinue to invest; this remains our pri-ority especially because we are ex-pecting another negative year in2013. January was not a good month,but then it never is. This time how-ever, despite some very attractive of-fers, even the New Year Sales did notgo well. Self has a very challengingyear ahead, but we remain optimistic

because we are determined to growand convinced we can do so.

Making outlets moreappealing to women andthe professional consumerHow are you going to do this?By changing our assortment for ex-ample. It’s amazing what results weachieve every time we re-vamp ouroffer whether by department or sec-tor; the positive impact is immediate.Self customers will be seeing a lot ofthis in 2013. We tend to refresh all

>>>>

our sectors anyway and this year, forexample, we will be concentratingmore on technical sectors: tools, elec-trical goods, plumbing supplies – allareas where we’ve seen a positive per-formance despite the general slumpin the market. What’s the reasoning behind this? We make investment a priority andthis means we continue to be a hubfor every type of item you might ex-pect to find in the macro sector wecall DIY. However it’s true that inrecent years we have been pushingproducts with more feminine appealand expanding the area dedicated todecorative hobbies and crafting. And you’ve also made professionalconsumers more of a priority...We’ve worked hard to expand ourprofessional customer base in theelectrical goods and plumbing sup-plies departments. Plumbers andelectricians may not be our primarytarget but the professional sector is amarket like any other and we wantour share of it. We have introducedsome very interesting assortments forplumbing and electrical supplies andthat gives us a full and comprehen-sive range of articles, which in turnincreases our credibility with the cus-tomer. More and more tradesmen arebuying from Self thanks to a specialcatalogue we have prepared and atargeted mailing list.How does this work in the singleoutlets considering the differencein their sizes?We use a rack system in larger stores,while the smaller stores work frombehind the counter. But the extent ofthe range of articles is almost thesame. What changes is the quantityof a given item kept in stock. Revis-ing our assortment is so importantbecause is keeps us out of the redeven in times like these when theconstruction sector is losing ground.So, is this a contradiction? Or does it

Kristos Basimas, head of purchasingand overseas markets.

Riccardo Baldi, communications director.

BricoMagazine30

simply mean that more people aredoing jobs around the home theywould have hired someone else to doa few years ago? It’s the same in thebathroom sector; if we look at thefigures for the professional segmentthey are falling, but the private mar-ket is growing. Are we looking at the classic “do itfor me” scenario?I think we are. Once upon a timetradesmen used to buy the suppliesand fittings, today the end user pur-chases them and then calls in a pro-fessional to do the installation. Ser-vices like the ones we and other DIYretailers have been supplying for years– installation and fitting for example –have also contributed to this change.

New items for Self in 2013Did any segments defy the overalltrend in 2012?Yes, for the first time in our marketsegments like lighting and homedecor fell. But here at Self our light-ing sales were up, because wechanged our assortment not once,but twice and thanks to a new part-nership with Philips which saw us setup a dedicated area for lighting atour Moncalieri outlet, as well as aradical change in our visual market-ing displays; we placed the emphasison well-known brands the customerrecognised and liked. What do you mean by “radicalchange”?When it comes to lighting we havediscovered that the number of itemson display is less important than thecustomers’ ability to “read” the as-sortment and understand what kindof light fitting they need. The answeris to have fewer items, but the rightkind of items displayed in the rightway to create a balance between therange of articles available and howthey are presented. The results have

been encouraging and we want tocontinue to explore this avenueacross the board. We are not rulingout further partnerships with suppli-ers. This will help us optimise ouruse of space and reach our goals interms of sales, profit margins andstock turnover. You’re preparing a new store open-ing in Alessandria. Have you gotany news for us about that?We are presenting a new series ofcourses in-store that will appeal towomen and kids. We hope that tak-ing part in a course will lead to thecreation of a sense of community and

we might even be able to make somespace available for our customers toorganise perhaps, children’s birthdayparties. The aim is to build a closerrelationship with our customers. Wesee this first project as more likely toadd value to our product than someother initiatives, promotions for ex-ample, that aren’t having the same ef-fect on sales they had in the past.And this is just one of many ideas. What about the assortment?Once again customers will be seeingsomething new: we are presenting aspecial sector dedicated to homedecor. We probably won’t manage toimplement it entirely, but we willtake a good step forward. This de-partment will be oriented towardssmaller items, not actual pieces offurniture. And we will also be open-ing a kitchen department with all theutensils you need to prepare food. Itwill be a very different assortmentcompared to what you would nor-mally find in a DIY outlet. In otherwords more performance, more solu-tions and less vertical variety; this isthe trend for DIY stores.

Distribution: the struggleand the evolutionLet’s talk about DIY chains: thenumber of stores in Italy is falling…I’ve said it before and I’ll say it again,the fact that Castorama disappearedfrom the Italian market almost fiveyears ago, has been disastrous. Therewas a kind of balance before, but to-day one company is very strong andthe other isn’t yet. But this situationcan change, above all now that a re-organisation is being attempted.Then there’s us and a few others whoare able to grab a share of the marketand continue to improve it. But thesmaller chains are suffering and somewill disappear entirely; either because

Interview

“It’s amazing what results we achieve

every time we re-vampour offer whether bydepartment or sector;the positive impact is

immediate. This is something you’ll beseeing a lot of at

Self in 2013.

“

>>>>

BricoMagazine32

“I insist on making

households a prioritytarget for our stores andon our ability to get cus-

tomers in-store andshow them DIY is notjust a job to be done

but an enjoyable hobby.

“

they don’t have a coping strategy inplace, or because management de-cides to close down, or simply as aresult of economic woes. Today youhave to be very careful about the dif-ference between sales and profit; weall survive thanks to our profit mar-gins and contributions. Why do you think the franchise for-mula, in particular, has sufferedmore than other business models?Firstly, as far as I can see, Italy has a“softer” franchise option than othercountries. Having said that, if wetake for granted that in today’s mar-ket anyone can find a good price ifthey look for it, what a workablefranchise should have is an identity,image and organisation, but aboveall it must have a consistent strategyand that comes from having a globalvision of where you want to go. On-ly a “full-on” franchising operationcan deliver these conditions and of-fer associates real advantages. If thefranchise is only about a commonpurchasing strategy obviously thatisn’t going to work; there are otheralternatives that are cheaper andprobably more suitable for an inde-pendent operator. So DIY is an impossible sectorwhen it comes to franchising?Personally I think it could succeed inItaly but only if all those involved ac-cept the same rules. There’s a marketout there for the taking. Per capitaexpenditure on DIY in Italy is a thirdof what is spent in Germany and halfwhat the French spend. It is up to us,those who operate in the retail andmanufacturing sector, to work to-gether so the customer can see theadvantages of using DIY products.This is a market with the potential todouble its sales, without even takinginto account the channels’ transfershare.An optimistic viewpoint…

I prefer to call it being aware. Beingaware that we are years behind othercountries. I’m not Italian and I comefrom markets that got started at least20 years before Italy. In those placesdevelopment followed a similar path,which is why I insist so much onhouseholds as a priority target forour stores and on our ability to getcustomers in-store and show themDIY is not just a job to be done butan enjoyable hobby, as it is abroad.Naturally to reach that goal cus-tomers have to be encouraged,trained if you like, and led into a newway of thinking.

Interview

New store openings for SelfSpecial offers no longer have the ef-fect they used to. Is this becausepeople have less money to spend orare there other reasons?A year ago it was different. Cus-tomers often came into a store be-cause there was a special offer. But inthe end too many special offers canproduce the opposite effect. A specialoffer from one chain tends to resem-ble to another until in the end thecustomer feels he has everything heneeds. This is why we retailers haveto be creative and find new solutionsand new products so we can gradual-ly leave behind the strategy of cut-ting prices to the bone. After all at atime when the “hard” sell and prod-uct promotions are increasing mosthouseholds really do have less moneyto spend. Now let’s talk about development.How is your second retail brandDottorbrico doing?Dottorbrico occupies a very differentposition in the market compared toSelf and the results have been inter-esting so far, so we want to continuethis type of development. It’s a localstore, with a target of customers nomore than five minutes from its loca-tion. It has to have a very versatilerange of products but there doesn’tneed to be a vast assortment. Theservices supplied there are also quitebasic. And what do you have planned forSelf?We have two store openings comingup. The first in Alessandria, sched-uled for July and the second later onin the year together with anotherDottorbrico opening. At the mo-ment we aren’t revealing the loca-tions but we can confirm they will bein northern Italy. �

BricoMagazine36

A survey of DIY chains in Italy

A negative year for the DIY retail networkAs 2012 came to a close, the DIY network was still suffering the effects of the economiccrisis, with the number of outlets down. Conversely, increases were recorded both in totaldisplay space and in the average size of Italian DIY centres.

The negative trend recorded bythe DIY retail network con-

tinued in the second half of 2012.This situation is, unfortunately, notsurprising and one that shows nosign of an upturn. The first news ofthe year from the sector was that ofthe disappearance of Punto Brico,a “historic” consortium that waspractically halved in size as resultof the loss – a serious blow – ofDefì Brico, with its Brico Pointbrand, followed by the closure ofanother of its members, “La Fab-brica delle Idee” in Palermo. It is

known that some of its six remain-ing members (nine stores) have de-cided to continue as independentoperators, while others are appar-ently forming a new group. Addedto this there is the “troubled” situa-tion of Brico Io: its most importantmember, which has 55 stores, hasapplied to go into receivership, andthe coming months therefore lookset to be crucial for this retailer.However, going back to the secondhalf of 2012 and the figures relat-ing to the DIY network, a dropwas recorded in the overall number

by Giulia Arrigoni

The survey considers italian Diychains that have at least threestores, regardless of their size or type (franchise or direct). Dottor Brico is included, eventhough it initially had only oneoutlet, because it is part of theSelf Group.

Diy retail chains inItaly: data as of 31 december 2012

BricoMagazine 37

=

=

=

=

=

=

��

��

�

�

Total n° of stores

Total n° of directstores

Total n° offranchise

stores

Total display

area (sq m)

Average display area

(sq m)

��

��

��

��

�

110

12

88

88

58

12

63

7

31

5

12

26

3

22

47

6

53

4

19

28

15

709

32

12

53

64

17

12

63

7

2

5

12

26

3

22

47

6

53

4

19

28

15

502

78

-

35

24

41

-

-

-

29

-

-

-

-

-

-

-

-

-

-

-

207

176.473

11.800

147.700

221.183

89.750

31.500

140.116

34.340

36.150

11.650

42.500

74.020

5.768

39.500

391.106

15.250

208.656

8.300

49.330

90.050

31.650

1.856.792

1.604

983

1.678

2.513

1.547

2.625

2.224

4.906

1.166

2.330

3.542

2.847

1.923

1.795

8.321

2.542

3.937

2.075

2.596

3.216

2.110

2.622

BRICO IOwww.bricoio.it

BRICO ITALIAwww.bricoitalia.it

BRICO OKwww.bricook.it

BRICOCENTERwww.bricocenter.it

BRICOFERwww.bricofer.it

BRICOLIFEwww.bricolife.com

BRICOMANwww.bricoman.it

BRICOMANIAwww.famigliulo.com

BRIGROSwww.brigros.com

GRANBRICOwww.granbrico.it

GRUPPO FDTwww.fdtgroup.it

DOTTOR BRICO*

ITALBRICO - CIB

LEROY MERLINwww.leroymerlin.it

MONDOBRICOwww.mondobrico.com

OBIwww.obi-italia.it

PRONTO HOBBY BRICO

PUNTO BRICOwww.puntobrico.com

BRICOLARGEwww.bricolarge.com

SELFwww.selfitalia.it

UTILITYwww.utility.it

TOTAL/AVERAGE

BricoMagazine38

% 1° sem. 2006 VS 2° sem. 2006

The evolution of the italian Diy retail chain network over the years (2002-2012)

2002 315 178 137 652140 2.070

2003 418 256 162 820.947 1.964

2004 477 293 184 982.398 2.060

2005 512 304 208 1.112.659 2.173

2006 576 371 205 1.288.539 2.237

2007 641 401 240 1.439.223 2.245

2008 717 459 258 1.622.714 2.263

2009 719 473 246 1.675.593 2.330

2010 742 487 255 1.864.685 2.513

2011 736 500 236 1.883.878 2.568

2012 709 502 207 1.856.792 2.622

Total n°of stores Year

Total n° of direct stores

Total n° of franchise stores

Total display area (sqm)

Average displayarea (sqm)

Source: BricoMagazine

% 1° sem. 2006 VS 2° sem. 2006Diy retail chain network: changes in the past year

Display area

Total number of stores

Total number of direct stores

Total number of franchise stores

1,0%

-1,1%

-0,2%

-3,3%

Second half of 2012 vs First half of 2012

Diy retail chain network by geographical area

North 54,2 61,1

Centre 18,1 16,2

South 17,1 13,6

Sicily/Sardinia 10,7 9,1

% stores % surface areaArea

Source: BricoMagazine

of stores, which fell from 717 to709. This was due to the loss of onedirect store (the number in this cat-egory thus fell from 503 to 502),but most of all to the endless trick-ling away of stores belonging tofranchising organisations and asso-

ciations (at the end of the year thesehad fallen by seven against the 214existing in the first half of 2012 andby 29 compared with the numberrecorded at the end of 2011). Con-versely, the total display space in-creased by over 19 thousand square

metres, from 1,837,549 to1,856,878, but it is still a long wayfrom reaching the 2011 record of1,883,878 square metres.

The second half of theyear, chain by chain Overall, the network of specialistDIY direct outlets was still holdingits own at the end of the year.However, some closures wererecorded: the Granbrico store inAlseno (near Piacenza) closed andanother Granbrico store was ab-sorbed by the Grancasa store inVillorba (near Treviso). Direct out-lets were also closed by Bricocenter(Gruppo Adeo), which stoppedtrading in Molfetta and Legnago,and Utility, which closed its Pied-imulera store (near Verbania).Brico Ok did better, closing twostores but opening four, while somechains recorded only new openings:Bricoman (1), Mondobrico (1), Obi(1) and Self (1). Leroy Merlin spentlast year busily expanding its Roma

A survey of DIY chains in Italy

BricoMagazine 39

Number of stores per region and breakdown by surface area category

2

87

20

139

44

45 7

253

50

41

14

22

38

22

17

18

58

22

LOMBARDYTRENTINO ALTO ADIGE

FRIULI VENEZIA GIULIA

EMILIA ROMAGNA

VENETO

��11

AOSTA VALLEY

����

1940235

���

576

����

35661028

����

1524127

����

8743

����

111674

MARCHE

���

8113

ABRUZZO

����

81112

APULIA

����

3812

CALABRIA

����

321431

BASILICATA

��

21

SICILY

����

101645

MOLISE

��52

����

11612

PIEDMONT

LIGURIA

���

� up to 1.500 sq m � from 1.501 to 3.000 sq m � from 3.001 to 5.000 sq m � more 5.000 sq m

26114

SARDINIA

����

13723

CAMPANIA

����

221436

LAZIO

���

782

UMBRIA

����

211634

TUSCANY

35

Laurentina outlet and moving itsArzano store, while Self convertedits own-brand stores in Turin andVillanova into Dottor Brico outlets,thereby increasing this chain to atotal of three stores. Seemingly un-stoppable, on the other hand, wasthe steady loss of franchise stores

which, the space of a year, fell by al-most 30 in number. Particularlyhard hit was the Bricocenter retailchain which, in just a year, lost 11franchise stores; other franchisingcompanies fared a little less badly:the Bricofer chain lost four stores,dropping from 45 to 41, while

Brico Ok lost three(falling from 38 to 35).

Bricomania held onto its 29 fran-chise stores, while Brico Io man-aged to add one, increasing its totalfrom 78 to 79 stores. There wasconsiderable activity among the

>>>>

BricoMagazine40

consortia, which, however, re-mained numerically stable on thewhole: Brico Italia added two newstores, Bricolife lost three andgained three in the second half, butincreased its total by a remarkable11 stores (from 52 to 63) over theyear as a whole. The FDT Grouplost one outlet, recording four newopenings but five closures in thesecond half of the year, while Ital-brico was stable in the second half(3 closures and 3 new stores), butdown by seven stores on the figure

recorded in December 2011; Brico-large, too, recorded no change inthe second half but closed the yeartwo stores down compared with theend of 2011. Finally, closures haveleft the Brikocasa chain with justtwo stores and it is therefore nolonger covered by the survey (we re-mind readers that only chains withat least three stores are included inthe survey). Other chains, likeBrigros, Bricomania and ProntoHobby Brico, remained stable,

N° of stores: % values by geographical areas and surface area categories

North 27,3% 43,5% 16,4% 12,8% 384

Centre 45,3% 38,3% 7,0% 9,4% 128

South 52,1% 35,5% 5,8% 6,6% 121

Sicily/Sardinia 47,4% 35,5% 10,5% 6,6% 76

up to 1.500 sq m 1.501-3.000 sq m 3.001-5.000 sq m more 5.000 mq Total (n°)Area

Source: BricoMagazine

Number of stores: the leading provinces by surface area category

Cosenza

Roma

Salerno

Cagliari

Perugia

Torino

Bergamo

Sassari

Brescia

Firenze

Macerata

Nuoro

Trento

17

14

9

7

7

7

6

6

5

5

5

5

5

Milano

Torino

Roma

Varese

Brescia

Pavia

Alessandria

Cosenza

Perugia

Vicenza

Como

Lecce

Novara

16

11

10

10

8

8

7

7

7

7

6

6

6

Torino

Bolzano

Brescia

Cuneo

Milano

Padova

Udine

Vicenza

12

4

3

3

3

3

3

3

Milano

Roma

Brescia

Napoli

Torino

Varese

Venezia

14

6

3

3

3

3

3

FROM 0 TO 1.500 SQ M FROM 1.501 TO 3.000 SQ M FROM 3.001 TO 5.000 SQ M MORE 5.000 SQ M

Source: BricoMagazine

>>>>

“

Despite a reduction inthe number of stores

(from 717 to 709), mainlyfranchise stores, the totaldisplay area increased,but it is still a long way

from reaching the recordresult of 2011.

“

A survey of DIY chains in Italy

BricoMagazine42

recording no changes either in re-lation to the previous year or in re-lation to the first half of 2012.

Increasing surface areaswith the North againleading the wayAlthough the network shrank interms of the total number of stores,which fell from 717 to 709, theoverall retail area increased, albeitwithout reaching the almost 1.9million square metres recorded atthe end of 2011. Nevertheless, theaverage surface area per store con-tinued to increase, rising from2,586 to the current 2,622 squaremetres, which is 36 square metres(14.7%) more than in 2011 and26.6% more than in 2002, whenthe mean surface area of a DIYcentre was little more than 2,000square metres. Due to the crisisand network reorganisation, theNorth of Italy once again emergesas a leading player; one need onlyconsider that having recorded a51% share of the total number ofsales outlets in 2011, at the end of2012 this figure had risen to54.2%. But at the expense of whichpart of Italy? Pretty much all of therest of the country, even thoughSicily and Sardinia seem to havebeen the hardest hit, their sharedropping from 12.5% in 2011 to10.7% a year later. A similar pat-tern emerges if the analysis insteadconsiders exhibition space, withthe North increasing its share from58.1% to 61.1% at the end of 2012.Generally speaking, the bulk of themodern DIY network (over 40% ofoutlets) is made up of stores with asurface area of between 1500 and3000 square metres. These, togeth-er with the ones covering up to1500 square metres, account forover 77% of the total. �

Number of stores per chain by surface area category

0 - 1.500 sq m: 262 stores 1.501 - 3.000 sq m: 286 stores

3.001 - 5.000 sq m: 87 stores More 5.000 sq m: 74 stores

BRICO IO 66

BRICO OK 42

BRICOFER 38

BRICOMANIA 24

BRICOLIFE 23

BRICOCENTER 21

ITALBRICO-CIB 12

BRICO ITALIA 11

PUNTO BRICO 7

FDT 5

BRICOLARGE 3

OBI 3

UTILITY 3

BRIGROS 1

GRANBRICO 1

PRONTO HOBBY BRICO 1

SELF 1

TOT 262

BRICO IO 44

BRICOCENTER 44

BRICO OK 43

BRICOLIFE 31

GRUPPO FDT 18

BRICOFER 17

OBI 17

SELF 15

UTILITY 11

ITALBRICO-CIB 8

PUNTO BRICO 7

BRICOLARGE 6

BRICOMANIA 6

GRANBRICO 5

MONDO BRICO 5

BRIGROS 3

DOTTOR BRICO 3

PRONTO BRICO HOBBY 2

BRICO ITALIA 1

TOT 286

OBI 21

BRICOCENTER 20

SELF 10

BRICOLIFE 8

PUNTO BRICO 4

BRICO OK 3

BRICOFER 3

BRICOLARGE 3

BRICOMAN 3

GRANBRICO 3

ITALBRICO-CIB 2

LEROY MERLIN 2

BRIGROS 1

GRUPPO FDT 1

MONDO BRICO 1

PRONTO BRICO HOBBY 1

UTILITY 1

TOT 87

LEROY MERLIN 45

OBI 12

BRICOMAN 4

BRICOCENTER 3

GRANBRICO 3

SELF 2

GRUPPO FDT 2

BRICOLIFE 1

BRICOMANIA 1

PUNTO BRICO 1

TOT 74

Source: BricoMagazine

hours buttonhole.

A

A survey of DIY chains in Italy

online catalog www.cecarredi.com

availability 24 hours 24

immediate delivery standard materials

study exhibition spaces

immediate response to every call

technical staff available 7 days a week 7

study and achievements intended exposure

customized for your environmentfurniture DIY

C.&C. METAL FURNITURE s.r.l.via San Cassiano 11 - 24030 Mapello (BG)

ph. +39 035 4945966 - fax +39 035 4945391 - e-mail: [email protected]

We operate in the construction of metal furniture from 1972: the quality is not invented, but it is built with the experience. Starting from the needs and the customer’s specifi cations we can provide offers without any commitment, develop projects and customized to make the products fi nished. With the knowledge that on-time delivery is our fi hours buttonhole.

ADVANCED TECHNOLOGYFOR QUALITY PRODUCTS

mini zeus

storagebulk material

port palletsfor external

delta

rear protectionand lateral

internal and externalcantilever

single-sided gondola

oil storage

shelf with loft

double-sided gondola

storage materialin vertical

integrated gondola

to pine

port pallets

storage panels

METAL FURNITUREFURNITURE DIY

BricoMagazine44

The shop is located in viaMarengo in Carate Brianza,

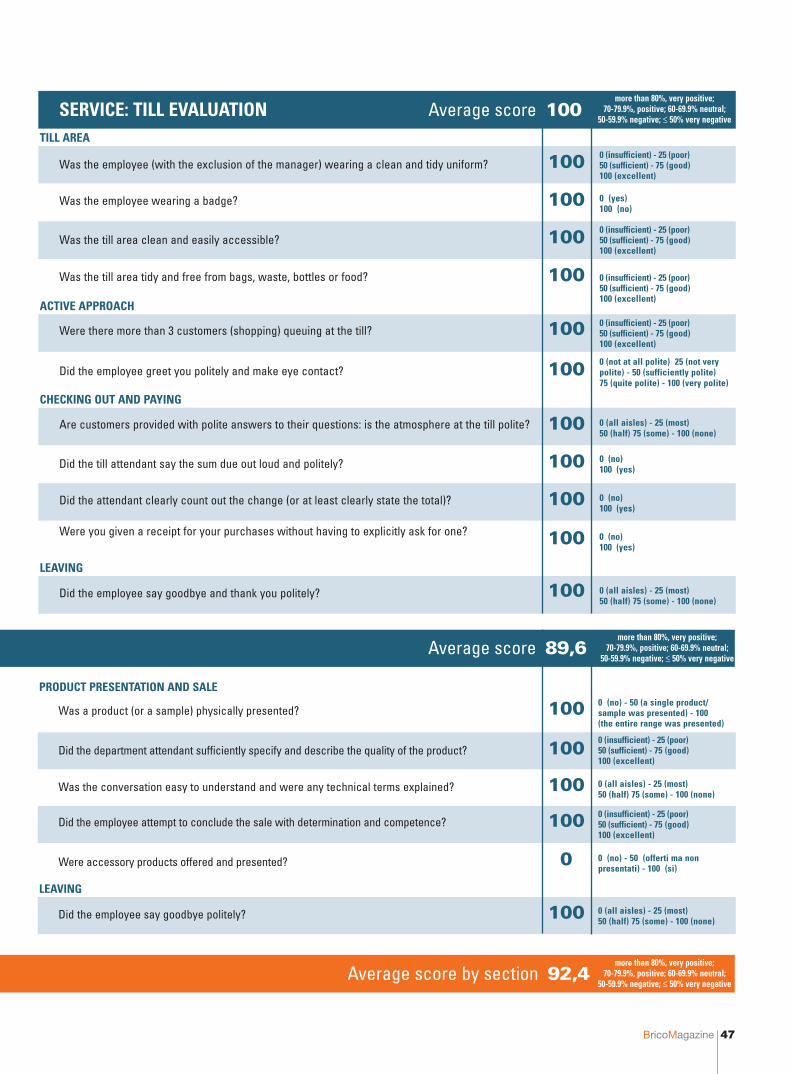

in the province of Monza Brianza,just off state road 36 NuovaValassina. Our mystery shopperwas a young man of 24 years, withdark brown hair, a beard, a slimframe and about 170 cm tall. Thevisit was made on 16 January thisyear at 10.40 am.

The outlet and generalatmosphereThe Bricoman stores are new con-structions that always have a largecar park and the Carate shop is noexception in this sense. A signifi-cant positive point is that, eventhough it was snowing at the timeof the visit, the car park was ac-cessible and tidy. There is nothing

Visiting the Bricomanoutlet in Carate Brianza

in collaboration with Interactive Market Research

A true “phenomenon” of Italy’s DIY retail sector, Bricoman is a brand of the Adeo Groupcomprising 7 shops. Our mystery client visited the Bricoman store in Carate Brianza.

Established in 1999 by a group of marketing pro-fessionals and market researchers for consumers,Interactive Market Research was the first marketresearch company in Italy to focus its developmentplans online and pursue a real strategy of special-ization in this field, while continuing to also con-duct traditional method research. The Interactiveteam was formed and refined over the years toprovide valid professional research and integratedconsultation to client, with expertise in the context

of marketing and re-search in every marketsector. Its decade of ex-perience in research has helped Interactive to re-spond to all major marketing requirements, involv-ing different consumer targets and guaranteeingthe representative qualities of the same with re-gard to the national population. www.interactive-mr.comInfo: Maurizio Pucci: [email protected]

About Interactive Market Research

Mistery Client

Bri-

negative to report in regard to thepresence of shopping trolleys andbaskets, the floors were very clean,there was no waste or dust on theshelves. Even the bathrooms wereclean although they was a slightbad odour. The bathrooms hadtoilet paper and soap, but the elec-tric dryers were off or out of work.Automatic drink and snack vend-ing machines were available. Mov-ing on to evaluate the sales out-let, the store islarge, with manywell displayedand easily identi-fiable products.Our shopper didnot note short-ages, and hefound boxes ona pallet and apallet truck,apparently

not being used, in only two aisles.Leaflets were available but notvery visible, the shopper only sawone after he had paid. In general,the atmosphere was typical of alarge DIY store. There was nomusic, the temperature was com-fortable, there was a generally

>>>>

pleasant smell. There is a largecentral aisle with signs clearly in-dicating the various departments.All members of staff were wearingneat, clean uniforms, includingsafety footwear. Only till atten-dants however were wearing aname badge.

Service: evaluation of thesales personnelAfter asking an employee in the

central aisle, the shopperwas introduced to theperson responsible forthe department he askedabout, who was wearinga clean and tidy uniformbut not a badge. Theevaluation was made inthe electrical depart-ment, and the shopperasked for information

FACT SHEET

Outlet visited:Bricoman, Via Marengo, 20841 Carate Brianza (MB).

Date and time of visit: 16 January2013 at 10.40.

Brief description of the outlet: large store, with large car park, located in a large building containingonly the store.

Mystery client description: 24 year old man, dark brown hair, blue eyes,beard, 170 cm tall, slim build.

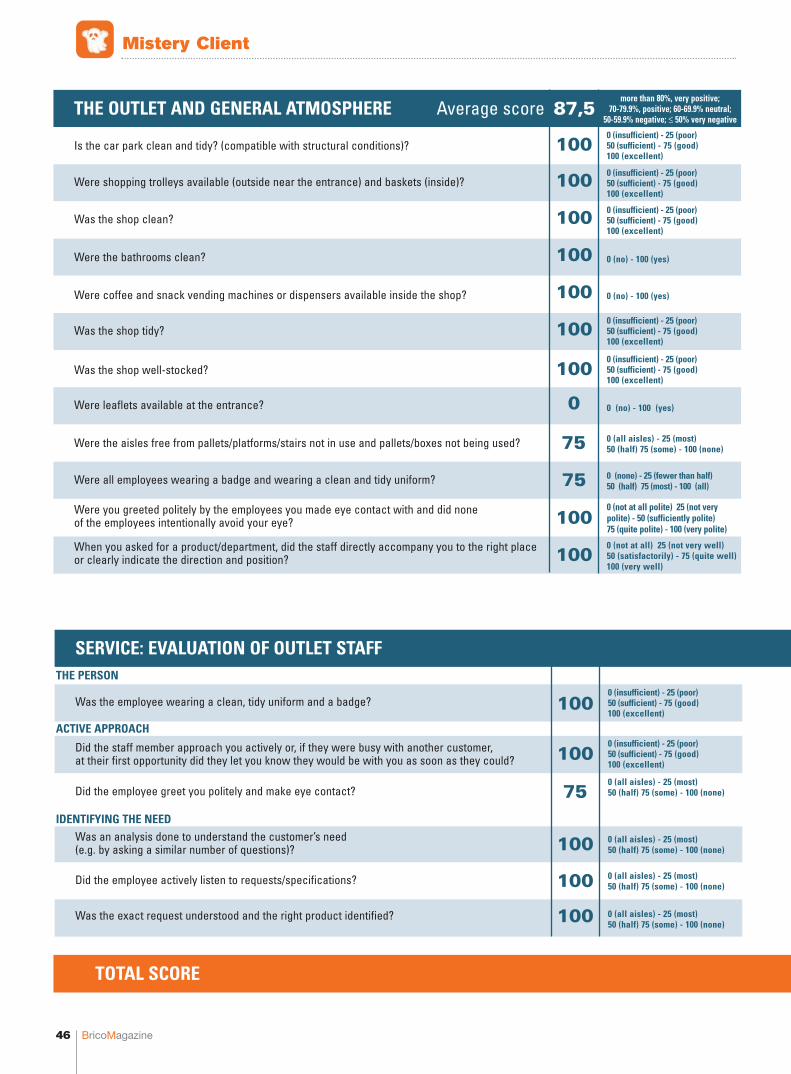

BricoMagazine46

THE OUTLET AND GENERAL ATMOSPHERE Average score 87,5

Is the car park clean and tidy? (compatible with structural conditions)?

Were shopping trolleys available (outside near the entrance) and baskets (inside)?

Was the shop clean?

Were the bathrooms clean?

Were coffee and snack vending machines or dispensers available inside the shop?

Was the shop tidy?

Was the shop well-stocked?

Were leaflets available at the entrance?

Were the aisles free from pallets/platforms/stairs not in use and pallets/boxes not being used?

Were all employees wearing a badge and wearing a clean and tidy uniform?

100

100

100

100

100

100

100

0

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (no) - 100 (yes)

0 (no) - 100 (yes)

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (no) - 100 (yes)

75 0 (all aisles) - 25 (most) 50 (half) 75 (some) - 100 (none)

75 0 (none) - 25 (fewer than half)50 (half) 75 (most) - 100 (all)

Were you greeted politely by the employees you made eye contact with and did none of the employees intentionally avoid your eye?

When you asked for a product/department, did the staff directly accompany you to the right placeor clearly indicate the direction and position?

1000 (not at all polite) 25 (not very polite) - 50 (sufficiently polite) 75 (quite polite) - 100 (very polite)

1000 (not at all) 25 (not very well) 50 (satisfactorily) - 75 (quite well)100 (very well)

Was the employee wearing a clean, tidy uniform and a badge?

Did the employee greet you politely and make eye contact?

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (insufficient) - 25 (poor) 50 (sufficient) - 75 (good)100 (excellent)

0 (all aisles) - 25 (most) 50 (half) 75 (some) - 100 (none)

Did the staff member approach you actively or, if they were busy with another customer, at their first opportunity did they let you know they would be with you as soon as they could? 100

75

THE PERSON

ACTIVE APPROACH

0 (all aisles) - 25 (most) 50 (half) 75 (some) - 100 (none)

Was an analysis done to understand the customer’s need (e.g. by asking a similar number of questions)? 100