bridging to finance

TRANSCRIPT

Bridging to Finance

Pavel V. ShevchenkoQuantitative Risk Management

CSIRO Mathematical & Information Sciences

Conference “ Quantitative Methods in Investment and Risk Management: sourcing new approaches from mathematical theory and the real world”Melbourne Centre For Financial Studies, 20 th September 2007.

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

• Commonwealth Scientific and Industrial Research Organization of Australia (CSIRO)

• National research agency formed in 1926. • Approx 6500 staff (Divisions: Industrial Physics, Minerals,

Mathematical & Information Sciences, Marine and Atmospheric Research, etc.) www.csiro.au

• Division of Mathematical and Information Sciences ( CMIS)• (over 100 researchers): Decision Technology, Biotechnology and Health

Informatics, Environmental Informaticswww.cmis.csiro.au

• Quantitative Risk Management (QRM) group• (approx. 20 staff): financial risk, infrastructure, environment risk,

security, air-transport. Activities/modes of engagement: research, consulting, model development/validation, software development,… . www.cmis.csiro.au/QRM

CSIRO Mathematical & Information Sciences

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

CSIRO Quantitative Risk Management

Risk assessment

Real-time monitoringInfrastructure, security, health

OATM

Energy/commodity modelling

Optimisation Air Traffic Management

Expert elicitation

Extremes, sparse dataFinancial Risk

Strategic researchApplication areas

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

CSIRO Mathematical & Information Sciences

Solutions• Development of mathematical models and customised software

according to the client methodology and specific needs.• Assisting with development of new models and their implementation

into software.• Independent review and advice on risk models, methodology and

software solutions.• Independent validation of derivatives and risk measurement models. • Time-series analysis of data.Modes of engagement

There are many ways CSIRO can work with you to understand andquantify financial risks:

• Consultancy engagement.• Contract research engagement.• Collaborative projects.• Software development.

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Track Records in Financial Risk

• Derivative pricing: work on CSIRO option pricing software Reditus since 1999, consulting projects in 2005, 2006, 2007.

• FX option pricing: plug-ins for Fenics launched in 2005 – 100 users in overseas banks.

• Operational Risk: validation projects in 2000, model development projects in 2001, 2003, R&D/software projects 2004-2007.

• Market Risk: validation projects in 2004, 2005, model development consultingproject in 2007.

• Credit Risk: validation projects in 1999, 2002; validation and model development projects 2004-ongoing.

• Underwriting risk: consulting projects in 1999, current proposals.• Forecasting electricity/commodities: consulting projects in 2002, 2005,

2005-06, current proposals. • Portfolio Management: model development projects in 2007, current

proposals.• Water/Carbon Trading: current proposals.• Collaborators: Monash Uni, Cambridge Uni, ETH Zurich, UNSW, UTS,

Macquarie Uni, Statistical Research Associates NZ• Industry clients : CBA, ANZ, NAB, St George, Integral Energy, IAG, Fenics

FX, Edgecap, Moore Capital, Ester Bank, Credit Swiss,… .

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

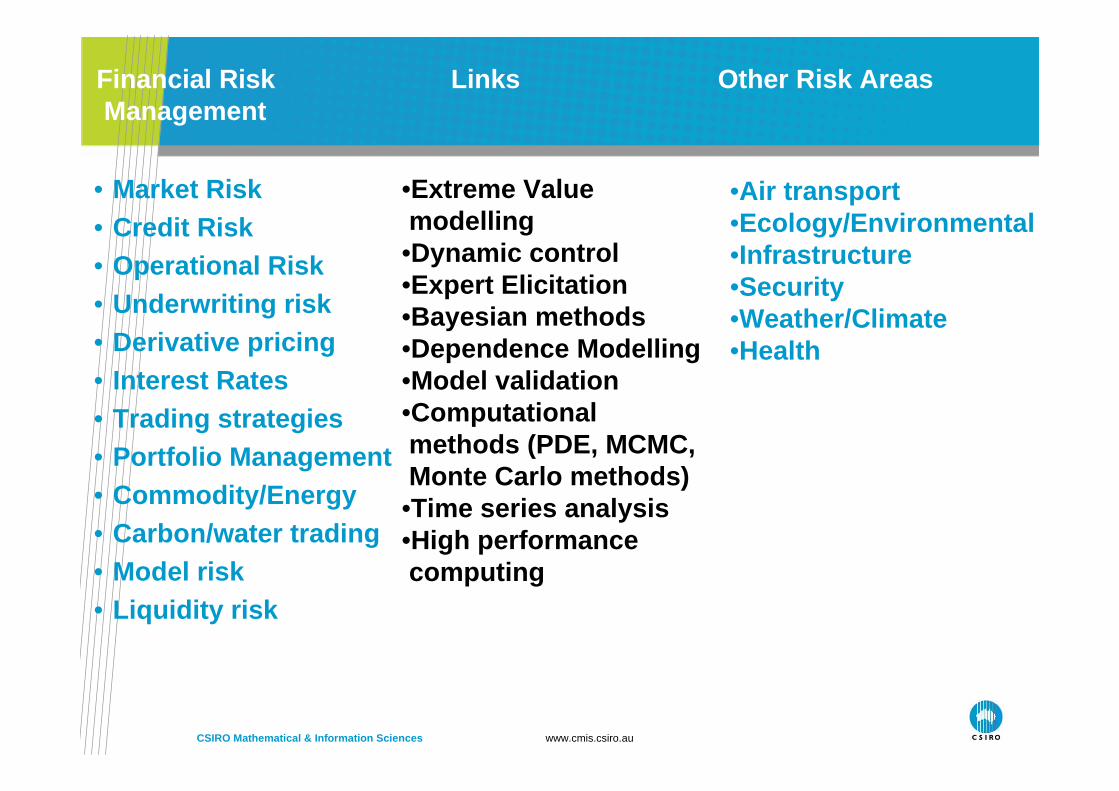

Financial Risk Links Other Risk AreasManagement

• Market Risk • Credit Risk • Operational Risk• Underwriting risk • Derivative pricing• Interest Rates• Trading strategies• Portfolio Management• Commodity/Energy• Carbon/water trading• Model risk• Liquidity risk

•Extreme Value modelling

•Dynamic control•Expert Elicitation•Bayesian methods•Dependence Modelling•Model validation•Computational methods (PDE, MCMC, Monte Carlo methods)

•Time series analysis•High performance computing

•Air transport•Ecology/Environmental•Infrastructure •Security•Weather/Climate•Health

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

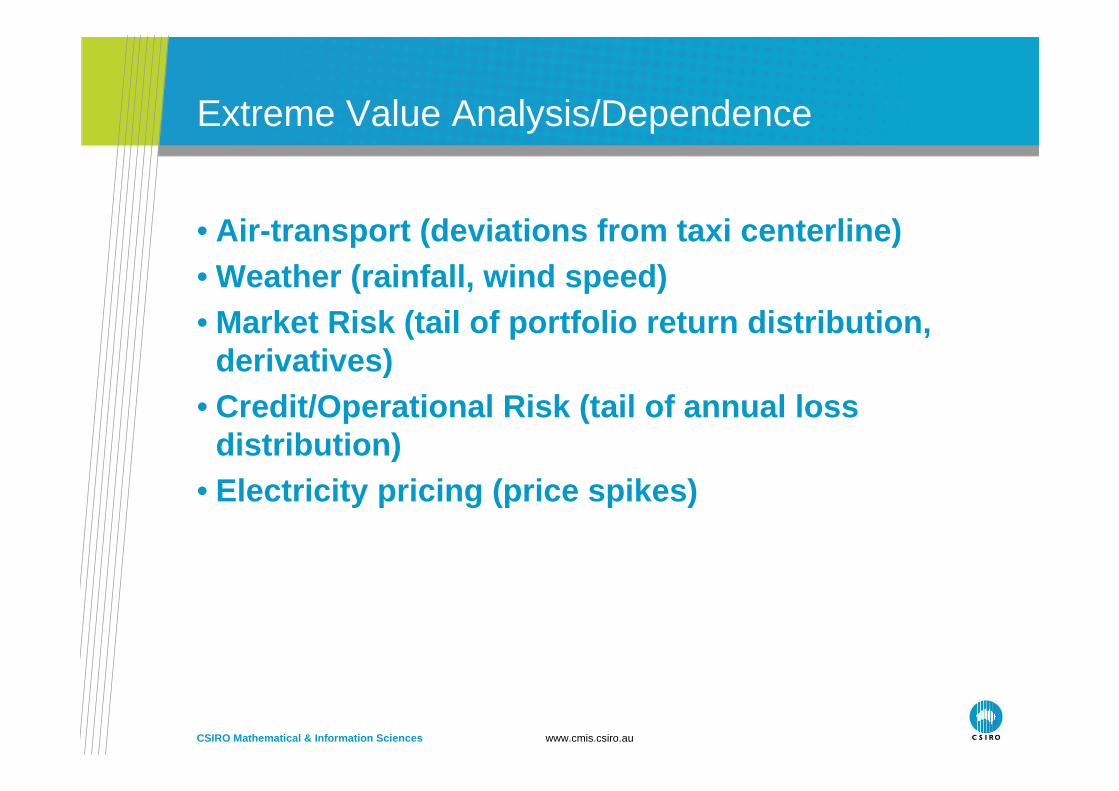

Extreme Value Analysis/Dependence

• Air-transport (deviations from taxi centerline)• Weather (rainfall, wind speed)• Market Risk (tail of portfolio return distribution,

derivatives)• Credit/Operational Risk (tail of annual loss

distribution)• Electricity pricing (price spikes)

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

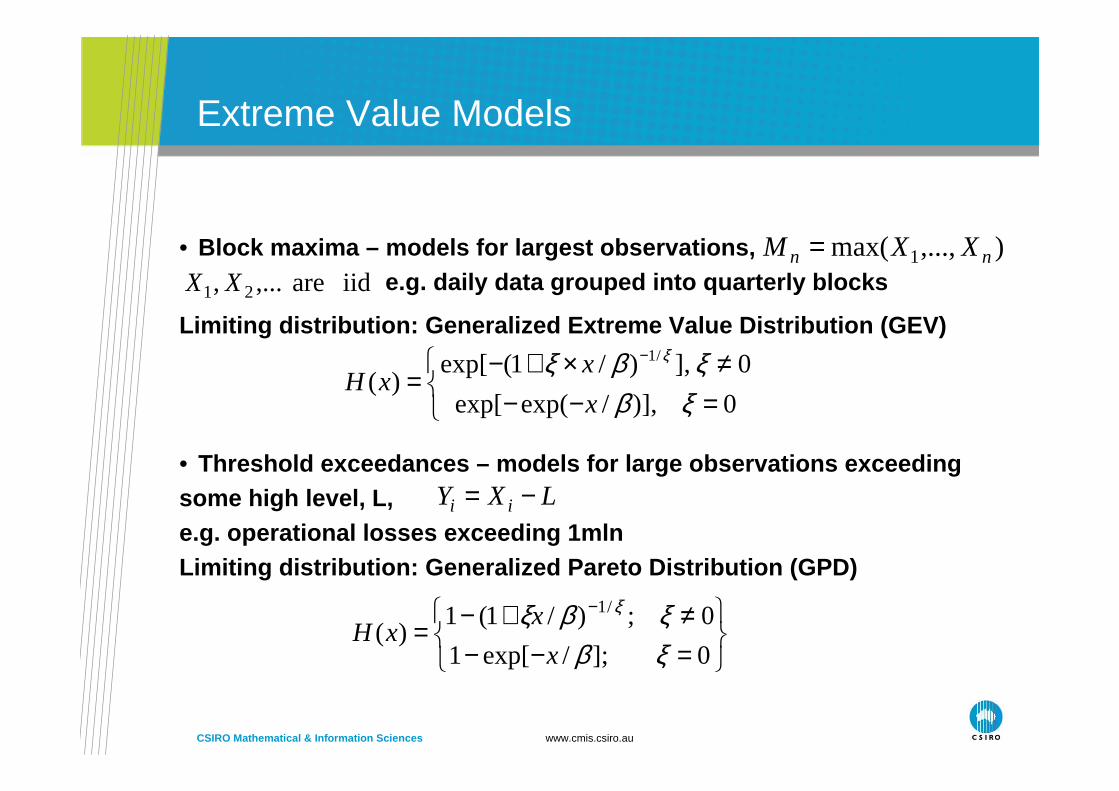

Extreme Value Models

• Block maxima – models for largest observations, e.g. daily data grouped into quarterly blocks

Limiting distribution: Generalized Extreme Value Di stribution (GEV)

• Threshold exceedances – models for large observations exceeding some high level, L,e.g. operational losses exceeding 1mln Limiting distribution: Generalized Pareto Distribut ion (GPD)

),...,max( 1 nn XXM =iid are ,..., 21 XX

=−−≠×+−

=−

0)],/exp(exp[

0],)/1(exp[)(

/1

ξβξβξ ξ

x

xxH

=−−≠+−=

−

0];/exp[1

0;)/1(1)(

/1

ξβξβξ ξ

x

xxH

LXY ii −=

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

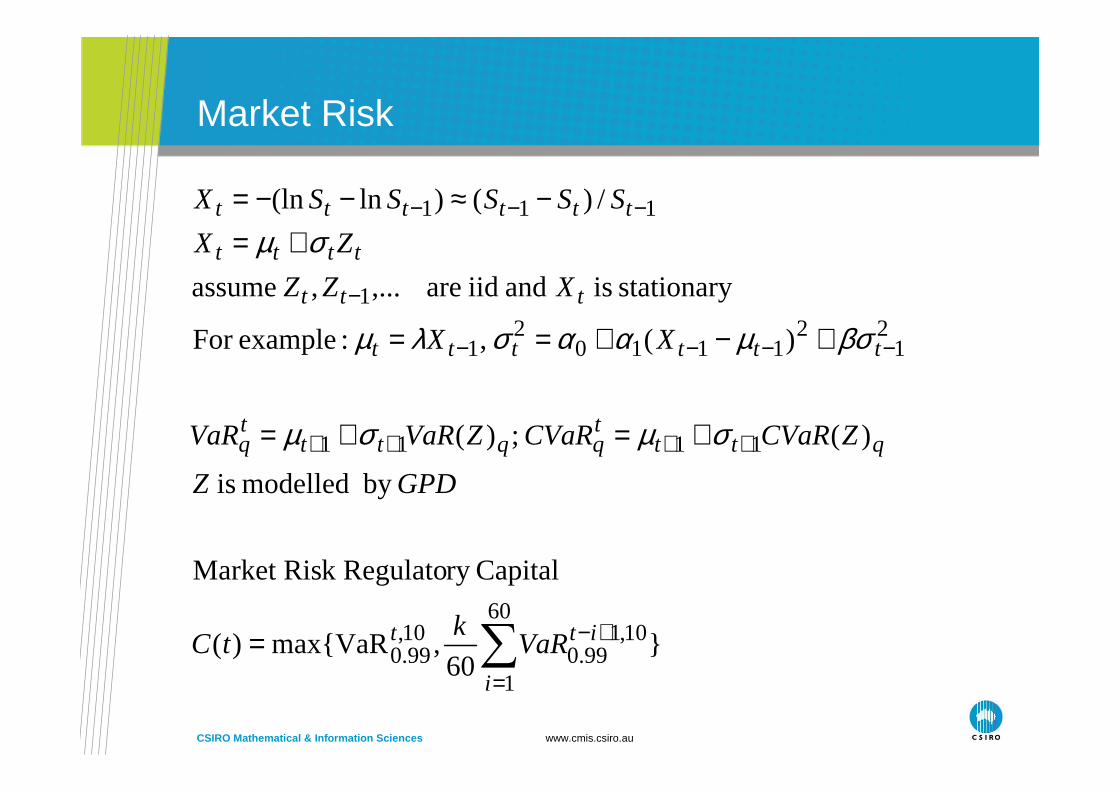

Market Risk

}60

,max{VaR)(

Capitalry k RegulatoMarket Ris

by modelled is

)(;)(

)(,:exampleFor

stationaryisandiidare,...,assume

/)()ln(ln

60

1

10,199.0

10,0.99

1111

21

21110

21

1

111

∑=

+−

++++

−−−−

−

−−−

=

+=+=

+−+==

+=−≈−−=

i

itt

qtttqqtt

tq

tttttt

ttt

tttt

tttttt

VaRk

tC

GPDZ

ZCVaRCVaRZVaRVaR

XX

XZZ

ZX

SSSSSX

σµσµ

βσµαασλµ

σµ

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Example: API returnsGARCH-Normal GARCH-Student t

GARCH-Generalized Pareto GARCH-volatility

Asset residual Q-Q plot

-5-4-3-2-1012345

-5 -4 -3 -2 -1 0 1 2 3 4 5

theoretical quantile

empi

rical

qua

ntile

Asset residual Q-Q plot

-5-4-3-2-1012345

-5 -4 -3 -2 -1 0 1 2 3 4 5

theoretical quantile

empi

rical

qua

ntile

Asset residual Q-Q plot

-5-4-3-2-1012345

-5 -4 -3 -2 -1 0 1 2 3 4 5

theoretical quantile

empi

rical

qua

ntile

volatility

0.010

0.030

0.050

0.070

0.090

0.110

28/07/01 10/12/02 23/04/04 05/09/05 18/01/07

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Derivative Pricing

methods. Carlo Monte ,Difference Finite Element, Finite :Methods Numericaldiffusion jump models,y volatilitstochastic

,),()(/ - modelsy volatilitlocal e.g.:skewy volatilitModelling

]|)([ pricingOption :

tdWttSdttqtrtStdS

tSTSPayoffEtQ

σ+−=

=

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

)(Prob)(with,...,1rvsConsider ixiXixiFdXX ≤=

)1,0(~)(),1,0(~),(1~)(1 UiUiXiFUiUiUiFiXiFiUiF =−=⇒−

cdfjointis]≤,...,2≤2,11[Prob),...,2,1( dxdXxXxXdxxxF ≤=

iF,behaviormarginal ),.,1(copula duuC

),...,2,1( dxxxF

),...,2,1())(),...,2(2),1(1( dxxxFdxdFxFxFC =

))(1),...,2(12),1(1

1(),...,2,1( dud

FuFuFFduuuC −−−=

Dependence modelling via Copula method

Copula is multivariate joint distribution of unifor m random variables

Dependence modelling

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Dependence modelling via copula

-4

-3

-2

-1

0

1

2

3

4

-4 -3 -2 -1 0 1 2 3 4

X

Y

-4

-3

-2

-1

0

1

2

3

4

-4 -3 -2 -1 0 1 2 3 4

X

Y

-4

-3

-2

-1

0

1

2

3

4

-4 -3 -2 -1 0 1 2 3 4

X

Y

7.0),(

)1,0(~);1,0(~

=YXcorr

NormalYNormalX

t2 Copula

Gumble Copula

Gaussian Copula

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Expert Elicitation/Bayesian methods(combining internal & external data with expert opinion)

• Ecology (estimation of fish density from gillnet ca tches)• Operational Risk (estimation of loss frequency and severity)• Air-transport (individual&collective risk of air-col lisions)• Insurance (pricing of policy premium)• Markov Chain Monte Carlo methods (signal processing )

• Recent Publications:• D. D. Lambrigger (ETH), P.V. Shevchenko (CSIRO) and M. V. Wüthrich (ETH), 2007. The

Quantification of Operational Risk using Internal Data, Relevant External Data and Expert Opinions. The Journal of Operational Risk.

• Hans Bühlmann (ETH), P.V. Shevchenko (CSIRO) and M. Wüthrich (ETH), 2006. A “Toy”Model for Operational Risk Quantification using Credibility Theory. The Journal of Operational Risk 2(1).

• P.V. Shevchenko (CSIRO) and M. Wüthrich (ETH), 2006. Structural Modelling of Operational Risk using Bayesian Inference: combining loss data with expert opinions. The Journal of Operational Risk 1(3), pp.3-26.

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

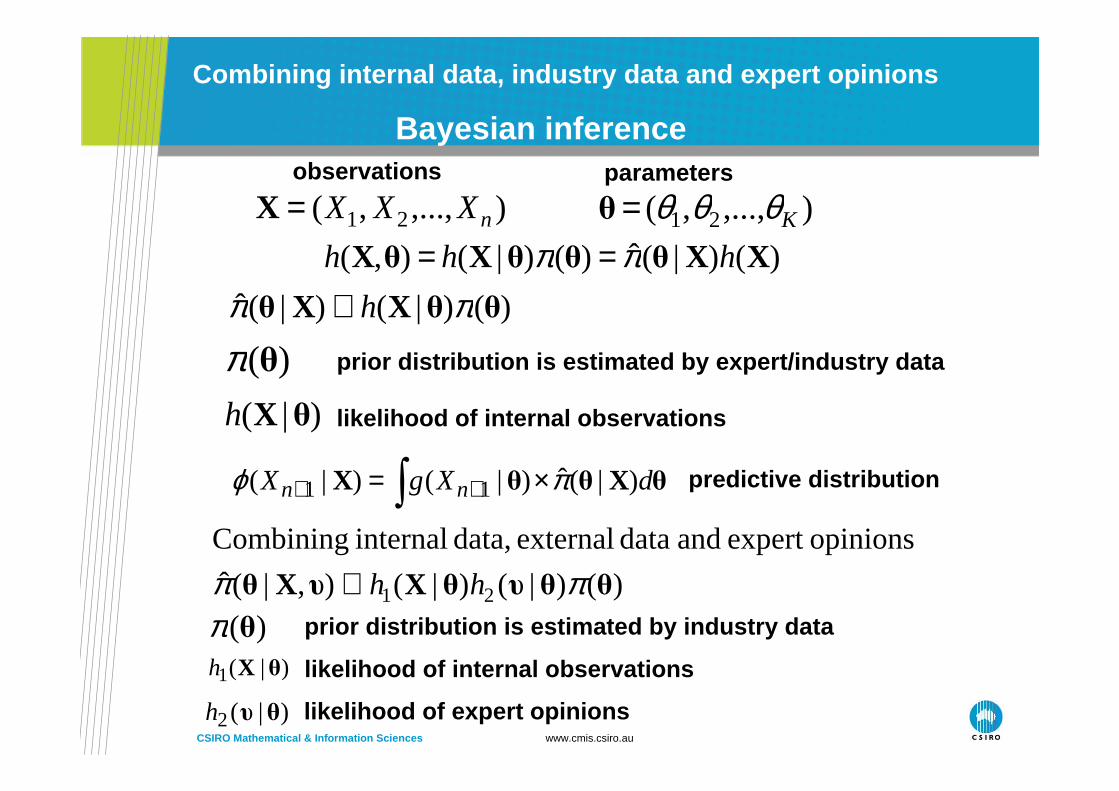

Combining internal data, industry data and expert o pinions

Bayesian inference

)()|(ˆ)()|(),( XXθθθXθX hhh ππ ==),...,,( 21 nXXX=X

)()|()|(ˆ θθXXθ ππ h∝

),...,,( 21 Kθθθ=θobservations parameters

)(θπ prior distribution is estimated by expert/industry data

)|( θXh likelihood of internal observations

∫ ×= ++ θXθθX dXgX nn )|(ˆ)|()|( 11 πϕ predictive distribution

)()|()|(),|(ˆ

opinionsexpert and data external data, internal Combining

21 θθυθXυXθ ππ hh∝)(θπ

)|(1 θXh

)|(2 θυh

prior distribution is estimated by industry data

likelihood of internal observations

likelihood of expert opinions

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

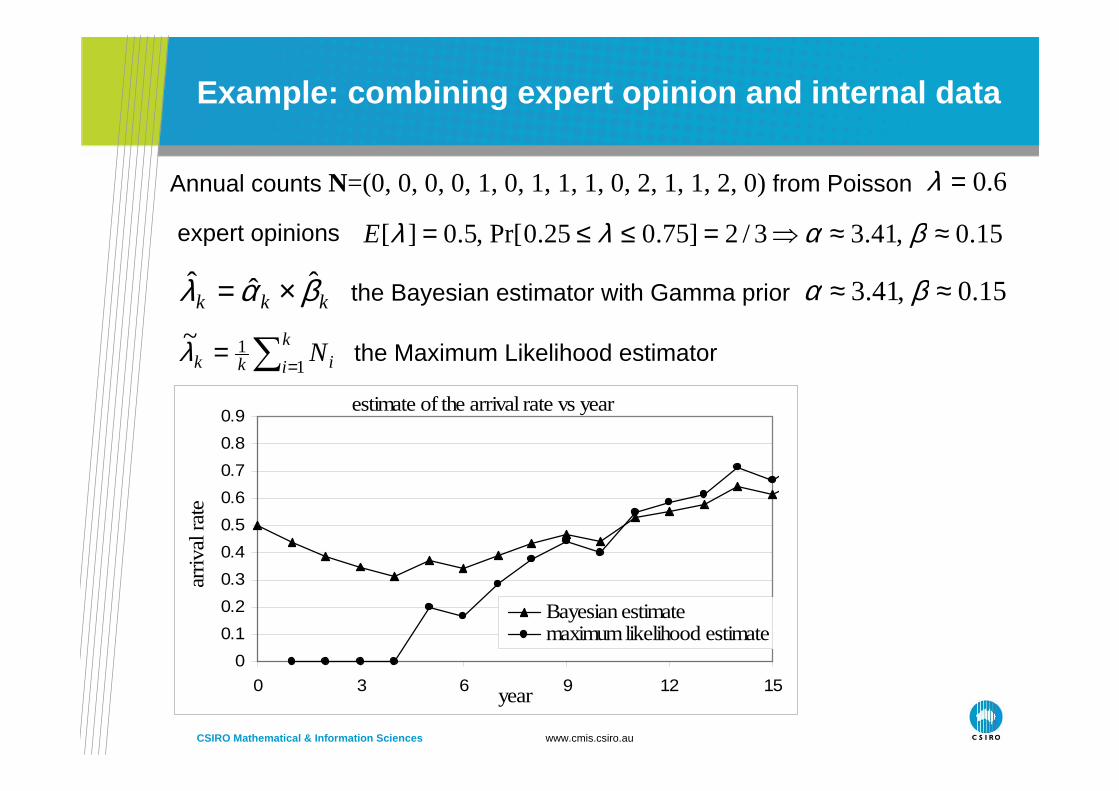

Example: combining expert opinion and internal data

estimate of the arrival rate vs year

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0 3 6 9 12 15year

arriv

al r

ate

j

Bayesian estimatemaximum likelihood estimate

15.0,41.3 ≈≈ βα

6.0=λ

the Bayesian estimator with Gamma prior

Annual counts N=(0, 0, 0, 0, 1, 0, 1, 1, 1, 0, 2, 1, 1, 2, 0) from Poisson

kkk βαλ ˆˆˆ ×=

∑ == k

i ikk N1

1~λ the Maximum Likelihood estimator

expert opinions 15.0,41.33/2]75.025.0Pr[,5.0][ ≈≈⇒=≤≤= βαλλE

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

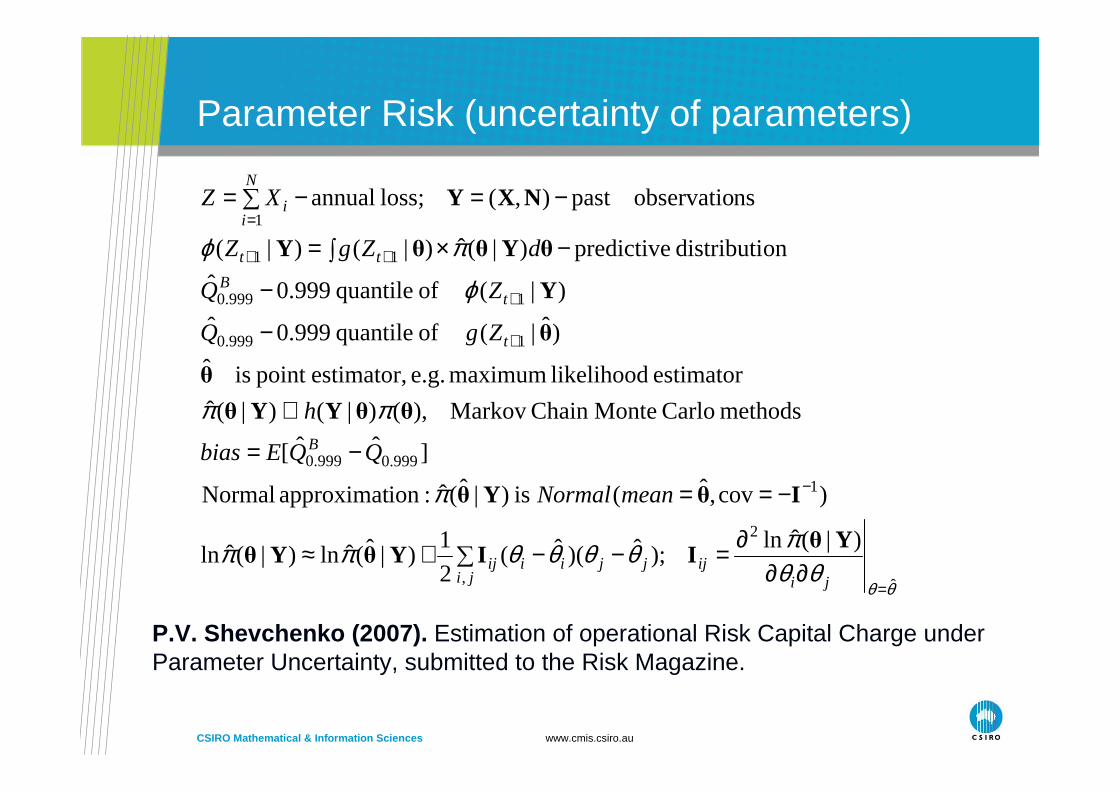

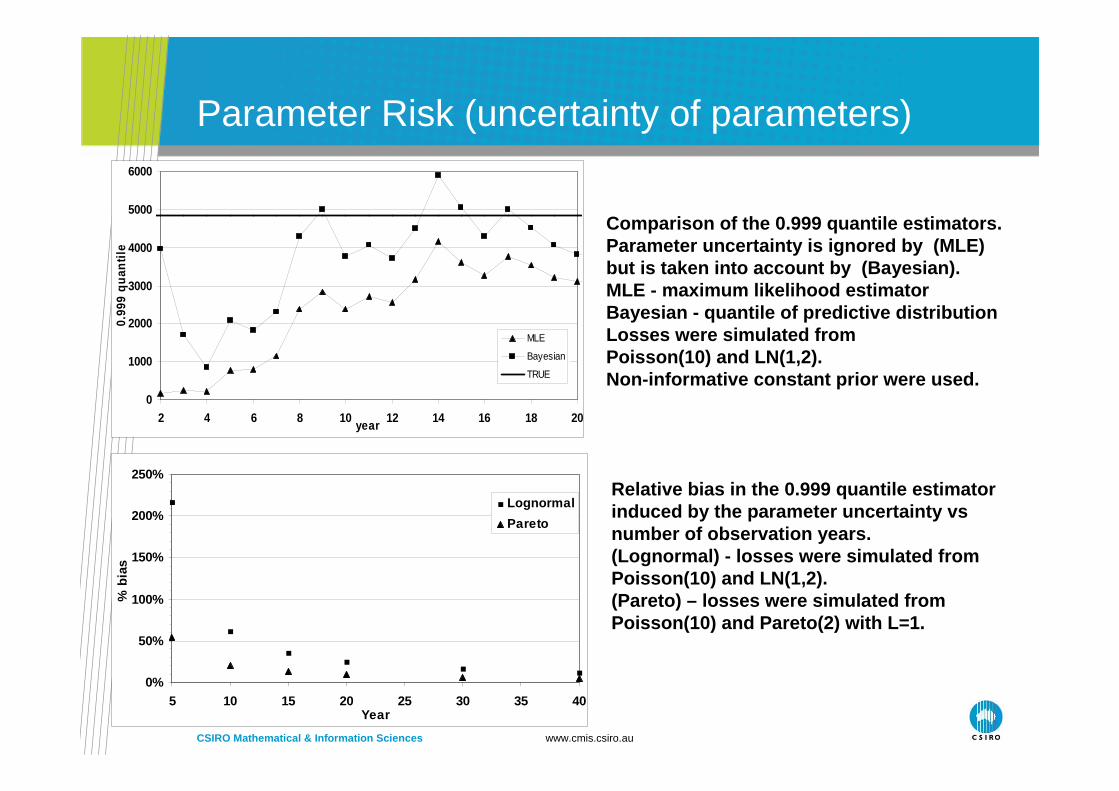

Parameter Risk (uncertainty of parameters)

θθθθ

πθθθθππ

π

ππ

ϕ

πϕ

ˆ

2

,

1

999.0999.0

1999.0

1999.0

11

1

)|(ˆln);ˆ)(ˆ(

2

1)|ˆ(ˆln)|(ˆln

)cov,ˆ(is)|ˆ(ˆ :ionapproximat Normal

]ˆˆ[

methods Carlo MonteChain Markov),()|()|(ˆ

estimator likelihood maximum e.g. estimator,point isˆ

)ˆ|(ofquantile999.0ˆ

)|(ofquantile999.0ˆ

ondistributipredictive)|(ˆ)|()|(

nsobservatiopast),(loss;annual

=

−

+

+

++

=

∂∂∂=−−∑+≈

−==

−=

∝

−

−

−∫ ×=

−=−∑=

jiijjjii

jiij

B

t

tB

tt

N

ii

meanNormal

QQEbias

h

ZgQ

ZQ

dZgZ

XZ

YθIIYθYθ

IθYθ

θθYYθ

θ

θ

Y

θYθθY

NXY

P.V. Shevchenko (2007). Estimation of operational Risk Capital Charge under Parameter Uncertainty, submitted to the Risk Magazine.

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Parameter Risk (uncertainty of parameters)

0

1000

2000

3000

4000

5000

6000

2 4 6 8 10 12 14 16 18 20year

0.99

9 qu

antil

e

MLE

Bayesian

TRUE

0%

50%

100%

150%

200%

250%

5 10 15 20 25 30 35 40Year

% b

ias

Lognormal

Pareto

Relative bias in the 0.999 quantile estimator induced by the parameter uncertainty vsnumber of observation years. (Lognormal) - losses were simulated from Poisson(10) and LN(1,2). (Pareto) – losses were simulated from Poisson(10) and Pareto(2) with L=1.

Comparison of the 0.999 quantile estimators. Parameter uncertainty is ignored by (MLE) but is taken into account by (Bayesian). MLE - maximum likelihood estimatorBayesian - quantile of predictive distributionLosses were simulated from Poisson(10) and LN(1,2). Non-informative constant prior were used.

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Kalman/Particle filter techniques(state-space models)

• On-line monitoring of water quality• Health surveillance• Modelling commodities/interest rates

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

State-space models: Kalman Filter

• Measurement Equation• Transition Equation

ttTtttTTt

tttttt

ttt

Tttt

tTCStTBtTAFSSEF

dtdWdWEdWdtXd

dWdtSd

FS

δδρσκδκαδ

σσδµ

δ

)(ln)()(ln],|[

][;][

][ln

prices futures yield, econveniencprice;spot

,,

)2()1()2(221

)1(1

212

1

,

−+−+−=⇒==+−−=

+−−=

−−−Commodity spot models:e.g. 2-factor convenience yie ld

Interest rate spot models:e.g. Vasicek model

tTttTt

ttt

Ttt

rtTBtTAPrTtBTtAP

dWdtrdr

Pr

)()(lnln]),(exp[),(

][

price bondrate; term-short

,,

,

−−−=⇒−=+−=

−−

σγα

eXBAF ttrrrr

+×+= ˆ

εrrrr

+×+=+ tt XTMX ˆ1

CSIRO Mathematical & Information Sciences www.cmis.csiro.au

Emerging over-arching research topics

• Mixing internal & external data with expert opinion s (credibility theory, Bayesian techniques)

• Dependence between risks: copula methods, structura l models

• Compound point processes • Modelling distribution tail: EVT, mixed distributio ns, splices• Efficient Markov Chain Monte Carlo, Monte Carlo, fi nite

element/finite difference methods • State-space models (sequential Monte Carlo, Kalman f ilter) • Time series analysis via chaos theory methods• Modelling truncated/censored data • Nonlinear optimization with constraints

Thank you

CSIRO Mathematical & Information SciencesPavel Shevchenko

Phone: 02 9325 3218Email: [email protected]/Pavel.Shevchenko