brimming with potential we re-initiate coverage on …ir.irchartnexus.com/mrcb/docs/analysts/mrcb -...

TRANSCRIPT

Eq

uit

y |

Ma

lay

sia

Pro

pe

rty

Produced by KAF-Seagroatt & Campbell Securities Sdn Bhd Important disclosures can be found in the Disclosure Appendix

MRCB

Brimming with potential We re-initiate coverage on MRCB with a higher TP of RM1.60 (35% discount to

NAV). 2017 will be a lift-off year for MRCB, as the group moves from optimizing its

balance sheet to the execution of a strong pipeline of NAV-accretive deals.

Trading at a steep 48% discount to its NAV, the stock is also an excellent election-

theme play amid a rejuvenated orderbook and improving balance sheet strength.

Financial Highlights

FYE Dec (RM m) FY14 FY15 FY16F FY17F FY18F

Revenue 1,514.8 1,696.7 1,629.1 2,382.5 2,578.7 Normalised net profit 16.5 1.0 10.7 63.8 145.7 Normalised EPS (sen) 1.6 1.7 1.9 3.9 7.0 EPS growth (%) n/m 9.8 10.0 104.0 78.6 DPS (sen) 2.5 2.5 2.0 2.0 2.0 Net gearing (%) 152.6 127.2 72.7 121.1 115.1 PE (x) 98.4 78.8 67.0 32.8 18.4 ROE (%) 8.3 15.6 7.8 2.3 5.2 Yield (%) 1.6 1.8 1.6 1.6 1.6 PBV (x) 1.4 1.1 1.0 1.0 0.9

Source: Company, KAF

NAV kicker from value-accretive deals

Leveraging its early success with KL Sentral, MRCB is set to elevate itself as a premier transport-oriented developer (TOD) following several NAV-accretive landbanking deals in the Klang Valley and Penang with immediate development potential – i.e. Kwasa Sentral, KL Sports City, Cyber City Centre (CCC) and Penang Sentral. The emphasis is on railway accessibility and connectivity in urban areas and the city centre to drive inward migration and end-user demand. MRCB is also exploring the creation of property funds/strategic tie-ups with select government-backed or private institutional investors to part-fund its projects. This has already started with the entry of the EPF as an 80% stakeholder in Phase 1 of KL Sports City for RM421m (~28 acres), with MRCB holding the balance 20%.

Restoring its balance sheet health

As at 30 June 2016, MRCB’s net gearing stood at 109% (net debt: RM2.7b) vs 190% in FY12. After taking into account proceeds from the second tranche of its placement exercise (RM220m) and disposal of Menara Shell to 31%-owned MRCB Quill REIT (MQREIT MK, RM1.24, Buy) for RM640m, we project MRCB’s net gearing to come down to 73% by year-end (pro-forma target: 71%). Further out, we expect more asset monetization moves by MRCB to lift its balance sheet. Capital locked-up in its investment properties will be recycled into MQ REIT; Menara Celcom and Ascott Sentral may be the next in line. Likewise, MRCB is looking to sell EDL concessions (debts: RM1.1b or ~35% of MRCB’s total debts). Moving into FY17F, our net gearing ratio is projected to rise to 121% vs 73% for FY16F after assuming close to RM1b in funding commitments for a 70% stake each in Kwasa Sentral and CCC (Phase 1). However, if the sale of EDL and Menara Celcom materializes, this could bring down our net gearing again to 53% (pro-forma target: 45%).

Key overhang removed – new Bumiputera status opens more doors Having met the Bumiputera shareholding requirements (36%), MRCB has solidified its position as one of the largest Bumiputera-controlled public-listed entities with a sizeable orderbook (RM5.3b) and property landbank (GDV: RM50b). This will pave the way for MRCB to bid for more contracts under the Bumiputera category. Some RM36b representing 46% of the combined value of RM79b for 12 mega infrastructure projects have been earmarked for Bumiputera contractors (e.g. MRT 1 & 2, LRT 3, KL 118, WCE, BBCC, Asia Aerospace City). Its construction unit have been rejuvenated, with a newfound focus on higher-margin infrastructure jobs and, more importantly, fee-based contracts (~RM569m). After a quiet 1H, pre-sales momentum is picking up with the launch of the first block for Sentral Suites in KL Sentral.

15 September 2016

Analyst

Mak Hoy Ken

+60 3 2171 0508

Performance

1M 3M 12M

Absolute (%) (2) 21 20

Rel market (%) (1) 18 18

Source: Bloomberg

Market data

Bloomberg code CIMB MK MRC MK

No. of shares (m) 2,080.2

Market cap (RMm) 2,662.7

52-week high/low (RM) 1.48 / 1.03

Avg daily turnover (RMm) 3.5

KLCI (pts) 1,661.39

Source: Bloomberg

Buy

Price

RM1.28

Target price

RM1.60 (from RM1.56)

Valuation

Target price (RM) 1.60

Methodology NAV

Key assumptions

WACC for property (%) 9

WACC for EDL (%) 7

Discount to NAV (%) 35

Source: KAF

2

Table 1 : NAV calculation for MRCB (1 of 2)

Divisions/Operations Size Value (RM) Method % of NAV Effective

(acres) psf mil /share stake (%)

Landbank

Kota Kinabalu, Sabah 3 25 3.0 0.00 MV 100

Sub-total 3.0 0.00 0.1

Development properties

Senawang Sentral 6.4 0.00 NPV @ 9% 100.0

St.Regis Service Residences (Lot C) 0.0 0.00 NPV @ 9% 30.0

Q Sentral (Lot B) 3.1 0.00 NPV @ 9% 66.0

Sentral Residences (Lot D) 69.5 0.03 NPV @ 9% 51.0

Lot F - Office Towers 310.6 0.13 NPV @ 9% 100.0

9 Seputeh, Old Klang Road 178.8 0.08 NPV @ 9% 100.0

Suria Subang, Subang Jaya 37.5 0.02 NPV @ 9% 100.0

Selborn 2, Shah Alam 17.0 0.01 NPV @ 9% 100.0

Sentral Suites, Brickfields 152.5 0.06 NPV @ 9% 100.0

Semarak City, Setapak 262.2 0.11 NPV @ 9% 100.0

MRCB Putra, Putrajaya 31.7 0.01 NPV @ 9% 70.0

PJ Sentral Phase 1 223.9 0.09 NPV @ 9% 100.0

MX-1, KWASA Damansara, Sg.Buloh 589.3 0.25 NPV @ 9% 70.0

Rahman Putra, Sg.Buloh 47.3 0.02 NPV @ 9% 100.0

German Embassy land, Jln Kia Peng 114.5 0.05 NPV @ 9% 100.0

Cyberjaya City Centre Phase 1, Cyberjaya 361.0 0.15 NPV @ 9% 70.0

KL Sports City land swap 904.8 0.38 NPV @ 9% 85.0

Batu Ferringghi land 33.2 0.01 NPV @ 9% 100.0

Penang Sentral 293.1 0.12 NPV @ 9% 100.0

Pulai Land 129.9 0.05 NPV @ 9% 100.0

The Easton, Burwood 15.7 0.01 NPV @ 9% 100.0

Unbilled sales 105.0 0.04 NPV @ 9% 100.0

Sub-total 3,887.0 1.64 67.0

NLA/room

Value (RM)

Method

Effective

bays mil /share stake (%)

Investment properties

Menara Celcom (Lot 8), PJ Sentral 450,908 402.6 0.17 [email protected]% 100.0

Menara MRCB, Shah Alam 216,000 25.9 0.01 NPI@7% 100.0

Plaza Alam Sentral, Shah Alam 433,349 105.7 0.04 [email protected]% 100.0

Kompleks Sentral, Segambut Industrial Park 484,689 45.0 0.02 [email protected]% 100.0

Nu Tower 2, KL Sentral 498,309 52.3 0.02 NPI@6% 100.0

Ascott Sentral (Lot 348), KL Sentral 143 rooms 114.4 0.05 RM0.8mil/room 100.0

St. Regis Hotel (Lot C), KL Sentral 208 rooms 62.4 0.03 RM1mil/room 30.0

Sub-total 808.3 0.34 13.9

Cark parks

Plaza Alam Sentral, Shah Alam 1,400 bays 70.0 0.03 RM50k/bay 100.0

St. Regis Hotel (Lot C), KL Sentral 797 bays 12.0 0.01 RM50k/bay 30.0

Sub-total 82.0 0.03 1.4

Property management

Quill Capita Management (QCM) 87.1 0.04 NPI@7% 41.0

Sub-total 87.1 0.04 1.5

Expressways

Eastern Dispersal Link (EDL) 220.5 0.09 DCF @ 7% 100.0

Sub-total 220.5 0.09 3.8

Construction & Facilities Management

Construction 232.5 0.10 8x FY16F net profit

Facilities management 20.5 0.01 6x FY16F net profit

Sub-total 253.0 0.11 4.4

Source: Company, KAF

3

Re-initiating coverage on MRCB with a BUY

Breakdown of NAV model

We re-initiate coverage on MRCB with a BUY and a TP of RM1.60. We arrive at our TP after

ascribing a 35% discount to its NAV. Our NAV calculations for each of MRCB’s business

segments are based on the Sum-Of-Parts methodology (Table 1):

Property division: The division makes up a bulk of MRCB’s valuations, accounting for

RM1.64 or c.67% of group NAV. Except for its landbank in Sabah, we value its property

development projects via the NPV method at a discount rate of 9%.

Property investments: We value MRCB’s stable of property investments based on the Net

Property Income method at an average cap rate of 6.25% to 7%. This includes Menara

Celcom, which will be leased out to the Celcom group under a 21-year lease. This portfolio of

assets, combined, is the second-largest contributor to MRCB’s NAV at 14% (RM0.34). Other

recurring income, i.e. its 41%-associate Quill Capita Management (QCM) and MRCB-operated

car parks, contributes another RM169m (RM0.07).

Eastern Disposal Link (EDL): The highway in Johor is 100%-owned by MRCB. Based on a

concession period 34 years (until 2041) and a WACC of 7%, we value the EDL concession at

RM220m (net of ~RM1.1b in concession debts)

Construction & facilities management (RM249m): We apply a target PE of 8x on the

construction profits for FY17F, where construction earnings are set to gain traction next year

with the expected roll-out of a few key projects (e.g. LRT3, MRT2) as well as fee-based

contracts at the Kwasa Damansara township. For the facilities management units, our target

PE is pegged at 6x.

Disposal of Menara Shell: The sale of the Grade-A building to MQ REIT (MQREIT MK,

RM1.24, Buy) for RM640m should be completed by 4Q16. After netting off estimated project

debts of RM430m and assuming MRCB allocates up to RM152m in the REIT’s private

placement exercise (to part-fund the building’s purchase), we expect MRCB to take-back net

proceeds of RM58m.

Table 1 : NAV calculation for MRCB (2 of 2)

Divisions/Operations Size Value (RM) Method % of NAV Effective

(acres) psf mil /share stake (%)

Listed-investments

MRCB-Quill REIT* 257.8 0.11 Market Value 32.9

Sub-total 257.8 0.11 4.7

Disposal of assets

Menara Shell* 58.0 0.02 Acquisition value (less est.debt) 100.0

Sub-total 58.0 0.02 1.0

Others

171.4

0.07

Book value

3.0

Gross NAV

5,842.2 2.46

Net debt* (1,385.4) (0.58) As at 31 December 2015 (24.2)

Proceeds from ESOS/warrant conversions 1,343.4 0.57 Warrants exercise price: RM2.30 23.4

Total NAV 5,800.2 2.44 100.0

FD no of shares 2,376.7

NAV/share 2.44

Fair Value (less: 30% discount) 1.60

Capital gain (%) 24.7

Yield (%) 1.6

Total Return (%) 27.9

Discount to RNAV (%) (47.6)

* (i) Less EDL & Menara Shell debt.

(ii) Assumes MRCB takes up its portion of MQ REIT’s private

placement (RM152m).

Source: Company, KAF

4

MQ REIT: Post MQREIT’s placement exercise, MRCB’s stake in the REIT will rise from 31%

to 33%. At today’s market prices, this will translate into RM272m (5% of NAV).

We have also incorporated an additional 263m shares arising from MRCB's share placement

exercise into our fully-diluted (FD) share base calculations (more details in the later sections).

De-leveraging efforts bearing fruits

Clearing the slack

Under the stewardship of the entrepreneurial management team from Gapurna, MRCB has

stepped up efforts to optimise its corporate structure, balance sheet and growth trajectory.

Following the emergence of the Gapurna group as its major shareholder, MRCB has been quietly

undergoing an internal reorganisation of its operations and processes (Table 2):

Disposal of non-core assets: One of the first things the new management team did when it

first came on board in March 2013 was to streamline its corporate structure. Non-core

businesses/units that were not in sync with its future direction were divested. This started with

the sale of its IT businesses for RM45m (January 2014). Other notable disposals were the

divestment of its:

- 30% associate stake in the DUKE highway concession in March 2015 (RM220m);

- 51% stake in Nu Sentral Mall in October 2015 (RM120m); and

- 100% stake in Sooka Sentral in June 2016 (RM91m)

Entry into MQ REIT: MRCB first surfaced as a substantial shareholder of MRCB-Quill REIT

last March following the disposal of Platinum Mall for RM640m in return for RM476m in cash

and a controlling 31% stake in the REIT.

Exiting non-core construction segments: Apart from the sale of the DUKE concession for

which MRCB was not the controlling shareholder, the group has also exited from two JV ventures

which appears to run against its future plans for the construction division: i.e. its entire (i) 40%

stake in the Ekovest-MRCB JV (the PDP for the Klang Valley River of Life project); and (ii) equity

interest in the Klang Valley Double Tracking JV (via a share swap agreement with DMIA Sdn

Bhd).

Table 2 : Disposal of non-core assets

Details Date Business unit Proceeds Net Gain/Loss

(RM m) (RM m)

Disposal of 100%-owned GTC Global Sdn Bhd Jan-14 IT 45.0 0.0

Disposal of 30% stake in DUKE concession Jun-14 Toll concession 228.0 94.9

Disposal of 100% stake in MRCB Technologies Sdn Bhd Oct-14 IT 7.8 0.2

Transfer of 100% interest in KV double tracking JV in exc for bal 30% stake in Sentral Suites land

Mar-15 Construction/Property development

0.0 0.0

Disposal of 70% stake in Salak South JV Jun-15 Property development 39.0 38.8

Disposal of 51% stake in Nu Sentral Mall Oct-15 Property investment 119.8 70.1

Disposal of entire 40% stake in Ekovest-MRCB JV Apr-16 Construction 8.5 2.8

Disposal of 100% stake in Sooka Sentral May-16 Property investment 90.8 41.6

Total 538.9 248.4

Source: Company, KAF

5

The MQ REIT factor

MQREIT provides MRCB with a perfect vehicle to unlock the deep-embedded value of its prime

commercial assets, particularly within its flagship KL Sentral project. This paves the way for

MRCB to redeploy its capital towards funding higher-ROE development projects.

We understand that the sale of Menara Shell to MQREIT should be consummated by 4Q16.

Located in KL Sentral, Menara Shell has an estimated Net Lettable Area (NLA) of 557,053sf. It

comprises of a 33-storey office building that is built atop a five-storey podium and four-storey

basement car park. The Grade-A building is fully-tenanted, and recorded total rental plus car park

income of RM46m in FY15.

MQREIT is expected to be fund the purchase via placements and borrowings, with a ratio of

roughly 65:35. Based on an earlier announcement, MRCB will commit up to RM152m and take up

about 36% of the placement shares, while EPF has expressed interest to take up another 7%.

After the placement exercise, we expect MRCB’s stake in MQREIT to rise from 31% to 33% (see

Table 3).

MRCB’s current portfolio of property investments includes Menara MRCB, Plaza Alam Sentral,

Kompleks Sentral, Menara Shell and Ascott Sentral, as well as a 30% stake in St.Regis Hotel @

KL Sentral. In addition, the group has also signed a long-term lease with the Celcom group, which

will occupy a tower block at PJ Sentral Phase 1 (Menara Celcom). We expect the tower block to

be ready by next year, with rentals kicking in from the second half of next year.

Management guided that Menara Celcom in PJ Sentral may be next to be injected into MQREIT,

followed by Ascott Sentral for a combined RM548m (our estimates: RM517m). The former has

already been pre-leased to the Celcom-Axiata Group under a 21-year lease reportedly worth over

RM300m.

With the purchase of Menara Shell from MRCB, MQREIT’s asset size will expand from RM1.6b to

RM2.3b. This, in turn, will lift the fee-income base of Quill Capita Management (QCM) – which

manages the assets under MQ REIT. MRCB owns a 41% stake in QCM. Based on the current

asset size of RM1.6b for MQ REIT, we estimate MRCB’s share of QCM’s fee-income to be

~RM5m p.a.

Table 3 : MRCB’s stake in MQ REIT to increase post-disposal of Menara Shell

MQ REIT's pro-forma funding mix for Menara Shell purchase

Placement at indicative price of RM1.05 427.0

Debts 229.0

Total 656.0

Debt/Equity mix 65:35

MQ REIT's total outlay for Menara Shell purchase (RM m)

Purchase consideration 640.0

Estimated expenses* 16.0

Total 656.0

Breakdown of estimated expenses for MQ REIT's Menara Shell acquisition (RM m)

Professional fees, placement fees, fees payable to relevant authorities, cost of convening 9.6

the Unitholders' meeting and other incidental expenses

Acquisition fee of 1% of the purchase consideration due to the manager 6.4

Total 16.0

Estimated total placement shares for MQ REIT (m shares) 406.7

Indicative issue price (RM) 1.05

Total proceeds from placement (RM m) 427.0

MRCB's maximum allocation for MQ REIT placement shares (RM m) 152.0

MRCB's estimated share of placement shares - m 144.8

- % 35.6

MQ REIT's share capital (m) - current 661.4

- enlarged (after placement) 1,068.0

MRCB's stake in MQ REIT (m) - current 206.3

MRCB's stake in MQ REIT - post-placement 351.0

MRCB's stake in MQ REIT (%) - current 31.2

MRCB's stake in MQ REIT - post-placement 32.9

Source: Company, MRCB

6

Balance sheet kickers coming through

As at 30 June 2016, MRCB’s net gearing stood at 109% on a net debt of RM2.7b. This is a

marked improvement from 190% in FY12. Along with its asset divestment programs, MRCB has

been gradually paring down its project debts upon the completion of its commercial projects - the

latest being the full repayment of the balance RM250m term loan that was taken for the

construction of Nu Tower offices.

With the execution of the (i) second tranche of the private placement exercise (RM220m); and (ii)

sale of Menara Shell (RM58m – net of project debts of RM430m and assuming MRCB commits

RM152m for MQ REIT’s private placement), we project MRCB’s net gearing to come down to 73%

vs the pro-forma target of 71% by the end of this year.

More is to come. After Menara Shell, several catalytic newflows to lift its balance sheet may

emerge in the coming months, we believe. As highlighted earlier, the divestment of Menara

Celcom and Ascott Sentral could follow suit along with the sale of EDL, which has concession

debts of RM1.1b (~35% of MRCB’s total debts).

Moving into FY17F, our net gearing ratio is projected to rise to 121% vs an estimated 73% for

FY16F after assuming close to RM1b in funding commitments for a 70% stake each in Kwasa

Sentral and Cyberjaya City Centre (CCC) Phase 1. But, we are unmoved. If the sale of EDL and

Menara Celcom materialises, this could bring down our net gearing again to 53% (pro-forma

target: 45%).

Rebuilding its construction portfolio

Leaner outfit – with an increasing focus on fee-based income

MRCB's management have taken constructive measures to stabilise its construction division; a

key earnings drag over the last few years. Building contracts that are both generic and labour

intensive have been de-emphasised. Open tenders will be carried out, even for its own projects.

Following this, MRCB has transformed its construction division into a leaner outfit with a newfound

focus on higher-margin infrastructure and, more importantly, fee-based income. This started with

the MRCB-George Kent JV’s appointment as the Project Delivery Partner (PDP) for the LRT 3

project, and subsequently, the Kwasa Utama C8 and Kwasa Land PDP (Infrastructure) projects

under the Kwasa Damansara integrated development in Sg.Buloh.

Much like its restructuring efforts, there are already early signs of a turnaround in the construction

division. After incurring normalised losses of RM52m-RM72m in FY12-13, the construction

division returned to the black in FY14-15 with profits of RM23m-RM52m. While FY16F profits will

likely be lower again, the dip would likely be temporary, and is mainly due to the completion of

certain legacy projects at lower margins (e.g. Ampang LRT 3 extension works).

Off a cleaner slate, we expect its construction earnings to resume their upward trajectory in FY17-

FY18F with projected profits of RM41m and RM93m, respectively. Likewise, we do not expect any

major provisions in the coming quarters.

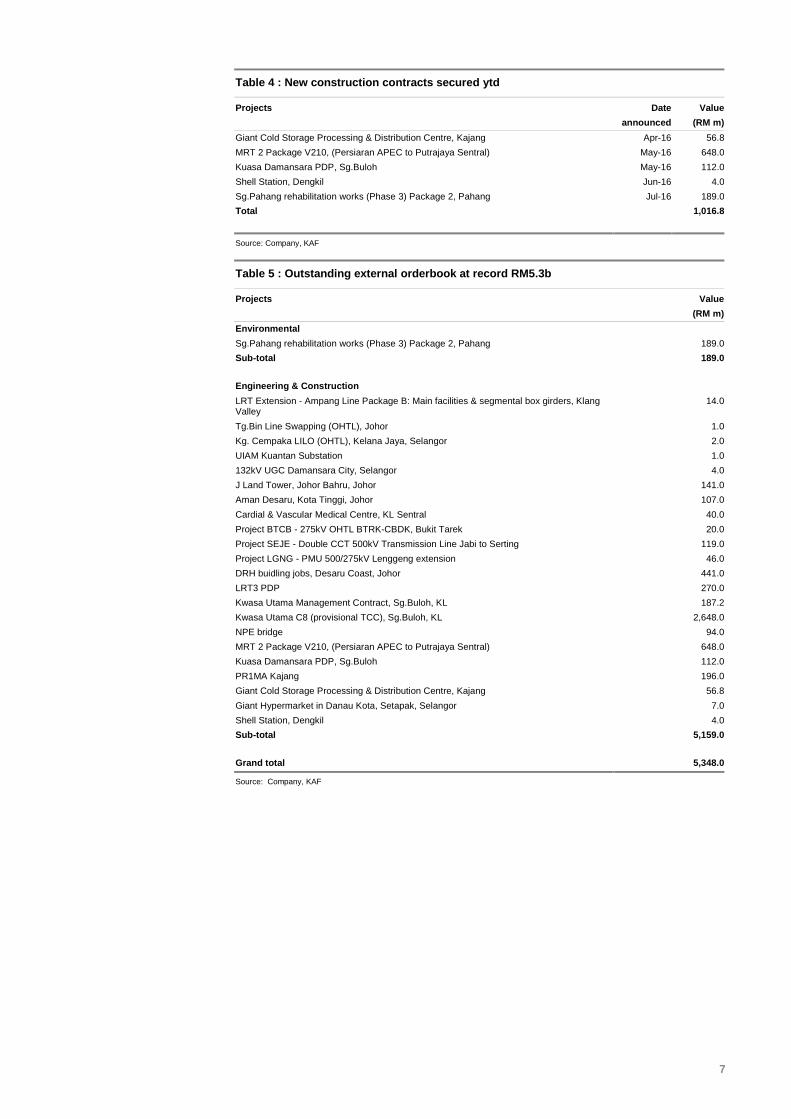

Orderbook at a record RM5.3b

Continuing its strong momentum in FY15, MRCB has secured ~RM1b worth of new projects ytd.

This brings its outstanding orderbook to a record RM5.3b, including RM569m worth of fee-based

contracts. By extension, it will provide MRCB with strong earnings visibility at least until 2027

(orderbook cover: close to 7x its FY15 construction revenue).

Further out, we expect MRCB to be at the forefront of more infrastructure bids under the 11th

Malaysia Plan (11MP). The group’s prospects will be further boosted by the group’s new status as

a Bumiputera-controlled publicly listed-entity (more in the next sections).

There could also be more recurring income coming its way; MRCB is tipped for the role as project

manager for the CCC development when it takes off. Based on the terms of the JV agreement,

MRCB will be due fees amounting to 4% of the project’s total construction cost (Table 4 & 5).

7

Table 4 : New construction contracts secured ytd

Projects Date Value

announced (RM m)

Giant Cold Storage Processing & Distribution Centre, Kajang Apr-16 56.8

MRT 2 Package V210, (Persiaran APEC to Putrajaya Sentral) May-16 648.0

Kuasa Damansara PDP, Sg.Buloh May-16 112.0

Shell Station, Dengkil Jun-16 4.0

Sg.Pahang rehabilitation works (Phase 3) Package 2, Pahang Jul-16 189.0

Total

1,016.8

Source: Company, KAF

Table 5 : Outstanding external orderbook at record RM5.3b

Projects Value

(RM m)

Environmental

Sg.Pahang rehabilitation works (Phase 3) Package 2, Pahang 189.0

Sub-total 189.0

Engineering & Construction

LRT Extension - Ampang Line Package B: Main facilities & segmental box girders, Klang Valley

14.0

Tg.Bin Line Swapping (OHTL), Johor 1.0

Kg. Cempaka LILO (OHTL), Kelana Jaya, Selangor 2.0

UIAM Kuantan Substation 1.0

132kV UGC Damansara City, Selangor 4.0

J Land Tower, Johor Bahru, Johor 141.0

Aman Desaru, Kota Tinggi, Johor 107.0

Cardial & Vascular Medical Centre, KL Sentral 40.0

Project BTCB - 275kV OHTL BTRK-CBDK, Bukit Tarek 20.0

Project SEJE - Double CCT 500kV Transmission Line Jabi to Serting 119.0

Project LGNG - PMU 500/275kV Lenggeng extension 46.0

DRH buidling jobs, Desaru Coast, Johor 441.0

LRT3 PDP 270.0

Kwasa Utama Management Contract, Sg.Buloh, KL 187.2

Kwasa Utama C8 (provisional TCC), Sg.Buloh, KL 2,648.0

NPE bridge 94.0

MRT 2 Package V210, (Persiaran APEC to Putrajaya Sentral) 648.0

Kuasa Damansara PDP, Sg.Buloh 112.0

PR1MA Kajang 196.0

Giant Cold Storage Processing & Distribution Centre, Kajang 56.8

Giant Hypermarket in Danau Kota, Setapak, Selangor 7.0

Shell Station, Dengkil 4.0

Sub-total

5,159.0

Grand total 5,348.0

Source: Company, KAF

8

Plugging the management gap

Apart from being more selective with its new bids, MRCB has moved quickly to fill the leadership

vacuum for its construction division, which was a major drag for the past few years.

At the same time, the MRCB-George Kent PDP (the JV vehicle for the LRT3 project) has been on

an aggressive recruitment drive ahead of the project's rollout next year. Among others, it has

headhunted Mr. Ong Gim Lip as Project Director for the JV. Ong has over 34 years’ experience in

handling various LRT/MRT projects, including a stint as head of the Singapore Land Transport

Authority’s (LTA) Strategic Land Transportation Model. His last port of call was as Project Director

for the MRT 1 Package V4 under Sunway Construction.

In terms of headcount, the JV is actively tapping into the local as well foreign talent pool to boost

its staff strength to 400 from ~160 currently (Chart 1).

Morphing into a Bumiputera-controlled powerhouse

Meets 35% Bumi threshold

Earlier this month, MRCB completed the second tranche of its private placement, where the group

placed out 194m shares to Bank Rakyat at RM1.15 and raised RM220m. This followed an earlier

tranche (100m shares @ RM1.09) that was placed out in April. To recap, MRCB had in November

proposed a private placement of up to 494m new shares or 20% of its enlarged share capital.

The main rationale of this exercise is to lift MRCB's Bumiputera shareholding to maintain its status

as a Bumiputera-controlled public listed entity.

With the completion of the second tranche, MRCB has successfully placed out a total 294m new

shares (~60% of the maximum placement shares), thereby raising its Bumiputera shareholding

from 28% as at end November 2015 to 36%. This is more than sufficient to meet the minimum

threshold of 35% as required by the authorities.

More importantly, it removes a key overhang for the stock going forward. As for the remaining

40% placement shares, management is in no hurry to do so; it will only decide after taking into

account its capital requirements going forward.

Chart 1 : LRT 3 project alignment (Bandar Utama to Klang)

Source: Prasarana, KAF

9

Opens up new opportunities

Having amassed an outstanding construction overbook of RM5.3b and 410-acre urban landbank

(estimated GDV: ~RM50b), MRCB has firmly established itself as one of the largest Bumiputera-

controlled contractors and property developers in Malaysia. Further out, its newly minted status

will help unlock more opportunities to tender projects or landbank that have specific Bumiputera

categories.

Under the Bumiputera Economic Empowerment Report Card 2015, some RM36b or ~46% out of

12 mega infrastructure projects worth a combined RM79b have been earmarked for Bumiputera

contractors under the Carve-out and Compete Program helmed by Unit Peneraju Agenda

Bumiputera (Teraju).

They are the MRT Lines 1 & 2, KL 118 Tower, West Coast Expressway (WCE), Bukit Bintang City

Centre (BBCC), Asia Aerospace City and the Sg.Besi Ulu Kelang Expressway (SUKE).

Other operational updates

Pre-sales momentum to pick-up in 2H16

After a lacklustre 1H, we expect MRCB’s pre-sales momentum to accelerate in the second half of

this year with the debut of Sentral Suites. With an indicative GDV of RM1.5b, Sentral Suites

comprises of three 43-storey towers that offers a total of 1,424 apartments and 41 retail units.

We expect the development to be well-received, as it represents the last residential component for

MRCB’s flagship KL Sentral project. And the initial signs are positive. The first tower (458 units),

which will be launched in 4Q16 (indicative pricing: RM1,100psf before discount), has already

generated 2,000 registrants. With this, management is confident of achieving a take-up rate of

80% within six months of its launch (Chart 2).

Apart from Sentral Suites, MRCB is set to launch the Kalista series at its Bukit Rahman Putra

project in Sg.Buloh soon. Kalista offers only 46 freehold units, i.e. 18 units of semi-detached

(40’x85’) and 28 units of super-link (24’x80’) homes.

For next year, MRCB will debut of Parcel D at its flagship 9 Seputeh project next year. The

existing Parcel C has already achieved an overall take-up rate of 82%.

EDL up for sale

During our recent meeting with MRCB, we understand that the group is actively seeking potential

suitors to dispose its toll road in Johor. Just last month, the local press reported that the UEM

Group may be interested in acquiring EDL if the price is right. Recall that back in November 2011,

Plus Malaysia Bhd, an SPV formed by UEM and EPF (51:49), completed the privatization of

PLUS Expressways Bhd for RM23b.

Chart 2 : Location of Sentral Suites within KL Sentral

Source: Company, KAF

10

The 8.1km-long EDL is an elevated highway that connects PLUS’ North-South Expressway to the

Sultan Iskandar Customers, Immigration & Quarantine Complex (CIQ) in JB city centre. It is also a

mere 10 minutes away from the JB-Singapore causeway via the Pandan Interchange.

Via 100%-owned MRCB Lingkaran Selatan Sdn Bhd, EDL has a 30-year concession period that

began in April 2012, and ends in March 2042. The highway was built at a cost of ~RM1.3bil

(including land acquisition). MRCB started collecting toll fares in August 2014 after the Malaysian

Government decided against purchasing the highway. Since then, we gather that the average

daily traffic for the EDL is still somewhat flattish, hovering around ~43k-44k trips.

In any case, continued uncertainties over Malaysia’s plans to implement the Vehicle Entry Permit

(VEP) system on all-foreign registered cars entering Johor does not bode well for EDL’s traffic, in

our view. In June, the Malaysian side conducted a test run on the VEP system although drivers

were not charged the RM20 fee.

Prior to this, the Singapore government had in August 2014 raised the VEP charges for foreign-

registered cars by S$15 to S$35 per day. During the same month, the toll charges from Singapore

into Johor were raised from RM2.90 to RM9.70. An additional charge of RM6.80 was also

imposed for users that are leaving Johor (previously: free).

Stacking it up, a removal of EDL from its balance sheet will be positive for MRCB, in our view.

Apart from reducing ~RM1.1b in concession debts, it will help free up management’s time for

other productive areas, and plug the associated earnings leakages (Chart 3).

Chart 3 : Eastern Dispersal Highway, Johor

Source: Company, KAF

11

Embracing technology

Property arm MRCB Land has been making great strides in utilizing technology as a tool to ramp

up its sales pitches. We believe this will help augment its status as a leading developer of transit-

oriented projects within prime urban locations.

(1) Building smarter properties: The local press reported recently that MRCB is teaming up

with Telekom Malaysia (T MK, RM6.88, Hold) to explore opportunities with integrated

telecommunications, ICT and the Internet of Things (IoT)-smart services. These initiatives are

to be implemented within MRCB’s property development projects. By working with TM,

MRCB aims to promote ‘Smart City living’ at its various developments – with ICT

infrastructure as a backbone for systems to respond to challenges, and enhance efficiency. It

aims to offer a whole suit of smart solutions that ranges from smart safety & security, smart

mobility and smart building management to tenant/citizen services.

(2) Going digital: MRCB has tied-up with PropertyGuru, Asia’s leading property portal, to create

an exclusive online platform to market the Sentral Suites project. As part of the deal,

PropertyGuru will develop a customized marketing and branding plan that is tailor-made for

Sentral Suites. MRCB’s investments, the largest digital marketing and branding spend to-

date in Malaysia at RM4m, will target prospective home buyers who utilize digital mediums in

their search for properties. This online strategy corroborates the findings of a survey by

PropertyGuru and Google, which found that ~90% of property buyers have used the online

space to search or research for properties (Chart 4).

Valuation and recommendation

1H16 results review

MRCB’s normalised 1H16 earnings of RM5m was 86% lower YoY against a 12% drop in billings.

The lower earnings were largely attributable to three key reasons (Table 6):

(i) Lower margins from legacy jobs (e.g. LRT extension) vs no contributions from the

environmental & transmission line projects (1H15: RM25m);

(ii) Slower progress billings on select projects (eg. 9 Seputeh Parcel C & PJ Sentral) vs the near-

completion of Q-Sentral; and

(iii) The continued drag from EDL (losses of c.RM15m in 1H16).

Earnings on the mend in FY17F-18F

While we do not envisage 2H16 to show marked improvements, we expect FY17F-18F to chart a

stronger recovery with projected earnings of RM64m-RM146m against an estimated RM11m for

FY16F.

Chart 4 : MRCB ties up with PropertyGuru under a digital campaign for Sentral Suites

Source: PropertyGuru

12

The basis for our optimism stems from:

Maiden contributions from the LRT3 PDP project, whereby construction works are scheduled

to commence next year.

Likewise, we expect the other fee-based contracts, i.e. Kwasa Utama C8 and Kwasa Land

PDP, together with the Kwasa Utama construction package, to kick-off once Kwasa Land

receives all the necessary approvals.

Work progress for select property projects, i.e. PJ Sentral Phase 1, 9 Seputeh Parcel C and

MRCB Putra, begins to move beyond the foundation stage.

Recognition from the en-Bloc disposal of the MRCB Putra office development in Putrajaya.

There is yet more earnings upside coming from other potential contracts (not in our forecast):

We have conservatively excluded MRCB's likely appointment as the management contractor

for Phase 1 of the CCC development for now, pending the formalization of a JV structure.

Phase 2 of CCC.

PJ Sentral Phase 2; where MRCB has the first right of refusal to purchase the land.

Disposal of Ascott Sentral and Menara Celcom; management has pegged a combined value

of RM548m for both assets (our estimates: RM517m).

13

Table 6 : Quarterly results

YE 31 Dec (RM m) 1H15 1H16 % YoY 1Q16 2Q16 % QoQ

Turnover 934.5 825.2 (11.7) 436.0 389.2 (10.7)

EBIT 152.1 125.1 (17.8) 66.5 58.6 (11.9)

Interest Expense (89.6) (91.1) (49.6) (41.5)

Interest Income 22.3 4.6 2.4 2.2

Pre-Exceptionals Profit 84.8 38.6 19.2 19.3

Exceptionals 259.3 44.4 0.0 44.4

Pre-Associates/JV Profit 344.1 83.0 19.2 63.7

Associates/JVs 0.3 9.4 (0.6) 10.0

Pretax Profit 344.4 92.4 (73.2) 18.7 73.8 295.4

Taxation (25.6) (21.9) (5.2) (16.7)

Minority Interest/disct. ops (20.9) (20.6) (9.1) (11.6)

Net Profit 298.0 49.9 (83.3) 4.4 45.5 n/m

Normalised Net Profit 38.7 5.5 (85.8) 4.4 1.1 (74.8)

Normalised EPS (sen)

2.2

0.3

0.2

0.1

Gross DPS (sen) 0.0 0.0 0.0 0.0

BV/share (RM)

1.29 1.28 1.27 1.28

EBIT Margin (%) 16.3 15.2 15.3 15.0

Pretax Margin (%) 36.9 11.2 4.3 19.0

Effective Tax (%) 7.4 23.7 27.8 22.6

Segmental Breakdown (RM m)

Turnover Construction 361.2 332.6 (7.9) 152.8 179.7 17.6

Property development & investment 477.7 376.8 (21.1) 229.1 147.7 (35.5)

Infrastructure & environmental 57.6 57.2 (0.6) 28.1 29.1 3.3

Facilities management & parking 36.3 37.2 2.5 18.0 19.2 7.0

Investment holding & Others 1.8 21.5 1,127.1 8.0 13.5 67.5

Total 934.5 825.2 (11.7) 436.0 389.2 (10.7)

EBIT

Construction 29.7 3.0 n/m 67.3 90.4 n/m

Property development & investment 93.4 157.8 (96.8) 1.1 1.8 61.1

Infrastructure & environmental 31.9 32.7 2.4 13.1 19.5 48.7

Facilities management & parking 2.6 12.0 363.4 7.4 4.6 (37.7)

Investment holding & Others (5.4) (77.4) n/m (22.5) (54.9) n/m

Total 152.1 125.1 n/m 66.5 58.6 n/m

EBIT margin (%)

Construction 8.2 0.9 44.1 50.3

Property development & investment 19.6 41.9 0.5 1.2

Infrastructure & environmental 55.4 57.1 46.7 67.2

Facilities management & parking 7.2 32.3 41.2 24.0

Investment holding & Others n/m n/m n/m n/m

Total 16.3 15.2 15.3 15.0

Source: Bursa Malaysia, KAF

14

Chart 5: PE BAND

Source: Bloomberg, KAF

Chart 6: PBV BAND

Source: Bloomberg, KAF

15

Income Statement

FYE Dec (RM m) FY14 FY15 FY16F FY17F FY18F

Revenue 1,514.8 1,696.7 1,629.1 2,382.5 2,578.7

EBITDA 294.0 242.5 366.9 386.1 518.1

Depreciation/Amortisation (52.4) (64.2) (90.9) (110.4) (112.7)

Operating income (EBIT) 241.6 178.3 276.0 275.7 405.4

Other income & associates (24.3) 7.9 18.3 40.8 60.8

Net interest expense (132.8) (145.5) (160.5) (193.3) (214.4)

Exceptional items 136.1 329.4 183.4 0.0 0.0

Pretax profit 220.6 370.1 317.1 123.3 251.8

Taxation (53.3) (6.1) (87.5) (42.6) (77.4)

Minorities/pref dividends (14.7) (33.6) (35.5) (16.8) (28.8)

Net profit 152.6 330.4 194.1 63.8 145.7

Normalised net profit 16.5 1.0 10.7 63.8 145.7

Source: Company, KAF

Cash flow Statement

FYE Dec (RM m) FY14 FY15 FY16F FY17F FY18F

Pre-tax profit 220.6 370.1 317.1 123.3 251.8

Depreciation/amortization 52.4 64.2 90.9 110.4 112.7

Net change in working capital (725.2) 606.2 (161.7) (89.4) 131.8

Others 332.0 (900.1) (105.8) (83.4) (138.1)

Cash flow from operations (120.2) 140.4 140.5 60.8 358.2

Capital expenditure (168.5) (943.6) (70.0) (1,370.0) (270.0)

Net investments & sale of fixed assets 228.1 4.2 519.3 0.0 0.0

Others 4.4 530.1 8.5 0.0 0.0

Cash flow from investing 64.0 (409.3) 457.8 (1,370.0) (270.0)

Debt raised/(repaid) (160.2) 0.9 (458.3) 1,000.3 20.3

Equity raised/(repaid) 0.1 0.8 328.5 0.0 0.0

Dividends paid (17.6) (82.4) (44.7) (41.6) (41.6)

Others 233.5 380.7 0.0 0.0 0.0

Cash flow from financing 55.9 299.9 (174.4) 958.6 (21.4)

Net cash flow (0.3) 31.0 424.0 (350.6) 66.8

Net cash/(debt) b/f 308.5 308.2 339.2 763.2 412.6

Exchange rate effects 0.0 0.0 0.0 0.0 0.0

Net cash/(debt) c/f 308.2 339.2 763.2 412.6 479.4

Source: Company, KAF

16

Balance Sheet

FYE Dec (RM m) FY14 FY15 FY16F FY17F FY18F

Fixed assets 83,045 90,300 95,368 99,720 103,561

Intangible assets 271.8 317.1 310.3 303.6 296.9

Other long-term assets 2,039.9 2,531.0 2,064.6 3,451.8 3,757.9

Total non-current assets 3,777.5 4,395.5 3,865.1 5,165.5 5,383.6

Cash & equivalent 660.7 521.5 945.5 594.9 661.7

Stock 42.6 63.1 45.6 72.2 74.5

Trade debtors 1,319.8 1,113.8 1,160.5 1,631.8 1,554.3

Other current assets 1,241.2 995.8 1,055.0 1,325.5 1,351.8

Total current assets 3,264.4 2,694.3 3,206.6 3,624.4 3,642.3

Trade creditors 1,121.5 1,199.3 1,126.0 1,805.0 1,887.9

Short-term borrowings 1,390.6 1,049.5 544.1 794.1 809.2

Other current liabilities 58.4 47.7 47.7 47.7 47.7

Total current liabilities 2,570.5 2,296.5 1,717.8 2,646.8 2,744.8

Long-term borrowings 2,300.1 2,345.9 2,393.0 3,143.2 3,148.4

Other long-term liabilities 106.8 134.6 134.6 134.6 134.6

Total long-term liabilities 2,406.9 2,480.5 2,527.6 3,277.8 3,283.0

Shareholders' funds 1,985.3 2,260.1 2,738.1 2,760.3 2,864.4

Minority interest 79.3 52.6 88.1 105.0 133.7

Source: Company, KAF

17

Appendix – MRCB’s ongoing and future TOD projects

KL Sentral, Klang Valley

Source: Company, KAF

PJ Sentral, Petaling Jaya

Source: Company, KAF

18

Penang Sentral, Butterworth

Source: Company, KAF

Kwasa Sentral, Sg.Buloh

Source: Company, KAF

19

Cyberjaya City Centre, Cyberjaya

Source: Company, KAF

KL Sports City, Bukit Jalil

Source: Company, KAF

Disclosure Appendix

Recommendation structure Absolute performance, long term (fundamental) recommendation: The recommendation is based on implied upside/downside for the stock from the target price and only reflects capital appreciation. A Buy/Sell implies upside/downside of 10% or more and a Hold less than 10%.

Performance parameters and horizon: Given the volatility of share prices and our pre-disposition not to change recommendations frequently, these performance parameters should be interpreted flexibly. Performance in this context only reflects capital appreciation and the horizon is 12 months.

Market or sector view: This view is the responsibility of the strategy team and a relative call on the performance of the market/sector relative to the region. Overweight/Underweight implies upside/downside of 10% or more and Neutral implies less than 10% upside/downside.

Target price: The target price is the level the stock should currently trade at if the market were to accept the analyst's view of the stock and if the necessary catalysts were in place to effect this change in perception within the performance horizon. In this way, therefore, the target price abstracts from the need to take a view on the market or sector. If it is felt that the catalysts are not fully in place to effect a re-rating of the stock to its warranted value, the target price will differ from 'fair' value.

Disclaimer This report has been prepared solely for the information of clients of KAF Group of companies. It is meant for private circulation only, and shall not be reproduced, distributed or published either in part or otherwise without the prior written consent of KAF-Seagroatt & Campbell Securities Sdn Bhd.

The information and opinions contained in this report have been compiled and arrived at based on information obtained from sources believed to be reliable and made in good faith. Such information has not been independently verified and no guarantee, representation or warranty, express or implied, is made by KAF-Seagroatt & Campbell Securities Sdn Bhd as to the accuracy, completeness or correctness of such information and opinion.

Any recommendations referred to herein may involve significant risk and may not be suitable for all investors, who are expected to make their own investment decisions at their own risk. Descriptions of any company or companies or their securities are not intended to be complete and this report is not, and should not, be construed as an offer, or a solicitation of an offer, to buy or sell any securities or any other financial instruments. KAF-Seagroatt & Campbell Securities Sdn Bhd, their Directors, Representatives or Officers may have positions or an interest in any of the securities or any other financial instruments mentioned in this report. All opinions are solely of the author, and subject to change without notice.

Dato' Ahmad Bin Kadis Managing Director KAF-Seagroatt & Campbell Securities Sdn Bhd (134631-U)