brock university pension plan · since your personal financial planning extends beyond the brock...

TRANSCRIPT

Brock University Pension Plan

Contents

Part 1: Your future is worth the investment 3

For more information 3

Part 2: Welcome to the pension plan 4

A “hybrid plan” 4

Morethanaretirementbenefit 4

Whopaysforthebenefits 4

Howtofindoutmoreaboutyourownsituation 5

Frequentlyaskedquestions 5

Part 3: Joining the plan 5

Permanentfull-timeemployees 5

Otherpermanentemployees,12-monthtermfull-timeemployeesandlimitedtermfacultyemployees 5

Otheremployees 5

Frequentlyaskedquestions 6

Part 4: Building your pension 7

MoneyPurchaseAccount 7

ShortTermAccounts 8

MinimumGuaranteeFund 8

Additionalvoluntarycontributions 9

Specialtransfersfromotherregisteredpensionplans 9

Onetrustfund 10

Contributionsunderspecialcircumstances 10

Maximumcontributions 11

Frequentlyaskedquestions 11

Part 5: Calculating your pension 12

How the plan works 12

MoneyPurchasePension 13

MinimumGuaranteedPension 13

Frequentlyaskedquestions 15

Part 6: Leaving the University before age 55 16

Additionalvoluntarycontributions 16

Specialtransfersfromotherregisteredpensionplans 16

Frequentlyaskedquestions 17

1

Booklet updated March 2016

2

Part 7: Leaving the University at age 55 or older 18

Activeplanmembers 18

Deferredplanmembers 19

Makingyourdecision 20

Ifyouchoosetoremainintheplan 20

Additionalvoluntarycontributions 20

Special transfers from other registered pension plans 21

Postponed retirement 21

Forms of pension payments 21

Annualadjustmentstoyourpension 24

Pensionamountsbasedonadditionalvoluntarycontributionsorspecialtransfers 25

Maximumpensionamount 25

Noticeofretirement 25

Receivingyourpensionpayments 26

Frequentlyaskedquestions 26

Part 8: Providing for your survivors 28

Deathbeforepensioncommencement 28

Deathafterpensioncommencement 28

Part 9: Taking care of administrative issues 29

Annualpensionstatements 29

Governance 29

Planassets 29

Frequentlyaskedquestions 30

Part 10: Other sources of retirement income 31

Canada Pension Plan 31

OldAgeSecurity 31

Personal savings 32

Frequentlyaskedquestions 32

Part 11: Covering all the bases 33

Frequentlyaskedquestions 34

Part 12: Glossary 35

3

Mostfinancialexpertswilltellyouthatthe“secret”toafinanciallysecure retirementistoplanandsaveaccordingtothatplan.Yourretirementmaylast longerandcostmorethanyouthink.Youcouldspendathirdormoreofyourlife inretirement.Themoreyousavenow,thebetterpreparedyouwillbeforthepleasuresandunexpectedchallengesthatsometimescomewithretirement.

Ifyoursavingsaresufficient,youshouldbeabletomaintainastandardoflivingafterretiringthatiscomparabletowhatyouenjoyedwhileworking.Yourmonthlypension from the University — as well as from any other employers, if applicable — whencombinedwithyourownsavingsandgovernmentpensionbenefits,will helpyoureachyourretirementgoals.

WeencourageyoutotakethetimetolearnabouttheBrockUniversityPension Plan—yourfutureisworththeinvestment!

Youcanfindoutwhattheplanprovides,whenandhow,byreadingthisbooklet. Youwillfindanswerstosomeofthequestionsthatotherplanmembersfrequentlyaskabouttheplanthroughoutthebooklet.Also,ifyourunintotermsthatyoudonotunderstand,youcanreadthedefinitionswehaveincludedinvarioussidebarsandintheglossarystartingonpage35.

SinceyourpersonalfinancialplanningextendsbeyondtheBrockUniversityPensionPlan,youwillalsofindgeneralinformationaboutpersonalsavingsandgovernmentbenefitsthatyoumayfinduseful.

Formorehelpinplanningandsavingforyourretirement,youshouldconsider usingtheservicesofaqualifiedfinancialadvisor.

For more information ThisbookletisagoodsourceofinformationabouttheBrockUniversityPensionPlan.Itspurposeistosummarizethetermsandconditionsoftheplan.Ifyou havequestionsorcommentsaboutthisbookletorabouttheBrockUniversityPensionPlan,pleasecontactpensionstaffintheHumanResourcesDepartment atextension3186orextension4898.

It is important to note that this booklet is designed to describe, in simple terms, the Brock University Pension Plan for eligible employees as at March 2016. It has been prepared for information purposes only. All examples of benefit calculations in this booklet are for illustrative purposes only. Your own pension benefit entitlement may differ based on your own circumstances and the application of the detailed provisions of the plan documents.

Subject to legislation and collective bargaining, as applicable, future amendments may be made to the plan. If there is a discrepancy between this booklet and the official plan text, or questions of interpretation arise, the official plan text will prevail. The official plan text, as amended from time to time, is available, on request, in the Human Resources Department.

Someday, perhaps not too far in the future, you will be spending your retirement years doing the things you love. Having a pension you can count on is important and the Brock University Pension Plan provides you with a starting point to build your retirement savings.

Part 1: Your future is worth the investment

For more information...

Ifyouhavequestionsabout

this booklet or the Brock

University Pension Plan, please

calltheHumanResources

Departmentatextension3186

orextension4898.

When… The pension plan provides…

YouleaveBrockUniversity Animmediatemonthlypension,adeferredpension atage55orolder startingatafuturedate,oralump-sumcommutedvalue

YouleaveBrockUniversity Deferredpensionstartingatafuturedateoralump-sum beforeage55 commutedvalue

Youdie Abenefitpayabletoyoureligiblespouse,beneficiary or estate

Takeawaythepensionjargon,thebenefitformulae,andthegovernment regulationsandyouwillfindthatmostpensionplansareoneoftwotypes: •definedcontribution(DC)plansthatoffertheopportunityforplanmembers tobenefitfrominvestmentperformance;and •definedbenefit(DB)plansthatofferthesecurityofaclearlydefined pensionbenefit.

A “hybrid plan” TheBrockUniversityPensionPlanisahybridplan,whichoffersyouthebest ofbothworlds.ItsDCcomponent—theMoneyPurchasePension—letsyou participate in the plan’s investment performance. At the same time, the DB component—theMinimumGuaranteedPension—providesaclearlydefined,formula-basedpension.TheMinimumGuaranteedPensionactsasabenefitfloor orsafetynetthathelpsprotectyoufrommarketdownturns.

Onceyourpensionpaymentsbegin,thepensionthatyoureceivefromtheplaneachyearwillbeequaltothegreaterofyourMoneyPurchasePensionorMinimumGuaranteedPension.

More than a retirement benefit Whilethepensionplan’smainpurposeistoprovideyouwithincomeafteryou retire,italsoprovidesbenefitsinothercircumstances.Aboveisanoverviewof whattheplanprovides.Youwillfindmoredetailsasyoureadtherestofthebooklet.

Who pays for the benefits MoneypurchasecontributionsmadebyyouandtheUniversityaredepositedintoyourMoneyPurchaseAccount.TheUniversityalsomakesadditionalcontributionstotheMinimumGuaranteeFund,whennecessary,basedonpensionlegislationandtheadviceoftheplanactuary.

Allcontributionsareplacedinatrustfund.Professionalmoneymanagers,hiredbytheBoardofTrustees,investtheassetsofthefundbasedoninvestmentpoliciesapprovedbytheBoardofTrustees.TheUniversity’sPensionCommitteemonitorsthe performance of the money managers and recommends changes to the University.YouhavenoinvestmentdecisionstomakeregardingtheMoney PurchaseAccountandMinimumGuaranteeFund.

Part 2: Welcome to the pension plan

4

Commuted value refers to

thelump-sumpresentvalueof

yourpension.Inotherwords,

thecommutedvalueofyour

pension is an estimate of what

youwouldneedtoinvestright

nowtogiveyouthepension

youwouldreceiveifyouwere

toleaveyourbenefitsinthe

plan.Thecalculationisbased

onanumberoffactors,such

as interest rates and mortality

rates,andiscarriedout

according to established

actuarialprinciplesandmethods.

5

Permanent full-time employees Ifyouareapermanentfull-timeemployee,youmaychoosetobecomeaplanmemberonthefirstdayofanymonthcoincidentwithornextfollowingyourdateofhire.However,itismandatorytojointheplanthemonthcoincidentwithornextfollowingthecompletionofonefullyearofserviceorwhenyoureachage 30,whicheverislater.

Other permanent employees, 12-month term full-time employees and limited term faculty employees Ifyouareapermanentemployee(otherthanapermanentfull-timeemployee), a12-monthtermfull-timeemployee,oralimitedtermfacultyemployee,youmaychoosetobecomeaplanmemberonthefirstdayofanymonthfollowingyourdateofhire.Membershipintheplanisnotmandatory,regardlessofyourageoryearsofservice with the University.

Other employees Ifyoudonotmeetoneofthecriteriasetoutabove,membershipintheplanisnotmandatory,regardlessofyourageoryearsofservicewiththeUniversity;however,youmayjointheplanafteryouhavebeenemployedbytheUniversityfor24 consecutivemonths,providedyouhave: •earnedatleast35%oftheCanadaPensionPlan’syear’smaximumpensionable earnings(YMPE)fromemploymentwithBrockUniversityineachofthetwo immediatelyprecedingcalendaryears;or •workedatleast700hoursayearatBrockUniversityineachofthetwo immediately preceding calendar years.

YMPE (year’s maximum

pensionable earnings) is the

earningsmaximumusedto

determinecontributionsand

benefitsundertheCanada

PensionPlan.TheYMPE

isadjustedeachyear.

In2016,itis$54,900.

Early participation in the plan might be one of the wisest financial choices you ever make. The sooner you join the plan, the sooner you can begin to build your retirement benefit. If you spend your career at the University, your Brock University pension could be one of your biggest financial assets at retirement.

Part 3: Joining the plan

How to find out more about your own situation Eachyear,youwillreceiveYour Personal Pension StatementasatJune30. Thestatementwillinclude: •yourpersonalinformationonrecord(includingthenamesofyourspouse andbeneficiary); •totalcontributionstoyourMoneyPurchaseAccountoverthepastyear; •youraccountbalances;and •thepensionyouhaveearnedasofthestatementdateandtheprojectedpension onyournormalretirementdate.

Frequently asked questions Q:WhenwillIreceivemyannualstatement? A:Your Personal Pension StatementispreparedasofJune30andissenttoyoubefore December 31 each year.

Q:HowcanIkeepinformedofthefund’sinvestmentperformance? A:Monthlyratesofreturn,marketreviewsandotherrelatedinvestment informationisavailableonthepensionwebsiteat:http://www.brocku.ca/hr-ehs/pension-new/investments

6

Frequently asked questions Q.WhatformsdoIfilloutatenrolment? A.Youmustcompleteandsignanenrolmentform,whichauthorizesthedeductionsfromyourearnings.Aswell,youarerequiredtocompleteaspousaldeclarationanddesignateabeneficiary.ThenecessaryformsareavailablefromtheHumanResourcesDepartment.

Q:WhocanInameasmybeneficiary? A:Ifyouhaveaspouseonthedateofyourdeath,pensionlegislationrequiresthatyourspousereceiveanydeathbenefitpayablefromtheplan,unlessyourspousehaswaivedhisorherentitlementtothisbenefit.Withoutaspousalwaiver,anydeathorsurvivorbenefitwillbepaidtoyourspouse,regardlessofwhomyou havenamedasyourbeneficiary.

Undertheplanandcurrentpensionlegislation,aspouseisdefinedasaperson towhomyouare: •legallymarried,providedyouarenotlivingseparateandapartfromthat persononthedateadeterminationismade(thatis,retirementordeath); •notlegallymarried,butyouandthatpersonhavecohabitedcontinuously inaconjugalrelationshipforatleastthreeyears;or •notlegallymarried,butyouandthatpersonarecohabitinginaconjugal relationshipofsomepermanence,andarejointlythenaturaloradoptive parentsofachild,asdefinedintheFamily Law Act (Ontario).

Thedefinitionofspouseinpensionlegislationmaybedifferentfromhowaspouseisdefinedforotherpurposes,forexample,undertheIncome Tax Act(Canada).

Ifyoudonothaveaspouseonthedateofyourdeathoryourspousehascompletedawaiver,yourdesignatedbeneficiarywillbeentitledtoreceivethedeathbenefitspayableundertheplan.Yourbeneficiarycanbeanypersonofyourchoice.

Ifyouwishtonameachildwhoisyoungerthanage18asyourbeneficiary,we suggestthatyouconsultyourlawyerbeforecompletingthebeneficiarydesignation.

Ifyoudonotnameabeneficiaryornoneofyourbeneficiariessurviveyou,andyoudonothaveaspouseonthedateofyourdeath,anydeathbenefitwillbepayabletoyourestate.

Yourbeneficiarymaybechangedatanytimeinwriting,subjecttoanylegalrestrictions.Tobevalid,yourwrittenbeneficiarydesignationmustbeprovided totheHumanResourcesDepartment.

Q:DoIhavetoupdatemypersonalinformation? A:Yes.KeepingtheUniversityinformedwheneveryouhavelifeeventsthatchangeyourpersonalcircumstancesisimportant.YoushouldnotifytheHumanResourcesDepartmentofanychangesinyourpersonalcircumstances,suchasachangeinyourmaritalstatus,yourdesignatedbeneficiary,oryouraddress.

Youshouldalsoreviewyourpersonalinformationeachyearwhenyoureceive yourannualpensionstatementtoensurethatyourinformationiscorrectand uptodate.

Q:CanIleavetheplanwhilestillemployedatBrockUniversity? A:Onceyouenrolintheplan,youcannotceaseparticipatingintheplanuntil youterminateemploymentorretire.

Example — total earnings below the YMPE

Pensionableearnings $40,000.00

Totalemployeecontributionsin2016 4.4%×$40,000.00=$1,760.00

Example — earnings below and above YMPE

Pensionableearnings $60,000.00

ContributionsonearningsbelowYMPE 4.4%×$54,900.00=$2,415.60

ContributionsonearningsaboveYMPE 6%×($60,000.00—$54,900.00)=$306.00

Totalemployeecontributionsin2016 $2,415.60+$306.00=$2,721.60

Example — earnings below and above YMPE

Pensionableearnings $120,000.00

ContributionsonearningsbelowYMPE 4.4%×$54,900.00=$2,415.60

ContributionsonearningsaboveYMPE 6%×($120,000.00—$54,900.00)=$3,906.00

Totalemployeecontributionsin2016 $2,415.60+$3,906.00=$6,321.60

7

Money Purchase Account Your contributions to the Money Purchase Account Asamember,youmakethefollowingcontributionsbypayrolldeductiontoyourMoneyPurchaseAccount(thedefinedcontributionportionofthepensionplan):

4.4%ofyourpensionableearningsuptotheYMPE plus 6%ofyourpensionableearningsabovetheYMPE

Employee Contributions Hereareexamplesofhowthisformulawouldworkin2016forafewhypotheticalemployees.TheYMPEin2016is$54,900.

Allofyourcontributionsarefullytax-deductiblefromyourannualincome.Youbenefitfromthistaxdeductibilityrightaway,sinceyourpensioncontributionsaretakenintoaccountwhentheincometaxdeductedfromyourpayiscalculated.

The University’s contributions to your Money Purchase Account TheUniversityisrequiredtomakethefollowingcontributionstoyourMoney PurchaseAccount:

7.4%ofyourpensionableearningsuptotheYMPE plus 9%ofyourpensionableearningsabovetheYMPE

Pensionable earnings

areyourregularannual

earnings received from

the University.

Part 4: Building your pension

Both you and the University contribute toward your pension.

Example — total earnings below the YMPE

Pensionableearnings $40,000.00

TotalUniversitycontributionsin2016 7.4%×$40,000=$2,960.00

Example — earnings below and above YMPE

Pensionableearnings $60,000.00

ContributionsonearningsbelowYMPE 7.4%×$54,900.00=$4,062.60

ContributionsonearningsaboveYMPE 9%×($60,000—$54,900.00)=$459.00

TotalUniversitycontributionsin2016 $4,062.60+$459.00=$4,521.60

Example — earnings below and above YMPE

Pensionableearnings $120,000.00

ContributionsonearningsbelowYMPE 7.4%×$54,900.00=$4,062.60

ContributionsonearningsaboveYMPE 9%×(120,000.00—$54,900.00)=$5,859.00

TotalUniversitycontributionsin2016 $4,062.60+$5,859.00=$9,921.60

University Contributions Hereareexamplesofhowthisformulawouldworkin2016forafewhypotheticalemployees.TheYMPEin2016is$54,900.

8

Short Term Accounts Ifyouareanactivememberandage62orolder,youhavetheoptionof transferringannuallyaportionofyourMoneyPurchaseAccounttotheShortTermAccount.Oncethefundshavebeentransferred,theywillremainintheShort TermAccountuntilyoumakeanelectionwithrespecttoyourpension.Thepurpose ofthisaccountistoassistmemberswiththeirfinancialplanningbyremovingsomeoftheuncertaintythatcomesfromfluctuatingmarketvalueinvestmentreturns ontheMoneyPurchaseAccount.

Atretirement,thecombinedbalancesinyourMoneyPurchaseAccountandShortTermAccountwillbeusedtoprovideapensioninthenormalmanner;thatis,withinthepensionplanorbytransferringthemoneyoutoftheplan.TheMinimumGuaranteedPensionrulescontinuetoapply.

TheHumanResourcesDepartmentcontactseligiblemembersonanannualbasiswith more information on this option.

Minimum Guarantee Fund TheUniversityisresponsibleforensuringthatthereisenoughmoneyinthe MinimumGuaranteeFund—thedefinedbenefitcomponentoftheplan—to financetheMinimumGuaranteedPensionthattheplanprovides.

9

Basedonacceptedactuarialprinciplesandmethods—andontherulesspecified inpensionlegislation—theactuaryfortheplandeterminestheamountof contributionstheUniversitymustmaketomaintaintheMinimumGuaranteeFundattherequiredfundinglevel.Becausethefutureisuncertain,thisdetermination isbasedonanumberofassumptions,includingthoseaboutperformanceofthepensionfundassetsandtherateofchangeinbenefitspayabletomembers.

Ateachvaluationoftheplan,ifinvestmentshavenotperformedaswellas assumed,and/orifthebenefitspayablearegreaterthanassumed,theUniversitymayhavetomakeadditionalcontributionstotheMinimumGuaranteeFund.

Ontheotherhand,theUniversitymaybeabletoreduceitscontributionstotheplanuntilthenextvaluationifthefundinvestmentshaveperformedbetterthanassumedand/orthebenefitspayablearelessthanassumed.

Additional voluntary contributions Inadditiontotherequiredcontributionsdiscussedabove,theplanallowsyou tomakeadditionalvoluntarycontributionsthroughpayrolldeductions.These contributionsareaccountedforinaseparateAdditionalVoluntaryContribution Accountinyourname,thatis,theyarenotco-mingledwithyourrequired contributionstotheMoneyPurchaseAccount.Theadditionalvoluntary contributions,however,arecreditedwiththerateofreturnthatisearned by the Brock University Pension Plan.

TheUniversitydoesnotmakeanycontributionsrelatedtotheadditional voluntarycontributionsandthereisnoguaranteedlevelofpensionwithrespect tothesecontributions.

AllpensioncontributionsarelimitedbytheIncome Tax Act(Canada). TheUniversitywillensurethatregularplanmemberandemployer-required contributionsdonotexceedthisgovernmentlimit;however,youareresponsible toensurethatyoudonotexceedthelimitwithadditionalvoluntarycontributions.Ifyougooverthelimitduetoadditionalvoluntarycontributions,youare responsibleforpayinganypenaltiesandcostsassociatedwiththeover-contribution.

Pleasesee“Part10:Othersourcesofretirementincome”formoreinformation.

Youradditionalvoluntarycontributionsstayintheplan,withintheseparate AdditionalVoluntaryContributionAccount,untiltheearliestofretirement, termination, or death.

Special transfers from other registered pension plans IfyouwereamemberofaregisteredpensionplaninCanadabeforejoining theUniversity,youmaybeabletotransferthelump-sumvalueofyourprior benefitintotheBrockUniversityPensionPlan.Theadministratorsofthetransferringplanwouldneedtoagreetothetermsofthetransferandyoumustcompletetherequiredpaperwork.

Thislump-sumtransferisaccountedforinaseparateSpecialTransferAccountinyourname,thatis,theassociatedfundsarenotco-mingledwithyourrequired contributionstotheMoneyPurchaseAccount.Thelump-sumtransfer,however, iscreditedwiththerateofreturnthatisearnedbytheBrockUniversity Pension Plan.

TheUniversitydoesnotmakeanycontributionsrelatedtoatransferandthereisnoguaranteedlevelofpensionwithrespecttothelump-sumtransfer.

The Variable Annuity Fund is

afundwithintheplan’strust

fundintowhichassetsfrom

yourMoneyPurchaseAccount,

AdditionalVoluntary

ContributionAccountand/

orSpecialTransferAccount

aretransferred,ifyouelect

a pension from one or more

oftheseaccounts.Theassets

are invested according to the

plan’s investment policies and

areusedtoprovidepensionsto

pensionersandtheirsurvivors,

according to the form of

pension elected at pension

commencement.Thevalueof

thisfundcanchangebecause

offactorssuchasinvestment

performance and mortality.

Assuch,theamountofmoney

available to pay pensions

varies from year to year and

thisresultsintheannual

increases or decreases to

pensionamounts.

Variable Annuity Fund

Minimum Guarantee Fund

Short Term Accounts

Special Transfer Accounts

Additional Voluntary Contribution Accounts

Money Purchase Accounts

10

Thelump-sumtransfermuststayintheplan,withintheseparateSpecialTransferAccount,untiltheearliestofretirement,termination,ordeath.TheUniversityadministersthefundsonalocked-inornon-locked-inbasis,accordingto instructionsreceivedfromtheotherplanadministrator.

One trust fund WhilethereareseparateaccountsundertheBrockUniversityPensionPlan,allofthemoneyisactuallyheldtogetherunderonetrustfundthatisadministeredbyprofessionalmoneymanagerswhoinvesttheassetsofthefundbasedonthe University’s Statement of Investment Policies and Procedures.

Thefollowingdiagramillustratesthemake-upofthattrustfund.Theproportionsallottedtoeachtypeofaccountcanchangeovertimewiththeflowof contributionsortransfersintoaccountsandbenefitpaymentsfromthoseaccounts.

ThetrustfundisapartfromtheUniversity’soperationalfunds.TheUniversity’sPension Committee monitors the performance of the money managers and makes relatedrecommendationstotheBoardofTrustees.

Contributions under special circumstances While you are totally disabled Ifyoubecometotallydisabled,yourmembershipintheplanwillcontinueas longasyoureceivebenefitsfromtheUniversity’sLongTermDisabilityIncome ContinuancePlan.YouwillcontinuetoearnpensionableserviceandtheUniversity willdeemaspaidbothemployeeandemployercontributionsduringthetime periodthatyouarereceivinglongtermdisabilitybenefits.

TheHumanResourcesDepartmentwillprovideyouwithspecificdetailsduring the disability management process.

While on leave without pay Whileyouareonleavewithoutpay,inaccordancewithapplicablecollective agreements,UniversitypoliciesandlimitsundertheIncome Tax Act(Canada), youmaybeabletoelectto: •providetheUniversitywithpost-datedchequestocoverrequiredcontributions toyourMoneyPurchaseAccountduringtheperiodoftheleave;or •stopcontributingtotheplanduringtheperiodoftheleave.

Beforechoosingtostopcontributingtotheplan,itisimportanttoconsiderthatyoucannotbuybackserviceoraddthesecontributionsatafuturedate.

ContacttheHumanResourcesDepartmenttoprovideyouwithspecificdetailsbeforeyoubeginyourleave.

A Statement of Investment

Policies and Procedures is

adocumentrequiredby

legislation for all pension

plans. It describes the

objectivesandoperation

of the plan. The statement

outlinesinvestment-related

policiesandprocedures,

includingassetallocation

guidelines.

Registered retirement plan

assets that are locked-in

cannot be taken in cash

whenyouleavetheplan.

Theseassetsmustbeused

toprovideyouwith

retirement income.

Plan assets that are

non-locked-in may be

takenincash.Ifyouhave

non-locked-inassetsand

choosetotakeacashrefund

whenyouleavetheplan,

incometaxeswillbededucted.

11

Maximum contributions The Income Tax Act(Canada)limitsyourandtheUniversity’scontributionsto thedefinedcontributioncomponentoftheplan.Themaximumamountchangeseverycalendaryear.For2016,themaximumamountisthelesserof18%ofyourpensionableearningsor$26,010.Thismaximumappliestothetotalofyourand theUniversity’scontributionstoyourMoneyPurchaseAccount,aswellasyour additionalvoluntarycontributions.

OncethetotalofyourandtheUniversity’srequiredcontributionsinacalendaryearreachthismaximum,nofurthercontributionswillbedeductedfromyour pay,andnofurthercontributionswillbemadebytheUniversityinrespectof yourMoneyPurchaseAccountfortherestofthatcalendaryear.

Frequently asked questions Q:CanIchoosehowmyMoneyPurchaseAccountisinvested? A:No.ThefundsinyourMoneyPurchaseAccountareinvestedbyprofessionalfundmanagers according to the plan’s Statement of Investment Policies and Procedures, whichisapprovedbytheBoardofTrustees.

Q:CanIusemypensioncontributionsascollateralonaloanorasadownpaymentonamortgage? A:No.Youcannotuseplancontributionsinthisway.Theycannotbeassignedtoanyone,forexample,topayadebtorsecurealoan,exceptincertaincasesofmarriage breakdown.

Q:Undertheplan,thenormalretirementageis65.MustIcontinuetomaketherequiredcontributionstothepensionplanifIworkpastage65? A:Yes.Employeeandemployer-requiredcontributionstoyourMoneyPurchase Accountarestillrequiredifyouworkbeyondyour65thbirthday.

Contributionswillcontinueuntilyouretireorreachtheageatwhichyoumustbeginreceivingapension.RegulationsundertheIncome Tax Act(Canada)requirethatyoustarttodrawyourpensionnolaterthanDecember1ofthecalendaryearinwhichyoureachage71.

Q:DoIhavetoparticipateintheplanifIamonaleaveofabsence? A:Whenyouareonaleaveofabsencewithoutpay,youcanchoosenotto makecontributionstotheplanduringtheleaveofabsence.Ifyoumakethischoice,however,pensionableserviceforfeitedduringthisperiodcannotbe purchasedlater.

Q:MayIcontributetotheBrockUniversityPensionPlanandaregisteredretirementsavingsaccount(RRSP)atthesametime? A:Yes.However,contributionsarelimitedbytheIncome Tax Act(Canada).FormoreinformationontherelationshipbetweenyourmembershipintheplanandRRSPcontributions,pleasesee“Part10:Othersourcesofretirementincome.”

If your … Then you will receive a pension equal to…

MoneyPurchasePensionisgreater YourMoneyPurchasePension thanyourMinimumGuaranteed Pension

MinimumGuaranteedPensionis YourMoneyPurchasePension,plusatopup greaterthanyourMoney fromtheMinimumGuaranteeFundequalto PurchasePension theexcessofyourMinimumGuaranteedPension overyourMoneyPurchasePension(tobringyour totalretirementincomeuptotheMinimum GuaranteedPensionamount)

The Brock University Pension Planprovides you withthe greater of:

the Money Purchase Pension provided by converting your Money Purchase Account

balance to a variable annuity at pension commencement;

the Minimum Guaranteed Pension determined

in accordance with a prescribed formula.

or

An annuity is a stream of

monthly payments.

Pensionable service is the

completed years and months

ofcontinuousservicewith

theUniversityduringwhich

youareacontributortothe

plan, or the former plan,

sinceJuly1,1964.Part-time

service is prorated.

12

How the plan works Here are the main differences between the DC and DB components. •TheMoneyPurchaseAccount—theDCcomponent—providesyouwithabenefit basedontheaccumulatedcontributionsandinvestmentearnings.Theamount ofyourretirementincomefromthiscomponentcannotbepredictedahead oftimebecauseitisdependentontheinvestmentearnings(orlosses)andthe costofprovidingtheMoneyPurchasePensionwhenyouretire(usingmortality andrate-of-returnassumptions). •TheMinimumGuaranteedPension—theDBcomponent—providesyouwitha benefitbasedonapredeterminedformulathatfactorsinyourpensionable earnings and years of pensionable service.

Hereishowtheplanprovidesyouwiththegreaterofthetwoamounts.

The Brock University Pension Plan is a hybrid pension plan made up of two parts — a defined contribution (DC) component and a defined benefit (DB) component. These parts are combined so that you have the opportunity to benefit from the investment performance of the pension fund, but your pension is protected against market downturns through the provision of a Minimum Guaranteed Pension.

Part 5: Calculating your pension

13

Money Purchase Pension YourMoneyPurchaseAccountholdstheUniversity’sandyourrequiredmoney purchasecontributions,alongwiththeinvestmentreturnsonthosecontributions. Theamountyoubuildinyouraccountisdirectlyaffectedbytheinvestment performanceofthepensionplan’sassetsoverthecourseofyouryearsof membership in the pension plan.

Atpensioncommencement,yourtotalbalanceintheaccountisconvertedto avariablepensionandtransferredtotheVariableAnnuityFund.Itiscalled “variable”becauseofannualincreasesordecreasestopensions,whichare basedoninvestmentandmortalityexperienceoftheVariableAnnuityFund. YourMoneyPurchasePensionispaidoutoftheVariableAnnuityFundand thestartingamountisbasedonactuarialfactorsineffectatthetimeof pension commencement.

YourMoneyPurchasePensionisdeterminedasfollows:

Money Purchase Account balance at pension commencement ÷ Annuity factor

Unlike most DC pension plans, the Brock University Pension Plan does not transfer yourMoneyPurchaseAccountbalancetoaninsurancecompanyatretirementforthepurchaseofanannuity.Ifyouchoosetoremainintheplan,theplanconvertsyouraccountbalancetoavariablepensionandyoucontinueparticipatinginthe experience of the plan.

WhenyourMoneyPurchaseAccountisconvertedtoavariablepension,the amountofyourpensionwillbeadjustedannuallytotakeintoaccountthe investmentreturnsoftheplanandmortalityexperienceofpensioners.For moreinformationontheseannualadjustments,see“Annualadjustmentsto yourpension”onpage24.

Minimum Guaranteed Pension YourMinimumGuaranteedPensionisdeterminedasfollows:

1.7% × your best average earnings × pensionable service

minus

1/35 × 25% × lesser of best average earnings and final average YMPE × pensionable service (maximum 35 years)

Thispensionispaidforyourlifetimewithafive-yearguaranteeandisactuariallyreducedifyourpensioncommencesbeforeage65.Atyourpensioncommencement, youcanchoosetoreceiveyourpensioninadifferentform,inwhichcasethe pensionamountisactuariallyadjustedaccordingtotheformselected.For example,theautomaticformifyouhaveaneligiblespouseprovidesa60% survivorpensionforyourspouseandtheamountofthispensionislessthanthat of the normal form. Please see “Forms of pension payments” starting on page 21 for more information.

TheMinimumGuaranteedPensionisadjustedannuallybasedontherateofchangeintheConsumerPriceIndex(CPI).Again,formoreinformationonadjustments, see“Annualadjustmentstoyourpension”onpage24.

Herearethreeexamplestoshowyouhowthepensioncalculationswork.Allexamplesassumethatthememberhaselectedtoreceivethepensioninthenormalform,whichispayableforthemember’slifetimewithafive-yearguarantee.

Money Purchase Pension

MoneyPurchaseAccountbalanceatpensioncommencement÷ annuityfactor $300,000÷12.3=$24,390 $24,390

Minimum Guaranteed Pension

(1.7%×bestaverageearnings×pensionableservice)—(1/35×25%× lesserofbestaverageearningsandfinalaverageYMPE×pensionable service(cappedat35years)) (1.7%×$40,000×35)—(1/35×25%×$40,000×35)= $23,800—$10,000=$13,800 $13,800

Emma’s annual pension

InEmma’scase,thehigherpensionisprovidedbytheMoneyPurchase Pensionandthereisnotop-upfromtheMinimumGuaranteeFund. $24,390+$0=$24,390 $24,390

Money Purchase Pension

MoneyPurchaseAccountbalanceatpensioncommencement÷ annuityfactor $150,000÷12.3=$12,195 $12,195

Minimum Guaranteed Pension

(1.7%×bestaverageearnings×pensionableservice)—(1/35×25%× lesserofbestaverageearningsandfinalaverageYMPE×pensionable service(cappedat35years)) (1.7%×$60,000×25)—(1/35×25%×$52,440×25)= $25,500—$9,364=$16,136 $16,136

Jakob’s annual pension

InJakob’scase,thehigherpensionisprovidedbytheMinimum GuaranteedPensionandthereisatop-upfromtheMinimumGuarantee FundtotheMoneyPurchasePension. $12,195+($16,136—$12,195)=$16,136 $16,136

An annuity factor is a factor

usedtoconverttheMoney

PurchaseAccounttoamonthly

retirementbenefit.Thefactor

takesintoaccountexpected

mortalityrates,yourage,

form of pension selected, and

theassumedrateofreturn

thatthefundwillearngoing

forward.Forexample,ifyou

retireatage55,adifferent

annuityfactorwillbeused

tocalculateyourpension

thanifyouretireatage65,

toaccountforthefactthat

yourpensionmaybepaidfor

a longer period of time.

The term best average

earnings refers to the average

ofyourpensionableearnings

duringyourfivehighest-paid

years of pensionable service.

Ifyouhavefewerthanfive

years of pensionable service,

theaverageofyourtotal

pensionableearningsisused.

Final average YMPE is the

averageoftheYMPEduring

thelastfiveyearsbefore

termination or retirement.

14

ExampleEmmaisage65,hasaMoneyPurchaseAccountbalanceof$300,000,bestaverageearningsof$40,000,and35yearsofpensionableservice.ThefinalaverageYMPEis$52,440.

ExampleJakobisage65,hasaMoneyPurchaseAccountbalanceof$150,000,bestaverageearningsof$60,000and25yearsofpensionableservice.ThefinalaverageYMPEis$52,440.

Money Purchase Pension

MoneyPurchaseAccountbalanceatpensioncommencement÷ annuityfactor $650,000÷12.3=$52,846 $52,846

Minimum Guaranteed Pension

(1.7%×bestaverageearnings×pensionableservice)—(1/35×25%× lesserofbestaverageearningsandfinalaverageYMPE×pensionable service(cappedat35years)) (1.7%×$120,000×30)—(1/35×25%×$52,440×30)= $61,200—$11,237=$49,963 $49,963

Cynthia’s annual pension

InCynthia’scase,thehigherpensionisprovidedbytheMoneyPurchase Pensionandthereisnotop-upfromtheMinimumGuaranteeFund. $52,846+$0=$52,846 $52,846

15

AswiththecontributionstoyourMoneyPurchaseAccount,theIncome Tax Act (Canada)placescertainlimitsontheleveloftheMinimumGuaranteedPensionthatcanbeprovidedbytheplan.Additionaldetailsregardingthedefinedbenefitlimitcanbefoundonpage24.

ExampleCynthiaisage65,hasaMoneyPurchaseAccountbalanceof$650,000,bestaverageearningsof$120,000and30yearsofpensionableservice.ThefinalaverageYMPEis$52,440.

Frequently asked questions Q:Iamanactiveplanmember.HowcanIfindoutformyselfwhatmypensionmightbe? A:TheBrockPensionEstimatorallowsyoutoestimateyourprojectedmonthlypension.YoucanusetheEstimatortoestimatethebenefitsyouwouldbeentitledtofromtheMoneyPurchaseAccountandtheMinimumGuaranteeFund.TheEstimator’scalculationsarebasedontheassumptionthatyouwillremainemployedbytheUniversityuntilyouretire.Tocompleteitscalculations,theEstimator usestheinformationonyourmostrecentannualstatementaswellasyour assumptionsoffutureratesofreturnandsalaryincreases.

FeaturesoftheEstimatorinclude: •yourup-to-datepersonaldata(employeenumber,dateofbirth,salary,etc.); •accountbalances; •projectedpension;and •howtheoptionalformofpensionyouchoosewouldimpactyourpensionand thebenefitthatwouldgotoyoursurvivingspouseorbeneficiary.

YoucanaccesstheEstimatorfromyour“MyWork”tabinthe“my.brocku.ca”portal.Detailedlogininstructionsareavailableonthewebsite.

IfyouhaveaShortTermAccount,orifyourequirepensionprojectionsbeyond age65,youshouldcontacttheHumanResourcesDepartmenttorequestestimates.

A deferred pension means

pension payments that start at

afuturedate,asopposedto

beingpaidasofthedayyou

stop working for the University.

A locked-in retirement

account (LIRA) is similar to a

RRSPforincometaxpurposes,

butissetupwithlocked-in

fundsthataretransferredout

of a pension plan. Financial

institutionsacceptinglocked-in

fundsmustagreetoadminister

themassetoutinthePension

Benefits Act(Ontario).The

range of investments offered

inaLIRAdependsonyour

financialinstitution,butis

often the same range as

for RRSPs.

16

Youcanchoose: •adeferredpension;or •totransferyourMoneyPurchaseAccountbalancetogetherwiththecommuted value,ifany,oftheexcessofyourMinimumGuaranteedPensionoveryour projectedMoneyPurchasePensionto: –yournewemployer’spensionplan,ifallowed;or –alocked-inretirementaccount(LIRA).

Ifyoucontributedtotheplanbefore1987,youcantake25%ofyourpre-1987MoneyPurchaseAccountbalanceincash(lesswithholdingtaxes)andtransfertheremaindertoalocked-inretirementaccount.

Ifyourpensionbenefitisconsideredtobea“smallbenefit”underpensionlegislation,youcantakeyourMoneyPurchaseAccountbalancetogetherwiththecommutedvalue,ifany,oftheexcessofyourMinimumGuaranteedPensionoveryourprojectedMoneyPurchasePension: •incash,lesswithholdingtaxes;or •transferittoanon-locked-inRRSP.

TheoptionsavailableifyouleaveemploymentwiththeUniversityatage55orolderaredescribedin“Part7:LeavingtheUniversityatage55orolder.”

Additional voluntary contributions Additionalvoluntarycontributions(alongwithinvestmentincomeonthem)canbe: •takenascash,lesswithholdingtaxes; •transferredtoyournewemployer’spensionplan,ifallowed;or •transferredtoanon-locked-inRRSP.

Theamountofinvestmentincomegeneratedisdependentoninvestmentearningsor losses.

Special transfers from other registered pension plans Whatyoucandowithamountstransferredfromotherpensionplans(alongwithinvestmentincomeonthoseamounts)willdependonwhetherornottheseamountsweretransferredtotheBrockUniversityPensionPlanonalocked-inbasis.

Theamountofinvestmentincomegeneratedisdependentoninvestmentearningsor losses.

Amountstransferredonalocked-inbasiscanbetransferred: •toyournewemployer’spensionplan,ifallowed;or •toaLIRA.

Amountstransferredonanon-locked-inbasiscanbe: •takenascash,lesswithholdingtaxes; •transferredtoyournewemployer’spensionplan,ifallowed;or •transferredtoanon-locked-inRRSP.

If you leave employment with the University before you reach age 55, the plan provides a termination benefit that allows you some flexibility.

Part 6: Leaving the University before age 55

Lump-sum amount Percentage of withholding tax

Uptoandincluding$5,000 10%

$5,000.01to$15,000 20%

Morethan$15,000 30%

17

Frequently asked questions Q:WhendoIfindoutwhatmybenefitsareifIleaveemploymentwiththeUniversity? A:TheUniversitywillprovideyouwithaStatement and Election of Benefits on Termination of Employmentformthatwilldetailallofyourpensionbenefits, theirvalue,andyouroptions.Theformsarenormallysentwithin30daysof yourterminationdate.It’simportantthatyoucompletetherequiredpaperwork,andreturnittotheHumanResourcesDepartmentsothatyourbenefitscanbe paidtoyouaccordingtoyourwishes.

Q:CanItransfermyBrockUniversitypensiontomynewemployer? A:Yes,youcantransferyourBrockUniversitypensiontoanotherregisteredpensionplansolongastheplanisregisteredinCanada,acceptssuchtransfers,andtheplan administrators agree to the terms of the transfer.

Q:Whatdoes“locked-in”mean? A:Locked-inreferstofundsthatcannotbetakenascash.Youmustusethese fundstoprovideyourselfwithretirementincome.Pensionlegislationandthetermsoftheplantextdeterminewhenyourpensionbenefitsbecomelocked-in.

Financialinstitutionsacceptinglocked-infundsmustagreetoadministertheminaccordancewithapplicablepensionregulations.Locked-inmoneydoesnothavetostayinthesameaccountuntilretirement.Youmaytransferittootherpermittedlocked-inarrangementsoruseittobuyanannuityatanytime.

Q:Whatarewithholdingtaxesandhowmucharethey? A:Withholdingtaxesaresetratesoftaxdeductedatthesourcefromany lump-sumcashpaymentyoureceivefromaregisteredpensionplan.Cash refundsaretaxablebecauseyoureceivedataxdeductionwhenyoumade contributionstotheplan.

SinceJanuary1,2005,thewithholdingtaxratesarethoseshowninthetable.ThesearesetbytheCanadaRevenueAgency(CRA)andaresubjecttochange.

Inadditiontowithholdingtaxes,theamountofyourcashrefundwillbeadded toyourincome.Dependingonyourpersonalsituation,youmayberequiredto payadditionalincometaxwhenyoufileyourreturnoryoucouldgetarefund.

Youarenotsubjecttowithholdingtaxesifyoutransferamountsdirectlyfrom aregisteredpensionplantoanotherregisteredplan,suchasaRRSP.

The normal retirement date

intheplanisthefirstofthe

monthfollowingyour65th

birthday,oronyourbirthday

shouldthedatescoincide.

(Whilethisisthenormal

retirementdateunderthe

plan,facultymembers

typicallyretireonJune30th,

which is aligned with the

academicyear.)

LIF (life income fund) is an

arrangement that provides

retirement income from

fundsthatoriginatedfrom

a registered pension plan or

LIRA.ALIFisregulatedby

the Income Tax Act(Canada)

and by provincial pension

benefitslegislation.

18

Active plan membersYoucanretireandbeginreceivingyourpension: •atage65(thenormalretirementdate); •asearlyasage55withapensionthatisactuariallyreducedfor earlyretirement;or •aslateasDecember1ofthecalendaryearinwhichyoureachage71.

Your two main choices for retirement income TheBrockUniversityPensionPlanoffersyouflexibility.Atnormal,early,or postponedretirement,youhavetwochoices.Youcan: •staywithintheplanandtakeapension;or •transferyourMoneyPurchaseAccountbalancetogetherwiththecommuted value,ifany,oftheexcessofyourMinimumGuaranteedPensionoveryour projectedMoneyPurchasePensionto: –alocked-inretirementaccount(LIRA);or –alifeincomefund(LIF).

AllamountspayablefromtheplanaresubjecttolimitsundertheIncome Tax Act(Canada).

Ifyouchooseapensionwithintheplan,ineachyearafterpensioncommencement,youwillreceivethegreaterofyourMoneyPurchasePensionoryourMinimum GuaranteedPension.Thiswasdescribedinmoredetailearlierinthisbookletin“Part5:Calculatingyourpension.”

Insteadofchoosingapensionwithintheplan,youcanchoosetotakethevalueofyourpensionoutoftheplantoalocked-inretirementaccount.ThisvalueismadeupofyourMoneyPurchaseAccountand,ifapplicable,thecommutedvalueof anyexcessofyourMinimumGuaranteedPensionoveryourprojectedMoney PurchasePension.

Your Brock University Pension Plan helps provide you with a foundation for retirement.

Part 7: Leaving the University at age 55 or older

19

Deferred plan membersYoucanbeginreceivingyourpension: •atage65(thenormalretirementdate); •asearlyasage55withapensionthatisactuariallyreducedfor earlyretirement;or •aslateasDecember1ofthecalendaryearinwhichyoureachage71.

Normal or early retirementTheBrockUniversityPensionPlanoffersyouflexibility.Atnormalor earlyretirement,youhavetwochoices.Youcan: •staywithintheplanandtakeapension;or •transferyourMoneyPurchaseAccountbalancetogetherwiththecommuted value,ifany,oftheexcessofyourMinimumGuaranteedPensionoveryour projectedMoneyPurchasePensionto: −alocked-inretirementaccount(LIRA);or −alifeincomefund(LIF).

AllamountspayablefromtheplanaresubjecttolimitsundertheIncome Tax Act (Canada).

Ifyouchooseapensionwithintheplan,ineachyearafterpensioncommencement,youwillreceivethegreaterofyourMoneyPurchasePensionoryourMinimumGuaranteedPension.Thiswasdescribedinmoredetailearlierinthisbookletin“Part5:Calculatingyourpension.”

Atnormalorearlyretirement,youcanchoosetotakethevalueofyourpensionoutoftheplantoalocked-inretirementaccount.ThisvalueismadeupofyourMoneyPurchaseAccountand,ifapplicable,thecommutedvalueofanyexcessofyourMinimumGuaranteedPensionoveryourprojectedMoneyPurchasePension.

Postponed retirement (after age 65)Atpostponedretirement(afterage65),youwillreceiveapensionfromthePlan.YoumustbeginreceivingapensionbyDecember1ofthecalendaryearinwhichyoureachage71.

AllamountspayablefromtheplanaresubjecttolimitsundertheIncome Tax Act (Canada).

Eachyearafterpensioncommencement,youwillreceivethegreaterofyourMoneyPurchasePensionoryourMinimumGuaranteedPension.Thiswasdescribedinmoredetailearlierinthisbookletin“Part5:Calculatingyourpension.”

20

Making your decisionThere are many reasons why some people choose to remain in the plan, while otherschoosetotransfertheirbenefitsoutoftheplan.

Somepeoplechoosetoremainintheplanbecause: •theylikethesecurityprovidedbytheMinimumGuaranteedPension;or •theydonotwanttheresponsibilityofinvestingtheirassetsandcreating retirement income.

Sometransferthevalueoftheirpensionoutoftheplanbecause: •theywanttomaintaincontrolovertheirretirementsavings; •theyareconfidenttheycangainahigherreturnusingtheirowninvestment strategy;or •theybelievetheydonothavealonglifeexpectancy.

Whateveryoudecide,youshouldconsiderspeakingwithaqualifiedindependentfinancialadvisorbeforemakingyourchoice.Anindependentadvisorcangive youunbiasedadviceonwhatoptionisbestbasedonyourpersonalcircumstances.BrockUniversitycannotgiveyoufinancialadvice.

If you choose to remain in the plan Ifyouchoosetoreceiveyourpensionfromtheplan,yourMoneyPurchase AccountbalancewillbetransferredtotheVariableAnnuityFundandconverted toavariablepension(yourMoneyPurchasePension)basedontheactuarialfactors ineffectatthetimeofyourretirement.

YourMinimumGuaranteedPensionwillbecalculatedbasedontheplanformula. Ifyouareleavingbeforeyournormalretirementdate,thispensionisactuariallyreducedtoreflecttheexpectedlongerpaymentperiod.

IfyourMoneyPurchasePensionislowerthanyourMinimumGuaranteedPension,thedifferencebetweenthetwoamountswillbepaidtoyouasatop-uppensionfromtheMinimumGuaranteeFund.

Formoreinformationonhowyourpensioniscalculated,see“Part5:Calculatingyourpension”earlierinthisbooklet.

Additional voluntary contributions Inthecaseofretirement,additionalvoluntarycontributionscanbe: •takenascash,lesswithholdingtaxes; •transferredtoanon-locked-inRRSP; •transferredtoaninsurancecompanytopurchasealifeannuity;or •usedtoprovideanadditionalpensionfromtheVariableAnnuityFund.The additionalamountofpensionwouldbecalculatedusingthesameactuarial factorsthatwereusedtocalculateyourMoneyPurchasePension,andbe subjecttothesameannualadjustments,butwithnominimumguarantee.

Actuarially reduced means

thatyourpensionwillbe

reducedbasedonactuarial

factorstoaccountforthefact

thatyouwouldbereceiving

the pension for a longer

period of time.

21

Special transfers from other registered pension plans Inthecaseofretirement,whatyoucandowithamountstransferredfromotherpensionplans(alongwithinvestmentincomeonthoseamounts)willdependonwhetherornottheseamountsweretransferredonalocked-inbasis.

Amountstransferredonalocked-inbasiscanbetransferred: •toaLIRAorLIF;or •toaninsurancecompanytopurchasealifeannuity.

Amountstransferredonanon-locked-inbasiscanbe: •takenascash,lesswithholdingtaxes; •transferredtoaregisteredretirementsavingsplan;or •transferredtoaninsurancecompanytopurchasealifeannuity.

Alternatively—whetherlocked-inornot—thetransferredamountscanbeusedtoprovideanadditionalpensionfromtheVariableAnnuityFund.TheadditionalamountofpensionwouldbecalculatedusingthesameactuarialfactorsthatwereusedtocalculateyourMoneyPurchasePension,andbesubjecttothesameannualadjustments,butwithnominimumguarantee.

Postponed retirement Retirementatage65isnotmandatory.Ifyoudecidetocontinueworkingat theUniversityafterage65,youwillcontinuecontributingtotheplanandaccruingservice. However, according to Income Tax Act(Canada)regulations,youmust beginyourpensionnolaterthanDecember1ofthecalendaryearinwhich youreachage71.

Forms of pension payments Onceyouarereadytoapplyforyourpension,andyouhavedecidedtoremain intheplan,youwillhavetochooseaformofpension.Theplanpromisesyouthe normalformofpension.Italsogivesyoutheflexibilitytochooseapensionoptionthatbestreflectsyourneedsatretirement.

Theavailableoptions—orthewayyourpensionwillbepaidout—willdependonwhetherornotyouhaveaneligiblespouseatthetimeyourpensionpaymentsstart.Howmuchthevariousoptionspaydependsonyourageandtheageofyoureligiblespouse(ifthereisone).Onceyourpensionstarts,theformofpension cannot be changed.

Normal form of pension Thenormalformofpensionisapensionpaidforyourlifetime(calledasingle-lifepension)withafive-yearguarantee.Underthisform,paymentswillendonyourdeath.Ifyoudiebeforetheendofthefive-yearguaranteeperiod,paymentsin thesameamountaswerepayableduringyourlifetimewillcontinuetobepaid toyourbeneficiaryforthebalanceoftheguaranteeperiod.Alternatively,your beneficiarycouldchoosetoreceivethevalueoftheremainingguaranteed paymentsinalumpsum.

Joint-and-survivor

percentage is a percentage

ofyourpensionthat

continuestoyoureligible

spouse,forthespouse’s

lifetime,ifyoudieduring

retirement. In Ontario, the

lawrequiresthatyourspouse’s

pensionbeatleast60%ofthe

pension that was being paid

toyou(unlessawaiverwas

signedbyyourspouse).

22

Automatic form of pension UndertheOntariopensionlegislation,ifyouhaveaneligiblespouseatpensioncommencement,youmustprovideatleasta60%survivorpensionforyoureligiblespouse(calleda60%joint-and-survivorpension),unlessheorshewaivestherighttothisbenefitbysigningaWaiver of Joint-and-Survivor Pension form. The waiver takeseffectprovidedtheUniversityreceivesitbeforeyourretirementdate.Thewaivermaybecancelledbywrittennoticereceivedbeforeyourpensionstarts.

Asaresult,ifyouhaveaneligiblespouseatpensioncommencement,theautomatic formforpayingyourbenefitsisonethatpaysyouapensionforyourlifetimeand a60%pensiononyourdeathtoyoureligiblespouse,untilyourspouse’sdeath. Thepensionamountthatyoureceiveunderthisformwillbeactuariallyadjusted toreflecttheadditionalcostofprovidingthesurvivorpensiontoyourspouse.

Optional forms of pension If you do not have a spouse or you have filed a spousal waiver Ifyoudonothaveaneligiblespouse,oryouhavefiledaspousalwaiver,instead ofthenormalform,youcanchoosetoreceiveyourpensionasasingle-life pensionwith: •noguarantee; •a10-yearguarantee;or •a15-yearguarantee.

Ifyoudiebeforetheendofanyguaranteeperiod,pensionpaymentsinthesameamountaswerepayableduringyourlifetimewillbepaidtoyourbeneficiaryforthebalanceoftheguaranteeperiod.Alternatively,yourbeneficiarywillhaveachoiceofchoosingtoreceivethevalueoftheremainingguaranteedpayments inalumpsum.

If you have a spouse Ifyouhaveaneligiblespouse,insteadoftheautomaticform,youcanchoose toreceiveyourpensionasajoint-and-survivorpensionat: •60%withaguaranteeof5,10,or15years; •75%withnoguaranteeoraguaranteeof5,10,or15years;or •100%withnoguaranteeoraguaranteeof5,10,or15years.

Thesepensionsarepayableforaslongasyoulive.Onyourdeath,thejoint-and-survivorpercentageofpensionthatwaspayabletoyouwillcontinuetoyourspouseforaslongasheorshelives.Ifyouandyourspousebothdiebeforetheendof theguaranteeperiod,theestateofthelastpensionrecipientwillreceivethe commutedvalueofthepaymentsremainingintheguaranteeperiod.

Eachoptiondiffersintwofundamentalways—howmuchyoureceiveforyour lifetime,andhowmuchyoureligiblespouseorbeneficiaryreceivesonyourdeath.

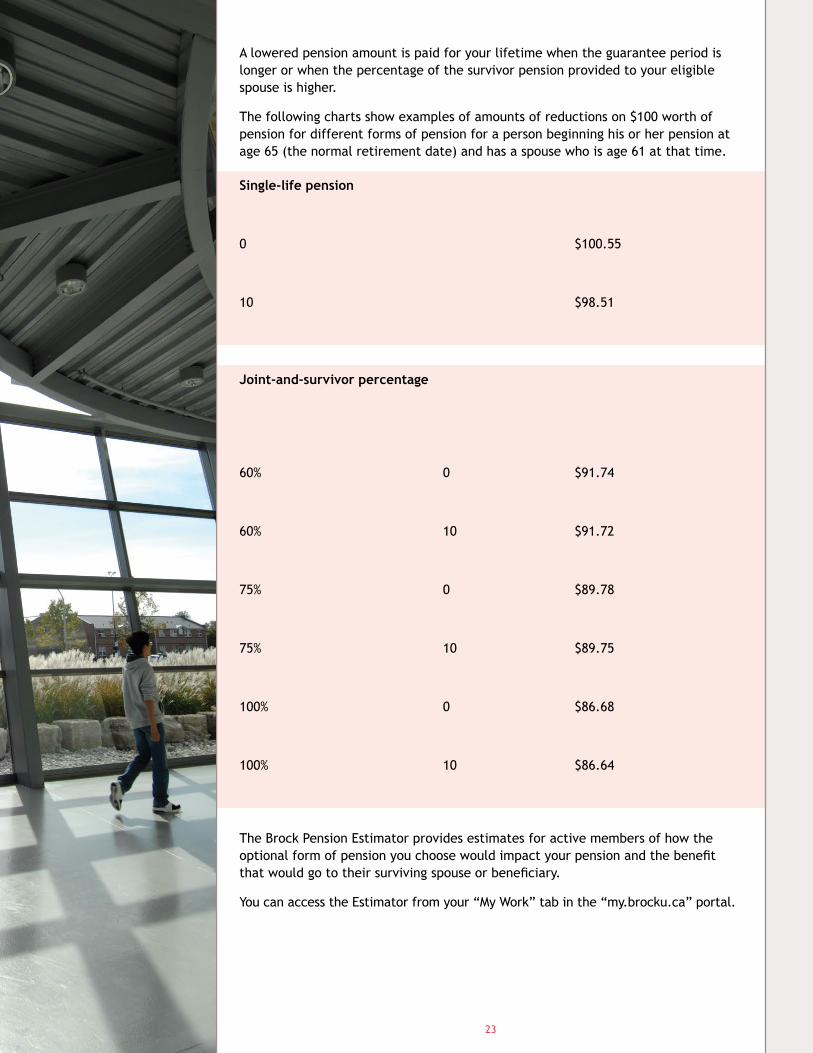

Joint-and-survivor percentage

Percentage of member’s pension paid to eligible spouse upon member’s death Years guaranteed Amount of member’s pension

60% 0 $91.74

60% 5 $91.74

60% 10 $91.72

60% 15 $91.63

75% 0 $89.78

75% 5 $89.78

75% 10 $89.75

75% 15 $89.64

100% 0 $86.68

100% 5 $86.68

100% 10 $86.64

100% 15 $86.51

Single-life pension

Years guaranteed Amount of member’s pension

0 $100.55

5(normalform) $100.00

10 $98.51

15 $96.29

23

Aloweredpensionamountispaidforyourlifetimewhentheguaranteeperiodislongerorwhenthepercentageofthesurvivorpensionprovidedtoyoureligiblespouseishigher.

Thefollowingchartsshowexamplesofamountsofreductionson$100worthofpension for different forms of pension for a person beginning his or her pension at age65(thenormalretirementdate)andhasaspousewhoisage61atthattime.

TheBrockPensionEstimatorprovidesestimatesforactivemembersofhowtheoptionalformofpensionyouchoosewouldimpactyourpensionandthebenefitthatwouldgototheirsurvivingspouseorbeneficiary.

YoucanaccesstheEstimatorfromyour“MyWork”tabinthe“my.brocku.ca”portal.

24

Annual adjustments to your pensionAfterpensioncommencement,bothyourMoneyPurchasePensionandyour MinimumGuaranteedPensionwillbeadjustedannuallyeffectiveJuly1.

Adjustment to Minimum Guaranteed Pension YourMinimumGuaranteedPensionwillbeadjustedeffectiveeachJuly1toreflectchangesintheConsumerPriceIndexduringthepreceding12months,cumulativefrompensioncommencement.TheincreaseintheMinimumGuaranteedPensioninanygivenyearislimitedto2%andyourMinimumGuaranteedPensionwillnotdecreaseasaresultofthisadjustment.

Adjustment to Money Purchase Pension YourMoneyPurchasePension,ontheotherhand,cangoupordowninagivenyear.

Whenyoufirstretire,theactuarialfactorsusedtoconvertyourMoneyPurchase AccountbalancetoaMoneyPurchasePensionarebasedonassumptionsregardingthe rateofreturnthattheplanassetswillearninthefutureandfuturemortalityrates.

Totheextentthattheactualinvestmentandmortalityexperienceisdifferentfrom theseassumptions,orexpectationsoffutureexperiencechange,yourMoneyPurchase Pensionswillbepositivelyornegativelyadjustedonanannualbasis.

Currentcalculationsassumethattheplanassetswillearnarateofreturnof6%annuallythroughoutyourretirement.Therefore,beforetakingintoaccountanymortalitygainsorlosses,theinvestmentsfromtheMoneyPurchaseAccountmustearn6%tomaintainaconstantpension.Forexample,iftheplan’srateofreturn inagivenplanyearis9%,withnomortalitygainsorlosses,yourMoneyPurchasePensionamountwouldincreaseby3%(9%minus6%=3%).Iftheplan’srateofreturnwas3%inagivenyear,withnomortalitygainsorlosses,yourMoneyPurchasePensionamountwoulddecreaseby3%(3%minus6%=-3%).

Throughoutyourretirement,thepensionyoureceiveeachyearwillbeequaltothegreaterofyourMoneyPurchasePensionforthatyearoryourMinimumGuaranteedPensionforthatyear.IntheyearsthatyourMinimumGuaranteedPensionexceedsyourMoneyPurchasePension,theexcesswillbepaidasatop-upfromthe MinimumGuaranteeFund.

WhileeffectiveJuly1eachyear,theannualadjustmentmaynotappearonyourpensionpaymentuntilOctober1.Theadjustmentsaremaderetroactively,asittakessometimetocalculate,confirm,andadministertheadjustments.

25

Pension amounts based on additional voluntary contributions or special transfers PensionsbasedonyouradditionalvoluntarycontributionsorspecialtransfersareadjustedonJuly1inthesamemannerasyourMoneyPurchasePension;however,thereisnominimumguaranteeamountassociatedwitheitherofthese.

Maximum pension amount The Income Tax Act(Canada)limitstheamountofpensionbenefityoumayearnundertheMinimumGuaranteedPensioncomponentoftheplan.Thelimitchangesfromtimetotime.Thecurrentlimitin2016is$2,890.00peryearofserviceforapension that starts at the normal retirement date.

Example Jimretiresin2016andhas35yearsofservice.ThemaximumlimitplacedbytheIncome Tax Act(Canada)onJim’sannualpensionwouldbe$101,150.00.

35×$2,890.00=$101,150.00.

Ifyouarestartingyourpensionbeforeyournormalretirementdate,thismaximumisreducedaccordingtotherulesprescribedbytheIncome Tax Act(Canada).

Notice of retirement YoushouldcontacttheHumanResourcesDepartment12monthsbeforeyourretirementdatetoreceiveestimatedpensionvalues.

YourwrittennoticeofretirementshouldbeprovidedtotheHumanResourcesDepartmentatleastthreemonthsbeforeyourretirementdate.Thenoticeshouldincludetheretirementdateandyoursignature.

OncetheUniversityreceivesyournotice,youwillbemailedaStatement and Election of Benefits on Retirement.Itwillinclude: •yourpersonalinformationonrecord(includingthenamesofyoureligible spouseandbeneficiary); •thetotalcontributions; •yourestimatedaccountbalancesintheMoneyPurchaseAccount,ShortTerm Account,AdditionalVoluntaryContributionsAccount,Locked-inTransfer Account,andNon-Locked-inTransferAccount; •theestimatedpensionyouhaveearnedasofyourretirementdate;and •abenefitoptionsform.

Youwillalsoreceiveotherformsrequiredfortransferringyourpensionbenefit toalocked-inretirementaccount(LIRA)orlifeincomefund(LIF).

Youwillbeaskedtoprovideproofofyourageaswellasyourspouse’sage.

Youwillalsoreceivea Declaration of Marital Status Formthatmustbecompletedregardlessofwhetheryouchoosetostayintheplanortransferyourpensionout of the plan.

CompletedpensionpaperworkshouldbeprovidedtotheHumanResources Departmentatleasttwomonthsbeforeyourretirementdate.

26

Receiving your pension payments Pensionsarepaidonthefirstbusinessdayofthemonth.Yourveryfirstpaymentwillbedelayedaweekortwoasyourpaymentcalculationtakesplace,the Universitypreparesinstructionfortheplan’scustodiantomakepaymentto you,andthecustodianupdatestheirsystemsforthenewpayment.

PaymentismadebydirectdeposittoaCanadianbankaccountofyourchoice.AvoidchequemustbeprovidedtotheHumanResourcesDepartmentbeforeyourpensionpaymentsbegin.IfyouwillbelivingoutsideofCanadaduringyourretirement,youshouldcontacttheHumanResourcesDepartmenttodiscussamethodofpayment.

AllpensionpaymentsfromtheplanaremadeinCanadianfunds.

Frequently asked questions

Q:Doesmypensionamountchangeifmyspousediesbeforeme? A:No,yourpensionamountdoesnotchangeafteraspouse’sdeath.Allthesame,youshouldnotifytheHumanResourcesDepartmentofyourspouse’sdeathifyouretiredwithajoint-and-survivorpension,asitisimportanttoensurethatyourrecordsareuptodate.

Q:WhathappensifIremarryafterpensioncommencement? A:Onlythespouseyouhaveonpensioncommencement,ifany,iseligibletoreceiveaspousalpension.Ifyouremarryorenterintoacommon-lawrelationshipafterthedateyourpensionpaymentsbegin,yournewspousewillnotbeeligible toreceiveaspousalbenefit.

Q:IfIretire,doIhavetostartdrawingmyBrockUniversitypensionimmediately? A:No,youcanelectadeferredpensionfromtheBrockUniversityPensionPlan.Regulationsunderthe Income Tax Act(Canada)requirethatyoustarttodrawyourpensionnolaterthanDecember1ofthecalendaryearinwhichyouturnage71.

Q:WhatisthelatestdatethatIcanstartreceivingmypension? A:YoumustbeginreceivingyourpensionnolaterthanDecember1ofthecalendar yearinwhichyoureachage71.

Q:IfIresignfromtheUniversityandgotoworkforanotheremployer,canIleavemypensionwithBrockUniversity? A:Yes.ChoosingtodeferyourpensionmeansthatthepensionispayablefromtheBrock University Pension Plan at a later date.

Under Ontario pension

legislation, a spouse is a

persontowhomyouare:

•legallymarried,provided

youarenotlivingseparate

and apart from that

person;

•notlegallymarried,but

youandthatpersonhave

cohabitedcontinuouslyin

aconjugalrelationshipfor

atleastthreeyears;or

•notlegallymarried,but

youandthatpersonare

cohabitinginaconjugal

relationship of some

permanence, and are

jointlythenaturalor

adoptive parents of a

child,asdefinedinthe

Family Law Act (Ontario).

Q:HowsooncanIhavemymoneyafterIretire? A:IfBrockUniversityreceivesyourpaperworkinatimelyfashion—thatis,atleasttwomonthsbeforepensioncommencement—yourfirstpensionpaymentwillbeprocessedtobedepositedtoyouraccountwithintwoweeksofthepension commencementdate.Thereafter,thepaymentwillbedepositedintoyour accountonthefirstbusinessdayofthemonth.

Ifyouchosealump-sumtransferratherthanapension,thetransfertypically willbeprocessedwithinthreeweeksofyourretirementdate.

Q:IfIdiewhilecollectingapension,doesmyspouse,family,orestatereceiveasurvivorbenefit? A:Ifyoudiewhilecollectingapension,thesurvivorbenefitdependsontheform ofpensionyouchoseatpensioncommencement.Forexample,ifyouchoseajoint-and-survivor60%witha15-yearguarantee,afteryourdeathyourspousewouldreceive60%ofyourpensionamountfortherestofyourspouse’slife.BothMoneyPurchaseandMinimumGuaranteedPensionamountsarereducedby60%andbothamountscontinuetobeadjustedonanannualbasis.Formoreinformationontheadjustmentprocess,seepage23.

Ifbothyouandyourspousediebeforetheendofthe15-yearguaranteeperiod,thevalueofanyremainingpaymentswouldbepaidtotheestateofthelastlivingpensionrecipient.Ifyouand/oryourspouselivebeyondthe15-yearguaranteeperiod, pension payments will end after the death of the last pension recipient. Nopaymentwouldbemadetotheestate.

27

Death before pension commencement

Options for an eligible spouse or beneficiary Ifyoudiebeforepensioncommencement,youreligiblespouseorbeneficiarywillreceiveasurvivorbenefitbasedonyourMoneyPurchaseAccountbalancetogetherwiththecommutedvalue,ifany,oftheexcessofyourMinimumGuaranteed PensionoveryourprojectedMoneyPurchasePension.

Note:Ifyouhaveaneligiblespouse,andunlessyourspousehaswaivedhisorherentitlementtothesurvivorbenefit,yourspousewillreceivethesurvivorbenefitevenifheorsheisnotyourdesignatedbeneficiary.

Options for an eligible spouse Insteadofalump-sumbenefit,asurvivingspousemaytransferthelump-sumbenefitamounttoaregisteredretirementsavingsplanortoaninsurancecompanytopurchasealifeannuity.

Alternatively,asurvivingspousemaychoosetotakeanannualpension.TheHumanResourcesDepartmentwillprovidethesurvivingspousewithdocumentationoutlininghisorheroptions.

Death after pension commencement

Ifyoudieafterpensioncommencement,anysurvivorbenefitsprovidedwill depend on the form of pension payment thatyouchoseatpensioncommencement (forexample,foryourlifeonly,foryourlifewithaguaranteedperiod,orajoint-and-survivorpensionthatcontinuestoyourspouseafteryoudie).

On your death, the plan provides your survivors with benefits, whether you die before or after your pension begins.

Part 8: Providing for your survivors

28

Annual pension statements As an active member of the plan, each year before December 31, the University will provide Your Personal Pension Statementtoyou. Thestatementwillinclude: •yourpersonalinformationonrecord(includingthenamesofyourspouse, ifapplicable,andbeneficiary); •totalcontributionsoverthepastyear; •theaccountbalancesintheMoneyPurchaseAccount,ShortTermAccount, AdditionalVoluntaryContributionsAccount,Locked-inTransferAccountand Non-Locked-inTransferAccount;and •thepensionyouhaveearnedasofthestatementdateandtheprojectedpension onyournormalretirementdate.

IfyouleavetheUniversity,theUniversitywillcontinuetosendyouanannual statement.Thisstatementwillincludeyourpersonalinformationonrecordand thebalancesofanyaccountsyouhold.

Youshouldreviewtheinformationonthisstatementandreportanyinaccuracies as soon as possible.

Yourstatementisanimportantestate-planningdocument.Reviewitcarefully andfileitforfuturereference.

Governance The plan is a registered pension plan, sponsored and administered by Brock University. TheplanisregisteredwiththeFinancialServicesCommissionofOntariounder registrationnumber0327767.ItisalsoregisteredwiththeCRA.

TheBrockUniversityPensionPlanbecameeffectiveJanuary1,1972,replacing theoriginalplanthatwasestablishedJuly1,1964.Amendmentshavebeenmadefromtimetotimetoclarifywordingortoreflectchangesinregulationspertainingto registered pension plans. The pension plan text was most recently restated July1,2009.

A Pension Committee, appointed by the University, acts in an advisory capacity regardingtheadministrationoftheplanandincludesrepresentativesfromvariousemployeegroupsandretirees.

Plan assets The plan’s assets are held separate from the remaining assets of Brock University. ThatmeanstheassetsoftheplanareprotectedifBrockUniversityshouldcease to exist.

The plan’s assets are invested so that the investment earnings can help to meet the cost of the promised pensions. The plan’s assets are managed in accordance with the terms of the plan, the Statement of Investment Policies and Procedures, and applicable legislation.Investment-relatedinformationisavailableonthepensionwebsite.

Part 9: Taking care of administrative issues

RRSP (registered retirement

savings plan)isatax-deferred

vehicle for retirement savings.

RRSPs were established to

encourageCanadianstosave

for retirement by permitting

tax-deductiblecontributions

andtax-deferredgrowth

of investments.

29

Frequently asked questions

Q:Whathappenstomypensionifmymarriagebreaksdown? A:ApensionisconsideredmaritalpropertyunderOntariolaw.Youmayassignup to50%ofthepensionbenefitearnedduringthemarriagetoyourformerspouseinthe case of marriage breakdown.

TheFinancialServicesCommissionofOntario(FSCO)introducedchangestothefamily law provisions of the Pension Benefits Act(Ontario)asofJanuary1,2012.TheprocessenactedrequiresthePlanAdministrator(BrockUniversity)tocalculatethevalueofthepension(the“FamilyLawValue”)andprovideforimmediatedivisionofassetsasprescribedbyFSCO,usingtheFSCOapprovedformsthroughoutthe process.

BelowisalinktotheFSCOwebsitewithmoreinformationontheValuationandDivisionofPensionAssetsonBreakdownofaSpousalRelationshiponandafterJanuary1,2012:http://www.fsco.gov.on.ca/en/pensions/Family-Law/Pages/ marriage_breakdown.aspx

Formoreinformationonnextsteps,seethelinkbelowandclickmarriagebreakdown: http://www.brocku.ca/hr-ehs/pension-new/member-pension

AllFamilyLawValuepensionrequestsarekeptinconfidence.

A pension adjustment (PA)

isthevalueassignedto

thebenefitearnedperyear

in a pension plan. A PA

reducestheamountyoucan

contributetoaRRSPinthe

following year.

30

31

YourBrockUniversityPensionPlanisakeypartofyourretirementincome.However, itisnotintendedtobeyouronlysourceofretirementincome.Twoothersourcesofretirementincome—governmentbenefitsandpersonalsavings—arenecessarytoensureacomfortableretirement.

Canada Pension Plan WhenyouworkinoutsideofQuebec,youandyouremployercontributetotheCanadaPensionPlan(CPP).Theretirementbenefityoureceiveisbasedonseveralfactors:youryearsintheworkforce,theCPPcontributionsyoumadewhileyouwereworkingandyourearningsduringthoseyears.Ifyoursalaryisbelowtheyear’smaximumpensionableearnings(YMPE),youdonotgetamaximumCPPbenefit.Themaximummonthlybenefitin2016is$1,092.50.

YoucanstartyourCPPbenefitasearlyasage60,oraslateasage70.Yourpension willbeadjustedtoreflecttheearlierorlaterpaymentstartingdate.AfteryoubeginreceivingyourCPPpension,adjustmentsaremadeeachyeartoreflect increases in the cost of living.

Ifyoudie,yoursurvivorscanapplyforCPPsurvivorbenefits.Ifyouandyourspousemeetcertaineligibilityrequirements,yourspousecouldreceiveamonthlybenefitafteryourdeath.Yourdependentchildrenmayalsoreceiveamonthlybenefit,andaone-timelumpsumequaltosixmonthsofyourpaymentsor$2,500tocoverthecostoffuneralexpenses,whicheverisless.

Old Age Security Ifyourincomeinretirementisbelowacertainamount,youmaybeeligibleto receiveamonthlypaymentfromOldAgeSecurity(OAS)atage65.Adjustments aremadetoOASpaymentstoreflectincreasesinthecostofliving.

Aboveacertainincome,OASpaymentswillbegintobereduced.Thisreductionbeginstoapplywhenyourindividualincomeisaboveacertainlevel($72,809in2015).Paymentswillnolongerbemadewhenyourindividualincomeisatoraboveacertainlevel($118,055in2015).

Up-to-dateCPPandOASbenefitamounts,aswellascompletedescriptionsoftheseplans,areavailableontheGovernmentofCanadawebsiteat:http://www.esdc.gc.ca/en/cpp/index.page

ThewebsitealsoallowsyoutoviewyourpersonalCPPbenefitsstatementonline.

Part 10: Other sources of retirement income

Thisyear,Astridearns$60,000.HerPAisthesumofher andtheUniversity’scontributionstoherMoneyPurchase Account.Astridhadnoadditionalvoluntarycontributions.$7,489.60.

Astrid’soveralltax-shelteredamountis$10,800, or18%ofherearnings. $60,000X18%=$10,800

Thenextyear,Astridcancontribute$3,310.40to aRRSP,plusanyunusedRRSProomshecarried $10,800—$7,489.60= forwardfrompreviousyears. $3,310.40

32

Personal savings Yourownsavingswillplayanimportantpartinensuringanadequateretirementincome.FormostCanadians,accumulatingpersonalsavingsforretirementmeanscontributingtoregisteredretirementsavingsplans(RRSPs).Youcanputmoney intoapersonalorspousalRRSPandsaveonincometax,uptocertainlimits.

The Income Tax Act(Canada)setsouthowmuchyoucancontributetoyourRRSP.Thetotalyoucancontribute—yourcontributionroom—fortheyeardependsonyourearnedincomeandthedeemedvalueofpensionbenefitsyouearnedundertheBrockUniversityPensionPlanthepreviousyear.

TheCRAindicatesyourRRSPcontributionroomontheNotice of Assessment youreceivewhenyoufileyourincometaxreturn.Youcancarryforwardunusedcontributionroomtolateryears.

RRSP contribution considerations The Income Tax Act (Canada)limitshowmuchyoucancontributetoyourRRSP. YourparticipationintheBrockUniversityPensionPlanaffectstheamountyou cancontributetoyourpersonalRRSP.

Aformulaprescribedunderthe Income Tax Act(Canada)determinesthedeemedvalueofthebenefityouearnunderthepensionplanforeachyear.Theendresult ofthisformulaisapensionadjustment(PA).YourPAisreportedontheT4slipyoureceive from the University andreducestheamountofRRSPcontributionroomyouhave available in the next year.

InthecaseoftheBrockUniversityPensionPlan,thePAisequaltothetotalofplanmemberandUniversity’sannualcontributionstotheMoneyPurchaseAccount,aswellasanyadditionalvoluntarycontributionsmadebytheplanmember.

ThefollowingexampleexplainshowthePAeffectsRRSPcontributionroom.

Frequently asked questions Q:WhenshouldIapplyformyCPPpension? A:Althoughyouarenotrequiredtodoso,itisbesttoapplyatleastsixmonthsbeforeyouwantyourCPPpensiontobegin.Pleasenotethattherearelegislativerestrictionsonretroactivepayments.Adelayinapplyingcouldresultinlost benefits.Forinformation,contactServiceCanada.

Q:HowdoesCPPaffectmyBrockUniversitypension? A:YourBrockUniversitypensiondoesnotchangewhenyoubegintoreceiveCPP.

Q:WhenshouldIapplyforOAS? A:AnapplicationforOASshouldbecompletedandsubmittedsixmonthsbeforeyour65thbirthday.

33

AsthetimenearswhenyouwillleaveemploymentwiththeUniversityandyourpensionwillbegin,considertakingthefollowingsteps:

•Reviewyourannualpensionstatementtoseehowmuchpensionyouhaveearned todateandtheestimatedamountyouwillreceivewhenyourpensionbegins.

•UsetheBrockPensionEstimatortoproduceestimatestobeginyourplanning process.

•Ifyouareage62orolder,considerwhetherornotyouwanttotransferannually aportionofyourMoneyPurchaseAccounttotheShortTermAccountineach oftheyearsbeforeretirement.TheHumanResourcesDepartmentprovides more information on this option to eligible members.

•Visitaqualifiedfinancialadvisortoreviewyouroptionsandyour retirement income.

•Checkdatesandproceduresforapplicationstoreceivegovernment retirementbenefits.

•Reviewyourbeneficiarydesignationandmakesureallofyourpersonal informationisuptodate.

•Around12monthsbeforethedateyouwishtoretire,contacttheHuman ResourcesDepartmenttorequestanestimateofyourpensionamount.

•ArrangeameetingwithstaffintheHumanResourcesDepartmenttodiscussyour pensionoptionsandotherretirementitems.Ifyouhaveaspouse,itisalso beneficialforyourspousetoattendthismeeting.

•Atleastthreemonthsbeforeyourretirementdate,providetheHuman ResourcesDepartmentwithwrittennoticeofyourretirement.

•Carefullyconsiderandthenchooseyourpensionoption.Rememberthatonce yourpensionpaymentsbeginoryourfundsaretransferred,youwillnotbeable tochangeyouroption.Allcompletedpaperworkshouldbereturnedtothe HumanResourcesDepartmenttwomonthsbeforeyourretirementdate.

Part 11: Covering all the bases

34

Frequently asked questions

Q:HowdoIprovidenoticeofmyretirement? A:WrittennoticeofyourretirementshouldbeprovidedtotheHumanResourcesDepartmentatleastthreemonthsbeforeyourretirementdate.Thenoticemustincludethedateofretirementandyoursignature.

Q:DoIpaytaxesonmypensionbenefits? A:Yes.YouwillpaytaxesonyourpensionaswellasbenefitsfromCPPandOAS.However,youmaybenefitfrombeinginalowertaxbracketduringretirementthanthebracketthatcurrentlyappliestoyou.Theplan’scustodianwilldeductapplicabletaxesandprovideyouwiththeappropriatetaxformrequiredforyou tousewhenpreparingyourincometaxreturn.

Q:Isitpossibleformetohavemoretaxesdeductedfrommypension? A:Yes.Ifyouprovidethecustodianwithwritteninstruction,theamountoftaxesdeductedcanbeincreased.Thewritteninstructionshouldincludethedollaramountofextrataxesthatyouwouldlikedeductedandthemonththatyou wouldliketheincreasetobegin.

Q:WhenIretire,canIsplitmypensionincomewithmyspouseforincome taxpurposes? A:Sincethe2007taxyear,underCRArules,Canadianresidentsmaysplitcertainpensionincomewiththeirresidentspouse.Youmaybeabletojointlyelectwithyourspousetosplityoureligiblepensionincomeifyoumeetalloftherequirements.

Tosplitpensionincome,youandyourspousewillneedtomakeajointelection onFormT1032,Joint Election to Split Pension Income,andsubmititwith yourandyourspouse’sincometaxreturnsfortheyearbyyourfilingduedate. Formoreinformation,visittheCRAwebsiteat: www.cra-arc.gc.ca/tx/ndvdls/tpcs/pnsn-splt/

Thedecisiontosplityourpensionincomedoesnotinanywayaffectthepensionpayable from the plan or the income taxes withheld at the time of payment. It issimplyanelectionthatyouandyourspousemakewhenyoufileyourpersonalincometaxreturnswiththeCRAandonlyaffectstheamountoftaxthatyouoweorthetaxrefundowedyou.

35

Actuarially reduced—referstoareductionbasedonactuarialfactorstoaccountforthefactthatyouwillbereceivingthepensionforalongerperiodoftime.

Annuity—isastreamofmonthlypayments.Whenbuyinganannuityfroman insurancecompany,youarebuyingapromiseoffuturemonthlypayments.Theamountofthesepaymentswilldependonmanyfactors,includingthesizeofthelump-sumamountthatyoustartwithandtheannuitypurchaseratesatthetime ofthepurchase.Theformofannuityyouchoosewillalsoaffecttheamountof yourmonthlypayment.

Annuity factor—isafactorusedtoconverttheMoneyPurchaseAccounttoamonthlyretirementbenefit.Thefactortakesintoaccountexpectedmortalityrates,yourage,maritalstatus,formofpensionselected,andtheassumedrateofreturnthatthefundwillearngoingforward.Forexample,ifyouretireatage55, adifferentannuityfactorwillbeusedtocalculateyourpensionthanifyouretireatage65,toaccountforthefactthatyourpensionmaybepaidforalonger period of time.

Beneficiary—canbeanypersonofyourchoice.Ifyouwishtonameachildas yourbeneficiary,itisadvisabletoconsultalawyerpriortodoingso.Pension lawsrequirethat,ifyouhaveaspouse,heorshewillautomaticallytakepriorityoveranynamedbeneficiarytoreceiveyourpensionbenefits.

Best average earnings—referstotheaverageofyourpensionableearningsduringyourfivehighest-paidyearsofpensionableservice.Ifyouhavebeenemployedforlessthanfiveyears,theaverageofyouractualpensionableearningsisused.

Commuted value—referstothelump-sumpresentvalueofyourpension.Inotherwords,thecommutedvalueofyourpensionisanestimateofwhatyouwouldneedtoinvestrightnowtogiveyouthepensionyouwouldreceiveifyouweretoleaveyourbenefitsintheplan.Thecalculationisbasedonanumberoffactors,suchasinterestratesandmortalityrates,andiscarriedoutaccordingtoestablished actuarialprinciplesandmethods.

Deferred pension—isapensioninwhichpaymentsstartatafuturedate,as opposedtobeingpaidasofthefirstofthemonthfollowingthedayyoustopworking for the University.

Final average YMPE (year’s maximum pensionable earnings) — is the average oftheYMPEduringthelastfiveyear’sbeforeterminationorretirement.

Joint-and-survivor percentage—isapercentageofyourpensionthatcontinuestoyoureligiblespouse,forthespouse’slifetime,ifyoudieduringretirement.InOntario,thelawrequiresthatyourspouse’spensionbeatleast60%ofthepensionthatwasbeingpaidtoyou(unlessawaiverwassignedbyyouandyourspouse).

Part 12: Glossary

36

LIF (life income fund) — is an arrangement that provides retirement income for lifefromfundsthatoriginatefromaregisteredpensionplanorLIRA.ALIFis regulatedbytheIncome Tax Act(Canada)andgovernedbyprovincialorfederal pensionbenefitslegislation.

LIRA (locked-in retirement account)—Alocked-inretirementaccount(LIRA)issimilartoaRRSPforincometaxpurposes,butissetupwithlocked-infundsthataretransferredoutofapensionplan.Financialinstitutionsacceptinglocked-infundsmustagreetoadministerthemassetoutinthePension Benefits Act (Ontario).TherangeofinvestmentsofferedinaLIRAdependsonyourfinancialinstitution,butisoftenthesamerangeasforRRSPs.

Locked-in—referstofundsthatcannotbetakenascash.Youmustusethefundstoprovideyourselfwithretirementincome.Pensionlegislationandthetermsof theplantextdeterminewhenyourpensionbenefitsbecomelocked-in.

Financialinstitutionsacceptinglocked-infundsmustagreetoadministerthem inaccordancewithapplicablepensionregulations.Locked-inmoneydoesnot havetostayinthesameaccountuntilretirement.Youmaytransferittootherpermittedlocked-inarrangementsoruseittobuyanannuityatanytime.

Incertainsituations,pensionlegislationallowslocked-infundstobe “unlocked.”Additionalinformationaboutthismaybeavailablefromyour financialinstitutionortheFinancialServicesCommissionofOntarioat:http://www.fsco.gov.on.ca/english/pensions/

Non-locked-in—referstofundsthatcanbetakenincash.Ifyouhavenon-locked-inassetsandchoosetotakeacashrefundwhenyouleavetheplan,incometaxeswillbededucted.

Normal retirement date—isthefirstofthemonthfollowingyour65thbirthday, orontheactualdateofyour65thbirthdayifyourbirthdayfallsonthefirstof a month.

Pension adjustment (PA)—isthevalueassignedtothebenefitearnedperyear inapensionplan.APAreducestheamountyoucancontributetoaRRSPinthefollowing year.

Pensionable earnings—areyourregularannualearningsreceivedfrom the University.

Pensionable service—isthecompletedyearsandmonthsofcontinuousservicewiththeUniversityduringwhichyouareacontributortotheplan,ortheformerplan,sinceJuly1,1964.Part-timeserviceisprorated.

RRSP (registered retirement savings plan) —isatax-deferredvehiclefor retirementsavings.RRSPswereestablishedtoencourageCanadianstosavefor retirementbypermittingtax-deductiblecontributionsandtax-deferredgrowth of investments.

37

Spouse—isapersontowhomyouare: •legallymarried,providedyouarenotlivingseparateandapartfrom thatperson; •notlegallymarried,butyouandthatpersonhavecohabitedcontinuously inaconjugalrelationshipforatleastthreeyears;or •notlegallymarried,butyouandthatpersonhavecohabitedinaconjugal relationshipofsomepermanence,andarejointlythenaturaloradoptive parentsofachild,asdefinedintheFamily Law Act(Ontario).

Statement of Investment Policies and Procedures—isadocumentrequiredbylegislationforallpensionplans.Itdescribestheobjectivesandoperationoftheplan.Thestatementoutlinesinvestment-relatedpoliciesandprocedures, includingassetallocationguidelines.

Variable Annuity Fund—thefundwithintheplan’strustfundintowhichassetsfromyourMoneyPurchaseAccount,AdditionalVoluntaryContributionAccount and/orSpecialTransferAccountaretransferred,ifyouelectapensionfromoneormoreoftheseaccounts.Theassetsareinvestedaccordingtotheplan’sinvestment policiesandareusedtoprovidepensionstopensionersandtheireligiblesurvivors, accordingtotheformofpensionelectedatpensioncommencement.Thevalue ofthisfundcanchangebecauseoffactorssuchasinvestmentperformanceand mortality.Assuch,theamountofmoneyavailabletopaypensionsvariesfromyeartoyearandthisresultsintheannualincreasesordecreasestopensionamounts.

YMPE (year’s maximum pensionable earnings)—isthemaximumearningsusedtodeterminecontributionsandbenefitsundertheCanadaPensionPlan.TheYMPEisadjustedeachyear.In2016,itis$54,900.

Brock University Niagara Region 500GlenridgeAve. St. Catharines, Ont. L2S3A1 Canada

905-688-5550

www.brocku.ca