brr manual-nov2017 final - picindia.org · !7!!...

TRANSCRIPT

1

GUIDE TO BETTER DISCLOSURE

Manual On Business Responsibility Reporting

Revised Edition September 2017

2 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

The revised edition is prepared by Pradeep Narayanan from Partners in Change and Shireen Kurian from Praxis – Institute for Participatory Practices The original manual, published in December 2015, was created by Dikshit Saluja and Sunanda Poduwal from Partners in Change and Kavitha Devadas and Shireen Kurian from Praxis – Institute for Participatory Practices

This work is licensed under the Creative Commons Attribution Non-‐Commercial-‐ShareAlike 3.0 Unported License. To view a copy of the license please visit https://creativecommons.org/licenses/by-‐nc/3.0/

Guideline for citation: Guide to Better Disclosure: Manual on Business Responsibility Reporting, Partners in Change, 2017

3

Table of contents

Foreword ............................................................................................................... 4

Chapter 1 Background ...................................................................................... 5 About National Voluntary Guidelines ............................................................................. 5 About Business Responsibility Reporting ........................................................................ 5 About the Guide to Better Disclosure ............................................................................. 5 Self-‐Assessment Bands ................................................................................................... 5

Chapter 2 Section D, Questions 2 and 3: Business Responsibility Information ...... 6

Chapter 3 Section E: Principle-‐wise Performance ................................................. 9 Principle 1: Businesses should conduct and govern themselves with ethics, transparency and accountability ......................................................................................................... 9 Principle 2: Businesses should provide goods and services that are safe and contribute to sustainability throughout their life cycle .................................................................. 12 Principle 3: Businesses should promote the wellbeing of all employees. ...................... 16 Principle 4: Businesses should respect the interests of, and be responsive towards all stakeholders, especially those who are disadvantaged, vulnerable and marginalised ... 20 Principle 5: Businesses should respect and promote human rights ............................... 22 Principle 6: Business should respect, protect, and make efforts to restore the environment ................................................................................................................ 24 Principle 7: Businesses, when engaged in influencing public and regulatory policy, should do so in a responsible manner .......................................................................... 27 Principle 8: Businesses should support inclusive growth and equitable development ... 29 Principle 9: Businesses should engage with and provide value to their customers and consumers in a responsible manner ............................................................................. 33

4 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Foreword This guide is the second edition of the Guide to Better disclosure: Manual On Business Responsibility Reporting, that analysed the BRR reporting of two financial years 2012-‐13 and 2013-‐14. Over the past four years Partners in Change (PiC) has been assisting in analysing information available in Business Responsibility Reports. BRRs up to the years 2016-‐17 have been examined for the revised edition. The objective of the manual is that it will help businesses improve the quality of reporting made through their BRR disclosures, thereby keeping intact the intent of the BRR. The document attempts to act as a guidance tool for companies to gain clarity on the gaps in information by showcasing examples of other companies and their competitors. Detailed analysis of disclosure of top100listed companies in India in their Business Responsibility Reports (BRR) has revealed the gaps information companies have provided, resulting in lack of completeness while answering questions. Thus, the extent companies have disclosed has a bearing on the quality of disclosure, which is being assessed through this manual. This lack of quality can be attributed both to the nature of questions asked in the reporting format prescribed by Securities and Exchange Board of India (SEBI), as well as the companies’ efforts to bypass responding in the most appropriate manner to questions that seek answers on their commitment to being responsible. This document is an attempt at defining the intent of each of the questions in the BRR and the quality of disclosure. The guide is, based on the responses from companies to the questions in BRR in the past one financial year (2016-‐17). For each of the questions, the following have been defined: • Intent: The objective with which the question has been put to the companies. This will hopefully guide companies on how their responses should be articulated so that they are in line with the intent of asking the questions. This manual/guide has been designed keeping in mind the guide should be a self-‐assessment tool for companies to categorise their responses depending on the relevant band. The three components covered in this report are:

1. Disclosure quality: Based on responses received from companies to questions asked in BRR in the past one year, following are the four bands that have been defined to assess the quality of disclosure: Not reported, Incomplete information, Complete information and Proactive disclosure.

2. Common errors: that companies have made for each principle have been highlighted as discrepancies seen throughout responses made by companies to the specific question.

3. Recommendations: to reframing some of the BRR questions have also been made. Lastly, as observed through this analysis, it is noteworthy that companies’ responses can be classified under all bands and that complete and proactive disclosures have been made for certain questions. Pradeep Narayanan, Director, Partners in Change

5

Chapter 1 Background

About National Voluntary Guidelines Securities and Exchange Board of India (SEBI) rightly states “At a time and age when enterprises are increasingly seen as critical components of the social system, they are accountable not merely to their shareholders from a revenue and profitability perspective but also to the larger society which is also its stakeholder. Hence, adoption of responsible business practices in the interest of the social set-‐up and the environment are as vital as their financial and operational performance”. The Ministry of Corporate Affairs, Government of India, in July 2011, came out with the 'National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business'. The Guidelines have been articulated in the form of nine principles with the Core Elements to actualize each principle. They were meant to be adopted by companies as part of their business practices. The NVGs are available on the ministry website: (www.mca.gov.in)

About Business Responsibility Reporting NVGs also have a structured business responsibility (BR) reporting format requiring specified disclosures demonstrating the steps taken by companies to implement the said principles. As per clause (f) of sub regulation (2) of regulation 34 of Listing Regulations, the annual report shall contain a BR report describing the initiatives taken by the listed entity from an environmental, social and governance perspective, in the format as specified by the Board. SEBI has provided a format that is available on their website (www.sebi.gov.in).

About the Guide to Better Disclosure Partners in Change (PiC) has been assisting in analyzing information available in Business Responsibility Reports (BRRs). While the first edition of the guide used BRRs of two financial years 2012-‐13 and 2013-‐14, the revised edition makes use of the BRRs up to the years 2016-‐17. The Guide is an attempt at defining the intent of each of the questions in the BRR so that the objective with which the question has been asked from companies is clear. This will hopefully guide companies on how their responses should be articulated so that they are in line with the intent behind the questions. The Guide covers Section D, Question 2 and 3, and the entire Section E.

Self-‐Assessment Bands The guide also defines the bands of “complete response” and “proactive disclosure” so that the companies can make self-‐assessment of its responses in terms of the following bands:

Bands for BRR Disclosure Quality Index I II III IV

Not Reported Incomplete Response

Complete Response Proactive disclosure

Blank Partly answered Complete answer Disclose significant information proactively without being asked

6 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Chapter 2 Section D, Questions 2 and 3: Business Responsibility Information

Part of Annexure 1: Suggested format for Business Responsibility Report, Page 4 of 13, available on the SEBI website here(www.sebi.gov.in). Question 2: Principle-‐wise (as per NVGs) Business Responsibility policy/policies Table 1.Question 2(a): Details of compliance (Reply in Y/N)

No Questions Principles

1 2 3 4 5 6 7 8 9

1 Do you have a policy/policies for...

2 Has the policy been formulated in consultation with the relevant stakeholders?

3.1 Does the policy conform to any national /international standards?

3.2 If yes, specify? (50 words)

4.1 Has the policy being approved by the Board?

4.2 If yes, has it been signed by MD/owner/CEO/appropriate Board Director?

5 Does the company have a specified committee of the Board/ Director/Official to oversee the implementation of the policy?

6 Indicate the link for the policy to be viewed online?

7 Has the policy been formally communicated to all relevant internal and external stakeholders?

8 Does the company have in-‐house structure to implement the policy/policies?

9 Does the Company have a grievance redressal mechanism related to the policy/policies to address stakeholders’ grievances related to the policy/policies?

10 Has the company carried out independent audit/evaluation of the working of this policy by an internal or external agency?

While Table 1 lists out the questions given in the format for BRRs, the Table 2 below provides the intention of each question along with characteristics of Complete Disclosure and Proactive Disclosure.

7

Table 2. Intent behind each of the questions asked in Question 2 (a)

No Questions INTENTION

Complete Disclosure

Proactive Disclosure Whether Company

has 1 Do you have a policy/policies

for.... Any policy related to principle

Yes or No

2 Has the policy being formulated in consultation with the relevant stakeholders?

Consulted stakeholders and listed them

Yes or No

3.1 Does the policy conform to any national /international standards?

Covers all Core elements of principles

Yes or No

3.2 If yes, specify? (50 words) Details of what is not covered

Detailing future plans

4.1 Has the policy being approved by the Board?

Top Management Commitment is committed

Yes or No

4.2 If yes, has it been signed by MD/owner/CEO/appropriate Board Director?

Yes or No

5 Does the company have a specified committee of the Board/ Director/Official to oversee the implementation of the policy?

Top Management Supervision is present

Yes or No

6 Indicate the link for the policy to be viewed online?

Public disclosure of policies is important

Yes or No Reasons if not linked

7 Has the policy been formally communicated to all relevant internal and external stakeholders?

Transparency commitment ensured

Yes or No

8 Does the company have in-‐house structure to implement the policy/policies?

Commitment to practice

Yes or No Link to a note

9 Does the Company have a grievance redressal mechanism related to the policy/policies to address stakeholders’ grievances related to the policy/policies?

A responsive institution

Yes or No Link to the site

10 Has the company carried out independent audit/evaluation of the working of this policy by an internal or external agency?

A learning organization, willing to make changes

Yes or no Link to the report or specifying future plan

8 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Table 3. Question 2 (b): If answer to the question on serial number 1 against any principle, is ‘No’, please explain why: (Tick up to 2 options)

No Questions Principles

1 2 3 4 5 6 7 8 9 1 The company has not understood the

Principles

2 The company is not at a stage where it finds itself in a position to formulate and implement the policies on specified principles

3 The company does not have financial or manpower resources available for the task

4 It is planned to be done within next 6 months

5 It is planned to be done within the next 1 year

6 Any other reason (please specify)

Intent: To help companies understand that there is an urgency in implementing these guidelines; and the companies are encouraged to know the reasons at the company level why they do not have policies

Complete Response: Choose 2 out of 6 options for each principle

Proactive Response: Provide link to a note that elucidates company’s commitment to enforce these principles in an urgent way

Table 4. Question 3: Governance related to Business Responsibility

Q3 Questions Complete Response

Proactive Disclosure

(a) Indicate the frequency with which the Board of Directors, Committee of the Board or CEO assess the BR performance of the Company. (i)Within 3 months, (ii) 3-‐6 months, (iii) Annually, (iv) More than 1 year

Do not Meet or (i), (ii), (iii) or (iv)

When did they actually last meet? And reasons if there were no meetings

(b) (i) Does the Company publish a BR or a Sustainability Report?

No or Yes

(ii) What is the hyperlink for viewing this report? Link provided (iii) How frequently it is published? Detail

Does the policy conform to any national /international standards? If yes, specify? (50 words) Generally companies say yes to this even if they conform to some elements of NVG principles. They do not specify. The objective here

is to report such components of principles that companies have not yet incorporated. Indicate the link for the policy to be viewed online? The companies do not provide link to exact policy document, but to their company website.

Common Errors

9

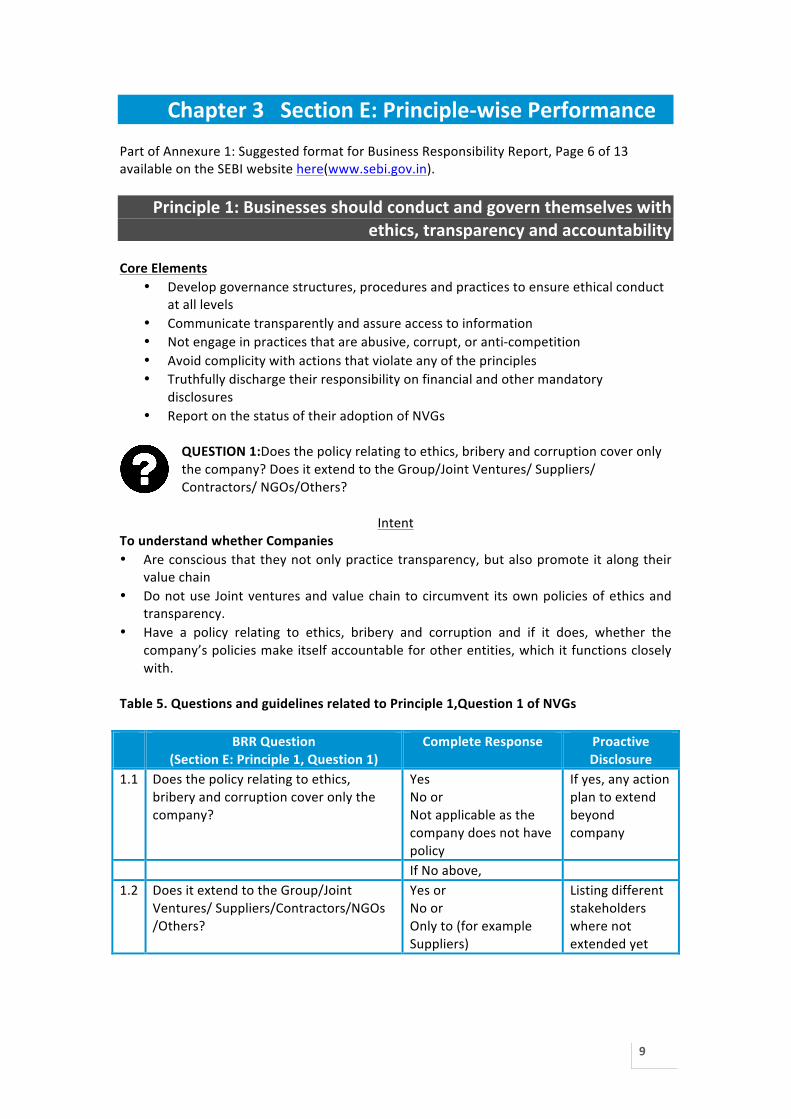

Chapter 3 Section E: Principle-‐wise Performance Part of Annexure 1: Suggested format for Business Responsibility Report, Page 6 of 13 available on the SEBI website here(www.sebi.gov.in).

Principle 1: Businesses should conduct and govern themselves with ethics, transparency and accountability

Core Elements

• Develop governance structures, procedures and practices to ensure ethical conduct at all levels

• Communicate transparently and assure access to information • Not engage in practices that are abusive, corrupt, or anti-‐competition • Avoid complicity with actions that violate any of the principles • Truthfully discharge their responsibility on financial and other mandatory

disclosures • Report on the status of their adoption of NVGs

QUESTION 1:Does the policy relating to ethics, bribery and corruption cover only the company? Does it extend to the Group/Joint Ventures/ Suppliers/ Contractors/ NGOs/Others?

Intent

To understand whether Companies • Are conscious that they not only practice transparency, but also promote it along their

value chain • Do not use Joint ventures and value chain to circumvent its own policies of ethics and

transparency. • Have a policy relating to ethics, bribery and corruption and if it does, whether the

company’s policies make itself accountable for other entities, which it functions closely with.

Table 5. Questions and guidelines related to Principle 1,Question 1 of NVGs

BRR Question

(Section E: Principle 1, Question 1) Complete Response Proactive

Disclosure 1.1 Does the policy relating to ethics,

bribery and corruption cover only the company?

Yes No or Not applicable as the company does not have policy

If yes, any action plan to extend beyond company

If No above, 1.2 Does it extend to the Group/Joint

Ventures/ Suppliers/Contractors/NGOs /Others?

Yes or No or Only to (for example Suppliers)

Listing different stakeholders where not extended yet

10 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Does it extend to the Group/Joint Ventures/ Suppliers/Contractors/NGOs /Others? Generally companies say Yes to this question, even if they extend to only one of these kinds of external stakeholders. The template

expects companies to specify only those to whom policies get extended. Companies can tick off the ones to whom the policy do not get extended and say Yes.

EXAMPLES Complete -‐ Shree Cement(Annual Report on www.shreecement.in) The policy relating to ethics, bribery and corruption is inclusive in code of conduct which is to be followed by all the employees and Directors of the Company. There are no group /joint ventures of the Company, though it has a subsidiary, but due to its non-‐operating nature, it does not practically attract any applicability of the policy. However, the Company as far as possible encourages all the associated parties including vendors, suppliers and contractors to follow the principles envisaged in the policy. Proactive – GAIL(Annual Report in Investor Zone section ofwww.gailonline.com) No, apart from company, it is also extended to GAIL Employees on secondment or deputation in any subsidiary or Joint Venture Company The Code of Conduct, CDA Rules / Standing Orders, Fraud Prevention Policy, and Whistle Blower Policy are applicable to all GAIL employees including those on secondment or deputation to the Joint Venture Companies, Subsidiaries, Government Bodies including autonomous institutions, Regulatory Authorities etc. Further, Vigilance department is taking care of the bribery and corruption related issues based on the CVC guidelines and related circulars. Scope Extended to Wholly Owned Subsidiary and Joint Ventures of GAIL where equity of GAIL is more than 50%. 'Integrity Pact' and “Fraud Prevention Policy” extend to Suppliers, contractors etc. GAIL adheres to the principles of United Nations Global Compact (UNGC) which also enlist principle on anti-‐corruption.

QUESTION 2:How many stakeholder complaints have been received in the past financial year? What percentage was satisfactorily resolved by the management? (If so, provide details thereof, in about 50 words or so.)

Intent

To understand • Whether the company has appropriate grievance and complaints redressal systems

in place. • Whether company is committed to addressing complaints relating to ethics and

corruption. • Whether the company reviews the information in the system to inform its wider

practices

Table 6: Questions and Guidelines related to Principle 1, Question 2 of NVGs BRR Section E Principle1,

Question 2 Complete Response Proactive

Disclosure 2.1 How many stakeholder complaints

have been received in the past financial year?

0 or 50 or 100 (as the number may be)

2.2 What percentage was satisfactorily resolved by the management?

If 10 out of 50 mentioned above is resolved, then 20% will be the

Common Errors

11

BRR Section E Principle1, Question 2

Complete Response Proactive Disclosure

answer. 2.3 If so, provide details thereof, in

about 50 words or so. For example, There were X unresolved complaints of last year, which were resolved this year. Nature of complaints.

Disaggregated numbers on the kinds of complaints.

Resolution of stakeholder complaints by management and details thereof In many cases, the companies just say Zero. In that case, in details, it is important that companies specify in 50 words, with examples,

how they know their system is functional. Companies often do not provide descriptive details about complaints.

EXAMPLES Complete – GMR Infrastructure Limited(Business Responsibility report on www.investor.gmrgroup.in) During the year under review, a total of 23 Whistleblower Complaints were received, of which 4 of were dropped, being frivolous in nature. Inquiries were conducted in the remaining 19 complaints, of which allegations were proved in 13 cases. Appropriate action was taken in all the above 13 enquiries. The balance 6 cases were not proved due to lack of evidence. None of the 13 cases involve fraud having serious financial implication on the Company. Proactive – Canara Bank(Annual Report on www.canarabank.com) Shareholders Complaints: The Bank received 738 representations / grievances from Shareholders during 2016-‐17 and all the grievances have been resolved satisfactorily. Majority of the representations is on account of non-‐receipt of Dividend Warrants. This is due to non-‐updation of the addresses by the concerned shareholders. While resolving the grievances, the Bank has been taking steps to update their addresses, bank details, ECS Mandate (by providing the necessary forms) so as to avoid recurrence of such instances. 66977 (including 39293 complaints related to ATMs) complaints were received from customers of which 65362 (including 38507 complaints related to ATMs) were resolved. The complaints received during the year are more compared to previous year due to demonetization exercise. Customer Complaints: During 2016-‐17, the Bank received 66977 complaints and 97.59% of the complaints were satisfactorily redressed. The Bank is taking several measures to improve customer service by bringing in diversified products/services, updated technology, staff training and responding to customer’s queries and redressal of customer complaints.

Additional recommended questions for Principle 1 of BRR framework

• What are the ways by which the company assures that its partners, vendors and such organisations adhere to the company’s policies?

• What is the total number of confirmed incidents in which employees were dismissed or disciplined for corruption?

• What is the total number of confirmed incidents when contracts with business partners were terminated or not renewed due to violations related to corruption?

• What are the public legal cases regarding corruption brought against the organisation or its employees during the reporting period and the outcomes of such cases?

Common Errors

12 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Principle 2: Businesses should provide goods and services that are safe and contribute to sustainability throughout their life cycle

Businesses should • Assure safety and optimal resource use over the life-‐cycle of the product – from design

to disposal – and ensure that everyone connected with it-‐ designers, producers, value chain members, customers and recyclers are aware of their responsibilities.

• Raise the consumer's awareness of their rights through education, product labelling, appropriate and helpful marketing communication, full details of contents and composition and promotion of safe usage and disposal of their products and services.

• ensure that the manufacturing processes and technologies required to produce it are resource efficient and sustainable.

• Regularly review and improve upon the process of new technology development, deployment and commercialization, incorporating social, ethical, and environmental considerations.

• Recognize and respect the rights of people who may be owners of traditional knowledge, and other forms of intellectual property.

• Should promote sustainable consumption, including recycling of resources. Table 7. Questions and guidelines related to Principle 2,Questions 1, 2of NVGs

Question BRR Section E Principle2, Questions 1,2

Complete Response

Proactive Disclosure

1 List up to 3 of your products or services whose design has incorporated social or environmental concerns, risks and/or opportunities.

All 3 products named. Or says They do not collect information

If not listed, provides an action plan for future

2 For each such product, provide the following details in respect of resource use (energy, water, raw material etc.) per unit of product (optional):

2.1 i. Reduction during sourcing/production/ distribution achieved since the previous year throughout the value chain?

Product 1 Product 2 Product 3

Details provided

2.2 ii. Reduction during usage by consumers (energy, water) has been achieved since the previous year?

Product 1 Product 2 Product 3

Details provided

Intent

These two questions are primarily for Business to report concrete and specific details about their efforts towards sustainable, optimal and efficient resource use. Further, the objective is also for businesses to actually measure the saving that it is making while deigning the product and processes.

13

The examples could involve any part of product development process, that is the entire life-‐cycle of the product, including post-‐development disposal. Further, it also encourages businesses to involve even such design that address “social concerns”. To that extent, the companies can also present their own indicators of measuring impact. The suggestion in terms of indicators such as energy, water, raw material is an optional example. Companies can use any indicator as example-‐ provided it does measure.

Listing of 3 products or services whose design has incorporated social or environmental concerns, risks and/or opportunities The companies just list products without providing any “measurable’ indicators. They provide generic measurements.

EXAMPLES

Complete – Aditya Birla Group (Annual Report on www.adityabirla.com) The Company is committed to align its business strategy with the Aditya Birla Group’s sustainability vision. For its 3 major products, i.e., Viscose Staple Fibre, Rayon Grade Pulp and Chemicals, the Company has developed an Environment Management Program with the novel two-‐pronged approach of Environment Protection and Resource Conservation. The Company understands its obligations relating to social and environmental concerns, risks and opportunities. Accordingly, the Company has devised the manufacturing processes of these products and systems, factoring social and environmental concerns. The Company responds to Climate Change Challenge by new product development, increasing absorption by securing availability and overcoming technical constraints; improving energy efficiency; transport and logistics optimisation, waste-‐to-‐energy recovery and emissions reduction. Proactive – Cummins India Limited (Annual Report on www.cumminsindia.com) During the year, the Company got the opportunity to work on projects addressing social or environmental concerns. Some of the projects are as listed below: -‐ 1. Development of 25 kWegenset using Rice Husk (Biomass): To address remote rural electrification requirements, the Company had developed a 25 kWegenset which uses locally available agricultural waste viz. rice husk (renewable) for meeting remote rural electrification requirements. This genset has been successfully running for over 1,000 hours for rural electrification at the field site in Bihar. 2. Development of 40 kWegenset using Wood (Biomass): To address remote rural electrification requirements, the Company uses locally available agricultural waste viz. wood waste (renewable) for meeting remote rural electrification requirements. The Company has commissioned a producer gas generator set at the Phaltan Mid-‐Range Upfit Center at the Cummins Megasite. 3. Development of 400 kWegenset using Wood (Biomass): To address use of renewable energy source for power generation, the Company uses locally available agro waste viz. wood waste (renewable) for electrical power generation. 243 56th Annual Report 2016-‐17 Two lean burn producer gas generator sets are running successfully for 3,000 hours, in grid parallel at Sattur, Tamil Nadu.

Table 8. Questions and guidelines related to Principle 2,Question 3 of NVGs

BRR Section E Principle2, Question 3

Complete response Proactive disclosure

3.1 Does the company have procedures in place for sustainable sourcing (including transportation)?

No or Yes or Yes, excluding transportation

No but we have plan to come out with procedure by….

Common Errors

14 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

BRR Section E Principle2, Question 3

Complete response Proactive disclosure

3.2 If yes, what percentage of your inputs was sourced sustainably?

Not measured, only approximate If measured, the (number)

If not measured, state the future plan

3.3 Also, provide details thereof, in about 50 words or so.

If percentage is 50%, what exactly are the denominator and numerator. And give some examples

Provide weblinks to a note on this.

Intent

To understand if the company has gone beyond making policy commitments, that is, has created procedures and systems in place for sustainable sourcing of inputs required for its product or services. Incidentally, transportation is provided as an example as it involves all sectors and any intervention on that can impact carbon footprints. Further, it is also expected from the companies to actually measure their efforts so that there is a continuous effort on increasing their sustainable sourcing efforts.

Percentage of inputs sourced sustainably The companies provide procedures rather than the percentage of sustainable sourcing on inputs

EXAMPLE

Complete -‐ Dabur (Annual Report on www.dabur.com) For procuring rare species of herbs and medicinal plants, which are essential ingredients for making our products, we follow a “bush-‐to-‐brand” approach and work directly with small and marginal farmers. This allows us to revive these endangered species and also promote sustainable agricultural practices in our supply chain. Inputs procured through this channel constituted around 5-‐10% of our total inputs purchased (by value and volume both).

Table 9. Questions and guidelines related to Principle 2,Question 4of NVGs

Intent

To understand if the company supports local and small producers; and local communities; it asks specifically about procurement of goods and services. However, the steps may include efforts done to create a facilitating environment for this procurement.

BRR Section E Principle2, Question 4

Complete Disclosure

Proactive Disclosure

4.1 Has the company taken any steps to procure goods and services from local & small producers, including communities surrounding their place of work?

No or Yes If no, provides a time frame by which this will be done

4.2 If yes, what steps have been taken to improve their capacity and capability of local and small vendors?

Details out the steps

Information on outcome as well as providing weblink to materials

Common Errors

15

EXAMPLE Complete: Indian Oil Corporation Limited (Annual Report on www.iocl.com) Yes. As per the Public Procurement Policy of Govt. of India for Micro and Small Enterprises (MSE), purchase preference is given to MSEs and PSUs. All efforts are made to procure items specified for procurement from MSEs. The MSEs and National Small Industries Corporation (NSIC) are exempted from payment of tender fees / earnest money deposit. As against the target of procurement of 20% from MSEs, the actual procurement during the year was 38.65%. Efforts are also being made to promote indigenisation of raw materials, which, at present, are imported at Company’s Petrochemical plants. Indian Oil also strives to maximize the services of local communities in carrying out operations across its value chain.

Table 10. Questions and guidelines related to Principle 2,Question 5of NVGs

Intent

To understand whether the company has taken steps to create any system for recycling of waste generated during the production processes and post consumption or usage

EXAMPLE Complete – Steel Authority India Limited (Annual Report on www.sail.co.in) SAIL believes in the Policy of 4Rs (reduce, recover, recycle and reuse) across all our operations. A large quantity of wastes and by-‐products like slag, dust, sludge, used firebricks, etc. is generated during the iron and steel making process. Slag, which accounts for a majority of by-‐products, is utilized internally and also sold to external agencies. Blast Furnace slag is used for cement making while BOF slag is used internally for sinter making and also as material for road base, internal rail track ballast, etc. During the year 2016-‐17, 89.47% of BF slag and 71.24% of BOF slag were utilised. Other wastes like, BF flue dust, mill scale, lime/dolo fines and refractory wastes are also used internally and sold to outside agencies. The belief of reuse and recycle is firmly embedded in the organizational approach of SAIL and there have been several initiatives to maximise the utilisation of solid waste generated at various operations. During 2016-‐17, 24.72% solid wastes were internally re-‐cycled out of total utilisation of 83.20% of solid wastes. Moreover, by-‐product gases like Coke Oven gas, BF gas and LD gas are used as fuels at the different shops of the Plants.

BRR Section E Principle2, Question 5 Complete Disclosure Proactive

disclosure 5.1 Does the company have a

mechanism to recycle products and waste?

No or Yes If no, provides details about a timeline

5.2 If yes what is the percentage of recycling of products and waste separately

In percentage If not measured, provide a timeline

5.3 Also, provide details thereof, in about 50 words or so.

What kinds of wastes are recycled and what not; Challenges

Provide weblink.

16 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Principle 3: Businesses should promote the wellbeing of all employees Core Principles

1. Businesses should respect the right to freedom of association, participation, collective bargaining, and provide access to appropriate grievance redressal mechanisms.

2. Businesses should provide and maintain equal opportunities at the time of recruitment as well as during the course of employment irrespective of caste, creed, gender, race, religion, disability or sexual orientation.

3. Businesses should not use child labour, forced labour or any form of involuntary labour, paid or unpaid.

4. Businesses should take cognizance of the work-‐life balance of its employees, especially that of women.

5. Businesses should provide facilities for the wellbeing of its employees including those with special needs. They should ensure timely payment of fair living wages to meet basic needs and economic security of the employees.

6. Businesses should provide a workplace environment that is safe, hygienic humane, and which upholds the dignity of the employees. Business should communicate this provision to their employees and train them on a regular basis.

7. Businesses should ensure continuous skill and competence upgrading of all employees by providing access to necessary learning opportunities, on an equal and non-‐discriminatory basis. They should promote employee morale and career development through enlightened human resource interventions.

8. Businesses should create systems and practices to ensure a harassment free workplace where employees feel safe and secure in discharging their responsibilities.

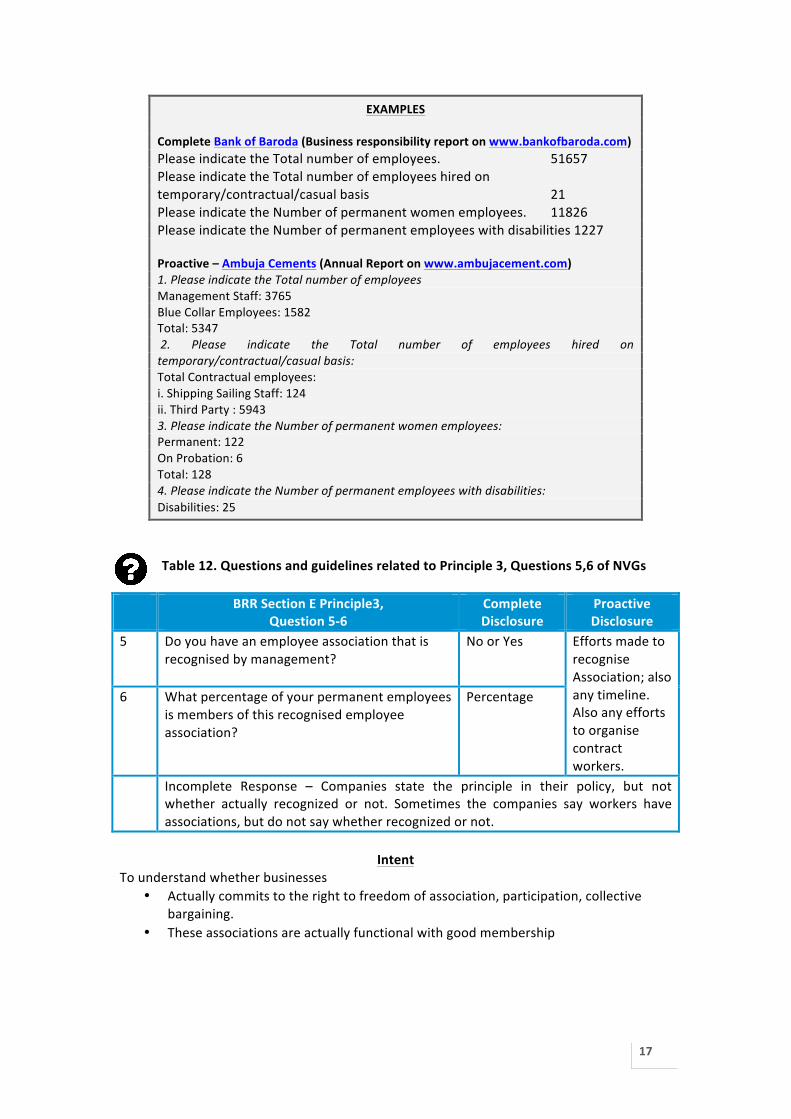

Table 11. Questions and guidelines related to Principle 3,Questions 1-‐4of NVGs

Question BRR Section E Principle3,Questions1-‐4

Complete response

Proactive disclosure

1 Please indicate the total number of employees. Number provided

2 Please indicate the total number of employees hired on temporary/contractual/casual basis

Number provided

Disaggegate across levels

3 Please indicate the number of permanent women employees.

Number provided

Disaggregate across levels

4 Please indicate the number of permanent employees with disabilities

Number provided

Disaggregate across levels and other social categories as well

Intent

To understand whether businesses • Largely commit to permanent nature of employment to ensure social security to its

employees • Commit to diveristy in work place, especially from the lens of gender and disabilities

17

EXAMPLES Complete Bank of Baroda (Business responsibility report on www.bankofbaroda.com) Please indicate the Total number of employees. 51657 Please indicate the Total number of employees hired on temporary/contractual/casual basis 21 Please indicate the Number of permanent women employees. 11826 Please indicate the Number of permanent employees with disabilities 1227 Proactive – Ambuja Cements (Annual Report on www.ambujacement.com) 1. Please indicate the Total number of employees Management Staff: 3765 Blue Collar Employees: 1582 Total: 5347 2. Please indicate the Total number of employees hired on temporary/contractual/casual basis: Total Contractual employees: i. Shipping Sailing Staff: 124 ii. Third Party : 5943 3. Please indicate the Number of permanent women employees: Permanent: 122 On Probation: 6 Total: 128 4. Please indicate the Number of permanent employees with disabilities: Disabilities: 25

Table 12. Questions and guidelines related to Principle 3, Questions 5,6 of NVGs

BRR Section E Principle3, Question 5-‐6

Complete Disclosure

Proactive Disclosure

5 Do you have an employee association that is recognised by management?

No or Yes

Efforts made to recognise Association; also any timeline. Also any efforts to organise contract workers.

6 What percentage of your permanent employees is members of this recognised employee association?

Percentage

Incomplete Response – Companies state the principle in their policy, but not whether actually recognized or not. Sometimes the companies say workers have associations, but do not say whether recognized or not.

Intent

To understand whether businesses • Actually commits to the right to freedom of association, participation, collective

bargaining. • These associations are actually functional with good membership

18 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

EXAMPLES Complete -‐ IDFC Bank(Annual Report on www.ifdc.com) No Proactive -‐ ONGC (www.ongcindia.com) Yes. A. Executive Cadre: The Association of Scientific and Technical Officers (ASTO) has been recognized to represent the issues related to the officers. B. Non-‐Executive Cadre: Twelve recognized unions as under: 1. ONGC (BOP) Karmachari Sanghatana, Mumbai; 2. ONGC Workmens’ Association, Kolkata; 3. Petroleum Employees Union, Chennai; 4. Petroleum Employees Union, Karaikal; 5. Petroleum Employees Union, Rajahmundry; 6. Petroleum Mazdoor Sangh, Ahmedabad; 7. ONGC Mazdoor Sangh, Ankleshwar; 8. ONGC Employees Mazdoor Sabha, Baroda; 9. ONGC Purbanchal Employees’ Association Sivasagar; 10. National Union of ONGC Employees, Dehradun; 11. ONGC Workers Union, Agartala; 12. Trade Union of ONGC Workers, Silchar. Besides above All India SC/ST Employees Welfare Association and All India OBC/ MOBC Employees Welfare Association are recognized by the Company. Complete –Indian Oil Corporation Limited (www.iocl.com) 90% of the employees (both non-‐executives and executives) are members of the recognised unions or officers’ association. Proactive -‐ Hindustan Unilever Limted (HUL) There are 105 employee associations across your Company. Nearly 11,000 permanent employees are members of these associations. There are over 119 permanent female blue-‐collar employees and over 21 permanent blue-‐collar employees with disabilities in your Company’s factories. During the last year, your Company entered into long-‐term settlements with around 4,341 employees covering 12 factories across India.

Table 13. Questions and guidelines related to Principle 3,Question 7 of NVGs

BRR Section E Principle3,Question 7

Complete Disclosure Proactive Disclosure

7 Category Number of complaints received during the year (201x-‐1y)

Number of complaints pending as on 31 March 1Y

Insights on nature of complaints and stakeholders. Also, if data not available, provide a timeframe by when will be provided.

7.1 Child labour (in figure) or not collected

(in figure)

7.2 Forced labour/Involuntary labour

(in figure) or not collected

(in figure)

7.3 Sexual harassment (in figure) Incomplete disclosure: Systems are explained. Principles stated. But needed details are

not provided

19

Intent To understand whether Businesses

• Are committed to put in place systems and mechanisms to address the various labour-‐related issues

• Have functional systems of grievance redressal on these issues

Table 14. Questions and guidelines related to Principle 3, Question 8 of NVGs

BRR Section E Principle3, Question 8

8 What percentage of your under mentioned employees were given safety & skill up-‐gradation training in the last year?

Complete Disclosure Proactive Disclosure

Permanent Employees

Permanent women

Casual/Temp EWD Additional insights are provided. Outcomes are detailed out. If not, plan is provided

Category of training

Total % Total % Total % T %

8.1 Safety 8.2 Skill

upgradation

All the above details be given in number. If data is not there, just say Data not available Incomplete disclosure: instead of number, they provide details about their commitments and systems

Intent To understand whether Businesses

• commit to provide a workplace environment that is safe, hygienic, humane, and which upholds the dignity of employees.

• commit to ensure continuous skill and competence upgrading of all employees by providing access to necessary learning opportunities,

• Commit to ensure an equal and non-‐discriminatory access in its training programme.

EXAMPLES Complete – Bank of India (Annual Report on http://www.bankofindia.co.in) (a) Permanent Employees -‐ 38 % (b) Permanent Women employees -‐ 35 % (c) Casual/Temporary/Contractual Employees – Nil (d) Employees with Disabilities -‐ 32 %

Additional Questions for Principle 3

Total number of complaints unresolved for more than a year. Do you have a system of calculating living wage for all employees, especially the lowest level? How many accidents related to work has taken place in the year? How many sub-‐contractors have you employed? How many workers work for your business through sub-‐contracting

20 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Principle 4: Businesses should respect the interests of, and be responsive towards all stakeholders, especially those who are

disadvantaged, vulnerable and marginalised Core Principles

• Businesses should systematically identify their stakeholders, understand their concerns, define purpose and scope of engagement, and commit to engaging with them

• Businesses should acknowledge, assume responsibility and be transparent about the impact of their policies, decisions, product & services and associated operations on the stakeholders

• Businesses should give special attention to stakeholders in areas that are underdeveloped.

• Businesses should resolve differences with stakeholders in a just, fair and equitable manner

Intent

To understand whether the Businesses • Have systems and processes to engage with stakeholders, especially those who are

vulnerable. • Have also made some activity plans based on the outcome of these engagements,

especially with marginalized

Table 15. Questions and guidelines related to Principle 4,Questions 1-‐3 of NVGs

BRR Section E Principle 4, Question 1-‐3

Complete Response Proactive Disclosure Response Details in

50 words

1 Has the company mapped its internal and external stakeholders?

Yes/No Detail periodicity

2 Out of the above, has the company identified the disadvantaged, vulnerable & marginalized stakeholders?

Yes/No If yes, who are they?

List all stakeholders; and then list marginalised

3 Are there any special initiatives taken by the company to engage with the disadvantaged, vulnerable and marginalized stakeholders.

Yes/no If yes, what are they?

Weblink to assessment reports

Incomplete disclosure: Provide principles and processes but no details on stakeholder mapping per se.

Intent

To understand whether businesses: • Identify and map their internal and external stakeholders, which may assist the

company in being accountable and responsive to their interests and concerns. • Are cognizant of varying levels of impacts of the company on its different

stakeholders and vice versa, and among the stakeholders, clearly mapped those who are disadvantaged, vulnerable or marginalised.

• Have any special initiatives for disadvantaged, vulnerable and marginalised stakeholders. Such initiatives should be over and above community development

21

projects and should address concerns and complaints raised by the said stakeholders.

EXAMPLES

Complete -‐ Ambuja Cement (Annual Report on www.ambujacement.com) The company has further identified the disadvantaged, vulnerable and marginalised stakeholders, namely the communities around its manufacturing sites and its workers/contractual workers and truck drivers. Disabled children and youth emerged as a separate group and hence are catered through education and skill development program. Complete-‐ Indian Oil Corporation Limited (Annual Report on www.iocl.com) Yes, special initiatives are taken up under Corporate Social Responsibility for upliftment of the disadvantaged, vulnerable and marginalised sections of the society. The details of such activities are available at the Company’s website. Indian Oil also provides dealerships to this section of the society as per Government of India guidelines. Indian Oil scrupulously follows the Presidential Directives and guidelines issued by Government of India regarding reservation in services for SC/ ST/ OBC/PWD (Persons with Disabilities)/ Ex-‐servicemen, etc. to promote inclusive growth. Proactive –Oil and Natural Gas Corporation (Annual Report onwww.ongcindia.com) The CSR policy of the Company covers CSR Projects / Programmes as listed under Schedule-‐VII of the Act, preferably towards the benefit of marginalized, disadvantaged, poor and deprived sections of the community and the environment. This way the ultimate objective is to reach the bottom of the pyramid in our demographic strata and touch their lives in a positive manner. Thus while the Company is engaged in serving the society through various welfare measures since its inception, it has now adopted a more structured approach in undertaking such welfare measures. Many projects related to infrastructure development, education.

Additional Questions Principle 4

Has there been a scenario where the company acknowledged and assumed responsibility about the impact of their policies, decisions, product & services and associated operations on the stakeholders? Please provide details in 50 words. Please provide one example where businesses should resolved differences with stakeholders in a just, fair and equitable manner?

22 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Principle 5: Businesses should respect and promote human rights Core Principles

1. Businesses should understand the human rights content of the Constitution of India, national laws and policies and the content of International Bill of Human Rights. Businesses should appreciate that human rights are inherent, universal, indivisible and interdependent in nature.

2. Businesses should integrate respect for human rights in management systems, in particular through assessing and managing human rights impacts of operations, and ensuring all individuals impacted by the business have access to grievance mechanisms.

3. Businesses should recognize and respect the human rights of all relevant stakeholders and groups within and beyond the workplace, including that of communities, consumers and vulnerable and marginalized groups.

4. Businesses should, within their sphere of influence, promote the awareness and realization of human rights across their value chain.

5. Businesses should not be complicit with human rights abuses by a third party.

Intent To understand whether Businesses

• Have policies on human rights. • Have committed not to be complicit with humna rights abuses by a third party • Have created systems and mechanisms to detect and address human rights abuses

Table 16. Questions and guidelines related to Principle 5,Questions 1-‐2of NVGs

Section E Principle 5, Question 1,2 Complete response Proactive

disclosure 1 Does the policy of the company on human rights cover

only the company or extend to the Group/Joint Ventures/Suppliers/ Contractors/NGOs/Others?

Yes/No Weblink provided

2 How many stakeholder complaints have been received in the past financial year and what percent was satisfactorily resolved by the management?

Category of stakeholders Number of complaints received during the year

Number of these complaints resolved by end March

Additional insights provided. Nature of complaints provided 2a Workers/Employees

2b Vendor/Contractors 2c NGOs 2d Communities 2e (Company may add…) Incomplete response: Exact figures are not provided. Only principles get stated.

23

EXAMPLES Complete -‐ Ambuja Cements (www.ambujacement.com) The Company does not have any policy on Human Rights for the time being. However, issues, if any, are covered by national and local laws. The company also refers to the guidelines provided by the parent company Lafarge Holcim and uses it as a tool for assessment of Human Rights impacts at its plants. Complete: Bharat Heavy Electricals Limited (www.bhel.com) No instance of Human Rights abuse has been reported in the Company. Proactive: Bank of Baroda (Business responsibility report on www.bankofbaroda.com) The Bank’s various policies protecting the Human Rights, directly or indirectly, cover only the operations of the Bank and do not extend to its subsidiaries etc. The Bank is well conscious of the fact that all human beings are free and equal, and that the basic human rights of individuals must be respected. The Bank follows such policies/practices that, directly or indirectly, do not discriminate on the basis of national origin, citizenship, color, race, belief, religion, ancestry, marital status, gender, disabilities, age, sexual orientation, place of birth, social status, or any other basis prohibited by the law. The Bank understands well the Human Rights content of the Constitution of India and other international laws on Human Rights at the work place. The Bank respects the freedom of associations and the right to collective bargaining. Prevention of Sexual Harassment The Bank prohibits sexual harassment at the work place. In the Service conditions, there are clauses exclusively for prevention of sexual harassment at workplace. Accordingly, for addressing issues related specifically to women employees in work places, the Bank has appointed Chief Lady Liaison Officer in the rank of Deputy General Manager at the Corporate Office level. Further, in compliance of the recent guidelines received from the Govt. of India, Bank has constituted Internal Complaints Committee at every Zone headed by a Lady Liaison Officer and comprising of -‐1-‐ Officer, -‐1-‐ Clerk and -‐1-‐ external member from an NGO committed to the cause of women. Bank has also appointed a Lady Liaison Officer at every Region. Dissemination of Information to public through the Bank’s web site: The Bank places up-‐to-‐date information about its Products/ Services/ Facilities available to public/any other information, which can be disclosed, in public domain. Being a listed company, the Bank displays its financial results in the public domain for information to the public. Bank of Baroda is a Public Authority, as per definition of Public Authority in the Right to Information Act, 2005, and, thus, is under obligation to provide the information to members of public. Redressal of Complaints The Bank has taken several measures to strengthen the customer complaint redressal machinery for fast disposal of customer complaints. One of such measures being Standardized Public Grievances Redressal System (SPGRS), a web based Online customer complaint redressal module. The Bank has appointed an Internal Ombudsman to further boost the quality of customer service and to ensure that there is undivided attention to resolution of customer complaints.

Additional Questions Principle 5 What are the steps taken by the company to promote the awareness and realisation of human rights across the value chain? Has the company organised human rights due diligence study across its operations, including the value chain? If yes, provide link to the study report.

24 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Principle 6: Business should respect, protect, and make efforts to restore the environment

Core Principles

• Businesses should utilize natural and manmade resources in an optimal and responsible manner and ensure the sustainability of resources by reducing, reusing, recycling and managing waste.

• Businesses should take measures to check and prevent pollution. They should assess the environmental damage and bear the cost of pollution abatement with due regard to public interest.

• Businesses should ensure that benefits arising out of access and commercialization of biological and other natural resources and associated traditional knowledge are shared equitably.

• Businesses should continuously seek to improve their environmental performance by adopting cleaner production methods, promoting use of energy efficient and environment friendly technologies and use of renewable energy.

• Businesses should develop Environment Management Systems (EMS) and contingency plans and processes that help them in preventing, mitigating and controlling environmental damages and disasters, which may be caused due to their operations or that of a member of its value chain.

• Businesses should report their environmental performance, including the assessment of potential environmental risks associated with their operations, to the stakeholders in a fair and transparent manner.

• Businesses should proactively persuade and support its value chain to adopt this principle.

Intent To understand whether Businesses

• Take responsibility of addressing environment concerns across its value chain. • Have adopted and is implementing any strategies to address global

environmental issues and if it makes information related to such activities public. • Have a system and practice of identifying and assessing potential environmental

risks associated with its own business processes internally or those associated with its supply chain.

Table 17. Questions and guidelines related to Principle 6,Questions 1-‐3 of NVGs

Section E Principle 6, Question 1-‐3 Complete Response

Proactive Disclosure

1 Does the policy related to Principle 6 cover only the company or extends to the Group/Joint Ventures/Suppliers/Contractors/NGOs/others

Yes or No Yes extends to A,B,C and not to D,E,F

2 Does the company have strategies/ initiatives to address global environmental issues such as climate change, global warming, etc?

Yes or No Yes, but it does not cover certain areas like

3 If yes, please give hyperlink for webpage etc.

Link provided

Details out systems and mechanisms

Incomplete response: Instead of saying yes or no, companies come out with philosophical statement

25

Table 18. Questions and guidelines related to Principle 6,Questions 4,5 of NVGs

Section E Principle 6, Question 4,5

Complete Response Proactive response

4.1 Does the company have any project related to Clean Development Mechanism?

No or Yes

4.2 If so, provide details thereof, in about 50 words or so.

If yes, detail about the project

If no, provides future action plan

4.3 if Yes, whether any environmental compliance report is filed?

Yes or No If yes or no, provides details about outcomes of compliance report

5.1 Has the company undertaken any other initiatives on –clean technology, energy efficiency, renewable energy, etc?

Yes or No If yes, provides details on challenges and successes

5.2 If yes, please give hyperlink for web page etc.

Link provided If No above, provides the action plan

Intent

To understand company’s commitment towards • Clean Development Mechanism; and whether periodic compliance reports relating

to the same are being filed • Clean and efficient energy

EXAMPLES

Complete -‐ Ambuja Cement (Sustainability Policy on www.ambujacement.com) Yes. The Company has a documented Sustainability Policy which is available on our website. The policy enshrines commitment for climate change mitigation. Apart from this, we also have an updated Climate Change Mitigation Policy. The Company measures & reports its carbon emissions as per the protocol of Cement Sustainability Initiative [CSI] of the World Business Council on Sustainable Development. The Company proactively discloses its carbon emissions annually in the Carbon Disclosure Project [CDP]. Ambuja continued its good performance in CDP 2016. Scope-‐3 carbon emissions from all our five integrated plants was verified by an independent third party. Further, we also keep our stakeholders informed on our carbon performance through our annual GRI based Sustainability Report. The company’s website also contains information on our Sustainability endeavors [see www.ambujacement.com/Sustainability]. The Company has strategies in place to address global warming and to ensure a low carbon growth path for our operations. Proactive: ONGC (Annual Report on www.ongcindia.com) Yes. The Company commenced its Clean Development Mechanism (CDM) journey in 2006. Currently, ONGC has 15 registered CDM projects with United Nations Framework Convention on Climate Change (UNFCCC) that yield (potential) Certified Emissions Reductions (CER) approx. 2.1 million yearly. The registered CDM projects are as under: http://www.ongcindia.com/wps/wcm/PDF/AnnualReport/AR201617.pdf

26 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Table 19. Questions and guidelines related to Principle 6,Questions 6,7 of NVGs

Section E Principle 6, Questions 6,7 of NVGs

Complete Response Proactive response

6 Are the Emissions/Waste generated by the company within the permissible limits given by CPCB/SPCB for the financial year being reported?

Yes or No Gives details of when it has gone beyond permissible limits and an action plan

7 Number of show cause/ legal notices received from CPCB/SPCB which are pending (i.e. not resolved to satisfaction) as on end of Financial Year.

Provides a number here

Gives details why certain notices are pending or challenges they faced in addressing the notices successfully

Intent

To understand whether businesses • Report on its adherence to the standard emissions/waste generation limits as set by

regulatory bodies. • Commit to addressing the issues raised by Central Pollution Control Board/State

Pollution Control Board and resolves them satisfactorily and on priority basis.

EXAMPLE Complete -‐ NMDC Yes. All emissions & wastes generated by NMDC are monitored on a regular basis and are within permissible limits as specified by CPCB/SPCB. Also, the returns are filed regularly to the statutory authorities as per requirement. To know more about the initiatives, please see the hyperlink given below: https://www.nmdc.co.in/EnvironmentalMgmt.aspx

27

Principle 7: Businesses, when engaged in influencing public and regulatory policy, should do so in a responsible manner

Core Elements

§ Businesses, while pursuing policy advocacy, must ensure that their advocacy positions are consistent with the Principles and Core Elements contained in these Guidelines.

§ To the extent possible, businesses should utilize the trade and industry chambers and associations and other such collective platforms to undertake such policy advocacy. QUESTION 1 Is your company a member of any trade and chamber or association? If Yes, Name only those major ones that your business deals with:

Intent To find out the various spaces, platforms and forums the company is part of where it can play an influential role in advocating for public good and changes in regulatory policy.

QUESTION 2 Have you advocated/lobbied through above associations for the advancement or improvement of public good? Yes/No. If yes specify the broad areas (Governance and Administration, Economic Reforms, Inclusive Development Policies, Energy security, Water, Food Security, Sustainable

Business Principles, Others)

Intent To find out whether the businesses have advocated for public good through any of the mentioned platforms and channels and the areas businesses are contributing to Table 20. Questions and guidelines related to Principle 7,Questions 1,2 of NVGs Section E Principle 7, Questions 1,2 Complete

Response Proactive response

1.1 Is your company a member of any trade and chamber or association?

Yes or No

1.2 If Yes, Name only those major ones that your business deals with:

Names of the associations

2.1 Have you advocated/lobbied through above associations for the advancement or improvement of public good? Yes/No;

Yes or No

2.2 If yes specify the broad areas (Governance and Administration, Economic Reforms, Inclusive Development Policies, Energy security, Water, Food Security, Sustainable Business Principles, Others)

Specify the same Provide details about the lobbying done, with outcomes

28 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

EXAMPLES Complete – Sun Pharma (Business Responsibility report at www.sunpharma.com) As we are focused on making affordable medicines accessible, we share our invaluable experience and leverage our leadership position to provide incisive insights and detailed inputs to key decision makers in planning better policies for the patients. Along with that, we also learn from the best practices of others in the industry. While we collaborate with various trade and industry associations, we are also members of: • Indian Drug Manufacturing Association • Indian Pharmaceutical Alliance • Bombay Chamber of Commerce and Industry • Confederation of Indian Industry • Pharmaceuticals Export Promotion Council of India • The Associated Chambers of Commerce of India • The Federation of Indian Chambers of Commerce and Industry Complete – Bharat Heavy Eelectricals Limited (Annual Report on www.bhel.com) BHEL participates in policy advocacy through these Industry bodies for promoting company's interests via knowledge sharing, surveys, representation to government on industry needs, due diligence in the formation of government policy like GST, Fiscal Budget, Foreign trade etc. Company participates in multilateral bodies such as Indo-‐US, Indo-‐French, Indo-‐Sweden, Indo-‐UK, Indo-‐Russia, Indo-‐Japan forums for trade promotion and collaboration. Company also interacts with NITI Aayog and participates in policy formulations like the policy for Coastal Economic Zone, Atal Tinkering Labs, Investment Summit etc. Company actively contributed through public advocacy towards development of policies meant for strengthening of technology base in country, skill development, development of Indian Power Sector and Indian Manufacturing Industry, and growth of Public Sector Enterprises. Proactive – Hindustan Unilever Limited (Annual Report on www.hul.co.in) Your Company participates in multi-‐stakeholder debates and, when relevant, responds to public consultations. Some of the key issues on which your Company engaged with the government in 2016-‐17 include: • Effective plastic waste management • Engagement with government on fiscal issues including Goods and Services Tax (GST) • Building greater awareness of handwashing practices to reduce diarrhoea • Seeking action against parallel imports of goods in the country • Seeking interventions by Tea Board for maintaining sustainable tea production • Seeking less time-‐consuming procedures for effecting Related Party Transactions • Offering partnership to the Government for Swachh Bharat Abhiyan • Consumer Protection Bill – seeking support for implementing ‘workable’ provisions

29

Principle 8: Businesses should support inclusive growth and equitable development

Core Elements • Businesses should understand their impact on social and economic development, and

respond through appropriate action to minimise the negative impacts. • Businesses should innovate and invest in products, technologies and processes that

promote the wellbeing of society. • Businesses should make efforts to complement and support the development priorities

at local and national levels, and assure appropriate resettlement and rehabilitation of communities who have been displaced owing to their business operations.

• Businesses operating in regions that are underdeveloped should be especially sensitive to local concerns.

QUESTION 1 Does the company have specified programmes/initiatives/projects in pursuit of the policy related to Principle 8? If yes details thereof.

Intent To understand whether the company • Has converted its commitment towards community development into action • Has started ‘measuring’ its outcomes from the lens of their contribution or harm

towards the communities Table 21. Questions and guidelines related to Principle 8, Question 1 of NVGs

Section E Principle 8, Question 1 Complete Response Proactive Disclosure 1.1 Does the company have specified

programmes/ initiatives/projects in pursuit of the policy related to Principle 8?

Yes or No If no, provides an action plan for the same

1.2 If yes details thereof. Details provided Also explains areas where business is yet to have projects on.

EXAMPLES

Complete – Oil and Natural Gas Corporation (Annual Report on www.ongcindia.com) The Company is committed to understand the developmental needs of economically weaker, differently abled and less privileged sections in identified geographical locations in India primarily around the remote operational areas of the company thus creating a more inclusive and equitable world. The Company has a structured mechanism for Corporate Social Responsibility and Sustainable Development (CSR&SD). It aims to strengthen the fabric of society that the Company operate in. Through partners we identify the needs of the communities, and select and implement programs that address those needs. The CSR projects are targeted towards empowering the weakest sections of the society, such as children, women, and the elderly. The programs generate employment and business opportunities, improving the living standards of the community in turn improving the economy of the region.

30 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

QUESTION 2 Are the programmes/projects undertaken through in-‐house team/own foundation/external NGO/government structures/any other organization? QUESTION 3 Have you done any impact assessment of your initiative?

Intent

To understand whether the company is willing to • Not just implement programmes – either by itself or through partner organizations -‐ but

is also focused on measuring and evaluating their impacts. • Make their community development activities also results-‐based.

Table 22. Questions and guidelines related to Principle 8, Questions 2,3 of NVGs

Section E. Principle 8, Questions 2,3 Complete Response Proactive Disclosure 2 Are the programmes /projects

undertaken through in-‐house team/own foundation/external NGO/government structures/any other organization?

Yes or No Provides details of engagement and reasons thereof

3 Have you done any impact assessment of your initiative?

Yes or No Provides weblink to assessment reports

EXAMPLES Complete – ACC (Annual Report on www.acclimited.com) The Company’s CSR Projects are implemented through an in-‐house CSR Department, ACC Ayushmaan Trust as well as in partnership with Non-‐Governmental Organizations (NGOs), Academic and Government Institutions. Proactive -‐ GAIL Yes, Subsequent to the revision of GAIL CSR Policy, third party Independent Impact Evaluation has been mandated for all CSR Projects with a cumulative value of INR 2 Crore (Clause 5.2 and 5.3). The process of conducting Impact Evaluation Study for projects undertaken in FY 2015-‐ 16 has been initiated. GAIL prefers govt. agencies and reputed institutes to take up the impact assessment of its CSR projects like M/s Delhi School of Social Work, M/s Madras School of Social Work, M/s Hardicon, and M/s HIMCON etc. The Third-‐Party Assessor provides feedback pertaining to the strengths, weaknesses, opportunities of improvement augmentation or modification of the programme (if any) and challenges or threats (if any) pertaining to each programme. Generally, feedback in the form of case studies and analysis for programmes is provided by the Third-‐Party Assessor for understanding; or feedback on sustainability of the programmes or any further suggestions to make it sustainable to be provided. The recent impact assessment study of Arogya founds that almost 98.3% people reported that they got cured aeer the treatment given by the MMUs. Also, the MMUs have become the first point of connect for 94.24% of the people. This shows the level of dependence and trust people have on the said flagship programme. Almost 98.3% people reported that they got cured aeer the treatment given by the MMUs. IA is taken up post-‐completion of a project so that a clear-‐cut picture of the project's impact is construed – both positive and negative. Therefore, projects executed in FY 2015-‐16 are under for IA in FY 2016-‐17. Data collection, choice of primary and secondary

31

stakeholder is conducted through the independent third-‐party Assessor according to their prerequisite. The same is shared with GAIL in the assessment report aeer the completion of valuation. Impact Assessment involves accounting of the expenditure of the programme fund with review of bills, vouchers, invoices, or any other document pertaining to the project to ensure transparency and accountability. Based on the documents furnished, the Assessor also provides inputs on rationalization of project expenditure and a comprehensive comparative analysis with the current scenario in case of programme where baseline or need identification study is available.

Question 4 What is your company’s direct contribution to community development projects-‐ Amount in INR and the details of the projects undertaken? Question 5 Have you taken steps to ensure that this community development initiative is successfully adopted by the community? Please explain in 50 words, or so.

Intent To understand whether the Business is • Transparently disclosing its investments on communities and the activities thereof. • Assessing the cost of its programmes in monetary terms and their outcomes • To understand whether the Business is investing in a sustainable way through building

community systems and thereby creating community ownership of its projects. Table 23. Questions and guidelines related to Principle 8, Questions 4,5 of NVGs Section E Principle 8, Questions 4,5 Complete

Response Proactive disclosure

4.1 What is your company’s direct contribution to community development projects-‐ Amount in INR?

Provide an amount here

If no number, provides reasons and action plan

4.2 Details of the projects undertaken Provides details

Provides a detailed disaggregated numbers against different categories

5.1 Have you taken steps to ensure that this community development initiative is successfully adopted by the community?

Yes or No

5.2 Please explain in 50 words, or so.

Details Provides link to an assessment report

32 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

EXAMPLES

Complete – Grasim Industries (Annual Report on www.grasim.com) During the year under review, the Company has spent an amount Rs 18.06 crore on CSR activities mainly on education, health care, environment and livelihood, rural development projects, women empowerment, etc., and to bring about social change by advocating and supporting various social campaigns and programmes. Proactive – Tata Power (Annual Report on www.tatapower.com) The process of community engagement begins right from business development stage, to projects and operations stage. The socio-‐economic study and baselines form the basis for identification of prioritized needs followed by program planning with help of external experts. This process is reviewed once in every 3-‐5 years with the objective of going back to community. This year, while Company implemented programs with prior community consultation through our teams, Company has also set itself on path of revisiting community needs for the future social aspiration of each location as envisaged by senior leadership. Hence the planning is based on community consultation based feedback of existing programs as per the stage followed by annual evaluations of programs and partners’ inputs with a collective approach.

Additional Questions (Principle 8) How many number of projects that required R&R during the year? Please specify details of ongoing projects for which any work on R&R including compensation took place in the year? How many projects required organising social impact assessments? If done, please provide the link? Name any business innovations that you have done in the year, which according to the company, has contributed immensely to the well-‐being of the society?

33

Principle 9: Businesses should engage with and provide value to their customers and consumers in a responsible manner

Core Principles • Businesses, while serving the needs of their customers, should take into account the

overall well-‐being of the customers and that of society. • Businesses should ensure that they do not restrict the freedom of choice and free

competition in any manner while designing, promoting and selling their products. • Businesses should disclose all information truthfully and factually, through labelling and

other means, including the risks to the individual, to society and to the planet from the use of the products, so that the customers can exercise their freedom to consume in a responsible manner. Where required, businesses should also educate their customers on the safe and responsible usage of their products and services.

• Businesses should promote and advertise their products in ways that do not mislead or confuse the consumers or violate any of the principles in these Guidelines.

• Businesses should exercise due care and caution while providing goods and services that result in over exploitation of natural resources or lead to excessive conspicuous consumption.

• Businesses should provide adequate grievance handling mechanisms to address customer concerns and feedback.

QUESTION 1 What percentage of customer complaints/consumer cases are pending as on the end of financial year?

Intent To understand whether Companies

• Have commitment towards consumers • Have a system of addressing consumer grievances

QUESTION 2 Does the company display product information on the product label, over and above what is mandated as per local laws? Yes/No/N.A. /Remarks(additional information) QUESTION 3 Is there any case filed by any stakeholder against the company

regarding unfair trade practices, irresponsible advertising and/or anti-‐competitive behaviour during the last five years and pending as on end of financial year. If so, provide details thereof, in about 50 words or so. QUESTION 4 Did your company carry out any consumer survey/ consumer satisfaction trends?

Intent To understand whether the company • Engages in practices that are not contrary with free and fair market competition, • Provides choice and adequate information to the consumer, • Is mindful of the well-‐being of society and whether it is willing to make public any issues

of conflict. • To find out if the company has engaged periodically to seek any form of feedback and

evaluation of consumer satisfaction towards the betterment of their products or services

34 GUIDE TO BETTER DISCLOSURE: MANUAL ON BUSINESS RESPONSIBILITY REPORTING

Table 24. Questions and guidelines related to Principle 9,Questions 1-‐4 of NVGs

Section E Principle 9, Questions 1-‐4 Complete Disclosure Proactive disclosure

1 What percentage of customer complaints/consumer cases are pending as on the end of financial year?

Number of Complaints received during the year=….

Number of complaints pending on March 31=….

Details in terms of nature of complaints

2 Does the company display product information on the product label, over and above what is mandated as per local laws? Yes/No/N.A (remarks)

Yes or No or NA Provides details and examples

3.1 Is there any case filed by any stakeholder against the company regarding unfair trade practices, irresponsible advertising and/or anti-‐competitive behaviour during the last five years and pending as on end of financial year?

Number of such complaints in the last 5 years=…..

Number of such complaints pending as on March 31=………