bruce biegel january 8, 2015 senior managing...

TRANSCRIPT

2015 Annual Outlook: What Financial Services Marketers Can Expect in Direct and Digital Marketing

Bruce Biegel Senior Managing Director

January 8, 2015

About Winterberry Group

• Corporate Strategy

• Brand Data Strategy, Marketing Technology & Process Re-engineering consulting

• M&A Buy side Targeting and Integration Planning

• Commercial Diligence Support

• Market Insight & Intelligence

A subsidiary of Investment bank

• The Leading Mid-Market Advisor (Bloomberg)

• 30 transactions completed in 2014!

A subsidiary of Investment bank

Market Advisor (Bloomberg)Market Advisor (Bloomberg)Market Advisor (Bloomberg)

2014 The Trends : What Happened, What Didn’t?

Global Perspective: Marketing and Advertising Around the World

Outlook 2015

2014 Recap: The Numbers

U.S. GDP started bad and wound up good—nasty weather led to some turbulence but then a nice ride almost to the end

Congress did not do bad things (or much of anything)—they were too busy playing politics

And there was something about more digital advertising…

The Year That Was…

Traditional Media Did Not Stagnate, But No Real Catalysts To Drive Growth

2014 U.S. “Measured Media” Spending: $124.4BB

Newspapers: $16.9BB

3.3%

-7.5%

Television: $68.5BB

Magazines: $15.1BB

Outdoor: $7.2BB

Radio: $15.9BB

Cinema: $0.7BB

Source: Winterberry Group analysis of multiple sourcesNote: Arrows reflect percentage change in spend, by channel, from 2013 levels

2.7%

1.2% 0.5%

2.2%

1.0%

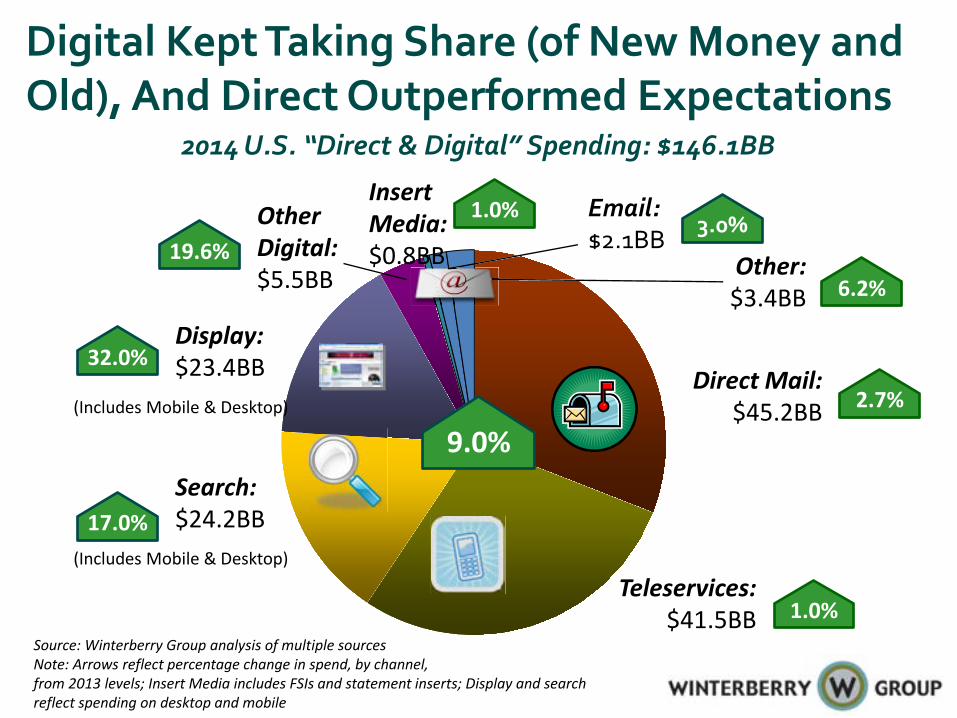

2014 U.S. “Direct & Digital” Spending: $146.1BB

Source: Winterberry Group analysis of multiple sources Note: Arrows reflect percentage change in spend, by channel, from 2013 levels; Insert Media includes FSIs and statement inserts; Display and search reflect spending on desktop and mobile

Teleservices: $41.5BB

Direct Mail: $45.2BB

Search: $24.2BB 17.0%

6.2% Other: $3.4BB

9.0%

Digital Kept Taking Share (of New Money and Old), And Direct Outperformed Expectations

1.0%

Insert Media: $0.8BB

Display: $23.4BB 32.0%

Other Digital: $5.5BB

19.6%

(Includes Mobile & Desktop)

(Includes Mobile & Desktop) 2.7%

1.0% Email: $2.1BB 3.0%

In Digital, It Was About Social, Mobile, Video and… Data

27.0% Social Technology

and Services¹: $3.0BB

3.0% Lead Gen &

Affiliate Services:

$2.1BB

2014 U.S. Digital Advertising Spending: $55.2BB

Other Mobile2 : $.4BB

24.1%

Email: $2.1BB 3.0%

29.4%

Source: Winterberry Group analysis of multiple sources Note: Arrows reflect percentage change in spend, by channel, from 2013 levels ¹Excludes social display and social search spend 2Excludes mobile display and mobile search spend

Search: $24.2BB 17.0%

Display: $23.4BB 32.0%

(Includes Mobile & Desktop)

(Includes Mobile & Desktop)

2014 The Trends : What Happened, What Didn’t?

Global Perspective: Marketing and Advertising Around the World

Outlook 2015

2014 Recap: The Numbers

And they did—volumes were down, though not as much as predicted and spend was up due to higher postage and package costs

Retention mail continued its systemic shift to email

Yet direct mail kept its share in acquisition marketing: • It can be integrated with digital channels

(mobile, behavioral triggers) • It is targetable, predictable & measureable

True or False: Postal Hikes Threatened Mail

True Still in process

False

Programmatic display (banners, video, mobile, social) advertising exploded in 2014 • Rising from 24% of all digital

display spending ($4.24BB) to $10.06BB

• Captured 45% of all display spending

And along with the growth of programmatic exchange based buying came a significant increase in the use of digital data

True or False: Programmatic Approaches Continued To Expand

Source: eMarketer and Winterberry Group analysis

increase

True Still in process

False

Facebook and Twitter Custom and Tailored Audiences options leveraging CRM data to target (or suppress) engagement on social platforms report extremely high lift • Social targeting soars • Social attribution matters • Social IDs for audience

recognition gives social sites a targeting advantage (we know what you did last summer…)

True or False: Social Targeting with CRM Data Went Mainstream

True Still in process

False

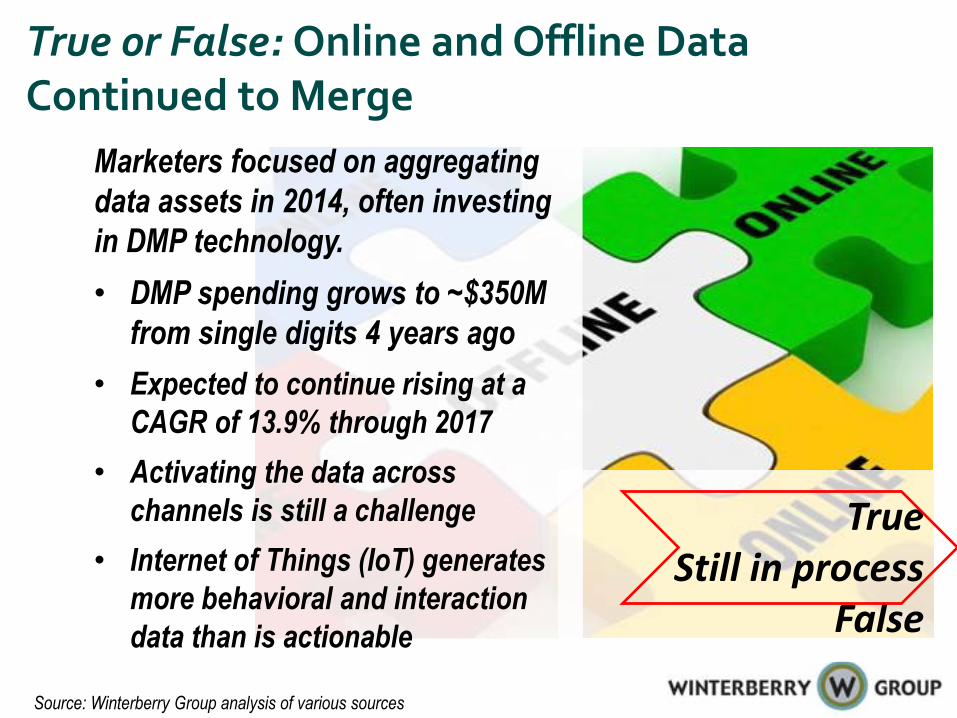

Marketers focused on aggregating data assets in 2014, often investing in DMP technology. • DMP spending grows to ~$350M

from single digits 4 years ago • Expected to continue rising at a

CAGR of 13.9% through 2017 • Activating the data across

channels is still a challenge • Internet of Things (IoT) generates

more behavioral and interaction data than is actionable

True or False: Online and Offline Data Continued to Merge

Source: Winterberry Group analysis of various sources

True Still in process

False

Native advertising came on in full force in 2014, with spending reaching $3.2BB

Its about owned driving earned and leveraging paid to get out the word • Still early • Good content is hard • Deceptive advertising is still a

risk

True or False: Content Came of Age

True Still in process

False

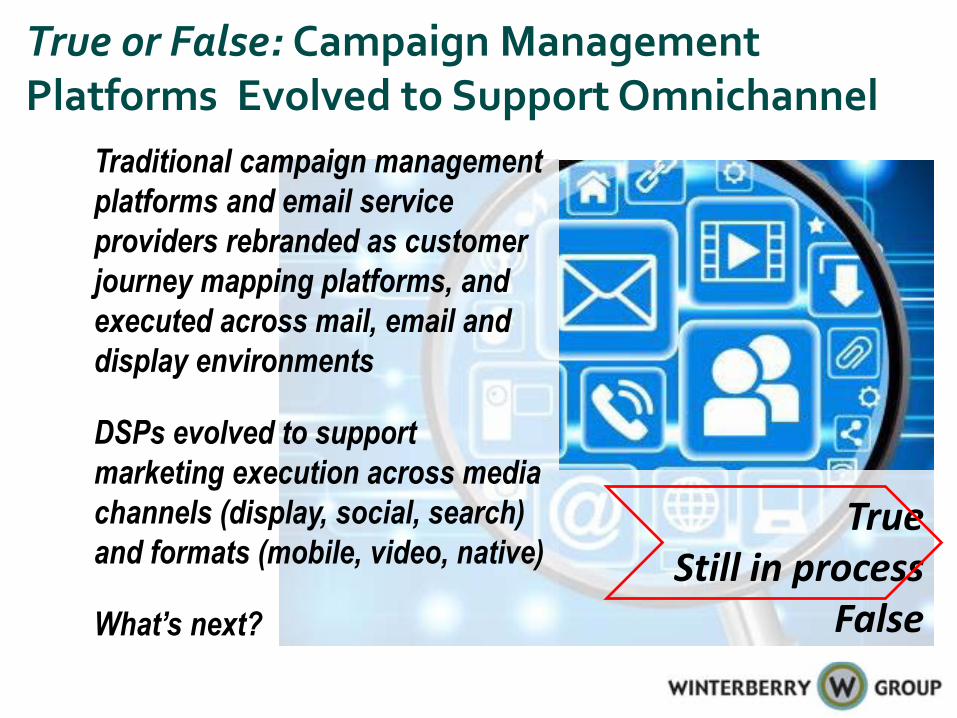

Traditional campaign management platforms and email service providers rebranded as customer journey mapping platforms, and executed across mail, email and display environments

DSPs evolved to support marketing execution across media channels (display, social, search) and formats (mobile, video, native)

What’s next?

True or False: Campaign Management Platforms Evolved to Support Omnichannel

True Still in process

False

2,904 deals were reported in the marketing, media and tech segments in 2014, equaling more than $126.1BB in aggregate value

• Data—LiveRamp, BlueKai, DLX,

Adometry, Convertro • Agency—Sapient, non Publi-com • Ad Tech—X+1, BrightRoll,

Conversant • Alibaba

True or False: Consolidation, Significant IPOs and More Digital Stacks

True Still in process

False

Source: Petsky Prunier 2014 Marketing Deal Overview Release

2014 The Trends : What Happened, What Didn’t?

Global Perspective: Marketing and Advertising Around the World

Outlook 2015

2014 Recap: The Numbers

Everybody’s Doing It: Three Quarters of Panel Confident in Data Driven Marketing Growth

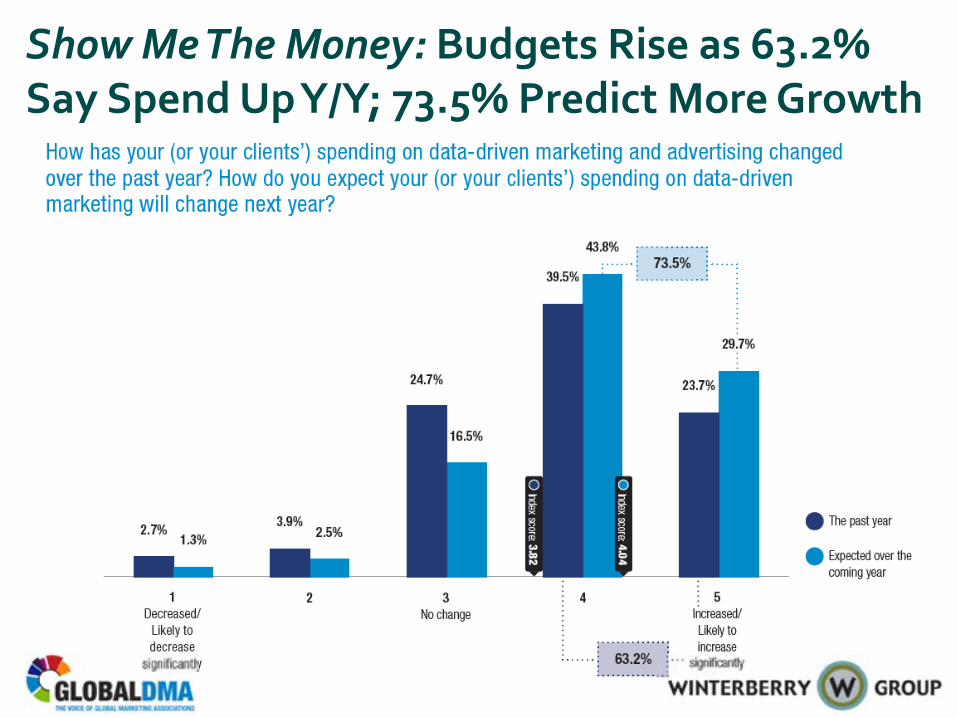

Show Me The Money: Budgets Rise as 63.2% Say Spend Up Y/Y; 73.5% Predict More Growth

Emerging Markets Posted Higher Levels of Confidence—Even With Tight Economies

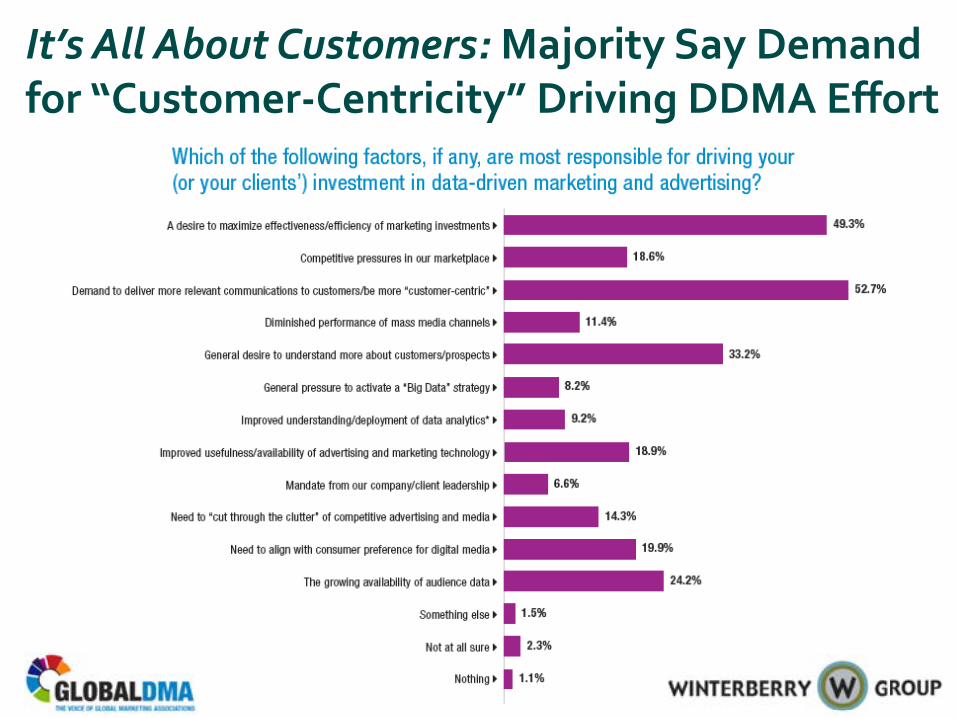

It’s All About Customers: Majority Say Demand for “Customer-Centricity” Driving DDMA Effort

Borders Matter Less: Embrace of “Data-Driven” Approach Fairly Consistent Worldwide

Tops Among Channels Capturing Share of Spend? Digital (Of Course)

Data Matters: 92% Say It’s Growing More Important to Efforts

“Consumer-Friendly” is Just Good Business: Marketers Aligned with Regulatory Aims

Doesn’t Matter Where You Are—Marketers Want More: Cash, Talent, Expertise (training)

2014 The Trends : What Happened, What Didn’t?

Global Perspective: Marketing and Advertising Around the World

Outlook 2015

2014 Recap: The Numbers

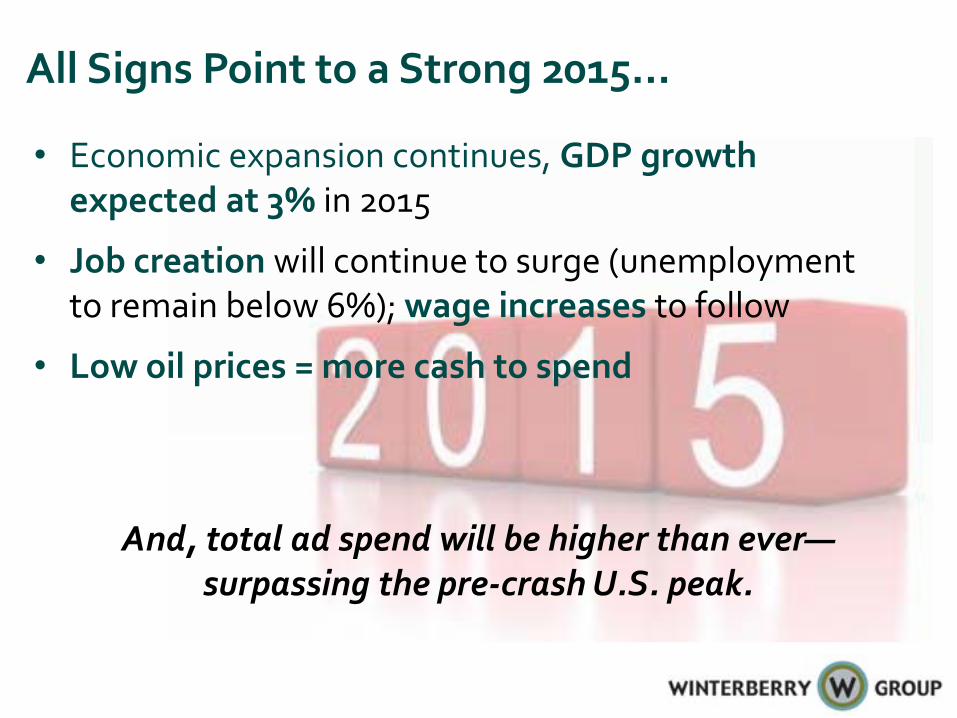

All Signs Point to a Strong 2015…

• Economic expansion continues, GDP growth expected at 3% in 2015

• Job creation will continue to surge (unemployment to remain below 6%); wage increases to follow

• Low oil prices = more cash to spend

And, total ad spend will be higher than ever—

surpassing the pre-crash U.S. peak.

All Signs Point to a Strong 2015… But

There are several inhibitors, raising red flags:

• No Olympics, World Cup or any global sports events

• Off year for elections (Less DC entertainment)

• Financial market nervousness about interest rates, global growth, geo-political meltdown, deflation, etc.

• The Bull has had a long run (70+ months). Is it tired?

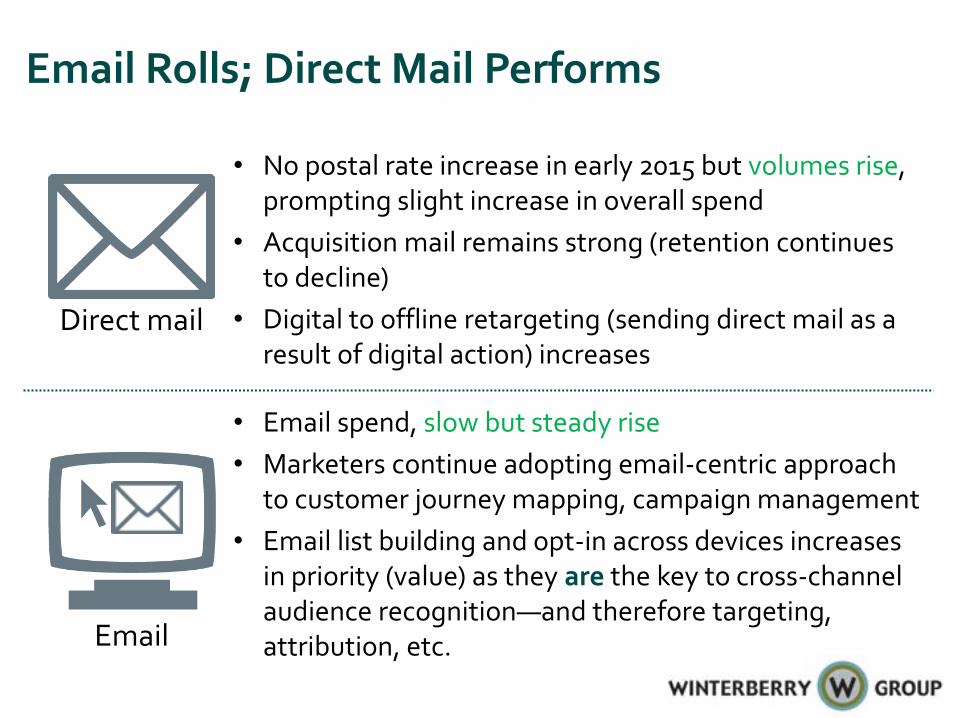

Email Rolls; Direct Mail Performs

• Email spend, slow but steady rise • Marketers continue adopting email-centric approach

to customer journey mapping, campaign management • Email list building and opt-in across devices increases

in priority (value) as they are the key to cross-channel audience recognition—and therefore targeting, attribution, etc.

• No postal rate increase in early 2015 but volumes rise, prompting slight increase in overall spend

• Acquisition mail remains strong (retention continues to decline)

• Digital to offline retargeting (sending direct mail as a result of digital action) increases

Direct mail

Search and Display Continue to Grow; New Spend Driven by Mobile Opportunities

• Search growth rates slow substantially though new spending is fueled by mobile

• Mobile, geo-location and tracking opportunities (beacons, etc.) continue to fuel new, real-time, relevant search marketing efforts Search

• Display (banners, video, social, mobile, etc.) spend to surpass search for first time

• Growth drivers: mobile and social targeting, video, native, programmatic—all similar to 2014—except maybe some TV share shift… Display

Measured Media Up Again—But Not in Line with GDP Growth

2015E U.S. “Measured Media” Spending: $126.3BB

Newspapers: $16.4BB

3.1%

-2.8%

Television: $70.6BB

Magazines: $15.0BB

Outdoor: $7.4BB

Radio: $16.2BB

Cinema: $0.7BB

Source: Winterberry Group analysis of multiple sourcesNote: Arrows reflect expected percentage change in spend, by channel, from 2014 levels

2.5%

1.53%

1.9%

-1.1%

1.0%

2015E U.S. “Direct & Digital” Spending: $156.8BB

Source: Winterberry Group analysis of multiple sources Note: Arrows reflect percentage change in spend, by channel, from 2014 levels; Insert Media includes FSIs and statement inserts; Display and search reflect spending on desktop and mobile

Teleservices: $42.6BB

Direct Mail: $45.7BB

Search: $26.9BB 11.1%

2.7% Other: $3.5BB

7.3%

Data-Driven Efforts Accelerate; Display UpBig—Driven By Programmatic Approaches

2.7%

Insert Media: $0.8BB

Display: $28.3BB 21.1%

Other Digital: $6.7BB

21.8%

(Includes Mobile & Desktop)

(Includes Mobile & Desktop) 1.0%

1.0% Email: $2.3BB 9.7%

Mobile and Social Fuel Most Digital Growth

31.5% Social Technology

and Services¹: $3.9BB

3.8% Lead Gen &

Affiliate Services:

$2.2BB

2015E U.S. Digital Advertising Spending: $64.2BB

Other Mobile2 : $.6BB

37.3%

Email: $2.3BB

16.3%

Source: Winterberry Group analysis of multiple sources Note: Arrows reflect expected percentage change in spend, by channel, from 2014 levels ¹Excludes social display and social search spend 2Excludes mobile display and mobile search spend

Search: $26.9BB 11.1%

Display: $28.3BB 21.1%

(Includes Mobile & Desktop)

(Includes Mobile & Desktop)

9.7%

2015 Trends: Is Social All That?

What we think is TRUE • Social sites and their apps rule • Social is delivered more often across more mobile devices • Social sites have tons of data (behavioral and other) • Social IDs eat cookies—social recognition and audience

extension a priority in 2015 BUT what else? • Transaction data is more predictive, so social commerce is an

imperative • Social effectiveness is…still to be proven (attribution required

across the journey) 2015 is the year that this gets sorted out

2015 Trends: It’s About The Beacons

It’s here now • It’s about in-store, location and recognition to drive

engagement/activation • It’s about behavioral data collection; not just targeting • It’s about leveraging data later, or “post beaconing” • 2014 tests lead to 2015 adoption: retail, finance, OOH; Macy’s,

Lord & Taylor, Barclays, Miami airport, entertainment centers (Levi’s Stadium, theaters)

However • It’s still early; roll-outs to accelerate; consumer adoption (opt-

in, new use cases, more retargeting) to grow significantly • It will be about direct sales/marketing before branding—will it

take share from promo spend or is it taking new money?

2015 Trends: Programmatic & Addressable TV

It’s all that • Set-top-box (STB) plus connected TV (apps, OTT) data

integrated with offline and online/behavioral data for deeper consumer insights

• Consistent messaging (offer management and targeting) across platforms (devices) possible at greater scale

• Audience buying—but not RTB—use cases take hold But, it’s not scalable yet • Buying processes still being sorted out; pricing still in process • Data availability and use case development not set However • Major brands in CPG, retail and finance are investing

2015 Trends: Big Data, the Internet of Things (IoT) and My Refrigerator is Talking to My Car!

¹A Strategist’s Guide to the Internet of Things, Frank Burkitt, 2014

It’s happening • 50 billion devices—sensors, beacons and computing

devices—will be connected to the Internet within 5 years¹ • The “Internet of Things” is reaching a tipping point in the

collection, management and deployment of data for marketing and sales uses cases

However • It’s not just about social • There’s still no easy way to parse (what to keep and what

to toss) that much data • We’re not quite there yet—but there’s no lack of money or

talent trying to solve the issues . Check back in 2016—on your wearable

2015 Trends: Campaign Orchestration / Execution Continues Omnichannel Expansion

¹A Strategist’s Guide to the Internet of Things, Frank Burkitt, 2014

What’s happened • It’s about touchpoint management (and attribution) • Customer journey maps are integrated into the campaign

platform across channels • Data architecture and integration are critical • Email is the preferred hub; mobile/social deployment is required • DMPs are an extension of traditional marketing databases for

enhanced data collection and audience insights What’s next • ESP platforms mature in 2015, offer enhanced channel support,

better integration of data, easier user interface • Verticals and segments (enterprise, mid-market and SMB) get

attention

2015 Trends: It’s the Year of Attribution and Measurement (or one of those years…) Today’s requirements • Accurate, data-driven, cross-environment measurement

and attribution, which can solve for “bad actors” and optimize spend—justifying investment with ROI

• Tools that are fast (real-time) and easy to implement (and don’t use budget already allocated)

Questions to be sorted • What channels should we move to? Not enough time (or

money) to test them all • How do we optimize? • Should I do this in-house? Or out? • What about fraud and bots and viewability (oh my!)

2015 Trends: Still More M&A Activity

What’s happened • 2014 saw tremendous deal volume and value • Ad tech and related IPOs—up then down What’s next • Big cliff of investible funds • Demand high for companies with first-party and compiled data • “Stacks” expand toward owning the entire audience insight,

management, engagement and measurement continuum; tech companies with early adoption will be integrated

• Companies that IPO’d in 2013/2014 use their cash and stock, become buyers to drive scale

• Valuation/multiples likely to remain high in 1H15

¹Pestky Prunier, Deal Notes, January 2015

2015 Trends in Fin Serv Marketing: Enter the “Marketing Compliance Office” What’s happening • Regulatory environment is tough and becoming

increasingly complex • Marketing and compliance are integrating

• Compliance requires view into operations, supply chain and marketing tech functions; marketing requires understanding of regulations on products, compliance management systems

What’s next • Emergence of the “Marketing Compliance Office” • Teams staffed with marketing professionals cross-

trained in compliance-focused product development and innovation

2015 Trends in Fin Serv Marketing: Enhanced Targeting for Regulated Data Online What’s happening • Facebook Custom Audiences and other solutions are

enabling individual targeting—to known users—online • Digital marketing offers lower-cost alternatives to

traditional media (vs. mass media and direct mail) while still offering compelling creative and rich formats

What’s next • Financial services marketers begin leveraging digital

pre-screening for lending, custom digital collateral and personalized, interactive experiences—delivering the reliability of offline with the flexibility and efficiency of online

Bruce A. Biegel Senior Managing Director [email protected] 212-842-6030

www.winterberrygroup.com @WinterberryGrp

Questions?