brunswick conference 2002

TRANSCRIPT

Alexander KorsikFirst Vice President

Brunswick UBS Warburg Conference 2002

Sibneft acquisition strategy as a key factor of sustained long

term growth

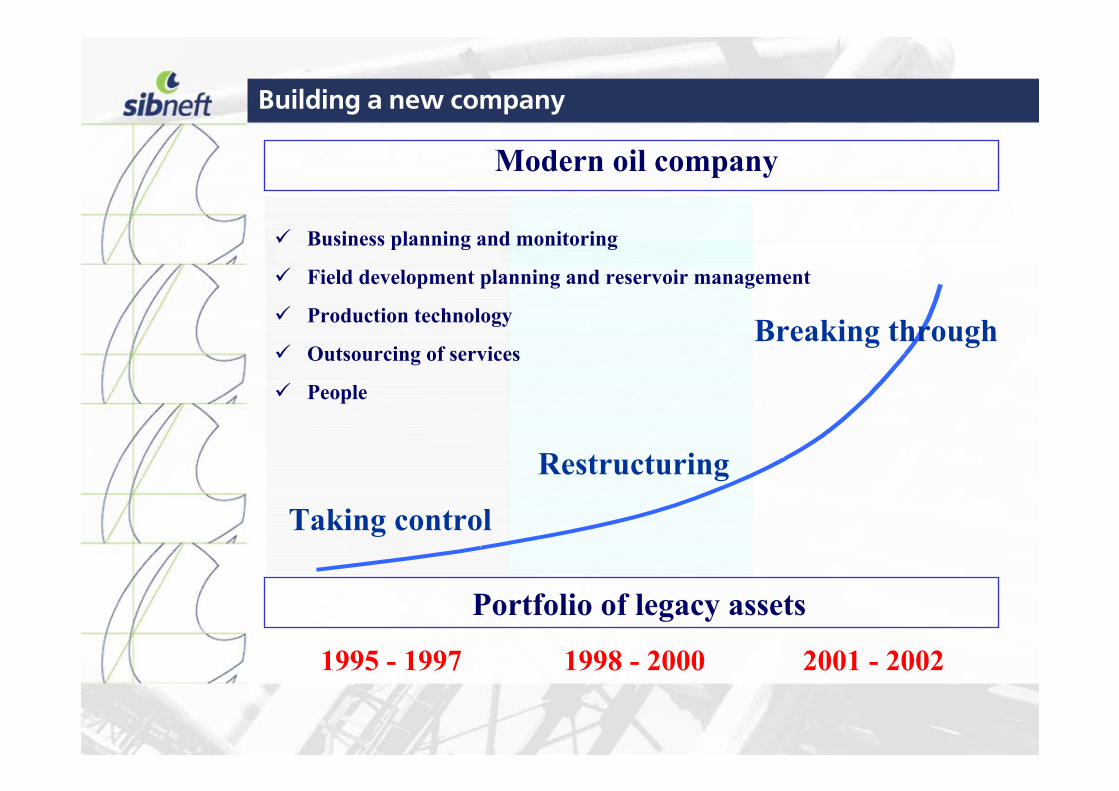

Building a new company

Modern oil company

Portfolio of legacy assets

1995 - 1997 1998 - 2000 2001 - 2002

Taking control

Restructuring

Breaking through

Business planning and monitoring

Field development planning and reservoir management

Production technology

Outsourcing of services

People

Production growth ahead of peers

Growth in output since January 2000 (%)

100

120

140

160

180

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gu

st

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gu

st

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gu

st

Lukoil Surgut Yukos TNK SIBNEFT

%

2000 2001 2002

2001 EBITDA per ton ahead of peers

0

20

40

60

80

100

Sibneft YUKOS SurgutNG TNK LUKoil Tatneft

Sibneft strategy

World class returns

Potential of existing assets

New upstream assets

Refining capacity

Retail network

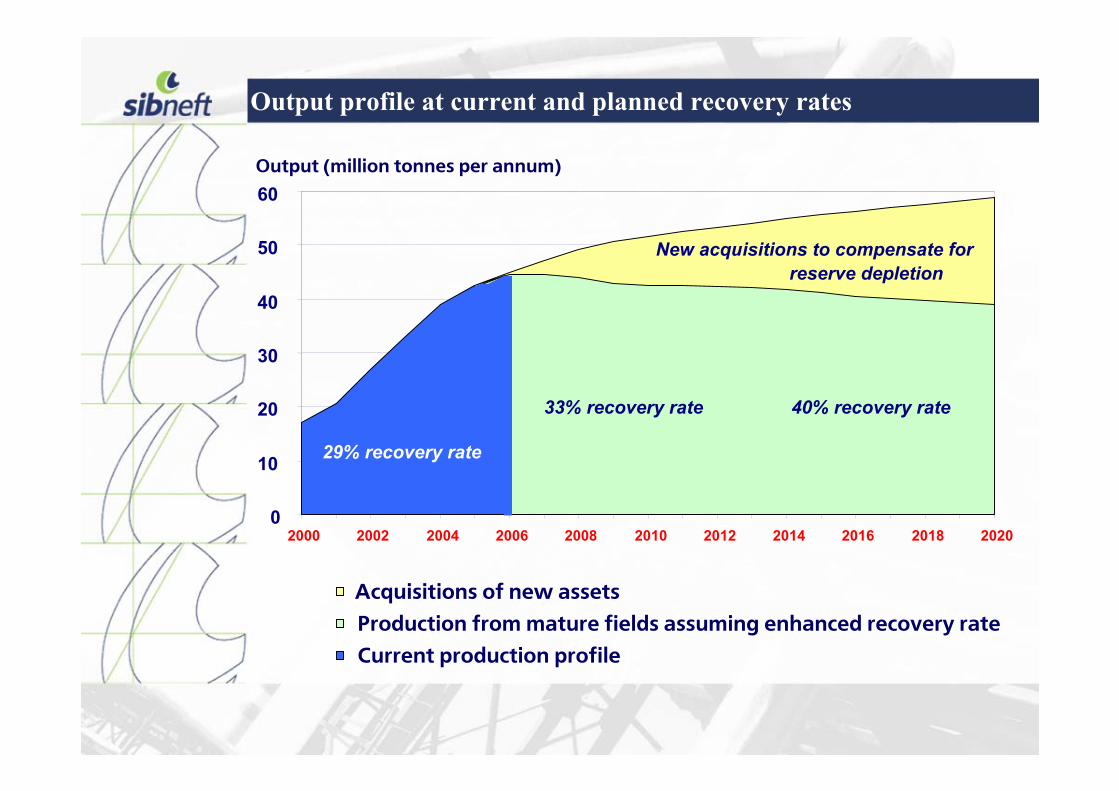

Output profile at current and planned recovery rates

0

10

20

30

40

50

60

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Acquisitions of new assetsProduction from mature fields assuming enhanced recovery rateCurrent production profile

33% recovery rate

New acquisitions to compensate for reserve depletion

40% recovery rate

29% recovery rate

Output (million tonnes per annum)

Sibneft upstream acquisitions 2000 - 2002

Orenburgneft

2001 – 50% stake in Sibneft-Yugra: Priobskoye and Palyanovskoye fields.

2002 – 67% stake in Meretoyahaneftegas: Meretoyahskoye field in “Noyabrsk region”.

2000 - 38% stake in Orenburgneft.

Slavneft Trust 2001 – 25% stake in Slavneft Trust.

New upstream acquisitions reserve addition

0 100 200 300 400 500 600 700 800

Sugmutskoye

Sutorminskoye

Vingapurovskoye

Sporishevskoye

Muravlenkovskoye

Vingayahinskoye

Sibneft-Yugra +Meretoyaha New 2001 upstream acquisitions

account for the 7-th biggest reserves group (in terms of Proved Reserves) of

Sibneft oil fields.

Future production growth, mln.tons. Acquisitions vs. old fields

0

10

20

30

40

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Old fields Sibneft-Yugra + Meretoyaha field

18%

82%

30%

70%

“New acquisitions of 2001 - 2002” will account for 18% in total production by 2005 and up to 30% by 2010.

Upstream acquisitions dilemma

In Russia or abroad ?

At what price?

Why do we go for Russian reserves – Finding Costs are low

(Exploration+Development)/ Reserves (extentions+discoveries+improved recovery+revaluation) - 5 years average, USD/ boe

0

1

2

3

4

5

6

7

8

9

USA Europe Canada Asia/ Pacific Middle East Russia

Russian Finding Costs are twice as low as the Finding Costs in the Persian Gulf

Why do we go for Russian reserves –Acquisition Costs are low

Acquisition Costs, USD/ boe - 5 year average

0

1

2

3

4

5

6

USA Europe Canada Asia/ Pacific Middle East Russia

Russian Reserve Acquisition costs are stil l about 10 times lower than the world

average

Sibneft upstream Acquisition Costs versus peers, USD/ boe

0

0,5

1

1,5

2

YUKOS (Arct

icgas)

Slavneft

(ObNGgeology)

LUKoil (B

itech

)LUKoil

(AmKomi)

TNK (Onaco

)

BP (Sidanco

)Sibneft

(Mere

toyaha)

Sibneft has low acquisition costs per

barrel of ABC1 Reserves

At what price ?

ReservesReservesReserves

Added value

Added value:FDP, Planning,

TechnologyPeople

Added value

Speculative value (high oil price)

Speculative value (high oil price) Upside for Sibneft

0

100

Company Y Sibneft Company X

we don't buy we buy!

Sibneft downstream acquisitions 2001

Moscow refinery characteristics:

Refining throughput – 9,8 mln.tons annually

Utilisation ratio – 91%

Depth of refining – 68%

In 2001 Sibneft acquired 37% in Moscow refinery. Currently Sibneft has a long term contract to deliver at least 350 thousand tons of crude a month to the refinery.

Central Federal Region, which includes Moscow and Moscow region,accounts for 20% of total fuel consumption in Russian Federation. Moscow share in this number is 45%. Moscow refinery is the second closest refinery to European exports markets.

Sibneft crude deliveries

Sibneft production growth will enable it to load Moscow refinery with its own crude. In 2002 Sibneft has about 14% of spare crude (net of export and Omsk refinery shipments) to supply to Moscow.

2001

Crude Exports

35%

Omsk Refinery

deliveries60%

Other deliveries

5%

2002

Crude Exports

36%

Omsk Refinery

deliveries50%

Other deliveries

14%

Due to the low direct production costs ($1.70 per barrel in 2001) Sibneft has a safe “transportation cushion” that will allow to transport crude directly from Noyabrsk and still to have competitive oil product prices on Moscow market.

Acquisition costs in downstream, USD per bbl.

0

3

6

9

12

LUKoil(Petrotel)

LUKoil(O dessa)

LUKoilNeftochim

LUKoil (Norsi) TNK(Lisichansk,

Ukraine)

YUKO S(Mazheikiu)

Sibneft(Moscow

Refinery)

USD/ Capacity USD/ Throughput

Competitive advantages of Moscow refinery acquisition

Was it expensive? Yes, it was value for money !

The last refinery for sale …

Good refinery for sale …

Excellent market …

Access to exports …

Bridgehead into St.Peterburg and Nizniy Novgorod and other European Russia markets ….

1300 – 30005500Sales per 1 station (cub.meters/ year)

1000 - 20003850Cars per 1 station

2000 - 4700

Europe

13150

Moscow

People per 1 station

Retail network growth

Sibneft acquired 20,5% of voting stock in Mosnefteprodukt. In 2002 Sibneft made acquisitions in Moscow, Tomsk and Krasnoyarsk retail businesses. We plan to add up more than 100 filling stations to the current 1125 stations by the end of 2002.

108 AZS 109 AZS 122 AZS

647 AZS732 AZS

824 AZS

1125 AZS

0

200

400

600

800

1000

1200

1996 1997 1998 1999 2000 2001 2002

own franchise+dealers

Currently 60% of light oil products are sold via own

regional marketing subsidiaries. 24% of gasoline is sold through

retail network.

Sibneft stations acquisition costs versus peers, th.USD per station

0

100

200

300

400

500

600

700

ANCAP (Arge

ntina)

Giant (U

SA)

OMV (Bulg

aria)

Genesis

(Lith

uania)

OK Petrole

um (S

weden)

Tesoro

Petrole

um (U

SA)

Parklan

d Indu

stries

(Cana

da)ENI (B

razil)

Kuwait

Petrole

um (It

aly)

Petron

as (Thai

land)

Sibnef

t (Russ

ia) min

/ max

Sibneft petrol stations acquisition costs in Russia are lower than

anywhere else in the world

Sibneft competitive position in retail products marketing

Since 1995 Sibneft added up 10 more oil product distribution companies.

Sibneft currently sells 25% of the products via marketing subsidiaries.

We control from 35% to 90% of the markets in the areas we operate.

How to maximize returns

RESERVOIR MANAGEMENT

PLANNING

TECHNOLOGIESOUTSOURCING OF SERVICES

PEOPLE