bsg webinar: upcoming changes to respa / tila

TRANSCRIPT

Upcoming Changes to RESPA / TILAGetting It Right

April 2, 2015

Long Time Coming

• The regulatory imperative to combine RESPA and TILA has existed for more than 17 years!

• Both of these regulations do similar things and create similar responsibilities at banks.

• The biggest difference is that RESPA only applies to mortgages while TILA applies to all consumer loans

• The basic purpose of both is to inform customers of the total cost of borrowing money

Well Earned

• As with all consumer regulations, these two rules were developed in response to unethical and illegal practices by financial institutions

• TILA’s purpose – “It is the purpose of this subchapter to assure a

meaningful disclosure of credit terms so that the consumer will be able to compare more readily the various credit terms available to him and avoid the uninformed use of credit, and to protect the consumer against inaccurate and unfair credit billing and credit card practices.”

Well Earned

• RESPA is supposed to make it easier to shop from one bank to another

• RESPA’s Purpose:

– is “to effect certain changes in the settlement process for residential real estate that will result in more effective advance disclosure to home buyers and sellers of settlement costs”

Changes are Coming

• The TILA/RESPA rules does a number of things

• The GFE and the initial Truth in Lending estimate have been combined into a new form called the loan estimate

• The loan estimate is due within three business days of the receipt of an application

Changes are Coming

• The HUD-1 and the final Truth in lending statement have also been combined into a new form called a closing document.

• The closing document has to be delivered three business days before the loan is closed.

• THESE RULES START ON AUGUST 1, 2015

• For exempt loans, such as HELOCs- the old GFE and HUD-1 can still be used

Prevented

• Imposing fees on a consumer before the consumer has received the Loan Estimate and indicated an intent to proceed with the transaction

• Providing written estimates of terms or costs specific to consumers before they receive the Loan Estimate without a written statement informing the consumer that the terms and costs may change

• Requiring the submission of documents verifying information related to the consumer’s application before providing the Loan Estimate

Loan Estimate

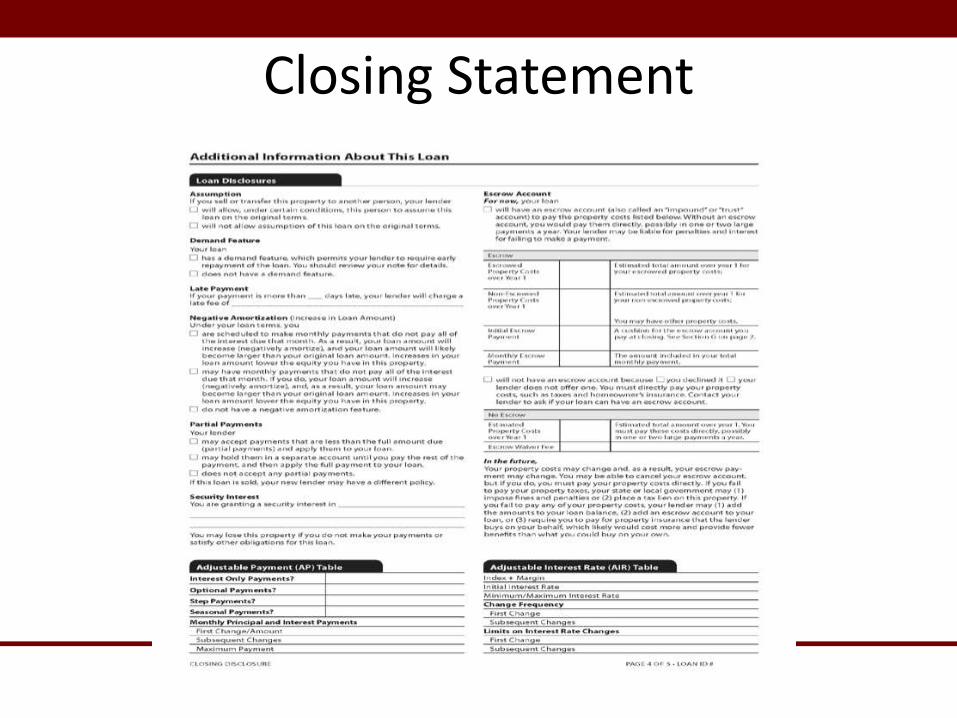

Closing Statement

Closing Statement

Closing Statement

Closing Statement

Closing Statement

Other Rules

• Exemptions

• TILA-RESPA rule does not apply to HELOCs, reverse mortgages or mortgages secured by a mobile home or by a dwelling that is not attached to real property

• Retention Rules

• Three years for the Loan Estimate

• Five years for the Closing statement

Summary

• August 1, 2015 is a Absolute Start

• The Loan Estimate replaces the GFE and the TILA

• No charges or information without the loan estimate

• Good Faith means the borrower pays less than what is on the Loan estimate

• The other rules still apply!

Upcoming Changes to RESPA / TILAGetting It Right

April 2, 2015