bsi base drive_storyline_v1

TRANSCRIPT

1

Draft 5/09/2001

Basedrive has identified a feasible business opportunity in electronic media aggregation, distribution and presentation that will require extensive system integration and project management expertise to bring to market Basedrive interface is designed to be the single interface to the world of available content and desktop applications on a subscription or pay per view basis

• The proprietary GUI will run on multiple platforms• The MHP standard is expected to become de facto

The potential market is global, constrained only by marketing reach, broadband costs and IP protection concerns• Marketing reach• Broadband costs• Digital rights management nd IP protection strategy

Basedrive will concentrate on packaging and distribution elements of the value chain and form strategic alliances for the rest of the system• Production, subscriber management systems (SMS) and billing are scale businesses• Packaging and distribution can utilise “narrow casting” economics• Utilise partners for highly specialised elements in which Basedrive do not yet have expertise or competitive advantage

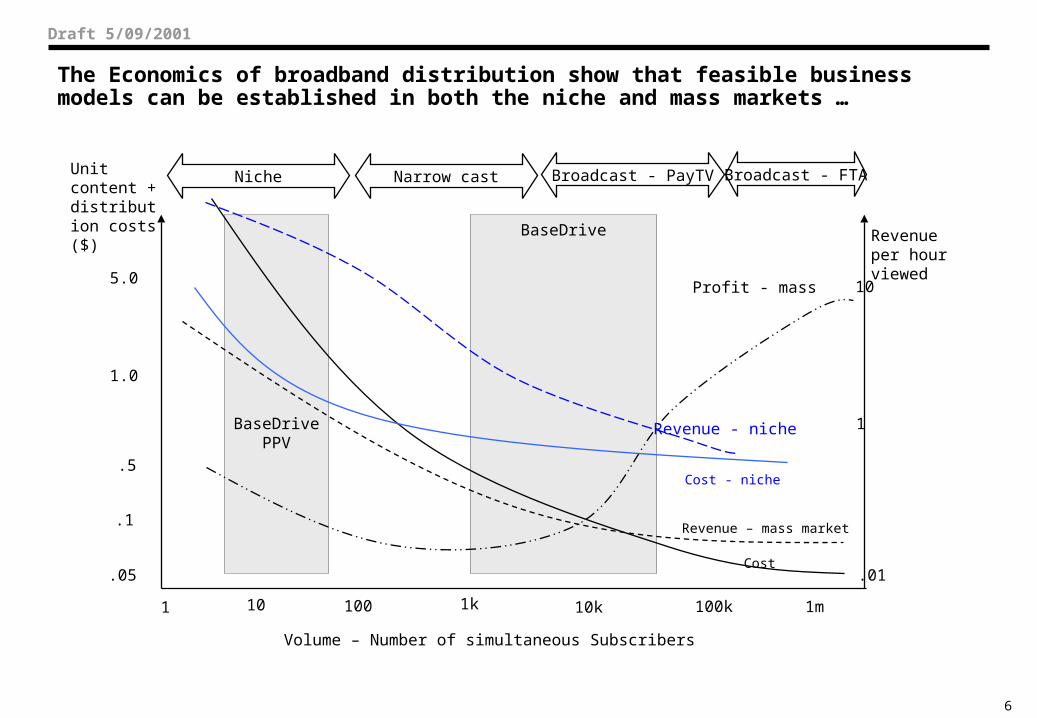

The Economics of broadband distribution show that feasible business models can be established in both the niche and mass markets• Appropriate head-end and edge-server infrastructure must be in place to achieve acceptable cost structures• Basedrive recognises that it is unable to lower costs substantially because of the relative negotiating power of (1) content owners and (2) broadband network providers

The product has the potential to generate revenues of $93m in the Australian market• Synchronous broadcast for second tier content packages based on Pay TV pricing models• Asynchronous content based on PPV (cost driven pricing) models• Synchronous live content distributed into new geographies and onto new display devices premium priced

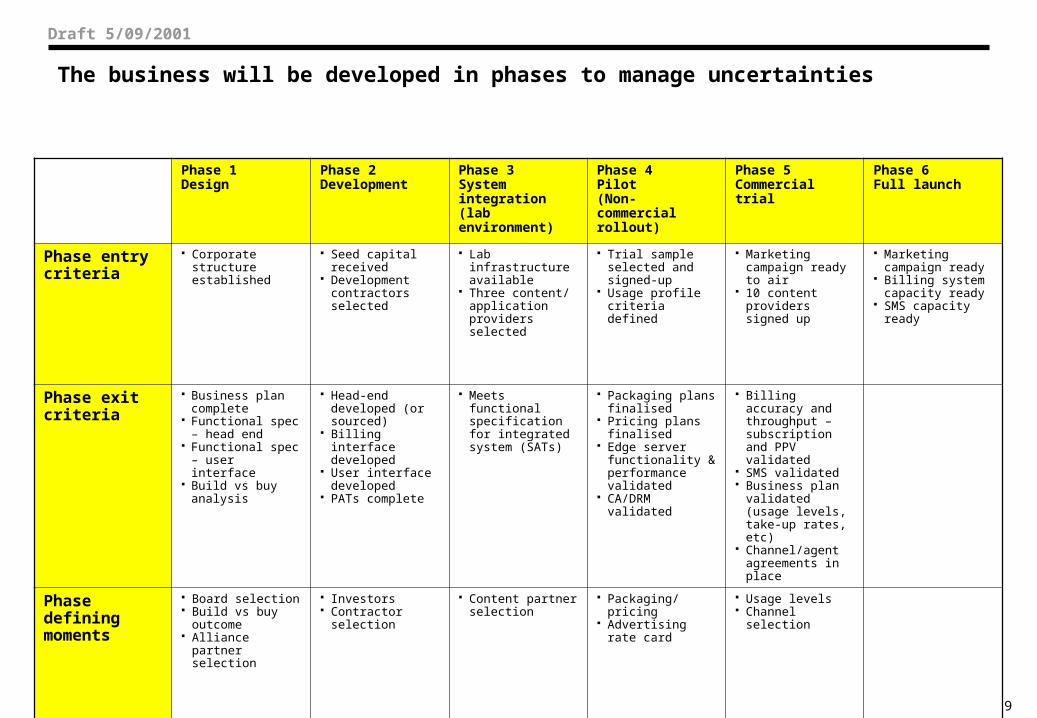

The business will be developed in phases to manage uncertainties • Phased approach matches funding risk and rollout uncertainty• Identify leading indicators to guide pace of rollout

Basedrive recognises a number of critical success factors for the execution of the business plan• Formation and management of key strategic alliances• Systems integration and project management• Time to market• Adequate funding

2

Draft 5/09/2001

Summary of business concept

Level of certainty

Level of completeness

Steps to address

What?

Basedrive interface is designed to be the single interface to the world of available content and desktop applications on a subscription or pay per view basis on a range of presentation devices

H L

Incremental approach to business development

Work closely with content and IT companies to refine vision

Where/when?

Global product limited only by marketing reach and broadband availability. M L

Develop project plan Develop market entry strategy

and rollout plan

How?

Concentrate on packaging and distributing second tier content for synchronous and asynchronous content

L L

Build vs buy analysis Strategic analysis of value chain

participation

Who?

Management team not yet in place

Shareholders not yet in place M M

Define skill requirements by phase

Define ideal shareholders, financial structure, etc

How big is the opportunity?

Australian revenues of $100m at maturity

Global revenues not yet estimated

L L

Qualitative market research Quantitative market research Non-commercial trial Commercial trial

3

Draft 5/09/2001

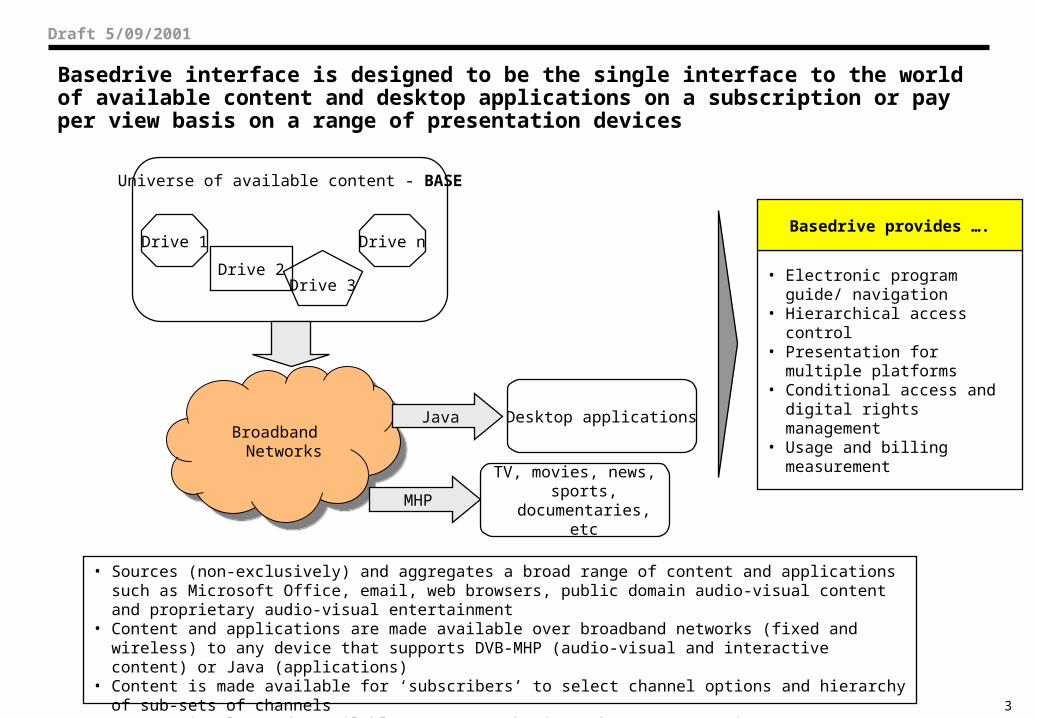

Basedrive interface is designed to be the single interface to the world of available content and desktop applications on a subscription or pay per view basis on a range of presentation devices

Universe of available content - BASE

Drive 1 Drive n

Drive 3Drive 2

Broadband Networks

Broadband Networks

Java

MHP

Desktop applications

TV, movies, news, sports, documentaries,

etc

• Electronic program guide/ navigation

• Hierarchical access control• Presentation for multiple platforms• Conditional access and digital

rights management• Usage and billing measurement

Basedrive provides ….

• Sources (non-exclusively) and aggregates a broad range of content and applications such as Microsoft Office, email, web browsers, public domain audio-visual content and proprietary audio-visual entertainment

• Content and applications are made available over broadband networks (fixed and wireless) to any device that supports DVB-MHP (audio-visual and interactive content) or Java (applications)

• Content is made available for ‘subscribers’ to select channel options and hierarchy of sub-sets of channels• Content is also made available on a usage basis such as pay-per-view or pay-per-hour of usage• Company provides authentication and access control to prevent copyright/IP infringement

4

Draft 5/09/2001

The potential market is global, constrained only by marketing reach, broadband costs and IP protection concerns

Broadband availability and price competitivenessL H

Audience/ market

size

Mass

Niche

Basedrive

Target Markets

• Hollywood vs independent studio• Language• Geographic rights• Stage in release cycle

Content value dimensions

• Edge servers/ ISP infrastructure• Level of telecom competition• Level of telecom regulation• Internet penetration• Broadband penetration• Pay-TV penetration• IP protection legislation

Infrastructure dimensions

Australia/ New ZealandUKUSA/CanadaSingapore

JapanWestern EuropeS. KoreaMalaysiaSpanish Sth America

South AfricaEastern EuropeChina

2nd tier TV content, regional news, 2nd tier apps

Delayed sports, Movie archives, independent studio movies

Premium TV content, live sports, premium apps

Content and application rollout

Geographic rollout

5

Draft 5/09/2001

Basedrive will concentrate on packaging and distribution elements of the value chain and form strategic alliances for the rest of the system

ProductionPackaging,Branding,

& Promotion

Acq

uisit

ion

DistributionSubscriber

ManagementSystems

Billing

Time-WarnerColumbiaSonyDisney…

Commercial broadcast networks (Seven, Nine, etc)Pay TV (Sky, FoxTel)…

Commercial & subscription TVWeb portalsStreaming providersEdge Server providers…

Pay TV operators…

Pay TV operatorsTelcos…

PVR

Value chain participants

Encryption BroadcastNetwork

MngtDisplay

• Production, SMS and billing are scale businesses

• Packaging and distribution can utilise “narrow casting” economics

Basedrive will use alliance partners for highly specialised system components in which Basedrive does not yet have expertise or

competitive advantage

6

Draft 5/09/2001

The Economics of broadband distribution show that feasible business models can be established in both the niche and mass markets …

BaseDrivePPV

BaseDrive

Volume – Number of simultaneous Subscribers

Unit content + distribution costs ($)

Revenue per hour viewed

.05

.1

.5

1.0

5.0

.01

10

1

1 10 100 1k 10k 100k 1m

Revenue – mass market

Cost

Profit - mass

Niche Narrow cast Broadcast - PayTV Broadcast - FTA

Cost - niche

Revenue - niche

7

Draft 5/09/2001

… based on the evolution of industry cost structures and revenue potential

Unicasts1 or video on demand of Hollywood movies or popular

sporting events

Unicasts1 of web-originated features

New types of interactive programs

High Value Today High Value in Future?

Inexpensive Uneconomical

Multicasts2 of existing TV shows

Simple interactive TV, for example – offering links text,

data, or both

Unicasts1 of broadcasters’ program archives

High-bandwidth interactive TV, for example, offering alternate

plotlines

Revenue per viewer hour

Higher (>$1 per

hour)

Lower (<$1 per

hour)

Costs per viewer-hour

Higher (>$1 per hour)

Lower (<$1 per hour)

1 Unicasts generat separate data streams for each receiver (many-to-many model)2 Multicasts generate single data stream this is received by many users simultaneously (one-to-many model)

Source: McKinsey Quarterly, 2001, Number 4

8

Draft 5/09/2001

The product has the potential to generate revenues of $93m in the Australian market

Type of deliverySynchronous

Mass

Niche

Target Markets

Asynchronous

Content

Subscription PPV

PPV

Desktop applications

PPV Subs

Volume –Australia(‘000)

36 - 360 60 - 300

Price (A$) 5 – 10 10 – 60

Paul Budde, Aug 2000: 880,000 pay-TV subscribers, excl Austar (410,000)Paul Budde, Aug 2000: Ave price of $50 p.m. equates to 25% penetration (6.2m homes in Australia)PPV take-up rates range from 20% to 200% ie. Number of PPVs per household per month (Europe.eu.net)PPV rates range from US$3 – 4 per event (Europe.eu.net)www.1globalplace.com/CountryResearch/CountryStatistics.asp?country=AU

Low Mid High

RevenuesA$ ‘000 p.a.

PPV 2,000 18,000 43,000

Subs 7,000 75,000 216,000

Total 9,000 93,000 259,000

9

Draft 5/09/2001

The business will be developed in phases to manage uncertainties

Phase 1Design

Phase 2Development

Phase 3System integration (lab environment)

Phase 4Pilot(Non-commercial rollout)

Phase 5Commercial trial

Phase 6Full launch

Phase entry criteria

Corporate structure established

Seed capital received Development

contractors selected

Lab infrastructure available

Three content/ application providers selected

Trial sample selected and signed-up

Usage profile criteria defined

Marketing campaign ready to air

10 content providers signed up

Marketing campaign ready

Billing system capacity ready

SMS capacity ready

Phase exit criteria

Business plan complete

Functional spec – head end

Functional spec – user interface

Build vs buy analysis

Head-end developed (or sourced)

Billing interface developed

User interface developed

PATs complete

Meets functional specification for integrated system (SATs)

Packaging plans finalised

Pricing plans finalised Edge server

functionality & performance validated

CA/DRM validated

Billing accuracy and throughput – subscription and PPV validated

SMS validated Business plan

validated (usage levels, take-up rates, etc)

Channel/agent agreements in place

Phase defining moments

Board selection Build vs buy outcome Alliance partner

selection

Investors Contractor selection

Content partner selection

Packaging/ pricing Advertising rate card

Usage levels Channel selection

10

Draft 5/09/2001

Basedrive recognises a number of critical success factors for the execution of the business plan

Factor Plan to address

Formation and management of key strategic alliances

Danny Schwartz has extensive experience in this area

Systems integration and project management Develop and sign off functional specification to achieve optimal system architecture

Hire appropriate staff Alliance with Sun Microsystems

Time to market Accelerate early offerings in Australian market

Develop alliances with content partners Adequate funding

Adequate funding Robust business plan Shareholders understand business model

11

Draft 5/09/2001

• Sources (non-exclusively) and aggregates a broad range of content and applications such as Microsoft Office, email, web browsers, public domain audio-visual content and proprietary audio-visual entertainment

• Content and applications are made available over broadband networks (fixed and wireless) to any device that supports DVB-MHP (audio-visual and interactive content) or Java (applications)

• Content is made available for ‘subscribers’ to select channel options and hierarchy of sub-sets of channels

• Content is also made available on a usage basis such as pay-per-view or pay-per-hour of usage

• Company provides authentication and access control to prevent copyright/IP infringement

What does the product do?

• Operates on a pay-TV and ASP business model:

• Pay-TV• Content is provided on a

subscription basis, paid in advance

• Premium or event content is provided on a PPV basis, paid in advance

• Access to the service is restricted by a secure conditional access system that can identify subscribers

• Revenue is principally derived from subscriptions, advertising is marginal and only follows once critical mass achieved

• Application Service Provider• Application access is provided

on a subscription basis (often bundled with access)

How does Base Drive make money?

• Marries two established business models: Pay-TV and ASP

• Early part of broadband growth – large upside

• Easy exit through acquisition• Opportunities to develop IP:

• User interface• Condition access• Billing

• Opportunity to redefine distribution business model for proprietary content

Why Invest?

Base Drive is developing a new content distribution business model

Basedrive provides an attractive business opportunity

12

Draft 5/09/2001

EXTRA SLIDES

13

Draft 5/09/2001

Subs

PPV

ASP

Advertising

GUI

0% 20% 40% 60% 80%

• Broadband (xDSL, cable, DTH, ..)• Multimedia Home Platform

(MHP)/Java TV technology• Media convergence• Set top box convergence• Java support on multiple platforms

including small footprint devices• VOIP• Personal video recorder (PVR)• Device convergence (PS2, STBs, etc)

Technologic Evolution

Acquisition BillingCust care

Packag-ing

Encryp-tion

Distribe

Augment

• Bandwidth chasing content• Narrow casting commercially and

legally feasible• Thin client capability• Asynchronous media consumption

supported by feasible business models

• Diminishing marginal distribution costs through the Internet

Business Trends

• Access and distribute content on a subscription and PPV basis

• Offer ASP services on a usage or subscription basis

• Develop user interface for content presentation and access management

• Develop business model

Base Drive Concept

Business Model/Revenue Streams

• Time to market• Alliance with Sun• Australian media environment

allows rapid commercialisation of concept

• Exclusive access to content

Competitive Advantages

• Prove technical viability• Demonstrate feasible approach

to IP protection• Conclude alliances with

dominant industry participants

Critical Success Factors

Proof of concept

Technical trial Commercial trial

Launch

Con

cep

tual

Fac

tors

Exe

cuti

onal

Fac

tors

BaseDriveparticipation

BaseDriveSummary

14

Draft 5/09/2001

Proof of concept

Technical trial Commercial trial

Launch

• Validate business model with market research, supplier agreements, technical investigation, etc

• Formalise relationship with Sun

• Secure three pilot content partners (SBS, …)

• Preliminary independent valuation

• Validate technical functionality in lab environment

• Achieve demonstrable offering in Australia

• Complete GUI development

• Complete CA development

• Second round of seed funding

• Validate initial market research with commercial trial (100 users)

• Complete billing system development

• Finalise product (price structures, packaging, distribution, etc)

• Third round of funding (venture capital)

• Revised independent valuation

• Non-exclusive distribution agreement with one major Hollywood studio

• Non-exclusive distribution agreement with two European studios

• Non-exclusive distribution agreement with SBS and ABC

• Adequate funding to meet business plan projections

Ob

jectives