btec level 3 national in business - wordpress.com · 01/10/2016 · btec level 3 national in...

TRANSCRIPT

BTEC Level 3 National in

Business

First teaching September 2016

Sample Marked Learner Work

External Assessment

Unit 3: Personal and Business Finance

In preparation for the first teaching from September 2016 and as a part of the on-going

support that we offer to our centres, we have been developing support materials to help

you better understand the application of Nationals BTEC Level 3 qualification.

What is Sample Marked Learner Work (SMLW)?

The following learner work has been prepared as guidance for centres and learners. It

can be used as a helpful tool when teaching and preparing for external units.

Each question explores two responses; one good response, followed by a poor response.

These responses demonstrate how marks can be both attained and lost.

The SMLW includes examples of real learners’ work, accompanied with examiner tips and

comments based on the responses of how learners performed.

Below displays the format this booklet follows. Each question will show a learner

response, followed by comments on the command verbs and the content of the question.

Tips may be offered where possible.

The appendix has attached a mark scheme showing all the possible responses that

perhaps were not explored in the SMLW, but can still be attained.

Tips offer helpful hints that the learner may find useful. For example:

Recommended length of the answer

Reference to the amount of marks awarded

General advice for the learner when answering questions

The red box comments on the command verbs used in the question. Command

typically means; to instruct or order for something to be done. Likewise, in

assessments, learners are required to answer questions, with the help of a

command verb which gives them a sense of direction when answering a question.

This box may choose to highlight the command verb used and comments if the

learner has successfully done this, or not.

The green box comments on the content words and phrases. Content makes

reference to subject knowledge that originates from the specification. Learners

are required to use subject specific knowledge to answer the questions in order to gain maximum marks.

The comments may include:

Any key words/phrases used in the learner’s answer.

Why has the learner gained x amount of marks? And why/how have they

not gained any further marks?

Any suggestions/ ideas regarding the structure of the answer.

If the answer meets full marks- why it is a strong answer? What part of

the content has been mentioned to gain these marks?

Question 1: Give two features of a premium current account.

[Total marks for Q1 – 2 marks]

Good response: The learner has stated two features that could be expected from

a premium current account. This is from section A3 bullet point 2 of the

specification which requires knowledge of the different types, features, advantages

and disadvantages, and services offered of packaged and premium accounts.

The command verb in this question is give. This is similar to list and requires a

simple identification, in this instance, of a feature of a premium current account.

Good response: The learner has correctly identified two features that a premium

account customer might expect to receive.

2

1

Poor response: In this second response, the learner has identified one correct

feature that the account holder has to pay a monthly fee.

No mark has been awarded for the first response about withdrawal and instant

access (two attempts at an answer), as these are also features of ordinary current

accounts.

Be aware this is a simple question requiring two responses

with one mark available of each response.

Question 2: Describe the role of the Financial Ombudsman Service.

[Total marks for Q2 – 2 marks]

Good response: The question is taken from section B3 of the specification, bullet

point 2, role of the FSO. The response provided has a description of the role, with

two examples of financial institutions that the FSO would negotiate/be involved

with. This is sufficient for the award of both marks. The response could have been

improved by stating that the FOS acts as an independent assessor, and/or that it

is a role set up by parliament.

Escribe the

The command verb in this question is describe, which requires a detailed account of

what is being questioned, in this case the role of the Financial Ombudsman Service.

The question requires a short open response that can include an example.

Good response: The learner has identified that the role is there to resolve disputes

of a financial nature, between consumers and financial institutions, an example of

which has been provided i.e. building societies or insurance companies. Both marks

can therefore be awarded.

This question required only one response. The marks can be

achieved by giving a detailed description or by a more basic

description with appropriate examples that demonstrate

sufficient understanding.

2

1

Poor response: In this second example, the learner has stated that the role is to

resolve disputes, but have not shown the understanding that these disputes occur

between consumer and financial institutions. Consequently only one mark can be

awarded.

Question 3: Explain two benefits of pre-paid credit cards of the type used when

on holiday. [Total marks for Q3 – 4 marks]

Good response: The question comes from section A2 of the specification about

the different ways to pay. The mark scheme allocates 1 mark for the identification

of a feature/benefit of pre-paid credit cards and the second mark for stating why

they are useful on holiday. Without this context to the use of the prepayment card

on holidays, the second mark cannot be awarded.

In the example above, one mark has been awarded for the first response, but the

second mark has not been awarded as the comment on ‘exchange’ has not been

developed. The second response has context and therefore achieves both marks

giving a total mark for the question of 3 marks.

The command verb ‘Explain’ requires learners’ work to show clear details of the

benefits of using pre-paid credit cards. The explanation also needs to provide

reasons and/or evidence to support the view that they are a benefit. The

question needs two benefits which the learner has attempted to provide.

3

22

Poor response: In this second example, the learner has identified two features

but has failed to provide a context for either response and has therefore been

limited to 2 marks.

Learners need to be taught to read the question fully. If

context is provided then this should be used in the response

to ensure full marks can be awarded.

Question 4: Discuss why it is important for Shekemi to avoid getting into

unmanageable debt. [Total marks for Q4 – 6 marks]

Good response: The learner has provided a logical and relatively accurate

response to the question. They have discussed the fact that that when money is

borrowed, the longer the repayment term, the higher the cost of repayment. A

second point about an individual’s credit rating would be affected by getting into

debt is made. Both of these points are shown in the indicative content section of

the mark scheme. Both of the issues are developed to identify that in the long term

this could cause problems when trying to obtain further credit. The first part of the

response suggests that interest rates could change during the repayment period.

This is not always the case i.e. with fixed rate loans, but the development has been

credited. This response is further developed by identifying that failure to pay back

the debt will incur further charges. . Whilst the argument is not well constructed,

the learner has demonstrated accurate understanding and has used the context of

the question, whilst showing logical reasoning. The response has been awarded 4

marks, top of band 2.

The question is taken from section A1 of the specification about planning to avoid

debt. The command verb is ‘Discuss’. Here, learners need to consider different

aspects of the topic, in this instance debt. The response should demonstrate clear

understanding of a range of issues linked to the question, and explain why this

might be a problem. A conclusion is not required.

Good response: In this response, the learner has provided two developed points

that address the issue of debt.

This is a levels of response mark scheme where learners have to demonstrate

accurate knowledge and understanding with logical reasoning and clarity in order

to achieve marks in the middle band.

4

Poor response: In the second response, the learner has identified that

unmanageable debt could lead to bankruptcy and can lead to stress on the

individual. The first response has some limited development but is insufficient to

move this out of mark band 1, and is therefore awarded 2 marks.

Learners should be encouraged to use the PEEL approach to

answering questions of this type. They should state a point,

refer to evidence either from the stimulus material or from

their own examples, and then evaluate the impact of the point

before clonking this back to the question.

2

Question 5: Assess the use of Premium Bonds as a method of saving.

[Total marks for Q5 – 10 marks]

The question uses the command verb ‘Assess’. This requires learners to provide a

careful and considered response using a number of points/issues that are linked

to the specific context. Both sides of the issue will be considered such as the

advantages and disadvantages associated with premium bonds as a form of

saving, and a conclusion will be present if the learner is to score higher marks.

Good response: In this response the learner has made strong points in favour of

the use of premium bonds, but the argument against their use is not as strong or

well developed. This has limited the marks awarded to mark band 2.

6

Good response: This is a reasonable response to a question from section A4 of

the specification that looks at the features, advantages and disadvantages of

different types of saving and investment.

The learner has correctly identified that there is an opportunity to win a monthly

prize and has identified the value of the prize. They have also correctly identified

that funds can be deposited and withdrawn at will and that if a prize is won, the

return on the investment will be greater than the interest that could have been

achieved by other forms of saving/investment.

The alternate view is not as well developed, but the learner does state that

premium bonds do not attract interest that could be expected from other types of

account.

No formal conclusion has been drawn, but the learner has provided a response that

shows accurate knowledge with some imbalance, but with appropriate context. The

response has therefore been awarded 6 marks which is the top of band 2. To

achieve band 3, both sides of the discussion should have been developed and a

conclusion would be present.

To achieve the top mark band in this type of question, both

sides of the argument/discussion must be equally developed

and a conclusion should be present.

Poor response: In this second response, the learner has made some simple points

about premium bonds being backed by the government and that this makes them

safe. There is also a point made that there is a chance to win a prize. There is an

incorrect statement that the value of the investment will not go down, which it

does, when inflation is taken into account. The work has not been developed and is

therefore capped at mark band 1, achieving 2 marks.

2

Question 6: Evaluate which student current account would be most suitable for

Nick. [Total marks for Q6- 12 marks]

8

Good response: The response considers factors such as some of the banks will pay

interest on credit balances in the current account, and that Santander offers the

highest interest of 3%. The response also details that all four providers offer a 0%

free overdraft, with one offering £3,000. Other content that is/could be include is

the

8% interest he would have to pay with Lloyds and that three providers charge high

fees for an unauthorised overdraft. The response is well considered with a range of

points discussed both positive and negative. Each of these is developed in the

context of the young person in the stimulus. There is balance in the response and

the context is used throughout. The work lacks a little clarity in places and the data

provided could have been discussed in a little more detail. A supported conclusion is

present. The response is therefore awarded 8 marks which is the middle of mark

band 3.

The question is from section A3 of the specification – different types of account.

The command verb used is ‘Evaluate’. This requires learners to draw from the

varied data provided in the stimulus and consider aspects such as the advantages

and disadvantages of the theme or concept, and to consider the relevance in light

of the context provided. In this instance, learners should consider the different

student accounts, comparing advantages and disadvantages which are relevant to

the actual individual in the stimulus.

Good response: The response provided in this example has compared a number

of features and suggested why they might be beneficial to the student in the

stimulus. They have also come to a reasoned conclusion as to the best account.

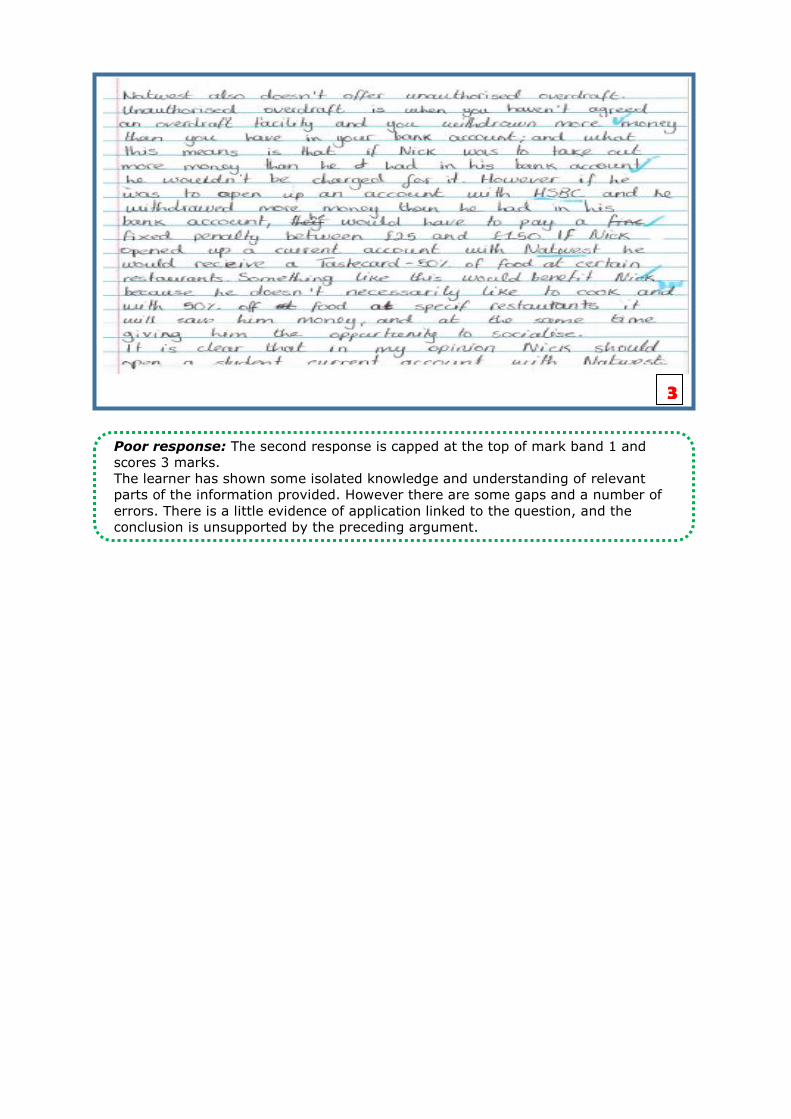

Poor response: The second response is capped at the top of mark band 1 and

scores 3 marks.

The learner has shown some isolated knowledge and understanding of relevant

parts of the information provided. However there are some gaps and a number of

errors. There is a little evidence of application linked to the question, and the

conclusion is unsupported by the preceding argument.

3

Question 7: Identify two types of intangible non-current assets.

[Total marks for Q7 – 2 marks]

Poor response: In this second response, the learner has correctly identified that

an intangible asset is one that cannot be touched i.e. it is not a physical asset.

However, the two examples provided are both incorrect and thus achieve no marks.

The command verb ‘Identify’ requires learners to list or state two types of

intangible assets.

Good response: The learner has identified two of the intangible assets identified in

section C3 of the specification.

Good response: The learner has provided two correct responses, ‘Brand’ Name and

‘Goodwill’. ‘Patents’ and ‘Trade marks’ would also have been a correct response.

There is no requirement for the response to be written in sentence form and this

would have wasted time.

In this question, learners need to know what an intangible

asset is, if they are to correctly give examples. Learners should

ensure they know both definitions of key terms and can give

examples of them.

2

0

Question 8: Outline what is meant by ‘capital income’.

[Total marks for Q8 – 2 marks]

The command verb ‘Outline’ requires a short summary or brief description to

demonstrate understanding of the term ‘Capital Income’

Good response: The learner has briefly described what this is, and has developed the

response by identifying correctly, the financial statement where this type of income is

found. Types of Capital Income are identified in section C2 of the specification.

Good response: In this response, the learner has correctly identified that capital

income is money invested in the business. They have developed the response by

showing understanding of which financial statement shows capital income. Other

correct responses would have included loans, mortgages, owner’s capital and

debentures.

Poor response: In this second response, the learner has identified that capital

income comes into the business from ‘selling shares. The response ends there and

achieves only 1 mark. To gain the development mark, the learner could have

commented that this is provided by investors, or that this is different to the day to

day capital gained by selling goods or services.

2

1

Question 9a: Calculate Connor’s new gross profit figure.

[Total marks for Q9a – 3 marks]

The command verb used in this question is ‘calculate’ and requires the learner to

work out a new Gross Profit level from a given set of data where one set of data

has been changed. The learner is required to recall the correct formula for gross

profit and then carry out the calculation accurately.

Learners are asked to show working out so that process marks can be awarded if

the final answer is not correct.

There are different ways in which the learner could achieve full marks. The

quickest method would be to calculate the difference between the closing stock

figures, £308, and then add this to the gross profit given in the question.

Good response: In the response above, the learner has carried out the calculation

from first principles, first working out the new cost of sales before subtracting this

from the revenue to reach the new gross profit figure of £614,151.

The completion, calculation or amendment of a gross profit figure is identified in

section F1 of the specification.

3

Calculation questions usually ask learners to show

working out. Learners should always do this so an

examiner can award process marks if the final answer

is incorrect as shown in the example above.

If a calculation from one part of a question is carried

over to another part of the question the learner won’t

be penalised twice. The original error loses the mark;

the ‘carry forward’ of this incorrect figure is not

penalised – so long as learner uses this own original figure.

Poor response: In this second response, the learner has attempted to carry out

the required calculation but has made a number of errors. The learner has made an

error in transposing both closing inventory figures and the final answer is incorrect

when allowing for own figure rule. One mark has been awarded for showing an

understanding of the formula ‘old gross profit - old closing inventory + new closing

inventory’.

1

Question 9b: Calculate the inventory turnover.

[Total marks for Q9b – 4 marks]

This question also uses ‘Calculate’ as the command verb. Learners have to calculate

the inventory turnover using the data given in question 9a. This question is based on

measuring efficiency from section F5 of the specification. In this question, learners

could have calculated inventory turnover in numbers of days, or used the alternative

formula (cost of sales/average stock), to give the response as a number of time per

year.

Good response: The response above was awarded full marks. The learner has shown

both formula (inventory turnover and average stock), which would have achieves

marks had no further work been provided. The learner has calculated the average

stock, then calculated the cost of goods sold before using both of these results to

calculate the inventory turnover in numbers of days. The result of the calculation has

then been transposed on to the answer line in the working box.

Poor response: The response above gains 1 mark for stating the correct formula for

inventory turnover in numbers of days.

1

4

Check the specification. This will advise which formulas,

if any, that will be given in the exam. Where formulas

are not given, learners will need to recall these and they

should be well practiced in carrying out the calculations.

Where alternative formulas or terms exist, learners

should be able to recall all forms.

Question 9c: Using your gross profit figure from part (a), calculate Connor’s

profit or loss for this year.

[Total marks for Q9c – 8 marks]

In this question the learner is asked to calculate profit for the year, using the gross

profit figure they calculated in question 9a and other data provided in the question.

They have also been given a cumulative depreciation figure for a van and have to

calculate this year’s depreciation, using the reducing balance method, so an overall

profit for the year figure can be determined. The completion of the comprehensive

income statement including making adjustments for prepayments accruals and

depreciation is in section F1 of the specification.

Good response: The learner’s response is awarded full marks. The answer is well

laid out showing first the gross profit figure from question 9a, before making the

prepayment adjustment to wages, the accruals adjustment to electricity, and the

calculation of depreciation for the year. The learner has then calculated the total

expenses and deducted this value from the gross profit to finish with the correct

profit for the year figure of £377,522.

8

Try to get learners to use formulae to show their working

out and use labels where necessary – it makes it easier to

award process marks.

Learner must use the correct separator when writing down

values. £377,522 and £377522 are both acceptable

responses to this question. £377.522 and £372.522 are not

acceptable representations of values in a finance paper and

marks could not be awarded for this response, but process

marks would be awarded.

Poor response: In this second response the learner has used an incorrect value

for gross profit carried forward from question 9a, but is not penalised for this.

Marks have been awarded for the correct calculation of the new wages and

electricity values, but no marks have been awarded for the depreciation calculation

which is in error. Finally, marks have been awarded for the correct use of the

‘other expenses’ value, for the correct formula for profit for the year, and for the

calculation of the final profit where own figure rule has been applied so that the

learner is not penalised twice for the two errors (depreciation and GP from

question 9a. The learner has therefore been awarded 5 marks.

5

Question 9d: Calculate the new net book value for the motor vehicle.

[Total marks for Q9d – 3 marks]

Once again learners are asked to perform a calculation and to show their working out

of the net book value of non-current assets in the statement of financial position

(section F2 of the specification). This question requires recall and the ability of the

learner to select the right data and to accurately perform the calculation.

Good response: In this response, the correct data and formula have been

identified. The learner has calculated the balance from the previous year and then

adjusted this for the current year’s depreciation to arrive at the new net book value

of £5950.

Remember to write down all formulae when answering

calculation questions.

Poor response: In this second response, the learner has attempted to write a

formula but has left this incomplete. As there is no further work provided, this

response scores zero marks. Had the learner completed the formula i.e. net book

value – asset cost – depreciation, 1 mark could have been awarded.

0

3

Question 10a: Calculate the margin of safety. [Total marks for Q10a – 4 marks]

Another calculate command verb. Here the learner needs to be able to calculate

the break-even point and then use this to calculate the margin of safety –

specification section E2 Break-even analysis.

Good response: The learner in this example has provided an almost exemplary

response. They have quoted the formula for both break even and margin of safety.

They have then used the data provided in the question stimulus to find the unit

variable cost and then used this to establish the break-even quantity of 66,000

cheeses. The learner has then converted the monthly production to an annual

production and subtracted the break-even quantity to arrive at the margin of safety.

In two parts of the response the learner has omitted one zero from the actual

production figure (quoting 24000 rather than 240000), but has corrected this error

when completing the calculation and writing the answer in the answer box. The

answer box has a £ sign already printed on the exam paper, but this is an error as

the MOS should be a quantity not a value.

4

It is better to attempt every question even if they are left

incomplete, rather than leave a question unanswered.

Poor response: In this second response, the learner has achieved one mark for

quoting the break-even formulae. They have then input the actual figures into this

formula but this does not warrant the award of a further mark. Finally, the learner

correctly calculates the break-even point and achieves a second mark. No other

evidence is provided leaving the question incomplete and giving the learner 2 marks

overall for this response.

1

Question 10b: Calculate how many months it will take to reach the break-even

point. [Total marks for Q10b – 2 marks]

Another calculate command verb where the learner has to use the break-even point

calculated as part of the last question to establish how many months it would take

the business to reach the breakeven level of output - section E2 of the unit

specification.

Good response: In this response the learner has correctly taken the break-even

point (66,000 units) from the previous working out, and divided this by the monthly

output (20,000 unit) quoted in the question, to arrive at the correct answer of 3.3

months.

2

0

Poor response: In this second response the learner has again calculated the break-

even point (66,000 units) but no marks are allocated in the mark scheme in this

question. The learner has failed to divide this value by the monthly production level.

It is not possible to deduce from this response that the learner understands the

process by which the number of months required to break even is calculated. They

have stated an answer, 3 months, but this is incorrect and therefore no marks can be

awarded.

Question 11: Discuss the benefits of crowd-funding to a business such as

Connor’s. [Total marks for Q11 – 6 marks]

6

The command verb for this question is ‘discuss’. This requires learners to consider

different aspects of a theme or topic. The response should show how the topic or

concept relates and is linked to the context.

The importance of different factors should also be considered such as does the

owner wish to keep full control or is he prepared to give up some equity. A

conclusion is not required.

Good response: The response above demonstrates accurate and thorough

knowledge and understanding of crowd funding as an alternative source of finance

for a business expansion. There are few gaps or omissions. The response is well

developed. A point is made and this is then explained in context of the business.

There is balance with both negative and positive sides of crowd funding discussed.

This demonstrate a good grasp of the competing arguments, and alternative

approaches which are fully in context are offered.

There is logical reasoning evident throughout the response which is clear and uses

specialist technical language consistently. The response therefore achieves full

marks, top of mark band 3.

6

Remember that the ‘discuss’ command verb requires a

balance (two sided) argument. This skill should be practiced

to ensure marks are not lost on the extended writing

questions.

Poor response: The second response achieves 3 marks, bottom of mark band 2.

There is some demonstration of knowledge and understanding of crowd funding as an

alternative source of finance for a business expansion. The response is not well

developed and is more of a list of points in places. There is no balance with only the

positive sides of crowd funding discussed. There is a small amount of context with the

reference to the new product but this should have been developed further. There is

some use of specialist technical language. To improve this response, the learner

should develop each of the points made and there should be some use of negative

consequences to add balance to the discussion

3

Question 12: Analyse the effect of a negative bank balance on a business such as

Connor’s. [Total marks for Q12 – 8 marks]

The command verb used in this question is analyse which requires learners to

present a detailed and logical examination of the topic – in this instance the effect a

negative bank balance would have on a business. There needs to be an interpretation

of any data provided in the question and the relationship between the data and the

question must be clearly explained. In order to achieve the highest grades, there

needs to be accuracy in the work, showing thorough knowledge and understanding of

the key issues and the response should be balanced. This question is taken from

section E1 of the specification -Prepare, complete, analyse, revise and evaluate cash

flow.

Good response: The response has scored 6 marks which is top of mark band 2. The

learner has demonstrated understanding that a cash flow problem could lead to an

increase in overdraft and that the implications are the business would struggle to pay

suppliers and meet deadlines. This is developed to show that suppliers may therefore

refuse the business credit which in turn could lead to the business not being able to

obtain stock. This response could have been improved further had this point been

further developed to show that failing to obtain stock or failing to pay suppliers would

hamper the ability to sell further goods and could have meant the firm had legal

proceedings instigated to recover any outstanding debts and this would have cause

further cash problems. The learner then suggests that if the overdraft grows this will

incur more interest which will worsen the cash position and possibly prevent the

business obtaining further loans, thus restricting expansion. The response shows

understanding, is logical and makes the linkages required. It is however unbalanced,

focusing only on the negative points. For example the problem could be caused by

the rapid growth of the business and may be a short term problem linked to timing.

As a consequence, the response does not get into mark band 3.

6

Learners should have lots of opportunity to practice

extended writing questions as well as focussing on the more

numeric questions linked to finance.

Learners should not response to extended writing questions

in list form unless they are about to run out of time.

Responses that are not developed will not get out of mark

band 1.

Poor response: The response has scored 3 marks which is top of mark band 1. The

learner has demonstrated some understanding of the issues of an increasing

overdraft but this has taken the form of a list with no development of any of the

points made. Even though five valid points have been made, the answer is capped

to mark band 1 and the learner scores only 3 marks.

3

Question 13: Assess the use of early payment discounting and debt factoring in

improving Connor’s cash flow. [Total marks for Q13 – 10 marks]

The question comes from section D1 of the specification (sources of finance) and is

clearly linked to the previous question on cash flow problems. The question uses

the command verb ‘Assess’, and this requires learners to provide a careful and

considered response using a number of points/issues that are linked to the specific

context. Both sides of the issue will be considered such as which of the two

methods of improving cash flow may be more beneficial to Connor’s business. Both

forms of finance must be considered in any response and a conclusion will be

normally be present if the learner is to score higher marks.

To achieve the highest marks, learners responses will have be logical, well-

reasoned, balanced, have clear links to the context and use specialist technical

language.

Good response: The response shown above has scored 8 marks – top of mark band

2.

The work first considered early payment discounting –shown in the specification as

invoice discounting. There is a definition followed by an explanation of how this

would encourage customers who bought on credit to make early payments and

therefore minimise the overdraft. This could have been developed further to explain

how this would prevent the cash flow problems identified in the previous question.

The down side of this method – the reduction in unit profit and reduced sales is also

considered. This is starting to show balance. The response then considers debt

factoring and the answer shows good understanding and knowledge. Effectively the

development for this part of the response is very similar to that of the previous part,

but the comments are accurate and factual. There is no conclusion present but the

response is balanced considering both methods and looking at the positives and

negatives, of each method, in equal proportion.

8

If a question has two options that a business might choose,

the learners answer must consider both if they are to score

higher than mark band 1.

Poor response: This second response has scored 2 marks – middle of mark band

1.

The work at first is unfocused. The learner does not make explicit until half way

through the answer that they discussing early payment discounts/ invoice

discounting. There is also a lack of clear understanding shown, but then the learner

makes some valid points with limited development.

There is no content on the second source of finance, debt factoring and thus there

is no balance and limited knowledge demonstrated.

2

Question 14: Evaluate Connor’s financial position using the data in the table of

financial ratios. [Total marks for Q14 – 12 marks]

The final question is from section F3 to F5 of the specification – different ratios and

measures of profitability and efficiency. The command verb used is ‘Evaluate’. This

requires learners to draw from the varied data provided in the stimulus and consider

aspects such as whether the efficiency and profitability f the business is improving

or decreasing year on year. The learners must use the data and comment upon it,

not simply requote the figures. Learners need to consider the relevant importance of

the ration or the changes that have taken place. Some may be more important than

others. The learners then have to provide a conclusion based on the prior analysis

and interpretation of the data to say what these data show about the business

performance.

9

Good response: In this learner’s response, they have divided their answer into

the three separate sections from the specification; F3- profitability, F4-Liquidity

and F5- efficiency.

The learner makes a point about gross profit and overall profit margin

increasing. They develop this by suggesting why the change may have taken

place – cheaper suppliers, and demonstrated clear understanding of what an

increase in margin means for the business i.e. they are now keeping 12 pence in

the pound as profit.

In the second paragraph, the learner comments on the change in the current

ratio and demonstrates knowledge of what this means. This is developed by

suggesting that whist the ratio has fallen, it is still within expected guidelines of

1.5:1 to 2:1 and that the business should not be too concerned. There is a lack

of clarity where the learner states the business has enough profit to pay bills.

What they should have said is that the business has enough assets to pay its

liabilities.

In the final paragraph, the learner identifies that trade receivables are taking

longer to come in from customers which is bad, and that this is made worse by

trade payables being paid to suppliers sooner than the previous year. There is

further development that if trade receivables are extended, then it would be

reasonable to expect trade payables to be extended but this has not happened.

The work demonstrates accurate knowledge and understanding of relevant

ratios and the information presented. There is evidence of application

demonstrating linkages and interrelationships between the ratios. There is

however no final conclusion that would limit the mark awarded. The response

displays a balanced between the three parts of the specification. There is a

logical organisation to the work and appropriate specialist technical language.

The mark awarded was 9, bottom of level 3.

For questions such as the one above where data is provided,

learners are expected to use the data in some way, not simply

requote figures otherwise marks will be capped at mark band 1.

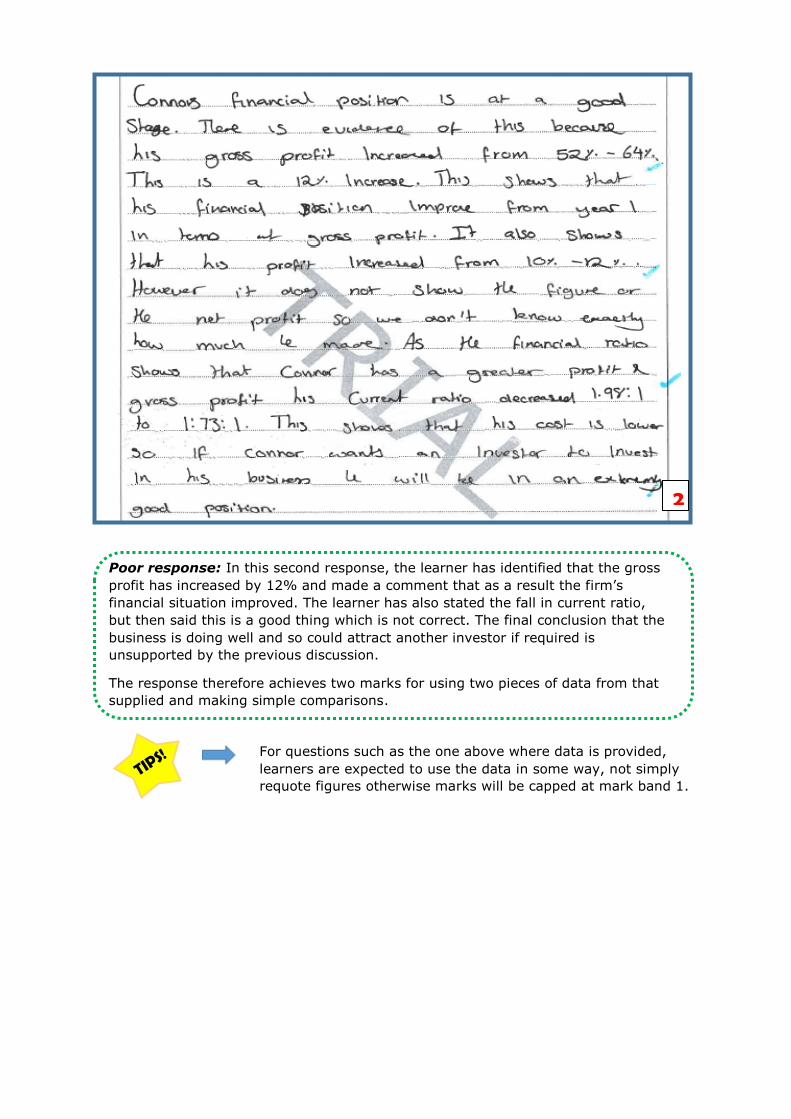

Poor response: In this second response, the learner has identified that the gross

profit has increased by 12% and made a comment that as a result the firm’s

financial situation improved. The learner has also stated the fall in current ratio,

but then said this is a good thing which is not correct. The final conclusion that the

business is doing well and so could attract another investor if required is

unsupported by the previous discussion.

The response therefore achieves two marks for using two pieces of data from that

supplied and making simple comparisons.

2

*S50318A01818*18

14 Evaluate Connor’s financial position using the data in the table of financial ratios.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Total for Question 14 = 12 marks

END OF EXAM TOTAL FOR SECTION B = 64 MARKSTOTAL FOR PAPER = 100 MARKS

Unit 3: Personal and Business Finance – sample mark scheme

General marking guidance________________________________ • All learners must receive the same treatment. Examiners must mark the first learner

in exactly the same way as they mark the last.• Mark schemes should be applied positively. Learners must be rewarded for what

they have shown they can do, rather than be penalised for omissions.• Examiners should mark according to the mark scheme, not according to their

perception of where the grade boundaries may lie.• All marks on the mark scheme should be used appropriately.• All the marks on the mark scheme are designed to be awarded. Examiners should

always award full marks if deserved, i.e. if the answer matches the mark scheme.Examiners should also be prepared to award zero marks if the learner’s response isnot worthy of credit according to the mark scheme.

• Where some judgement is required, mark schemes will provide the principles bywhich marks will be awarded and exemplification may be limited.

• When examiners are in doubt regarding the application of the mark scheme to alearner’s response, the team leader must be consulted.

• Crossed-out work should be marked UNLESS the learner has replaced it with analternative response.

Specific marking guidance for levels-based mark schemes

Levels-based mark schemes (LBMS) have been designed to assess learner work holistically. They consist of two parts: indicative content and levels-based descriptors. Indicative content reflects specific content-related points that a learner might make. Levels-based descriptors articulate the skills that a learner is likely to demonstrate in relation to the assessment outcomes being targeted by the question. Different rows within the levels represent the progression of these skills. When using a levels-based mark scheme, the ‘best fit’ approach should be used. • Examiners should first make a holistic judgement on which band most closely

matches the learner’s response and place it within that band. Learners will be placedin the band that best describes their answer.

• The mark awarded within the band will be decided based on the quality of the answerin response to the assessment focus/objective and will be modified according to howsecurely all bullet points are displayed at that band.

• Marks will be awarded towards the top or bottom of that band depending on howthey have evidenced each of the descriptor bullet points.

Section A Personal Finance Question number Answer Mark

1 1 mark for each feature identified, up to a maximum of 2 marks: • pay a monthly fee (1)

• phone insurance (1)

• travel insurance (1)

• membership discount (1)

• breakdown cover (1)

• cinema tickets (1)

• free overdraft (1).

Accept any other reasonable answer. (2)

Question number Answer Mark

2 Up to 2 marks for a description of the role of the ombudsman: • acts as an independent assessor (1) when dealing with

complaints between consumers and financial service providers (1)

• set up by Parliament (1) to sort out individual complaintsbetween consumers and financial service providers that theycan’t solve themselves (1).

Accept any other correct answer. (2)

Question number Answer Mark

3 1 mark for identification of a feature of pre-paid credit cards and 1 mark for a reason why they are useful on holiday: • it allows you to take money on holiday in a safe and secure way

(1) because if the pre–paid credit card is stolen it cannot be used without the PIN (1)

• it will allow you to control spending (1) as the card will be up toa fixed amount (1)

• can act as a budget (1) and money not spent can be returned(1).

Accept any other correct answer. (4)

3

Question number Indicative Content Mark

4 Points candidates may use: • because debt could be very expensive due to interest payments

and bank charges

• could cause stress

• could give a bad credit rating

• which may mean it will be more difficult to borrow money in thefuture as the normal high street providers might not lend

• so your choice of product may be limited

• might have to go to other more expensive providers

• may not be able to get the best deals as seen as a risk

• could lead to bankruptcy.(6)

Level Mark Award up to 6 marks. Refer to the guidance on the cover of this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–2 • Demonstrates isolated knowledge and understanding of relevantinformation; there may be major gaps or omissions.

• Provides little evidence of weighing up of competingarguments/pros and cons in context; discussion likely to consistof basic description of information.

• Meaning may be conveyed but in a non-specialist way; responselacks clarity and fails to provide an adequate answer to thequestion.

2 3–4 • Demonstrates accurate knowledge and understanding of relevantinformation with a few gaps or omissions.

• Discussion is partially developed, but will be imbalanced.Evidences the weighing up of competing arguments/pros andcons in context.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

3 5–6 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissions areminor.

• Displays a well-developed and balanced discussion,demonstrating a thorough grasp of competing arguments/prosand cons in context.

• Logical reasoning evidenced throughout response which is clearand uses specialist technical language consistently.

Question number Indicative content Mark

5 Points candidates may use are: Advantages: • premium bonds are a tax free method of saving

• don’t lose initial investment

• no risk

• withdraw money at any time

• entered into a monthly lottery to win cash prizes ranging from£25 to £1 million

• can invest £100 up to £40,000

• buy these online or through the Post Office.

Disadvantages: • not guaranteed to win

• no interest paid

• initial investment loses value with inflation

• no updates/regular statements may mean the owner forgetsabout them.

(10) Level Mark Award up to 10 marks. Refer to the guidance on the cover of

this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–3 • Demonstrates isolated knowledge and understanding of relevantinformation; there may be major gaps or omissions.

• Provides little evidence of weighing up of competingarguments/pros and cons in context; discussion likely to consistof basic description of information.

• Meaning may be conveyed but in a non-specialist way;response lacks clarity and fails to provide an adequate answerto the question.

2 4–6 • Demonstrates accurate knowledge and understanding ofrelevant information with a few gaps or omissions.

• Discussion is partially developed, but will be imbalanced.Evidences the weighing up of competing arguments/pros andcons in context.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

3 7–10 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissions

are minor.

• Displays a well-developed and balanced discussion,demonstrating a thorough grasp of competing arguments/prosand cons in context.

• Logical reasoning evidenced throughout response which is clearand uses specialist technical language consistently.

Question number Indicative content Mark

6 • Lloyds and Santander will pay interest on credit balances in thecurrent account.

• Santander offers the highest interest of 3% and up to thehighest amount. He might not have that amount of money buthe will be getting some reward.

• All four providers offer a 0% free overdraft, with HSBC offeringthe largest at £3,000. This is good because Nick won't have topay interest, but he might not like this as it might encouragehim to spend more than he needs.

• Only one provider, Lloyds, allows him to extend his overdraft.This would give Nick flexibility if he needs it, but he would haveto pay 8% interest.

• Three providers charge high fees for an unauthorised overdraft.

• All four providers give offers, but probably the best offer may bethe railcard with Santander as it will help him save moneytravelling to and from university.

(12) Level Mark Award up to 12 marks. Refer to the guidance on the cover of

this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–3 • Demonstrates isolated knowledge and understanding of relevantinformation; there may be major gaps or omissions.

• Provides little evidence of application and links between relevantinformation. Evaluation likely to consist of basic description ofinformation.

• Conclusions may be presented, but are likely to be genericassertions rather than supported by evidence.

• Meaning may be conveyed but in a non-specialist way; responselacks clarity and fails to provide an adequate answer to thequestion.

2 4–6 • Demonstrates accurate knowledge and understanding of relevantinformation with a few omissions.

• Evidence of application demonstrating some linkages andinterrelationships between factors leading to ajudgement/judgements being made.

• Evaluation is presented leading to conclusions but some may belacking support.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

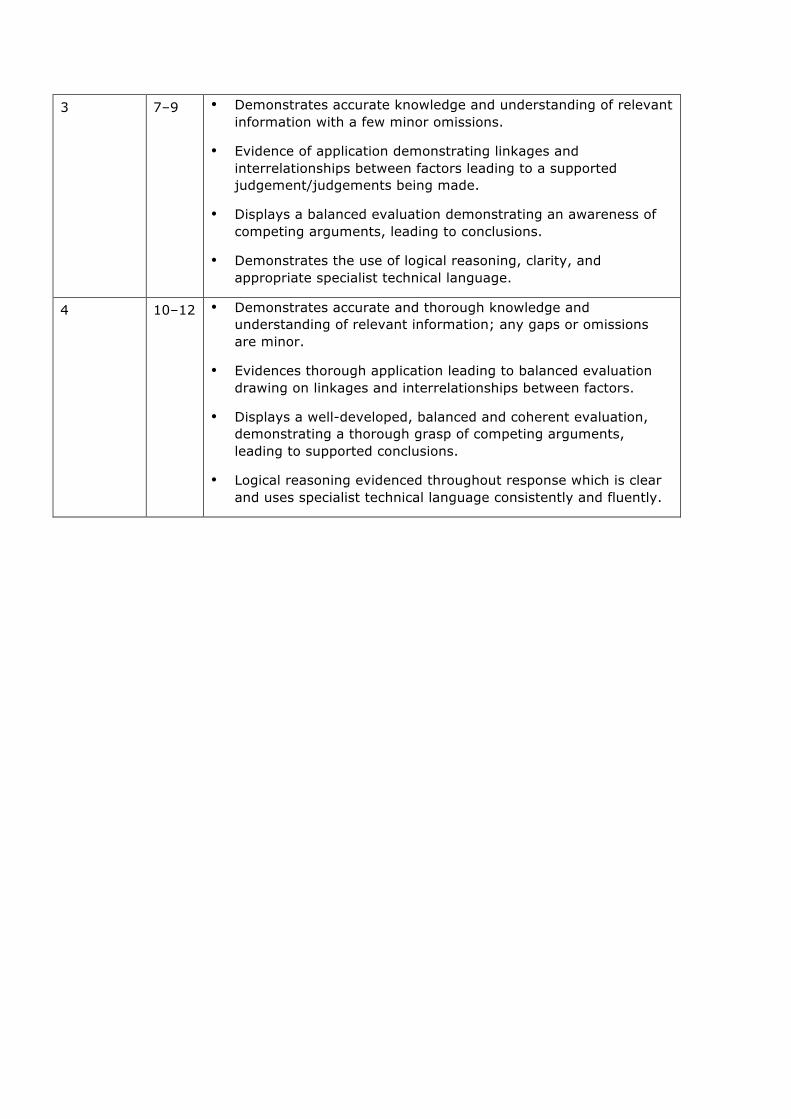

3 7–9 • Demonstrates accurate knowledge and understanding of relevantinformation with a few minor omissions.

• Evidence of application demonstrating linkages andinterrelationships between factors leading to a supportedjudgement/judgements being made.

• Displays a balanced evaluation demonstrating an awareness ofcompeting arguments, leading to conclusions.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

4 10–12 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissionsare minor.

• Evidences thorough application leading to balanced evaluationdrawing on linkages and interrelationships between factors.

• Displays a well-developed, balanced and coherent evaluation,demonstrating a thorough grasp of competing arguments,leading to supported conclusions.

• Logical reasoning evidenced throughout response which is clearand uses specialist technical language consistently and fluently.

Section B Business Finance Question number Answer Mark

7 1 mark for each type identified, up to a maximum of 2 marks: • goodwill (1)

• patents (1)

• trademarks (1)

• brand names (1).

Accept any other reasonable answer. (2)

Question number Answer Mark

8 1 mark for each correct meaning, up to a maximum of 2 marks: • capital income is the amount of money invested in the

business(1) and appears on the statement of financial position (1)

• capital income is income which comes from wealth itself(1) and not the day to day running of the business (1)

• capital income is income generated by an asset over time(1) and will not directly affect profit (1).

Accept any other reasonable answer. (2)

Question number Answer Mark

9(a) difference in closing stock: 49,102 – 48,794 = 308 (1)

new gross profit: 613,843 + 308 (1) = 614,151 (1) ofr = own figure rule If a calculation from one part of a question is carried over to another part of the question the learner won’t be penalised twice. The original error loses mark; the ‘carry forward’ of it doesn’t – so long as learner uses own original figure.

OR

613,843 – 48,798(1) + 49,102 (1) = 614,151 (1) (3)

Question number Answer Mark

9(b) (average stock/cost of sales ) × 365 (1)

average stock = (36,325 + 49,102)/2 = 42,713.5 (1) cost of sales = (36,325 + 348,973 – 49,102 = 336,196 (1) (42,713.5/336,196) × 365 = 46.37 days

cost of sales/average stock (1) average stock = (36,325 + 49,102)/2 (1) cost of sales = (36,325+348,973 – 49,102 = 336,196 (1) = 336,196/42,713.5 = 7.87 (1) (4)

Question number Answer Mark

9(c) Working Gross profit 614,151 Less expenses

Electricity 44,130 43,272 + 858 2 marks for CAO (correct answer only) Maximum 1 mark for use of incorrect function

Wages 83,116 84,327 – 1,211 2 marks for CAO Maximum 1 mark for use of incorrect function

Depreciation 1,050 (18,000 −11,000) × 15% 2 marks for CAO Maximum 1 mark for use of incorrect function

Other expenses 108,333 (1) Profit 377,352 (1ofr) (8)

Question number Answer Mark

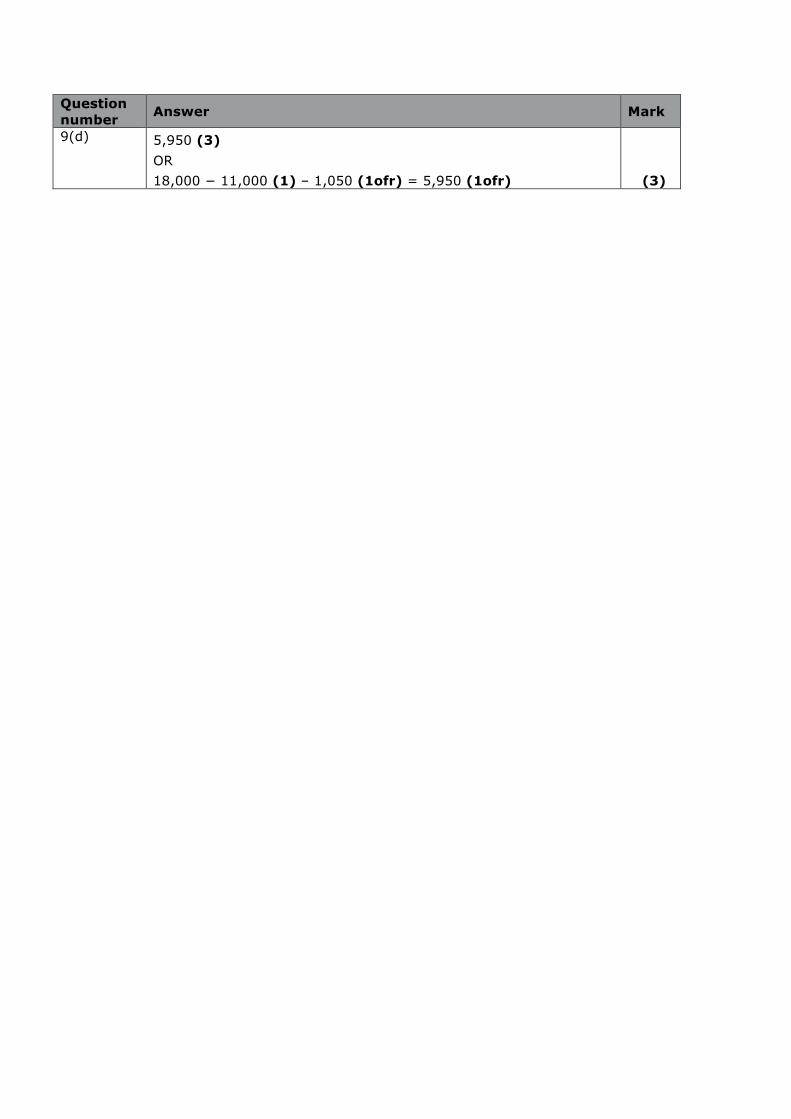

9(d) 5,950 (3)

OR 18,000 − 11,000 (1) – 1,050 (1ofr) = 5,950 (1ofr) (3)

Question number Answer Mark

10(a) Maximum 4 marks for CAO = 174,000

Workings: break-even: fixed cost/contribution per unit (1) OR break-even point = 132,000/3.50 − 1.50 (1) break-even point = 66,000 cheeses (1)

annual production = 20,000 × 12 = 240,000 cheeses (1)

MOS = 240,000 − 66,000 = 174,000 cheeses (1ofr) (4)

Question number Answer Mark

10(b) Maximum 2 marks for CAO = 3.3 Workings: 66,000/20,000 (1) = 3.3 months (1ofr) (2)

Question number

Indicative content Mark

11 • Crowd-funding – raising external finance from a number ofpeople or organisations normally via the internet.

• Connor could use it as a reward by paying interest to investors.

• It can be more expensive, but they may be more supportive to abusiness like Connor's.

• Connor could pay them in products rather than a financialreward which could help with his cash flow.

• Connor could also use it as an equity-based/Dragons’ Densolution where they become part owner of the business.

(6) Level Mark Award up to 6 marks. Refer to the guidance on the cover of

this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–2 • Demonstrates isolated knowledge and understanding ofrelevant information; there may be major gaps or omissions.

• Provides little evidence of weighing up of competingarguments/pros and cons in context; discussion likely toconsist of basic description of information.

• Meaning may be conveyed but in a non-specialist way;response lacks clarity and fails to provide an adequate answerto the question.

2 3–4 • Demonstrates accurate knowledge and understanding ofrelevant information with a few gaps or omissions.

• Discussion is partially developed, but will be imbalanced.Evidences the weighing up of competing arguments/pros andcons in context.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

3 5–6 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissionsare minor.

• Displays a well-developed and balanced discussion,demonstrating a thorough grasp of competingarguments/pros and cons in context.

• Logical reasoning evidenced throughout response which isclear and uses specialist technical language consistently.

Question number

Indicative content Mark

12 • Purchase of non-current assets will affect the bank balance, butwill not affect profit as it appears on the statement of financialposition.

• Depreciation will lower profit but by a smaller amount dependingon the method used.

• Credit sales – this will lead to an increase in profit, but will havea negative effect on cash flow as money will be delayed cominginto the business, dependent on the credit period.

• Cash will also have been spent on purchases.

• Large closing inventories – this will increase profit as it will lowercost of sales, but if inventory has been bought for cash will havea negative impact on the bank balance.

• Cash flow is affected by the timing of receipts and paymentswhereas profit is the result of the year’s trading activities andmay not correspond to when the income is received or thepayments made.

(8) Level Mark Award up to 8 marks. Refer to the guidance on the cover of

this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–3 • Demonstrates isolated knowledge and understanding of relevantinformation; there may be major gaps or omissions.

• Provides little evidence of application and links between relevantinformation. Analysis likely to consist of basic description ofinformation.

• Meaning may be conveyed but in a non-specialist way; responselacks clarity and fails to provide an adequate answer to thequestion.

2 4–6 • Demonstrates accurate knowledge and understanding of relevantinformation with a few omissions.

• Evidence of application demonstrating some linkages andinterrelationships between factors leading to an analysis beingpresented.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

3 7–8 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissionsare minor.

• Evidences thorough application leading to a balanced analysis

containing linkages and interrelationships between factors.

• Logical reasoning evidenced throughout response which is clearand uses specialist technical language consistently.

Question number

Indicative content Mark

13 Early payment discount • Connor will receive money straight away/within the agreed

shorter time period.

• Will lower the amount of cash that Connor actually receivesfrom his customers, so he may be worse off.

• Not all customers may take up the offer, which still wouldn'tsolve Connor's liquidity position.

• It could act as an incentive and may encourage new customersto buy items from Connor.

• Existing customers encouraged to buy more.

Debt factoring • Connor will receive money straight away.

• Connor will have to pay a fee or a percentage to be able to usethis service.

• Can be very expensive if the business is seen as high risk.

• Only a short-term solution, a one-off.(10)

Level Mark Award up to 10 marks. Refer to the guidance on the cover of this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–3 • Demonstrates isolated knowledge and understanding ofrelevant information; there may be major gaps or omissions.

• Provides little evidence of application and links betweenrelevant information. Assessment likely to consist of basicdescription of information.

• Judgements on significance may be presented, but are likely tobe generic assertions rather than supported by evidence.

• Meaning may be conveyed but in a non-specialist way;response lacks clarity and fails to provide an adequate answerto the question.

2 4–8 • Demonstrates accurate knowledge and understanding ofrelevant information with a few omissions.

• Evidence of application demonstrating some linkages andinterrelationships between factors leading to ajudgement/judgements being made.

• Assessment is presented leading to judgements on significancebut some may be lacking support.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

3 9–10 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissionsare minor.

• Evidences thorough application containing linkages andinterrelationships between factors leading to ajudgement/judgements being made.

• Displays a well-developed and balanced assessment leading torationalised judgements on significance.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

Question number

Indicative content Mark

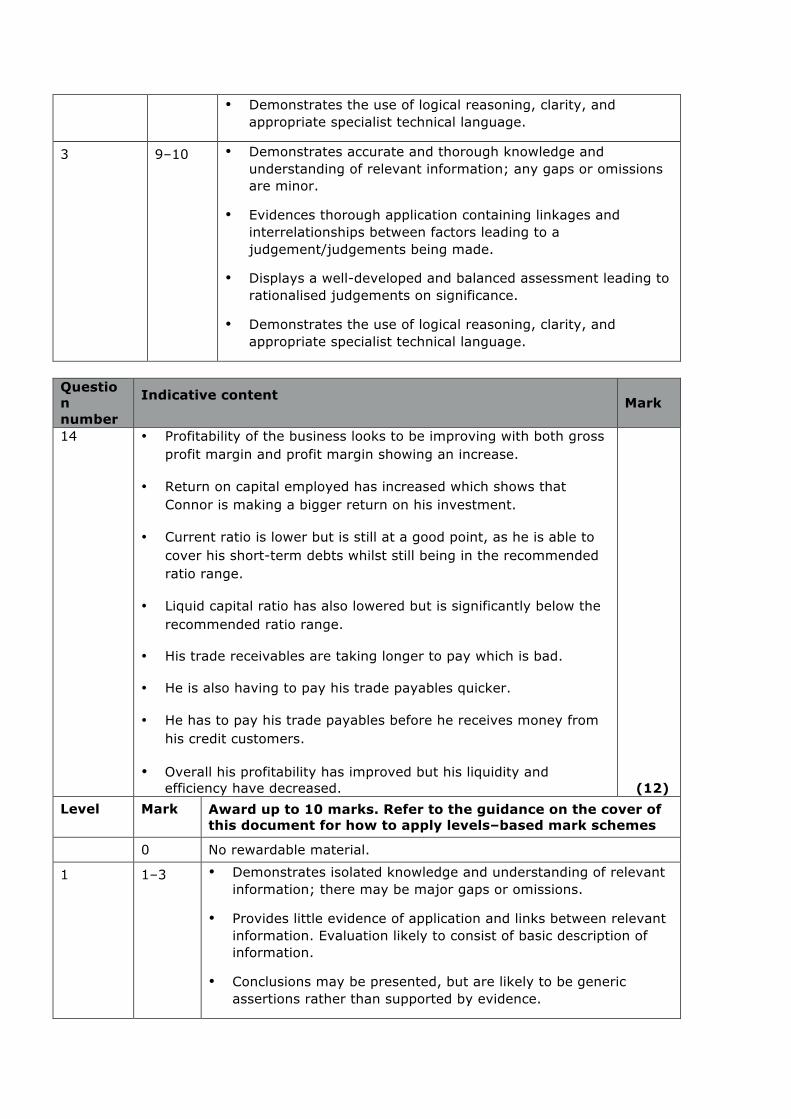

14 • Profitability of the business looks to be improving with both grossprofit margin and profit margin showing an increase.

• Return on capital employed has increased which shows thatConnor is making a bigger return on his investment.

• Current ratio is lower but is still at a good point, as he is able tocover his short-term debts whilst still being in the recommendedratio range.

• Liquid capital ratio has also lowered but is significantly below therecommended ratio range.

• His trade receivables are taking longer to pay which is bad.

• He is also having to pay his trade payables quicker.

• He has to pay his trade payables before he receives money fromhis credit customers.

• Overall his profitability has improved but his liquidity andefficiency have decreased. (12)

Level Mark Award up to 10 marks. Refer to the guidance on the cover of this document for how to apply levels–based mark schemes

0 No rewardable material.

1 1–3 • Demonstrates isolated knowledge and understanding of relevantinformation; there may be major gaps or omissions.

• Provides little evidence of application and links between relevantinformation. Evaluation likely to consist of basic description ofinformation.

• Conclusions may be presented, but are likely to be genericassertions rather than supported by evidence.

• Meaning may be conveyed but in a non-specialist way; responselacks clarity and fails to provide an adequate answer to thequestion.

2 4–8 • Demonstrates accurate knowledge and understanding of relevantinformation with a few omissions.

• Evidence of application demonstrating some linkages andinterrelationships between factors leading to ajudgement/judgements being made.

• Evaluation is presented leading to conclusions but some may belacking support.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

3 9–10 • Demonstrates accurate knowledge and understanding of relevantinformation with a few minor omissions.

• Evidence of application demonstrating linkages andinterrelationships between factors leading to a supportedjudgement/judgements being made.

• Displays a balanced evaluation demonstrating an awareness ofcompeting arguments, leading to conclusions.

• Demonstrates the use of logical reasoning, clarity, andappropriate specialist technical language.

4 11–12 • Demonstrates accurate and thorough knowledge andunderstanding of relevant information; any gaps or omissions areminor.

• Evidences thorough application leading to balanced evaluationdrawing on linkages and interrelationships between factors.

• Displays a well-developed, balanced and coherent evaluation,demonstrating a thorough grasp of competing arguments,leading to supported conclusions.

• Logical reasoning evidenced throughout response which is clearand uses specialist technical language consistently and fluently.