btw en douane update - pwc · btw en douane update 1. ... (drawback) period of validity ... expo rt...

TRANSCRIPT

Btw en douane update

Nicolas ThomasSenior Manager&Bart VranckenDirector

Btw en douane update

1. Customs & International trade

• Union Customs Code (UCC)

• The Rise of Export Control

2. Btw

• Opeisbaarheid…anno 2016

• Onroerend goed

• Substance & btw

• HvJ Skandia

• Varia

• Speerpunten voor 2016?

Customs & International tradeUCC

1. Union Customs CodeWhat’s happening?

The changes apply in all EU Member States

The Union Customs code will come into effect on 1 May

2016

The UCC will replace the current EU

customs legislation

The last major update to EU

customs legislation took

place over 20 years ago!

These changes affect companies in different ways!

How will this affect thebusiness

Remember it’s not a one size fits all!

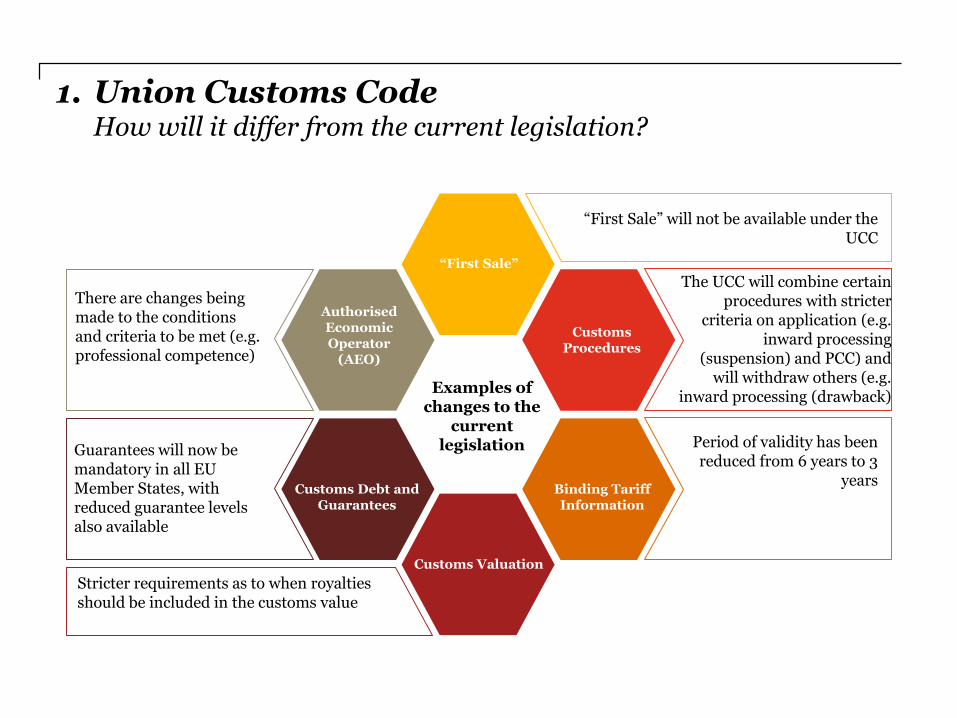

1. Union Customs CodeHow will it differ from the current legislation?

“First Sale”

Authorised Economic Operator

(AEO)

Customs Procedures

Binding Tariff Information

Customs Valuation

Customs Debt and Guarantees

There are changes being made to the conditions and criteria to be met (e.g. professional competence)

Guarantees will now be mandatory in all EU Member States, with reduced guarantee levels also available

Stricter requirements as to when royalties should be included in the customs value

“First Sale” will not be available under the UCC

The UCC will combine certain procedures with stricter

criteria on application (e.g. inward processing

(suspension) and PCC) and will withdraw others (e.g.

inward processing (drawback)

Period of validity has been reduced from 6 years to 3

years

Examples of changes to the

current legislation

1. Union Customs CodeStructure under the UCC

Special procedures;• Transit• Warehousing• Processing• Specific use

Release for free circulation

At arrival –presentation to Customs

Temporary storage (max. 90 days)

Simplification –declaration based upon summary entry declaration

Where possible, similar rules &

procedures

(Re-)export

1. Union Customs CodeKey attention points

Entry into the recordse.g. replaces current local clearance procedure, requirementAEO-C certificate…

Centralised Clearancee.g. legal basis, co-operation mandatory for Member States…

Storagee.g. abolishment type D warehouse, internet sales allowed…

Outward processinge.g. customs debt rules, release for free circulation by other persons…

Inward processinge.g. broader application, no drawback system,compensatory interest…

Transitional measurese.g. impact on BTI’s, PCC, IP-drawback authorisations, customs warehouse type D…

BTI-BOI-Binding rulingse.g. only for EU persons/entities…

Levy of interest on customs debte.g. impact mandatory interest…

Customs valuatione.g. abolishment first sale, royalties, simplifcations…

Authorized Economic Operator (AEO)e.g. reducing guarantees, impact AEO-C certificate…

UCC Opportunities

Customs & International tradeThe Rise of Export Control

2. Export ControlIn a nutshell

Export

Controls

Foundations

End

-Use

rDestination

Product E

nd-Use

Product control

End-user control

End-use control

Destination control

2. Export ControlWhat is it ?

Control ? Product Control : Materials, chemicals, "micro-organisms" and "toxins“

End user, End use and Destination control …. MASTER DATA

• Fines• Business disruption

(black lists)• Supply chain

disruption• Damage to

reputation

What if ?

SUPPLY CHAIN

Regulations imposed by governments to restrict the movement of certain goods, software and technology

As a result, companies must require approvals from the relevant national authorities before exporting

What ?

COMPLIANCE

2. Export ControlAm I hit ?

• Awareness: Knowledge

• Roles & Responsibilities: governance model

Data Screening: Regulatory environment

Data Screening: Operations

Compliance: documentary

1

2

3

4

SOLUTION

2. Export ControlKey attention point

Blue Print of operationsReview supply chain model and assess export controllable flows

Master Data quality assessment in view of Export

control

Regulatory monitoringSet-up regulatory screening process

Governance modelDesign internal roles and responsibilitiesmodel towards export control management

Knowledge Building Create awareness within the teams

AEO UCC 1st may 2016

Network building Organize KLAMA collaboration

Reporting Obligations

System based approachBenchmark existing supporting solutions

Procedural aspectsDefine practical procedure as regards to documentary obligations

Export

Control

Btw – opeisbaarheid... Anno 2016

1. Opeisbaarheid…anno 2016

• Oude regeling en factuur wint (zelfs) aan belang

• Oude regeling, maar let op!

• Incassostelsel

• Incassostelsel

Goederen & diensten

Intracom. handelingen

B2C

B2G

Btw – onroerend goed

2. Onroerend goedC-55/14, Régie communale du stade Luc Varenne

De terbeschikkingstelling, onder bezwarende titel, van een voetbalstadion is geen (passieve vrijgestelde) onroerende verhuur wanneer:• de eigenaar zich bepaalde rechten en voorrechten

voorbehoudt, en • verschillende diensten verstrekt die goed zijn voor

80 % van de contractuele vergoeding zoals instandhouding, schoonmaak, onderhoud en aanpassing aan de geldende normen

Uiteindelijke (feitelijke) beoordeling door nationale rechter.

Kantoren meer dan 10%

2. Onroerend goedRuling nr. 2015.035, 3 maart 2015

Zinvoller om de 10 %-drempel te beoordelen in functie van het volume opslagruimte (in 3D) in vergelijking methet volume van het kantoor voor het personeel dat belast is met het beheer van de opgeslagen goederen

Btw – substance & btw

3. Substance & btwHof van Beroep te Brussel dd. 30.04.2015

NV L

NV S

Klanten

• NV L heeft vaste inrichting in België

• Toepassing van DFDS-principe

• Link met BEPS actie 7

Btw – HvJ Skandia

4. Btw-eenheid C-7/13, Skandia America & Beslissing van 3 april 2015 (nr. E.T. 127.577)

• US bijkantoor is, als lid van de btw-eenheid, samen met de andere BE entiteiten een afzonderlijke btw-plichtige

• BE btw verschuldigd in aangifte btw-eenheid, geen toepassing FCE-bank

• Geen rekening houden met omzet US HQ voor berekening omzet (pro-rata)

• Artikel 19bis wordt opgeheven

• Interpretatieproblemen tussen Lidstaten

Skandia US HQSkandia BE entiteitenBelastbare

handeling?

Skandia US bijkantoor

Btw - varia

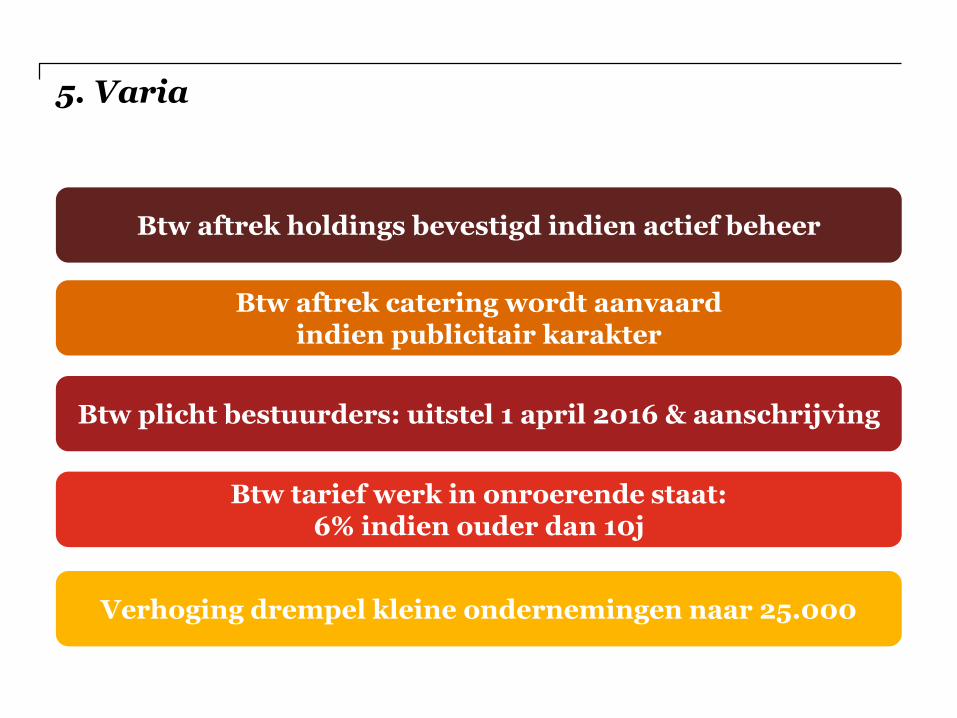

5. Varia

Btw aftrek holdings bevestigd indien actief beheer

Btw aftrek catering wordt aanvaard indien publicitair karakter

Btw tarief werk in onroerende staat: 6% indien ouder dan 10j

Btw plicht bestuurders: uitstel 1 april 2016 & aanschrijving

Verhoging drempel kleine ondernemingen naar 25.000

Btw - speerpunten 2016?

6. Speerpunten 2016

Versoepelen van de

bewijslast bij IC

handelingen

Nieuwe regels kostendelendeverenigingen

Nieuwe regels btw-eenheden

Rechtszekerheidbtw-statuut

AGB’s, publiekrechtelijke

lichamen enjeugdhuizen

Wegwerken van

concurrentie-verstoring

Hervorming btw boeten

uitgangspunt goede trouw

Toelichting op diensten betreffende onroerende

goederen

Contacts

Philippe VancloosterPartner

tel: +32 (0)3 259 32 88gsm: +32 (0)475 51 03 [email protected]

Bart VranckenDirector

tel: +32 (0)9 268 81 82gsm: +32 (0)479 42 63 [email protected]

Tom WallynDirector

tel: +32 (0)9 268 80 21gsm: +32 (0)474 34 23 [email protected]

Nicolas ThomasSenior Manager

tel: +32 (0)2 710 42 41gsm: +32 (0)474 68 58 [email protected]

Nic BoydensDirector

tel: +32 (0)3 259 32 83gsm: +32 (0)473 91 02 [email protected]

Philippe VynckePartner

Tel: +32 (0)9 268 83 03Gsm: +32 (0)475 56 13 [email protected]

About PwC

PwC helps organisations and individuals create the value they’re looking for. We’re a network of firms in 157 countries with more than 195,000 people who are

committed to delivering quality in assurance, tax and advisory services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

© 2015 PwC. All rights reserved.

Thank you.We’ll send you a survey invitation by e-mail, after completing it you will be able to download today’s slides.