budget execution report - minecofin · budget execution report january ... projections reflecting...

TRANSCRIPT

MINISTRY OF FINANCE AND ECONOMIC PLANNING

Budget Execution

Report January – March 2015

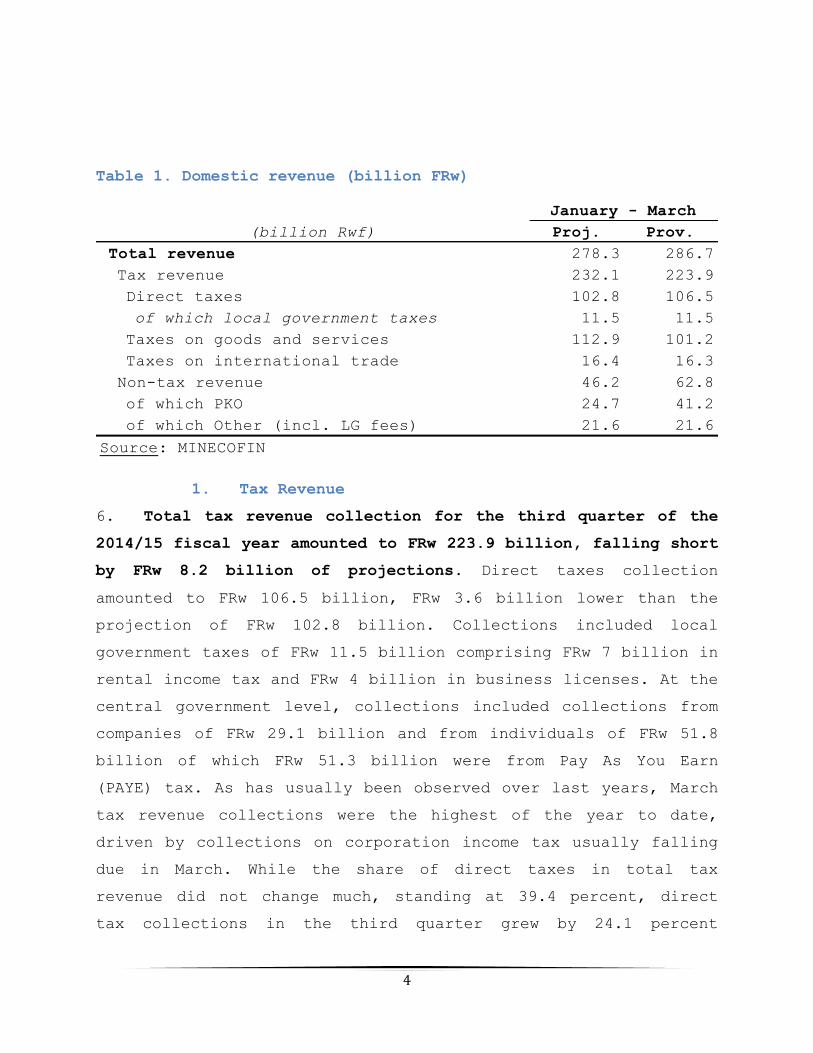

June 2015

Office of the Chief Economist

Macroeconomic Policy Unit

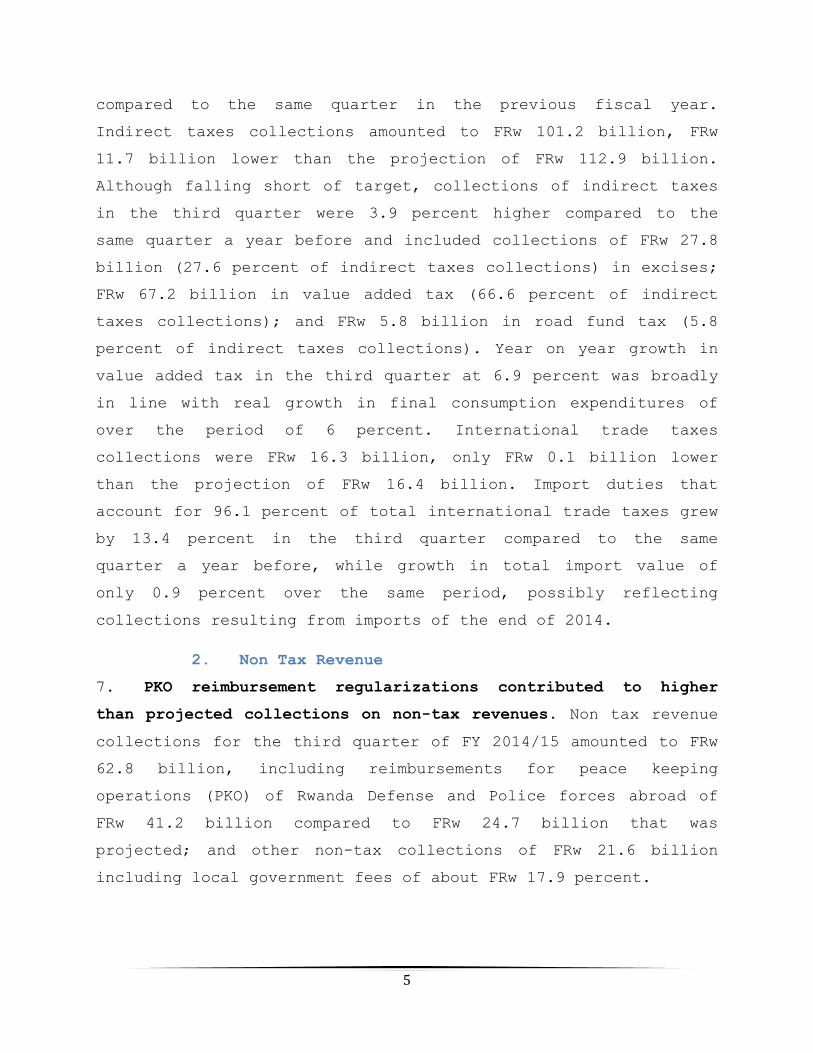

1

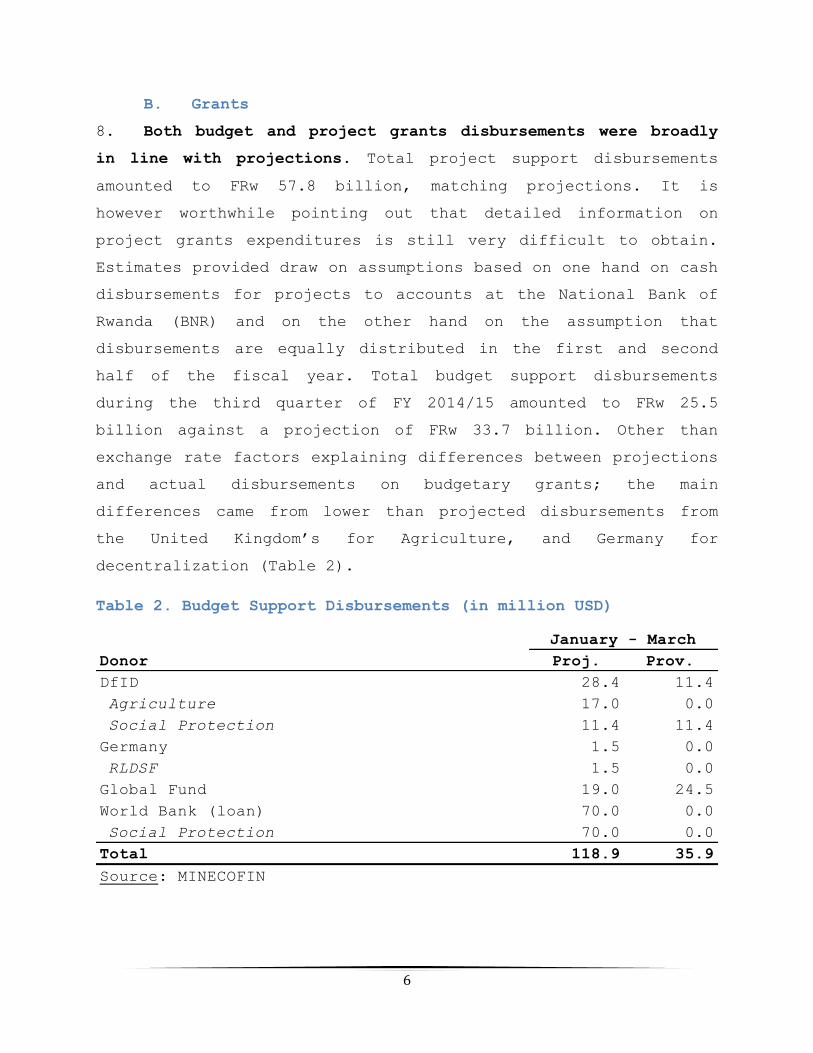

CONTENTS

CONTENTS ------------------------------------------------------------------------------------------------------------ 1

I. INTRODUCTION ------------------------------------------------------------------------------------------- 2

II. FISCAL PERFORMANCE IN THE THIRD QUARTER OF FY 2014/15 ------------ 2

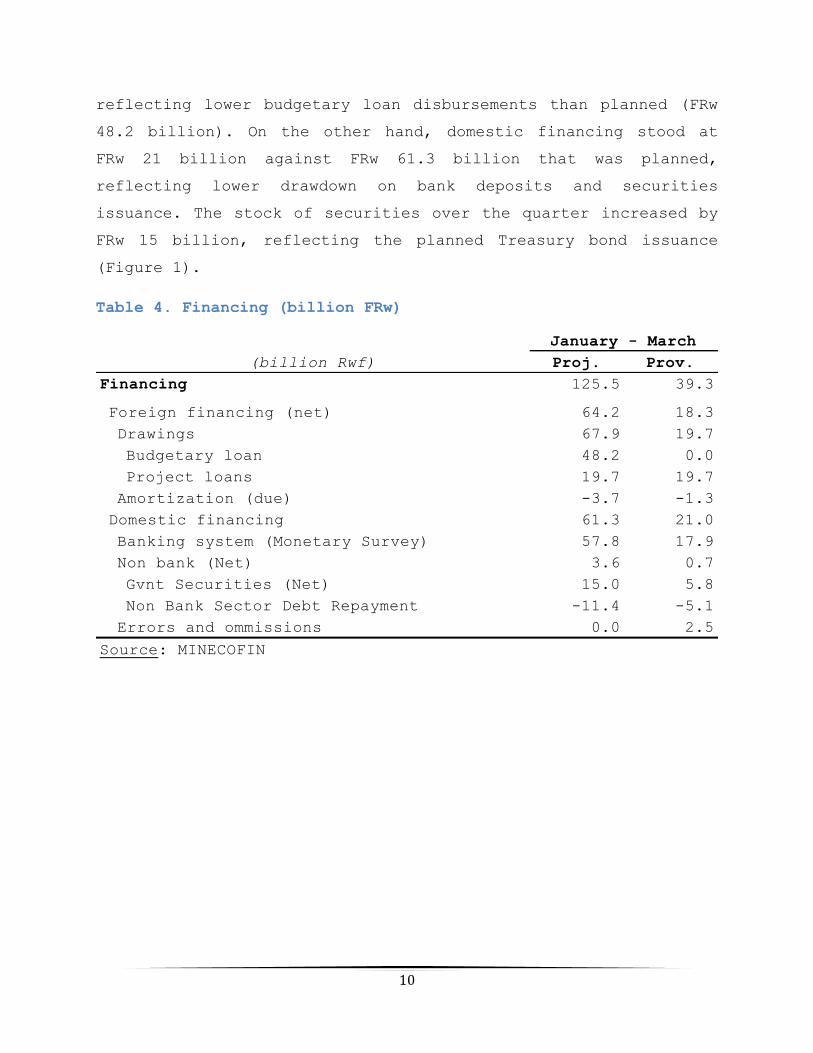

A. Domestic Revenue -------------------------------------------------------------------------------------------- 3

1. Tax Revenue ----------------------------------------------------------------------------------------------------------------- 4

2. Non Tax Revenue --------------------------------------------------------------------------------------------------------- 5

B. Grants --------------------------------------------------------------------------------------------------------------- 6

C. Expenditures and Net Lending -------------------------------------------------------------------- 7

1. Recurrent Expenditures ------------------------------------------------------------------------------------------- 7

2. Capital Expenditures ----------------------------------------------------------------------------------------------- 8

3. Net Lending ----------------------------------------------------------------------------------------------------------------- 9

D. Deficit and Financing ---------------------------------------------------------------------------------- 9

III. Sector Performance for the period January-March for the

2014/2015 Fiscal Year--------------------------------------------------------------------------------- 11

IV. CONCLUSION --------------------------------------------------------------------------------------------- 17

TABLES

Table 1. Domestic revenue (billion FRw) ----------------------------------------------------------- 4

Table 2. Budget Support Disbursements (in million USD) ------------------------------ 6

Table 3. Expenditures and net lending (billion FRw) ------------------------------------ 7

Table 4. Financing (billion FRw) ------------------------------------------------------------------------ 10

Table 5. Operations of the Central Government (provisional) ------------------- 20

FIGURES

Figure 1. Domestic Government Securities (billion Rwf) ----------------------------- 11

Figure 2. Fiscal performance -------------------------------------------------------------------------------- 18

Figure 3. Tax Revenue Collections ---------------------------------------------------------------------- 19

2

I. INTRODUCTION

1. Rwanda’s economic performance remains strong. On the

international scene, global growth remains moderate at 3.5

percent in 2015, as reflected The International Monetary Fund’s

(IMF) April 2015 World Economic Outlook, albeit with uneven

prospects across countries and regions. Rwanda’s economy remains

strong, with growth at 7.6 percent in the first quarter of 2015,

boding well for achieving the forecasted 6.5 percent growth for

the year. Inflation remained subdued, in the single digits, and

lower compared to regional peers. Headline inflation at end May

2015 stood at 2.2 percent, slightly up compared to the first

four months on account on increased food, housing and energy

prices.

2. Fiscal performance in the first half of FY 2014/15 (July-

December 2014) was moderate. Tax revenue collections were

slightly lower than projections mainly on account of lower than

expected yields on revenue measures. While current spending was

on track, capital spending and net lending fell short of

projections reflecting delays in project implementations and the

completion of KCC. The lower than projected spending resulted

into a lower deficit and moderate deposits accumulation in the

banking system. With some of the issues that plagued capital

spending in the first half being addressed, it was expected that

spending would pick up in the second half.

II. FISCAL PERFORMANCE IN THE THIRD QUARTER OF FY 2014/15

3. Performance in the third quarter aligned to the revised FY

2014/15. To reflect changes in revenue sources, the 2014/15

budget was revised upwards from FRw 1,753.3 billion to FRw

1,762.3. Changes in the budget included a downward revision of

3

budget support, increase in domestic borrowing, and some

expenditure reallocations.

4. Projections for the third quarter of FY 2014/15 assumed a

pick-up in economic activity allowing for higher domestic

revenue collections and accelerated spending on investment

projects to further boost growth. Although fiscal performance

throughout the first half of the fiscal year fell short of

expectations on domestic revenue collection and absorptive

capacity to implement investment projects, a pickup was expected

during the second half, starting in the third quarter. Total

revenue 1 and grants were projected at FRw 369.8 billion, with

total expenditures and net lending set at FRw 432.3 billion and

clearance of arrears worth FRw 62.9 billion resulting into a

deficit on cash basis including grants of FRw 125.5 to be

financed externally to the tune of FRw 64.2 billion and FRw 61.3

billion domestically.

A. Domestic Revenue

5. Domestic revenue collections exceeded forecasts for the

quarter. The over performance in domestic revenue driven by

higher than projected reimbursements for peace keeping

operations overshadowed underperformance in tax revenue

collection. Local government tax collections most of which fell

due at the end of the quarter were on track. The lower

performance in tax revenue collections against forecast

reflected continued delays in revenue administration measures

translating into additional revenue inflows (Table 1).

1 The revenue projections referred to in this report are based on the FY

2014/15 revised budget submitted to Parliament.

4

Table 1. Domestic revenue (billion FRw)

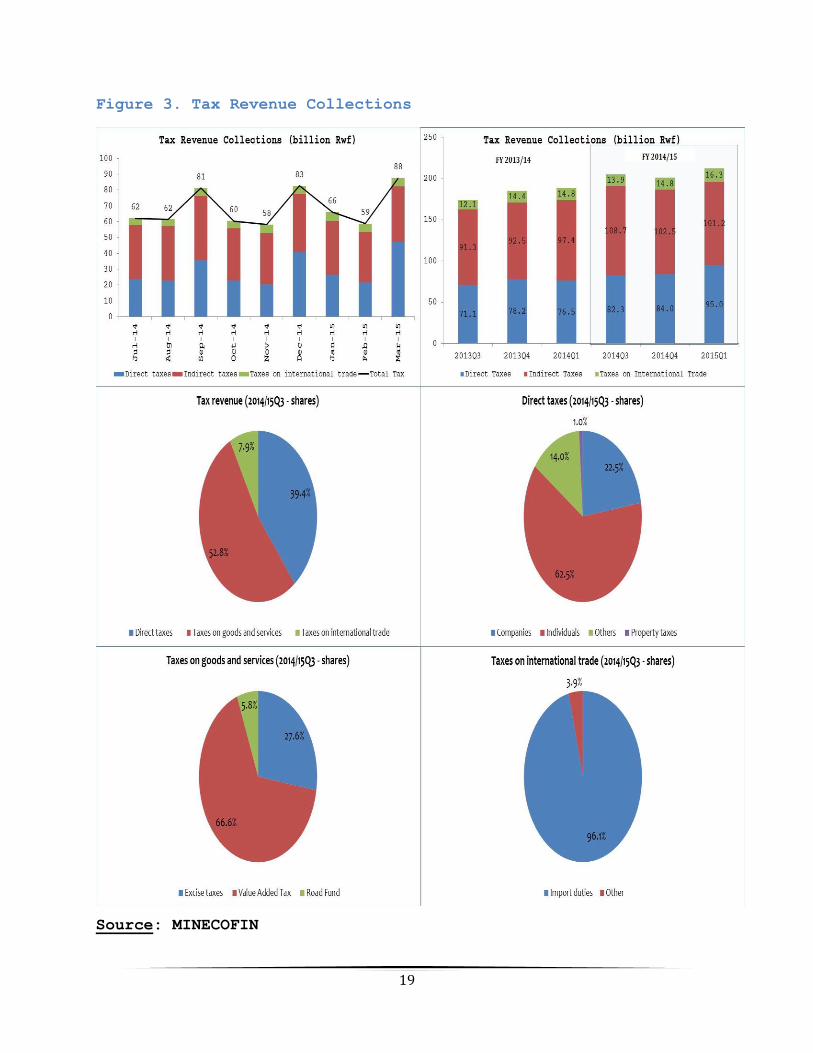

1. Tax Revenue

6. Total tax revenue collection for the third quarter of the

2014/15 fiscal year amounted to FRw 223.9 billion, falling short

by FRw 8.2 billion of projections. Direct taxes collection

amounted to FRw 106.5 billion, FRw 3.6 billion lower than the

projection of FRw 102.8 billion. Collections included local

government taxes of FRw 11.5 billion comprising FRw 7 billion in

rental income tax and FRw 4 billion in business licenses. At the

central government level, collections included collections from

companies of FRw 29.1 billion and from individuals of FRw 51.8

billion of which FRw 51.3 billion were from Pay As You Earn

(PAYE) tax. As has usually been observed over last years, March

tax revenue collections were the highest of the year to date,

driven by collections on corporation income tax usually falling

due in March. While the share of direct taxes in total tax

revenue did not change much, standing at 39.4 percent, direct

tax collections in the third quarter grew by 24.1 percent

(billion Rwf) Proj. Prov.

Total revenue 278.3 286.7

Tax revenue 232.1 223.9

Direct taxes 102.8 106.5

of which local government taxes 11.5 11.5

Taxes on goods and services 112.9 101.2

Taxes on international trade 16.4 16.3

Non-tax revenue 46.2 62.8

of which PKO 24.7 41.2

of which Other (incl. LG fees) 21.6 21.6

Source: MINECOFIN

January - March

5

compared to the same quarter in the previous fiscal year.

Indirect taxes collections amounted to FRw 101.2 billion, FRw

11.7 billion lower than the projection of FRw 112.9 billion.

Although falling short of target, collections of indirect taxes

in the third quarter were 3.9 percent higher compared to the

same quarter a year before and included collections of FRw 27.8

billion (27.6 percent of indirect taxes collections) in excises;

FRw 67.2 billion in value added tax (66.6 percent of indirect

taxes collections); and FRw 5.8 billion in road fund tax (5.8

percent of indirect taxes collections). Year on year growth in

value added tax in the third quarter at 6.9 percent was broadly

in line with real growth in final consumption expenditures of

over the period of 6 percent. International trade taxes

collections were FRw 16.3 billion, only FRw 0.1 billion lower

than the projection of FRw 16.4 billion. Import duties that

account for 96.1 percent of total international trade taxes grew

by 13.4 percent in the third quarter compared to the same

quarter a year before, while growth in total import value of

only 0.9 percent over the same period, possibly reflecting

collections resulting from imports of the end of 2014.

2. Non Tax Revenue

7. PKO reimbursement regularizations contributed to higher

than projected collections on non-tax revenues. Non tax revenue

collections for the third quarter of FY 2014/15 amounted to FRw

62.8 billion, including reimbursements for peace keeping

operations (PKO) of Rwanda Defense and Police forces abroad of

FRw 41.2 billion compared to FRw 24.7 billion that was

projected; and other non-tax collections of FRw 21.6 billion

including local government fees of about FRw 17.9 percent.

6

B. Grants

8. Both budget and project grants disbursements were broadly

in line with projections. Total project support disbursements

amounted to FRw 57.8 billion, matching projections. It is

however worthwhile pointing out that detailed information on

project grants expenditures is still very difficult to obtain.

Estimates provided draw on assumptions based on one hand on cash

disbursements for projects to accounts at the National Bank of

Rwanda (BNR) and on the other hand on the assumption that

disbursements are equally distributed in the first and second

half of the fiscal year. Total budget support disbursements

during the third quarter of FY 2014/15 amounted to FRw 25.5

billion against a projection of FRw 33.7 billion. Other than

exchange rate factors explaining differences between projections

and actual disbursements on budgetary grants; the main

differences came from lower than projected disbursements from

the United Kingdom’s for Agriculture, and Germany for

decentralization (Table 2).

Table 2. Budget Support Disbursements (in million USD)

Donor Proj. Prov.

DfID 28.4 11.4

Agriculture 17.0 0.0

Social Protection 11.4 11.4

Germany 1.5 0.0

RLDSF 1.5 0.0

Global Fund 19.0 24.5

World Bank (loan) 70.0 0.0

Social Protection 70.0 0.0

Total 118.9 35.9

Source: MINECOFIN

January - March

7

C. Expenditures and Net Lending

9. Total spending in the third quarter of FY 2014/15 was

broadly in line with projections, albeit with mixed performance.

Total expenditures and net lending amounted to FRw 432.7

billion, FRw 0.4 billion higher than projected. While current

expenditures and net lending performance fell below projections,

capital expenditures exceeded projections.

Table 3. Expenditures and net lending (billion FRw)

1. Recurrent Expenditures

10. Current spending fell short of projections. Total current

spending amounted to FRw 226.1 billion, FRw 5.1 billion lower

than the FRw 231.2 billion projected owing mainly to a

combination of lower than projected spending on wages and

salaries and transfers and higher than projected on goods and

services and exceptional expenditures.

(billion Rwf) Proj. Prov.

Total expenditure and net lending 432.3 432.7

Current expenditure 231.2 226.1

Wages and salaries 54.5 52.2

Purchases of goods and services 30.9 34.9

Interest payments 6.5 6.7

Domestic Int (paid) 2.6 4.6

External Int (due) 4.0 2.1

Transfers 111.3 98.4

of which expenditures on local government taxes29.3 29.3

Exceptional social expenditure 27.9 33.9

Capital expenditure 169.2 181.5

Domestic 91.7 104.0

Foreign 77.4 77.4

Net lending 31.9 25.1

Source: MINECOFIN

January - March

8

Wages and salaries payments in the third quarter amounted

to FRw 52.2 billion compared to FRw 54.5 billion projected for

the period. The lower than projected performance was due to

delayed hiring of staff that had been planned for the fiscal

year.

Goods and services spending amounted to FRw 34.9 billion,

FRw 3.9 billion higher than the projected FRw 30.9 billion. The

overspending was due to payments of ICT equipment and software,

consultancy services and maintenance and repairs for office

buildings and equipment.

Exceptional expenditures stood at FRw 33.9 billion, FRw 6

billion higher than projected, mostly driven by higher spending

on peace keeping operations expenditures as a result of new

deployments. Payments on other exceptional expenditures, for

demobilization and assistance, and Genocide survivors were

broadly on track.

Transfers and subsidies amounted to FRw 98.4 billion and

were FRw 12.9 billion lower than projections. The delays were

mainly due to low payments on international subscriptions for

some Organizations as well as transfers to other agencies.

Interest payments amounted to FRw 6.7 billion, slightly

higher than the projection of FRw 6.5 billion. The FRw 0.2

billion over performance was a combination of excess spending on

domestic interest payment by FRw 2 billion and lower spending on

external interest payment by FRw 1.9 billion.

2. Capital Expenditures

11. Capital expenditures performance in the third quarter of FY

2014/15 was very strong. Total capital expenditures amounted to

FRw 181.5 billion of which FRw 104 billion were capital

9

expenditures domestically financed and FRw 77.4 billion

externally financed. Domestically financed capital spending

exceeded projections by FRw 12.3 billion, reflecting a

resumption of projects that had experienced delays throughout

the first half.

3. Net Lending

12. Lower than projected use of the proceeds of the Eurobond

affected net lending performance. Net lending in the third

quarter of FY 2014/15 amounted to FRw 25.1 billion against a

projection of FRw 31.9 billion reflecting the net effect of

higher than anticipated spending on strategic investments and

subsidies to Rwandair; and no spending on KCC as construction

works delayed.

D. Deficit and Financing

13. The fiscal deficit was much lower than projected during the

third quarter of FY 2014/15. At the end of the quarter, the

deficit on payment order basis (including grants) was only FRw

0.2 billion higher than projections. Accumulation of arrears

during the quarter amounting to FRw 23.4 billion instead of the

planned reduction of FRw 62.9 billion led to a much lower fiscal

deficit on cash basis (including grants) than was projected

(Table 5). Lower than expected budgetary disbursement led to

accumulation of arrears as commitments in agriculture and social

protections were made in anticipation of disbursements from the

World Bank and the UK – they are now expected to be cleared

during the fourth quarter. The budget closed with a deficit on

cash basis of FRw 39.3 billion compared to a deficit of FRw

125.5 billion that was projected (Table 4). Financing of the

deficit came on one hand from foreign sources to the tune of FRw

18.3 billion compared to FRw 64.2 billion that was planned,

10

reflecting lower budgetary loan disbursements than planned (FRw

48.2 billion). On the other hand, domestic financing stood at

FRw 21 billion against FRw 61.3 billion that was planned,

reflecting lower drawdown on bank deposits and securities

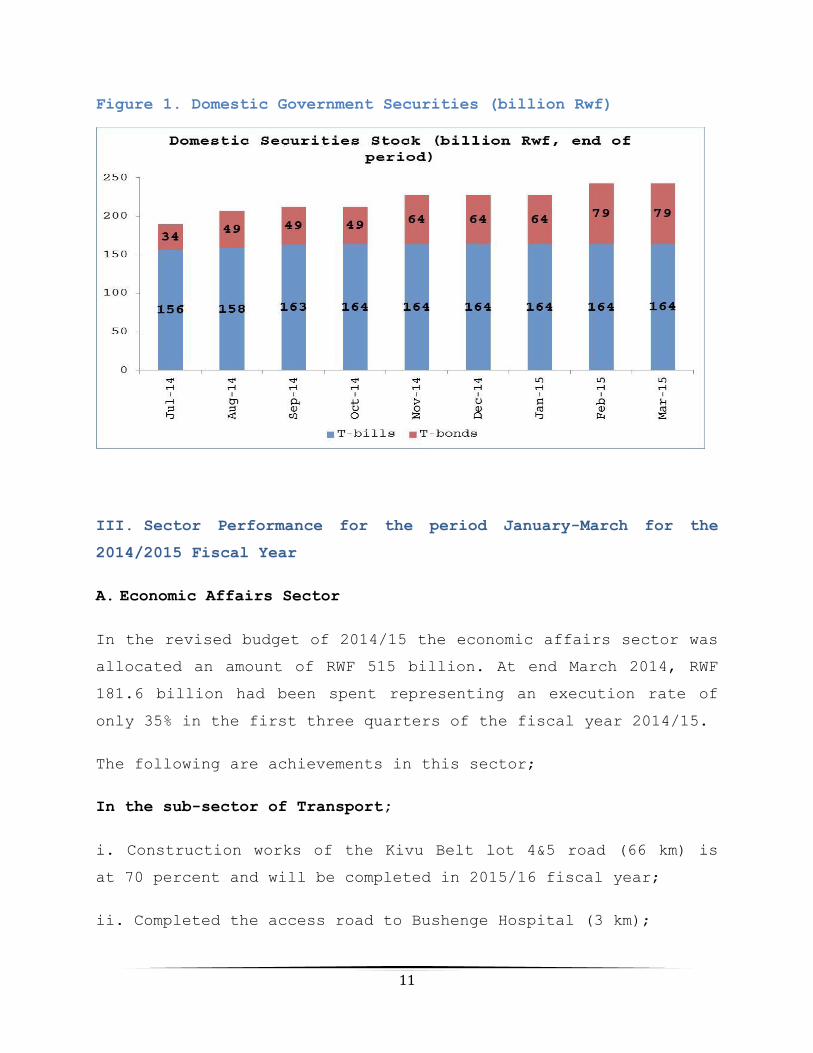

issuance. The stock of securities over the quarter increased by

FRw 15 billion, reflecting the planned Treasury bond issuance

(Figure 1).

Table 4. Financing (billion FRw)

(billion Rwf) Proj. Prov.

Financing 125.5 39.3

Foreign financing (net) 64.2 18.3

Drawings 67.9 19.7

Budgetary loan 48.2 0.0

Project loans 19.7 19.7

Amortization (due) -3.7 -1.3

Domestic financing 61.3 21.0

Banking system (Monetary Survey) 57.8 17.9

Non bank (Net) 3.6 0.7

Gvnt Securities (Net) 15.0 5.8

Non Bank Sector Debt Repayment -11.4 -5.1

Errors and ommissions 0.0 2.5

Source: MINECOFIN

January - March

11

Figure 1. Domestic Government Securities (billion Rwf)

III. Sector Performance for the period January-March for the

2014/2015 Fiscal Year

A. Economic Affairs Sector

In the revised budget of 2014/15 the economic affairs sector was

allocated an amount of RWF 515 billion. At end March 2014, RWF

181.6 billion had been spent representing an execution rate of

only 35% in the first three quarters of the fiscal year 2014/15.

The following are achievements in this sector;

In the sub-sector of Transport;

i. Construction works of the Kivu Belt lot 4&5 road (66 km) is

at 70 percent and will be completed in 2015/16 fiscal year;

ii. Completed the access road to Bushenge Hospital (3 km);

12

iii. Construction works of Muhanga – Ngororero - Mukamira (99

km) road are ongoing at 75 percent;

iv. Constructed the access road to Mugombwa Refugee camp;

v. Maintained the road Ndatemwa - Muhura (23 km);

vi. Completed the detailed study of Muhanga - Karongi

rehabilitation and negotiations for funds will be carried out in

2015/16 fiscal year;

Vii. Construction works of the road CIMERWA - Bugarama are at 80

percent;

viii. Completed Rusumo One Border Post;

ix. Completed the runway for Kamembe Airport

In the sub- sector of Energy;

I. Electricity connectivity was increased by 2 percent and

50,000 new households was connected whereby access to

electricity reached 21 percent;

ii. Transmission lines increased by 318.9 km of MV lines, 517.6

km of LV and 140.4 km of HV;

ii. Construction works of Rusumo Hydro Power Plant that will

give 80 MW are on track and the plant is expected to be

completed in 2019;

iv. Negotiations for a new methane project are ongoing as

planned and expected to be completed by June 2015.

In the sub-sector of Water and Sanitation, the total primary

spending to water and sanitation sector, was 6.4 billion at the

13

end March. Execution was at 30.3 per cent against the total

revised allocated budget 2014/2015 amounted 21.1 billion. Keys

achievements are as follow:

i. Constructed 149.3 Km of water pipe line in Rubavu, Rulindo

and Nyamagabe and that supplied clean drinking water to 152,869

households;

ii. Construction works of 66Km water pipe line in

Rulindo expected supply 28,250 is at 75% and will be

completed by June 2015;

iii. Upgraded 47 Km in urban areas, Nasho - Ngoma, Cyampirita -

Gatsibo, Katabogamua - Nyagatare;

iv. Reinforced water system in Nkombo and construction

of Mbona – Nyabirasi - Kivumu water pipeline are ongoing;

v. Construction works of Runda Water supply system are at

advanced stage;

vi. Introduced the e-payment system to facilitate the

payment of water consumption bills using mobile money and

electronic banking

In the sub-sector of agriculture, the total revised budget

2014/2015 allocated was 60 billion. At the end of the third

quarter in March 15.1 billion was spent this represents an

execution rate of 25.3%. The following are the key achievements:

i. A total number of 16,115 ha of radical terraces and 44,499 ha

of progressive terraces were constructed;

ii. The number of marshland irrigation constructed was 750ha and

construction works of new 1,270 ha are under way;

14

iii. The number of hillside irrigation reached 1,095 ha

that was constructed and prepared for maize and vegetables

cultivation.

iv. Livestock development has been enhanced through GIRINKA

Programme whereby 13,658 animals were distributed to poor

families. Also the number of artificially inseminated cows was

94,868;

v. The feeder roads network improved whereby 117 km were

constructed in 2014/15 fiscal year.

vi. The number of students undertaking specialized

training in agriculture increased whereby 106 students were

sent to Israel for specialization in irrigation,

agribusiness and horticulture.

In the sub-sector of Trade and Industry, basing on the 2014/2015

revised budget allocated to this sector amounted of 58.4

billion; the total spending at the end March was 33.8 billion,

at which comes 57.9 per cent as an execution rate. The following

are the key achievements:

i. In order to facilitate national Exporters to access foreign

markets , 90 exporters have been trained in handcrafts,

honey, bananas, pineapple, Nuts, essential oil, flour and

light and 16 exporters have been supported to attend the Uganda

and Germany trade fairs;

ii. The Market Infrastructure Master Plan was completed

and Implementation Plans for Districts are being developed;

iii. Relocation of industries from Gikondo Park is ongoing as

planned;

15

iv. Completed expropriation for five provincial industrial parks

of Huye, Rusizi, Nyabihu, Bugesera and Rwamagana.

v. In order to help new entrepreneurs to access finance

to start their businesses, 1500 Start - up toolkits were

provided.

B. Education Sector

The total primary spending in the education sector at the end

March of the 2014/15 fiscal year amounted to RWF 151.8 billion

which represented about 70.8% of the approved budget of RWF

214.4 billion. The following are the key achievements in the

sector:

i. In pre-primary education, 1260 kits were distributed in 1260

nursery schools and one teacher from each school was trained.

Also enrolment has increased by nearly 12% in 2014 and the

number of institutions increased by 17%;

ii. In primary education, the Government continued to increase

the number of class rooms and 1,609 new classrooms and 2,604

latrines were built in line with the intention to increase

education for all children and expanding access to 12 years of

basic education

iii. For secondary education, 19 new schools were created and

new classrooms were equipped with 24,840 desks;

iv. The number of TVET center’s increased from 306 in 2013 to

365 in 2014. Also the number of trainees enrolled in TVET

programmes increased from 83,893 students in 2013 to 93,024

students in 2014; and the number of trainers in TVET centres

increased from 3,020 trainers in 2013 to 3,595 trainers in 2014;

16

v. In order to strengthen the performance in science,

technology and innovation at all levels of education, and

application of science, technology and innovation in relevant

sectors of the economy, 274 12YBE schools with sciences

combination received science practical examination materials;

vi. 274 12YBE schools with sciences combination received science

practical examination materials. Hence, 658 teachers from

these schools were trained on skills related to

preparation of practical experiments and administration of

practical exams.

vii. In tertiary education, 22.5% of tertiary students

are in science and technology fields, of which 34% in

agriculture and health sciences;

Viii. The University of Rwanda was established and merged the

former 7 Higher Learning Institutions to improve the quality of

education;

C. Health sector

The total spending in the Health sector at the end of March

amounted to 95.6 billion compared to 2014/2015 revised budget

that amounted to 200.1 billion. That represents an execution

rate of 47.8 %. Below are the achievements for the sector:

i. The construction and rehabilitation works at

various Hospitals are ongoing (Nyabikenke Hospital

stands at 30%, Rutare modern health center at 82% and

Nyagatare Hospital at 74% while the Architectural

and technical design for Ruhengeri Hospital was completed

and the construction works will begin next Fiscal Year.

17

ii. In order to ensure quality and availability of human

resources for health, deployment of qualified nurses,

Midwives, Medical Doctors, and Specialists in health

facilities continued across the country, including in new

provincial and referral hospitals.

iii. For District pharmacies to comply with national

standards, 5 District Pharmacies (Gatsibo, Nyagatare,

Nyaruguru, Ruhango and Muhanga) are under construction

and the work progress is estimated at 80%.

iv. The availability of vital medical products in health

facilities has improved and on average 100 % of Health

facilities (District pharmacies and District hospitals) reported

less than 5% of vital medical products stocked-outs

IV. CONCLUSION

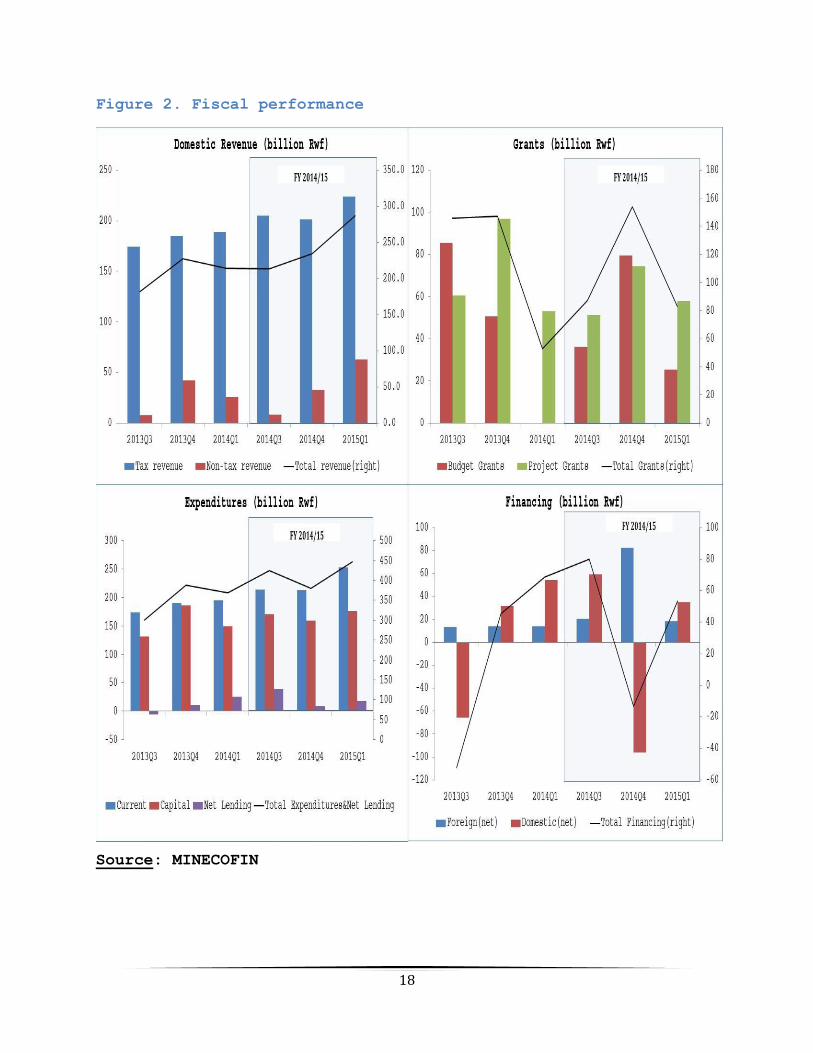

14. Fiscal performance in the third quarter of FY 2014/15 was

broadly on track. Spending performance was mixed but portraying

resumption in capital spending that had been delayed in the

first half of the year. Revenue performance remained dismal

however. Continued good economic performance is expected to

boost revenue collections in the fourth quarter and spending is

expected to remain on track, allowing closing the fiscal year as

planned.

18

Figure 2. Fiscal performance

Source: MINECOFIN

19

Figure 3. Tax Revenue Collections

Source: MINECOFIN

20

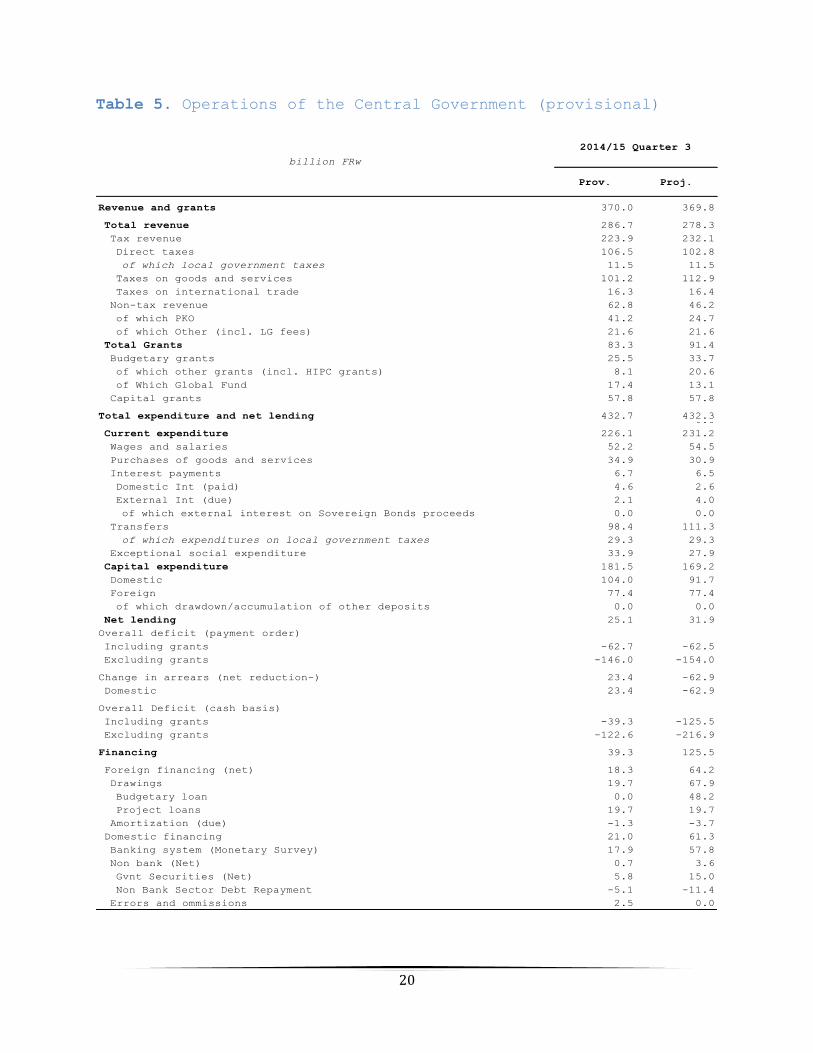

Table 5. Operations of the Central Government (provisional)

Prov. Proj.

Revenue and grants 370.0 369.8

Total revenue 286.7 278.3

Tax revenue 223.9 232.1

Direct taxes 106.5 102.8

of which local government taxes 11.5 11.5

Taxes on goods and services 101.2 112.9

Taxes on international trade 16.3 16.4

Non-tax revenue 62.8 46.2

of which PKO 41.2 24.7

of which Other (incl. LG fees) 21.6 21.6

Total Grants 83.3 91.4

Budgetary grants 25.5 33.7

of which other grants (incl. HIPC grants) 8.1 20.6

of Which Global Fund 17.4 13.1

Capital grants 57.8 57.8

Total expenditure and net lending 432.7 432.30.0

Current expenditure 226.1 231.2

Wages and salaries 52.2 54.5

Purchases of goods and services 34.9 30.9

Interest payments 6.7 6.5

Domestic Int (paid) 4.6 2.6

External Int (due) 2.1 4.0

of which external interest on Sovereign Bonds proceeds 0.0 0.0

Transfers 98.4 111.3

of which expenditures on local government taxes 29.3 29.3

Exceptional social expenditure 33.9 27.9

Capital expenditure 181.5 169.2

Domestic 104.0 91.7

Foreign 77.4 77.4

of which drawdown/accumulation of other deposits 0.0 0.0

Net lending 25.1 31.9

Overall deficit (payment order)

Including grants -62.7 -62.5

Excluding grants -146.0 -154.0

Change in arrears (net reduction-) 23.4 -62.9

Domestic 23.4 -62.9

Overall Deficit (cash basis)

Including grants -39.3 -125.5

Excluding grants -122.6 -216.9

Financing 39.3 125.5

Foreign financing (net) 18.3 64.2

Drawings 19.7 67.9

Budgetary loan 0.0 48.2

Project loans 19.7 19.7

Amortization (due) -1.3 -3.7

Domestic financing 21.0 61.3

Banking system (Monetary Survey) 17.9 57.8

Non bank (Net) 0.7 3.6

Gvnt Securities (Net) 5.8 15.0

Non Bank Sector Debt Repayment -5.1 -11.4

Errors and ommissions 2.5 0.0

billion FRw

2014/15 Quarter 3