budget execution: tracking progress and controlling funds - case studies parminder brar, fm anchor...

TRANSCRIPT

Budget Execution: Tracking Progress and Controlling Funds - Case Studies

Parminder Brar, FM AnchorBudget Management and Financial Accountability CourseMarch 1-2, 2004

The World Bank

Outline

Case Study 1: India : Why India? Bank lending of around $1.5 bn. Is 1.29% of GoI’s budget, and around 0.6% of general government spending. Supporting budget management reform is critical for achieving MDG’s. Budget Management System based upon Treasury Single Account and reimbursement to commercial banks.

Case Study 2: Nigeria : Why Nigeria? Cash management crucial for budget management. Role of CBN in budget management. Budget management based upon cash advances and multiplicity of bank accounts and banks for each agency.

Conclusion

The World Bank

Case 1: India – Expenditure Trends

Trend of GOI Expenditure1999-2000

0

10000

20000

30000

40000

50000

60000

Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar

Rs

. C

r.

Plan Non Plan

Trend of GOI Expenditure 2000-2001

0

10000

20000

30000

40000

50000

60000

Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar

Rs

. C

r.

Plan Non Plan

Trend of GOI Expenditure 1997/98

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar

Rs

. C

r.

Plan Non Plan

Trend of GOI Expenditure 1998-99

0

10000

20000

30000

40000

50000

60000

Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar

Rs

. C

r.

Plan Non Plan

Annual expenditure trends are remarkably similar.

* Rs. 1 crore = Rs.10 million.

The World Bank

Case 1: India – Expenditure Trends

GOI's Cumulative Expenditure Trend

0%

20%

40%

60%

80%

100%

120%

Per

cen

t o

f Act

ual

s

1996-97 7% 13% 21% 27% 32% 39% 46% 52% 61% 73% 81% 100%

1997-98 6% 12% 20% 27% 33% 39% 46% 53% 61% 71% 79% 100%

1998-99 7% 13% 21% 28% 34% 43% 50% 56% 64% 74% 81% 100%

1999-00 6% 11% 20% 27% 34% 42% 49% 56% 64% 74% 80% 100%

2000-01 5% 12% 18% 25% 32% 40% 47% 56% 63% 73% 81% 100%

2001-02 (Prov.) 5% 10% 18% 26% 33% 40% 48% 56% 65% 74% 82% 100%

2002-03 5% 11%

Apl May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

18% 21%22%Quarterly Trend 35%

Annual expenditure trends are remarkably similar.

The World Bank

Case 1: India – Overall Expenditure

Share of GOI Expenditure: Plan and Non Plan

27% 25% 24% 26% 25% 28% 28%

73% 75% 76% 74% 75% 72% 72%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996/97 1997-98 98/99 99/00 00/01 01/02(Prov.) 02/03 (BE)

Pe

rce

nt

of

Ac

tua

ls

Plan Non Plan

Around 75% of GOI expenditure is recurrent (Non Plan) and the rest is capital (Plan) *.

* There could be some overlap in capital and recurrent expenditure between Plan and Non Plan.

The World Bank

Case 1: India – Non Plan Trend

Non Plan Expenditure Trend (Cumulative)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996-97 8% 13% 23% 30% 34% 42% 48% 54% 62% 76% 83% 100%

1997-98 6% 13% 21% 27% 32% 39% 46% 53% 62% 72% 80% 100%

1998-99 7% 13% 22% 29% 35% 44% 50% 56% 64% 75% 81% 100%

1999-00 6% 12% 20% 27% 34% 42% 49% 56% 63% 75% 80% 100%

2000-01 5% 11% 16% 24% 31% 39% 47% 56% 63% 75% 82% 100%

2001-02 (Prov.) 5% 10% 18% 27% 34% 41% 49% 57% 66% 77% 84% 100%

2002-03 6% 12%

Apl May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

18% 25%23%Quarterly Trend

34%

Annual trends of recurrent expenditure are remarkably similar.

The World Bank

Case 1: India – Non Plan Expenditure

Non Plan Expenditure Shares

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1997-98 1998-99 1999-2000 2000-2001 2001-2002 (Prov.) 2002-03 (% of BE)

Per

cen

t o

f N

on

Pla

n

Interest Payments (40%) Ministry of Defence (26%)

Department of Food & Public Distribution (7%) Transfers to State and UT Governments (6%)

Department of Fertilisers (4%) Police (4%)

Department of Agriculture and Cooperation (0%) Pensions (1%)

Department of Secondary and Higher Education (1%)

The World Bank

Case 1: India - Plan expenditure

Plan Expenditure Trend (Cumulative)

0%

20%

40%

60%

80%

100%

120%

Per

cen

t o

f Act

ual

s

1996-97 4% 11% 16% 20% 27% 33% 39% 47% 56% 66% 76% 100%

1997-98 5% 9% 18% 27% 33% 40% 47% 54% 61% 69% 78% 100%

1998-99 5% 12% 17% 23% 33% 42% 49% 57% 64% 70% 78% 100%

1999-00 4% 10% 19% 28% 36% 42% 50% 56% 65% 71% 79% 100%

2000-01 4% 14% 23% 28% 37% 43% 49% 55% 61% 68% 76% 100%

2001-02 (Prov.) 4% 11% 18% 24% 31% 38% 46% 52% 62% 69% 78% 100%

2002-03 4% 10%

Apl May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

24%20%18%Quarterly Trend 38%

Around 40% of capital expenditure is spent in the last quarter.

The World Bank

Case 1: India – Plan expenditure

Plan Expenditure (Share of Actuals)

0%

10%

20%

30%

40%

50%

60%

70%

80%

97-98 1998-99 1999-2000 2000-01 2001-02 (Prov.) 2002-03(% of BE)

Transfers to State and UT's (37%) Rural Development (9%) Department of Education (6%)

Ministry of Power (3%) Ministry of Railways (5%) Department of Family Welfare (4%)

Ministry of Road Transport (6%) Ministry of Social Justice (1%) Department of Women and Child Dev. (2%)

The World Bank

Case 1: India - Ministry trendsThe Indian Rope Trick:

Plan Expenditure of the Ministry of Power

3%

7%

1%

5%

2%

6%

2%

7%

4%

8%

11%

44%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

April May June July Aug Sept Oct Nov Dec Jan Feb March

Pe

rce

nt

of

Ac

tua

ls

01-02 00-01 99-00 98-99 97/98

The World Bank

Case 1: India - Ministry trendsThe Peaks:

Plan Expenditure of Department of Road Transport

0%3%

1%

5%

18%20%

1%

7%

51%

2%

6%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

April May June July Aug Sept Oct Nov Dec Jan Feb March

Pe

rce

nt

of

Ac

tua

ls

01-02 00-01 99-00 98-99 97/98

The World Bank

Case 1: India - Ministry trendsThe Rolling Hills:

Plan Expenditure of the Department of Family Welfare

5%

7%

18%

1% 2%

5%

22%

7%

22%

3% 3%

6%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

April May June July Aug Sept Oct Nov Dec Jan Feb March

Pe

rce

nt

of

Ac

tua

ls

01-02 00-01 99-00 98-99 97/98

The World Bank

Case 1: India - Ministry trendsThe Stress Reliever:

Transfers to States and UT's

7%

6%

8%8% 7%

8%7%

9%

7%

9%

5%

19%

0%

5%

10%

15%

20%

25%

April May June July Aug Sept Oct Nov Dec Jan Feb March

Pe

rce

nt

of

Ac

tua

ls

01-02 00-01 99-00 98-99 97/98

The World Bank

Case 1: India - ReceiptsTax receipts account for 60% of GOI receipts

GOI Receipts

70% 67%63% 66% 66%

60% 63%

24%27%

27%28% 27%

31% 26%

6% 6%10%

6% 7% 9% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

96-97 97-98 98-99 99-00 00-01 01-02 (Prov.) 02-03(BE)

Tax Receipts (Net) Non-Tax Receipts Non Debt Capital Receipts

The World Bank

Case 1: India - ReceiptsReceipt trends are remarkably similar.

Trend of GOI's Total Receipts (Cumulative)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pe

rce

nt

of

Ac

tua

ls

1996-97 5% 10% 17% 23% 31% 41% 48% 55% 67% 74% 81% 100%

1997-98 3% 10% 16% 22% 29% 40% 48% 56% 71% 79% 85% 100%

1998-99 4% 8% 15% 21% 29% 37% 47% 53% 64% 74% 79% 100%

1999-00 0% 6% 13% 19% 28% 37% 46% 53% 64% 72% 79% 100%

2000-01 1% 8% 15% 22% 33% 42% 50% 56% 68% 73% 81% 100%

2001-02 (Prov.) 1% 4% 10% 16% 28% 39% 49% 55% 65% 72% 81% 100%

2002-03 (% of BE) 2% 6%

Apl May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

The World Bank

Case 1: India - ReceiptsTax receipts have been overestimated for the last 7 years.

GOI Total Receipts

100,000

120,000

140,000

160,000

180,000

200,000

220,000

240,000

260,000

280,000

300,000

Rs.

Cr.

BE 142,394 166,722 176,903 203,928 227,211 258,909 274,785

RE 139,167 148,900 178,174 194,839 223,551 232,715

Actuals 134,275 143,131 166,017 193,368 206,796 222,859

1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 (Prov.) 2002-03

+52,113 +31,698

+15,876

+51,926

The World Bank

Case 1: India - ReceiptsBudget Management challenges are partly due to overestimating receipts every year.

+8,856

+16,063+13,428+27,350

+22,886

+33,459+27,527

+18,773

+47,270

+31,060

GOI's Receipts, Expenditure and Deficit

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Rs.

Cr.

Total Receipts 134,275 143,131 166,017 193,368 206,796 222,859 274,785

Total Expenditure 201,007 232,068 279,366 298,084 325,611 359,070 410,309

Fiscal Deficit 66,732 88,937 113,349 104,717 118,815 136,211 135,524

1996/97 1997-98 98/99 99/00 00/01 01/02 (Prov.) 02/03 (BE)

+51,239

+51,926

The World Bank

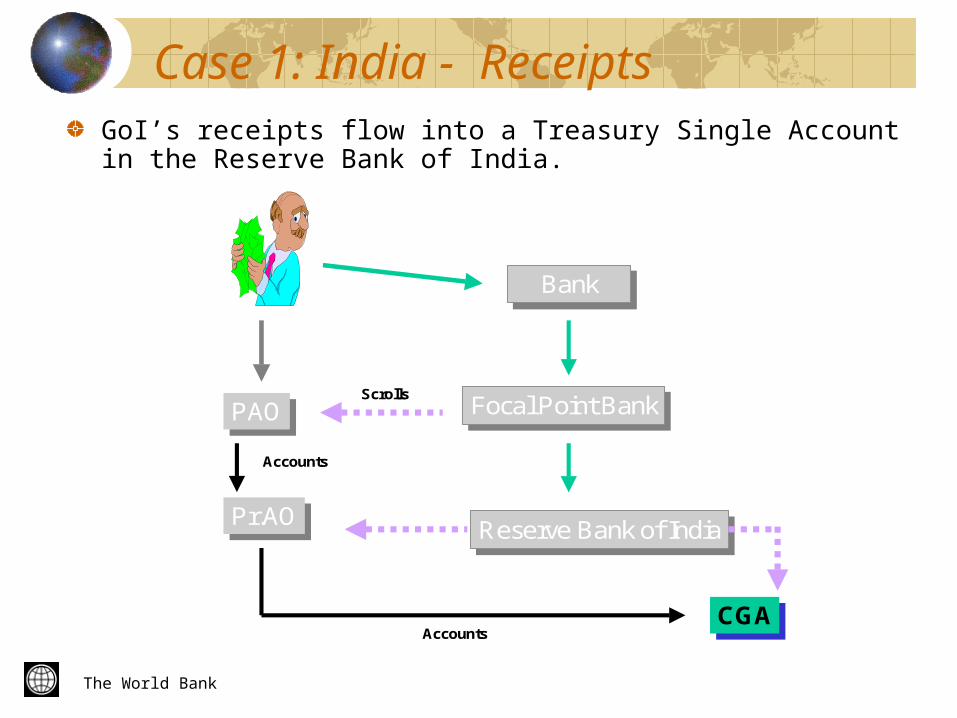

Case 1: India - Receipts

BankBank

Focal Point BankFocal Point Bank

Reserve Bank of IndiaReserve Bank of India

PAOPAO

Pr.AOPr.AO

CGACGA

Scrolls

Accounts

Accounts

GoI’s receipts flow into a Treasury Single Account in the Reserve Bank of India.

The World Bank

Case 1: India - Disbursements

D e a lin g B ra n c h

D e a lin g B ra n c h

F o c a l P o in t B a n kF o c a l P o in t B a n k

L in k C e llL in k C e ll

P A OP A O

P r .A OP r .A O

R e s e r v e B a n k o f In d iaR e s e r v e B a n k o f In d ia

S c ro lls

A c c o u n ts

P u t T h ru

C la im

C h e q u e

C G AC G A

R e im b u rs e m e n t

Disbursements are on the basis of reimbursement of funds to commercial banks. One Ministry deals with one bank.

The World Bank

Case 2: Nigeria - Receipts

Central Bank of Nigeria (CBN)

Consolidated Revenue Fund

Central CapitalFund

Federation Account

Health

Federal

State

Local

Sub Treasury (FPO Abuja)

Line Ministry Receipts

Oil Revenues

VAT

Customs

Roads

Ports

Internal Affairs

Education

etc.

Cash management is based on funds available in the CRF.

The World Bank

Case 2: Nigeria - Expenditures

DGBudget

OAGF

CBN

ConsolidatedRevenue Fund

Central CapitalFund

Warrant Mandate

Cash Back

58 Line Ministry’s

Authority to Incur Expenditure

37 Field Pay Offices Account No. 4 Receipts (Private Bank No. 3)

Account No. 1 Capital Exp.

Account No.3 Recurrent Exp.(Private Bank No.2)

Account No. 2 OH. Exp. (Private Bank No. 1)

Cash Back

Cash Management Committee

Disbursement system operates on the basis of cash advances to numerous banks.

The World Bank

Case 2: Nigeria – CRF Receipts

Nigeria : CRF 2003 : Receipts

77%

16%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec. Ave.

Pe

rce

nt

NTB Statutory Other

77% of receipts are on account of Treasury Bonds.

* Provisional unaudited data

The World Bank

Case 2: Nigeria – CRF Expenditures

Nigeria : CRF 2003 : Disbursement

79%

5%

4%

1%

10%

1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec. Ave.

Per

cen

t

NTB Regular Capital Overhead Pension Salaries Other

79% of disbursements are on account of Treasury Bonds.

* Provisional unaudited data

The World Bank

Case 2: Nigeria – Net TB Support

Nigeria : Consolidated Revenue Fund 2003 : Net Position

-200

-100

0

100

200

300

400

500

600

700

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec.

Nia

ra (

Tr.)

NTB Receipts NTB Disbursements Net

In FY 03 - in ten out of twelve months NTB operations reduced monthly cash balances.

* Provisional unaudited data

The World Bank

Case 2: Nigeria – Non NTB Disbursements

Nigeria : CRF 2003: Disbursements

0

10

20

30

40

50

60

Regular Capital Overhead Pension Salaries Other

Nia

ra (

Tr.

)

Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec.

In FY 03 – Cash constraints severely impacted capital and recurrent expenditures.

* Provisional unaudited data

The World Bank

Conclusion

Poor budgeting can aggravate stress of budget management (India).Unpredictability of fund flows can severely impact project performance (Nigeria). Multitude of bank accounts result in sub optimal cash management (Nigeria).Are there robust systems for linking financial progress with physical progress?Does flow of funds result in better outcomes?