budget plan 101 mr. roeshink – finance & business technology 1

TRANSCRIPT

Budget Plan 101

• Mr. Roeshink – Finance & Business Technology

1

Debt is common in the U.S. but shouldn’t be!!!

Current as of April 2014

U.S. household consumer debt profile:• Average credit card debt: $15,191 • Average mortgage debt: $154,365 • Average student loan debt: $33,607

2

3

Why should you budget, save & invest instead of get in debt?

• You can retire early • Have a better quality of life• Don’t have to work all of your life• Can buy things out of enjoyment not necessity• If you are laid off or fired from a job you have

the funds to survive until you get a new job

4

Life Expectancy

• Average Life Expectancy– Female 82– Male 77

• Average Retirement Age (2014)– 62 Years Old

• Mounting debt, both credit card and school debt pushes Mellenial Generation retirement to 73 Years Old

5

1st Step – Emergency Fund

• The first step is to fund an emergency savings account

• If you make under $25,000 per year you should save $500 as quickly as possible

• If you make more than $25,000 per year you should save $1,000 as quickly as possible

6

1st Step – Emergency Fund

• This money is an EMERGENCY account• It is for emergencies such as:– Paying the deductible if you are in an accident or

need to go to the hospital– You have something wrong with your car and

need to get it fixed

• Once you use the emergency money you start paying it back

7

2nd Step – Debt Snowball• The principle is to stop everything except minimum

payments and focus on one thing at a time. Otherwise, nothing gets accomplished because all your effort is diluted.

• Then begin intensely getting rid of all debt (except the house) using my debt snowball plan.

• List your debts in order with the smallest payoff or balance first. Do not be concerned with interest rates or terms unless two debts have similar payoffs, then list the higher interest rate debt first.

• Paying the little debts off first gives you quick feedback, and you are more likely to stay with the plan.

8

2nd Step – Debt Snowball

• By not having debt you have the ability to save and invest instead of constantly being broke

• Most of the United States lives paycheck to paycheck

• If you have a plan of attack you can have a better quality of life

• The United States has a 4% savings per household where other countries like France has a 15% rate

9

3rd Step – Fully Funded Savings

• A fully funded savings account should have 3-6 months of savings in it

• If you get to Step 3 means you are debt free (except your house)

• Take note – a fully-funded Emergency Fund should be 3-6 months of your living expenses, not your income

10

3rd Step – Fully Funded Savings

• You’re probably looking at your mortgage or rent, utilities, groceries, gas, internet service, and phone service (or just your cell phone).

• If you’re in the midst of a true emergency, you probably would cut out (or at least pare down) eating out, entertainment, major gift giving, and big purchases that aren’t life and death.

• That new dress can most likely wait until the emergency has passed.

11

3rd Step – Fully Funded Savings

• You’re probably looking at your mortgage or rent, utilities, groceries, gas, internet service, and phone service (or just your cell phone).

• If you’re in the midst of a true emergency, you probably would cut out (or at least pare down) eating out, entertainment, major gift giving, and big purchases that aren’t life and death.

• That new dress can most likely wait until the emergency has passed.

12

3rd Step – Fully Funded Savings

• You’re probably looking at your mortgage or rent, utilities, groceries, gas, internet service, and phone service (or just your cell phone).

• If you’re in the midst of a true emergency, you probably would cut out (or at least pare down) eating out, entertainment, major gift giving, and big purchases that aren’t life and death.

• That new dress can most likely wait until the emergency has passed.

13

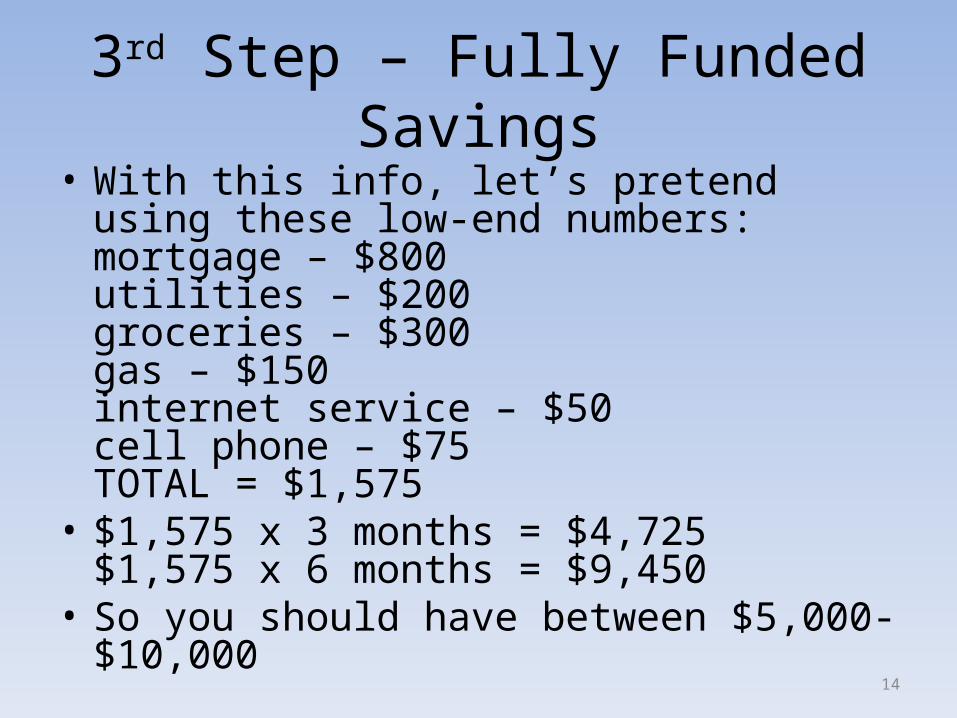

3rd Step – Fully Funded Savings• With this info, let’s pretend using these low-end

numbers:mortgage – $800utilities – $200groceries – $300gas – $150internet service – $50cell phone – $75TOTAL = $1,575

• $1,575 x 3 months = $4,725$1,575 x 6 months = $9,450

• So you should have between $5,000-$10,00014

4th Step – 15% Invested in Roth IRA & Company Plan

• Most of you will work for companies that offer a 401k retirement account

• This allows you to contribute money pre-tax into the 401k and your company matches– 8 out of 10 companies do a 401k and a match

(averages up to 3% for most companies)– The match is up to 50% of what your percentage is up

to 3%– In other words…if you contribute 6% of your income

and the company matches 50% of that it would equal up to the 3% match

15

4th Step – 15% Invested in Roth IRA & Company Plan

• By contributing 6% and the company matching 3%, you are already putting 9% of your 15% away in investments

• Now you have to fund the remaining 6%

16

4th Step – 15% Invested in Roth IRA & Company Plan

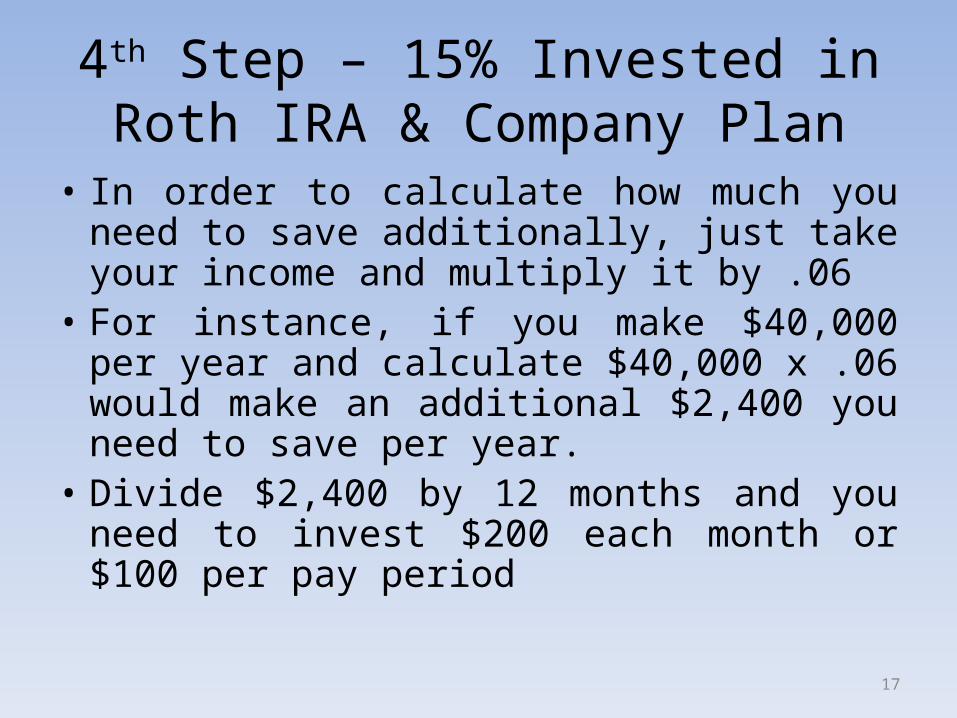

• In order to calculate how much you need to save additionally, just take your income and multiply it by .06

• For instance, if you make $40,000 per year and calculate $40,000 x .06 would make an additional $2,400 you need to save per year.

• Divide $2,400 by 12 months and you need to invest $200 each month or $100 per pay period

17

What do I invest the other 6% in?

Roth IRA• Tax-free growth• Tax-free qualified withdrawals

Traditional IRA• Tax-deferred growth• Contributions may be tax-deductible

18

Which IRA is better? Roth or Traditional?

Overall the Roth IRA is a better investment because it grows tax-free.

In other words, whatever the value grows to can be used and withdrawn tax-free when you reach 59 1/2

19

Roth IRA facts

You can contribute $5500 maximum per year as long as you are employed

If you are married and your spouse doesn’t work you can also contribute $5500 into a Roth IRA for them as well

20

4th Step – 15% Invested in Roth IRA & Company Plan

• What should you invest in?– Growth mutual funds will give you the best

returns historically– Most funds typically earn 12-15% on average per

year when held for at least 5 years or more– Not only will you find a good fund to invest in on

your additional investments, but you will do the same for your 401k

21

4th Step – 15% Invested in Roth IRA & Company Plan

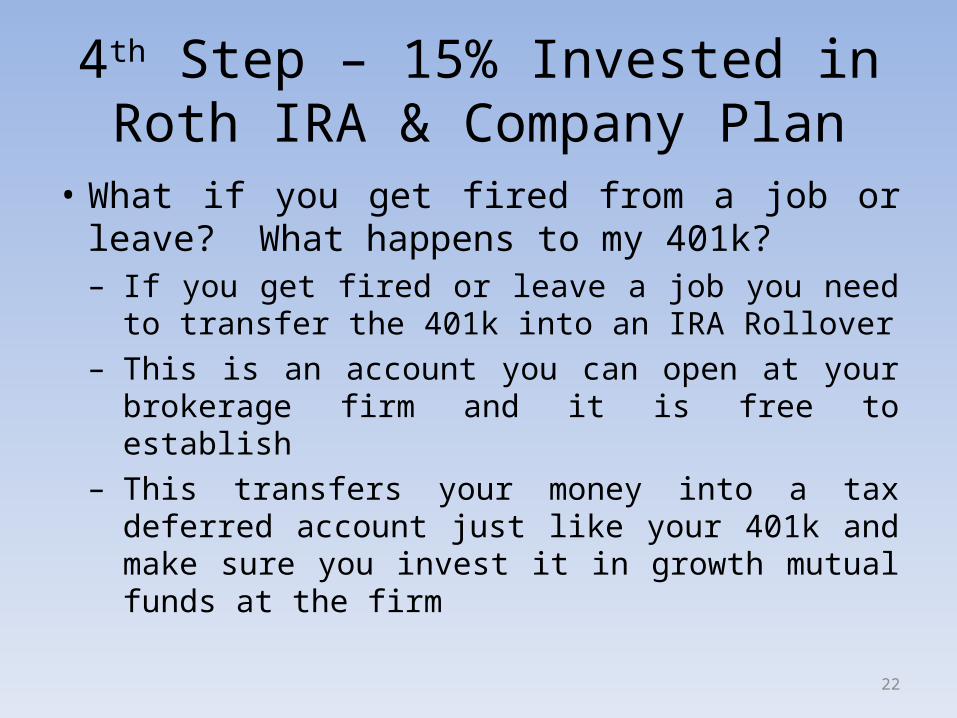

• What if you get fired from a job or leave? What happens to my 401k?– If you get fired or leave a job you need to transfer

the 401k into an IRA Rollover– This is an account you can open at your brokerage

firm and it is free to establish– This transfers your money into a tax deferred

account just like your 401k and make sure you invest it in growth mutual funds at the firm

22

4th Step – 15% Invested in Roth IRA & Company Plan

• Let’s see what 15% of a sample $40,000 salary gets you over time

• In Google type – “Compound Interest Calculator”

• Choose any of the first calculators• Parameters: $1,000 initial investment, $500

per month, 35 years to invest• If you start at age 25 you will be 60 years old

at the end of this scenario

23

Where to look at investing…

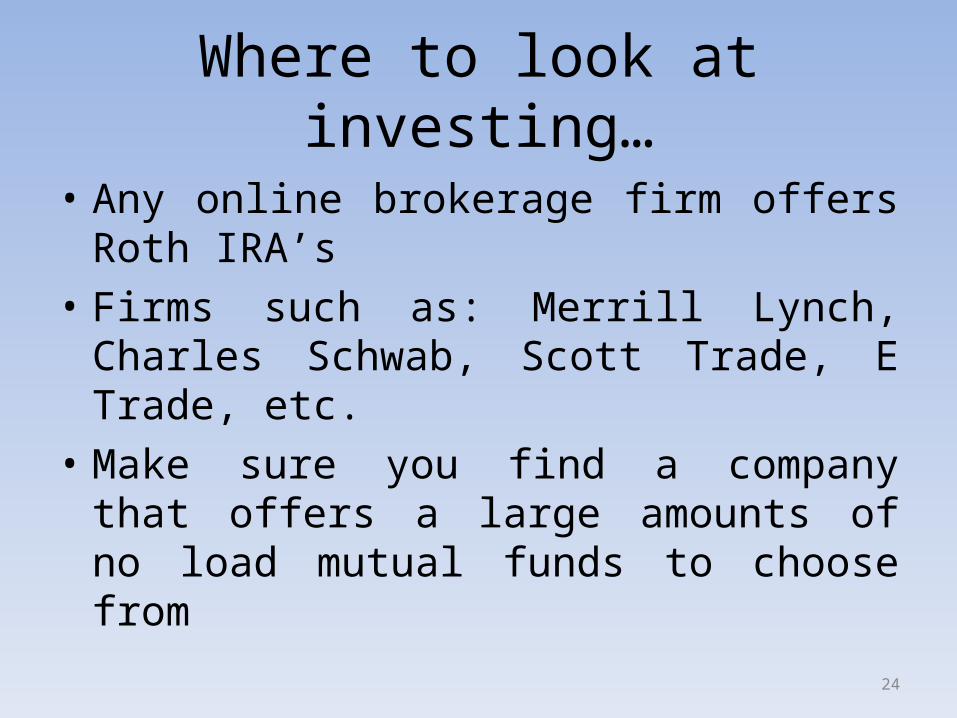

• Any online brokerage firm offers Roth IRA’s• Firms such as: Merrill Lynch, Charles Schwab,

Scott Trade, E Trade, etc.• Make sure you find a company that offers a

large amounts of no load mutual funds to choose from

24

What should you invest in a Roth IRA?

• Once you open the Roth IRA you should fund it by putting money in it

• Figure out how much you are going to put in per year

• One of the best ways to put money in is do it monthly by an Automatic Investment Plan– This is where you put in a set amount each month

and it gets invested automatically out of your bank

25

What type of investments are right for my Roth IRA

• Both your 401k and your Roth IRA should have something that requires very little thought on your part

• Most people who day trade (someone who gets in and out of stock in short amounts of time) do not make great rates of return

• Consider a mutual fund to invest in– Mutual Funds are managed portfolios where money is

pooled together to invest in certain types of stocks or sectors or strategies

26

Let’s look at a fund screener and then a compound interest calculator

• Type in Merrill Lynch in Google

• Type in “Compound Interest Calculator” in Google

27

Let’s Review So Far…

• Step 1 - $500-$1000 in an emergency fund• Step 2 – No Debt (Debt Snowball)• Step 3 – Fully Funded Savings• Step 4 – 15% in investments (Combination of

401k & Roth IRA)

28

Step 5 – Invest In Your Child’s Education

• If you have children your next step will be to invest for their education beyond high school

• Since you are all high school students, just write this step down and some of the things you can do in order to have enough money in the future for their college/university

29

Step 5 – Invest In Your Child’s Education

• There are many types of accounts set up to establish for your child’s education

• 529 Plan – Tax Deferred• UTMA/UGMA – You act as custodian• ESA (Education Savings Account) – Grows tax

free just like Roth IRA

30

Step 6 – Pay Your House Off Early

• There are many types of loans you can do

• Fixed• Interest Only• Variable

31

Step 6 – Pay Your House Off Early

• Fixed Rate Mortgage – you pay a fixed interest rate for the life of the mortgage

• Interest Only – You pay the interest only for the loan for a period of 5-10 years and then it changes to a different type of loan

• Variable Rate – Pay a rate that changes throughout time

32

Step 6 – Pay Your House Off Early

• A fixed interest rate is the best choice for a mortgage

• Also, it is highly advised to do a 20 or 15 year mortgage instead of a 30 year.

• Most people do a 30 year loan, but a 15 is the preferred if you want financial freedom from the biggest debt you will have in your lifetime

33

Step 6 – Pay Your House Off Early

• Example:– As of 5/28/14 we will look at a 15 year and a 30

year mortgage of $150,000– The 15 year payment would be $1000 and the 30

year would be $700– It would save over $80,000 in interest doing a 15

year instead of a 30 year and it would free up whatever you were paying to the mortgage for investing in a Roth IRA

34