budgetary overview of 2007-2008 budget development

DESCRIPTION

BUDGETARY OVERVIEW OF 2007-2008 BUDGET DEVELOPMENT. January 24, 2007. 2007-2008 SCHOOL BUDGET. DISTRICT GOALS FISCAL RESPONSIBILITY Educate the community on the liability associated with tax certiorari claims and develop a long-range plan to address this. HOME AND COMMUNITY PARTNERSHIPS - PowerPoint PPT PresentationTRANSCRIPT

BUDGETARY OVERVIEW OF 2007-2008 BUDGET

DEVELOPMENT

January 24, 2007

2007-2008 SCHOOL BUDGET

DISTRICT GOALS FISCAL RESPONSIBILITY

1. Educate the community on the liability associated with tax certiorari claims and develop a long-range plan to address this.

HOME AND COMMUNITY PARTNERSHIPS1. Develop and implement a contract

between families and our school that outlines teaching and learning responsibilities for all parties.

2007-2008 SCHOOL BUDGET

DISTRICT GOALS

STUDENT SUPPORT

1. Review and evaluate special education services and delivery models in light of state and federal requirements.

2. Pilot an inclusive education model for students in the intermediate house.

3. Staff the school system in ways that better represent our diverse student population.

2007-2008 SCHOOL BUDGET

DISTRICT GOALS

ACADEMIC EXCELLENCE

1. Integrate new instructional technologies with classroom instruction.

2. Implement revised math curriculum through multiple resources including our new math textbooks and software.

2007-2008 SCHOOL BUDGET

DISTRICT GOALS

STAFF EFFECTIVENESS1. Review and map the social studies curriculum,

Grades K-8, aligning it with NYS Standards and identify resources necessary to implement it.

2. Continue professional development in instructional technology, differentiated instruction, English Language Arts and standards-based math.

BOARD GOALS1. Develop a school budget process that reflects

the community’s interests.

2007-2008 SCHOOL BUDGETCommunication Plan

The school community newsletter that will be released within the next two weeks will provide a listing of all budget workshop dates.

The district has created 2007-2008 Budget Communication Plan & Timeline to further assist the community in learning about the proposed school budget.

2007-2008 SCHOOL BUDGETCommunication Plan Recommendations

1. At each of the six identified budget workshops the entire budget will be presented to ensure that residents that miss one or more budget workshops will not miss the description of the budget.

2. The budget workshops will be televised on the public access educational television channels.

3. The instructional staff, student government, School Foundation and PTA will be provided with a budget presentation.

4. The Budget Newsletter will be mailed at two distinct times to generate community input, once prior to the Board’s adoption of the budget, and once prior to the legally required budget hearing.

5. A special e-mail address has been reestablished to provide an avenue for community residents to pose questions and/or comments, and receive a response from the Assistant Superintendent – [email protected]

2007-2008 SCHOOL BUDGETCommunication Plan Recommendations

6. Budget information will be posted to the District’s website throughout the budget development process

7. In addition to the community wide invitation to attend the budget workshops, key neighborhood community members will be invited to attend budget workshops.

8. Reminder to Vote telephone chains will be employed to encourage community members to vote on May 15, 2007.

9. The K12 alerts system will be used periodically to remind all who have registered to attend the budget workshops.

2007-2008 SCHOOL BUDGET

2007-2008 Budget Communications Plan & Timeline

2007-2008 SCHOOL BUDGET

A school budget is a financial plan created to support the operation of the school system and the delivery of the educational program.

The budget process begins in November with a workshop with the staff.

2007-2008 SCHOOL BUDGET

Budget Presentation: the budget must be presented at the budget hearing, not less than seven (7) or more than fourteen (14) days prior to the annual meeting/budget vote date. - May 7

Budget Availability; the budget document shall be complete and available upon request to residents within the district (7) days before the budget hearing and fourteen (14) days before the annual meeting/vote date. – May 1

2007-2008 SCHOOL BUDGET

Annual Meeting and Election: The annual meeting and election must be held on the third Tuesday of May. (May 15, 2007)

Three-Part Budget: Districts are required to prepare a three-part budget containing administrative, program, and capital components.

2007-2008 SCHOOL BUDGET Budget Development Timeline

November 2, Staff Orientation to Budget Development

December 20, Budget Worksheets Submitted to the Business Office

March 12, Board of Education Meeting/Review of Preliminary Budget

March 6, Board of Education Meeting/Review of Preliminary Budget

January 24, 2007 Board Discussion of Significant Budgetary Considerations

2007-2008 SCHOOL BUDGET Budget Development Timeline

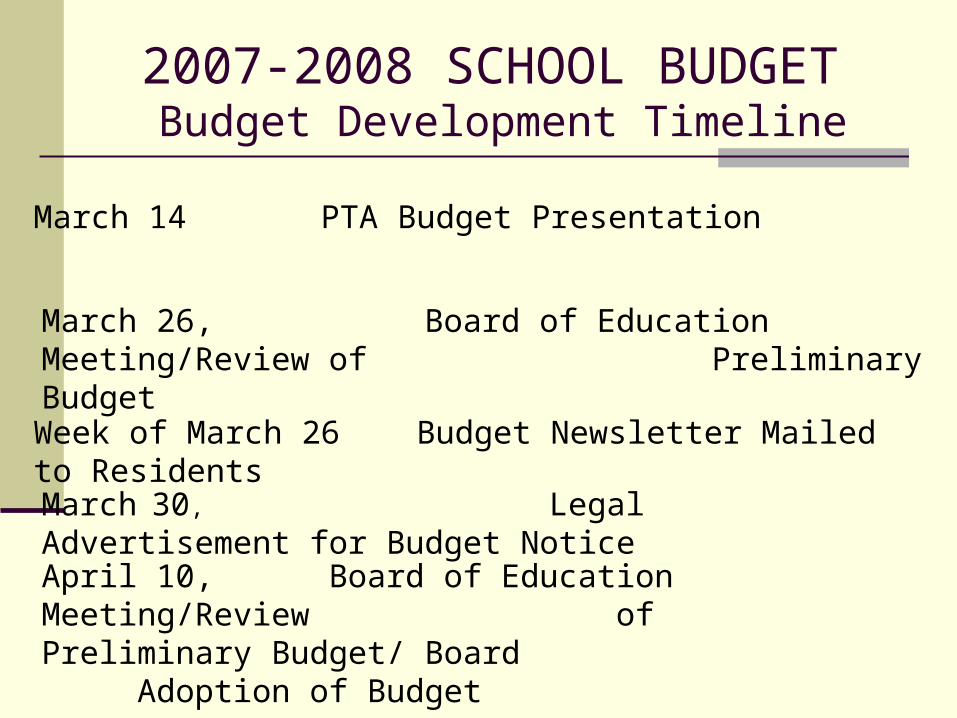

March 26, Board of Education Meeting/Review of Preliminary Budget

April 10, Board of Education Meeting/Review of Preliminary Budget/ Board Adoption of Budget

March 30, Legal Advertisement for Budget Notice

Week of March 26 Budget Newsletter Mailed to Residents

March 14 PTA Budget Presentation

2007-2008 SCHOOL BUDGET Budget Development Timeline

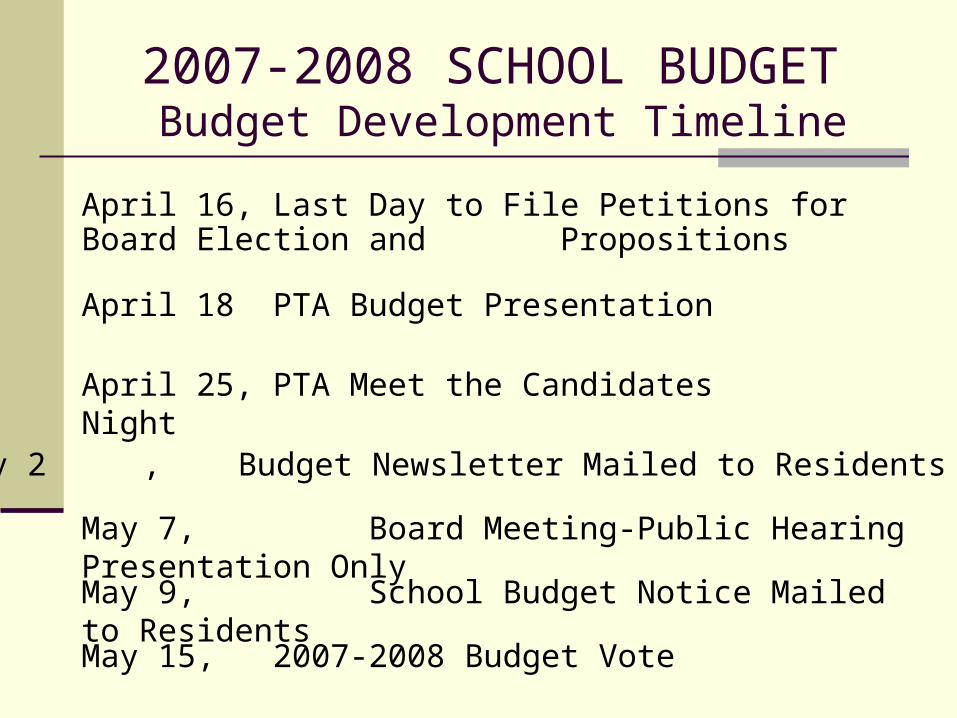

May 15, 2007-2008 Budget Vote

May 7, Board Meeting-Public Hearing Presentation OnlyMay 9, School Budget Notice Mailed to Residents

May 2 , Budget Newsletter Mailed to Residents

April 16, Last Day to File Petitions for Board Election and Propositions

April 18 PTA Budget Presentation

April 25, PTA Meet the Candidates Night

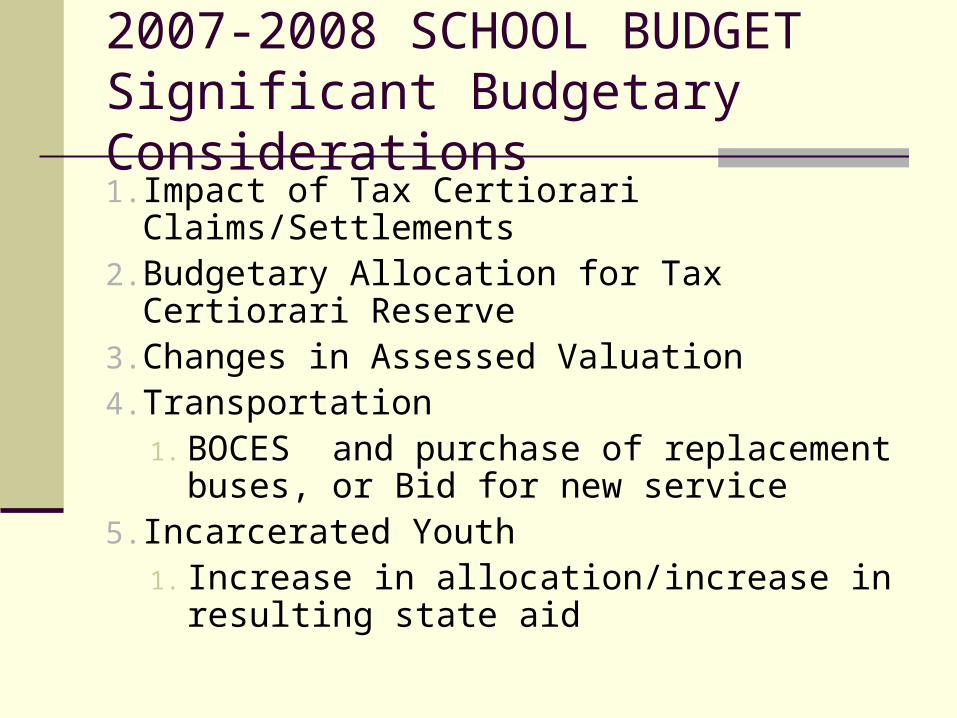

2007-2008 SCHOOL BUDGETSignificant Budgetary Considerations1. Impact of Tax Certiorari

Claims/Settlements2. Budgetary Allocation for Tax Certiorari

Reserve3. Changes in Assessed Valuation4. Transportation

1. BOCES and purchase of replacement buses, or Bid for new service

5. Incarcerated Youth1. Increase in allocation/increase in

resulting state aid

2007-2008 SCHOOL BUDGETSignificant Budgetary Considerations6. Health Insurance Increases7. Salary Increases8. Retirement Cost Increases9. Workers Compensation/Liability

Insurance Cost Increases10.High School Tuition Increases11.One Time Offsets for Fire Alarm Bid

Savings

School District Funds

• The general fund relies on taxes, state aid, and miscellaneous revenue and supports all regular school activities

• The school lunch fund provides the child nutrition program to our students and is a self sustaining program • The special aid fund provides for the district’s grant funded programs

School District Funds

•The capital fund provides for all permanent improvements to our facilities and is funded from the general fund and bond issue proceeds • The trust and agency funds are used to account for assets held by a governmental unit in a trustee capacity and/or as agent for individuals. The funds are custodial in nature and are used to account for contributions or endowments

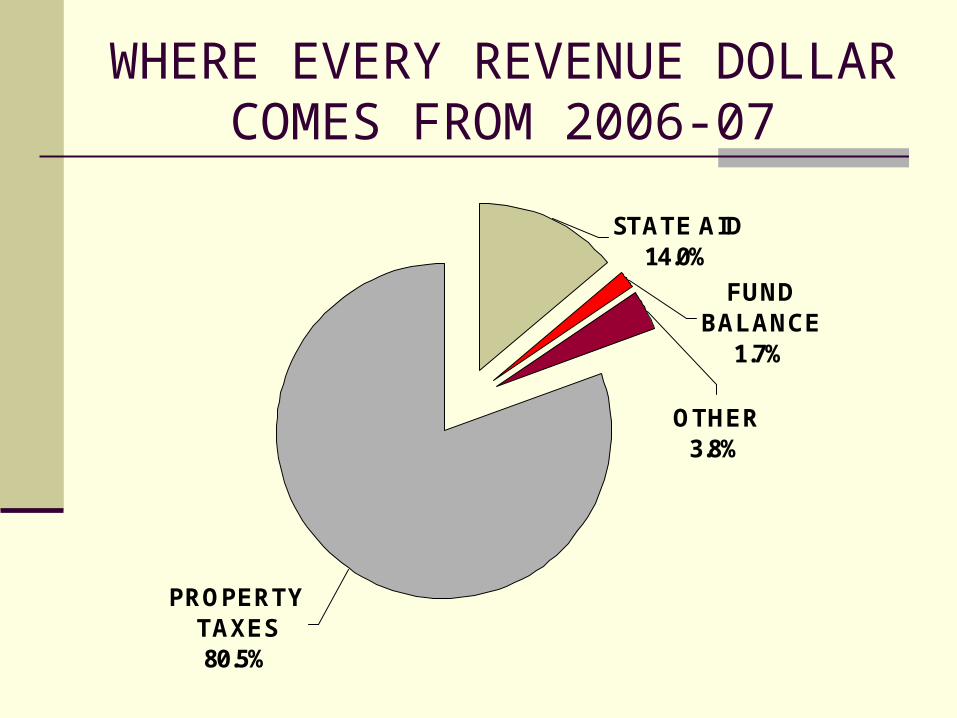

WHERE EVERY REVENUE DOLLAR COMES FROM 2006-07

STATE AID14.0%

FUND BALANCE

1.7%

OTHER3.8%

PROPERTY TAXES80.5%

Assessed Valuation Mt. Pleasant

Mt Pleasant

15,200,000

15,400,00015,600,000

15,800,000

16,000,000

16,200,00016,400,000

16,600,000

16,800,000

2003-04 2004-05 2005-2006

2006-2007

2007-2008

Mt Pleasant

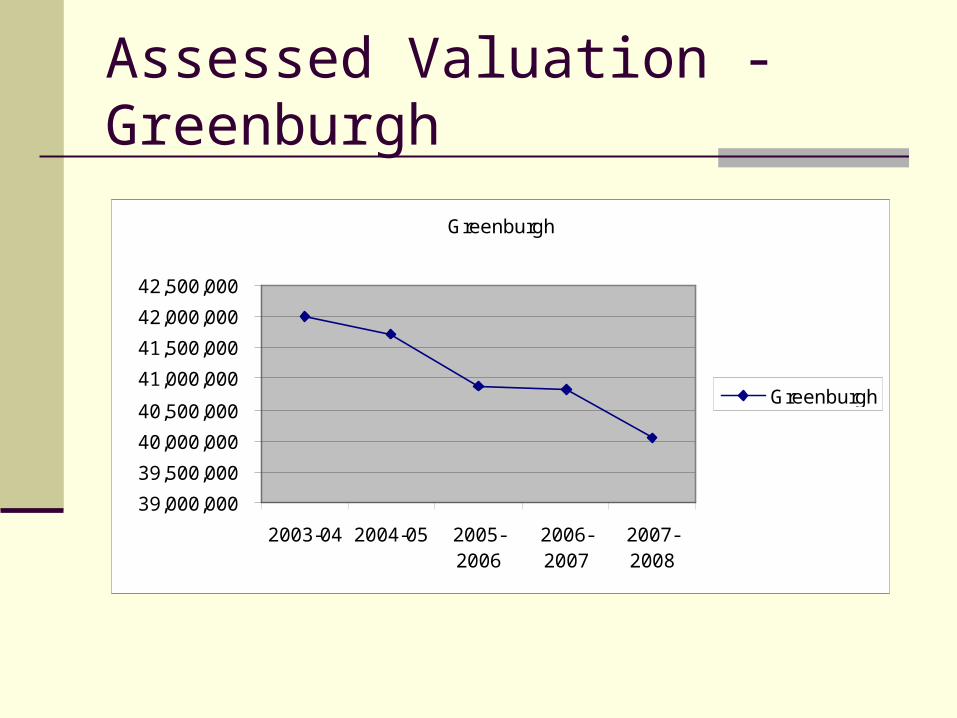

Assessed Valuation - Greenburgh

Greenburgh

39,000,000

39,500,000

40,000,000

40,500,000

41,000,000

41,500,000

42,000,000

42,500,000

2003-04 2004-05 2005-2006

2006-2007

2007-2008

Greenburgh

Tax Rate Table

BUDGET AMOUNT IMPACT ON TAX RATE$ 100,000 .67%

$ 147,000 1.00%

$ 250,000 1.69%

$ 500,000 3.38%

$ 770,000 5.20%

$ 1,000,000 6.75%

Contingency Budgets

Single revote: Upon the defeat of the original proposed school budget, a district may resubmit the original budget, submit a revised budget, or adopt a contingency budget. If the voters fail to approve the budget upon the second vote, the district must adopt a contingency budget. Expanded definition: Interscholastic athletics, field trips, other extracurricular activities, and related transportation expenses are contingent expenses.

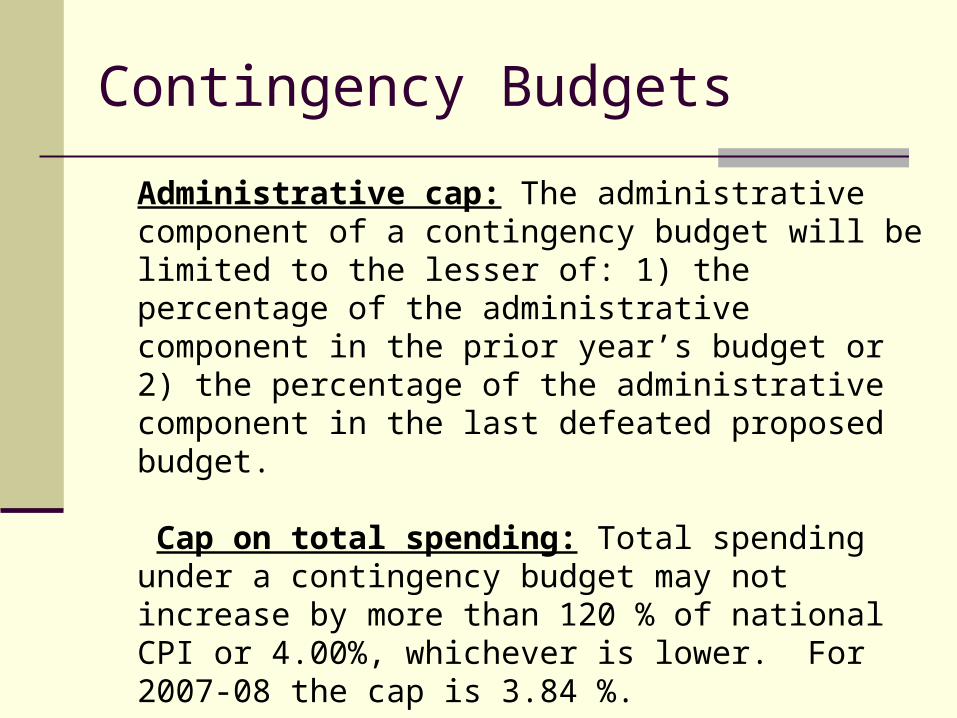

Contingency Budgets

Administrative cap: The administrative component of a contingency budget will be limited to the lesser of: 1) the percentage of the administrative component in the prior year’s budget or 2) the percentage of the administrative component in the last defeated proposed budget. Cap on total spending: Total spending under a contingency budget may not increase by more than 120 % of national CPI or 4.00%, whichever is lower. For 2007-08 the cap is 3.84 %.

BUDGETARY OVERVIEW OF 2007-2008 BUDGET DEVELOPMENT