builders risk coverage and claims - saxe .... saxe is one of the panelists for workshop t3,...

TRANSCRIPT

CIn

Workshop T3

Tuesday, November 139:00 a.m.–noon and 1:30–4:30 p.m.

BUILDERS RISK COVERAGE AND CLAIMS

Presented by

Panelists:

Worksh

Steven A. CoombsPresident

Risk Resources, Inc.

William B. NoonanVice President—

Risk ManagementStructure Tone Organization

Tracy Alan SaxePartner

Saxe Doernberger & Vita, P.C.

Vincent ZegersNational Construction

Placement Specialist—Property PracticeMarsh USA, Inc.

op T3Moderator:

William S. McIntyre IVChairman

American ContractorsInsurance Group

Builders risk insurance is a key element of a constructionrisk management program. Because it is a nonstandardcoverage, policy terms and provisions vary, which makesunderstanding and arranging appropriate coveragechallenging. Disputes on claims can arise from a variety ofsources, including cause of loss, waivers of subrogation, anddelay damages, application of sublimits, and more. Thispanel will examine some of the more complex andproblematic coverage and claims issues encountered inbuilders risk insurance, including contractors’ need for amaster builders risk program when the project owner isproviding coverage.

1

opyright © 2012 International Risk Management stitute, Inc.

www.IRMI.com

XL GroupInsuranceReinsurance

From contract to construction, we’re with you.XL Group’s global reach covers every phase of your project, no matter where in the world you’re building it. Beginning to end. Front to back. Start to finish. You get the idea.

CapAssure, our Contractor/Subcontractor Default coverageConstructAssure, Subcontractor Default coverageUmbrella LiabilityGeneral LiabilityEnvironmental LiabilityArchitects & EngineersBuilder’s RiskProperty & Business InterruptionEmployer’s LiabilityWorkers CompDirectors’ and Officers’ LiabilityProfessional LiabilityAuto LiabilityEquipment Breakdown

With our mix of underwriting expertise, risk engineering and quick, fair claims handling, we’re here to support you every step of the way.

We’re the perfect size. Big enough to protect you and small enough to stay flexible.

Talk to your broker or visit us online: xlgroup.com/insurance

MAKE YOUR WORLD GO

and MAKE YOUR WORLD GO are trademarks of XL Group plc companies. XL Group is the global brand used by XL Group plc’s insurance subsidiaries. In the US, the insurance companies of XL Group plc are Greenwich Insurance Company, Indian Harbor Insurance Company, XL Insurance America, Inc., XL Insurance Company of New York, Inc., XL Select Insurance Company and XL Specialty Insurance Company. Not all of the insurers do business in all jurisdictions nor is coverage available in all jurisdictions.

XLGroup_IRMI Conference Tab_2012.indd 1 6/21/2012 9:59:06 AM

Worksh

op T3

William McIntyre IVChairman

American Contractors Insurance Group

Mr. McIntyre is cochairman of this Conference, and he is moderating Monday’s General Session as well asthe panel for Workshop T3, “Builders Risk Coverage and Claims,” on Tuesday. For more than 40 years, Mr.McIntyre has been involved in the insurance industry. He is Chairman of American Contractors InsuranceGroup, Ltd. (ACIG), in Dallas. ACIG is construction-industry-owned. Mr. McIntyre has been very activeover the years with the Associated General Contractors of America, writing articles and reviewing indus-try contract documents. He has written many articles on insurance and risk management for constructionand insurance industry trade journals. He coauthored 101 Ways To Cut Business Insurance Costs, publishedby International Risk Management Institute, Inc. (IRMI). Mr. McIntyre also is a technical adviser for IRMI’sreference manual for contractors, Construction Risk Management.

Steve Coombs, ARM, CPCUPresident

Risk Resources, Inc.

Mr. Coombs is one of the panelists for Workshop T3, “Builders Risk Coverage and Claims,” on Tuesday. Mr.Coombs has 34 years of industry experience, with the last 28 years in a consulting environment. Prior tothat, he was a national accounts underwriter for a large international insurance group. Risk Resources is arisk management and commercial insurance consulting firm based in LaGrange Park, IL. Risk Resourcesdoes not sell insurance and provides consulting services on a fee-for-service basis. Common projects includerisk management and insurance audits, insurance RFPs/proposal management, wrap-up feasibility reviews,agent/broker/administrator selection, risk financing studies, litigation support, and testimony.Mr. Coombs has significant experience in underwriting and consulting on builders risk insurance programs,while representing owners, developers, design teams, construction managers, and general contractors. Hehas extensive knowledge and experience regarding various aspects of construction insurance. He is a coau-thor of The Builders Risk Book, published by IRMI. He is an IRMI Expert Commentator on builders risk issues.He is also a former president of the Society of Risk Management Consultants.Mr. Coombs is a graduate of Western Michigan University with a Bachelor of Business Administrationdegree. He also holds an M.A. from DePaul University with a concentration in Risk Management and Insur-ance. He has earned the Associate in Risk Management (ARM) certificate from the Insurance Institute ofAmerica and received the Chartered Property Casualty Underwriter (CPCU) designation.

3

William NoonanVice President—Risk Management

Structure Tone Organization

Mr. Noonan is one of the panelists for Workshop T3, “Builders Risk Coverage and Claims,” on Tuesday. Mr.Noonan is the chief risk officer/vice president of risk management for the Structure Tone Organization,which includes Structure Tone Inc., Pavarini Construction Company, Pavarini McGovern, and ConstructersConstruction Company. The Structure Tone Organization performs interior fit out construction, renova-tion, and new core and shell construction with an annual construction volume of more than $2 billion.In his role as vice president of risk management, Mr. Noonan oversees the corporate insurance programand the rolling contractor controlled insurance program and leads risk management initiatives through-out the organization. Mr. Noonan holds the CRIS and MLIS certifications from International Risk Manage-ment Institute, Inc. (IRMI).Prior to working at Structure Tone, Mr. Noonan has 21 years’ experience in the risk management industry,and prior to working at Structure Tone, he served as a regional director for Turner Construction’s Casu-alty and Surety Division. Mr. Noonan is a speaker at many national conferences and seminars, includingthe IRMI Construction Risk Conference. Tracy Saxe

PartnerSaxe Doernberger & Vita, P.C.

Mr. Saxe is one of the panelists for Workshop T3, “Builders Risk Coverage and Claims,” on Tuesday. Mr.Saxe is a skilled commercial litigator with more than 25 years of trial experience. Since 1990, he hasfocused his practice on insurance coverage issues, disputes, litigation, and trials on behalf of policyhold-ers, handling cases involving coverage for comprehensive general liability, directors & officers, profes-sional liability, builders risk, subguard, first-party property damage, additional insured, business inter-ruption claims, and crime bonds. Mr. Saxe has handled cases involving coverage for construction defects,completed operations, product liability, property damage and bodily injury related to mold and asbestos,bodily injury related to construction, “sick building” syndrome, environmental claims, business interrup-tion, employment disputes, patent infringement, contempt, RICO, unfair practices, breach of fiduciaryduty, bad faith, and professional malpractice. Mr. Saxe was a principal at the law firm of Sachs, Berman, Rashba & Shure, P.C., from 1987 to 1994. Hejoined that firm following 4 years as an associate with Wofsey, Rosen, Kweskin & Kuriansky in Stamford,Connecticut. He left in 1994 to open the Connecticut office of Anderson, Kill, Olick & Oshinsky, and in 1996founded Saxe Doernberger & Vita, P.C.Mr. Saxe holds a J.D. from Georgetown University Law Center, 1983; and a B.A., Policy Studies, magna cumlaude, Phi Beta Kappa, Syracuse University, 1980.He is American Bar Association Insurance Coverage Litigation Committee (ICLC) Construction Sub-com-mittee Cochair and ABA ICLC Program Committee Co-Vice-Chair.

4

Worksh

op T3

Vincent ZegersNational Construction Placement Specialist—Property Practice

Marsh USA, Inc.

Mr. Zegers is one of the panelists for Workshop T3, “Builders Risk Coverage and Claims,” on Tuesday. Mr.Zegers is a Placement Specialist focusing on construction—Construction All Risk, Builders All Risk, Erec-tion All Risk, and Installation Risks. In addition to driving placements in the market, Mr. Zegers also assistson new business production. Mr. Zegers combines the technical expertise of an engineer with the innova-tion of a creative underwriter to assess and creatively manage construction risk. Mr. Zegers is located inMarsh’s Chicago, Illinois, office.Prior to joining Marsh in 2011, Mr. Zegers was a managing director in the global property solutionsdepartment at another large broker. He was responsible for structuring property and contingency risksolutions for complex construction projects, and projects located in regions exposed to catastrophic risk.He has over 30 years of underwriting experience in the international (re)insurance marketplace, and willfurther enhance the company’s ability to structure creative solutions utilizing global risk capital. He hasalso previously held a number of senior leadership positions with Swiss Re both in the United States andEurope.While working in Europe, Mr. Zegers started his career as a loss adjuster and was a primary insurer in theConstruction line of business for 14 years. He worked for the Swiss Re for more than 10 years.Mr. Zegers earned his Civil Engineering degree in the Netherlands.

5

Notes

This file is set up for duplexed printing. Therefore, there are pages that are intentionally left blank. If you print this file, we suggest that you set your printer to duplex.

6

Worksh

op T3

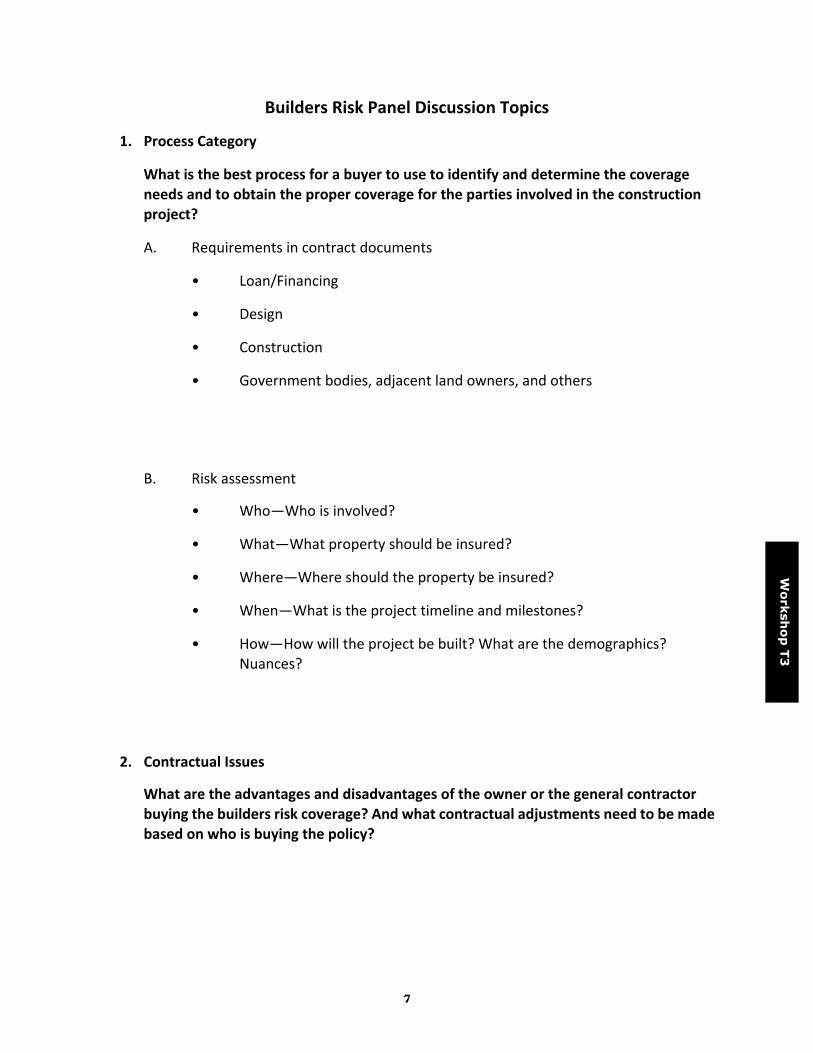

Builders Risk Panel Discussion Topics

1. Process Category

What is the best process for a buyer to use to identify and determine the coverage needs and to obtain the proper coverage for the parties involved in the construction project?

A. Requirements in contract documents

• Loan/Financing

• Design

• Construction

• Government bodies, adjacent land owners, and others

B. Risk assessment

• Who—Who is involved?

• What—What property should be insured?

• Where—Where should the property be insured?

• When—What is the project timeline and milestones?

• How—How will the project be built? What are the demographics? Nuances?

2. Contractual Issues

What are the advantages and disadvantages of the owner or the general contractor buying the builders risk coverage? And what contractual adjustments need to be made based on who is buying the policy?

7

3. Contractual Issues

Should contractors and subcontractors be a “named insured,” an “additional named insured,” or an “additional insured” under the builders risk policy? What are the practical differences in these terms, and what is the impact of defining parties incorrectly? Also, should all parties be listed as the named insured?

• First of all , read the specific policy language because each policy form uses its own definition; i.e., named insured versus additional named insured and additional insured.

• The named insured is the entity taking out the policy and is responsible for paying the premium and handling the claims and will be receiving the insurance proceeds if there is not a designated “loss payee.”

• With naming an additional entity an additional named insured, you give this entity the same “status” as the named insured so, for instance, insurance proceeds can go the this entity, as well.

• Be aware that by adding a party to the list of additional insureds, you automatically waive the rights of subrogation against that entity. Is that the purpose?

4. Direct Property Issues

Under what circumstances is a builders risk policy cancelable, and under what circumstances is it noncancelable?

• Typically a builders risk policy is cancelable by the (1) insurer if premium has not been paid (10 days’ notification), (2) insurer for any reason (45 days), or (3) named insured for any reason.

• Each situation has a certain (minimum earned) return premium calculation applied to it.

• Typically there is no provision for when it is noncancelable.

• Insurers should NOT be allowed to cancel the policy other than for nonpayment of premium (or material change of project or losing their treaties).

• BR policies overseas are always noncancelable by insurers (except for nonpayment of premium).

8

Worksh

op T3

• Specialty lenders should not accept cancelable builders risk policies.

• Check special state provisions for admitted insurers.

5. Direct Property Issues

Builders risk policies sometimes include coverage for increased costs of construction in rebuilding damaged property. What about the unbuilt portion? Are increased costs of construction for the not-yet-built property also covered?

A. Possibly. The specific policy language and legal jurisdiction governing the loss maybe significant to the outcome of a higher building cost claim.

Policy Language

• Builders risk policies are nonstandardized.

• Insofar as the unbuilt portion of the construction project is not physically damaged, it might not be considered a “direct physical loss.”

• Many builders risk policies also exclude “delay” damages.

• The specific policy’s “covered property” definition may also be important.

• Newer builders risk policies may also include specific provisions for these higher building costs.

Legal Jurisdiction

• There is minimal caselaw addressing this topic, and it is divided:

A. Zurich Am. Ins. Co. v. Keating Bld. Corp., 513 F. Supp. 2d 155 (D. N.J. 2007)(finding coverage)

B. Oceanside Pier View, LP v. Travelers Prop. & Cas. Co. of Am., 2008 WL7822214 (S.D. Cal 2008) (rejecting coverage)

• Given the limited amount of legal precedent addressing this issue, it is hard to predict within any certainty how other courts would rule.

9

Solutions

A. Review the builders risk policy to determine if it contains broader (or more restrictive) loss and covered property insuring conditions.

B. Couch the claim as a loss involving “hard costs” directly caused by property damage, with “delay” as a secondary factor or nonfactor.

C. Review the caselaw to determine if there are any new decisions on the topic, and determine if the claim is plausibly within a favorable jurisdiction or outside an unfavorable jurisdiction.

6. Soft Costs Category

Let’s clarify what are soft costs, and what are the most common soft costs coverage gaps?

A. What are soft costs?

• This is a moving target for the insurance industry.

• Underwriters and insurers cannot agree on what “soft costs” are.

• Provide definitions of hard costs and soft costs.

• Provide examples.

• Each insurer defines differently—some are in preprinted forms, check the box, or manuscripted.

B. What are the most common coverage gaps?

• Failure to list the needed specific soft costs in the policy

• Inadequate limits

• Insurer deems the costs as “not necessary” or repairs were not timely completed

• Exclusion of expenses prior to “anticipated completion date”

10

Worksh

op T3

7. Soft Cost Coverage

When does the “period of indemnity” for soft costs coverage begin and end? What are some of the issues and challenges?

8. Claims Category

Large builders risk claims are complex and pose a variety of challenges for adjusters. What should the insureds expect from the insurer’s and broker’s claim teams?

A. Insureds should expect from insurer(s):

• Immediate investigation

• Timely initial request of documents

• Appointment of a “clerk of the works” for larger claims

• Rapid approval of expenses to mitigate/avoid delays

• Interim payments—initial and ongoing

• Flexibility

B. Insureds should expect from their brokers:

• Support—review of documents

• Technical review of coverage issues

• Advocacy and advice

11

9. Claims

What are some basic tips that, if followed, will really help at the time of a claim but are often forgotten because they are so simple?

10. Claims

If the anticipated completion date changes, what adjustments need to be made to the builders risk policy?

• An endorsement should be issued reflecting the revised expiration date.

• An endorsement should be issued reflecting the revised trigger date for the delay cover if added to the builders risk policy.

• An explanation should be provided by the named insured for why the anticipated completion date has changed.

• A revised schedule should be provided so Insurers can review the new schedule.

• A new delay in start-up time deductible could/should be determined depending on (1) the reason of the revised term and/or (2) whether the time deductible is based on a “per occurrence basis” or has been defined as “an aggregate time deductible.”

• Verification of whether or not the sum insured would stay the same. (Different trigger date could mean different amounts to be insured for the potential loss of revenue stream because of seasonal fluctuations, for instance.)

12

Worksh

op T3

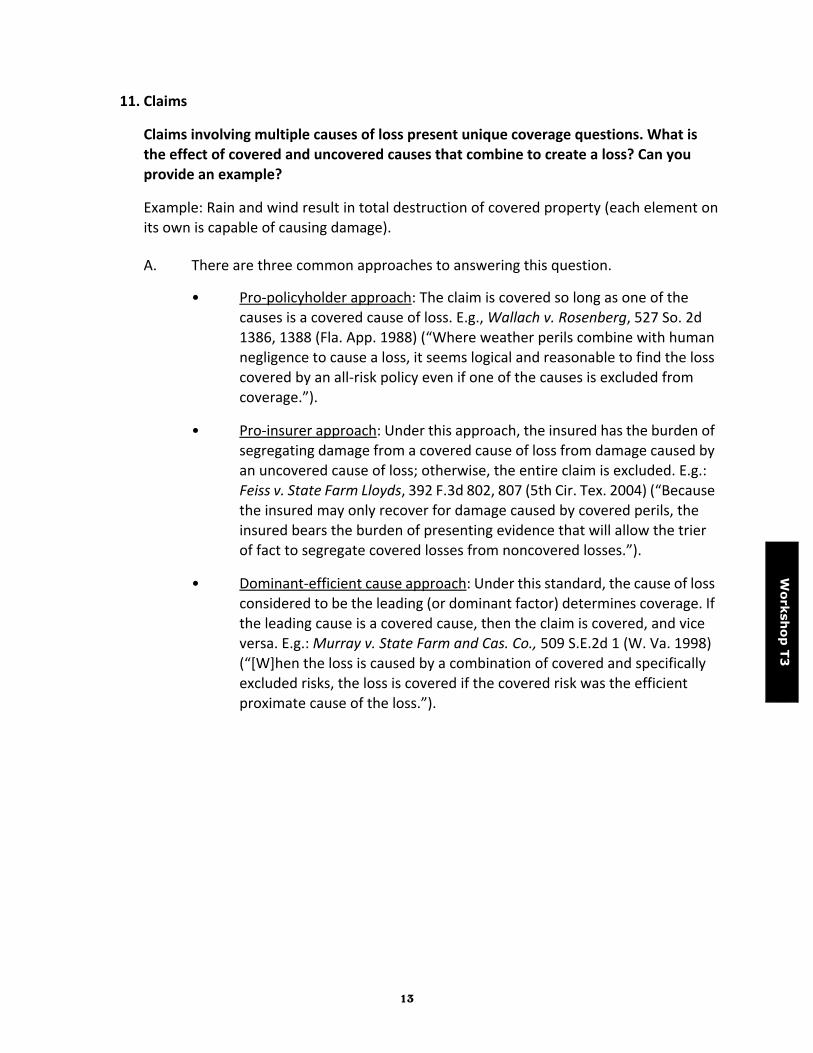

11. Claims

Claims involving multiple causes of loss present unique coverage questions. What is the effect of covered and uncovered causes that combine to create a loss? Can you provide an example?

Example: Rain and wind result in total destruction of covered property (each element onits own is capable of causing damage).

A. There are three common approaches to answering this question.

• Pro-policyholder approach: The claim is covered so long as one of the causes is a covered cause of loss. E.g., Wallach v. Rosenberg, 527 So. 2d 1386, 1388 (Fla. App. 1988) (“Where weather perils combine with human negligence to cause a loss, it seems logical and reasonable to find the loss covered by an all-risk policy even if one of the causes is excluded from coverage.”).

• Pro-insurer approach: Under this approach, the insured has the burden of segregating damage from a covered cause of loss from damage caused by an uncovered cause of loss; otherwise, the entire claim is excluded. E.g.: Feiss v. State Farm Lloyds, 392 F.3d 802, 807 (5th Cir. Tex. 2004) (“Because the insured may only recover for damage caused by covered perils, the insured bears the burden of presenting evidence that will allow the trier of fact to segregate covered losses from noncovered losses.”).

• Dominant-efficient cause approach: Under this standard, the cause of loss considered to be the leading (or dominant factor) determines coverage. If the leading cause is a covered cause, then the claim is covered, and vice versa. E.g.: Murray v. State Farm and Cas. Co., 509 S.E.2d 1 (W. Va. 1998) (“[W]hen the loss is caused by a combination of covered and specifically excluded risks, the loss is covered if the covered risk was the efficient proximate cause of the loss.”).

13

Preface to Panelists Articles—T3

In Their Words …

We asked the panelists to describe a troublesome builders risk coverage or claims issue and

outline possible solutions. They provided some great food for thought.1

1 The opinions expressed in these vignettes are those of the authors and are not necessarily held by IRMI or its employees. These articles do not purport to provide legal advice or opinion, which can only be given when related to specific fact situations. When seeking to resolve specific safety, legal, or business issues or concerns, consult your safety consultant, attorney, or business advisers.

14

Worksh

op T3

What Costs Should Be Included in “Soft Costs” Coverage, and How Do I Quantify These Costs?

by Steve Coombs, Risk ResourcesSoft costs insurance is one of the most misunderstood coverages—by insurers, underwriters, brokers, owners, designers, and contractors alike. Ask five people what “soft costs” mean, and you will likely hear five different answers. It seems like no one really has a good handle on this important coverage.Everything about this coverage is nonstandard. Policy forms used by insurers differ greatly, as do the specific types of soft costs that are insured by these forms. It is rare when a “soft costs” coverage form includes the phrase “… including but not limited to….” Generally, underwriters like to specify the exact types of soft costs that are to be insured. As a result, the purchasers of this coverage and their advisers must do their homework before the builders risk insurance program is put in place. This can be challenging because specified information may not be readily available or may be difficult to quantify.Each project is different. As such, there is no standard list of soft costs that should be insured. So how does one go about it? Essentially, there are three steps.The first step is to identify each of the different soft costs that will be incurred if there is a project delay due to accidental damage to the project. A checklist is very helpful in this regard, as it is next to impossible to recall all the possible types of costs that could result. (A sample form is attached for reference.) A project owner may not know offhand which costs will be incurred following a project delay. The owner often will confer with others to gain their thoughts and ideas.The second step is to estimate the dollar value for each of the identified soft costs. This is done by first estimating the length of a project delay (keep in mind that the period of delay lengthens when (a) the size/severity of the underlying physical damage loss increases, and/or (b) the loss occurs during the latter stages of the project). Once the duration of the delay is estimated, a dollar amount can be established. This is typically done with the input of the owner, contractor, and architect.The last step is to evaluate whether or not the policy forms proposed by the builders risk insurer will apply to the different soft costs identified and quantified. Chances are that the answer is “no.” This will necessitate the negotiation and issuance of specialized or manuscripted endorsements. Insurance underwriters will generally go along with customizing the coverage once they become comfortable with the coverage request(s) being made and after charging an appropriate premium.A side benefit of this process is that those involved will have a deeper understanding of theproject and the associated risks.

15

Construction Soft Cost Checklist

Date: ______________________________________________Project: ______________________________________________Owner: ______________________________________________Architect: ______________________________________________

Description of Extra Cost Estimated Cost ($) Yes No CommentsAbatement costAccounting feesAdditional cost of construction materials and laborAdvertising, promotional, sales, and marketing expensesAppraisalsArchitect, engineering, and consultants feesAssessmentsBuilding inspection feesCommissions/fees for renegotiation of leasesConstruction loan feesConstruction management feesDebt service paymentsDevelopment fees and other costsEquipment rentalExpediting expensesExpenses to prepare a proof of lossExtended general conditionsExtra printing, copying, and mailing costsExtra travel and lodging costs for employeesFeasibility/plan studiesFees for letters of credit and remarketing of bondsFinancing/refinancing costsFounders fee refundsFurniture, fixtures, and equipment storage feeGeneral overhead expenses (developer)Historic tax creditsInsurance costsInterest expense for loans/bondsInterest pointsLeasing expenses (including renegotiation)Letters of credit Legal feesLicense feesLoan origination commitment/closing costsLoss of tax creditsOffice expensesPermit feesPreopening expenses (new hires, training, etc.)Real estate/property taxesSite inspection servicesSite safety and protection expensesSlotting chargesSurety bond premiumsSurveys Tenant bonuses/allowancesTesting/inspection feesUtility hook up expenses (sewer, water, etc.)Utility survey feesOther:Other:Other:

Insurance Coverage?

16

Worksh

op T3

Delay in Start-Up (DSU) Coverage

by Vincent Zegers, Marsh USA, Inc.

Issue: A coverage that always causes a problem if not underwritten properly is the delay in start-up (“DSU”) coverage when added as an extension to the builders risk policy.

First of all, the correct underwriting information required when DSU coverage is added to the builders risk policy should at least be the following:

1. What is the correct insured amount for this coverage, and how did the named insured arrive at that number in correlation with the period of indemnity?

Insurers should not offer any “blanket limits,” i.e., they should not accept just a sum insured without any explanation in their file. A pro forma is needed so all parties know that, if a claim is filed, what the amount is comprised of.

Important questions regarding this insured amount are:

a. Is this amount the total of debt services only or based on loss of revenue/loss of rent?

b. Are there other costs involved such as holdover agreements or “take-or-pay” agreements?

c. Are there any documents available to “back up” these numbers, such as “financial agreements” or “rental agreements”?

d. What is the period of indemnity related to the amount insured? Typically, it is 12 months or 18 months. That period of indemnity HAS to be included in the builders risk policy.

17

e. How did the parties arrive at that period of indemnity? What is the logic behind that period? The period of indemnity should be based on a certain catastrophic PML scenario. In other words, the question asked should be what the maximum potential period of delay could be caused by a certain peril and causing that delay. The two perils typically determining a catastrophic event triggering a delay could be either a fire (explosion) or a CAT-driven peril (wind/earthquake/flood). If that peril will occur, what is the potential length of the delay as a result thereof? The named insured has to provide details how long the delay could be usually looking at the lead time for the most exposed equipment along the critical path.

f. Is the total amount equally spread out over the 12 or 18 months, or are there “ramp-up periods” (staggered amounts) or seasonal fluctuations applicable?

g. Could the amount be a “lump sum amount” (bullet payment) based on a single event or several events when missed? This could apply, for instance, for a new stadium when certain games have been scheduled over a period of years, including the very important “opening game.”

h. Any delay claim filed will be handled on an “actual loss sustained” principle. Is the named insured aware of that? How can a claim be solved when the amounts to be paid out cannot be properly substantiated at the time of loss? (Examples are loss of gaming receipts for a casino or toll revenues for a highway.)

2. What is the correct trigger date for the DSU coverage extension?

a. Usually the trigger date for the DSU cover is the anticipated completion date, which would be the anticipated expiration date of the BR policy, but there are many situations where the trigger date can be set earlier or later!! Examples of an earlier trigger date can be certain phases if completed earlier or parts of buildings rented out/sold prior to completion date. When asked for a “prior occupancy” clause, you have to ask that question yourself automatically. A later trigger date could apply if, for instance, units are

18

Worksh

op T3

sold later or debt services are to be paid much later in time—or, in case of the stadium, when the first game is much later than the expiration date of the builders risk policy.

3. What is the correct time deductible for the DSU coverage?

a. Typically in the United States builders risk policies carry a time deductible on a “per occurrence” basis, but in the London markets you often see a time deductible based on a “term aggregate” basis. This is a very big difference so all parties should be working from the same understanding of what type of time deductible applies.

4. What is the correct way to issue the DSU coverage endorsement?

a. When an endorsement is issued, all the above criteria/definitions should be included in the endorsements reflecting exactly what all parties have agreed upon.

b. In addition the correct named insured should be used, which is the entity who has the financial interest in the delay cover (typically not the contractor).

c. Perhaps a loss payee should be added to the policy (e.g., mortgage holder/lenders).

5. What to do when a builders risk extension is required?

a. First of all, it’s important to find out what the reason is for the extension request. It can be driven by a loss covered under the BR policy or triggered by nonphysical damage delays.

19

b. All the questions raised above in this article should be asked again. Don’t just extend the builders risk policy and the DSU coverage, as well, assuming that the new requested anticipated completion date is the new DSU trigger date.

c. Is the lead time for critical equipment still the same? Is the critical path still the same? For sure, the “cushion” or “float” is gone when a project is delayed (if there was any to begin with).

d. Do you need to reset the time deductible?

20

Worksh

op T3

What Types of Losses Fall within the Scope of the Faulty Workmanship Exclusion?

by Tracy Saxe, Saxe Doernberger & Vita, P.C.

The term faulty workmanship is not defined within the builders risk policy. There is widedisagreement among the courts as to whether “faulty workmanship” concerns a flawed product, aflawed process of construction, or both.

• The faulty workmanship exclusion typically includes language similar to thefollowing:

We will not pay for loss or damage caused by or resulting from any of the following:

Faulty, inadequate or defective: . . .

(2) Design, specifications, workmanship, repair, construction, renovation, remodeling, grading, compaction . . .

of part or all of any property on or off an insured premises. . . .

However, any ensuing loss not excluded or excepted in this policy is covered.

• It is perhaps the most controversial and most relied upon builders risk policyexclusion, given that losses at a construction project are often due to human error(or fault) in some way, shape, or form.

• An expansive view of the term “faulty workmanship” can substantially diminish theprotection afforded under a builders risk policy. As one court has stated: “the ‘allrisks' peril expressly insured would become perilously close to a policy insuring norisk.” Dow Chem. Co. v. Royal Indem. Co., 635 F.2d 379, 387 (5th Cir.1981).

21

• Some courts consider the term “workmanship” to be ambiguous; does it concern the“process” of construction (accidental damage done to the product during theconstruction process) or the product, structure, itself (i.e., flawed quality of productworked upon)? Such courts have applied the interpretation most beneficial to theinsured:

Allstate v. Smith, 929 F.2d. 447 (9th Cir. 1991) (finding that a roofing contractor’s failure to place a protective tarp over a temporary hole in the roof, leading to rain damage, was a faulty process, thereby not excluded). E.g.:

M.A. Mortenson Co. v. Indemnity. Ins. Co. of N. Am., 1999 U.S. Dist. LEXIS 22641 (D. Minn. Dec. 23, 1999) (inadequate protective measures leading to storm damage were not found to be faulty workmanship because such measures did not involve a flawed product);

City of Barre v. New Hampshire Ins. Co., 396 A.2d 121 (VT 1978) (faulty workmanship exclusion did not apply to damage to building arches that were not sufficiently tethered, as the arches themselves were not faulty).

• Other courts have determined that the term is not ambiguous and thus conclude thatit applies to errors in both the construction process and the product. E.g.:

Schultz v. Erie Ins. Group, 754 N.E.2d 971, 977 (Ind. App. 2001). (Contractor’s negligence in leaving the insured personal property outside, causing it to get wet, involved faulty workmanship. Since “workmanship” denotes both “process” and “product,” an insurer could just as likely have both perils in mind when it drafts a policy’s list of exclusions.)

22

Worksh

op T3

Arnold v. Cincinnati Ins. Co., 688 N.W.2d 708 (Wis. App. 2004) (damage caused by the contractor’s negligent stripping and staining of the home’s cedar siding involved “faulty workmanship”).

Solutions

A. Assess whether the loss can reasonably be categorized as something other than faultyworkmanship and, if not, whether it can be categorized as either faulty product or faultyprocess (as opposed to both).

B. Assess whether there is a valid argument that the “ensuing loss” exception applies; i.e.whether the excluded faulty workmanship resulted in damage due to a covered cause ofloss. (For example, faulty constructed windows (excluded) allow water penetration(covered) which causes damage to the framing and sheetrock.)

C. Perform a choice of law analysis to determine which jurisdictions’ law potentially appliesand seek out a favorable jurisdiction.

23

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.1 of 11

To navigate between form fields, use TAB and SHIFT+TAB, only. Please do not use the arrow keys as it may fill in a form field you have not selected.

Insured

Insurer

Policy Period

Completed by

Date

Check All That Apply Recommendations/Comments

COVERED PROPERTY INTERESTS

Buildings or structures being erected

Fixtures, materials, supplies, machinery, and equipment that will become part of the completed structures

Temporary structures, scaffolding, construction forms, falsework

Fences

Signs

Office and utility trailers

Foundations, underground pipes, and other underground works

Site preparation and excavation works

Sidewalks and other paved surfaces

Trees, grass, shrubbery, plants, landscaping materials

Waterborne property

Airborne property

Contractors tools and equipment not destined to become part of the structure

Personal property of others for which the insured may be liable

24

Worksh

op T3

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.2 of 11

Check All That Apply Recommendations/Comments

Real and personal property to which alterations or additions are being made

Maps, plans, blueprints, specifications

Property used or installed in bridges, dams, tunnels

COVERED LOCATIONS

Construction site(s) scheduled in policy (list)

Construction sites reported in (monthly, quarterly) reports to insurer

Temporary off-site storage locations

Permanent off-site storage locations

Property in transit

Modes of transportation (describe)

Released bills of lading permitted

Policy territory (describe)

COVERED CAUSES OF LOSS

Named perils (list)

All risks

Dishonesty exclusion excepts carriers for hire

Design error exclusion excepts ensuing unexcluded loss

Faulty workmanship and materials exclusion excepts ensuing unexcluded loss

Testing

No testing exclusion

25

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.3 of 11

Check All That Apply Recommendations/Comments

Only “hot testing” is excluded (define hot testing)

Other (describe)

Hot testing coverage deductible $

Testing period of days

Boiler and machinery exclusions deleted (mechanical breakdown, electrical injury, boiler explosion)

Property damage due to power failure

Collapse coverage

Full collapse coverage (no collapse exclusion or exclusion excepts ensuing unexcluded loss)

Named perils collapse (no coverage for collapse due to design error)

Mold, other fungus, wet or dry rot, or bacteria

Full coverage for loss resulting from a covered cause

Excluded unless caused by fire or lightning

Limited coverage applies to mold loss from specified causes

$

Other (describe)

Earthquake

$ sublimit

Deductible: $

Flat dollar: $

% of values: %

26

Worksh

op T3

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.4 of 11

Check All That Apply Recommendations/Comments

% of loss: %

Coverage for other earth movement (subsidence, landslide)

Flood

$ sublimit

Deductible $

Coverage for other water damage (leakage, seepage, sewer backup)

$ sublimit

Building ordinance coverage (demolition, increased cost of construction, contingent liability from operation of building laws)

Asbestos materials

No exclusion or exclusion deleted

Excluded unless materials damaged by specified perils

Exclusion applies only to loss for which asbestos contractor is liable

Guarantee, warranty, or obligation

No exclusion or exclusion deleted

Exclusion applies only to obligation of manufacturers and suppliers (not contractors)

Architects and engineers professional services

No exclusion or exclusion deleted

TERRORISM PROVISIONS

No exclusion or limitation except TRIA’s $100 billion maximum

27

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.5 of 11

Check All That Apply Recommendations/Comments

Terrorism exclusion applies

Excludes loss from terrorism

Excludes loss from nuclear, chemical or biological terrorism; TRIA’s $100 billion maximum applies to covered losses

Exception for direct damage from ensuing fire, subject to TRIA’s $100 billion maximum (list states: )

Terrorism sublimit applies

$ annual aggregate: TRIA’s $100 billion maximum applies to covered losses

Exception for direct damage from ensuing fire, subject to TRIA’s $100 billion maximum (list states: )

Other terrorism provision (describe)

LIMITS OF INSURANCE

Scheduled construction site $(completed value)

Automatically adjusts as contract value increases (except delay coverage and policy sublimits)

Any one location of type of construction $

Scaffolding sublimit

Fences sublimit

Temporary structures $

Office trailers $

Property in transit—per conveyance $

Off-site storage locations—per location

28

Worksh

op T3

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.6 of 11

Check All That Apply Recommendations/Comments

$

Earthquake sublimit $

Earthquake annual aggregate $

Flood sublimit $

Flood annual aggregate $

Windstorm sublimit $ Named storms windstorm sublimit $ Other limits (describe and list)

DEDUCTIBLES

$ per occurrence

Earthquake

Flat dollar $ % of values ( %)

% of loss ( %)

Dollar minimum $ Windstorm

Flat dollar $ % of values ( %)

% of loss ( %)

Dollar minimum $ Windstorm deductible applies only to "named storms"

Flood

Flat dollar $ % of values ( %)

% of loss ( %)

29

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.7 of 11

Check All That Apply Recommendations/Comments

Dollar minimum $ Others (list)

COVERAGE DETAILS

Debris removal

Included within limits

Sublimit within limits applies $

Subject to separate additional limit $

Pollutant cleanup

$ sublimit

Valuation of property

Replacement cost value

Actual cash value

Coinsurance

%

No coinsurance

Full value reporting requirement

Policy type

Completed value

Reporting form

Monthly

Quarterly

Other (describe)

DELAY IN COMPLETION COVERAGE

Loss of income/rents $

30

Worksh

op T3

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.8 of 11

Check All That Apply Recommendations/Comments

Gross income less noncontinuing expenses

Net income plus continuing expenses

Rental income for signed rental agreements only

Offset for liquidated damages owed by contractor

Whether collectible or not

Soft costs

Additional interest expense $

Additional real estate taxes $

Additional promotional expense $

Additional design fees

Additional insurance costs

Additional consulting fees (accounting, legal, etc.)

Additional license/permit fees

Commissions on renegotiated leases

Additional overhead

Others (describe):

Expenses to reduce loss

Denial of access (civil authority)

weeks

Loss due to ordinance or laws covered

Loss due to damage to property in transit covered

Changing the anticipated date of completion (which starts period of

31

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.9 of 11

Check All That Apply Recommendations/Comments

indemnity) requires endorsement

Time limitation on the period of indemnity days/months

Coinsurance

No coinsurance provision

% coinsurance provision

Monthly limitation

$ each month

Deductible: hours/waiting period or $

Special deductible for peril(s): $

Maximum period of indemnity days

Additional exclusions: delay/soft costs

Interference by strikers/others

Breach or suspension of contract

Suspension, lapse, or cancellation of lease, license, contract, or order

Enforcement of laws governing construction

Enforcement of laws governing cleaning up of pollutants

Unavailability of funds to complete construction

Unavailability of subcontractors

Customs regulations

Correcting deficiencies in design/construction

Weather conditions

32

Worksh

op T3

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.10 of 11

Check All That Apply Recommendations/Comments

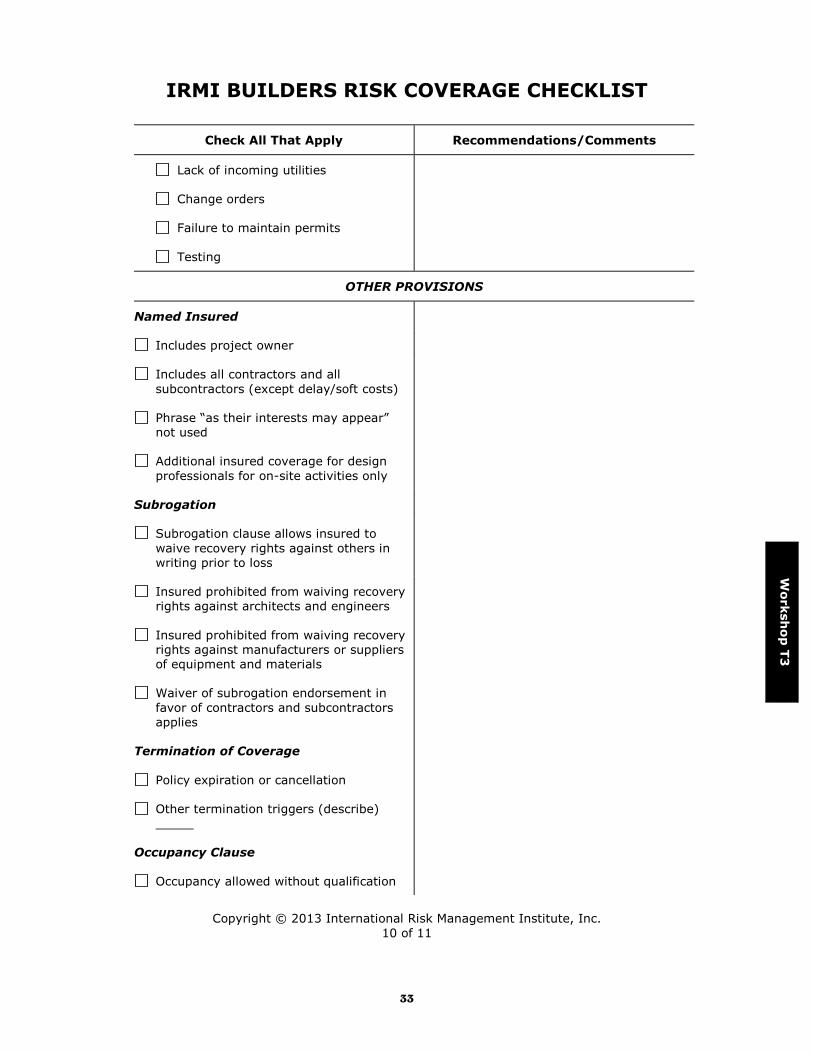

Lack of incoming utilities

Change orders

Failure to maintain permits

Testing

OTHER PROVISIONS

Named Insured

Includes project owner

Includes all contractors and all subcontractors (except delay/soft costs)

Phrase “as their interests may appear” not used

Additional insured coverage for design professionals for on-site activities only

Subrogation

Subrogation clause allows insured to waive recovery rights against others in writing prior to loss

Insured prohibited from waiving recovery rights against architects and engineers

Insured prohibited from waiving recovery rights against manufacturers or suppliers of equipment and materials

Waiver of subrogation endorsement in favor of contractors and subcontractors applies

Termination of Coverage

Policy expiration or cancellation

Other termination triggers (describe)

Occupancy Clause

Occupancy allowed without qualification

33

IRMI BUILDERS RISK COVERAGE CHECKLIST

Copyright © 2013 International Risk Management Institute, Inc.11 of 11

Check All That Apply Recommendations/Comments

Occupancy voids coverage

Other occupancy clause (describe)

Definition of occupancy (if occupancy voids or restricts coverage)

Cancellation

Notice of cancellation days

Notice of nonrenewal days

Notice of material change in coverage days

34