building quÉbec’s first diamond...

TRANSCRIPT

BUILDING QUÉBEC’S FIRST DIAMOND MINEAnnual General Meeting, October 19th 2015, Montreal

Matt Manson Patrick GodinPresident, CEO & Director COO & Director

2

Forward-Looking Information

This presentation contains "forward-looking information" within the meaning of Canadian securities legislation. This information and these statements, referred to herein as“forward-looking statements”, are made as of the date of this presentation and the Corporation does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by law. These forward-looking statements include, among others, statements with respect to our beliefs, plans, objectives, expectations,anticipations, estimates and intentions. Although management considers these assumptions to be reasonable based on information currently available to it, they may prove tobe incorrect.

Forward-looking statements relate to future events or future performance and reflect current expectations or beliefs regarding future events and include, but are not limited to,statements with respect to: (i) the amount of Mineral Resources and exploration targets; (ii) the amount of future production over any period; (iii) net present value and internalrates of return of the mining operation; (iv) assumptions relating to recovered grade, average ore recovery, internal dilution, mining dilution and other mining parameters set outin the 2011 Feasibility Study or the Optimization Study; (v) assumptions relating to gross revenues, operating cash flow and other revenue metrics set out in the 2011Feasibility Study or the Optimization Study; (vi) mine expansion potential and expected mine life; (vii) expected time frames for completion of permitting and regulatoryapprovals related to construction activities at the Renard Diamond Project; (viii) the expected time frames for the completion of the open pit and underground mine at theRenard Diamond Project; (ix) the expected time frames for the completion of construction, start of mining and commercial production at the Renard Diamond Project and thefinancial obligations or costs incurred by Stornoway in connection with such mine development; (x) future exploration plans; (xi) future market prices for rough diamonds; (xii)the economic benefits of using liquefied natural gas rather than diesel for power generation; (xiii) sources of and anticipated financing requirements; (xiv) the effectiveness,funding or availability, as the case may require, of the Stream, the Senior Secured Loan, the COF and the Equipment Facility and the use of proceeds therefrom; (xv) theCorporation’s expectations regarding receipt of the remaining deposits under the Stream and its ability to meet its delivery obligations thereunder; (xvi) the impact of theFinancing Transactions on the Corporation’s operations, infrastructure, opportunities, financial condition, access to capital and overall strategy; (xvii) the foreign exchange ratebetween the US dollar and the Canadian dollar; and (xviii) the availability of excess funding for the construction and operation of the Renard Diamond Project. Any statementsthat express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but notalways, using words or phrases such as “expects”, “anticipates”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “schedule” or variationsthereof or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similarexpressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are made based upon certain assumptions by Stornoway or its consultants and other important factors that, if untrue, could cause the actualresults, performances or achievements of Stornoway to be materially different from future results, performances or achievements expressed or implied by such statements.Such statements and information are based on numerous assumptions regarding present and future business prospects and strategies and the environment in whichStornoway will operate in the future, including the price of diamonds, anticipated costs and Stornoway’s ability to achieve its goals, anticipated financial performance, regulatorydevelopments, development plans, exploration, development and mining activities and commitments, and the foreign exchange rate between the US and Canadian dollars.Although management considers its assumptions on such matters to be reasonable based on information currently available to it, they may prove to be incorrect. Certainimportant assumptions by Stornoway or its consultants in making forward-looking statements include, but are not limited to: (i) required capital investment and estimatedworkforce requirements; (ii) estimates of net present value and internal rates of return; (iii) anticipated timelines for completion of construction, commencement of mineproduction and development of an open pit and underground mine at the Renard Diamond Project, which heavily depend, among other things, on adequate availability andperformance of skilled labour, engineering and construction personnel, performance of mining and construction equipment and timely delivery of components; (iv) anticipatedgeological formations; (v) market prices for rough diamonds and the potential impact on the Renard Diamond Project; (vi) the satisfaction or waiver of all conditions under eachof the Stream, the Senior Secured Loan, the COF and the Equipment Facility to allow the Corporation to draw on the funding available under those financing elements for thecompletion of the development and construction of the Renard Diamond Project; (vii) Stornoway’s interpretation of the geological drill data collected and its potential impact onstated Mineral Resources and mine life; (viii) future exploration plans and objectives; (ix) the receipt of the remaining deposits under the Stream and the Corporation’s ability tomeet its delivery obligations thereunder; and (x) the continued strength of the US dollar against the Canadian dollar. Additional risks are described in Stornoway's most recentlyfiled Annual Information Form, annual and interim MD&A, and other disclosure documents available under the Corporation’s profile at: www.sedar.com.

3

Forward-Looking Information (contd)

The RenardDiamond Project, September 16, 2015

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that estimates, forecasts, projections andother forward-looking statements will not be achieved or that assumptions do not reflect future experience. We caution readers not to place undue reliance on these forward-looking statements as a number of important risk factors could cause the actual outcomes to differ materially from the beliefs, plans, objectives, expectations, anticipations,estimates, assumptions and intentions expressed in such forward-looking statements. These risk factors may be generally stated as the risk that the assumptions andestimates expressed above do not occur, including the assumption in many forward-looking statements that other forward-looking statements will be correct. Stornowayinvites the reader to take note of the risk and uncertainties set out in the most recently filed Annual Information Form, annual and interim MD&A and other disclosuredocuments available under the Corporation’s profile at: www.sedar.com and cautions the reader that the list of risk and uncertainties set out in these disclosure documents ofthe Corporation and that may affect future results is not exhaustive, and new, unforeseeable risks may arise from time to time.

Readers are also referred to the technical reports dated as of February 28th, 2013 entitled “The Renard Diamond Project, Québec, Canada, Feasibility Study Update, NI 43-101 Technical Report, February 28, 2013” in respect of the January 2013 Optimization Study, and dated October 14, 2015 entitled “2015 Mineral Resource Update, for theRenard Diamond Project, Québec, Canada, NI 43-101 Technical Report”. Disclosure of a scientific or technical nature in this presentation was prepared under the supervisionof Patrick Godin, P. Eng (Québec), Chief Operating Officer and Robin Hopkins, P. Geol. (NT/NU), Vice President, Exploration, both “qualified persons” under NationalInstrument (NI) 43-101 - Standards of Disclosure for Mineral Projects. Ms. Darrell Farrow, PrSciNat, P. Geo. (BC), Ordre des géologue du Québec (Special Authorization #332) of Geostrat Consulting Services Inc. is the independent qualified person responsible for preparation of the mineral resource estimate for the Renard Diamond Project.

4

Stornoway Diamond Corporation TSX:SWY

On Budget, On ScheduleConstruction 47.4% complete compared to 42.9% planned by end September 2015.

Forecast cost to complete within C$811m budget.Plant Commissioning 2H 2016. Commercial Production 2Q 2017.

Building the Renard Diamond Project, Québec’s First Diamond Mine

Site Overview Sep 16, 2015The RenardDiamond Project, September 16, 2015

5

From the 2014 AGM…

43

Québec’s First Diamond Mine is Ready to Build

Project Green-lighted: Authorizations Issued

Community Agreements in Place

Stornoway Operating Team in Place

Access Road Opened

Resource Growing

Project Design Fully Optimized

Favourable Cost Environment

Stornoway is Fully Focused on the Timely Completion of Final Project

Financing

50Stornoway Diamond Corporation TSX:SWYOur Priorities

www.stornowaydiamonds.com

Solid project execution

Budget, schedule and operating excellence

Disciplined management of cash and expenditures

Strong balance sheet

Delivering on project’s strong margin and cash flow potential

Then…

Retain exposure to pipeline exploration assets through JVs

With successful construction and commissioning behind us, look to the future

6Good TimingThe Renard Project Financing, Closed July 8th, 2014

Type Amount (% of Total) Description

Common Equity C$374M (40%)• C$132M marketed public equity offering of subscription receipts• C$242M private placement to Orion (US$110M), RQ (C$100M) and Caisse (C$22M)

Diamond Stream US$250M (29%) • 20% diamond stream (Orion 16%, Caisse 4%) with ~US$56/ct(1) ongoing payment

Convertible Debentures US$81M (9%) • Provided by Orion; 7 year, 6.25% coupon, 35% conversion premium to equity issue price

Senior Debt C$120M (11%) • Provided by IQ; 7 year amortizing payment, Fixed (QC Bond)+5.75% or Prime +4.75%

Equipment Financing US$35M (4%) • Provided by Caterpillar

Cost Overrun Facility C$48M (5%) • C$20M provided by IQ (same terms as senior debt)• C$28M provided by Caisse (unsecured, 7 year term, 10% coupon)

Total C$946M (100%)

Assumes US$1.00 = C$1.101. Includes reimbursement of marketing expenses

Counter-Party Amount (% of Total)

Orion Mine Finance C$367M (39%)

Investissement Québec/ Ressources Québec C$240M (25%)

Caisse de dépôt et placement du Québec C$105M (11%)

Caterpillar Financial C$39M (4%)

Public C$195M (21%)

Total C$946M (100%)

In April 2015 Blackstone Tactical Opportunities, an affiliate of Blackstone (NYSE-BX), acquired a c.5% equity position in Stornoway and a minority 4% ownership interest in the Renarddiamond stream by way of a secondary market transaction with Orion Mine Finance (“Orion”).

The first two of three tranches of the Renard Diamond stream funded in March and September 2015, on schedule. The third and final tranche is scheduled for March 2016.

Subsequent to Transaction Closing

7Good Timing: Sources and Uses of Funds to July 31, 2015On Current C$:US$ Exchange Rates, Unaudited unless noted

(all amounts in millions of C$) Assumed

Actual use of Proceeds to July 31,

2015

Renard Diamond Project

Capital Expenditures 811 311

Route 167 Extension (1) 70 70

Financing Costs, Interest during Construction 58 24

Mine Closure Guarantee 16 2

Pre-production Net Revenue (26) -

Total Project Costs 929 407

General Corporate Purposes

Equity fees and transaction costs 18 29

General working capital, administrative and salary expenses 14 6

Total Uses 961 442

Costs

Notes1. The total amount borrowed pursuant to the Renard Mine Road loan was $77 million, of which $70 million was used for construction of the Renard Mine Road and $7 million was used

for civil works related to the airstrip. Costs related to the airstrip were included in the $811 million capital expenditures line in the table above.2. On September 30, 2015, Stornoway received the second tranche of US$80m of stream funding, which was subsequently converted to C$ at an exchange rate of $1.336, representing

a cash gain of C$18.9 million compared to the July 2014 funding plan, which assumed a C$:US$ exchange rate of $1.10. 3. Cost Overrun Facility includes the $20 million Senior Loan Facility, Tranche B and the $28 million Cost Overrun Facility with the CDPQ4. Assuming a C$:US$ conversion rate of C$1.255. This forecast assumes a project cost of $811 million (which includes assumed levels of escalation and contingencies), the satisfaction of all covenants and conditions precedent for

future funding, and a CAD$:US$ exchange rate of $1.25 for unfunded US dollar denominated financing commitments.

(all amounts in millions of C$)

Sources of Funds

Stream Deposits not yet received(2) 213

Senior Loan Facility, Tranche A 100

Cost Overrun Facility(3) 48

Equipment Financing Facility(4) 17

Undrawn Sources of Funds

As of July 31, 2015, Stornoway forecasts excessfinancing capacity available to complete the projectof approximately $101 million comprised of $53million of cash, receivables and expected minetax credits and $48 million of undrawn costoverrun facilities(5).

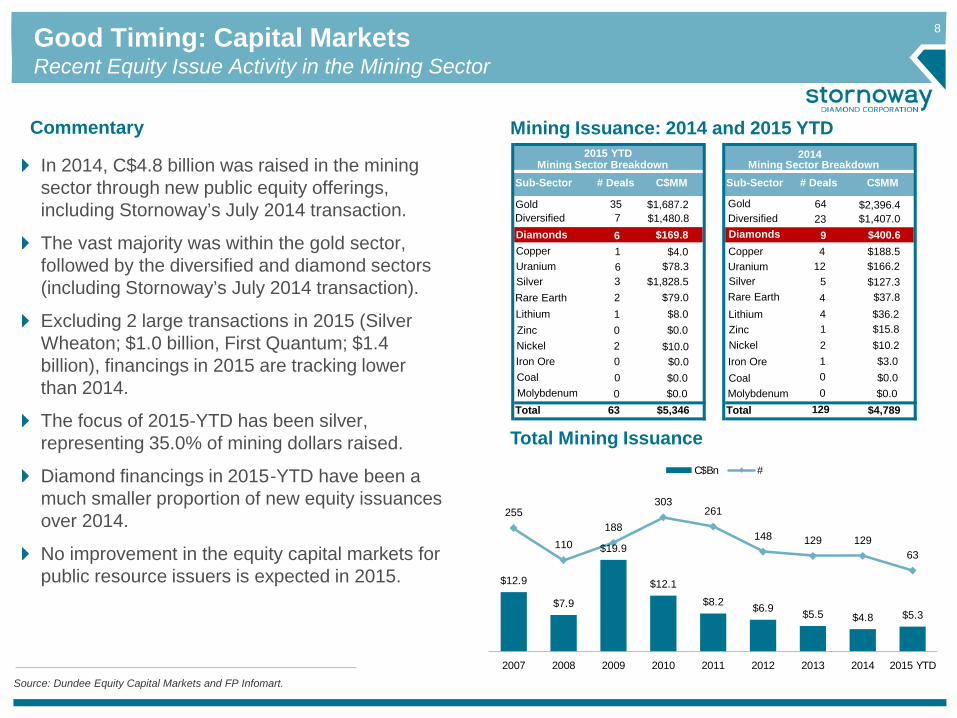

8Good Timing: Capital MarketsRecent Equity Issue Activity in the Mining Sector

Total Mining Issuance

Mining Issuance: 2014 and 2015 YTD

Sub-Sector # Deals C$MM

Gold 35 $1,687.2

Uranium 6 $78.3Silver 3 $1,828.5Rare Earth 2 $79.0

Zinc 0 $0.0

Coal 0 $0.0Molybdenum 0 $0.0

Nickel 2 $10.0

Total 63 $5,346

2015 YTDMining Sector Breakdown

Diamonds 6 $169.8Diversified 7 $1,480.8

Lithium 1 $8.0

Iron Ore 0 $0.0

Sub-Sector # Deals C$MM

Gold 64 $2,396.4Diversified 23 $1,407.0

Uranium 12 $166.2Copper 4 $188.5

Lithium1 $15.8

Silver 5 $127.3Rare Earth

4$37.8

Coal1

$0.0Molybdenum

0$0.0

Nickel

0

$10.2

Total 129 $4,789

2014Mining Sector Breakdown

Zinc

4$36.2

Iron Ore2

$3.0

Diamonds 9 $400.6

In 2014, C$4.8 billion was raised in the mining sector through new public equity offerings, including Stornoway’s July 2014 transaction.

The vast majority was within the gold sector, followed by the diversified and diamond sectors (including Stornoway’s July 2014 transaction).

Excluding 2 large transactions in 2015 (Silver Wheaton; $1.0 billion, First Quantum; $1.4 billion), financings in 2015 are tracking lower than 2014.

The focus of 2015-YTD has been silver, representing 35.0% of mining dollars raised.

Diamond financings in 2015-YTD have been a much smaller proportion of new equity issuances over 2014.

No improvement in the equity capital markets for public resource issuers is expected in 2015.

Commentary

$12.9

$7.9

$19.9

$12.1

$8.2 $6.9 $5.5 $4.8 $5.3

255

110

188

303261

148 129 12963

2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD

C$Bn #

Copper 1 $4.0

Source: Dundee Equity Capital Markets and FP Infomart.

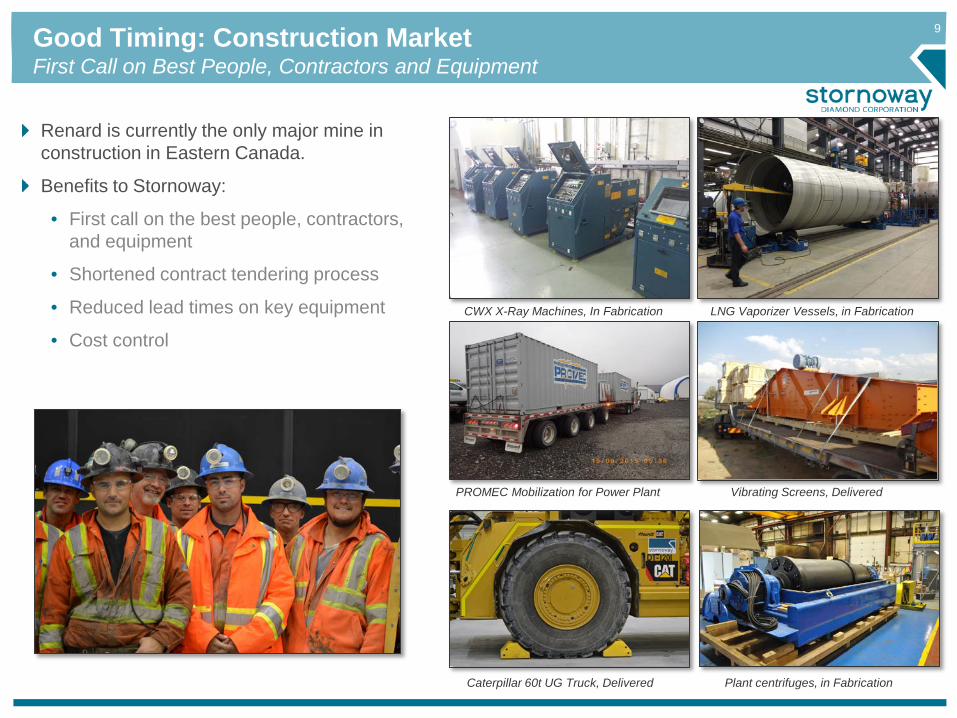

9Good Timing: Construction MarketFirst Call on Best People, Contractors and Equipment

CWX X-Ray Machines, In Fabrication LNG Vaporizer Vessels, in Fabrication

PROMEC Mobilization for Power Plant Vibrating Screens, Delivered

Caterpillar 60t UG Truck, Delivered Plant centrifuges, in Fabrication

Renard is currently the only major mine in construction in Eastern Canada.

Benefits to Stornoway:

• First call on the best people, contractors, and equipment

• Shortened contract tendering process

• Reduced lead times on key equipment

• Cost control

10Good Timing: Diamond Market and Canadian DollarRough Diamond Pricing 2009-2015

May 2011 FS Diamond Valuation

50

100

150

200

250

300

350

1-Jan-09 1-Jan-10 1-Jan-11 1-Jan-12 1-Jan-13 1-Jan-14 1-Jan-15

Inde

x to

200

9=10

0

WWW Rough Index, Renard Model Price Growth, Real Terms

CAD

USD

FS 2.5% Price Model (Nominal, adjusted

for CPI) with +/- 10% Sensitivity

WWW Rough Diamond Price Index

11Publicly Listed Diamond Producers, Developers and ExplorersConsensus Analyst Views on Value

Ticker Price(16/10/15)

Shares O/S

(mm)

MarketCap

($mm)NAV/sh(1) Current

P/NAV(1) Target (1) % Return to Target

AnnualDividend

Diamond ProducersALROSA ALRS:M ₽56.06 7,365.0 ₽412,880 (n/a) (n/a) ₽77.17 40% ₽1.47/sh

Dominion Diamonds DDC:T $13.95 85.1 $1,187.6 $29.88 0.5x $24.80 81% US$0.40/sh

Gem GEMD:LN £1.08 138.3 £149.7 £2.16 0.5x £1.84 73% US$0.05/sh

Lucara LUC:T $1.73 379.6 $656.6 $2.48 0.7x $2.50 47% $0.04/sh

Petra PDL:LN £0.94 512.1 £478.8 £1.85 0.5x £1.78 93% £0.02/sh

Diamond DevelopersFirestone FDI:LN £0.22 309.0 £67.6 £0.51 0.4x £0.45 104% (n/a)

Mountain Province MPV:T $4.16 159.7 $664.2 $7.15 0.6x $6.69 61% (n/a)

Stornoway SWY:T $0.74 732.3 $541.9 $1.47 0.5x $1.21 64% (n/a)

Diamond ExplorersKennady Diamonds KDI:LN $2.95 46.3 $136.4 (n/a) (n/a) (n/a) (n/a) (n/a)

North Arrow Minerals NAR:V $0.25 54.0 $13.5 (n/a) (n/a) (n/a) (n/a) (n/a)

Peregrine Diamonds PGD:T $0.175 282.7 $49.5 (n/a) (n/a) (n/a) (n/a) (n/a)

Shore Gold SGF:T $0.17 248.7 $42.3 (n/a) (n/a) (n/a) (n/a) (n/a)

Notes:

1. Bloomberg and Thomson One Analyst Consensus

All Currencies in C$ unless specified

12

ShareholdingShare Price (TSX-SWY):Oct 16, 2015 C$ $0.74

52 week High-Low C$ $0.46–$0.85

Average Daily Volume:Last 12 Months 374,593

Market Capitalization: C$ 542 million

Total Shares Outstanding: 732 million

Total Options & Warrants Outstanding:(28.2m Options $0.59-$5.36; 123.8m warrants $0.90-$1.21)

152 million

Consolidated Cash1,2: (as of July 31, 2015) C$ 270 million

Consolidated Debt1: (as of July 31, 2015) C$ 220 million

Undrawn Financing Commitments2,3: (Subject to Financing Agreement CPs) C$ 352 million

Balance Sheet

Balance Sheet and Capital Structure

Notes1. Unaudited2. Does not include funds received from second tranche of the Stream on

September 30th

3. Assuming a C$:US$ conversion rate of C$1.10

Investissement Québec 28.6% 22.7%

Orion Mine Finance 19.5% 17.5%

CDPQ 6.1% 6.2%

Float 45.8% 53.6%

DilutedBasic

-100.0%

-50.0%

0.0%

50.0%

100.0%

150.0%

One Year Equity Performance of Selected Diamond Companies

SWY DDC GEMD LUCPDL FDI MPV KDINAR PGD SGF

1313

Renard Mineral Resources and Exploration Upside

800m

900m

1100m

1200m

1000m

Renard Mine Plan and Key Operating AssumptionsA Combined Open Pit and Underground Operation

Notes1. Key Assumptions:C$1=US$1, Oil US$95/barrel, 2.5% real terms diamond

price growth, 82.9% ore recovery, 23.8% mining and internal dilution, 0cpht dilution grade.

2. Expressed in May 2011 terms. Average price US$190/carat in March 2014 terms.

3. Expressed in October 2012 terms, as adjusted in October 2013 LNG FS. Includes C$754m of costs and contingencies and C$57m of escalation allowance.

4. Expressed in October 2012 terms. Operating costs C$54/tonne in October 2013 LNG FS terms. Excludes capitalized preproduction costs.

5. Before stream

Reserve and Resource categories are compliant with the "CIM Definition Standards on Mineral Resources and Reserves". Mineral resources that are not mineral reserves do not have demonstrated economic viability. The potential quantity and grade of any Exploration Target is conceptual in nature, and it is uncertain if further exploration will result in the target being delineated as a mineral resource.

Reserve Based Mine Plan1

(Jan 2013 FS Optimization and October 2013 LNG Option FS)

Mine Life 11 yearsMineral Reserve 17.9 mcaratsAve. Diamond Price2 $180/caratProduction Rate 2.2 mtonnes/yrAve. Diamond Production 1.6 mcarats/yrGross Revenue (C$M)2 $4,268Initial Capital Costs3 $811mOperating Cost4 $58/t ($76/carat)Operating Margin5 67%Payback 4.8 years

0m

100m

200m

400m

600m

700m

500m

300m

Renard 4

Renard 9

Renard 65Renard 2 Renard 3

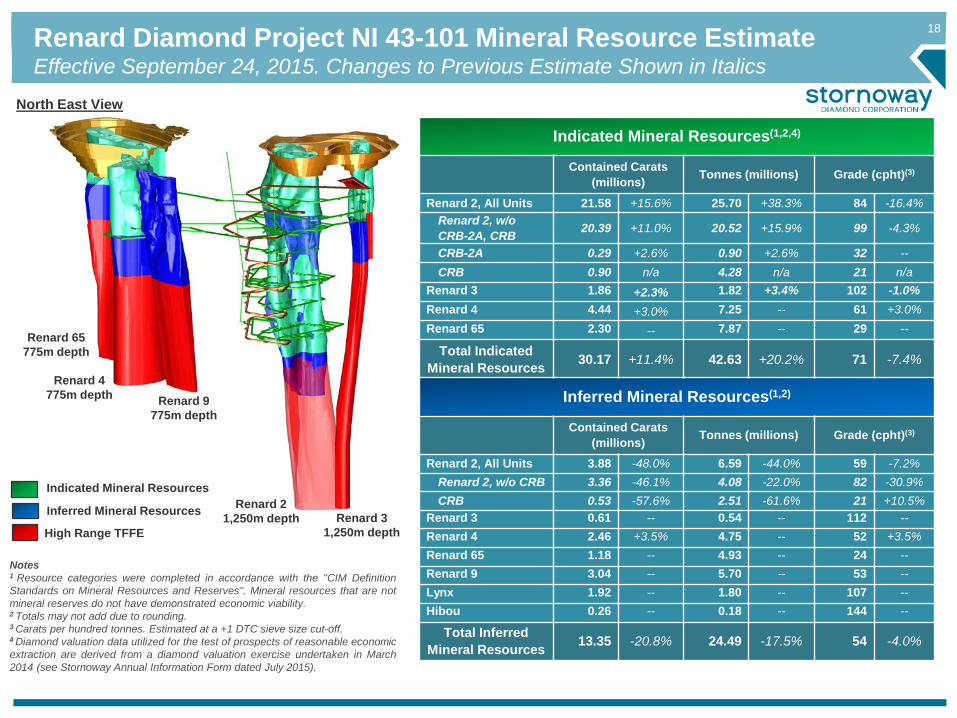

Mineral Resource Estimate Effective September 24, 2015 (NI 43-101)

13 mcarats Inferred Mineral Resources33 to 71 mcarats TFFE

30 mcarats Indicated Mineral Resources

An Updated Renard Mine Plan, scheduled for Q22016, is expected to include additional mineproduction from new Indicated Mineral Resourcesin Renard 2 and Renard 65, deepening of theRenard 2-3 open pit, extension of the undergroundmine infrastructure to 700m, and an optimizedschedule for plant commissioning and ramp-up.

14

15Renard 2 Mineral Resource ClassificationEffective September 24, 2015. Changes to Previous Estimate Shown in Italics

Pipe shape at surface (1.89ha)

High TFFE at 1,250m (1.38ha)

Notes1 Reserve and Resource categories were completed in accordance with the "CIM Definition Standardson Mineral Resources and Reserves". Mineral resources that are not mineral reserves do not havedemonstrated economic viability.2 Totals may not add due to rounding.3 Carats per hundred tonnes. Estimated at a +1 DTC sieve size cut-off.4 Diamond valuation data utilized for the test of prospects of reasonable economic extraction arederived from a diamond valuation exercise undertaken in March 2014 (see Stornoway AnnualInformation Form dated July 2015).

0m

700m

850m

1250m

INDICATED

INFERRED

TFFE

600m: Base of Previous Indicated Mineral Resources

Depth Below

SurfaceKimberlite

outlineat surface (0.75ha)

Low TFFE at 1,250m (0.62ha)

Base of New Indicated

Resources (1.55ha)

Indicated Mineral Resources(1,2,4)

Contained Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 21.58 +15.6% 25.70 +38.3% 84 -16.4%Renard 2, w/o CRB-2A, CRB 20.39 +11.0% 20.52 +15.9% 99 -4.3%

CRB-2A 0.29 +2.6% 0.90 +2.6% 32 --CRB 0.90 n/a 4.28 n/a 21 n/a

Inferred Mineral Resources(1,2)

Contained Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 3.88 -48.0% 6.59 -44.0% 59 -7.2%Renard 2, w/o CRB 3.36 -46.1% 4.08 -22.0% 82 -30.9%CRB 0.53 -57.6% 2.51 -61.6% 21 +10.5%

Target for Further Exploration(1)

Contained Carats (millions)

Tonnes (millions) Grade (cpht)(2)

Renard 2, All Units 3.7 to 15.5 6.1 to 15.5 60 to 100

North View Renard 2 NI 43-101 Mineral Resource Estimate

Renard 2 Targets for Further Exploration

Notes1 Represents potential upside that can be reasonably assumed given the nature and grade of materialwithin the current 2015 Mineral Resource. The potential quantity and grade of any Exploration Target isconceptual in nature, there has been insufficient information to define a mineral resource, and it isuncertain if further exploration will result in the target being delineated as a mineral resource.2 Carats per hundred tonnes. Potential at a +1 DTC sieve size cut-off.

Pinch in model in area lacking drill

coverage

16Renard 2 Geological Model and Unit GradesEffective September 24, 2015. Changes to Previous Estimate Shown in Italics

Within the Indicated Mineral Resources

Average Grade (cpht)(1)

Average Dilution (%)(2)

Kimb 2a (“Blue”) 76 +3.0% 52 -0.9%Kimb 2b (“Brown”) 145 +1.0% 30 -0.9%Kimb 2c (HK)3 229 +0.5% 12 -3.1%CRB-2a 32 -- 93 --CRB 21 n/a 96 n/a

Within the Inferred Mineral Resources

Average Grade (cpht)(1)

Average Dilution (%)(2)

Kimb 2a (“Blue”) 67 -2.4% 65 +9.2%Kimb 2b (“Brown”) 145 +0.3% 30 +1.5%Kimb 2c (HK)3 229 +0.5% 12 -3.1%CRB 21 +10.5% 96 --

Notes1 Carats per hundred tonnes. Estimated at a +1 DTC sieve size cut-off.2 Represents the average amount of non-diamond bearing country rockestimated within each geological unit.3 The Kimb 2c (Hypabyssal Kimberlite, or “HK”) unit is a constituent componentof each of the Kimb2a, Kimb2b, CRB and CRB-2a units.

Renard 2 Average Mineral Resource Grades, by Geological Unit

Kimb2b (“Brown”)

Kimb2a (“Blue”) CRB CRB-2a Kimb2c (HK)

West View

Contact

Pinch in model in area lacking drill coverage

0m

700m

850m

1250m

INDICATED

INFERRED

TFFE

600m: Base of Previous Indicated Mineral Resources

Depth Below

Surface

North View

Photographs of geological units from

the 2007 Renardunderground bulk

sample program

17Renard 2 Geological Model and Renard 2-Renard 3 ConvergenceEffective September 24, 2015

Pipe shape at surface (1.89ha)

Kimberlite outlineat surface (0.75ha)

Kimb2b (“Brown”)

Kimb2a (“Blue”)

CRBCRB-2a

Surface View, Looking Down

Surface View, Looking Down

0m

700m

850m

1250m

R2 INDICATED

R2 INFERRED

R2 TFFE

Depth Below

Surface

R3 INDICATED

R3 INFERRED

R3 TFFE

North East View

Resource categories were completed in accordance with the "CIM Definition Standardson Mineral Resources and Reserves". Mineral resources that are not mineral reserves donot have demonstrated economic viability. The potential quantity and grade of anyExploration Target is conceptual in nature, there has been insufficient information todefine a mineral resource and it is uncertain if further exploration will result in the targetbeing delineated as a mineral resource.

Renard 2 Renard 3

Renard 2

Renard 3

126.6m R3 intersection in DDH R2-81J (in red) starting 942.2m downhole: 47m true width.

R3 TFFE: >500m potential between drill intersections

18Renard Diamond Project NI 43-101 Mineral Resource EstimateEffective September 24, 2015. Changes to Previous Estimate Shown in Italics

Notes1 Resource categories were completed in accordance with the "CIM DefinitionStandards on Mineral Resources and Reserves". Mineral resources that are notmineral reserves do not have demonstrated economic viability.2 Totals may not add due to rounding.3 Carats per hundred tonnes. Estimated at a +1 DTC sieve size cut-off.4 Diamond valuation data utilized for the test of prospects of reasonable economicextraction are derived from a diamond valuation exercise undertaken in March2014 (see Stornoway Annual Information Form dated July 2015).

Indicated Mineral Resources(1,2,4)

Contained Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 21.58 +15.6% 25.70 +38.3% 84 -16.4%Renard 2, w/o CRB-2A, CRB 20.39 +11.0% 20.52 +15.9% 99 -4.3%

CRB-2A 0.29 +2.6% 0.90 +2.6% 32 --CRB 0.90 n/a 4.28 n/a 21 n/a

Renard 3 1.86 +2.3% 1.82 +3.4% 102 -1.0%Renard 4 4.44 +3.0% 7.25 -- 61 +3.0%Renard 65 2.30 -- 7.87 -- 29 --

Total Indicated Mineral Resources 30.17 +11.4% 42.63 +20.2% 71 -7.4%

Inferred Mineral Resources(1,2)

Contained Carats (millions) Tonnes (millions) Grade (cpht)(3)

Renard 2, All Units 3.88 -48.0% 6.59 -44.0% 59 -7.2%Renard 2, w/o CRB 3.36 -46.1% 4.08 -22.0% 82 -30.9%CRB 0.53 -57.6% 2.51 -61.6% 21 +10.5%

Renard 3 0.61 -- 0.54 -- 112 --Renard 4 2.46 +3.5% 4.75 -- 52 +3.5%Renard 65 1.18 -- 4.93 -- 24 --Renard 9 3.04 -- 5.70 -- 53 --Lynx 1.92 -- 1.80 -- 107 --Hibou 0.26 -- 0.18 -- 144 --

Total Inferred Mineral Resources 13.35 -20.8% 24.49 -17.5% 54 -4.0%

Inferred Mineral Resources

Indicated Mineral Resources

High Range TFFE

Renard 65775m depth

Renard 4775m depth Renard 9

775m depth

Renard 21,250m depth Renard 3

1,250m depth

North East View

19Renard Diamond Project Exploration PotentialEffective September 24, 2015. Changes to Previous Potential Shown in Italics

Notes1 Target for Further Exploration: representspotential upside that can be reasonablyassumed given the nature and grade of materialwithin the current 2015 Mineral Resource. TheRenard 2 shape has been projected 250mbelow the deepest kimberlite intersection at1,000m depth. Tonnage and grade ranges arenot directly applicable to potential totalcarats.The potential quantity and grade of anyExploration Target is conceptual in nature, therehas been insufficient information to define amineral resource, and it is uncertain if furtherexploration will result in the target beingdelineated as a mineral resource.2 Carats per hundred tonnes. Potential at a +1DTC sieve size cut-off.

NotesResource categories were completed in accordance with the "CIM DefinitionStandards on Mineral Resources and Reserves". Mineral resources that are notmineral reserves do not have demonstrated economic viability.

Area indicated in yellow represents a gap in drill coverage that may representadditional exploration potential outside of the current Mineral Resource Estimateand not included in the current Targets for Further Exploration.

Renard 65775m depth

Renard 4775m depth Renard 9

775m depth

Renard 21,250m depth Renard 3

1,250m depth

Inferred Mineral Resources

Indicated Mineral Resources

High Range TFFE

North East View

R10 R7 R1 R65

R4 R9

R2R3

Targets for Further Exploration(1)

Contained Carats (millions)

Tonnes (millions) Grade (cpht)(2)

Renard 1 1.7 to 3.9 8.6 to 13.0 20 to 30

Renard 2, All Units 3.7 to 15.5 6.1 to 15.5 60 to 100

Renard 3 3.6 to 6.3 3.4 to 3.8 105 to 168

Renard 4 5.6 to 11.8 11.1 to 15.4 50 to 77

Renard 65 7.3 to 13.5 29.0 to 40.9 25 to 33

Renard 7 1.9 to 3.8 6.3 to 9.4 30 to 40

Renard 9 2.0 to 4.3 3.9 to 6.3 52 to 68

Renard 10 0.7 to 2.1 1.2 to 1.7 60 to 120

Lynx 3.0 to 3.8 3.1 to 3.2 96 to 120

Hibou 3.6 to 6.1 3.5 to 4.0 104 to 151

Total TFFE 33.0+28% to 71.1

+40%76.2

+49% to 113.2+51%

2020

Construction Report (Patrick Godin)

21

Environment, Health, Safety, and Stornoway’sTeam

“Courage to Care”

On Personal SafetyOn the Safety of our Colleagues

On the EnvironmentWith our Inter-cultural workforce

Lost Time Injury RateSWY employees: 0.0 (43,453 hours worked to end of Sept.)

Contractors: 0.7 (79,149 hours worked to end of Sept.)

Renard Total: 0.44

Québec Construction Industry: 2.2

Québec Mining Industry: 0.8

22Approach to Mine ConstructionChevrolet/Cadillac

Access Road

Airport Terminal

Accommodation Complex

Mine Dry and Office

Process Plant

Power Plant

Airport Landing Strip

Water Management and Treatment Facility

Maintenance Facility

Mining Equipment

“Chevrolet” “Cadillac”

23

Construction Sequence

2H 2H 2H 2H1H 1H 1H1H

2013 2014 2015 2016

All in parallel with open pit and underground mining activities

R2-R3

R65

Camp

ProcessPlant

Portal

1. Construct Access:

Road and Airport

3. Close Buildings of Major

Facilities (“Outside-In”)

2. Build Camp and

Mine Office/Dry

4. Equip Major Facilities

5. Commence Operations

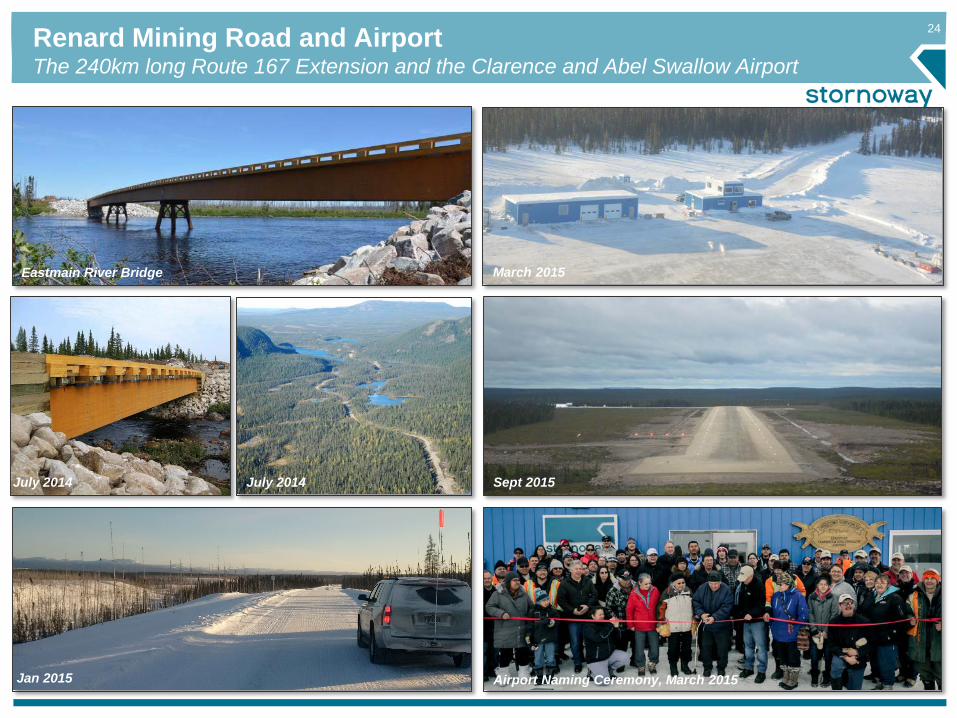

24Renard Mining Road and AirportThe 240km long Route 167 Extension and the Clarence and Abel Swallow Airport

Eastmain River Bridge March 2015

Sept 2015July 2014

Jan 2015 Airport Naming Ceremony, March 2015

July 2014

25

Camp and Mine Dry

Sept 2014 Oct 2014 Jan 2015: Occupation

Sept 2015 June 2015

26Maintenance FacilityCompleted Approximately 6 Months Ahead of Schedule

July 2015April 2015

Inauguration Ceremony, September 24, 2015 Oct 2015

27

Primary Crusher and LNG Power Plant

Sept 2015Oct 2015

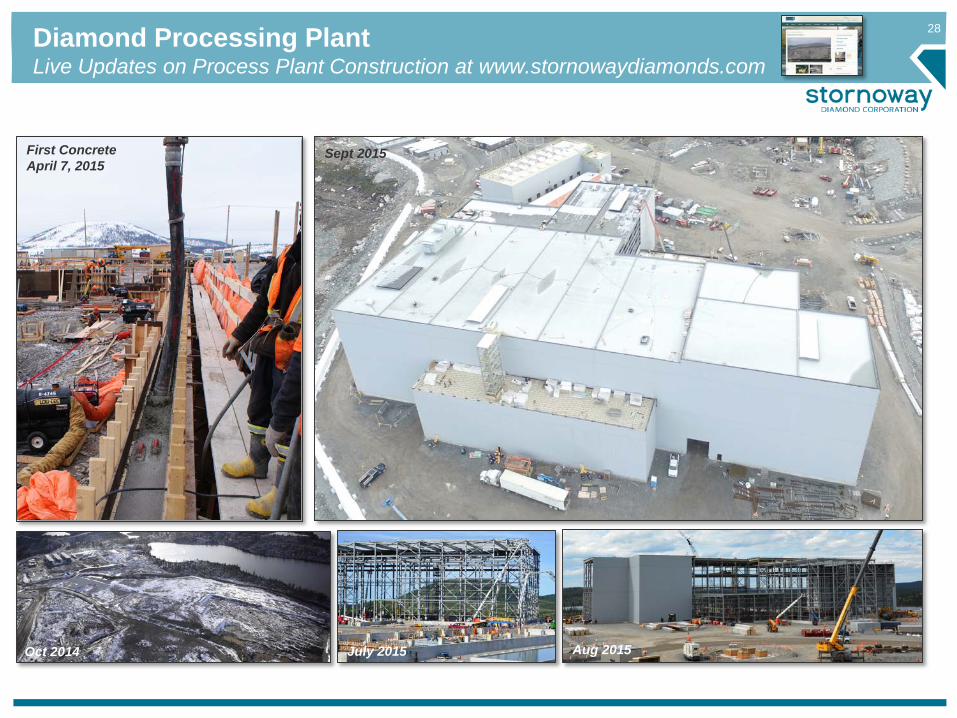

28Diamond Processing PlantLive Updates on Process Plant Construction at www.stornowaydiamonds.com

Oct 2014

Sept 2015First ConcreteApril 7, 2015

Aug 2015July 2015

29Open Pit MiningRenard 2 – Renard 3 Pit Pre-stripping Commenced March 2015

R2-R3 Pre-Strip, March 5, 2015

Open Pit Mining Team, March 5, 2015

R2-R3

R65

Portal

R2-R3 Pit, May 23, 2015

Decline Ventilation, May 10, 2015

Mining Progress as of July 31 20151,842,582 tonnes extracted from R2/R3 and vs plan of

2,042,680 (93%)

R2-R3 Pit August 2015

30

August 2015

Sept 2015

R2-R3

R65

Portal

Decline Progressas of July 31, 2015

486m against plan of 504m (96%)

Underground MiningPortal Development December 2014, Ramp Development Commenced March 2015

31

The Mecheshoo Agreement, March 2012

Renard’s Social LicenceWorking with Stakeholders

The Declaration of Partnership, July 2012

Environmental Exchange Group, 2011

The design of the project, and the December 2011 Environmental and Social Impact Assessment, was developed in conjunction with an environmental Exchange Group that met during the course of 2011 in Mistissini.

The Renard Project has been designed to minimize impact on local water quality and fish habitat, the principal concern of the Crees. The project has been “built to close”, and reclamation liabilities have been bonded 100% with the MERN

In July 2012 Stornoway concluded a “Declaration of Partnership” with the communities of Chapais and Chibougamau.

The Declaration of Partnership provides a framework to address issues of mutual interest such as communication, employment and economic diversification.

In March 2012 Stornoway concluded the “Mecheshoo Agreement” with the Cree Nation of Mistissini and the Grand Council of the Crees (EI).

The “Mecheshoo Agreement” provides for employment and business opportunities, the Crees, fosters cultural, environmental and social protection,

and provides for the Crees’ participation in the project’s long term financial success.

32

Main Contractors at Mine Site in 2014-2015

Construction Talbon Matoush-Grimard

Manseau & Perron inc MY Surveying

Sakhiikan Consortium Kesi Construction

Eskan Company RCM Habitation Modulaire

Jos Ste-Croix Swallow-Fournier inc

Kiskinshiish Camp Services Tessier Ltée

Communications Telesignal SPI Santé/Sécurité

Structures GB Ltée Prevost et Frères

H2O Innovation Nordic Structures Bois

Anixter Canada Recyclage Ungava

Plomberie Chibougamau Sanivac Réseau

Blasteck International Barette et fils

Convoyeur Continental ASDR Environnement

Installations AC Washeyaabiin Const.

Industrie Fournier Biron

Yves Lacombe Pétrole MJ

Roche Ltée Mabarex

Equ. Pétrolier Lac St-Jean Hewitt

Construction Proco Corner Cast

Air Creebec Revetement RHR

Petronor Groupe Industriel Premium

Dyno Nobel Canada Mansour Mining Techno.

Groupe Robert PAR Tanguay (WEC)

Invoiced Expenses from Québec ($245M)

CHIB-CHAP-MIST

MONTREAL

BEAUCE

ABITIBI

SAGUENAY-LAC ST-JEAN

GASP-BSL-COTE-NORD

MAURICIE-CENTRE-SUD

QUEBEC

Total of Invoiced Expenses ($290M)

Renard’s Social LicenceLocal & Regional Participation – Invoiced expenses from September 2014 to August 2015

Chib.-Chap.-Mistissini.

38%

QUEBEC

ONTARIO

OTHER PROVINCES

USA

Elsewhere (SA, TURKEY,SWITZERLAND)

Quebec86%

33Employment StatisticsAverage of 410 people/day Working at the Renard Site in September 2015

Longueuil43%

Renard34%

Vancouver9%

Toronto8% Chiboug/

Mistissini 6%

Crees58%

Non-Crees42%

Crees22%Non-Crees

78%

Longueuil20% Renard

75%

Vancouver2%

Toronto2%

Chiboug/ Mistissini 1%

Personnel at Site

Sept 2014: 193

Sept 2014: 68

Stornoway EmployeesSept 2015: 410

Sept 2015: 290

34Innovation at RenardLiquefied Natural Gas Power Plant

On October 21st, 2013 Stornoway announced it will proceed with an LNG fuelled gen-set option, made possible by the ability to receive regular cryogenic LNG shipments on the Renard Mine Road.

The Renard LNG plant will comprise seven 2.1MW rated gas gen-sets, providing sufficient power generation capacity for the project’s normal operating specification of 9.5MW.

LNG has significant advantages over traditional diesel powered gen-sets. Operating costs are estimated to be $8-$10m less annually, for an incremental capital cost of $2.6m, with 42% less greenhouse gas emissions.

LNG will be purchased from Gaz-Metro in Montreal, with deliveries of three tankers per day by road.

Diesel will continue to be used for the mobile mining fleet and construction activities.

Renard will be one of the first LNG powered mines in Canada, made

possible by road access

35

PKC

Waste Rock

Overburden

UG Mine Portal

Process Plant

Mine Waste Water TreatmentPlant

Collection Trench

Pumping Station

Innovation at RenardSurface Water Management

Sept 2014

Jan 2015

Mine Water Treatment PlantOct 2015

Camp Waste Water Treatment PlantSept 2014

Jan 2015

Camp Waste Water Treatment Plant

100% of surface precipitation and mine waste water at Renard is collected and treated before release.

36Innovation at RenardThe First Diamond Mine to Dry Stack Processed Kimberlite

Processed Kimberlite Containment (PKC)

Dry stacking of processed kimberlite minimizes impacts of project on fish habitat and local water quality

Centrifuges in process plant de-water processed kimberlite (PK)…

…producing a cake for re-handling.

PK cake is loaded-out… …trucked… …and deposited at PKC facility with progressive reclamation.

3737

Looking Forward (Matt Manson)

38

The Challenge of Finding and Developing New Diamond Mines

“Tier 1” defined as mines with Ultimate reserves greater than US$20B: Jwaneng, Orapa, Mir, Udachnya, Venetia, Catoca, Premier

Kimberlite Discoveries Since 1870

6,800

1,000

65

7

875420

20

1

10

100

1,000

10,000

KimberlitesDiscovered

Diamondiferous Economic Tier 1*

Recent Diamond Mines

Source: De Beers/SWY

Economic kimberlites represent just 1% of all discoveries made since 1870 (1.7% in Canada)

Time from Discovery to First Production

Ekati (1998, BHPB, now Dominion) 7 years

Diavik (2002, Rio Tinto/Dominion) 9 years

Victor (2008, De Beers) 20 years

Snap Lake (2008, De Beers) 11 years

Karowe (2012, Lucara) 10 years

Grib (2013, Lukoil) 18 years

Ghaghoo (2014, Gem) 23 years

Renard (2017, Stornoway) 16 years

Gahcho Kué (2017, DeBeers/MPV) 21 years

Bunder (2019, Rio Tinto) 15 Years

Projects are taking longer to develop

39Stornoway will be a Significant Diamond ProducerCurrent and Future Diamond Producers

Latest 12 Month Sales/ Forecast Future Average Sales 1 De Beers (Anglo/Botswana) $6,312m

2 Alrosa (Russia) $4,901m

3 Dominion Diamond (TSX: DDC) $872m

4 Rio Tinto (ASE: RIO) $801m

5 Petra (L: PDL) $425m

6 Stornoway (note 2; TSX: SWY) $310m7 Mountain Province (note 2; TSX: MPV) $259m

8 Gem Diamonds (TSX: GEMD) $241m

9 Lucara (TSX: LUC) $196m

10 Firestone (note 3; L: FDI) $125m

11 Others $2,558m

Total $17,000m

DeBeers37%

Alrosa29% Dominion

5%

RioTinto5%Petra2%

SWY2%

MPV1%

GEM1%LUC

1%Firestone1%

Others15%

Notes:

1. Renard estimated at FS average annual diamond production of 1.63 million carats, and WWW March 2014 weighted diamond price of US$190/ct, un-escalated

2. Gahcho Kué estimated at 49% of Revised FS average annual production of 4.45 million carats, and average modeled diamond price of US$118/ct, un-escalated

3. Firestone estimated at revised 2015 mine plan average annual production of 0.95 million carats at an average price of US$132/ct un-escalated

6 Stornoway (note 1; TSX: SWY) $310m

Source: Kimberly Process, WWW and Company Reports

40Renard’s Cash Flow PotentialBase Case Economics

Renard is Expected to Generate Substantial Cash Flow over its first 11 years of Mining

After Tax, After Stream Operating Cash Flow of between $150 and $250 million, or $0.20 to $0.30 per share

Assumptions

Mineral reserve case only

Capital and operating cost parameters as established in the January 2013 Optimization Study and October 2013 LNG FS

Base case diamond pricing from March 2014; No “special” diamonds.

2.5% annual real diamond price escalation

C$:US$ conversion rate of C$1.10

Based on terms of Financing Transaction closed on July 8th, 2014

Assumes full conversion to equity of US$81million of Convertible Debentures giving 825 million shares outstanding.

41

Stornoway will sell 100% of the Renard diamond production by tender sale in Antwerp. 10 times a year, every 5 weeks. This will create a “Stornoway Sales Week” in the diamond market.

To this end, Stornoway’s wholly owned subsidiary FCDC Sales and Marketing has entered into a sales and marketing agreement with the well known diamond industry broker and rough distributor Bonas-Couzyn, which will act as sales commissionaire and tender agent for arm's length market sales.

Sales of diamonds under the Renard Streaming Agreement will be undertaken by Bonas-Couzyn, on an undivided basis, on behalf of FCDC and the Streamers

Other than under exceptional circumstances, Stornoway will sell 100% of what it produces, will not carry a stockpile outside of normal goods-in-progress, and will be a market price taker.

Stornoway’s Diamond Sales

As a miner, Stornoway will focus on mine production and cost efficiency. Diamond sales will

be by arm's length tender sales in Antwerp, 10 times a year. Stornoway will support the Québec or

Canadian brand identification initiatives of its clients through chain of custody certification.

42Renard’s ProductQuébec Diamonds in the World Market

March 2014 Diamond Valuations (WWW International Diamond Consultants Ltd.)

KimberliteBody

Valuation Sample(carats)

WWW March 2014 Sample

Price(US$/carat)1

WWW March 2014 Base Case

Price Model(US$/carat)1

Sensitivities(Minimum to High)

Renard 2 1,580 $187 $197 $178 to $222Renard 3 2,753 $179 $157 $146 to $192Renard 4 2,674 $101 $106 ($155)2 $100 to $174Renard 65 997 $262 $187 $175 to $211

Notes

1. All prices in US$/carat. Samples utilizing a +1 DTC sieve size cut-off.

2. Should the Renard 4 diamond population prove to have a diamond population with a size distribution equal to the average of Renard 2 and 3, WWW have estimated that a base case diamond price model of $155 per carat based on March 2014 pricing. Source: WWW March 2014 Valuation Update

Base Case Diamond Valuation Estimates Using on Best Practice Methodology

Average weighted diamond price estimate in March 2014 for the Mineral Reserves of US$190/ct (un-escalated).

High Quality Production

The Renard kimberlites have similar, but marginally different diamond populations exhibiting a high incidence of large white gems and only 1% boart by weight.

XRT technology in Plant for Large Diamond Recovery

Coarse Size Distribution in Renard 2 predicts 3 to 6 50-100ct stones and 1 to 2 +100ct stones every 100,000 carats (2-3 weeks).

Plant flow sheet:• Primary jaw crushing to < 230mm• Twin DMS circuits at +1mm -19mm• LDR circuit at +19mm -45mm, scalable to -60mm• Oversize +45mm to secondary cone crusher• LDR and DMS tails +6mm -19mm to tertiary High

Pressure Grinding Rolls

43

Renard: Québec’s Next Major Mine

Fourteen years in the making

Diamonds

Demand underpinned by gifting traditions that are universal, aspirational and cross-cultural…

…but mined: supply is limited and finite

Stornoway

Focus on budget, schedule, operating excellence, cash flow

Stornoway Diamond Corporation (TSX: SWY)Our Priorities

www.stornowaydiamonds.com

4444

Thank You