bulletin - internal revenue service

TRANSCRIPT

INCOME TAX

Rev. Rul. 97–43, page 00.LIFO; price indexes; department stores. The August1997 Bureau of Labor Statistics price indexes are acceptedfor use by department stores employing the retail inventoryand last-in, first-out inventory methods for valuing inventoriesfor tax years ended on, or with reference to, August 31,1997.

T.D. 8731, page 00.Final and temporary regulations under section 42 of theCode relate to the application of the low-income housing taxcredit to certain federal rental assistance programs.

T.D. 8732, page 00.Final regulations under section 42 of the Code provide rulesfor determining the treatment of low-income housing units.

EXEMPT ORGANIZATIONS

REG–246250–96, page 00.This proposed regulation relates to the public disclosurerequirements of section 6104(e) of the Code. A public hear-ing will be held on February 4, 1998.

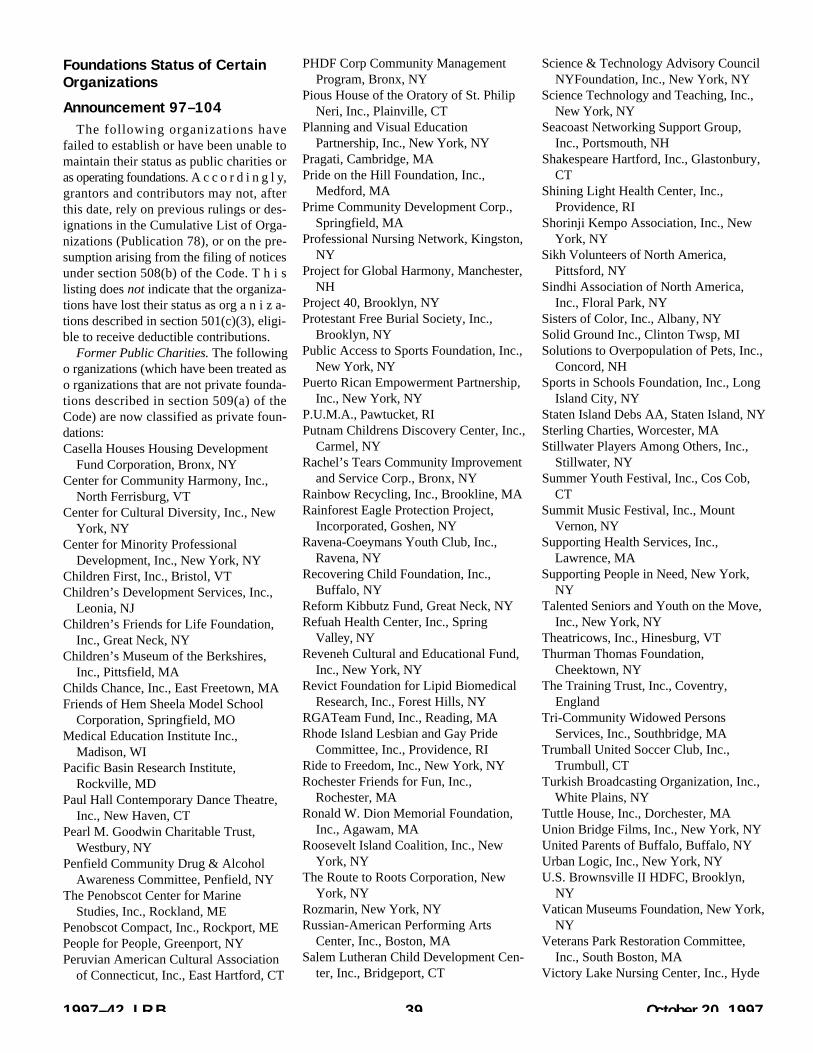

Announcement 97–104, page 00.A list is provided of organizations now classified as privatefoundations.

Announcement 97–105, page 00.A list is provided of organizations that no longer qualify asorganizations for which contributions are deductible undersection 170 of the Code.

EXCISE TAXRev. Proc. 97–46, page 00.Rural airports. This procedure contains a list of “rural air-ports,” as defined in section 4261(e)(1)(B) of the Code, forpurposes of computing the tax on air transportation. Theprocedure also provides guidance on how to calculate thetax where at least one segment of multiple segment domes-tic transportation does not begin or end at a rural airport.

ADMINISTRATIVERev. Proc. 97–47, page 00.This procedure sets forth the requirements of the Form 941Electronic Filing (ELF) Program under which a taxpayer thatis a Reporting Agent may electronically file Form 941,Employer’s Quarterly Federal Tax Return.

Internal Revenue

bulletinBulletin No. 1997–42

October 20, 1997

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

Department of the Tr e a s u r yInternal Revenue Service

Finding Lists begin on page 00.Announcement of Disbarments and Suspensions begins on page 00.

Mission of the Service

The purpose of the Internal Revenue Service is to collectthe proper amount of tax revenue at the least cost; serv ethe public by continually improving the quality of our prod-

ucts and services; and perf o rm in a manner warr a n t i n gthe highest degree of public confidence in our integrity, eff i-c i e n c y, and fairn e s s .

2

Statement of Principlesof Internal RevenueTax AdministrationThe function of the Internal Revenue Service is to adm i n i s-ter the Internal Revenue Code. Tax policy for raising re v e n u eis determined by Congre s s .

With this in mind, it is the duty of the Service to carry out thatpolicy by correctly applying the laws enacted by Congress;to determine the reasonable meaning of various Code provi-sions in light of the Congressional purpose in enacting them;and to perform this work in a fair and impartial manner, withneither a government nor a taxpayer point of view.

At the heart of administration is interpretation of the Code. Itis the responsibility of each person in the Service, chargedwith the duty of interpreting the law, to try to find the truemeaning of the statutory provision and not to adopt astrained construction in the belief that he or she is “protect-ing the revenue.” The revenue is properly protected onlywhen we ascertain and apply the true meaning of the statute.

The Service also has the responsibility of applying andadministering the law in a reasonable, practical manner.Issues should only be raised by examining officers whenthey have merit, never arbitrarily or for trading purposes.At the same time, the examining officer should never hesi-tate to raise a meritorious issue. It is also important thatc a re be exercised not to raise an issue or to ask a court toadopt a position inconsistent with an established Serv i c ep o s i t i o n .

Administration should be both reasonable and vigorous. Itshould be conducted with as little delay as possible andwith great courtesy and considerateness. It should nevert ry to overreach, and should be reasonable within thebounds of law and sound administration. It should, howev-e r, be vigorous in requiring compliance with law and itshould be relentless in its attack on unreal tax devices andf r a u d .

The Internal Revenue Bulletin is the authoritative instrumentof the Commissioner of Internal Revenue for announcing offi-cial rulings and procedures of the Internal Revenue Serviceand for publishing Treasury Decisions, Executive Orders, TaxConventions, legislation, court decisions, and other items ofgeneral interest. It is published weekly and may be obtainedf rom the Superintendent of Documents on a subscriptionbasis. Bulletin contents of a permanent nature are consoli-dated semiannually into Cumulative Bulletins, which are soldon a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform applicationof the tax laws, including all rulings that supersede, revoke,modify, or amend any of those previously published in theBulletin. All published rulings apply retroactively unless other-wise indicated. Procedures relating solely to matters of in-ternal management are not published; however, statementsof internal practices and pro c e d u res that affect the rightsand duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service onthe application of the law to the pivotal facts stated in therevenue ruling. In those based on positions taken in rulingsto taxpayers or technical advice to Service field off i c e s ,identifying details and information of a confidential natureare deleted to prevent unwarranted invasions of privacy andto comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not havethe force and effect of Tre a s u ry Department Regulations,but they may be used as precedents. Unpublished ru l i n g swill not be relied on, used, or cited as precedents by Servicepersonnel in the disposition of other cases. In applying pub-lished rulings and procedures, the effect of subsequent leg-islation, regulations, court decisions, rulings, and pro c e-

dures must be considered, and Service personnel and oth-ers concerned are cautioned against reaching the same con-clusions in other cases unless the facts and circumstancesare substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisionsof the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions, and Subpart B, Legislation and RelatedCommittee Reports.

P a rt III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross re f e rences tothese subjects are contained in the other Parts and Sub-parts. Also included in this part are Bank Secrecy Act Admin-istrative Rulings. Bank Secrecy Act Administrative Rulingsare issued by the Department of the Treasury’s Office of theAssistant Secretary (Enforcement).

Part IV.—Items of General Interest.With the exception of the Notice of Proposed Rulemakingand the disbarment and suspension list included in this part,none of these announcements are consolidated in the Cumu-lative Bulletins.

The first Bulletin for each month includes a cumulative indexfor the matters published during the preceding months.These monthly indexes are cumulated on a quarterly andsemiannual basis, and are published in the first Bulletin of thesucceeding quarterly and semiannual period, re s p e c t i v e l y.

3

Introduction

The contents of this publication are not copyrighted and may be reprinted freely.Acitation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

October 20, 1997 4 1997–42 I.R.B.

Section 42.—Low-IncomeHousing Credit

26 CFR 1.42–15: Available unit rule.

T.D. 8732

D E PA RTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Available Unit Rule

A G E N C Y: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

S U M M A RY: This document containsfinal regulations concerning the treatmentof low-income housing units in a buildingthat are occupied by individuals whose in-comes increase above 140 percent of theincome limitation applicable under sec-tion 42(g)(1). These regulations aff e c towners of those buildings who claim thelow-income housing tax credit.

D ATES: These regulations are eff e c t i v eSeptember 26, 1997.

For dates of applicability of these regu-lations, see §1.42–15(i).

FOR FURTHER INFORMATION CON-TACT: David Selig, (202) 622-3040 (nota toll-free number).

SUPPLEMENTARYINFORMATION:

Background

On May 30, 1996, the IRS published anotice of proposed rulemaking in the Fed-eral Register (PS–29–95 at 61 FR 27036[1997–1 C.B. 862]) proposing amend-ments to the Income Tax Regulations (26CFR part 1) under section 42(g)(2)(D) ofthe Internal Revenue Code. A p u b l i chearing was scheduled for September 17,1996, pursuant to a notice of public hear-ing published simultaneously with the no-tice of proposed rulemaking. However,the IRS received no requests to speak atthe public hearing, and no public hearingwas held. Written comments respondingto the notice were received. After consid-eration of all the comments, the proposedregulations are adopted as revised by thisTreasury decision.

Explanation of Revisions and Summaryof Comments

The general rule in section 42(g)(2)-(D)(i) provides that if the income of anoccupant of a low-income unit increasesabove the income limitation applicableunder section 42(g)(1), the unit continuesto be treated as a low-income unit. Thisgeneral rule only applies if the occupant’sincome initially met the income limitationand the unit continues to be rent-re-stricted. Section 42(g)(2)(D)(ii), how-ever, provides an exception to the generalrule in section 42(g)(2)(D)(i). Under thisexception, the unit ceases being treated asa low-income unit when two conditionsoccur. The first condition is that the occu-p a n t ’s income increases above 140 per-cent of the income limitation applicableunder section 42(g)(1), or above 170 per-cent for a deep rent skewed project de-scribed in section 142(d)(4)(B) (applica-ble income limitation). When this occurs,the unit becomes an over-income unit.The second condition is that a new occu-pant, whose income exceeds the applica-ble income limitation (nonqualified resi-dent), occupies any residential unit in thebuilding of a comparable or smaller size(comparable unit).

Rules and Definitions

One commentator suggested that theavailable unit rule under the proposedregulations did not clearly indicatewhether the aggregate income of all occu-pants of a unit is taken into account. Ac-cordingly, the final regulations clarify thatan over-income unit means a low-incomeunit in which the aggregate income of theoccupants of the unit increases above 140percent of the applicable income limita-tion under section 42(g)(1), or above 170percent of the applicable income limita-tion for deep rent skewed projects de-scribed in section 142(d)(4)(B).

Commentators requested that the finalregulations specify whether a comparableunit is measured by floor space or numberof bedrooms. The final regulations pro-vide that a comparable unit must be mea-sured by the same method the taxpayerused to determine qualified basis for thecredit year in which the comparable unitbecame available.

Some commentators stated that the pro-vision in the proposed regulations that allavailable comparable units (not just the“next available” unit) must be rented toqualified residents to continue treating anover-income unit as a low-income unit isinconsistent with the title of section42(g)(2)(D)(ii). Although the title of thatprovision uses the term next availableunit, the text of the rule provides that ifany available comparable unit is occupiedby a nonqualified resident, the over- i n-come unit ceases to be treated as a low-in-come unit. This means that if a buildinghas more than one over-income unit, rent-ing any available comparable unit (a com-parably sized or smaller unit) to a quali-fied resident preserves the status of allo v e r-income units as low-income units.S i m i l a r l y, if any available comparableunit is rented to a nonqualified resident,all over-income units for which the avail-able unit was a comparable unit lose theirstatus as low-income units; thus, compa-rably sized or larger over-income unitswould lose their status as low-incomeunits. In operation, this means that theowner must continue to rent any availablecomparable unit to a qualified residentuntil the percentage of low-income unitsin a building (excluding the over-incomeunits) is equal to the percentage of low-in-come units on which the credit is based.At that point, failure to maintain the over-income units as low-income units has noimmediate significance. (However, thefailure to maintain an over-income unit asa low-income unit may affect the owner’sdecision of whether or not to rent a partic-ular available unit at market rate at a latertime.) Consequently, the final regulationsprovide that all available comparableunits in the building, not only the nextavailable comparable unit, must be rentedto qualified residents to retain the low-in-come status of the over-income units.

Application of Rules on a Building byBuilding Basis

The proposed regulations provide thatin a project containing more than onelow-income building, the available unitrule applies separately to each building.Some commentators suggested that theregulations should permit residents ofo v e r-income units to move to available

P a rt I. Rulings and Decisions Under the Internal Revenue Code of 1986

units in different buildings within thesame low-income housing project withoutviolating the available unit rule. How-ever, because the requirements under sec-tion 42 must be satisfied on a building bybuilding basis, the final regulations pro-vide that the available unit rule only per-mits a current resident to move to anotherunit within the same building of a low-in-come housing project.

In addition, in response to requestsfrom several commentators, the final reg-ulations make clear that when a currentresident moves to a different unit withinthe same low-income building, the unitsexchange status. (See example 2 of§1.42–15(g) of the proposed regulationsand §1.42–15(h) of the final regulations.)Thus, the newly occupied unit adopts thestatus of the vacated unit, and the vacatedunit assumes the status the newly occu-pied unit had immediately prior to its oc-cupancy by the qualifying residents.

Timing Issues

The methods of committing rental unitsto tenants varies in different jurisdictions.H o w e v e r, it is a common rental practiceto have some form of preliminary reserva-tion for a unit prior to the date on which alease is signed or the unit is occupied.Thus, several commentators have re-quested clarification that once a unit is re-served for a prospective tenant, it is nolonger treated as available for purposes ofthe available unit rule. A c c o r d i n g l y, thefinal regulations provide that a unit is notavailable for purposes of the availableunit rule when the unit is no longer avail-able for rent due to a reservation that isbinding under local law.

F i n a l l y, financing arrangements usingobligations that purport to be exempt fa-cility bonds under section 142 must meetthe requirements of sections 103 and 141through 150 for interest on the obligationsto be excluded from gross income undersection 103(a). The requirements undersection 142(d) may differ from thoseunder section 42. A c c o r d i n g l y, the finalregulations provide that the rules underthe final regulations are not intended as aninterpretation of the applicable rulesunder section 142.

Special Analyses

It has been determined that this Tr e a-sury decision is not a significant regula-

tory action as defined in EO 12866.Therefore, a regulatory assessment is notrequired. It also has been determined thatsection 553(b) of the Administrative Pro-cedure Act (5 U.S.C. chapter 5) does notapply to these regulations, and, becausethese regulations do not impose on smallentities a collection of information re-quirement, the Regulatory Flexibility Act(5 U.S.C. chapter 6) does not apply.Therefore, a Regulatory FlexibilityAnalysis is not required. Pursuant to sec-tion 7805(f) of the Internal RevenueCode, the notice of proposed rulemakingpreceding these regulations was submit-ted to the Chief Counsel for Advocacy ofthe Small Business Administration forcomment on its impact on small business.

Drafting Information

The principal author of these regulationsis David Selig, Office of the A s s i s t a n tChief Counsel (Passthroughs and SpecialIndustries), IRS. However, other person-nel from the IRS and Treasury Departmentparticipated in their development.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 is amendedas follows:

PART 1—INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by adding an entry innumerical order to read as follows:

Authority: 26 U.S.C. 7805 * * * Section 1.42-15 is also issued under 26U.S.C. 42(n); * * *

Par. 2. Section 1.42-15 is added to readas follows:

§1.42–15 Available unit rule.

(a) D e f i n i t i o n s . The following defini-tions apply to this section:

Applicable income limitation means thelimitation applicable under section42(g)(1) or, for deep rent skewed projectsdescribed in section 142(d)(4)(B), 40 per-cent of area median gross income.

Available unit ru l e means the rule insection 42(g)(2)(D)(ii).

Comparable unit means a residentialunit in a low-income building that is com-parably sized or smaller than an over-in-

come unit or, for deep rent skewed pro-jects described in section 142(d)(4)(B),any low-income unit. For purposes of de-termining whether a residential unit iscomparably sized, a comparable unit mustbe measured by the same method used todetermine qualified basis for the credityear in which the comparable unit becameavailable.

Current resident means a person who isliving in the low-income building.

Low-income unit is defined by section42(i)(3)(A).

Nonqualified resident means a new oc-cupant or occupants whose aggregate in-come exceeds the applicable income limi-tation.

Over-income unit means a low-incomeunit in which the aggregate income of theoccupants of the unit increases above 140percent of the applicable income limita-tion under section 42(g)(1), or above 170percent of the applicable income limita-tion for deep rent skewed projects de-scribed in section 142(d)(4)(B).

Qualified re s i d e n t means an occupanteither whose aggregate income (com-bined with the income of all other occu-pants of the unit) does not exceed the ap-plicable income limitation and who isotherwise a low-income resident undersection 42, or who is a current resident.

(b) General section 42(g)(2)(D)(i) rule.Except as provided in paragraph (c) ofthis section, notwithstanding an increasein the income of the occupants of a low-income unit above the applicable incomelimitation, if the income of the occupantsinitially met the applicable income limita-tion, and the unit continues to be rent-restricted—

(1) The unit continues to be treated as alow-income unit; and

(2) The unit continues to be included inthe numerator and the denominator of theratio used to determine whether a projectsatisfies the applicable minimum set-aside requirement of section 42(g)(1).

(c) E x c e p t i o n . A unit ceases to betreated as a low-income unit if it becomesan over-income unit and a nonqualifiedresident occupies any comparable unitthat is available or that subsequently be-comes available in the same low-incomebuilding. In other words, the owner of alow-income building must rent to quali-fied residents all comparable units that areavailable or that subsequently become

1997–42 I.R.B. 5 October 20, 1997

available in the same building to continuetreating the over-income unit as a low-in-come unit. Once the percentage of low-income units in a building (excluding theover-income units) equals the percentageof low-income units on which the credit isbased, failure to maintain the over-incomeunits as low-income units has no immedi-ate significance. The failure to maintainthe over-income units as low-incomeunits, however, may affect the decision ofwhether or not to rent a particular avail-able unit at market rate at a later time. Aunit is not available for purposes of theavailable unit rule when the unit is nolonger available for rent due to contrac-tual arrangements that are binding underlocal law (for example, a unit is not avail-able if it is subject to a preliminary reser-vation that is binding on the owner underlocal law prior to the date a lease is signedor the unit is occupied).

(d) Effect of current resident movingwithin building. When a current residentmoves to a different unit within the build-ing, the newly occupied unit adopts thestatus of the vacated unit. Thus, if a cur-rent resident, whose income exceeds theapplicable income limitation, moves froman over-income unit to a vacant unit in thesame building, the newly occupied unit istreated as an over-income unit. The va-cated unit assumes the status the newlyoccupied unit had immediately before itwas occupied by the current resident.

(e) Available unit rule applies sepa -rately to each building in a project. In aproject containing more than one low-in-come building, the available unit rule ap-plies separately to each building.

(f) Result of noncompliance with avail -able unit rule. If any comparable unit thatis available or that subsequently becomesavailable is rented to a nonqualified resi-dent, all over-income units for which theavailable unit was a comparable unitwithin the same building lose their statusas low-income units; thus, comparablysized or larger over-income units wouldlose their status as low-income units.

(g) Relationship to tax-exempt bondp ro v i s i o n s . Financing arrangements thatpurport to be exempt-facility bonds undersection 142 must meet the requirementsof sections 103 and 141 through 150 forinterest on the obligations to be excludedfrom gross income under section 103(a).This section is not intended as an interpre-tation under section 142.

(h) Examples. The following examplesillustrate this section:

Example 1. This example illustrates noncompli-ance with the available unit rule in a low-incomebuilding containing three over-income units. OnJanuary 1, 1998, a qualified low-income housingproject, consisting of one building containing tenidentically sized residential units, received a hous-ing credit dollar amount allocation from a statehousing credit agency for five low-income units.By the close of 1998, the first year of the credit pe-riod, the project satisfied the minimum set-aside re-quirement of section 42(g)(1)(B). Units 1, 2, 3, 4,and 5 were occupied by individuals whose incomesdid not exceed the income limitation applicableunder section 42(g)(1) and were otherwise low-in-come residents under section 42. Units 6, 7, 8, and9 were occupied by market-rate tenants. Unit 10was vacant. To avoid recapture of credit, the pro-ject owner must maintain five of the units as low-in-come units. On November 1, 1999, the certificatesof annual income state that annual incomes of theindividuals in Units 1, 2, and 3 increased above 140percent of the income limitation applicable undersection 42(g)(1), causing those units to becomeo v e r-income units. On November 30, 1999, Units 8and 9 became vacant. On December 1, 1999, theproject owner rented Units 8 and 9 to qualified resi-dents who were not current residents at rates meet-ing the rent restriction requirements of section42(g)(2). On December 31, 1999, the project ownerrented Unit 10 to a market-rate tenant. BecauseUnit 10, an available comparable unit, was leased toa market-rate tenant, Units 1, 2, and 3 ceased to betreated as low-income units. On that date, Units 4,5, 8, and 9 were the only remaining low-incomeunits. Because the project owner did not maintainfive of the residential units as low-income units, thequalified basis in the building is reduced, and creditmust be recaptured. If the project owner had rentedUnit 10 to a qualified resident who was not a cur-rent resident, eight of the units would be low-in-come units. At that time, Units 1, 2, and 3, the over-income units, could be rented to market-rate tenantsbecause the building would still contain five low-in-come units.

Example 2. This example illustrates the provi-sions of paragraph (d) of this section. A l o w - i n-come project consists of one six-floor building.The residential units in the building are identicallysized. The building contains two over-income unitson the sixth floor and two vacant units on the firstf l o o r. The project owner, desiring to maintain theo v e r-income units as low-income units, wants torent the available units to qualified residents. J, aresident of one of the over-income units, wishes tooccupy a unit on the first floor. J’s income has re-cently increased above the applicable income limi-tation. The project owner permits J to move intoone of the units on the first floor. Despite J’s in-come exceeding the applicable income limitation, Jis a qualified resident under the available unit rulebecause J is a current resident of the building. T h eunit newly occupied by J becomes an over- i n c o m eunit under the available unit rule. The unit vacatedby J assumes the status the newly occupied unit hadimmediately before J occupied the unit. The over-income units in the building continue to be treatedas low-income units.

(i) Effective date. This section appliesto leases entered into or renewed on andafter September 26, 1997.

Michael P. Dolan,Acting Commissioner of

Internal Revenue.

Approved August 28, 1997.

Donald C. Lubick,Acting Assistant Secretary of

the Treasury.

(Filed by the Office of the Federal Register on Sep-tember 25, 1997, 8:45 a.m., and published in theissue of the Federal Register for September 26,1997, 62 F.R. 50503)

26 CFR 1.42–16: Eligible basis reduced by federalgrants.

T.D. 8731

D E PA RTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Section 42(d)(5) Federal Grants

A G E N C Y: Internal Revenue Service(IRS), Treasury.

ACTION: Final and temporary regula-tions.

S U M M A RY: This document containsfinal regulations with respect to the low-income housing tax credit relating to theapplication of section 42(d)(5) to certainrental assistance programs under section42(g)(2)(B)(i). The regulations clarifythat certain types of federal rental assis-tance payments do not result in a reduc-tion in the eligible basis of a low-incomehousing building. DATES: These regula-tions are effective September 26, 1997.

For date of applicability for these regu-lations, see §1.42–16(d).

FOR FURTHER INFORMATION CON-TACT: Christopher J. Wilson, (202) 622-3040 (not a toll-free call).

SUPPLEMENTARYINFORMATION:

Background

Temporary regulations (TD 8713[1997–14 I.R.B. 4]) and a notice of pro-posed rulemaking cross-referencing the

October 20, 1997 6 1997–42 I.R.B.

temporary regulations were published inthe Federal Register for January 27,1997 (62 FR 3792, 3848 [REG–254394–96 I.R.B. 14]). Those regulations providethat certain federal rental assistance pay-ments made to the owner of a building onbehalf of low-income tenants are not fed-eral grants with respect to a building or itsoperation that require a reduction in theb u i l d i n g ’s eligible basis under section42(d)(5) of the Internal Revenue Code(Code). These payments include rentalassistance payments made under section 8of the United States Housing Act of 1937(Act) (42 U.S.C. 1437f), certain paymentsmade under section 9 of the Act, and pay-ments made under such other programs ormethods of rental assistance as may bedesignated in the Federal Register or theInternal Revenue Bulletin. The notice ofproposed rulemaking indicated that com-ments would be considered on those areasaddressed in the temporary regulations.Written comments responding to the no-tice of proposed rulemaking were re-ceived. There was no request for a publichearing, and no public hearing was held.After consideration of all the written com-ments, the proposed regulations havebeen adopted, without change, by thisTreasury decision.

Summary of Comments

One commenter suggested that the finalregulations provide additional guidancefor state agencies to use in determiningwhether similar programs beyond thosedescribed in the regulations should beconsidered grants that cause a reductionin a building’s eligible basis under section42(d)(5) of the Code. The final regula-tions do not adopt this suggestion. T h escope of this regulation is limited to spec-ified rental assistance payments that arenot grants requiring a reduction in a build-i n g ’s eligible basis and any additionalpayments the Secretary may designate inthe future.

Another commenter suggested that§1.42–16(c)(3) should be deleted if it isintended to impose conditions beyond therestrictions under section 9 of the Act, be-cause the IRS is improperly infringingupon the Department of Housing andUrban Development’s (HUD) authority toprovide subsidies under section 9. T h efinal regulations do not adopt this sugges-tion. Section 1.42–16 does not interpret

H U D ’s authority for paying subsidiesunder section 9; it describes the extent towhich section 9 payments may be madewithout a reduction in a building’s eligiblebasis under section 42(d)(5) of the Code.The conditions imposed on section 9 pay-ments in §1.42–16(c)(3) serve to diff e r e n-tiate section 9 assistance for operating ex-penses that function in a manner similar torental assistance payments under section 8of the Act from section 9 assistance that isapplied to uses more closely associatedwith operational expenses requiring a re-duction in a building’s eligible basis undersection 42(d)(5).

This commenter also suggested that if§1.42–16(c)(3) were to be retained, itshould be clarified to provide that actualoperating costs be determined by HUDand/or the appropriate public housinga g e n c y. The commenter reasons thatHUD is already making this determinationin the context of deciding the properamount of assistance to make under sec-tion 9 of the Act, and that precedent al-ready exists for allowing HUD to makecertain interpretations relating to the sec-tion 42 program. The final regulations donot adopt this suggestion. The IRS andTreasury believe they should retain theability to determine what costs are appro-priately characterized as operating coststhat require a reduction in a building’s eli-gible basis under section 42(d)(5) of theC o d e .

Special Analyses

It has been determined that this Tr e a-sury decision is not a significant regula-tory action as defined in EO 12866.Therefore, a regulatory assessment is notrequired. It also has been determined thatsection 553(b) of the Administrative Pro-cedure Act (5 U.S.C. chapter 5) does notapply to these regulations and, becausethese regulations do not impose on smallentities a collection of information re-quirement, the Regulatory Flexibility Act(5 U.S.C. chapter 6) does not apply.Therefore, a Regulatory FlexibilityAnalysis is not required. Pursuant to sec-tion 7805(f) of the Internal RevenueCode, the notice of proposed rulemakingpreceding these regulations was submit-ted to the Chief Counsel for Advocacy ofthe Small Business Administration forcomment on its impact on small business.

Drafting Information

The principal author of these regulationsis Christopher J. Wilson, Office of A s s i s t-ant Chief Counsel (Passthroughs and Spe-cial Industries). However, other personnelfrom the IRS and Treasury Departmentparticipated in their development.

* * * * *

Adoption of Amendments to the Regulations

Accordingly, 26 CFR part 1 is amendedas follows:

PART 1—INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by removing the entryfor §1.42–16T and adding an entry in nu-merical order to read as follows:

Authority: 26 U.S.C. 7805 * * *Section 1.42–16 also issued under 26U.S.C. 42(n); * * *

P a r. 2. Section 1.42–16 is added toread as follows:

§1.42–16 Eligible basis reduced by federal grants.

(a) In general. If, during any taxableyear of the compliance period (describedin section 42(i)(1)), a grant is made withrespect to any building or the operationthereof and any portion of the grant isfunded with federal funds (whether or notincludible in gross income), the eligiblebasis of the building for the taxable yearand all succeeding taxable years is re-duced by the portion of the grant that is sofunded.

(b) Grants do not include certain rentalassistance payments. A federal rental as-sistance payment made to a buildingowner on behalf or in respect of a tenantis not a grant made with respect to abuilding or its operation if the payment ismade pursuant to—

(1) Section 8 of the United StatesHousing Act of 1937;

(2) A qualifying program of rental as-sistance administered under section 9 ofthe United States Housing Act of 1937; or

(3) A program or method of rental as-sistance as the Secretary may designateby publication in the Federal Register orin the Internal Revenue Bulletin (see§601.601(d)(2) of this chapter).

(c) Qualifying rental assistance pro -

1997–42 I.R.B. 7 October 20, 1997

g r a m . For purposes of paragraph (b)(2)of this section, payments are made pur-suant to a qualifying rental assistance pro-gram administered under section 9 of theUnited States Housing Act of 1937 to theextent that the payments—

(1) Are made to a building owner pur-suant to a contract with a public housingauthority with respect to units the ownerhas agreed to maintain as public housingunits (PH-units) in the building;

(2) Are made with respect to units oc-cupied by public housing tenants, pro-vided that, for this purpose, units may beconsidered occupied during periods ofshort term vacancy (not to exceed 60days); and

(3) Do not exceed the difference be-tween the rents received from a building’sPH-unit tenants and a pro rata portion ofthe building’s actual operating costs thatare reasonably allocable to the PH-units(based on square footage, number of bed-rooms, or similar objective criteria), andprovided that, for this purpose, operatingcosts do not include any developmentcosts of a building (including developer’sfees) or the principal or interest of anydebt incurred with respect to any part of

the building. (d) Effective date. This section is effec-

tive September 26, 1997.

§1.42–16T [Removed]

Par. 3. Section 1.42–16T is removed.

Michael P. Dolan,Acting Commissioner of

Internal Revenue.

Approved August 26, 1997.

Donald C. Lubick,Acting Assistant Secretary of

the Treasury.

(Filed by the Office of the Federal Register on Sep-tember 25, 1997, 8:45 a.m., and published in theissue of the Federal Register for September 26,1997, 62 F.R. 50502)

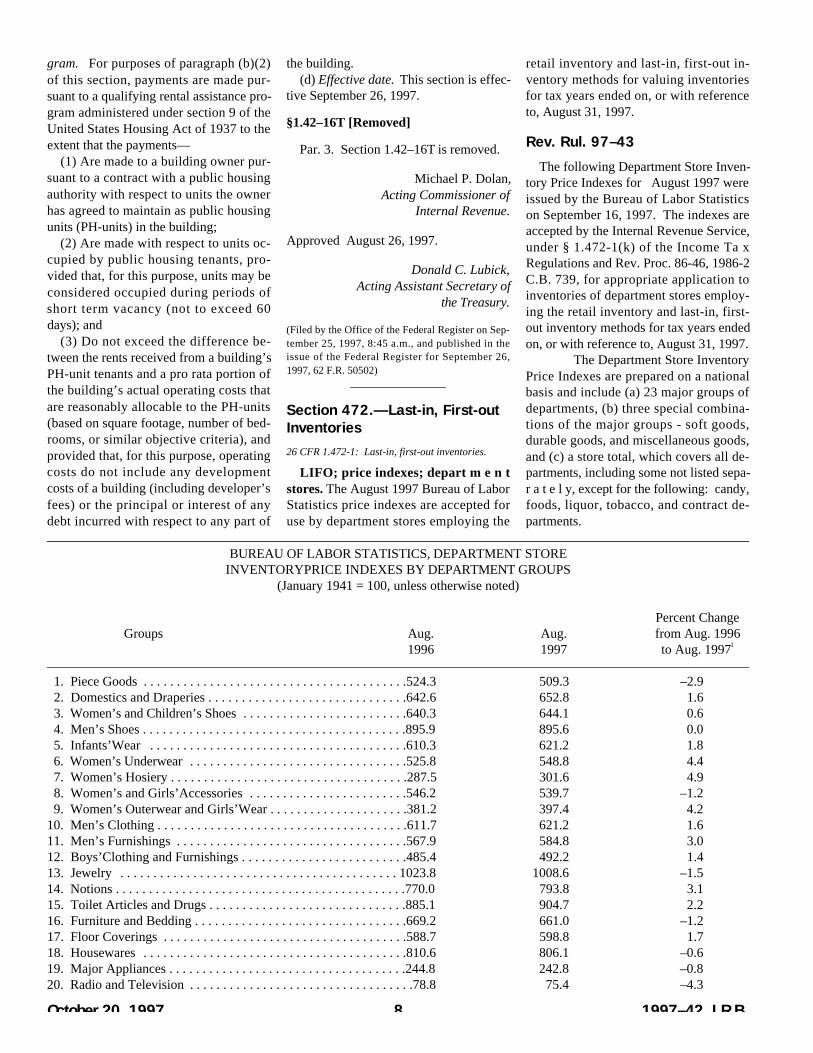

Section 472.—Last-in, First-outInventories 26 CFR 1.472-1: Last-in, first-out inventories.

LIFO; price indexes; depart m e n tstores. The August 1997 Bureau of LaborStatistics price indexes are accepted foruse by department stores employing the

retail inventory and last-in, first-out in-ventory methods for valuing inventoriesfor tax years ended on, or with referenceto, August 31, 1997.

Rev. Rul. 97–43

The following Department Store Inven-tory Price Indexes for August 1997 wereissued by the Bureau of Labor Statisticson September 16, 1997. The indexes areaccepted by the Internal Revenue Service,under § 1.472-1(k) of the Income Ta xRegulations and Rev. Proc. 86-46, 1986-2C.B. 739, for appropriate application toinventories of department stores employ-ing the retail inventory and last-in, first-out inventory methods for tax years endedon, or with reference to, August 31, 1997.

The Department Store InventoryPrice Indexes are prepared on a nationalbasis and include (a) 23 major groups ofdepartments, (b) three special combina-tions of the major groups - soft goods,durable goods, and miscellaneous goods,and (c) a store total, which covers all de-partments, including some not listed sepa-r a t e l y, except for the following: candy,foods, liquor, tobacco, and contract de-partments.

October 20, 1997 8 1997–42 I.R.B.

BUREAU OF LABOR STATISTICS, DEPARTMENT STOREINVENTORYPRICE INDEXES BY DEPARTMENT GROUPS

(January 1941 = 100, unless otherwise noted)

Percent ChangeGroups Aug. Aug. from Aug. 1996

1996 1997 to Aug. 19971

1. Piece Goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .524.3 509.3 –2.92. Domestics and Draperies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .642.6 652.8 1.63. Women’s and Children’s Shoes . . . . . . . . . . . . . . . . . . . . . . . . .640.3 644.1 0.64. Men’s Shoes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .895.9 895.6 0.05. Infants’Wear . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .610.3 621.2 1.86. Women’s Underwear . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .525.8 548.8 4.47. Women’s Hosiery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .287.5 301.6 4.98. Women’s and Girls’Accessories . . . . . . . . . . . . . . . . . . . . . . . .546.2 539.7 –1.29. Women’s Outerwear and Girls’Wear . . . . . . . . . . . . . . . . . . . . .381.2 397.4 4.2

10. Men’s Clothing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .611.7 621.2 1.611. Men’s Furnishings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .567.9 584.8 3.012. Boys’Clothing and Furnishings . . . . . . . . . . . . . . . . . . . . . . . . .485.4 492.2 1.413. Jewelry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1023.8 1008.6 –1.514. Notions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .770.0 793.8 3.115. Toilet Articles and Drugs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .885.1 904.7 2.216. Furniture and Bedding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .669.2 661.0 –1.217. Floor Coverings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .588.7 598.8 1.718. Housewares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .810.6 806.1 –0.619. Major Appliances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .244.8 242.8 –0.820. Radio and Television . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .78.8 75.4 –4.3

DRAFTING INFORMATION

The principal author of this revenueruling is Stan Michaels of the Office ofAssistant Chief Counsel (Income Tax andAccounting). For further information re-garding this revenue ruling, contact Mr.Michaels on (202) 622-4970 (not a toll-free call).

Section 3504.—Acts To BePerformed by Agents26 CFR 31.3504–1: Acts to be performed by agents.

Requirements of the Form 941 Electronic Filing(ELF) Program are provided. See Rev. Proc. 97–47,page 00.

Section 4261.—Imposition ofTax

26 CFR 49.4261–1: Imposition of Tax; in general.

This revenue procedure provides a list of “ruralairports” as that term is defined in § 4261(e)(1)(B)of the Internal Revenue Code, for purposes of com-puting the tax on air transportation. The revenueprocedure also provides guidance on how to calcu-late the tax where at least one segment of multiplesegment domestic transportation does not begin orend at a rural airport. See Rev. Proc. 97–46, page 00.

Section 6011.—GeneralRequirements of Return,Statement, or List26 CFR 31.6011(a)–7: Execution of returns.

Requirements of the Form 941 Electronic Filing(ELF) Program are provided. See Rev. Proc. 97–47,page 00.

Section 6061.—Signing ofReturns and Other Documents26 CFR 31.6061–1: Signing of returns.

Requirements of the Form 941 Electronic Filing

(ELF) Program are provided. See Rev. Proc. 97–47,page 00.

26 CFR 301.6061–1: Signing of returns and otherdocuments.

Requirements of the Form 941 Electronic Filing(ELF) Program are provided. See Rev. Proc. 97–47,page 00.

Section 6071.—Time for FilingReturns and Other Documents26 CFR 31.6071(a)(1): Time for filing returns andother documents.

Requirements of the Form 941 Electronic Filing(ELF) Program are provided. See Rev. Proc. 97–47,page 00.

1997–42 I.R.B. 9 October 20, 1997

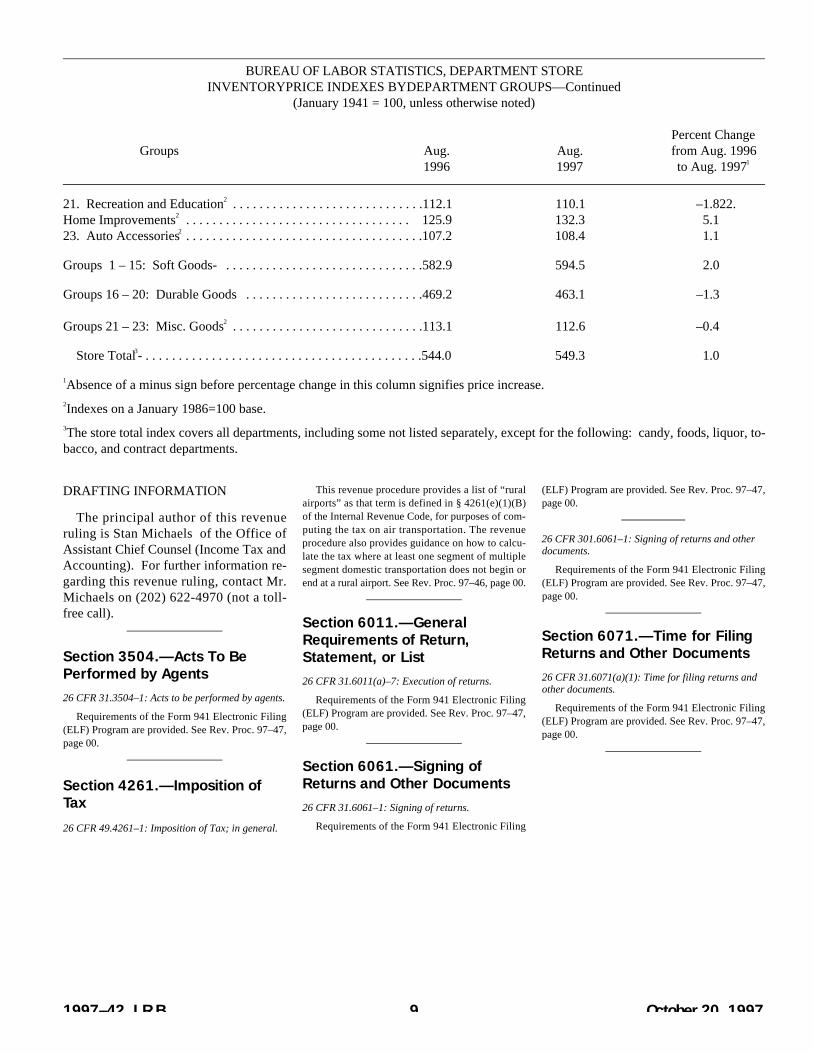

BUREAU OF LABOR STATISTICS, DEPARTMENT STOREINVENTORYPRICE INDEXES BYDEPARTMENT GROUPS—Continued

(January 1941 = 100, unless otherwise noted)

Percent ChangeGroups Aug. Aug. from Aug. 1996

1996 1997 to Aug. 19971

21. Recreation and Education2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .112.1 110.1 –1.822.Home Improvements2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125.9 132.3 5.123. Auto Accessories2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .107.2 108.4 1.1

Groups 1 – 15: Soft Goods- . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .582.9 594.5 2.0

Groups 16 – 20: Durable Goods . . . . . . . . . . . . . . . . . . . . . . . . . . .469.2 463.1 –1.3

Groups 21 – 23: Misc. Goods2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .113.1 112.6 –0.4

Store Total3- . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .544.0 549.3 1.0

1Absence of a minus sign before percentage change in this column signifies price increase. 2Indexes on a January 1986=100 base.3The store total index covers all departments, including some not listed separately, except for the following: candy, foods, liquor, to-bacco, and contract departments.

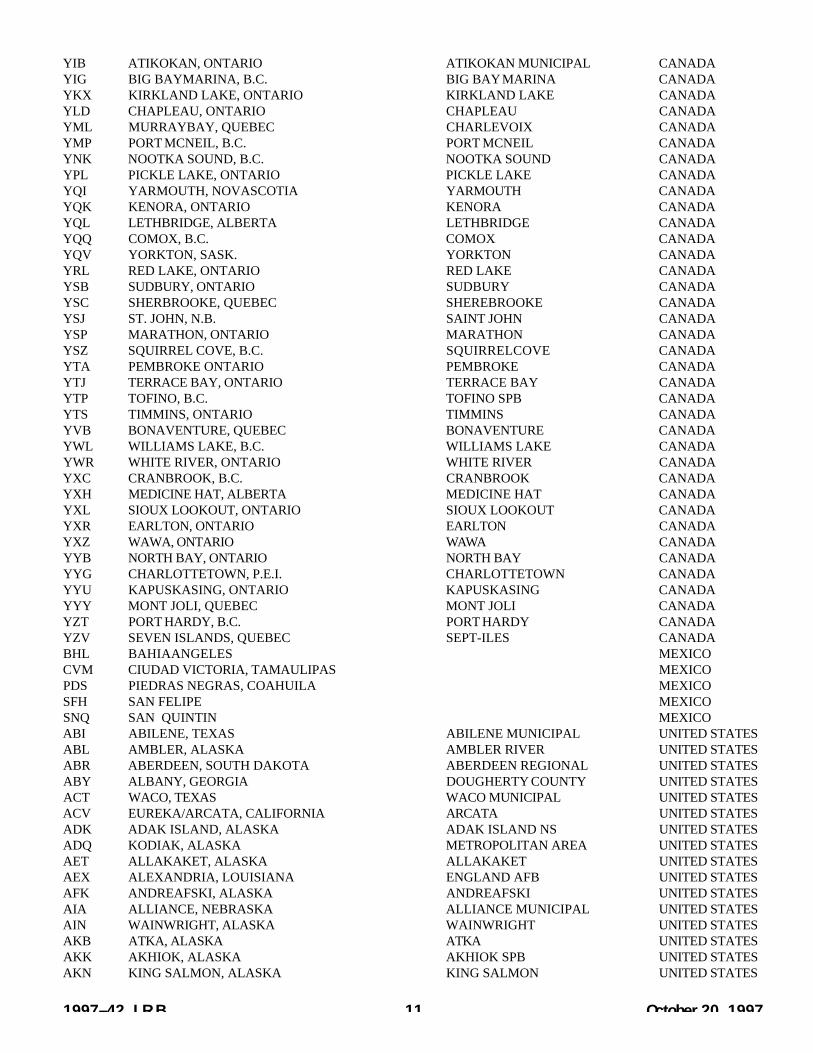

CODE LOCATION* AIRPORT NAME COUNTRYYAC CAT LAKE, ONTARIO CATLAKE CANADAYAG FORT FRANCES, ONTARIO FORT FRANCES MUNI CANADAYAM SAULTSTE. MARIE, ONTARIO SAULTSTE MARIE CANADAYAZ TOFINO, B.C. TOFINO CANADAYBC BAIE COMEAU, QUEBEC BAIE COMEAU CANADAYBG SAGUENAY, QUEBEC BAGOTVILLE CANADAYBL CAMPBELLRIVER, B.C. CAMPBELL RIVER CANADAYBR BRAN WN, MANITOBA BRANDON CANADAYBV BERENS RIVER MANITOBA BERENS RIVER CANADAYCF CORTES BAY, B.C. CORTES BAY CANADAYCG CASTLEGAR/NELSON/TRAIL,B.C. CASTLEGAR CANADAYCL CHARLO, NEW BRUNSWICK CHARLO CANADAYDN DAUPHIN, MANITOBA DAUPHIN CANADAYDS DESOLATION SOUND, B.C. DESOLATION SOUND CANADAYEL ELLIOT LAKE, ONTARIO ELLIOT LAKE MUNI CANADAYFC FREDERICTON, NEW BRUNSWICK FREDERICTON CANADAYGE GORGE HARBOR, B.C. GORGE HARBOR CANADAYGK KINGSTON, ONTARIO KINGSTON CANADAYGN GREENWAYSOUND, B.C. GREENWAYSOUND CANADAYGP GASPE, QUEBEC GASPE CANADAYGQ GERALDTON, ONTARIO GERALDTON CANADAYHD DRYDEN, ONTARIO DRYDEN MUNICIPAL CANADAYHH CAMPBELL RIVER, B.C. HARBOR SPB CANADAYHN HORNEPAYNE, ONTARIO HORNEPAYNE CANADA

October 20, 1997 10 1997–42 I.R.B.

26 CFR 601.102: Classification of taxes col-lected by the Internal Revenue Serv i c e .(Also Part I, §4261.)

Rev. Proc. 97–46

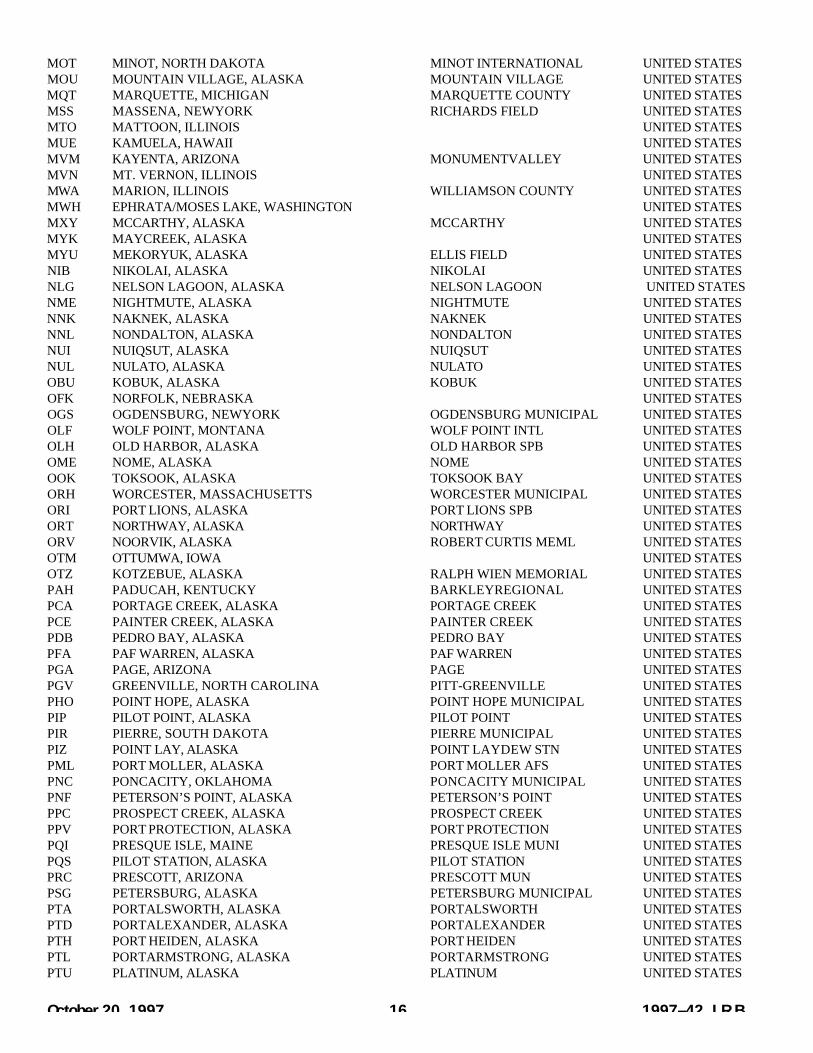

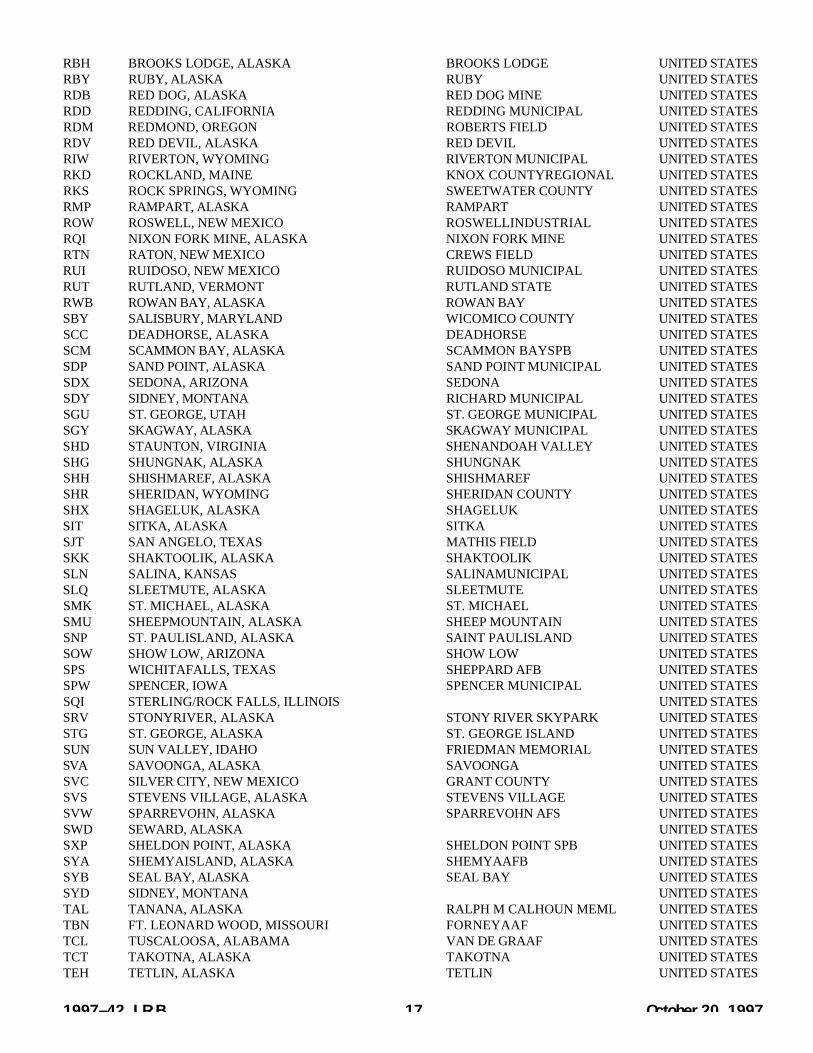

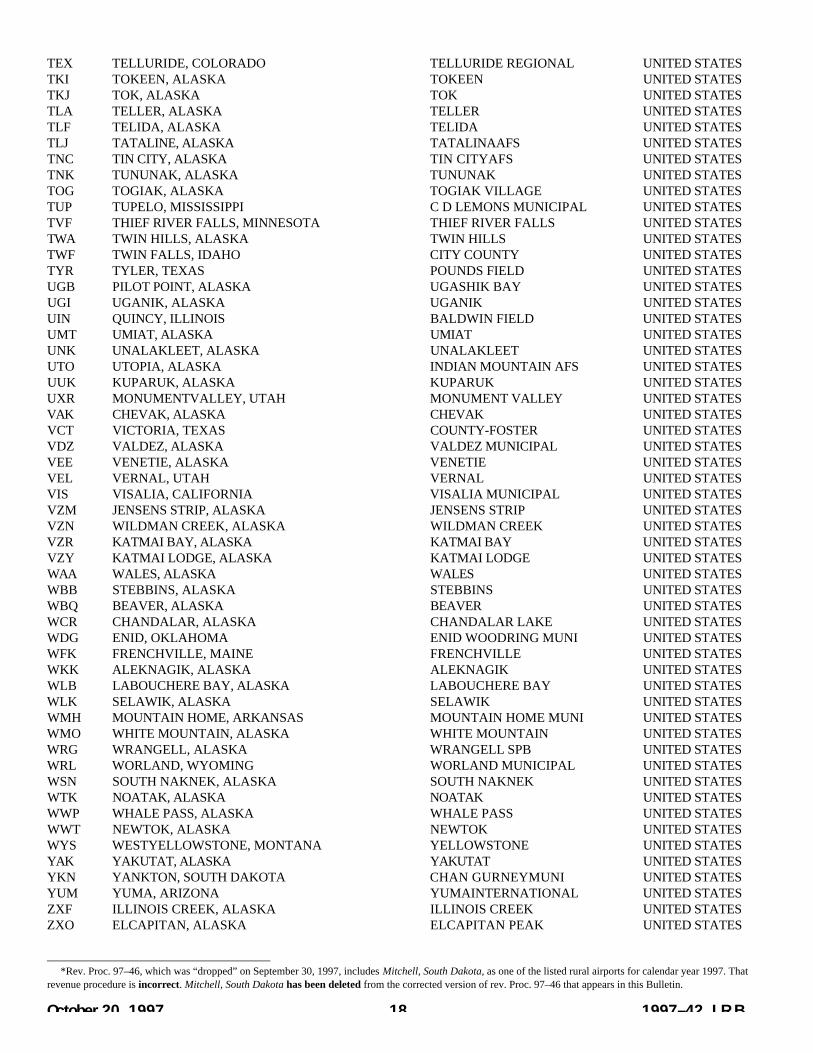

SECTION 1. PURPOSE

This revenue procedure provides a listof “rural airports” as that term is definedin § 4261(e)(1)(B) of the Internal Rev-enue Code, for purposes of computing thetax on air transportation. The revenueprocedure also provides guidance on howto calculate the tax in certain circum-stances.

SECTION 2. BACKGROUND

Section 1031 of the Taxpayer ReliefAct of 1997, Pub. L. No. 105–34, (theAct) extends and modifies the tax im-posed by § 4261 on amounts paid for thetransportation of persons by air. The newrules relating to domestic air transporta-tion apply to amounts paid after Septem-ber 30, 1997, for transportation beginningafter that date. The Act generally pro-vides a tax rate of 7.5 percent of theamount paid for taxable transportation.H o w e v e r, the rate is 9 percent for trans-portation beginning after September 30,

1997, and before October 1, 1998, and 8percent for transportation beginning afterSeptember 30, 1998, and before October1, 1999. The 7.5 percent rate is effectivefor transportation beginning after Septem-ber 30, 1999.

In addition, the Act subjects each do-mestic segment of taxable transportationto a segment tax. The initial tax rate is$1.00 per domestic segment for segmentsbeginning after September 30, 1997, andbefore October 1, 1998. The segment taxincreases to a fully phased in rate of $3.00per domestic segment for segments begin-ning during calendar year 2002. A f t e rcalendar year 2002, the $3.00 segment taxwill be indexed for inflation.

Transportation segments beginning orending at a rural airport are not subject tothe temporary 9 percent and 8 percentrates and are exempt from the segmenttax. Thus, transportation segments begin-ning or ending at a rural airport are sub-ject only to a 7.5 percent rate on theamount paid for the transportation seg-ments.

An airport is a rural airport, as definedin § 4261(e)(1)(B), for a calendar year if -

(i) fewer than 100,000 commercial pas-sengers departed by air during the secondpreceding calendar year from that airport,

and (ii) the airport is either (A) not located

within 75 miles of another airport fromwhich 100,000 or more commercial pas-sengers departed during the second pre-ceding calendar year, or (B) receiving es-sential air service subsidies as of August5, 1997.

SECTION 3. SCOPE

This revenue procedure lists, based oninformation supplied by the Office of A i r-line Information at the Department ofTransportation, airports that will be treatedas rural airports for calendar year 1997. Asubsequent revenue procedure will providea similar list of rural airports for calendaryear 1998. For calendar year 1997, the listin this revenue procedure may be reliedupon unless and until modified or super-seded by a subsequent revenue procedure.In addition, any airport not listed in thisrevenue procedure is, nevertheless, a ruralairport if it meets the requirements of §4261(e)(1)(B) set forth above.

SECTION 4. PROCEDURE

.01 The following airports will betreated as rural airports for calendar year1997:

Part III. Administrative, Procedural, and Miscellaneous

1997–42 I.R.B. 11 October 20, 1997

YIB ATIKOKAN, ONTARIO ATIKOKAN MUNICIPAL CANADAYIG BIG BAYMARINA, B.C. BIG BAY MARINA CANADAYKX KIRKLAND LAKE, ONTARIO KIRKLAND LAKE CANADAYLD CHAPLEAU, ONTARIO CHAPLEAU CANADAYML MURRAYBAY, QUEBEC CHARLEVOIX CANADAYMP PORT MCNEIL, B.C. PORT MCNEIL CANADAYNK NOOTKA SOUND, B.C. NOOTKA SOUND CANADAYPL PICKLE LAKE, ONTARIO PICKLE LAKE CANADAYQI YARMOUTH, NOVASCOTIA YARMOUTH CANADAYQK KENORA, ONTARIO KENORA CANADAYQL LETHBRIDGE, ALBERTA LETHBRIDGE CANADAYQQ COMOX, B.C. COMOX CANADAYQV YORKTON, SASK. YORKTON CANADAYRL RED LAKE, ONTARIO RED LAKE CANADAYSB SUDBURY, ONTARIO SUDBURY CANADAYSC SHERBROOKE, QUEBEC SHEREBROOKE CANADAYSJ ST. JOHN, N.B. SAINT JOHN CANADAYSP MARATHON, ONTARIO MARATHON CANADAYSZ SQUIRREL COVE, B.C. SQUIRRELCOVE CANADAYTA PEMBROKE ONTARIO PEMBROKE CANADAYTJ TERRACE BAY, ONTARIO TERRACE BAY CANADAYTP TOFINO, B.C. TOFINO SPB CANADAYTS TIMMINS, ONTARIO TIMMINS CANADAYVB BONAVENTURE, QUEBEC BONAVENTURE CANADAYWL WILLIAMS LAKE, B.C. WILLIAMS LAKE CANADAYWR WHITE RIVER, ONTARIO WHITE RIVER CANADAYXC CRANBROOK, B.C. CRANBROOK CANADAYXH MEDICINE HAT, ALBERTA MEDICINE HAT CANADAYXL SIOUX LOOKOUT, ONTARIO SIOUX LOOKOUT CANADAYXR EARLTON, ONTARIO EARLTON CANADAYXZ WAWA, ONTARIO WAWA CANADAYYB NORTH BAY, ONTARIO NORTH BAY CANADAYYG CHARLOTTETOWN, P.E.I. CHARLOTTETOWN CANADAYYU KAPUSKASING, ONTARIO KAPUSKASING CANADAYYY MONT JOLI, QUEBEC MONT JOLI CANADAYZT PORT HARDY, B.C. PORT HARDY CANADAYZV SEVEN ISLANDS, QUEBEC SEPT-ILES CANADABHL BAHIAANGELES MEXICOCVM CIUDAD VICTORIA, TAMAULIPAS MEXICOPDS PIEDRAS NEGRAS, COAHUILA MEXICOSFH SAN FELIPE MEXICOSNQ SAN QUINTIN MEXICOABI ABILENE, TEXAS ABILENE MUNICIPAL UNITED STATESABL AMBLER, ALASKA AMBLER RIVER UNITED STATESABR ABERDEEN, SOUTH DAKOTA ABERDEEN REGIONAL UNITED STATESABY ALBANY, GEORGIA DOUGHERTY COUNTY UNITED STATESACT WACO, TEXAS WACO MUNICIPAL UNITED STATESACV EUREKA/ARCATA, CALIFORNIA ARCATA UNITED STATESADK ADAK ISLAND, ALASKA ADAK ISLAND NS UNITED STATESADQ KODIAK, ALASKA METROPOLITAN AREA UNITED STATESAET ALLAKAKET, ALASKA ALLAKAKET UNITED STATESAEX ALEXANDRIA, LOUISIANA ENGLAND AFB UNITED STATESAFK ANDREAFSKI, ALASKA ANDREAFSKI UNITED STATESAIA ALLIANCE, NEBRASKA ALLIANCE MUNICIPAL UNITED STATESAIN WAINWRIGHT, ALASKA WAINWRIGHT UNITED STATESAKB ATKA, ALASKA ATKA UNITED STATESAKK AKHIOK, ALASKA AKHIOK SPB UNITED STATESAKN KING SALMON, ALASKA KING SALMON UNITED STATES

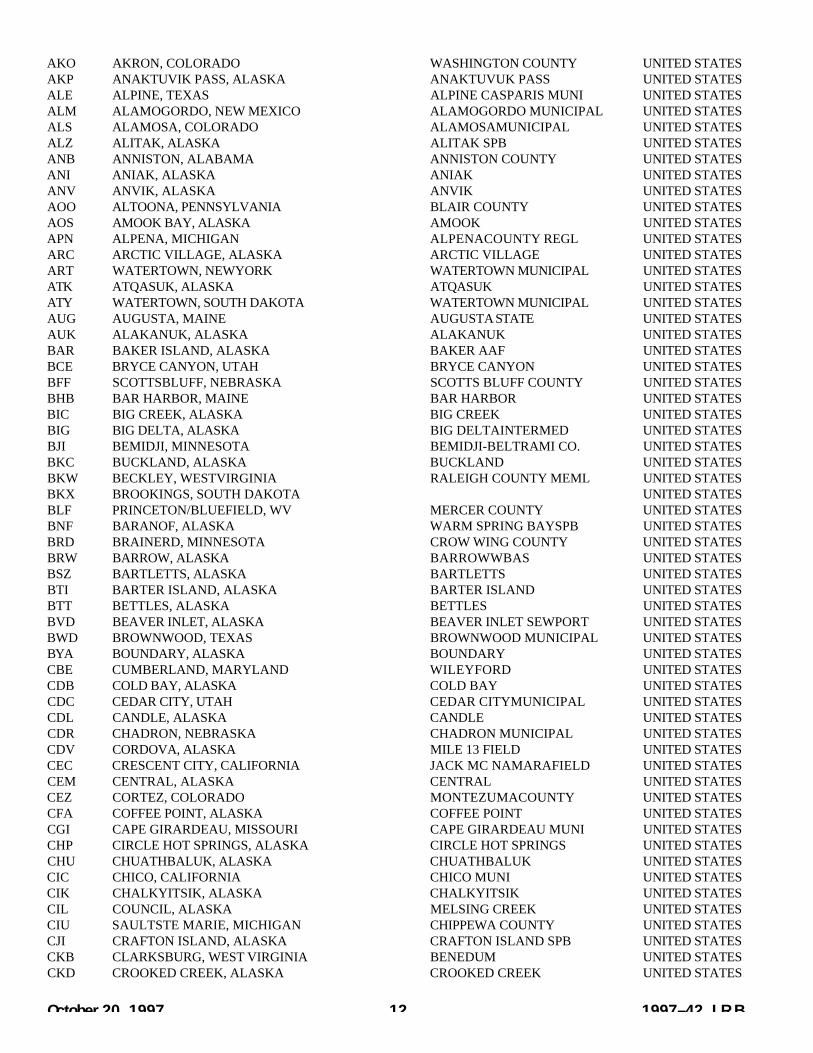

AKO AKRON, COLORADO WASHINGTON COUNTY UNITED STATESAKP ANAKTUVIK PASS, ALASKA ANAKTUVUK PASS UNITED STATESALE ALPINE, TEXAS ALPINE CASPARIS MUNI UNITED STATESALM ALAMOGORDO, NEW MEXICO ALAMOGORDO MUNICIPAL UNITED STATESALS ALAMOSA, COLORADO ALAMOSAMUNICIPAL UNITED STATESALZ ALITAK, ALASKA ALITAK SPB UNITED STATESANB ANNISTON, ALABAMA ANNISTON COUNTY UNITED STATESANI ANIAK, ALASKA ANIAK UNITED STATESANV ANVIK, ALASKA ANVIK UNITED STATESAOO ALTOONA, PENNSYLVANIA BLAIR COUNTY UNITED STATESAOS AMOOK BAY, ALASKA AMOOK UNITED STATESAPN ALPENA, MICHIGAN ALPENACOUNTY REGL UNITED STATESARC ARCTIC VILLAGE, ALASKA ARCTIC VILLAGE UNITED STATESART WATERTOWN, NEWYORK WATERTOWN MUNICIPAL UNITED STATESATK ATQASUK, ALASKA ATQASUK UNITED STATESATY WATERTOWN, SOUTH DAKOTA WATERTOWN MUNICIPAL UNITED STATESAUG AUGUSTA, MAINE AUGUSTA STATE UNITED STATESAUK ALAKANUK, ALASKA ALAKANUK UNITED STATESBAR BAKER ISLAND, ALASKA BAKER AAF UNITED STATESBCE BRYCE CANYON, UTAH BRYCE CANYON UNITED STATESBFF SCOTTSBLUFF, NEBRASKA SCOTTS BLUFF COUNTY UNITED STATESBHB BAR HARBOR, MAINE BAR HARBOR UNITED STATESBIC BIG CREEK, ALASKA BIG CREEK UNITED STATESBIG BIG DELTA, ALASKA BIG DELTAINTERMED UNITED STATESBJI BEMIDJI, MINNESOTA BEMIDJI-BELTRAMI CO. UNITED STATESBKC BUCKLAND, ALASKA BUCKLAND UNITED STATESBKW BECKLEY, WESTVIRGINIA RALEIGH COUNTY MEML UNITED STATESBKX BROOKINGS, SOUTH DAKOTA UNITED STATESBLF PRINCETON/BLUEFIELD, WV MERCER COUNTY UNITED STATESBNF BARANOF, ALASKA WARM SPRING BAYSPB UNITED STATESBRD BRAINERD, MINNESOTA CROW WING COUNTY UNITED STATESBRW BARROW, ALASKA BARROWWBAS UNITED STATESBSZ BARTLETTS, ALASKA BARTLETTS UNITED STATESBTI BARTER ISLAND, ALASKA BARTER ISLAND UNITED STATESBTT BETTLES, ALASKA BETTLES UNITED STATESBVD BEAVER INLET, ALASKA BEAVER INLET SEWPORT UNITED STATESBWD BROWNWOOD, TEXAS BROWNWOOD MUNICIPAL UNITED STATESBYA BOUNDARY, ALASKA BOUNDARY UNITED STATESCBE CUMBERLAND, MARYLAND WILEYFORD UNITED STATESCDB COLD BAY, ALASKA COLD BAY UNITED STATESCDC CEDAR CITY, UTAH CEDAR CITYMUNICIPAL UNITED STATESCDL CANDLE, ALASKA CANDLE UNITED STATESCDR CHADRON, NEBRASKA CHADRON MUNICIPAL UNITED STATESCDV CORDOVA, ALASKA MILE 13 FIELD UNITED STATESCEC CRESCENT CITY, CALIFORNIA JACK MC NAMARAFIELD UNITED STATESCEM CENTRAL, ALASKA CENTRAL UNITED STATESCEZ CORTEZ, COLORADO MONTEZUMACOUNTY UNITED STATESCFA COFFEE POINT, ALASKA COFFEE POINT UNITED STATESCGI CAPE GIRARDEAU, MISSOURI CAPE GIRARDEAU MUNI UNITED STATESCHP CIRCLE HOT SPRINGS, ALASKA CIRCLE HOT SPRINGS UNITED STATESCHU CHUATHBALUK, ALASKA CHUATHBALUK UNITED STATESCIC CHICO, CALIFORNIA CHICO MUNI UNITED STATESCIK CHALKYITSIK, ALASKA CHALKYITSIK UNITED STATESCIL COUNCIL, ALASKA MELSING CREEK UNITED STATESCIU SAULTSTE MARIE, MICHIGAN CHIPPEWA COUNTY UNITED STATESCJI CRAFTON ISLAND, ALASKA CRAFTON ISLAND SPB UNITED STATESCKB CLARKSBURG, WEST VIRGINIA BENEDUM UNITED STATESCKD CROOKED CREEK, ALASKA CROOKED CREEK UNITED STATES

October 20, 1997 12 1997–42 I.R.B.

1997–42 I.R.B. 13 October 20, 1997

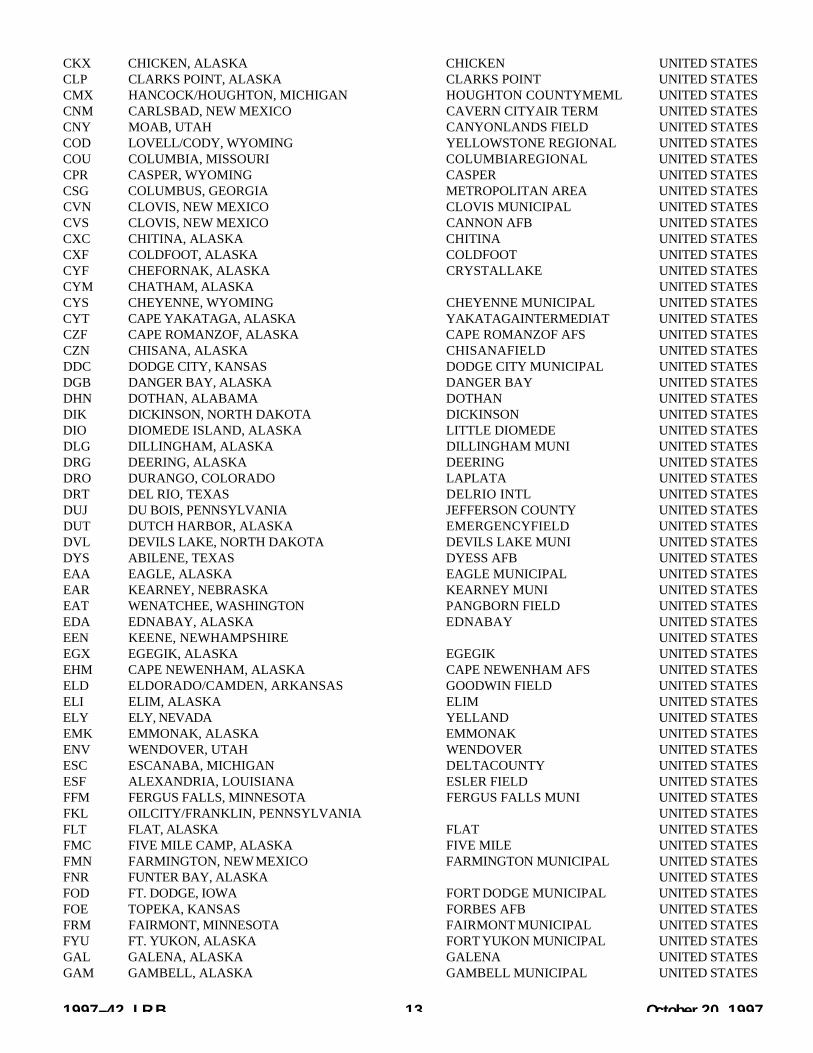

CKX CHICKEN, ALASKA CHICKEN UNITED STATESCLP CLARKS POINT, ALASKA CLARKS POINT UNITED STATESCMX HANCOCK/HOUGHTON, MICHIGAN HOUGHTON COUNTYMEML UNITED STATESCNM CARLSBAD, NEW MEXICO CAVERN CITYAIR TERM UNITED STATESCNY MOAB, UTAH CANYONLANDS FIELD UNITED STATESCOD LOVELL/CODY, WYOMING YELLOWSTONE REGIONAL UNITED STATESCOU COLUMBIA, MISSOURI COLUMBIAREGIONAL UNITED STATESCPR CASPER, WYOMING CASPER UNITED STATESCSG COLUMBUS, GEORGIA METROPOLITAN AREA UNITED STATESCVN CLOVIS, NEW MEXICO CLOVIS MUNICIPAL UNITED STATESCVS CLOVIS, NEW MEXICO CANNON AFB UNITED STATESCXC CHITINA, ALASKA CHITINA UNITED STATESCXF COLDFOOT, ALASKA COLDFOOT UNITED STATESCYF CHEFORNAK, ALASKA CRYSTALLAKE UNITED STATESCYM CHATHAM, ALASKA UNITED STATESCYS CHEYENNE, WYOMING CHEYENNE MUNICIPAL UNITED STATESCYT CAPE YAKATAGA, ALASKA YAKATAGAINTERMEDIAT UNITED STATESCZF CAPE ROMANZOF, ALASKA CAPE ROMANZOF AFS UNITED STATESCZN CHISANA, ALASKA CHISANAFIELD UNITED STATESDDC DODGE CITY, KANSAS DODGE CITY MUNICIPAL UNITED STATESDGB DANGER BAY, ALASKA DANGER BAY UNITED STATESDHN DOTHAN, ALABAMA DOTHAN UNITED STATESDIK DICKINSON, NORTH DAKOTA DICKINSON UNITED STATESDIO DIOMEDE ISLAND, ALASKA LITTLE DIOMEDE UNITED STATESDLG DILLINGHAM, ALASKA DILLINGHAM MUNI UNITED STATESDRG DEERING, ALASKA DEERING UNITED STATESDRO DURANGO, COLORADO LAPLATA UNITED STATESDRT DEL RIO, TEXAS DELRIO INTL UNITED STATESDUJ DU BOIS, PENNSYLVANIA JEFFERSON COUNTY UNITED STATESDUT DUTCH HARBOR, ALASKA EMERGENCYFIELD UNITED STATESDVL DEVILS LAKE, NORTH DAKOTA DEVILS LAKE MUNI UNITED STATESDYS ABILENE, TEXAS DYESS AFB UNITED STATESEAA EAGLE, ALASKA EAGLE MUNICIPAL UNITED STATESEAR KEARNEY, NEBRASKA KEARNEY MUNI UNITED STATESEAT WENATCHEE, WASHINGTON PANGBORN FIELD UNITED STATESEDA EDNABAY, ALASKA EDNABAY UNITED STATESEEN KEENE, NEWHAMPSHIRE UNITED STATESEGX EGEGIK, ALASKA EGEGIK UNITED STATESEHM CAPE NEWENHAM, ALASKA CAPE NEWENHAM AFS UNITED STATESELD ELDORADO/CAMDEN, ARKANSAS GOODWIN FIELD UNITED STATESELI ELIM, ALASKA ELIM UNITED STATESELY ELY, NEVADA YELLAND UNITED STATESEMK EMMONAK, ALASKA EMMONAK UNITED STATESENV WENDOVER, UTAH WENDOVER UNITED STATESESC ESCANABA, MICHIGAN DELTACOUNTY UNITED STATESESF ALEXANDRIA, LOUISIANA ESLER FIELD UNITED STATESFFM FERGUS FALLS, MINNESOTA FERGUS FALLS MUNI UNITED STATESFKL OILCITY/FRANKLIN, PENNSYLVANIA UNITED STATESFLT FLAT, ALASKA FLAT UNITED STATESFMC FIVE MILE CAMP, ALASKA FIVE MILE UNITED STATESFMN FARMINGTON, NEW MEXICO FARMINGTON MUNICIPAL UNITED STATESFNR FUNTER BAY, ALASKA UNITED STATESFOD FT. DODGE, IOWA FORT DODGE MUNICIPAL UNITED STATESFOE TOPEKA, KANSAS FORBES AFB UNITED STATESFRM FAIRMONT, MINNESOTA FAIRMONT MUNICIPAL UNITED STATESFYU FT. YUKON, ALASKA FORT YUKON MUNICIPAL UNITED STATESGAL GALENA, ALASKA GALENA UNITED STATESGAM GAMBELL, ALASKA GAMBELL MUNICIPAL UNITED STATES

GBD GREATBEND, KANSAS GREAT BEND MUNICIPAL UNITED STATESGBH GALBRAITH LAKE, ALASKA GALBRAITH LAKE UNITED STATESGCC GILLETTE, WYOMING CAMPBELL COUNTY UNITED STATESGCK GARDEN CITY, KANSAS GARDEN CITYMUNI UNITED STATESGDV GLENDIVE, MONTANA DAWSON COMMUNITY UNITED STATESGFB TOGIAK FISH, ALASKA TOGIAK FISH UNITED STATESGGW GLASGOW, MONTANA GLASGOW INTL UNITED STATESGKN GULKANA, ALASKA GULKANA UNITED STATESGLD GOODLAND, KANSAS RENNER FIELD UNITED STATESGLH GREENVILLE, MISSISSIPPI GREENVILLE MUNICIPAL UNITED STATESGLV GOLOVIN, ALASKA GOLOVIN UNITED STATESGMT GRANITE MOUNTAIN, ALASKA GRANITE MOUNTAIN UNITED STATESGNU GOODNEWS BAY, ALASKA GOODNEWS BAY UNITED STATESGRI GRAND ISLAND, NEBRASKA GRAND ISLAND AIR PK UNITED STATESGST GUSTAVUS, ALASKA GUSTAVUS UNITED STATESGTR COLUMBUS, MISSISSIPPI GOLDEN TRIANGLE REGL UNITED STATESGUP GALLUP, NEW MEXICO SENATOR CLARKE FIELD UNITED STATESHAY HAYCOCK, ALASKA HAYCOCK UNITED STATESHBH HOBART BAY, ALASKA HOBART BAY UNITED STATESHCR HOLY CROSS, ALASKA HOLY CROSS UNITED STATESHDN STEAMBOAT SPRINGS, COLORADO YAMPAVALLEY UNITED STATESHGZ HOGATZA, ALASKA HOGATZA UNITED STATESHII LAKE HAVASU CITY, ARIZONA LAKE HAVASU CTYMUNI UNITED STATESHKB HEALYLAKE, ALASKA HEALY LAKE UNITED STATESHOB HOBBS, NEW MEXICO LEACOUNTY UNITED STATESHON HURON, SOUTH DAKOTA W W HOWES MUNICIPAL UNITED STATESHOT HOT SPRINGS, ARKANSAS UNITED STATESHPB HOOPER BAY, ALASKA HOOPER BAY UNITED STATESHRO HARRISON, ARKANSAS BOONE COUNTY UNITED STATESHSI HASTINGS, NEBRASKA HASTINGS MUNICIPAL UNITED STATESHSL HUSLIA, ALASKA HUSLIA UNITED STATESHUS HUGHES, ALASKA HUGHES MUNICIPAL UNITED STATESHVR HAVRE, MONTANA HAVRE CITY-COUNTY UNITED STATESHYS HAYS, KANSAS HAYS MUNICIPAL UNITED STATESIAN KIANA, ALASKA BOB BARKER MEMORIAL UNITED STATESICY ICYBAY, ALASKA ICYBAY UNITED STATESIGG IGIUGIG, ALASKA IGIUGIG UNITED STATESIGM KINGMAN, ARIZONA KINGMAN MUNICIPAL UNITED STATESIKO NIKOLSKI, ALASKA NIKOLSKI AFS UNITED STATESILI ILIAMNA, ALASKA ILIAMNA UNITED STATESIMT IRON MOUNTAIN/KINGSFD, MICHIGAN FORD UNITED STATESINL INTERNATIONALFALLS, MINNESOTA FALLS INTERNATIONAL UNITED STATESIPL ELCENTRO, CALIFORNIA IMPERIALCOUNTY UNITED STATESIRC CIRCLE, ALASKA CIRCLE CITY UNITED STATESIRK KIRKSVILLE, MISSOURI KIRKSVILLE MUNICIPAL UNITED STATESISL ISABELPASS, ALASKA ISABELPASS UNITED STATESISN WILLISTON, NORTH DAKOTA SLOULIN FIELD INTL UNITED STATESIWD IRONWOOD, MICHIGAN GOGEBIC COUNTY UNITED STATESJBR JONESBORO, ARKANSAS UNITED STATESJMS JAMESTOWN, NORTH DAKOTA JAMESTOWN MUNICIPAL UNITED STATESKAE KAKE, ALASKA KAKE UNITED STATESKAL KALTAG, ALASKA KALTAG UNITED STATESKBC BIRCH CREEK, ALASKA BIRCH CREEK UNITED STATESKCG CHIGNIK FISHERIES, ALASKA CHIGNIK FISHERIES UNITED STATESKCL CHIGNIK LAGOON, ALASKA CHIGNIK LAGOON UNITED STATESKCN CHERNOFSKI, ALASKA CHERNOFSKI HARBOR UNITED STATESKCQ CHIGNIK, ALASKA CHIGNIK UNITED STATESKEK EKWOK, ALASKA EKWOK UNITED STATES

October 20, 1997 14 1997–42 I.R.B.

1997–42 I.R.B. 15 October 20, 1997

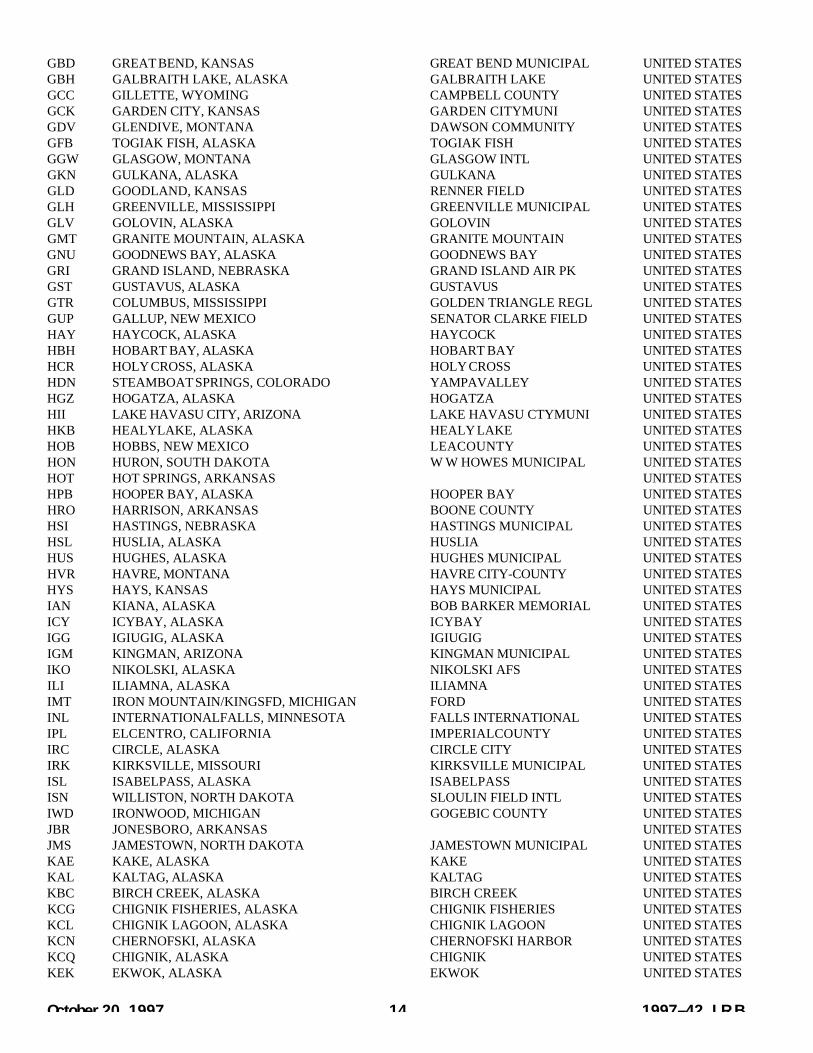

KFP FALSE PASS, ALASKA FALSE PASS UNITED STATESKGK KOLIGANEK, ALASKA NEW KOLIGANEK UNITED STATESKGX GRAYLING, ALASKA GRAYLING UNITED STATESKIB IVANOFF BAY, ALASKA IVANOF BAYSPB UNITED STATESKKA KOYUK, ALASKA KOYUK UNITED STATESKKB KITOI BAY, ALASKA KITOI BAYSPB UNITED STATESKKU EKUK, ALASKA EKUK UNITED STATESKLL LEVELOCK, ALASKA LEVELOCK UNITED STATESKLN LARSEN BAY, ALASKA LARSEN BAY SPB UNITED STATESKMO MANOKOTAK, ALASKA MANOKOTAK SPB UNITED STATESKMY MOSER BAY, ALASKA MOSER BAY UNITED STATESKNK KAKHONAK, ALASKA KAKHONAK UNITED STATESKNW NEWSTUYAHOK, ALASKA NEW STUYAHOK UNITED STATESKOT KOTLIK, ALASKA KOTLIK UNITED STATESKOY OLGABAY, ALASKA OLGABAYSPB UNITED STATESKOZ OUZINKIE, ALASKA OUZINKIE SPB UNITED STATESKPB POINT BAKER, ALASKA POINT BAKER SPB UNITED STATESKPC PORT CLARENCE, ALASKA PORT CLARENCE CGS UNITED STATESKPK PARKS, ALASKA PARKS SPB UNITED STATESKPN KIPNUK, ALASKA KIPNUK SPB UNITED STATESKPR PORT WILLIAMS, ALASKA PORTWILLIAMS SPB UNITED STATESKPV PERRYVILLE, ALASKA PERRYVILLE SPB UNITED STATESKPY PORT BAILEY, ALASKA PORT BAILEY SPB UNITED STATESKQA AKUTAN, ALASKA AKUTAN UNITED STATESKSM ST. MARY’S, ALASKA SAINT MARYS UNITED STATESKTS BREVIG MISSION, ALASKA BREVIG MISSION UNITED STATESKVC KING COVE, ALASKA KING COVE UNITED STATESKVL KIVALINA, ALASKA KIVALINA UNITED STATESKWK KWIGILLINGOK, ALASKA KWIGILLINGOK UNITED STATESKWP WEST POINT, ALASKA WEST POINT VILLAGE UNITED STATESKYK KARLUK, ALASKA KARLUK UNITED STATESKYU KOYUKUK, ALASKA KOYUKUK UNITED STATESKZB ZACHAR BAY, ALASKA ZACHAR BAY SPB UNITED STATESLAA LAMAR, COLORADO LAMAR FIELD UNITED STATESLAR LARAMIE, WYOMING GENERALBREES FIELD UNITED STATESLBF NORTH PLATTE, NEBRASKA LEE BIRD FIELD UNITED STATESLBL LIBERAL, KANSAS LIBERALMUNICIPAL UNITED STATESLMA MINCHUMINA, ALASKA MINCHUMINA UNITED STATESLPW LITTLE PORT WALTER, ALASKA LITTLE PORTWALTER UNITED STATESLRD LAREDO, TEXAS LAREDO INTL UNITED STATESLUR CAPE LISBURNE, ALASKA CAPE LISBURNE AFS UNITED STATESLVD LIME VILLAGE, ALASKA LIME VILLAGE UNITED STATESLWS LEWISTON, IDAHO NEZ PERCE COUNTY UNITED STATESLWT LEWISTOWN, MONTANA LEWISTOWN MUNICIPAL UNITED STATESMBL MANISTEE, MICHIGAN UNITED STATESMCE MERCED, CALIFORNIA MERCED MUNICIPAL UNITED STATESMCG MCGRATH, ALASKA MCGRATH UNITED STATESMCK MC COOK, NEBRASKA MC COOK MUNICIPAL UNITED STATESMCN MACON, GEORGIA LEWIS B WILSON UNITED STATESMDH CARBONDALE, ILLINOIS SOUTHERN ILLINOIS UNITED STATESMEI MERIDIAN, MISSISSIPPI KEY FIELD UNITED STATESMHK MANHATTAN/JCT.CTY/FT.RILEY, KANSAS MANHATTAN MUNICIPAL UNITED STATESMHM MINCHUMINA, ALASKA MINCHUMINA UNITED STATESMKT MANKATO, MINNESOTA UNITED STATESMLC MC ALESTER, OKLAHOMA MC ALESTER MUNICIPAL UNITED STATESMLS MILES CITY, MONTANA MILES CITYMUNICIPAL UNITED STATESMLY MANLEY HOTSPRINGS, ALASKA MANLEY HOTSPRINGS UNITED STATESMMH MAMMOTH LAKES, CALIFORNIA MAMMOTH LAKES UNITED STATES

MOT MINOT, NORTH DAKOTA MINOT INTERNATIONAL UNITED STATESMOU MOUNTAIN VILLAGE, ALASKA MOUNTAIN VILLAGE UNITED STATESMQT MARQUETTE, MICHIGAN MARQUETTE COUNTY UNITED STATESMSS MASSENA, NEWYORK RICHARDS FIELD UNITED STATESMTO MATTOON, ILLINOIS UNITED STATESMUE KAMUELA, HAWAII UNITED STATESMVM KAYENTA, ARIZONA MONUMENTVALLEY UNITED STATESMVN MT. VERNON, ILLINOIS UNITED STATESMWA MARION, ILLINOIS WILLIAMSON COUNTY UNITED STATESMWH EPHRATA/MOSES LAKE, WASHINGTON UNITED STATESMXY MCCARTHY, ALASKA MCCARTHY UNITED STATESMYK MAYCREEK, ALASKA UNITED STATESMYU MEKORYUK, ALASKA ELLIS FIELD UNITED STATESNIB NIKOLAI, ALASKA NIKOLAI UNITED STATESNLG NELSON LAGOON, ALASKA NELSON LAGOON UNITED STATESNME NIGHTMUTE, ALASKA NIGHTMUTE UNITED STATESNNK NAKNEK, ALASKA NAKNEK UNITED STATESNNL NONDALTON, ALASKA NONDALTON UNITED STATESNUI NUIQSUT, ALASKA NUIQSUT UNITED STATESNUL NULATO, ALASKA NULATO UNITED STATESOBU KOBUK, ALASKA KOBUK UNITED STATESOFK NORFOLK, NEBRASKA UNITED STATESOGS OGDENSBURG, NEWYORK OGDENSBURG MUNICIPAL UNITED STATESOLF WOLF POINT, MONTANA WOLF POINT INTL UNITED STATESOLH OLD HARBOR, ALASKA OLD HARBOR SPB UNITED STATESOME NOME, ALASKA NOME UNITED STATESOOK TOKSOOK, ALASKA TOKSOOK BAY UNITED STATESORH WORCESTER, MASSACHUSETTS WORCESTER MUNICIPAL UNITED STATESORI PORT LIONS, ALASKA PORT LIONS SPB UNITED STATESORT NORTHWAY, ALASKA NORTHWAY UNITED STATESORV NOORVIK, ALASKA ROBERT CURTIS MEML UNITED STATESOTM OTTUMWA, IOWA UNITED STATESOTZ KOTZEBUE, ALASKA RALPH WIEN MEMORIAL UNITED STATESPAH PADUCAH, KENTUCKY BARKLEYREGIONAL UNITED STATESPCA PORTAGE CREEK, ALASKA PORTAGE CREEK UNITED STATESPCE PAINTER CREEK, ALASKA PAINTER CREEK UNITED STATESPDB PEDRO BAY, ALASKA PEDRO BAY UNITED STATESPFA PAF WARREN, ALASKA PAF WARREN UNITED STATESPGA PAGE, ARIZONA PAGE UNITED STATESPGV GREENVILLE, NORTH CAROLINA PITT-GREENVILLE UNITED STATESPHO POINT HOPE, ALASKA POINT HOPE MUNICIPAL UNITED STATESPIP PILOT POINT, ALASKA PILOT POINT UNITED STATESPIR PIERRE, SOUTH DAKOTA PIERRE MUNICIPAL UNITED STATESPIZ POINT LAY, ALASKA POINT LAYDEW STN UNITED STATESPML PORT MOLLER, ALASKA PORT MOLLER AFS UNITED STATESPNC PONCACITY, OKLAHOMA PONCACITY MUNICIPAL UNITED STATESPNF PETERSON’S POINT, ALASKA PETERSON’S POINT UNITED STATESPPC PROSPECT CREEK, ALASKA PROSPECT CREEK UNITED STATESPPV PORT PROTECTION, ALASKA PORT PROTECTION UNITED STATESPQI PRESQUE ISLE, MAINE PRESQUE ISLE MUNI UNITED STATESPQS PILOT STATION, ALASKA PILOT STATION UNITED STATESPRC PRESCOTT, ARIZONA PRESCOTT MUN UNITED STATESPSG PETERSBURG, ALASKA PETERSBURG MUNICIPAL UNITED STATESPTA PORTALSWORTH, ALASKA PORTALSWORTH UNITED STATESPTD PORTALEXANDER, ALASKA PORTALEXANDER UNITED STATESPTH PORT HEIDEN, ALASKA PORT HEIDEN UNITED STATESPTL PORTARMSTRONG, ALASKA PORTARMSTRONG UNITED STATESPTU PLATINUM, ALASKA PLATINUM UNITED STATES

October 20, 1997 16 1997–42 I.R.B.

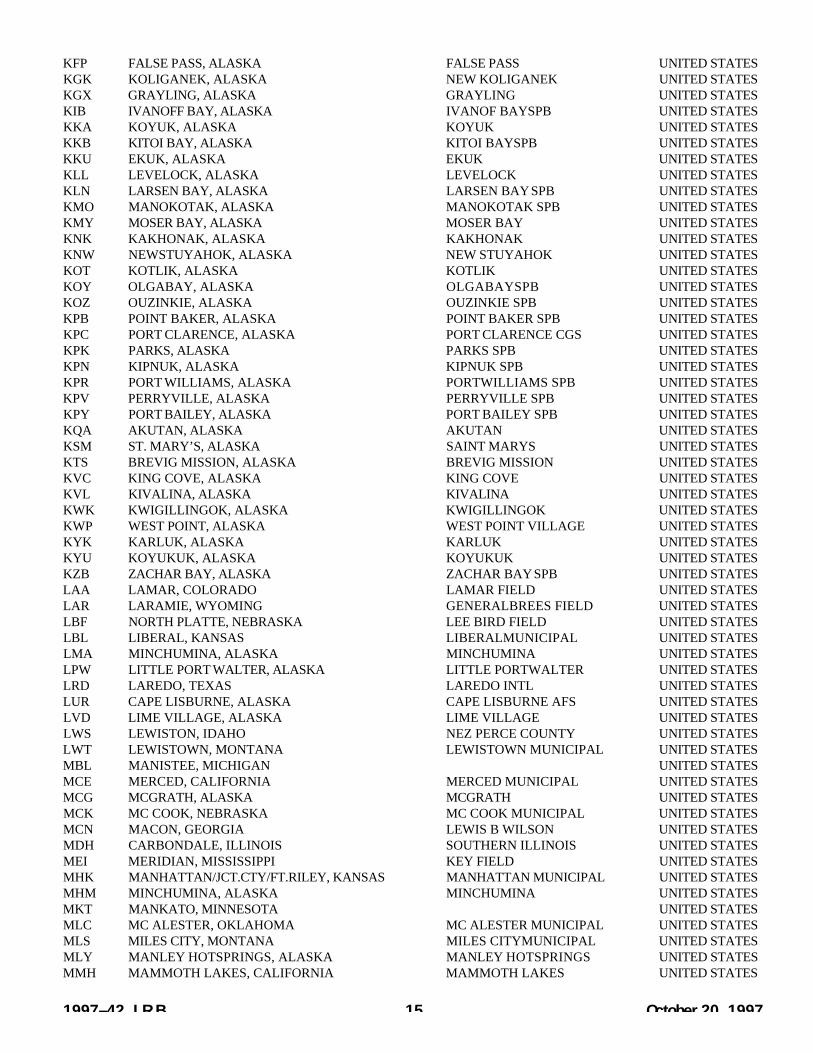

RBH BROOKS LODGE, ALASKA BROOKS LODGE UNITED STATESRBY RUBY, ALASKA RUBY UNITED STATESRDB RED DOG, ALASKA RED DOG MINE UNITED STATESRDD REDDING, CALIFORNIA REDDING MUNICIPAL UNITED STATESRDM REDMOND, OREGON ROBERTS FIELD UNITED STATESRDV RED DEVIL, ALASKA RED DEVIL UNITED STATESRIW RIVERTON, WYOMING RIVERTON MUNICIPAL UNITED STATESRKD ROCKLAND, MAINE KNOX COUNTYREGIONAL UNITED STATESRKS ROCK SPRINGS, WYOMING SWEETWATER COUNTY UNITED STATESRMP RAMPART, ALASKA RAMPART UNITED STATESROW ROSWELL, NEW MEXICO ROSWELLINDUSTRIAL UNITED STATESRQI NIXON FORK MINE, ALASKA NIXON FORK MINE UNITED STATESRTN RATON, NEW MEXICO CREWS FIELD UNITED STATESRUI RUIDOSO, NEW MEXICO RUIDOSO MUNICIPAL UNITED STATESRUT RUTLAND, VERMONT RUTLAND STATE UNITED STATESRWB ROWAN BAY, ALASKA ROWAN BAY UNITED STATESSBY SALISBURY, MARYLAND WICOMICO COUNTY UNITED STATESSCC DEADHORSE, ALASKA DEADHORSE UNITED STATESSCM SCAMMON BAY, ALASKA SCAMMON BAYSPB UNITED STATESSDP SAND POINT, ALASKA SAND POINT MUNICIPAL UNITED STATESSDX SEDONA, ARIZONA SEDONA UNITED STATESSDY SIDNEY, MONTANA RICHARD MUNICIPAL UNITED STATESSGU ST. GEORGE, UTAH ST. GEORGE MUNICIPAL UNITED STATESSGY SKAGWAY, ALASKA SKAGWAY MUNICIPAL UNITED STATESSHD STAUNTON, VIRGINIA SHENANDOAH VALLEY UNITED STATESSHG SHUNGNAK, ALASKA SHUNGNAK UNITED STATESSHH SHISHMAREF, ALASKA SHISHMAREF UNITED STATESSHR SHERIDAN, WYOMING SHERIDAN COUNTY UNITED STATESSHX SHAGELUK, ALASKA SHAGELUK UNITED STATESSIT SITKA, ALASKA SITKA UNITED STATESSJT SAN ANGELO, TEXAS MATHIS FIELD UNITED STATESSKK SHAKTOOLIK, ALASKA SHAKTOOLIK UNITED STATESSLN SALINA, KANSAS SALINAMUNICIPAL UNITED STATESSLQ SLEETMUTE, ALASKA SLEETMUTE UNITED STATESSMK ST. MICHAEL, ALASKA ST. MICHAEL UNITED STATESSMU SHEEPMOUNTAIN, ALASKA SHEEP MOUNTAIN UNITED STATESSNP ST. PAULISLAND, ALASKA SAINT PAULISLAND UNITED STATESSOW SHOW LOW, ARIZONA SHOW LOW UNITED STATESSPS WICHITAFALLS, TEXAS SHEPPARD AFB UNITED STATESSPW SPENCER, IOWA SPENCER MUNICIPAL UNITED STATESSQI STERLING/ROCK FALLS, ILLINOIS UNITED STATESSRV STONYRIVER, ALASKA STONY RIVER SKYPARK UNITED STATESSTG ST. GEORGE, ALASKA ST. GEORGE ISLAND UNITED STATESSUN SUN VALLEY, IDAHO FRIEDMAN MEMORIAL UNITED STATESSVA SAVOONGA, ALASKA SAVOONGA UNITED STATESSVC SILVER CITY, NEW MEXICO GRANT COUNTY UNITED STATESSVS STEVENS VILLAGE, ALASKA STEVENS VILLAGE UNITED STATESSVW SPARREVOHN, ALASKA SPARREVOHN AFS UNITED STATESSWD SEWARD, ALASKA UNITED STATESSXP SHELDON POINT, ALASKA SHELDON POINT SPB UNITED STATESSYA SHEMYAISLAND, ALASKA SHEMYAAFB UNITED STATESSYB SEAL BAY, ALASKA SEAL BAY UNITED STATESSYD SIDNEY, MONTANA UNITED STATESTAL TANANA, ALASKA RALPH M CALHOUN MEML UNITED STATESTBN FT. LEONARD WOOD, MISSOURI FORNEYAAF UNITED STATESTCL TUSCALOOSA, ALABAMA VAN DE GRAAF UNITED STATESTCT TAKOTNA, ALASKA TAKOTNA UNITED STATESTEH TETLIN, ALASKA TETLIN UNITED STATES

1997–42 I.R.B. 17 October 20, 1997

TEX TELLURIDE, COLORADO TELLURIDE REGIONAL UNITED STATESTKI TOKEEN, ALASKA TOKEEN UNITED STATESTKJ TOK, ALASKA TOK UNITED STATESTLA TELLER, ALASKA TELLER UNITED STATESTLF TELIDA, ALASKA TELIDA UNITED STATESTLJ TATALINE, ALASKA TATALINAAFS UNITED STATESTNC TIN CITY, ALASKA TIN CITYAFS UNITED STATESTNK TUNUNAK, ALASKA TUNUNAK UNITED STATESTOG TOGIAK, ALASKA TOGIAK VILLAGE UNITED STATESTUP TUPELO, MISSISSIPPI C D LEMONS MUNICIPAL UNITED STATESTVF THIEF RIVER FALLS, MINNESOTA THIEF RIVER FALLS UNITED STATESTWA TWIN HILLS, ALASKA TWIN HILLS UNITED STATESTWF TWIN FALLS, IDAHO CITY COUNTY UNITED STATESTYR TYLER, TEXAS POUNDS FIELD UNITED STATESUGB PILOT POINT, ALASKA UGASHIK BAY UNITED STATESUGI UGANIK, ALASKA UGANIK UNITED STATESUIN QUINCY, ILLINOIS BALDWIN FIELD UNITED STATESUMT UMIAT, ALASKA UMIAT UNITED STATESUNK UNALAKLEET, ALASKA UNALAKLEET UNITED STATESUTO UTOPIA, ALASKA INDIAN MOUNTAIN AFS UNITED STATESUUK KUPARUK, ALASKA KUPARUK UNITED STATESUXR MONUMENTVALLEY, UTAH MONUMENT VALLEY UNITED STATESVAK CHEVAK, ALASKA CHEVAK UNITED STATESVCT VICTORIA, TEXAS COUNTY-FOSTER UNITED STATESVDZ VALDEZ, ALASKA VALDEZ MUNICIPAL UNITED STATESVEE VENETIE, ALASKA VENETIE UNITED STATESVEL VERNAL, UTAH VERNAL UNITED STATESVIS VISALIA, CALIFORNIA VISALIA MUNICIPAL UNITED STATESVZM JENSENS STRIP, ALASKA JENSENS STRIP UNITED STATESVZN WILDMAN CREEK, ALASKA WILDMAN CREEK UNITED STATESVZR KATMAI BAY, ALASKA KATMAI BAY UNITED STATESVZY KATMAI LODGE, ALASKA KATMAI LODGE UNITED STATESWAA WALES, ALASKA WALES UNITED STATESWBB STEBBINS, ALASKA STEBBINS UNITED STATESWBQ BEAVER, ALASKA BEAVER UNITED STATESWCR CHANDALAR, ALASKA CHANDALAR LAKE UNITED STATESWDG ENID, OKLAHOMA ENID WOODRING MUNI UNITED STATESWFK FRENCHVILLE, MAINE FRENCHVILLE UNITED STATESWKK ALEKNAGIK, ALASKA ALEKNAGIK UNITED STATESWLB LABOUCHERE BAY, ALASKA LABOUCHERE BAY UNITED STATESWLK SELAWIK, ALASKA SELAWIK UNITED STATESWMH MOUNTAIN HOME, ARKANSAS MOUNTAIN HOME MUNI UNITED STATESWMO WHITE MOUNTAIN, ALASKA WHITE MOUNTAIN UNITED STATESWRG WRANGELL, ALASKA WRANGELL SPB UNITED STATESWRL WORLAND, WYOMING WORLAND MUNICIPAL UNITED STATESWSN SOUTH NAKNEK, ALASKA SOUTH NAKNEK UNITED STATESWTK NOATAK, ALASKA NOATAK UNITED STATESWWP WHALE PASS, ALASKA WHALE PASS UNITED STATESWWT NEWTOK, ALASKA NEWTOK UNITED STATESWYS WESTYELLOWSTONE, MONTANA YELLOWSTONE UNITED STATESYAK YAKUTAT, ALASKA YAKUTAT UNITED STATESYKN YANKTON, SOUTH DAKOTA CHAN GURNEYMUNI UNITED STATESYUM YUMA, ARIZONA YUMAINTERNATIONAL UNITED STATESZXF ILLINOIS CREEK, ALASKA ILLINOIS CREEK UNITED STATESZXO ELCAPITAN, ALASKA ELCAPITAN PEAK UNITED STATES

*Rev. Proc. 97–46, which was “dropped” on September 30, 1997, includes Mitchell, South Dakota, as one of the listed rural airports for calendar year 1997. Thatrevenue procedure is incorrect. Mitchell, South Dakota has been deleted from the corrected version of rev. Proc. 97–46 that appears in this Bulletin.

October 20, 1997 18 1997–42 I.R.B.

.02 Where transportation involves twoor more segments, at least one of whichbegins or ends at a rural airport and atleast one of which does not, the 7.5 per-cent rate is applied to the rural portion ofthe transportation and the nonrural rate isapplied to the nonrural portion. The ruralportion is determined by calculating thenumber of great circle miles in those seg-ments beginning or ending at rural air-ports and the total number of great circlemiles in all segments of the transporta-tion. The fraction formed by using thegreat circle miles of the rural portion asthe numerator and the total great circlemiles as the denominator is multiplied bythe amount paid for the transportation.The result is the portion of the totalamount paid that is subject to the 7.5 per-cent rate. The remaining portion of thetotal amount paid is subject to the non-rural rate. In addition, all segments notbeginning or ending at rural airports aresubject to the segment tax.

SECTION 5. EFFECTIVE DATE

This revenue procedure is effective foramounts paid after September 30, 1997,for transportation beginning after Septem-ber 30, 1997.

DRAFTING INFORMATION

The principal author of this revenueprocedure is Patrick S. Kirwan of the Of-fice of Assistant Chief Counsel (Pass-throughs and Special Industries). For fur-ther information regarding this revenueprocedure contact Mr. Kirwan at 202-622-3130 (not a toll-free call).

26 C.F.R. 601.602: Tax forms and instructions.(Also Part I, Sections 3504, 6011, 6061, 6071;31.3504–1, 31.6011(a)–7, 31.6061– , 301.6061–1,31.6071(a)–1.)

Rev. Proc. 97–47

Table of ContentsSECTION 1. PURPOSESECTION 2. BACKGROUND A N D

CHANGESSECTION 3. SCOPESECTION 4. DEFINITIONSSECTION 5. A P P L I C ATION FOR

THE FORM 941 ELFPROGRAM

SECTION 6. A C C E P TANCE IN T H EFORM 941 ELF PRO-GRAM

SECTION 7. ADDING AND DELET-ING TA X PAYERS ONTHE REPORT I N GAGENT’S L I S T

SECTION 8. ELECTRONIC FILINGOF FORM 941

SECTION 9. ADJUSTMENTS TOFORM 941

SECTION 10. RESPONSIBILITIES OFAN ELECTRONIC FILER

SECTION 11. A LT E R N ATIVE FILINGPROCEDURES

SECTION 12. REVISION OF COM-PUTER SPECIFICA-TIONS BY THE SER-VICE

SECTION 13. A D V E RTISING STA N-DARDS

SECTION 14. REASONS FOR SUS-PENSION

SECTION 15. A D M I N I S T R ATIVE RE-V I E W PROCESS FORPROPOSED SUSPEN-SION

SECTION 16. E F F E C T OF SUSPEN-SION

SECTION 17. A P P E A L OF SUSPEN-SION

SECTION 18. P E N A LT Y FOR FA I L-URE TO T I M E LY F I L EARETURN

SECTION 19. FILING FORMS W- 4WITH THE INTERNALREVENUE SERVICE

SECTION 20. FILING FORMS W – 2( C O P Y A) WITH T H ES O C I A L S E C U R I T YADMINISTRATION

SECTION 21. I N T E R N A L R E V E N U ESERVICE CONTACT

SECTION 22. E F F E C T ON OTHERDOCUMENTS

SECTION 23. EFFECTIVE DATESECTION 24. PA P E RWORK REDUC-

TION ACT

SECTION 1. PURPOSE

This revenue procedure sets forth therequirements of the Form 941 ELF Pro-gram under which a taxpayer that is a Re-porting Agent (“Agent” as defined in sec-tion 4.07 of this revenue procedure) mayelectronically file Form 941, Employer’sQuarterly Federal Tax Return. The tech-nical specifications for filing Form 941electronically are published separately inPublication 1855, Technical Specifica-tions Guide for the Electronic Filing Sys-

tem of Form 941, Employer’s QuarterlyFederal Tax Return. For further informa-tion, see Publication 1264, File Specicifi-cations, Process Criteria, and Record Lay-outs for Magnetic Tape Filing of Form941, Employer’s Quarterly Federal Ta xReturn. This revenue procedure ampli-fies, clarifies, modifies, and supersedesRev. Proc. 96–19, 1996–1 C.B. 644.

SECTION 2. BACKGROUND

.01 Section 6011(a) of the Internal Rev-enue Code provides that any person liablefor any tax imposed by this title, or for thecollection thereof, must make a return orstatement according to the forms and regu-lations prescribed by the Secretary. Everyperson required to make a return or state-ment must include therein the informationrequired by such forms or regulations.

.02 Section 31.6011(a)–4 of the Em-ployment Tax Regulations provides ingeneral that every person required tomake a return of income tax withheldfrom wages pursuant to § 3402 mustmake a return for the first calendar quarterin which the person is required to deductand withhold such tax and for each subse-quent calendar quarter until the personhas filed a final return. Except as other-wise provided, Form 941 is the form pre-scribed for making the return.

.03 Section 31.6011(a)–7 provides thateach return, together with any prescribedcopies or supporting data, must be filledin and disposed of in accordance with theforms, instructions, and regulations ap-plicable thereto. The return may be madeby an agent in the name of the person re-quired to make the return if an acceptablepower of attorney is filed with the InternalRevenue Service office with which suchperson is required to file returns and ifsuch a return includes all taxes required tobe reported by such person on such re-turn. Form 8655, Reporting Agent Autho-rization for Magnetic Tape/Electronic Fil-ers, is an acceptable power of attorney, ifprepared in accordance with the require-ments set forth in Rev. Proc. 96–17,1996–1 C.B. 633, as modified by section22.02 of this revenue procedure.

.04 Section 31.6061–1 provides that thereturn may be signed for the taxpayer byan agent that is fully authorized in accor-dance with § 31.6011(a)–7 to make suchreturn. An Agent may sign the Form 941on behalf of a taxpayer that has a validForm 8655 on file with the Service.

1997–42 I.R.B. 19 October 20, 1997

.05 Section 301.6061–1 of the Regula-tions on Procedure and A d m i n i s t r a t i o nprovides that the Secretary may prescribein forms, instructions, or other appropri-ate guidance the method for signing anyreturn, statement, or other document re-quired to be made under any provision ofthe internal revenue laws or regulations.The Service has prescribed in the elec-tronic filing instructions to Form 941 thatan electronically filed Form 941 is signedby the entry of the Electronic Filer’s Per-sonal Identification Number (“PIN”).

.06 Section 31.6071(a)–1 generallyprovides that each return required to bemade under § 31.6011(a)–1 for taxes im-posed by the Federal Insurance Contribu-tions Act, or required to be made under § 31.6011(a)–4 for withheld incometaxes, must be filed on or before the lastday of the first calendar month followingthe period for which it is made. However,under § 31.6071(a)–1 a return may befiled on or before the 10th day of the sec-ond calendar month following such pe-riod if timely deposits under § 6302(c)and the regulations thereunder have beenmade in full payment of such taxes duefor the period.

.07 Procedures for the magnetic filingof Form 941 are in Rev. Proc. 96–18,1996–1 C.B. 637, and the specificationsare in Publication 1264.

.08 The submission of federal tax de-posit (“FTD”) information on magnetictape is addressed in Rev. Proc. 89–48,1989–2 C.B. 599. For taxpayers that arerequired to make FTDs by electronicfunds transfer pursuant to § 6302(h), thesubmission of the FTD information alongwith the transfer of funds is addressed inRev. Proc. 97–33, 1997–30 I.R.B. 10.

.09 This revenue procedure updatesR e v. Proc. 96–19. The updates includechanges in the 941 ELF Program, clarifi-cations of prior Form 941 ELF Programstatements, and additional guidance de-rived from other Service documents thatrelate to the Form 941 ELF Program.Some of the updates are:

(1) the signature provisions for anelectronically filed Form 941 have beenmodified, amplified, and clarified to re-quire use of a PIN instead of filing a Form4996, Electronic/Magnetic Media FilingTransmittal for Wage and Wi t h h o l d i n gTax Returns (sections 2.05, 4.05, 5.02,6.06, 8.02, 10.02, 10.03, and 10.04);

(2) the definition of an ElectronicFiler:

(a) is prospectively limited to Re-porting Agents whose applications (re-ceived after the effective date of this rev-enue procedure) include an A g e n t ’s Listcontaining 10 or more taxpayers (sections4.02, 5.03, and 23.02); and

(b) has been expanded to includeSoftware Developers (sections 4.02, 5.02,5.04, 6.04, 6.05, and 10.05); and

(3) a Reporting Agent is not requiredto replace a previously submitted Autho-rization under certain circumstances (sec-tion 5.05).

SECTION 3. SCOPE

.01 The Form 941 ELF Program ac-cepts electronically filed Forms 941 inElectronic Data Interchange (“EDI”) for-mat developed by the American NationalStandards Institute that meets the require-ments of this revenue procedure and Pub-lication 1855.

.02 An Electronic Filer in the Form 941ELF Program must use asynchronouscommunications protocols to transmitelectronic returns. See Publication 1855for further information regarding commu-nications and formatting requirements.

.03 The Form 941 ELF Program ac-cepts timely current returns that are zerobalance, refund, or limited balance due re-turns. For the current limitations on bal-ance due returns, refer to Publication1855. For the due dates of returns underthe Form 941 ELF Program, see section8.01 of this revenue procedure. The Form941 ELF Program will not accept theelectronic filing of the following returns:

(1) amended returns;(2) corrected returns;(3) returns containing attachments;

or(4) untimely returns.

A violation of any of these restrictionswill cause a Processing Interruption (asdefined in section 4.06 of this revenueprocedure).

SECTION 4. DEFINITIONS

.01 Authorized Signatory. The “Autho-rized Signatory” is the person who is au-thorized to use the PIN for returns filed byan Electronic Filer under the Form 941ELF Program or during software develop-ment testing.