bulletin no. 2004-22 highlights of this issueannouncement 2004–48, page 998. this announcement...

TRANSCRIPT

Bulletin No. 2004-22June 1, 2004

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Ct. D. 2079, page 978.Tax assessment; partnership. The Supreme Court holdsthat the proper assessment against the partnership suffices toextend the statute of limitations to collect the tax in a judicialproceeding from the general partners who are liable for thepayment of the partnership’s debts. United States v. Gallettiet al.

Rev. Rul. 2004–45, page 971.Health Savings Account (HSA) – interaction with otherhealth arrangements. This ruling addresses the interactionbetween Health Savings Accounts (HSAs), health flexible spend-ing arrangements (health FSAs), and health reimbursement ar-rangements (HRAs).

Rev. Rul. 2004–52, page 973.Credit card annual fees. This ruling holds that credit cardannual fees are not interest for federal income tax purposes.Moreover, the ruling holds that credit card annual fees are in-cludible in the gross income by the card issuer when they be-come due and payable by cardholders under the terms of thecredit card agreements.

Notice 2004–39, page 982.This notice explains how the changes to section 1(h) of theCode made by the Jobs and Growth Tax Relief ReconciliationAct of 2003 (JGTRRA) apply to capital gain dividends paid (oraccounted for as if paid) by regulated investment companies(RICs) and real estate investment trusts (REITs) in taxable yearsthat end on or after May 6, 2003.

Rev. Proc. 2004–31, page 986.Changes in method of accounting for transfers to trustsunder section 461(f). This document provides proceduresfor taxpayers to change their method of accounting for deduct-ing under section 461(f) of the Code amounts transferred totrusts in transactions described in Notice 2003–77, 2003–49I.R.B. 1182.

Rev. Proc. 2004–32, page 988.This document provides automatic consent procedures for tax-payers to change their method of accounting to a method thatcomplies with Rev. Rul. 2004–52, in this Bulletin, or to the Rat-able Inclusion Method for Credit Card Annual Fees described inthis revenue procedure. Rev. Proc. 2002–9 modified and am-plified.

Rev. Proc. 2004–33, page 989.This procedure describes conditions under which the Commis-sioner will allow a taxpayer to treat its income from credit cardlate fees as interest income on a pool of credit card loans. Thisdocument also provides automatic consent procedures for ataxpayer to change its method of accounting for credit cardlate fee income to a method that treats these fees as interestthat creates or increases the amount of OID on a pool of creditcard loans to which the fees relate. Rev. Proc. 2002–9 modi-fied and amplified.

EXEMPT ORGANIZATIONS

Rev. Rul. 2004–51, page 974.Joint ventures. This ruling illustrates the tax consequencesfor a section 501(c)(3) organization that enters into a joint ven-ture with a for-profit organization as an insubstantial part of itsactivities.

(Continued on the next page)

Announcements of Disbarments and Suspensions begin on page 1001.Finding Lists begin on page ii.

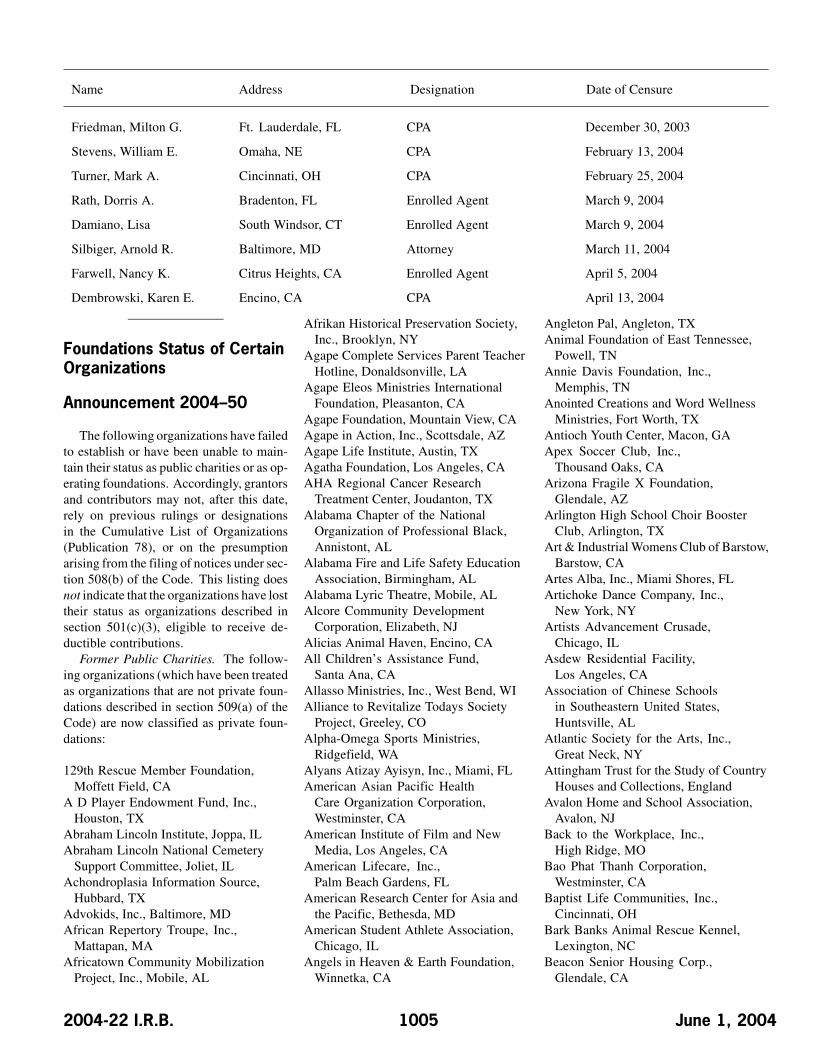

Announcement 2004–50, page 1005.A list is provided of organizations now classified as private foun-dations.

ADMINISTRATIVE

Rev. Rul. 2004–50, page 977.Indian tribal government. This ruling provides clarificationwith regard to an Indian tribal government’s ability to qualifyas an eligible shareholder under section 1361 of the Code.Specifically, the ruling explains that a federally recognized In-dian tribal government does not qualify as a permissible S cor-poration shareholder under section 1361(b)(1)(B) because it isnot treated as an individual subject to individual income taxesunder section 1 of the Code. The ruling also explains that a fed-erally recognized Indian Tribe cannot qualify as a permissible Scorporation shareholder under section 1361(c)(6) because it isneither a section 501(c)(3) organization, nor a section 401(a)qualified plan, profit-sharing, or stock bonus plan organization.

Rev. Proc. 2004–28, page 984.This procedure provides guidance to regulated investmentcompanies (RICs) who must comply with the asset diversifi-cation rules of section 851(b)(3) of the Code. The proceduredescribes conditions under which a RIC may look througha repurchase agreement (repo) to government securitiesserving as the underlying collateral to treat itself as the ownerof the government securities for purposes of these rules.The procedure is effective for repos held by a RIC on or afterAugust 15, 2001.

Rev. Proc. 2004–34, page 991.This procedure provides a method of accounting under whichtaxpayers using an accrual method of accounting may defer in-cluding all or part of certain advance payments in gross incomeuntil the year after the year the payment is received. Rev. Proc.71–21 modified and superseded and Rev. Proc. 2002–9 mod-ified and amplified.

Announcement 2004–48, page 998.This announcement provides background information relatingto Rev. Proc. 2004–34 in this Bulletin. Rev. Proc. 2004–34provides a method of accounting under which taxpayers usingan accrual method of accounting may defer including all or partof certain advance payments in gross income until the yearafter the year the payment is received.

June 1, 2004 2004-22 I.R.B.

The IRS MissionProvide America’s taxpayers top quality service by helpingthem understand and meet their tax responsibilities and by

applying the tax law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly and may be obtained from theSuperintendent of Documents on a subscription basis. Bulletincontents are compiled semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, mod-ify, or amend any of those previously published in the Bulletin.All published rulings apply retroactively unless otherwise indi-cated. Procedures relating solely to matters of internal man-agement are not published; however, statements of internalpractices and procedures that affect the rights and duties oftaxpayers are published.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpayersor technical advice to Service field offices, identifying detailsand information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,

court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautionedagainst reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions and Other Related Items, and Subpart B, Leg-islation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Sec-retary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative indexfor the matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

2004-22 I.R.B. June 1, 2004

Part I. Rulings and Decisions Under the Internal Revenue Codeof 1986Section 61.—Gross IncomeDefined

Rev. Rul. 2004-52 holds that credit card annualfees are not interest for federal income tax purposes.Moreover, the ruling holds that credit card annual feesare includible in the gross income by the card issuerwhen they become due and payable by cardholdersunder the terms of the credit card agreements. SeeRev. Rul. 2004-52, page 973.

Section 223.—HealthSavings Accounts

Health Savings Account (HSA) –interaction with other health arrange-ments. This ruling addresses the inter-action between Health Savings Accounts(HSAs), health flexible spending arrange-ments (health FSAs), and health reim-bursement arrangements (HRAs).

Rev. Rul. 2004–45

ISSUE

In the situations described below, mayan individual make contributions to aHealth Savings Account (HSA) under sec-tion 223 of the Internal Revenue Code ifthe individual is covered by a high de-ductible health plan (HDHP) and alsocovered by a health flexible spendingarrangement (health FSA) or a health re-imbursement arrangement (HRA)?

FACTS

Situation 1. An individual is coveredby an HDHP (as defined under section223(c)(2)(A)). The HDHP has an 80/20percent coinsurance feature above thedeductible. The individual is also cov-ered by a health FSA under a section 125cafeteria plan and an HRA that meets therequirements of Notice 2002–45, 2002–2C.B. 93. The health FSA and HRA pay orreimburse all section 213(d) medical ex-penses that are not covered by the HDHP(such as co-payments, coinsurance, ex-penses not covered due to the deductibleand other medical expenses not coveredby the HDHP). The health FSA and HRAcoordinate the payment of benefits underthe ordering rules of Notice 2002–45. The

individual is not entitled to benefits underMedicare and may not be claimed as adependent on another person’s tax return.

Situation 2. Same facts as Situation1, except that the health FSA and HRAare limited-purpose arrangements that payor reimburse, pursuant to the written plandocument, only vision and dental expenses(whether or not the minimum annual de-ductible of the HDHP has been satisfied).In addition, the health FSA and HRA payor reimburse preventive care benefits asdescribed in Notice 2004–23, 2004–15I.R.B. 725.

Situation 3. Same facts as Situation 1,except that the individual is not coveredby a health FSA. Under the employer’sHRA, the individual elects, before the be-ginning of the HRA coverage period, toforgo the payment or reimbursement ofmedical expenses incurred during that cov-erage period. The decision to forgo thepayment or reimbursement of medical ex-penses does not apply to permitted insur-ance, permitted coverage and preventivecare (“excepted medical expenses”). Seesection 223(c)(1)(B) and Notice 2004–23.Medical expenses incurred during the sus-pended HRA coverage period (other thanthe excepted medical expenses if other-wise allowed to be paid or reimbursed byan HRA), cannot be paid or reimbursedby the HRA currently or later (i.e., afterthe HRA suspension ends). However, theemployer decides to continue to make em-ployer contributions to the HRA during thesuspension period and thus the maximumavailable amount under the HRA is not af-fected by the suspension but is availablefor the payment or reimbursement of theexcepted medical expenses incurred dur-ing the suspension period as well as medi-cal expenses incurred in later HRA cover-age periods.

Situation 4. Same facts as Situation1, except that the health FSA and HRAare post-deductible arrangements that onlypay or reimburse medical expenses (in-cluding the individual’s 20 percent coin-surance responsibility for expenses abovethe deductible) after the minimum annualdeductible of the HDHP has been satisfied.

Situation 5. Same facts as Situation 1,except that the individual is not covered

by a health FSA. The employer’s HRAis a retirement HRA that only reimbursesthose medical expenses incurred after theindividual retires.

LAW AND ANALYSIS

Section 223(a) allows a deduction forcontributions to an HSA for an “eligibleindividual” for any month during the tax-able year. Section 223(c)(1)(A) providesthat an “eligible individual” means, withrespect to any month, any individual whois covered under an HDHP on the first dayof such month and is not, while coveredunder an HDHP, “covered under any healthplan which is not a high deductible healthplan, and which provides coverage for anybenefit which is covered under the high de-ductible health plan.”

Section 223(b) provides a limit onamounts that can be contributed to anHSA. The maximum annual contribu-tion limit for an eligible individual withself-only coverage is the amount requiredby section 223(b)(2)(A). The maximumannual contribution limit for an eligibleindividual with family coverage is theamount required by section 223(b)(2)(B).

Section 223(c)(2)(A) defines an HDHPas a health plan that satisfies certain re-quirements with respect to minimumannual deductibles and maximum annualout-of-pocket expenses. Generally, if sub-stantially all of the coverage in a healthplan that is intended to be an HDHP isprovided through a health FSA or HRA,the health plan is not an HDHP.

In addition to coverage under an HDHP,section 223(c)(1)(B) provides that an eligi-ble individual may have specifically enu-merated coverage that is disregarded forpurposes of the deductible. Coverage thatmay be disregarded includes “permittedinsurance” and other specified coverage(“permitted coverage”). “Permitted insur-ance” is coverage under which substan-tially all of the coverage provided relatesto liabilities incurred under workers’ com-pensation laws, tort liabilities, liabilitiesrelating to ownership or use of property, in-surance for a specified disease or illness,and insurance that pays a fixed amountper day (or other period) of hospitalization.

2004-22 I.R.B. 971 June 1, 2004

“Permitted coverage” (whether through in-surance or otherwise) is coverage for acci-dents, disability, dental care, vision care orlong-term care. Section 223(c)(2)(C) alsoprovides a safe harbor for the absence ofa preventive care deductible. See Notice2004–23.

The legislative history of section 223explains these provisions by stating that“eligible individuals for HSAs are individ-uals who are covered by a high deductiblehealth plan and no other health plan thatis not a high deductible health plan.” Thelegislative history also explains that, “[a]nindividual with other coverage in additionto a high deductible health plan is still el-igible for an HSA if such other coverageis certain permitted insurance or permit-ted coverage.” H.R. Conf. Rep. No. 391,108th Cong., 1st Sess. 841 (2003).

Section 125(a) states that no amountwill be included in the gross income of aparticipant in a cafeteria plan solely be-cause, under the plan, the participant maychoose among the benefits of the plan.Section 125(d) defines a cafeteria plan as awritten plan under which participants maychoose among two or more benefits con-sisting of cash and qualified benefits.

Section 125(f) defines qualified bene-fits as any benefit not included in the grossincome of the employee by reason of anexpress provision in the Code. Qualifiedbenefits include employer-provided acci-dent and health coverage under section106, including health FSAs.

Notice 2002–45, 2002–2 C.B. 93, de-scribes the tax treatment of HRAs. Thenotice explains that an HRA that receivestax-favored treatment is an arrangementthat is paid for solely by the employer andnot pursuant to a salary reduction elec-tion under section 125, reimburses the em-ployee for medical care expenses incurredby the employee and by the employee’sspouse and dependents, and provides reim-bursement up to a maximum dollar amountwith any unused portion of that amount atthe end of the coverage period carried for-ward to subsequent coverage periods.

Notice 2002–45, Part IV, states that if anemployer provides an HRA in conjunctionwith another accident or health plan andthat other plan is provided pursuant to asalary reduction election under a cafeteriaplan, then all the facts and circumstancesare considered in determining whether thesalary reduction is attributable to the HRA.

An accident or health plan funded pursuantto salary reduction is not an HRA and issubject to the rules under section 125.

Under section 223, an eligible individ-ual cannot be covered by a health plan thatis not an HDHP unless that health planprovides permitted insurance, permittedcoverage or preventive care. A healthFSA and an HRA are health plans andconstitute other coverage under section223(c)(1)(A)(ii). Consequently, an indi-vidual who is covered by an HDHP anda health FSA or HRA that pays or reim-burses section 213(d) medical expensesis generally not an eligible individual forthe purpose of making contributions to anHSA. See Rev. Rul. 2004–38, 2004–15I.R.B. 717, which holds that an individualwho is covered by an HDHP that does notprovide prescription drug coverage anda separate prescription drug plan or riderthat provides benefits before the minimumannual deductible of the HDHP has beensatisfied is not an eligible individual forHSA purposes.

However, an individual is an eligible in-dividual for the purpose of making contri-butions to an HSA for periods the individ-ual is covered under the following arrange-ments:

Limited-Purpose Health FSA or HRA.A limited-purpose health FSA that paysor reimburses benefits for “permitted cov-erage” (but not through insurance or forlong-term care services) and a limited-pur-pose HRA that pays or reimburses bene-fits for “permitted insurance” (for a spe-cific disease or illness or that provides afixed amount per day (or other period) ofhospitalization) or “permitted coverage”(but not for long-term care services). Inaddition, the limited-purpose health FSAor HRA may pay or reimburse preventivecare benefits. The individual is an eligibleindividual for the purpose of making con-tributions to an HSA because these ben-efits may be provided whether or not theHDHP deductible has been satisfied.

Suspended HRA. A suspended HRA,pursuant to an election made before thebeginning of the HRA coverage period,that does not pay or reimburse, at anytime, any medical expense incurred dur-ing the suspension period except preven-tive care, permitted insurance and permit-ted coverage (if otherwise allowed to bepaid or reimbursed by the HRA). The indi-vidual is an eligible individual for the pur-

pose of making contributions to an HSA.When the suspension period ends, the in-dividual is no longer an eligible individ-ual because the individual is again entitledto receive payment or reimbursement ofsection 213(d) medical expenses from theHRA. An individual who does not forgothe payment or reimbursement of medicalexpenses incurred during an HRA cover-age period, is not an eligible individual forHSA purposes during that HRA coverageperiod.

If an HSA is funded through salary re-duction under a cafeteria plan during thesuspension period, the terms of the salaryreduction election must indicate that thesalary reduction is used only to pay for theHSA offered in conjunction with the HRAand not to pay for the HRA itself. Thus,the mere fact that an individual participatesin an HSA funded pursuant to a salary re-duction election does not necessarily re-sult in attributing the salary reduction tothe HRA.

Post-Deductible Health FSA or HRA. Apost-deductible health FSA or HRA thatdoes not pay or reimburse any medical ex-pense incurred before the minimum annualdeductible under section 223(c)(2)(A)(i) issatisfied. The individual is an eligible in-dividual for the purpose of making con-tributions to the HSA. The deductible forthe HRA or health FSA (“other coverage”)need not be the same as the deductible forthe HDHP, but in no event may the HDHPor other coverage provide benefits beforethe minimum annual deductible under sec-tion 223(c)(2)(A)(i) is satisfied. Where theHDHP and the other coverage do not haveidentical deductibles, contributions to theHSA are limited to the lower of the de-ductibles. In addition, although the de-ductibles of the HDHP and the other cover-age may be satisfied independently by sep-arate expenses, no benefits may be paid be-fore the minimum annual deductible undersection 223(c)(2)(A)(i) has been satisfied.

Retirement HRA. A retirement HRAthat pays or reimburses only those medicalexpenses incurred after retirement (andno expenses incurred before retirement).In this case, the individual is an eligibleindividual for the purpose of making con-tributions to the HSA before retirementbut loses eligibility for coverage periodswhen the retirement HRA may pay or re-imburse section 213(d) medical expenses.Thus, after retirement, the individual is

June 1, 2004 972 2004-22 I.R.B.

no longer an eligible individual for thepurpose of the HSA.

In the arrangements described, the in-dividual does not fail to be an eligible in-dividual under section 223 and may con-tribute to an HSA. In addition, combina-tions of these arrangements which are con-sistent with these requirements would notdisqualify an individual from being an el-igible individual. For example, if an em-ployer offers a combined post-deductiblehealth FSA and a limited-purpose healthFSA, this would not disqualify an other-wise eligible individual from contributingto an HSA.

An individual may not be reimbursedfor the same medical expense by more thanone plan or arrangement. However, if theindividual has available an HSA, a healthFSA and an HRA that pay or reimburse thesame medical expense, the health FSA orthe HRA may pay or reimburse the med-ical expense, subject to the ordering rulesin Notice 2002–45, Part V, so long as theindividual certifies to the employer that theexpense has not been reimbursed and thatthe individual will not seek reimbursementunder any other plan or arrangement cov-ering that expense (including the HSA).

HOLDINGS

In Situation 1, the individual is cov-ered by an HDHP and by a health FSAand HRA that pay or reimburse medi-cal expenses incurred before the min-imum annual deductible under section223(c)(2)(A)(i) has been satisfied. Thehealth FSA and HRA pay or reimbursemedical expenses that are not limited tothe exceptions for permitted insurance,permitted coverage or preventive care.As a result, the individual is not an eligi-ble individual for the purpose of makingcontributions to an HSA. This result isthe same if the individual is covered bya health FSA or HRA sponsored by theemployer of the individual’s spouse. See,Rev. Rul. 2004–38.

In Situation 2, the individual is cov-ered by an HDHP and by a health FSAand HRA that pay or reimburse medi-cal expenses incurred before the min-imum annual deductible under section223(c)(2)(A)(i) has been satisfied. How-ever, the medical expenses paid or reim-bursed by the health FSA and HRA includeonly vision and dental benefits (which are

permitted coverage) and preventive care.All of these benefits may be covered asa separate health plan, as a separate oroptional rider, or as part of the HDHP andwhether or not the minimum annual de-ductible under section 223(c)(2)(A)(i) hasbeen satisfied. The individual is an eligi-ble individual for the purpose of makingcontributions to an HSA.

In Situation 3, the individual elects toforgo the payment or reimbursement ofmedical expenses incurred during an HRAcoverage period. The suspension of pay-ments and reimbursements by the HRAdoes not apply to permitted insurance, per-mitted coverage and preventive care (ifotherwise allowed to be paid or reimbursedby the HRA). The individual is an eligibleindividual for the purpose of making con-tributions to an HSA until the suspensionperiod ends and the individual is again en-titled to receive, from the HRA, paymentsor reimbursements of section 213(d) med-ical expenses incurred after the suspensionperiod.

In Situation 4, the health FSA and HRApay or reimburse medical expenses (in-cluding the 20 percent coinsurance not oth-erwise covered by the HDHP) only afterthe HDHP’s minimum annual deductiblehas been satisfied. The individual is an el-igible individual for the purpose of makingcontributions to an HSA.

In Situation 5, the HRA is a retirementHRA that only pays or reimburses medi-cal expenses incurred after the individualretires. The individual is an eligible indi-vidual for the purpose of making contribu-tions to an HSA before retirement becausethe HRA will pay or reimburse only med-ical expenses incurred after retirement.

Drafting Information

The principal author of this noticeis Shoshanna Tanner of the Office ofDivision Counsel/Associate Chief Coun-sel (Tax Exempt and Government Enti-ties). For further information regardingthis notice, contact Ms. Tanner at (202)622–6080 (not a toll-free call).

Section 446.—General Rulefor Methods of Accounting26 CFR 1.446-2: Method of accounting for interest.

Rev. Rul. 2004-52 holds that credit card annualfees are not interest for federal income tax purposes.Moreover, the ruling holds that credit card annual feesare includible in the gross income by the card issuerwhen they become due and payable by card holdersunder the terms of the credit card agreements. SeeRev. Rul. 2004-52, page 973.

Rev. Proc. 2004–32 provides automatic proce-dures for taxpayers to change their method of ac-counting to a method that complies with Rev. Rul.2004–52, 2004–22 I.R.B. dated June 1, 2004, or tothe Ratable Inclusion Method for Credit Card Annualfees described in this revenue procedure. See Rev.Proc. 2004-32, page 988.

Rev. Proc. 2004-33 provides automatic proce-dures for taxpayers to change their method of ac-counting for credit card late fee income to treat thesefees as interest that creates or increases the amount ofOID on a pool of credit card loans to which the feesrelate. This revenue procedure also sets forth the con-ditions under which the Commissioner will not chal-lenge a taxpayer’s treatment of these fees as interestor as OID on a pool of credit card loans to which thefees relate. See Rev. Proc. 2004-33, page 989.

Section 451.—General Rulefor Taxable Year of Inclusion

Rev. Proc. 2004–32 provides automatic proce-dures for taxpayers to change their method of ac-counting to a method that complies with Rev. Rul.2004–52, 2004–22 I.R.B. dated June 1, 2004, or tothe Ratable Inclusion Method for Credit Card Annualfees described in this revenue procedure. See Rev.Proc. 2004-32, page 988.

26 CFR 1.451–1: Taxable year of inclusion.(Also: §§ 61, 446.)

Credit card annual fees. This rulingholds that credit card annual fees are notinterest for federal income tax purposes.Moreover, the ruling holds that credit cardannual fees are includible in the gross in-come by the card issuer when they becomedue and payable by cardholders under theterms of the credit card agreements.

Rev. Rul. 2004–52

ISSUES

(1) Are credit card annual fees interestfor federal income tax purposes?

2004-22 I.R.B. 973 June 1, 2004

(2) When are credit card annual fees in-cludible in gross income by the card is-suer?

FACTS

X, a taxpayer that uses an overall ac-crual method of accounting for federalincome tax purposes, issues credit cards.Each card allows the cardholder to ac-cess a revolving line of credit to makepurchases of goods and services and, ifotherwise provided for under the applica-ble cardholder agreement, to obtain cashadvances.

Credit card issuers, including X, chargecertain cardholders an annual fee. Thesecredit card issuers make various benefitsand services available to their cardholdersduring the year, regardless of whether thecardholder actually utilizes them. Further,although they provide these benefits andservices to cardholders, no part of the an-nual fee that is charged to any cardholderis for a specific benefit or service providedby a credit card issuer to that cardholder.

Each cardholder’s credit card agree-ment sets forth the applicable terms andconditions under which X may charge thatcardholder an annual fee. X charges somecardholders a nonrefundable annual fee.X charges other cardholders an annual feethat is refundable on a pro rata basis if thecardholder closes the account during theperiod covered by the fee.

Under the applicable cardholder agree-ment, no annual fee becomes due andpayable until X posts an annual fee chargeto the cardholder’s credit card account.X reflects this posting in the cardholder’scredit card statement. X generally poststhe full amount of the annual fee in a singlecharge unless the terms of the agreementrequire X to post the annual fee charge ininstallments.

LAW AND ANALYSIS

For federal income tax purposes, in-terest is an amount that is paid in com-pensation for the use or forbearance ofmoney. Deputy v. DuPont, 308 U.S. 488(1940), 1940–1 C.B. 118; Old ColonyRailroad Co. v. Commissioner, 284 U.S.552 (1932), 1932–1 C.B. 274. Neitherthe label used for the fee nor a taxpayer’streatment of the fee for financial or regu-latory reporting purposes is determinativeof the proper federal income tax charac-

terization of that fee. See Thor PowerTool Co. v. Commissioner, 439 U.S. 522,542–43 (1979), 1979–1 C.B. 167, 174–75;Rev. Rul. 72–315, 1972–1 C.B. 49.

The annual fee that credit card issuers,including X, charge any cardholder isnot for any specific benefit provided bythe credit card issuer to that cardholder.Rather, it is charged for all of the benefitsand services that are available to the card-holder under the applicable cardholderagreement. Because cardholders pay an-nual fees to credit card issuers, includingX, in return for all of the benefits andservices available under the applicablecredit card agreement, annual fees are notcompensation for the use or forbearanceof money. Thus, X’s annual fee income isnot interest income for federal income taxpurposes.

Under § 451(a) of the Internal RevenueCode, the amount of any item of gross in-come is includible in gross income for thetaxable year in which it is received by thetaxpayer, unless that amount is to be prop-erly accounted for in a different period un-der the method of accounting used by thetaxpayer in computing taxable income.

Under § 1.451–1(a) of the Income TaxRegulations, income is includible in grossincome by a taxpayer that uses an accrualmethod of accounting when all events haveoccurred that fix the taxpayer’s right to re-ceive that income and the amount of thatincome can be determined with reasonableaccuracy. See also § 1.446–1(c)(1)(ii)(A).Generally, all the events that fix the right toreceive income occur when either the re-quired performance takes place, paymentis due, or payment is made, whichever oc-curs first (the all events test). See Rev.Rul. 2003–10, 2003–1 C.B. 288; Rev. Rul.80–308, 1980–2 C.B. 162.

X is required to include these annualfees in gross income under § 1.451–1(a)when the fee income becomes due andpayable under its agreements, because X’sright to the income is fixed at that pointand the amount of the income can be deter-mined with reasonable accuracy. Thus, theall events test is satisfied when X posts anannual fee charge to a cardholder’s creditcard account even if X later is requiredto refund a portion of a previously postedrefundable annual fee charge because thecardholder closes the account during theperiod covered by that fee.

Notwithstanding the holding of this rev-enue ruling, Rev. Proc. 2004–32, 2004–22I.R.B. 988, dated June 1, 2004, this Bul-letin, allows card issuers to account for an-nual fee income using the Ratable Inclu-sion Method for Credit Card Annual Fees,which is described in section 4 of that rev-enue procedure. Rev. Proc. 2004–32 alsoprovides automatic consent for a taxpayerdescribed in this revenue ruling to changeits method of accounting for annual fee in-come.

HOLDINGS

(1) Credit card annual fees are not inter-est for federal income tax purposes.

(2) Credit card annual fees are includi-ble in gross income by the card issuer whenthey become due and payable by cardhold-ers under the terms of the credit card agree-ments.

DRAFTING INFORMATION

The principal authors of this revenueruling are Rebecca E. Asta, Alexa Dubert,and Tina Jannotta of the Office of ChiefCounsel (Financial Institutions and Prod-ucts). For further information regardingthis revenue ruling, contact the principalauthors at (202) 622–3930 (not a toll-freecall).

Section 481.—AdjustmentsRequired by Changes inMethod of Accounting

Taxpayers changing a method of accounting forcertain transfers to trusts to satisfy contested liabili-ties under section 461(f) may be required to take intoaccount a positive adjustment under section 481(a)entirely in one year. See Rev. Proc. 2004-31, page986.

Section 501.—ExemptionFrom Tax on Corporations,Certain Trusts, etc.26 CFR 1.501(c)(3)–1: Organizations organized andoperated for religious, charitable, scientific, testingfor public safety, literary, or educational purposes, orfor the prevention of cruelty to children or animals.(Also sections 511–513.)

Joint ventures. This ruling illus-trates the tax consequences for a section501(c)(3) organization that enters into ajoint venture with a for-profit organizationas an insubstantial part of its activities.

June 1, 2004 974 2004-22 I.R.B.

Rev. Rul. 2004–51

ISSUES

1. Whether, under the facts describedbelow, an organization continues to qual-ify for exemption from federal income taxas an organization described in § 501(c)(3)of the Internal Revenue Code when it con-tributes a portion of its assets to and con-ducts a portion of its activities through alimited liability company (LLC) formedwith a for-profit corporation.

2. Whether, under the same facts, theorganization is subject to unrelated busi-ness income tax under § 511 on its distribu-tive share of the LLC’s income.

FACTS

M is a university that has been rec-ognized as exempt from federal incometax under § 501(a) as an organization de-scribed in § 501(c)(3). As a part of its edu-cational programs, M offers summer sem-inars to enhance the skill level of elemen-tary and secondary school teachers.

To expand the reach of its teacher train-ing seminars, M forms a domestic LLC,L, with O, a company that specializes inconducting interactive video training pro-grams. L’s Articles of Organization andOperating Agreement (“governing docu-ments”) provide that the sole purpose of Lis to offer teacher training seminars at off-campus locations using interactive videotechnology. M and O each hold a 50 per-cent ownership interest in L, which is pro-portionate to the value of their respectivecapital contributions to L. The governingdocuments provide that all returns of cap-ital, allocations and distributions shall bemade in proportion to the members’ re-spective ownership interests.

The governing documents provide thatL will be managed by a governing boardcomprised of three directors chosen by Mand three directors chosen by O. Under thegoverning documents, L will arrange andconduct all aspects of the video teachertraining seminars, including advertising,enrolling participants, arranging for thenecessary facilities, distributing the coursematerials and broadcasting the seminarsto various locations. L’s teacher trainingseminars will cover the same content cov-ered in the seminars M conducts on M’scampus. However, school teachers willparticipate through an interactive video

link at various locations rather than in per-son. The governing documents grant Mthe exclusive right to approve the curricu-lum, training materials, and instructors,and to determine the standards for suc-cessful completion of the seminars. Thegoverning documents grant O the exclu-sive right to select the locations whereparticipants can receive a video link to theseminars and to approve other personnel(such as camera operators) necessary toconduct the video teacher training semi-nars. All other actions require the mutualconsent of M and O.

The governing documents require thatthe terms of all contracts and transactionsentered into by L with M, O and any otherparties be at arm’s length and that all con-tract and transaction prices be at fair mar-ket value determined by reference to theprices for comparable goods or services.The governing documents limit L’s activi-ties to conducting the teacher training sem-inars and also require that L not engagein any activities that would jeopardize M’sexemption under § 501(c)(3). L does infact operate in accordance with the govern-ing documents in all respects.

M’s participation in L will be aninsubstantial part of M’s activitieswithin the meaning of § 501(c)(3) and§ 1.501(c)(3)–1(c)(1) of the Income TaxRegulations.

Because L does not elect under§ 301.7701–3(c) of the Procedure andAdministration Regulations to be classi-fied as an association, L is classified as apartnership for federal tax purposes pur-suant to § 301.7701–3(b).

LAW

Exemption under § 501(c)(3)

Section 501(c)(3) provides, in part, forthe exemption from federal income tax ofcorporations organized and operated ex-clusively for charitable, scientific, or edu-cational purposes, provided no part of theorganization’s net earnings inures to thebenefit of any private shareholder or indi-vidual.

Section 1.501(c)(3)–1(c)(1) providesthat an organization will be regarded as op-erated exclusively for one or more exemptpurposes only if it engages primarily in ac-tivities that accomplish one or more of theexempt purposes specified in § 501(c)(3).

Activities that do not further exempt pur-poses must be an insubstantial part ofthe organization’s activities. In BetterBusiness Bureau of Washington, D.C. v.United States, 326 U.S. 279, 283 (1945),the Supreme Court held that “the presenceof a single . . . [non-exempt] purpose,if substantial in nature, will destroy theexemption regardless of the number or im-portance of truly . . . [exempt] purposes.”

Section 1.501(c)(3)–1(d)(1)(ii) pro-vides that an organization is not organizedor operated exclusively for exempt pur-poses unless it serves a public rather than aprivate interest. To meet this requirement,an organization must “establish that it isnot organized or operated for the benefitof private interests....”

Section 1.501(c)(3)–1(d)(2) defines theterm “charitable” as used in § 501(c)(3) asincluding the advancement of education.

Section 1.501(c)(3)–1(d)(3)(i) pro-vides, in part, that the term “educational”as used in § 501(c)(3) relates to the in-struction or training of the individual forthe purpose of improving or developinghis capabilities.

Section 1.501(c)(3)–1(d)(3)(ii) pro-vides examples of educational organi-zations including a college that has aregularly scheduled curriculum, a regularfaculty, and a regularly enrolled body ofstudents in attendance at a place wherethe educational activities are regularly car-ried on and an organization that presentsa course of instruction by means of cor-respondence or through the utilization oftelevision or radio.

Joint Ventures

Rev. Rul. 98–15, 1998–1 C.B. 718,provides that for purposes of determiningexemption under § 501(c)(3), the activitiesof a partnership, including an LLC treatedas a partnership for federal tax purposes,are considered to be the activities of thepartners. A § 501(c)(3) organization mayform and participate in a partnership andmeet the operational test if 1) participationin the partnership furthers a charitable pur-pose, and 2) the partnership arrangementpermits the exempt organization to act ex-clusively in furtherance of its exempt pur-pose and only incidentally for the benefitof the for-profit partners.

Redlands Surgical Services, 113 T.C.47, 92–93 (1999), aff’d 242 F.3d 904 (9th

2004-22 I.R.B. 975 June 1, 2004

Cir. 2001), provides that a nonprofit or-ganization may form partnerships, or en-ter into contracts, with private parties tofurther its charitable purposes on mutu-ally beneficial terms, “so long as the non-profit organization does not thereby imper-missibly serve private interests.” The TaxCourt held that the operational standard isnot satisfied merely by establishing “what-ever charitable benefits [the partnership]may produce,” finding that the nonprofitpartner lacked “formal or informal controlsufficient to ensure furtherance of chari-table purposes.” Affirming the Tax Court,the Ninth Circuit held that ceding “effec-tive control” of partnership activities im-permissibly serves private interests. 242F.3d at 904.

St. David’s Health Care System v.United States, 349 F.3d 232, 236–237 (5thCir. 2003), held that the determinationof whether a nonprofit organization thatenters into a partnership operates exclu-sively for exempt purposes is not limitedto “whether the partnership provides some(or even an extensive amount of) charita-ble services.” The nonprofit partner alsomust have the “capacity to ensure that thepartnership’s operations further charitablepurposes.” Id. at 243. “[T]he non-profitshould lose its tax-exempt status if it cedescontrol to the for-profit entity.” Id. at 239.

Tax on Unrelated Business Income

Section 511(a), in part, provides for theimposition of tax on the unrelated businesstaxable income (as defined in § 512) oforganizations described in § 501(c)(3).

Section 512(a)(1) defines “unrelatedbusiness taxable income” as the gross in-come derived by any organization fromany unrelated trade or business (as definedin § 513) regularly carried on by it less thedeductions allowed, both computed withthe modifications provided in § 512(b).

Section 512(c) provides that, if a tradeor business regularly carried on by a part-nership of which an organization is a mem-ber is an unrelated trade or business withrespect to the organization, in computingits unrelated business taxable income, theorganization shall, subject to the excep-tions, additions, and limitations containedin § 512(b), include its share (whether ornot distributed) of the gross income ofthe partnership from the unrelated tradeor business and its share of the partner-

ship deductions directly connected withthe gross income.

Section 513(a) defines the term “unre-lated trade or business” as any trade orbusiness the conduct of which is not sub-stantially related (aside from the need ofthe organization for income or funds or theuse it makes of the profits derived) to theexercise or performance by the organiza-tion of its charitable, educational, or otherpurpose or function constituting the basisfor its exemption under § 501.

Section 1.513–1(d)(2) provides that atrade or business is “related” to an or-ganization’s exempt purposes only if theconduct of the business activities has acausal relationship to the achievement ofexempt purposes (other than through theproduction of income). A trade or busi-ness is “substantially related” for purposesof § 513, only if the causal relationshipis a substantial one. Thus, to be substan-tially related, the activity “must contributeimportantly to the accomplishment of [ex-empt] purposes.” Section 1.513–1(d)(2).Section 513, therefore, focuses on “themanner in which the exempt organiza-tion operates its business” to determinewhether it contributes importantly to theorganization’s charitable or educationalfunction. United States v. American Col-lege of Physicians, 475 U.S. 834, 849(1986).

ANALYSIS

L is a partnership for federal tax pur-poses. Therefore, L’s activities are at-tributed to M for purposes of determiningboth whether M operates exclusively foreducational purposes and therefore con-tinues to qualify for exemption under§ 501(c)(3) and whether M has engagedin an unrelated trade or business andtherefore may be subject to the unrelatedbusiness income tax on its distributiveshare of L’s income.

The activities M is treated as conduct-ing through L are not a substantial partof M’s activities within the meaning of§ 501(c)(3) and § 1.501(c)(3)–1(c)(1).Therefore, based on all the facts and cir-cumstances, M’s participation in L, takenalone, will not affect M’s continued qual-ification for exemption as an organizationdescribed in § 501(c)(3).

Although M continues to qualify asan exempt organization described in

§ 501(c)(3), M may be subject to unre-lated business income tax under § 511if L conducts a trade or business that isnot substantially related to the exercise orperformance of M’s exempt purposes orfunctions.

The facts establish that M’s activitiesconducted through L constitute a tradeor business that is substantially relatedto the exercise and performance of M’sexempt purposes and functions. Eventhough L arranges and conducts all aspectsof the teacher training seminars, M aloneapproves the curriculum, training mate-rials and instructors, and determines thestandards for successfully completing theseminars. All contracts and transactionsentered into by L are at arm’s length andfor fair market value, M’s and O’s owner-ship interests in L are proportional to theirrespective capital contributions, and allreturns of capital, allocations and distribu-tions by L are proportional to M’s and O’sownership interests. The fact that O se-lects the locations and approves the otherpersonnel necessary to conduct the semi-nars does not affect whether the seminarsare substantially related to M’s educa-tional purposes. Moreover, the teachertraining seminars L conducts using inter-active video technology cover the samecontent as the seminars M conducts onM’s campus. Finally, L’s activities haveexpanded the reach of M’s teacher trainingseminars, for example, to individuals whootherwise could not be accommodatedat, or conveniently travel to, M’s campus.Therefore, the manner in which L conductsthe teacher training seminars contributesimportantly to the accomplishment of M’seducational purposes, and the activities ofL are substantially related to M’s educa-tional purposes. Section 1.513–1(d)(2).Accordingly, based on all the facts andcircumstances, M is not subject to unre-lated business income tax under § 511 onits distributive share of L’s income.

HOLDINGS

1. M continues to qualify for exemp-tion under § 501(c)(3) when it contributesa portion of its assets to and conducts a por-tion of its activities through L.

2. M is not subject to unrelated businessincome tax under § 511 on its distributiveshare of L’s income.

June 1, 2004 976 2004-22 I.R.B.

DRAFTING INFORMATION

The principal author of this revenue rul-ing is Virginia G. Richardson of ExemptOrganizations, Tax Exempt and Govern-ment Entities Division. For further in-formation regarding this revenue ruling,contact Virginia G. Richardson at (202)283–8938 (not a toll-free call).

Section 511.—Imposition ofTax on Unrelated BusinessIncome of Charitable, etc.,Organizations

Unrelated business income tax consequences for asection 501(c)(3) organization that enters into a jointventure with a for-profit organization as an insubstan-tial part of its activities. See Rev. Rul. 2004-51, page974.

Section 512.—UnrelatedBusiness Taxable Income

Unrelated business income tax consequences for asection 501(c)(3) organization that enters into a jointventure with a for-profit organization as an insubstan-tial part of its activities. See Rev. Rul. 2004-51, page974.

Section 513.—UnrelatedTrade or Business

Unrelated business income tax consequences for asection 501(c)(3) organization that enters into a jointventure with a for-profit organization as an insubstan-tial part of its activities. See Rev. Rul. 2004-51, page974.

Section 1272.—CurrentInclusion in Income ofOriginal Issue Discount

Rev. Proc. 2004-33 provides automatic proce-dures for taxpayers to change their method of ac-counting for credit card late fee income to treat thesefees as interest that creates or increases the amount ofOID on a pool of credit card loans to which the feesrelate. This revenue procedure also sets forth the con-ditions under which the Commissioner will not chal-lenge a taxpayer’s treatment of these fees as interestor as OID on a pool of credit card loans to which thefees relate. See Rev. Proc. 2004-33, page 989.

Section 1361.—S Corpo-ration Defined26 CFR 1.1361(b): Small business corporation de-fined.(Also: §§ 401, 501, 1362, 7701, 7871, 305.7871–1.)

Indian tribal government. This rul-ing provides clarification with regard to anIndian tribal government’s ability to qual-ify as an eligible shareholder under sec-tion 1361 of the Code. Specifically, theruling explains that a federally recognizedIndian tribal government does not qualifyas a permissible S corporation shareholderunder section 1361(b)(1)(B) because it isnot treated as an individual subject to indi-vidual income taxes under section 1 of theCode. The ruling also explains that a feder-ally recognized Indian Tribe cannot qual-ify as a permissible S corporation share-holder under section 1361(c)(6) becauseit is neither a section 501(c)(3) organiza-tion, nor a section 401(a) qualified plan,profit-sharing, or stock bonus plan organi-zation.

Rev. Rul. 2004–50

ISSUE

Is a federally recognized Indiantribal government, as described in§ 7701(a)(40)(A) of the Internal RevenueCode, an eligible S corporation share-holder under § 1361?

FACTS

X is a federally recognized Indian tribalgovernment (Indian tribal government)and a shareholder in Corporation, a do-mestic entity, formed in accordance withthe laws of State. Corporation wants tomake an election to be an S corporation.

LAW AND ANALYSIS

Section 1361(a) provides that for pur-poses of this title, the term “S corporation”means, with respect to any taxable year,a small business corporation for which anelection under § 1362(a) is in effect for theyear.

Section 1361(b)(1) provides that forpurposes of this subchapter, the term“small business corporation” means adomestic corporation which is not an inel-igible corporation and which does not (A)have more than 75 shareholders, (B) have

as a shareholder a person (other than an es-tate, a trust described in subsection (c)(2),or an organization described in subsection(c)(6)) who is not an individual, (C) havea nonresident alien as a shareholder, and(D) have more than one class of stock.

Section 1361(c)(6) provides that forpurposes of subsection (b)(1)(B), anorganization which is (A) described in§§ 401(a) or 501(c)(3), and (B) exemptfrom taxation under § 501(a), may be ashareholder in an S corporation.

Section 401(a) provides the definitionof a qualified pension, profit-sharing, andstock bonus plans that qualifies under§ 1361(b) as an eligible S corporationshareholder.

Section 501(a) provides that an organ-ization described in subsection (c) or (d)or § 401(a) shall be exempt from taxationunder this subtitle unless that exemption isdenied under § 502 or § 503.

Section 501(c)(3) describes corpora-tions, and any community chest, fund, orfoundation, organized and operated exclu-sively for religious, charitable, scientific,testing for public safety, literacy, or edu-cational purposes, or to foster national orinternational amateur sports competition(but only if no part of its activities involvethe provision of athletic facilities or equip-ment), or for the prevention of crueltyto children or animals, no part of the netearnings of which inures to the benefit ofany private shareholder or individual, nosubstantial part of the activities of which iscarrying on propaganda, or otherwise at-tempting, to influence legislation (exceptas otherwise provided in section (h)), andwhich does not participate in, or intervenein (including the publishing or distributionof statements), any political campaign onbehalf of (or in opposition to) any candi-date for public office.

Section 7701(a)(40)(A) states that theterm “Indian tribal government” refers tothe governing body of any tribe, band,community, village, or group of Indians,or (if applicable) Alaska Natives, which isdetermined by the Secretary of the Trea-sury, after consultation with the Secretaryof the Interior, to exercise governmentalfunctions.

Section 7871(a) and § 305.7871–1 ofthe Income Tax Regulations provide thatIndian tribal governments will be treatedas states for certain enumerated federal taxpurposes.

2004-22 I.R.B. 977 June 1, 2004

Section 7871(d) states that, for pur-poses of § 7871(a), a subdivision of anIndian tribal government shall be treatedas a political subdivision of a state if (andonly if) the Secretary of the Treasury de-termines (after consultation with the Sec-retary of the Interior) that the subdivisionhas been delegated the right to exercise oneor more of the substantial governmentalfunctions of the Indian tribal government.

Rev. Proc. 2002–64, 2002–2 C.B. 717,provides the most recent list of federallyrecognized tribal governments. In the sit-uation described in this ruling, X is a feder-ally recognized Indian tribal government.

Generally, federal income tax statutesdo not tax Indian tribes. See Rev. Rul.67–284, 1967–2 C.B. 55. An Indian tribeis not subject to federal income tax as anindividual under § 1 or as a corporation un-der § 11. However, colleges and universi-ties formed by Indian tribes are subject to§ 511(a)(2)(B) (relating to the taxation ofcolleges and universities which are agen-cies or instrumentalities of governmentsor their political subdivisions) pursuant to§ 7871(a)(5). Indian tribes also are subjectto certain excise taxes.

Rev. Rul. 60–384, 1960–2 C.B. 172,provides circumstances under which agovernmental agency is prohibited fromqualifying as a § 501(c)(3) organization. Astate or municipality itself will not qualifyas an organization described in § 501(c)(3)since its purposes are clearly not exclu-sively those described in § 501(c)(3).Where a particular branch or departmentunder whose jurisdiction the activity inquestion is being coordinated is an integralpart of a state or municipal government,the provisions of § 501(c)(3) would alsonot be applicable.

Based on the above law and publishedguidance, X, an Indian tribal government,is not subject to federal income tax as anindividual under § 1. Because an Indiantribal government is not subject to tax as anindividual for § 1 purposes, it is not consid-ered an individual under § 1361(b)(1)(B).

In addition, X, an Indian tribal gov-ernment, does not qualify under the§ 1362(c)(6) exception for certain exemptorganizations described in § 501(c)(3) or§ 401(a). X is not a § 401(a) organiza-tion because it is not a qualified pension,profit-sharing, or stock bonus plan. Fur-thermore, X is not a § 501(c)(3) organ-ization because it is a government and

its purposes are not exclusively those de-scribed in § 501(c)(3). Consequently, X isnot an eligible S corporation shareholder,and Corporation cannot make an electionto be an S corporation.

HOLDING

A federally recognized Indian tribalgovernment is not an eligible S corpora-tion shareholder for purposes of § 1361.

DRAFTING INFORMATION

The principal author of this revenue rul-ing is Laura C. Nash of the Office of As-sociate Chief Counsel (Passthroughs andSpecial Industries). For further informa-tion regarding this revenue ruling, con-tact Ms. Nash at (202) 622–3050 (not atoll-free call).

Section 6501.—Limitationson Assessment andCollection

Ct. D. 2079

SUPREME COURT OF THEUNITED STATES

No. 02-1389

UNITED STATES v. GALLETTI ET AL.

CERTIORARI TO THE UNITEDSTATES COURT

OF APPEALS FOR THE NINTHCIRCUIT

March 23, 2004

Syllabus

“[T]he amount of any tax imposed [bythe Internal Revenue Code] shall be as-sessed within three years after the returnwas filed.” 26 U.S.C. Sec. 6501(a). If atax is properly so assessed, the statute oflimitations for collecting it is extended by10 years from the assessment date. Sec.6502(a). Respondents were general part-ners of a partnership (hereinafter Partner-ship) that failed to pay significant federalemployment taxes from 1992 to 1995. TheInternal Revenue Service (IRS) timely as-sessed the Partnership, but the taxes werenever paid. Respondents later filed forChapter 13 bankruptcy protection, and the

IRS then filed proof of claims against themfor the Partnership’s unpaid employmenttaxes. Respondents objected, arguing thatthe timely assessment of the Partnershipdid not extend the 3-year limitations periodagainst the general partners, who had notbeen separately assessed within that pe-riod. The Bankruptcy Court and the Dis-trict Court agreed and sustained respon-dents’ objections. The Ninth Circuit af-firmed, holding that since respondents are“taxpayers” under Sec. 7701, which de-fines “taxpayer” to mean “any person sub-ject to any internal revenue tax,” they arealso “taxpayers” under Secs. 6203 and6501. As such, the court held that the as-sessment against the Partnership extendedthe limitations period only with respect tothe Partnership.

Held: The proper tax assessmentagainst the Partnership suffices to extendthe statute of limitations to collect the taxin a judicial proceeding from the generalpartners who are liable for the payment ofthe Partnership’s debts. Pp. 4–9.

(a) Respondents argue that a valid as-sessment triggering the 10-year increasein the limitations period must name themindividually, as they are primarily liablefor the tax debt. They claim, first, thatthey are the relevant taxpayers under Sec.6203, which requires the assessment tobe made by “recording the liability ofthe taxpayer.” Although the Ninth Cir-cuit correctly concluded that an individualpartner can be a “taxpayer,” Sec. 6203speaks of the taxpayer’s “liability,” whichindicates that the relevant taxpayer mustbe determined. Here, the liability arosefrom the Partnership’s failure to complywith Sec. 3402(a)(1)’s requirement thatan “employer [paying] wages” deduct andwithhold employment taxes. And Sec.3403 makes clear that the “employer” thatfails to withhold and submit the requisiteemployment taxes is the “liable” taxpayer.In this case, the Partnership is the “em-ployer.” Second, respondents claim thatthey are primarily liable for the tax debtbecause California law makes them jointlyand severally liable for the Partnership’sdebts. However, to be primarily liablefor this debt, respondents must show thatthey are the “employer.” And, under Cal-ifornia law, a partnership and its generalpartners are separate entities. Thus re-spondents cannot argue that, for all intentsand purposes, imposing a tax directly on

June 1, 2004 978 2004-22 I.R.B.

the Partnership is equivalent to imposinga tax directly on the general partners, butmust instead prove that the tax liabilitywas imposed both on the Partnership andon respondents as separate “employers.”That respondents are jointly and severallyliable for the Partnership’s debts is irrele-vant to this determination. Pp. 4–7.

(b) The Code does not require the Gov-ernment to make separate assessments ofa single tax debt against persons or enti-ties secondarily liable for that debt in orderfor Sec. 6502’s extended limitations pe-riod to apply to judicial collection actionsagainst those persons or entities. It is clearthat “assessment” refers to little more thanthe calculation or recording of a tax liabil-ity, see, e.g., Sec. 6201, and that it is thetax that is assessed, not the taxpayer, see,e.g., Sec. 6501. The limitations period re-sulting from a proper assessment governsthe time extension for enforcing the tax li-ability. United States v. Updike, 281 U.S.489, 495. Once a tax has been properlyassessed, nothing in the Code requires theIRS to duplicate its efforts by separatelyassessing the same tax against individualsor entities who are not the actual taxpay-ers but are, by reason of state law, liablefor the taxpayer’s debt. The assessment’sconsequences—the extension of the limi-tations period for collecting the debt—at-tach to the debt without reference to thespecial circumstances of the secondarily li-able parties. Here, the tax was properly as-sessed against the Partnership, thereby ex-tending the limitations period for collect-ing the debt. The United States now timelyseeks to collect that debt in judicial pro-ceedings against respondents. Pp. 7–9.

314 F.3d 336 reversed and remanded.THOMAS, J., delivered the opinion for

a unanimous Court.

SUPREME COURT OF THEUNITED STATES

No. 02-1389

UNITED STATES, PETITIONER v.ABEL COSMO GALLETTI ET AL.

ON WRIT OF CERTIORARI TO THEUNITED STATES COURT

OF APPEALS FOR THE NINTHCIRCUIT

March 23, 2004

JUSTICE THOMAS delivered theopinion of the Court.

Section 6501(a) of the Internal RevenueCode states that, except as otherwise pro-vided, “the amount of any tax imposed bythis title shall be assessed within 3 yearsafter the return was filed . . . and no pro-ceeding in court without assessment for thecollection of such tax shall be begun afterthe expiration of such period.” 26 U.S.C.Sec. 6501(a). If a tax is properly assessedwithin three years, however, the statute oflimitations for the collection of the tax isextended by 10 years from the date of as-sessment. Sec. 6502(a). We must decidein this case whether, in order for the UnitedStates to avail itself of the 10-year increasein the statute of limitations for collectionof a tax debt, it must assess the taxes notonly against a partnership that is directlyliable for the debt, but also against each in-dividual partner who might be jointly andseverally liable for the debts of the part-nership. Under California law a partner-ship maintains a separate identity from itsgeneral partners, and the partners are onlysecondarily liable for the tax debts of thepartnership, as they are for any debt of thepartnership. Because, in this case, the onlyrelevant “taxpayer” for purposes of Secs.6501–6502 is the partnership, we hold thatthe proper assessment of the tax against thepartnership suffices to extend the statute oflimitations for collection of the tax fromthe general partners who are liable for thepayment of the partnership’s debts. TheGovernment’s timely assessment of the taxagainst the partnership was sufficient toextend the statute of limitations to collectthe tax in a judicial proceeding, whetherfrom the partnership itself or from those li-able for its debts.

I

Respondents, Abel Cosmo Galletti,Sarah Galletti, Francesco Briguglio, andAngela Briguglio, were general partnersof Marina Cabrillo Company (Partner-ship). From 1992 to 1995, the Partnershipfailed to pay significant federal employ-ment tax liabilities that it had incurred.Although the Internal Revenue Service(IRS) timely assessed those taxes againstthe Partnership in 1994, 1995, and 1996,the Partnership never satisfied the debt.

Respondents Abel and Sarah Gallettiand respondents Francesco and Angela

Briguglio filed joint petitions for reliefunder Chapter 13 of the Bankruptcy Codeon October 20, 1999, and February 4,2000, respectively. In the Gallettis’ pro-ceedings, the IRS filed a proof of claim inthe amount of $395,179.89 for unpaid em-ployment taxes assessed between January1994 and July 1995 against the Partner-ship. In the Briguglios’ proceedings, theIRS filed a proof of claim in the amount of$427,402.74. The proof of claim includedsecured claims totaling $403,264.06 forunpaid employment taxes assessed be-tween January 1994 and November 1996against the Partnership.

Respondents objected to the claimson the ground that they were not provenagainst the estates. Respondents did notdispute that under California law they arejointly and severally liable for the debts ofthe Partnership. Nor did they dispute thatthe IRS had properly assessed the taxesagainst the Partnership within the 3-yearstatute of limitations, thereby extendingthe limitations period for collection of thetaxes by 10 years. Rather, respondentsargued that the timely assessment of thePartnership extended the statute of limi-tations only against the Partnership. Toextend the 3-year statute of limitationsagainst the general partners, respondentsargued, the IRS had to separately assessthe general partners within the 3-yearlimitations period. Because it did not,and because the 3-year limitations pe-riod had expired, respondents argued thatthe IRS could no longer collect the debtfrom them. The Bankruptcy Court andthe District Court agreed and sustainedrespondents’ objections to the claims.

The Court of Appeals for the NinthCircuit affirmed. The Government arguedthat the Code does not require that theindividual partners be assessed within the3-year period prescribed by Sec. 6501 andthat the IRS made a valid assessment ofthe taxpayer here because the Partnershipis the only relevant “taxpayer.” The Courtof Appeals held that since respondentsare “taxpayers” under Sec. 7701(a)(14),which defines “taxpayer” to mean “anyperson subject to any internal revenuetax,” they are also “taxpayers” under Secs.6203 and 6501. As such, the Court of Ap-peals held that “[t]he assessment againstthe Partnership extended the statute oflimitations only with respect to the Part-nership.” 314 F.3d 336, 340 (2002).

2004-22 I.R.B. 979 June 1, 2004

The Government argued in the alter-native that because respondents concededthat they were liable for the Partnership’semployment tax debts as a matter of Cali-fornia law, the Government had a right topayment, which suffices to prove a validclaim in bankruptcy. See 11 U.S.C. Sec.101(5)(A) (defining “claim” as includinga “right to payment, whether or not suchright is reduced to judgment, liquidated,unliquidated, fixed, contingent, matured,unmatured, disputed, undisputed, legal,equitable, secured, or unsecured”). TheCourt of Appeals rejected this argumentbecause, under California law, a creditormust obtain a judgment against a part-ner before holding that partner liable forthe partnership’s debt. Cal. Corp. CodeAnn. Sec. 16307(c) (Supp. 2004). At thetime the United States filed its proof ofclaim, it had not obtained a separate judg-ment against respondents, and the time forobtaining a judgment under the InternalRevenue Code against respondents hadexpired.

We granted certiorari, 539 U.S.(2003), and now reverse.

II

Section 6501(a) of the Internal RevenueCode provides that “the amount of any taximposed [by the Code] shall be assessedwithin 3 years after the return was filed.”26 U.S.C. Sec. 6501(a). “The assess-ment shall be made by recording the lia-bility of the taxpayer in the office of theSecretary [of the Treasury] in accordancewith rules or regulations prescribed by theSecretary.” Sec. 6203. Within 60 days ofthe assessment, the Secretary is requiredto “give notice to each person liable forthe unpaid tax, stating the amount and de-manding payment thereof.” Sec. 6303(a).If the tax is properly assessed within 3years, the limitations period for collectionof the tax is extended by 10 years from thedate of the assessment. Sec. 6502.

The dispute in this case centers onwhether the United States can collect thePartnership’s unpaid employment taxesfrom respondents in a judicial proceedingoccurring more than three years after thetax return was filed but within the 10-yearextension to the 3-year limitations periodthat attached when the tax was timelyassessed against the Partnership.1 Respon-dents insist that a valid assessment (that is,one that would trigger the 10-year increasein the statute of limitations) must namethem individually. This is so, accordingto respondents, because they are primar-ily liable for the tax debt, both becausethey are “the [relevant] taxpayer[s]” underSec. 6203 and because they are jointlyand severally liable for the tax debts of thepartnership.2 We reject both arguments inturn.

A

Respondents argue, and the Court ofAppeals agreed, that each partner is pri-marily liable for the debt and must be in-dividually assessed because each partneris a separate “taxpayer” under 26 U.S.C.Sec. 6203. The statutory definition of“taxpayer” includes “any person subject toany internal revenue tax,” and “person” in-cludes both “an individual” and a “part-nership,” Secs. 7701(a)(14), (a)(1). TheCourt of Appeals observed that althoughthe Partnership is a “taxpayer,” each indi-vidual partner is also a separate “taxpayer.”As such, the Court of Appeals interpretedSec. 6203’s requirement that the Secretaryof the Treasury record “the liability of thetaxpayer” to require a separate assessmentagainst each of the general partners.

Although the Court of Appeals cor-rectly concluded that an individual partnercan be a “taxpayer,” the inquiry does notend there. Section 6203 speaks of “the li-ability of the taxpayer” (emphasis added),which indicates that the relevant taxpayermust be determined. The liability in thiscase arose from the Partnership’s failure to

comply with Sec. 3402(a)(1) of the Code,which requires “every employer makingpayment of wages” to deduct and with-hold employment taxes. Moreover, “[t]heemployer shall be liable for the paymentof the tax required to be deducted andwithheld.” Sec. 3403. When an employerfails to withhold and submit the requisiteamount of employment taxes, Sec. 3403makes clear that the liable taxpayer is theemployer. In this case, the “employer”was the Partnership.3

B

Respondents also argue that they areprimarily liable for the Partnership’s taxdebt because, under California law, gen-eral partners are jointly and severally li-able for the debts of their partnership, Cal.Corp. Code Ann. Sec. 16306 (Supp.2004). Brief for Respondents 8–16. Asour prior discussion demonstrates, how-ever, respondents cannot show that theyare primarily liable for the payment ofthe Partnership’s employment taxes un-less they can show that they are the “em-ployer.” However, under California’s part-nership principles, a partnership and itsgeneral partners are separate entities. SeeCal. Corp. Code Ann. Sec. 16201(Supp. 2004). Thus respondents cannotargue that, for all intents and purposes, im-posing a tax directly on the Partnership isequivalent to imposing a tax directly onthe general partners. Respondents must in-stead prove that the tax liability was im-posed both on the Partnership and respon-dents as separate “employers.” The factthat respondents are jointly and severallyliable for the debts of the Partnership is ir-relevant to this determination.

III

We now turn to the question whether theGovernment must make separate assess-ments of a single tax debt against personsor entities secondarily liable for that debt

1 Because the Government is attempting to enforce the Partnership’s tax liabilities against respondents in a judicial proceeding, we do not address whether an assessment only against thePartnership is sufficient for the IRS to commence administrative collection of the Partnership’s tax debts by lien or levy against respondents’ property.

We also decline to address whether an assessment against the partnership suffices to trigger liability against the partners for interest and penalties without separate notice and demand tothem.

2 Respondents argue that even if we were to hold that the partners are secondarily liable, the IRS would still be barred from collecting the taxes. Respondents contend that if partners arenot “taxpayers” under Sec. 6203, then their liability arises only under state law, and the state 3-year statute of limitations therefore applies. Brief for Respondents 30–34. Respondents haveforfeited this argument by failing to raise it in the courts below. Indeed, the closest respondents have come to arguing that the state limitations period applies was in the Court of Appeals,when respondents argued that “under California law, any collections suit filed against a partner to collect a partnership debt is subject to the statute limitation provision which applies to theunderlying debt of the partnership.” Brief for Respondents in Nos. 01–55953, 01–55954 (CA9), p. 14. This argument, of course, is contrary to respondents’ position in this Court.

3 Our decision is consistent with this Court’s holding in United States v. Williams, 514 U.S. 527, 532–536 (1995), where we interpreted “taxpayer” under 26 U.S.C. Sec. 6511 more broadly.Here, it is clear that we must interpret “the taxpayer” under Sec. 6203 with reference to the underlying liability.

June 1, 2004 980 2004-22 I.R.B.

in order for Sec. 6502’s extended statuteof limitations to apply to those persons orentities.4 We hold that the Code containsno such requirement. Respondents’ argu-ment that they must be separately assessedturns on a mistaken understanding of thefunction and nature of an assessment asidentical to the initiation of a formal col-lection action against any person or en-tity who might be liable for payment of adebt. In its numerous uses throughout theCode, it is clear that the term “assessment”refers to little more than the calculation orrecording of a tax liability. See, e.g., 26U.S.C. Sec. 6201 (assessment authority);Sec. 6203 (method of assessment); Sec.6204 (supplemental assessments); 26 CFRSec. 601.103 (2003). See also Black’sLaw Dictionary 111 (7th ed. 1999) (defin-ing “assessment” as the “[d]eterminationof the [tax] rate or amount of something,such as a tax or damages”). “The Federaltax system is basically one of self-assess-ment,” whereby each taxpayer computesthe tax due and then files the appropriateform of return along with the requisite pay-ment. 26 CFR Sec. 601.103(a) (2003).In most cases, the Secretary accepts theself-assessment and simply records the lia-bility of the taxpayer. Where the taxpayerfails to file the form of return or miscalcu-lates the tax due, as in this case, the Sec-retary can assess “all taxes (including in-terest, additional amounts, additions to thetax, and assessable penalties),” 26 U.S.C.

Sec. 6201(a), by “recording the liabilityof the taxpayer in the office of the Secre-tary,” Sec. 6203. In other words, wherethe Secretary rejects the self-assessment ofthe taxpayer or discovers that the taxpayerhas failed to file a return, the Secretary cal-culates the proper amount of liability andrecords it in the Government’s books.

To be sure, the assessment of a taxtriggers certain consequences. After theamount of liability has been establishedand recorded, the IRS can employ adminis-trative enforcement methods to collect thetax. Secs. 6321–6327, 6331–6334. Theassessment of a tax liability also extendsthe period during which the Governmentcan collect the tax. But the fact that the actof assessment has consequences does notchange the function of the assessment: tocalculate and record a tax liability.

Under a proper understanding of thefunction and nature of an assessment, itis clear that it is the tax that is assessed,not the taxpayer. See Sec. 6501(a) (“theamount of any tax . . . shall be as-sessed”); Sec. 6502(a) (“[w]here the as-sessment of any tax”). And in UnitedStates v. Updike, 281 U.S. 489 (1930), theCourt, interpreting a predecessor to Sec.6502, held that the limitations period re-sulting from a proper assessment governs“the extent of time for the enforcementof the tax liability,” id., at 495. In otherwords, the Court held that the statute oflimitations attached to the debt as a whole.

The basis of the liability in Updike was atax imposed on the corporation, and theCourt held that the same limitations pe-riod applied in a suit to collect the tax fromthe corporation as in a suit to collect thetax from the derivatively liable transferee.Id., at 494–496. See also United Statesv. Wright, 57 F.3d 561, 563 (CA7 1995)(holding that, based on Updike’s principleof “all-for-one, one-for-all,” the statute oflimitations governs the debt as a whole).

Once a tax has been properly assessed,nothing in the Code requires the IRS toduplicate its efforts by separately assessingthe same tax against individuals or entitieswho are not the actual taxpayers but are, byreason of state law, liable for payment ofthe taxpayer’s debt. The consequences ofthe assessment—in this case the extensionof the statute of limitations for collectionof the debt—attach to the tax debt withoutreference to the special circumstances ofthe secondarily liable parties.

In this case, the tax was properly as-sessed against the Partnership, thereby ex-tending the statute of limitations for col-lection of the debt. The United States nowtimely seeks to collect that debt in judi-cial proceedings against respondents.5 Wetherefore reverse the judgment of the Courtof Appeals and remand the case for furtherproceedings consistent with this opinion.

It is so ordered.

4 We use the term “secondary liability” to mean liability that is derived from the original or primary liability.

5 The Court of Appeals also held that the claims were barred by California partnership law, which requires a creditor first to obtain a judgment against a partnership before holding the partnersliable for the partnership’s debt. 314 F.3d 336, 344 (CA9 2002). When respondents filed for bankruptcy, an automatic stay barred the Government from bringing suit outside the BankruptcyCourt to enforce respondents’ secondary liability. 11 U.S.C. Sec. 362(a)(1). Respondents do not dispute, however, that the adjudication of a disputed claim satisfies California’s requirementthat there be a “judgment against a partner.” Cal. Corp. Code Ann. Sec. 16307(c) (Supp. 2004) Moreover, a claim is allowable in bankruptcy “whether or not such right is reduced tojudgment.” 11 U.S.C. Sec. 101(5)(A).

2004-22 I.R.B. 981 June 1, 2004

Part III. Administrative, Procedural, and MiscellaneousCapital Gain Dividends of RICsand REITs

Notice 2004–39

SECTION 1. PURPOSE

This notice provides guidance to regu-lated investment companies (“RICs”), realestate investment trusts (“REITs”), andtheir shareholders in applying § 1(h) ofthe Internal Revenue Code to capital gaindividends of RICs and REITs. The noticeexplains how the changes to § 1(h) madeby the Jobs and Growth Tax Relief Rec-onciliation Act of 2003 (the “JGTRRA”),Pub. L. No. 108–27, 117 Stat. 752, applyto RIC and REIT capital gain dividendspaid (or accounted for as if paid) in taxableyears that end on or after May 6, 2003.