bumrungrad hospital plc - listed companybh.listedcompany.com/misc/cr/20131106-bh-trisno92-en.pdf ·...

TRANSCRIPT

Rating Rationale TRIS Rating affirms the company and senior debenture ratings of Bumrungrad

Hospital PLC (BH) at “A”. The ratings reflect BH’s leading position in Thailand’s private healthcare industry, strong market position in the medical tourist segment, and stable cash flow. However, these strengths are partially offset by competition in the local and international healthcare markets, the risk from having single location, and the potential risks from BH’s future investments.

BH operates a hospital in Bangkok under the name “Bumrungrad International Hospital”. The company is a leading private healthcare provider in Thailand and the ASEAN region, with service capacities of 5,500 outpatients per day and 538 registered inpatient beds. The company’s strong business profile reflects its solid brand equity and three decades of respectable medical records. BH targets mostly the premium local and foreign patients and competes with differentiation on services and quality.

In 2012, BH’s sales were Bt12,856 million, with approximately 70% from self-pay patients. Foreign patients accounted for about 60% of total sales. The company’s competitive edge in the medical tourist segment reflects its strong overseas network. Patients from the Middle East region account for the largest portion of BH’s total foreign patients. Accepting many foreign patients gives BH diverse sources of revenue. As a result, BH can ease the competitive pressure it faces and reduce its reliance on domestic demand for healthcare services.

BH is currently expanding, yet it retains its focus on the premium healthcare segment. The company acquired two land plots over the past two years. One is on Petchburi road and the other is on Sukhumvit Soi 1. On the Petchburi road site, BH will build a 200-bed hospital facility. Construction is expected to finish by 2017. The Sukhumvit Soi 1 plot will be used for capacity expansion of its near-by flagship facility. The total investment for these two projects is approximately Bt9,800 million, excluding land costs. Based on BH’s cash on hand and strong cash flow, TRIS Rating believes that these investments will not materially alter BH’s sound financial profile.

TRIS Rating expects BH to continue delivering solid operating performance. Revenue is forecasted to grow by at least 5%-8% per annum during the next three years. Operating income before depreciation and amortization as a percentage of sales before depreciation and amortization (operating margin) is expected to remain stable and average above 23% over the next three years. With its strong operations, funds from operations (FFO) is expected to be Bt2.5-Bt3 billion per annum during the next three years. FFO, together with the Bt4.5 billion in cash BH received from selling shares of Bangkok Chain Hospital PLC (BCH), is considered sufficient to fund BH’s planned capital expenditures and dividend payment.

BH has a sound liquidity profile even though it is expanding. Total debt at the end of June 2013 comprised only long-term bonds, with the earliest maturity date in 2016. In addition, BH had approximately Bt3.3 billion in uncommitted and undrawn credit lines with financial institutions. This financial slack gives BH needed financial flexibility should the opportunities arise for an acquisition. BH has been looking for acquisition opportunities either for its second brand in the mid- to upper-income segment or an expansion abroad. However, TRIS Rating believes that it will take some time for BH to find and execute a deal.

Company Rating: A

Outlook: Stable

New Issue Rating: -

Rating History: Date Company Issue

(Secured/

Unsecured)

18/11/11 A/Sta -/A

21/10/11 A/Sta -

Contacts: Chanaporn Pinphithak [email protected] Sarinthorn Sosukpaibul [email protected] Nopalak Raktham [email protected]

Suchada Pantu, Ph. D. [email protected]

WWW.TRISRATING.COM

BUMRUNGRAD HOSPITAL PLC

No. 92/2013 6 November 2013

THAI AIRWAYS INTERNATIONAL PLC

Announcement no. 111 12 November 2011

Page 2

Bumrungrad Hospital PLC 6 November 2013

Rating Outlook The “stable” outlook is based on the expectation that BH will maintain its leading position in the private healthcare

segment and continue delivering strong performance. Its business is stable, with moderate gearing. These factors provide financial flexibility while the company is investing and expanding. However, BH should keep its debt to capitalization ratio below 50% in order to maintain its credit quality.

Bumrungrad Hospital PLC (BH) Company Rating: A

Issue Ratings: BH16DA: Bt1,500 million senior debentures due 2016 A BH18DA: Bt1,000 million senior debentures due 2018 A BH21DA: Bt2,500 million senior debentures due 2021 A

Rating Outlook: Stable

KEY RATING CONSIDERATIONS Strengths/Opportunities

Leading private hospital in premium segment Strong market position in medical tourism

segment Cash flow stability Growth in demand for healthcare

Weaknesses/Threats Competition in both domestic and regional markets Single location risk Shortage of physicians and healthcare personnel

CORPORATE OVERVIEW BH operates a hospital in Bangkok under the name

“Bumrungrad International Hospital”. The company was established in 1980 as a 220-bed facility. BH was listed on the SET in 1989. In 1997, the company opened a 554-bed facility that was operated by its subsidiary, Bumrungrad Medical Center Co., Ltd. (BMC). In 2004, BMC sold all its movable assets and transferred its hospital operating licenses back to BH.

The company’s flagship hospital in Bangkok generates over 95% of total revenue. At the end of June 2013, the hospital had service capacities of 5,500 outpatient (OP) visits per day and 538 registered inpatient (IP) beds. The actual number of beds was 487. BH is renovating the IP wards in its main facility. The renovation will ultimately raise the number of registered beds to 572 by 2016.

The revenue contributions from the OP and IP segments have stayed about equal. Revenue from foreign patients accounts for approximately 60% of BH’s total revenue. About 70% of BH’s total revenue is from self-pay patients. The remaining 30% is from insurance payments and corporate contracts. Corporate contracts also cover patients from the Middle East region, whose services are paid by their respective state authorities.

Chart 1: BH’s Revenue Contribution by Service Type

Source: BH

Chart 2: BH’s Revenue Contribution by Nationality

Source: BH

At the end of August 2013, BH’s single largest shareholder was Bangkok Dusit Medical Services PLC (BGH), holding about 23.93% of BH’s total outstanding shares. BGH became BH’s largest shareholder since 2010. The second largest shareholder was Bangkok Bank PLC (BBL) and its affiliates, which includes BBL, Sinsuptawee

53% 52% 52% 53% 54%

47% 48% 48% 47% 46%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 7M13

OPD IPD

45% 43% 41% 39% 39%

55% 57% 59% 61% 61%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 7M13

Local Foreign

Page 3

Bumrungrad Hospital PLC 6 November 2013

Asset Management Co., Ltd., and Bangkok Insurance PLC. BBL and its affiliates together held approximately 23.6%. RECENT DEVELOPMENTS Set up a subsidiary in Hong Kong for overseas

investments BH set up a wholly-owned subsidiary, Live and

Longevity Limited, in Hong Kong, with registered capital of US$100,000 million. The company is a holding company, responsible for BH’s overseas investments.

Acquired land and a building

On 30 October 2013, BH acquired land and a 23-storey building on Rama 4 Road at a price of Bt837.5 million. The building will be used as dorm rooms for 1,000 nurses and accommodate about 300-400 back office employees. INDUSTRY ANALYSIS

The private healthcare segment of the healthcare service industry in Thailand has good growth prospects. Demand is being driven by an ageing population, the upcoming ASEAN Economic Community (AEC) in 2015, and Thailand’s widely-accepted reputation among foreign patients for good medical care. The Thai government tries to promote Thailand as a medical hub in Southeast Asia. However, a shortage of medical personnel and political instability will be major concerns for private hospital operators.

Healthcare expenditures are expected to rise

The Thai healthcare industry has grown steadily over the past 10 years. The compound annual growth rate (CAGR) of healthcare expenditures was around 6.5% from 2002 through 2012. Healthcare expenditures rose from around Bt214 billion in 2002 to Bt402 billion in 2012. The growth was driven mainly by the public sector. After the introduction of the universal healthcare scheme in 2002, Thai citizens are covered by at least one of three public health protection schemes. The three schemes are the universal healthcare scheme covering 75% of the population, the social security scheme (16%), and the civil servant medical benefits scheme (8%). Because of the expanded coverage, government healthcare expenditures increased from around 63% of total healthcare expenditures in 2002 to around 75% in the past five years.

Currently, Thailand is considered an aging society because the population aged more than 60 years old accounted for more than 10% of the total population. The National Economic and Social Development Board (NESDB) estimated that number of people aged 60 years old or higher will increase from 12% of the total population in 2010 to 18% in 2020 and 25% in 2030. The rising proportion of elderly will increase the demand for

healthcare services from both the public and private sectors.

Chart 3: Thailand’s Healthcare Expenditures

3.30%

3.40%

3.50%

3.60%

3.70%

3.80%

3.90%

4.00%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

% o

f G

DP

He

alth

care

Exp

en

dit

ure

s (B

t. M

il.)

Healthcare Expenditures % of GDP

Source: NESDB

Good prospects in medical tourism

Thailand is regarded as the most competitive destination for medical tourism, due to the availability of sophisticated medical care and treatments, lower costs, the service-minded attitude of Thai people, and the fact that Thailand is an attractive tourist destination. The private healthcare services available in Thailand have been widely accepted by foreign patients and international health insurance companies. The most popular medical services include health check-ups, cosmetic surgery, and dentistry.

Over the past 10 years, the number of foreign patients in Thailand grew at a CAGR of 15%. However, the 2008 global financial crisis affected medical tourism. The number of foreigners traveling to Thailand for medical services did not grow during 2008 and 2009.

Chart 4: No. of Foreign Patients Travelling to Thailand for

Medical Services

Source: Department of Export Promotion, Ministry of Commerce

0%

10%

20%

30%

40%

50%

60%

-

500

1,000

1,500

2,000

2,500

3,000

% G

row

th

No

. of

Fore

ign

Pat

ien

ts (

'00

0)

No. of foreign patients ('000) growth rate (%)

Page 4

Bumrungrad Hospital PLC 6 November 2013

The number rebounded sharply in 2010. The Ministry of Public Health (MOPH) estimates that medical tourism generates around Bt140 billion towards national income, of which around Bt70 billion is from private hospitals. Most foreign patients are from Japan, the United States (US), the United Kingdom (UK), United Arab Emirates (UAE), Qatar, and Australia. The number of foreign patients from neighboring countries is also growing significantly, especially patients from Myanmar. Investments are continuing Due to the upcoming AEC in 2015 and the growing number of foreign patients, major Thai private hospital operators have prepared themselves by merging with each other, expanding their existing capacities, and diversifying their networks of hospitals. Thus, the amount of investment in this industry is expected to continue over the next two to three years. Some of the major investments, which have already been announced, are: BGH’s plan to increase the number of hospitals under its umbrella from 31 hospitals to 50 hospitals within 2015, BH’s plan to build a new 200-bed hospital on Phetchaburi Road and expand its existing campus, and BCH’s plan to invest in three more hospitals in Bangkok, Nonthaburi, and Chiang Rai. The total amount of capital expenditures (excluding maintenance capital expenditures) at these three major hospitals during 2013-2016 is expected to be around Bt30 billion. Shortage of healthcare personnel is a concern

Thailand’s healthcare industry is developing rapidly and it continues to expand. The extent of coverage, services offered, and health care spending in both the public sector as well as the private sector continue to rise. Currently, the healthcare system covers around 67 million Thai people and around 2-2.5 million foreign patients. Going forward, the market will expand to cover a larger base, taking into account potential customers from ASEAN countries after the opening of the AEC. According to World Health Statistics 2011, using the average values across 2000 to 2010, Thailand had only three physicians and 15 nursing personnel per 10,000 population. These figures are relatively low compared with developed countries and major ASEAN countries. Therefore, the shortage of healthcare professionals is a major concern. Currently, some private hospitals have had to import nursing personnel from the Philippines.

Table 1: Health Workforce 2000-2010: Average Density per 10,000 Population

Country Physicians Nursing Personnel

Dentistry Personnel

Thailand 3.1 15.2 0.7

Singapore 18.3 59.0 3.2

Malaysia 9.4 27.3 1.4

United States 26.7 98.2 16.3

United Kingdom 27.4 103.0 5.2

Japan 20.6 41.4 7.4

Source: World Health Statistics 2011, World Health Organization

BUSINESS ANALYSIS

Leading private hospital in premium segment

BH’s strong business profile reflects its market position as a leading private hospital in the premium segment of Thailand’s healthcare service industry. The company’s flagship hospital in Bangkok, Bumrungrad International Hospital, has earned very strong brand recognition, built for over three decades. BH targets mostly premium local and foreign patients and competes by differentiating itself based on superior services and medical quality. The hospital is highly regarded for its broad range of specialist services, tertiary care, and use of advanced technologies.

BH is the second largest SET-listed healthcare provider in terms of revenue, following BGH. In TRIS Rating’s view, BH’s ability to generate strong and steady growth in revenues is underpinned by a strong brand name and a respected medical track record. Over the past five years, BH’s revenue has grown satisfactorily for two reasons: patient volumes and revenue intensity, after undertaking more complex cases which allow BH to charge higher prices. Notwithstanding, revenue intensity has played a larger role in driving growth over the years.

Chart 5: BH’s OP Visits per Day

Source: BH

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012 6M13

No. of

Patient

Page 5

Bumrungrad Hospital PLC 6 November 2013

Chart 6: BH’s OP Revenue per Visit

Source: BH

Chart 7: BH’s IP Days

Source: BH

Chart 8: BH’s IP Revenue per Admission

IP days = average daily census x number of days Source: BH

Strong position in medical tourism segment

BH’s business profile is supported by a strong share in the medical tourism segment as Thailand is one of the most popular medical hubs in the Asia Pacific region. BH has successfully maintained a steady number of foreign patients during the past several years. The number of

foreign OP visits per day ranged between 1,100-1,400 visits per day or approximately 45% of daily OP visits. Foreign patients also accounted about half of the total IP admission during the past three years.

About 60% of BH’s total revenue has been derived from foreign patients, particularly patients from the Middle East. Patients from the UAE, BH’s top foreign patient group, accounted for 8%-11% of BH’s total revenue during the past three years. BH’s strong market position among the Middle East patients is derived from the company’s established referral network, as well as the location of its flagship facility, which is in the Middle Eastern neighborhood of Bangkok.

Chart 9: BH’s Revenue by Patient Nationality (Jan-Jun 2013)

Source: BH

In TRIS Rating’s view, by accepting foreign patients,

BH has diverse sources of revenue, reducing its reliance on domestic demand and reducing competitive pressure. The large number of foreign patients also yields economies of scale, as overhead costs for hospitals accepting foreign patients are relatively high. However, Thailand’s ongoing political instability may drive away foreign patients. BH would be more adversely affected, compared with other private hospital operators.

Capacity expansion focused on domestic market

Over the next five years, BH plans to focus on the domestic market. The growth will come from the on-going plan to expand the capacities of the OP and IP departments at its flagship facility. BH also has new expansion project on its newly acquired land plots on Petchburi Road and Sukhumvit Soi 1. The land plot on Petchburi Road will house a 200-bed hospital facility. Construction is expected to finish by 2017. The land plot on Sukhumvit Soi 1 will add capacity to its near-by flagship facility. The total investment for these two projects is approximately Bt9,800 million, excluding land costs.

The capacity expansions will help reduce BH’s reliance on a single location. BH has been looking for

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2008 2009 2010 2011 2012 6M13

Baht per visit

0

25,000

50,000

75,000

100,000

125,000

150,000

2008 2009 2010 2011 2012 6M13

No. of IP

Days

0

50,000

100,000

150,000

200,000

250,000

300,000

2008 2009 2010 2011 2012 6M13

Baht per

admission

Thai, 38%

UAE, 8%

Myanmar, 7%

Oman, 5%

US, 5%

Qatar, 3%

Others, 34%

Page 6

Bumrungrad Hospital PLC 6 November 2013

acquisition opportunities for its second brand in the upper mid-tier segment or an expansion abroad. Although expansion strategy offers benefits from diversification, TRIS Rating believes that it will take some time for BH to find and execute a deal. FINANCIAL ANALYSIS Continue delivering strong profitability

BH is expected to continue delivering solid operating performance. The company reported revenue of Bt7,004 million for the first half of 2013, up by 10% from the same period last year. The revenue increase was driven mainly by higher revenue intensity. The company’s operating margin has been strong and stable over the past few years, ranging between 23%-26%. BH’s operating margins have stayed consistently above the average operating margin of other SET-listed healthcare providers by around 5%-8%. The company’s ability to increase prices reflects the strong demand for premium healthcare services.

Chart 10: BH’s Operating Margin VS SET-listed Peers

Sources: 1) BH

2) TRIS Rating’s calculation

In the medium term, TRIS Rating expects BH’s revenue to grow by at least 5%-8% per annum during the next three years. Operating margins are expected to remain quite stable, at 23%-25%. Sound capital structure despite expansion

BH’s capital structure is expected to remain strong during its investment period. At the end of June 2013, BH had Bt6,120 million in cash on hand, while total debt was only Bt4,958 million. In addition, BH is expected to generate FFO of Bt2.5-Bt3 billion per annum over the next three years. The remaining cash on hand and its relatively stable cash flow from operations will be sufficient to fund its planned capital expenditures and dividend payments. The company plans to spend approximately Bt3-Bt3.5 billion in capital annually over the next three years. The planned capital expenditures are mainly for its expansion projects and maintenance. Dividend payments is expected to be around Bt1 billion per annum. The company has no debt due during the next 12 months.

BH has approximately Bt3.3 billion in uncommitted, undrawn credit lines with banks. This amount leaves plenty of financial flexibility for BH to pursue any acquisition opportunity that may arise. At the end of June 2013, BH’s debt to capitalization ratio stood at 36.8%. Under TRIS Rating’s base case scenario, BH’s debt to capitalization ratio is expected to stay at 30%-35%. In order to maintain the company’s credit quality, the debt to capitalization ratio should be kept below 50%.

0%

5%

10%

15%

20%

25%

30%

2006 2007 2008 2009 2010 2011 2012 6M13

BH SET-listed Peers

Page 7

Bumrungrad Hospital PLC 6 November 2013

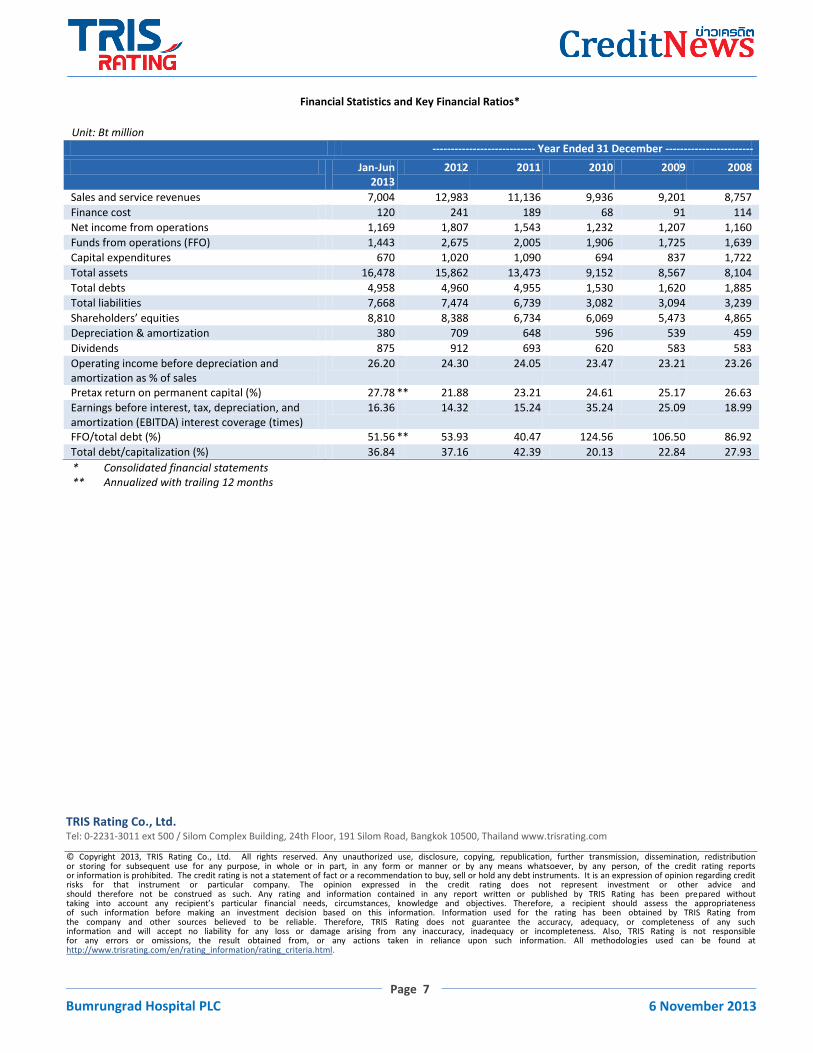

Financial Statistics and Key Financial Ratios*

Unit: Bt million

* Consolidated financial statements ** Annualized with trailing 12 months

TRIS Rating Co., Ltd. Tel: 0-2231-3011 ext 500 / Silom Complex Building, 24th Floor, 191 Silom Road, Bangkok 10500, Thailand www.trisrating.com

---------------------------- Year Ended 31 December ------------------------

Jan-Jun 2013

2012 2011 2010 2009 2008

Sales and service revenues 7,004 12,983 11,136 9,936 9,201 8,757

Finance cost 120 241 189 68 91 114

Net income from operations 1,169 1,807 1,543 1,232 1,207 1,160

Funds from operations (FFO) 1,443 2,675 2,005 1,906 1,725 1,639

Capital expenditures 670 1,020 1,090 694 837 1,722

Total assets 16,478 15,862 13,473 9,152 8,567 8,104

Total debts 4,958 4,960 4,955 1,530 1,620 1,885

Total liabilities 7,668 7,474 6,739 3,082 3,094 3,239

Shareholders’ equities 8,810 8,388 6,734 6,069 5,473 4,865

Depreciation & amortization 380 709 648 596 539 459

Dividends 875 912 693 620 583 583

Operating income before depreciation and amortization as % of sales

26.20 24.30 24.05 23.47 23.21 23.26

Pretax return on permanent capital (%) 27.78 ** 21.88 23.21 24.61 25.17 26.63

Earnings before interest, tax, depreciation, and amortization (EBITDA) interest coverage (times)

16.36 14.32 15.24 35.24 25.09 18.99

FFO/total debt (%) 51.56 ** 53.93 40.47 124.56 106.50 86.92

Total debt/capitalization (%) 36.84 37.16 42.39 20.13 22.84 27.93

© Copyright 2013, TRIS Rating Co., Ltd. All rights reserved. Any unauthorized use, disclosure, copying, republication, further transmission, dissemination, redistribution or storing for subsequent use for any purpose, in whole or in part, in any form or manner or by any means whatsoever, by any person, of the credit rating reports or information is prohibited. The credit rating is not a statement of fact or a recommendation to buy, sell or hold any debt instruments. It is an expression of opinion regarding credit risks for that instrument or particular company. The opinion expressed in the credit rating does not represent investment or other advice and should therefore not be construed as such. Any rating and information contained in any report written or published by TRIS Rating has been prepared without taking into account any recipient’s particular financial needs, circumstances, knowledge and objectives. Therefore, a recipient should assess the appropriateness of such information before making an investment decision based on this information. Information used for the rating has been obtained by TRIS Rating from the company and other sources believed to be reliable. Therefore, TRIS Rating does not guarantee the accuracy, adequacy, or completeness of any such information and will accept no liability for any loss or damage arising from any inaccuracy, inadequacy or incompleteness. Also, TRIS Rating is not responsible for any errors or omissions, the result obtained from, or any actions taken in reliance upon such information. All methodologies used can be found at http://www.trisrating.com/en/rating_information/rating_criteria.html.