burnley borough council pendle borough council

TRANSCRIPT

Burnley Borough Council Pendle Borough Council

Update Report 2010

Adopted 8th February 2011

Table o f Contents

Page i

Table of Contents

1. Introduction to study .........................................................................................................................1

2. Site appraisals ....................................................................................................................................3

3. Appraisal results ..............................................................................................................................11

4. Threshold modelling: results ..........................................................................................................17

5. Study findings...................................................................................................................................23

6. Dynamic Viability: Burnley ..............................................................................................................27

7. Dynamic Viability: Pendle................................................................................................................35

Appendix 1. Newbuild schemes .........................................................................................................43

Appendix 2. Proposed Burnley benchmark appraisal......................................................................45

Appendix 3. Proposed Pendle benchmark appraisal .......................................................................53

Appendix 4. Financial appraisal summaries .....................................................................................61

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page i i

1. In t roduct ion to s tudy

Page 1

1. Introduction to study

Introduction

1.1 This report provides the results of an update of affordable housing viability in Burnley and Pendle. The

study was commissioned by the two Borough Councils to provide guidance on the scope for seeking

affordable housing in the market conditions of June 2010, from sites both above and below the

national guidance threshold of 15 dwellings (PPS3, DCLG).

Basis for study

1.2 The work builds upon and draws from, an earlier study by Fordham Research for Burnley and Pendle

Borough Councils, an Affordable Housing Site Viability Study (AHSVS) for the Burnley & Pendle

Housing Market Area. Whilst the final study report was published in October 2009, the work was

primarily carried out in November and December 2008, and reflects the market conditions which

prevailed at that time.

1.3 That study was designed to produce guidance on affordable housing targets and site viability for each

Council area. To achieve this, financial appraisals were prepared for a total of 16 sites across the two

areas. The final AHSVS Report set out the results of those appraisals, and made recommendations in

respect of targets for each Council area.

1.4 At the time of the original study, house prices had been declining since the onset of housing finance

difficulties (commonly termed the ‘credit crunch’) in late 2007, which by the time of the study had

developed into a major economic downturn. Despite the continuing difficult economic conditions,

house prices began to recover from mid 2009 but have again faltered during 2010. The present report:

• Updates the financial appraisals of the original 16 sites to reflect the market conditions of June

2010, and provides recommendations on what affordable targets would now be deliverable in

the two Councils’ areas on sites above the national guidance threshold

• carries out further analysis of viability on sites below the national guidance threshold and

produces appropriate policy guidance for small sites

• sets out a methodology (‘Dynamic Viability’) which will allow the affordable targets to be

revised periodically as market conditions change, by applying nationally published index

figures to a pre-programmed matrix of percentage targets

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 2

2. S i te appra isa ls

Page 3

2. Site appraisals

Relationship to AHSVS

2.1 The 16 sites in the AHSVS were actual sites; eight in each Borough area. Of the total, only one site

was below the national guidance threshold of 15 dwellings – Pendle Site P7, land at Warehouse Lane,

Foulridge (12 dwellings, 0.34 ha). Consequently, the AHSVS could provide only very limited guidance

on viability below the size threshold specific to Burnley and Pendle.

2.2 This report provides details of the assumptions used to produce updated appraisals for the 16 sites.

The bulk of the appraisal assumptions remained as they were in the AHSVS, and are not repeated

here. Where specific assumptions are identified and discussed below, to aid understanding we have

followed as far as possible the sequence of topic headings used in the earlier report.

AHSVS update sites

2.3 For convenience the AHSVS site details are summarised below.

Table 2.1 Site details

Area ha SiteRef Site

gross net Dw

Densitynet

(dw/ha) Planning status

B1 Dorma, Burnley 1.97 1.97 110 55.8 Approved

B2 Summit Works, Burnley 0.45 0.45 25 55.6 Under construction

B3 Park Mill, Burnley 1.35 1.35 77 57.0 Under construction

B4 Spa Mill, Padiham 1.40 1.40 55 39.3 Under construction

B5 Former Coal Yard, Burnley 1.90 1.90 57 30.0 Proposed site

B6 Langham St, Burnley 3.20 3.20 96 30.0 Proposed site

B7 Gorple Mill, Worsthorne 0.90 0.90 27 30.0 Proposed site

B8 Albion Mill, Padiham 1.20 1.20 36 30.0 Proposed site

P1 Lob Lane Mill, Brierfield 1.00 1.00 99 99.5 Approved

P2 Richard St, Brierfield 0.98 0.98 70 71.1 Refused (Oversupply)

P3 Lamberts Woodyard, Nelson 0.90 0.90 52 58.1 Approved

P4 J Nelson Sports Club, Nelson 1.81 1.81 65 35.9 Proposed

P5 Spen Brook Mill, Spen Brook 0.90 0.90 52 58.0 Proposed site

P6 Glen Mill, Colne 1.24 1.24 37 29.9 Proposed site

P7 Warehouse Lane, Foulridge 0.34 0.34 12 35.3 Proposed site

P8 Garage Site, Earby 0.63 0.63 35 55.3 Proposed site

Source: Affordable Housing Site Viability Study Table 2.1

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 4

Affordable housing assumptions

2.4 Update appraisals were prepared for 10%, 20%, 30% and 40% options, as originally, and with a

tenure split of 90/10 social rented/intermediate for Burnley, but 80/20 for Pendle. The financial terms –

the prices at which RSLs would purchase affordable housing provided by a developer – were updated

to current values from spring 2008. As before, the assumption of zero grant support applies and that

properties would be built to Sustainable Homes Code Level 3.

2.5 After considering evidence from the Retail Price Index (RPI), social rented values were uplifted by

3.75% (RPI November 2008 216.0, June 2010 224.1). After consideration, the intermediate prices

were increased by a similar amount.

2.6 The resulting figures are compared to the previous (AHSVS) figures, below.

Table 2.2 Affordable housing purchase prices

November 2008 June 2010 Category Type

£ per sq ft £ per sq m £ per sq ft £ per sq m

Social rented Flat 70 753 72.5 781

House 80 861 83 893

Intermediate Flat 104 1,120 108 1,162

House 104 1,120 108 1,162 Source: Affordable Housing Viability Update Fordham Research 2010

Other developer contributions

2.7 In the main study, developer contributions assumptions were based upon a modelled approach

drawing on contributions sought or achieved on a number of sites in the two Council areas. The

approach assumed an average contribution figure of £3,000 per dwelling, which was applied

generally, but increased to £3,500 per dwelling for the substantial greenfield site P4 (James Nelson

Sports Club, to allow for a larger transport contribution.

2.8 Most established contributions policies provide for the average per dwelling contribution to reduce on

the smallest sites, as size thresholds for the individual elements come into play. However with the

smallest site being 12 dwellings no reduction was assumed. Developer contributions policies are

currently under review. With the possibility of a move to a tariff based system, the across the board

approach seems in any case a sensible one.

2.9 It is necessary to allow for cost inflation from the November 2008 base date; the figures were

therefore increased by 3.75%, though then also rounded to reflect the strategic approach being used.

This gave a general figure of £3,100 per dwelling and a higher figure of £3,650 per dwelling at site P4.

2. S i te appra isa ls

Page 5

2.10 As with the figures in the main study, we must emphasise that these figures cannot be assumed to

reflect the contributions that would arise in practice, either in amount or topic coverage.

Price assumptions for financial appraisals

2.11 It was necessary to carry out a current housing market survey in order to form a view about the

appropriate prices to assume as at June 2010 for the 16 AHSVS sites. The Halifax quarterly Regional

House Price Index figures since the peak Q4 2007 are shown in the table below.

Table 2.3 Price index movements

Period North West Region House Price Index

2007 Q4 604.0

2008 Q1 597.3

2008 Q2 575.7

2008 Q3 536.1

2008 Q4 500.4

2009 Q1 485.4

2009 Q2 474.2

2009 Q3 502.9

2009 Q4 501.7

2010 Q1 493.8 North West Region All Buyers Seasonally Adjusted 2010

Source: Halifax Price Index

2.12 It can be seen that the regional index figure fell steadily from the peak to Q2 2009, and after a

relatively strong surge to Q3 of 2009 has made no further progress. The Q2 figure for 2010 will make

it clear in due course where prices stood at June 2010, but this figure will not be available just yet.

However, between the time of the AHSVS and Q1 2010, the regional data suggest prices have moved

very little – 500.4 to 493.8, a drop of 1.3%.

2.13 There is very little new build housing currently available to provide comparables for the appraisal

updates. The details of what is currently available as at June 2010 are set out in Appendix 1. Taking

these and the index data into consideration we came to the view that there was only limited scope for

changing the base price structure in the 2008 study of £150/£145/£135 per sq ft for flats,

detached/semis, and terraced town houses (£1,615/£1,560/£1,453 per sq m). It appeared that prices

for two storey detached and semis of reasonable quality had edged just a little higher to around £150

per sq ft, whilst the flat and town house figures should be left unchanged.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 6

2.14 In the 2008 study the majority of sites were priced at these base levels. Two green edge sites, B6

Langham St Burnley and P4 Sports Club Nelson, received a modest premium, and the two rural sites

a more substantial mark-up, whilst prices on one urban site (B8 Albion Mill Padiham) were slightly

discounted. For the update the first and last of these groups were adjusted in line with the base, whilst

the middle group was left unchanged.

2.15 As before, the sale prices for the three categories were combined on the basis of the proportions in

each scheme, to produce a single composite average price. The resulting figures are set out in Table

2.4 below.

Table 2.4 Price bands

Price £ per Price £ per Site/location

Sq ft Sq m Site/location

Sq ft Sq m

Dorma 150 1,614 Lob Lane Mill Brierfield 135 1,453

Summit Wks 143 1,533 Richard St Brierfield 135 1,453

Park Mill 139 1,493 Lamberts Woodyard 143 1,533

Spa Mill 143 1,533 J Nelson Sports Club 161 1,727

Former Coal Yard 143 1,533 Spen Brook Mill 225 2,421

Langham St 143 1,533 Glen Mill 146 1,574

Gorple Mill Worsthorne 161 1,727 Warehouse La Foulridge 185 1,991

Albion Mill Padiham 138 1,480 Garage Site Earby 139 1,493 Source: Affordable Housing Update Fordham Research 2010

Current and Alternative Use Values

2.16 All but two of the sites in the AHSVS were assumed to have the industrial benchmark value; P7

Warehouse Lane was given agricultural value and the open space/sports club at P4 an intermediate

value between the two.

2.17 The likely change to alternative use values was considered. The 2008 study used a benchmark value

of £175k per acre (£430k per ha) for industrial/warehousing land throughout the two Council areas.

The agricultural value was assumed to be £10k per acre (£25k per ha).

2.18 We looked at update data on industrial values from the Valuation Office Agency’s (VOA) Property

Market report.

2. S i te appra isa ls

Page 7

Table 2.5 Industrial land values

Value of typical industrial land per ha over half year period ending

Jan 08 Jul 08 Jan 09 Jul 09 Jan 10

North West Region 502 502 460 409 n/a

Liverpool 275 275 250 240 450

Manchester 650 650 600 540 650

Leeds 900 750 600 540 600

Blackburn/Burnley 500 500 475 380 n/a

Rochdale/Oldham 475 475 435 390 n/a

Bolton/Bury 550 550 500 450 n/a

Preston/Central Lancs 625 625 625 500 n/a Source: Valuation Office Agency Property Market Reports

2.19 Unfortunately, from the January 2010 issue the Property Market Report appears with a much more

limited range of locations, and no regional average. Consequently we have very limited guidance on

local movements in values since the middle of 2009. We can see that the value of £190k per acre

(£475k per ha) for Blackburn/Burnley in late 2008 slipped to around £155k per acre (£380k per ha) in

early 2009, with slightly smaller falls (typically around 10%) in other nearby locations. However, we do

not know to what extent if any it has now recovered: we only have subsequent information for the big

urban centres of Liverpool, Manchester and Leeds, where values have picked up, though to varying

degrees.

2.20 There is limited guidance from industrial land currently on the market in the two areas. We have found

examples of land at £127k and £225k per acre, and another recently offered for sale at Accrington

(2.4 acres at £177k per acre/£438k per ha). Although it is possible that land values in Burnley and

Pendle may have fallen back just a little since November 2008 we have not got sufficient evidence to

support a specific reduction in the previous benchmark of £175k per acre/£430k per ha. After

consideration, therefore, we left the benchmark value unchanged.

2.21 The most recent Property Market Report gives a value for agricultural land at January 2010 of £7,000

per acre/£17,290 per ha (Equipped Mixed land with vacant possession Lancashire) - identical to the

January 2009 figure for the North West Region (which is not now published). This suggests that the

2008 benchmark value of £10k per acre could be left unchanged. Similarly the threshold value of £75k

per acre for the sports club land at P4 was retained.

2.22 The resulting values area as set out in the table below.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 8

Table 2.6 Alternative Use Value bases

Ref Site Basis £k per acre £k per ha

P7 Warehouse Lane, Foulridge agricultural 10 25

P4 J Nelson Sports Club, Nelson open space 75 185

All other sites industrial 175 430

Source: Affordable Housing Update Fordham Research2010

Development costs

(i) Construction costs

2.23 In the AHSVS, build costs for all (market and affordable) housing were built up from the Fordham data

base for houses and flats, re-based to a November 2008 base date using a BCIS cost index, and

adjusted to meet the requirements of CSH Level 3 and 10% renewables. A ‘small site’ premium of 3%

was added for the one site of fewer than 15 dwellings – P7.

2.24 The general cost level was adjusted to the new June 2010 base date using BCIS index figures (295.9

compared to the 289.3 used in AHSVS rebasing).

2.25 The final build cost figures following these adjustments and allowing for the mix of houses and flats on

each site, are as in the table below.

Table 2 7 Construction costs adjusted and

rounded

Build cost £ per sq ft/sq m

Site sq ft sq m Site sq ft sq m

B1 88.0 947 P1 101.8 1,095

B2 85.4 919 P2 99.2 1,068

B3 90.5 974 P3 99.2 1,068

B4 89.0 958 P4 83.4 897

B5 83.9 903 P5 96.7 1,040

B6 84.9 914 P6 83.9 903

B7 83.4 897 P7 85.9 925

B8 87.5 941 P8 85.5 920 Source: Affordable Housing Update Fordham Research 2010

2. S i te appra isa ls

Page 9

(ii) Other development costs et alia

2.26 Alongside the per sq ft/sq ms build costs, a range of allowances provided for other costs of

development including infrastructure costs, estimated site specific abnormals, contingency and fees.

Except for abnormals, the AHSVS dealt with these as percentage allowances on build cost, so that

they increase automatically with a rise in build costs. Although abnormals were identified as site

specific cash sums, they were entered into the appraisal software as a site specific additional

percentage mark-up on build cost, and are therefore subject to the same automatic updating process

in practice.

Financial and other appraisal assumptions:

2.27 All the other appraisal assumptions were left unchanged, including interest rate, developer’s profit and

phasing assumptions.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 10

3. Appra isa l resu l ts

Page 11

3. Appraisal results

Appraisals

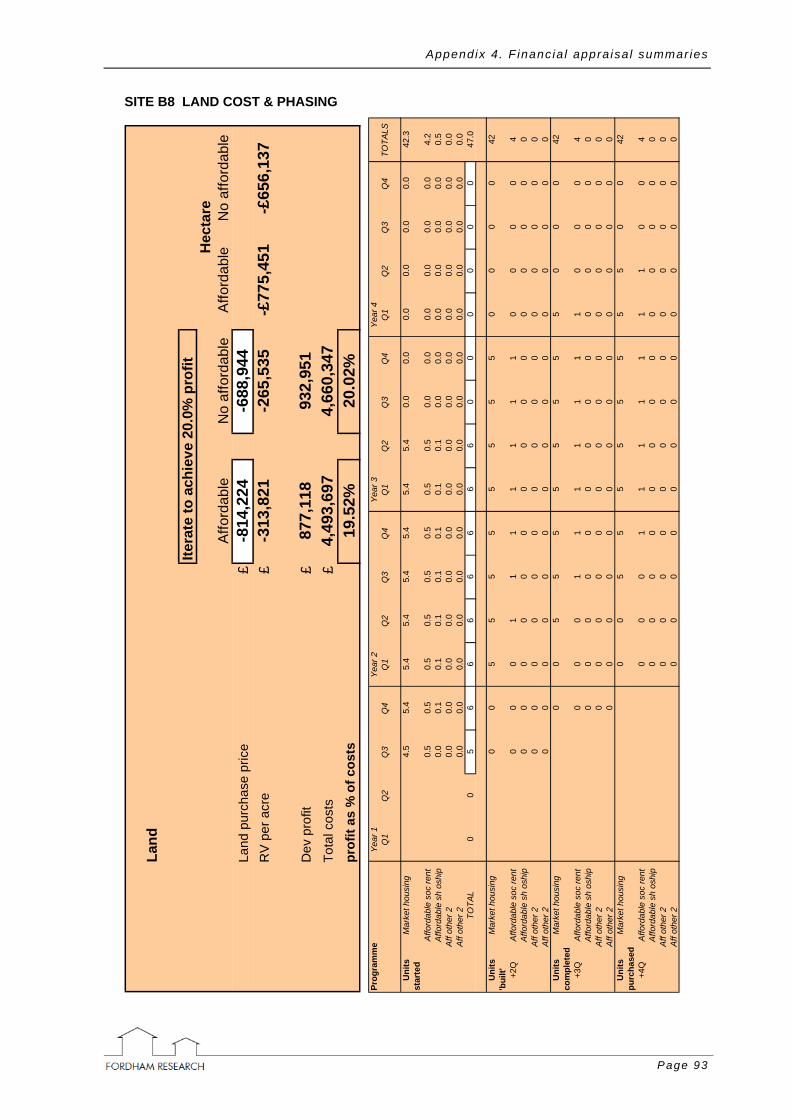

3.1 Update appraisals were prepared for the 16 AHSVS sites. Appendix 4 provides the appraisal

summaries for each site.

Results of viability analysis

3.2 The results of the two sets of appraisals, for prices and costs as at June 2010, are set out below. As in

the main AHSVS report they are expressed as residual values.

Table 3.1 Appraisal results for five affordable options

Zero grant: shared ownership at 25% share

Residual value £k per acre for affordable option: No Site

No aff 10% 20% 30% 40%

B1 Dorma, Burnley -170 -245 -321 -397 -473

B2 Summit Works, Burnley -129 -206 -285 -364 -443

B3 Park Mill, Burnley -304 -364 -424 -485 -547

B4 Spa Mill, Padiham -199 -269 -339 -409 -479

B5 Former Coal Yard, Burnley -50 -100 -149 -199 -250

B6 Langham St, Burnley -107 -156 -206 -256 -306

B7 Gorple Mill, Worsthorne 95 35 -27 -87 -150

B8 Albion Mill, Padiham -266 -314 -362 -412 -461

P1 Lob Lane Mill, Brierfield -1,175 -1,282 -1,387 -1,493 -1,601

P2 Richard St, Brierfield -633 -701 -772 -841 -911

P3 Lamberts Woodyard, Nelson -512 -580 -648 -717 -786

P4 J Nelson Sports Club, Nelson 103 48 -10 -70 -129

P5 Spen Brook Mill, Spen Brook 371 227 79 -75 -230

P6 Glen Mill, Colne -73 -124 -174 -226 -276

P7 Warehouse Lane, Foulridge 345 271 189 107 25

P8 Garage Site, Earby -220 -276 -333 -391 -449 Source: Affordable Housing Update Fordham Research 2010

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 12

3.3 Table 3.1 shows that, as with the AHSVS, with no requirement for affordable housing all but four of the

sites deliver a negative residual land value. As before, the residual value for the two rural Pendle sites

is quite substantial, around £350k per acre, with lesser figures around £100k per acre for the two

green edge sites. For the rest of the sites, the figures suggest that in present conditions most are

unlikely to come forward.

3.4 Land values fall away as increasingly high affordable housing requirements are sought; as before they

do so more rapidly on the two higher value sites P5 and P7, and also the higher density site P1.

Alternative use benchmarks

3.5 The results from the above table have to be compared with the alternative use value in order to show

whether the site is viable. To be viable the site has to deliver more value than the alternative use, and

by a margin that provides some incentive to the landowner. That margin was called the ”cushion’’ in

the AHSVS. In the AHSVS a fixed value of £40k per acre was used for the cushion for all sites except

for the greenfield site P7 which had only agricultural value, where it was increased to £90k per acre.

3.6 On several sites there were assumed to be some abnormal costs involved in achieving the alternative

use value. For simplicity we did not index the cost element and so the viability thresholds and cushion

values set out in AHSVS Table 6.2 were carried over unchanged to the current study. By comparing

the results from Table 3.1 with the alternative use values, we obtain a view of the likely viability of the

affordable options for each site. This is set out below in Table 3.2. As in the AHSVS, a site is only

viable if it produces a Residual Value fully equalling the required alternative use value plus cushion. If

the site’s Residual Value exceeds the Table 6.2 alternative use value but not by the full amount of the

cushion, it is considered marginal; the landowner may not receive sufficient incentive to bring the site

forward.

Table 3.2 Appraisal outcomes: base appraisals

Value £k per acre No Site Alt use

value No

affordable 10% 20% 30% 40%

B1 Dorma, Burnley 135-175 -170 -245 -321 -397 -473

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

B2 Summit Works, Burnley 160-200 -129 -206 -285 -364 -443

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

B3 Park Mill, Burnley 160-200 -304 -364 -424 -485 -547

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

B4 Spa Mill, Padiham 160-200 -199 -269 -339 -409 -479

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

3. Appra isa l resu l ts

Page 13

Table 3.2 Appraisal outcomes: base appraisals

Value £k per acre No Site Alt use

value No

affordable 10% 20% 30% 40%

B5 Former Coal Yard, Burnley 160-200 -50 -100 -149 -199 -250

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

B6 Langham St, Burnley 160-200 -107 -156 -206 -256 -306

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

B7 Gorple Mill, Worsthorne 160-200 95 35 -27 -87 -150

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

B8 Albion Mill, Padiham 160-200 -266 -314 -362 -412 -461

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

P1 Lob Lane Mill, Brierfield 135-175 -1,175 -1,282 -1,387 -1,493 -1,601

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

P2 Richard St, Brierfield 160-200 -633 -701 -772 -841 -911

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

P3 Lamberts Woodyard, Nelson 160-200 -512 -580 -648 -717 -786

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

P4 J Nelson Sports Club, Nelson 80-120 103 48 -10 -70 -129

MARGINAL NOT VIAB NOT VIAB NOT VIAB NOT VIAB

P5 Spen Brook Mill, Spen Brook 160-200 371 227 79 -75 -230

VIABLE VIABLE NOT VIAB NOT VIAB NOT VIAB

P6 Glen Mill, Colne 135-175 -73 -124 -174 -226 -276

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

P7 Warehouse Lane, Foulridge 10-100 345 271 189 107 25

VIABLE VIABLE VIABLE VIABLE MARGINAL

P8 Garage Site, Earby 175-215 -220 -276 -333 -391 -449

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB Source: Affordable Housing Update Fordham Research 2010

Comparison results

3.7 With zero affordable housing, two sites are viable, as at 2008 in the AHSVS. However the 2010

update shows that there is now one other marginal site, P4.

3.8 At 10% the marginal site becomes unviable, leaving two viable sites as with the AHSVS. Spen Brook

P5 becomes unviable at 20%, whilst P7 warehouse Lane remains viable through to 30%. This is again

in line with the AHSVS. In fact Warehouse Lane becomes marginal at 40%.

3.9 It should be noted that Warehouse Lane is the smallest site, with 12 dwellings.

3.10 The results are summarised below.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 14

Table 3.3 Viability by site size

Sites viable with Status

No afff 10% aff 20% aff 30% aff 40% aff

Burnley 0 viable

8 unviable

0 viable

8 unviable

0 viable

8 unviable

0 viable

8 unviable

0 viable

8 unviable

Pendle

2 viable

1 marginal

5 unviable

2 viable

6 unviable

1 viable

7 unviable

1 viable

7 unviable

0 viable

1 marginal

7 unviable Source: Affordable Housing Update Fordham Research 2010

3.11 The implications for what the affordable targets should be as at June 2010 market conditions, are

taken forward in the next chapter. Before that we consider the sensitivity of the results to changes in

the basic assumptions, in particular cost and price levels.

Sensitivity: price and cost levels

3.12 We carried out sensitivity testing to show how possible changes in market conditions impacted upon

the base appraisal outcomes.

3.13 Whilst clearly over the lifetime of the two Boroughs’ LDF policies prices are likely to recover – and

indeed move ahead of costs – the short term may well see prices falling back. We therefore looked at

the impact of a 10% reduction in market prices, and a return to the market peak level of autumn 2007.

The results for these under the 10% affordable option are compared to those from the base appraisals

(i.e. current market prices and costs) in the table below. The peak level was assumed to be prices 19-

20% above current levels, and costs 8-9% lower.

Table 3.4 Appraisal outcomes: sensitivity on price

Value £k per acre for 10% affordable with

No Site Alt use value

BASE Current prices

PRICES DOWN

10%

PRICES MARKET

PEAK B1 Dorma, Burnley 135-175 -245 -417 229

NOT VIAB NOT VIAB VIABLE

B2 Summit Works, Burnley 160-200 -206 -403 346

NOT VIAB NOT VIAB VIABLE

B3 Park Mill, Burnley 160-200 -364 -518 76

NOT VIAB NOT VIAB NOT VIAB

B4 Spa Mill, Padiham 160-200 -269 -436 202

NOT VIAB NOT VIAB VIABLE

3. Appra isa l resu l ts

Page 15

Table 3.4 Appraisal outcomes: sensitivity on price

Value £k per acre for 10% affordable with

No Site Alt use value

BASE Current prices

PRICES DOWN

10%

PRICES MARKET

PEAK B5 Former Coal Yard, Burnley 160-200 -100 -226 252

NOT VIAB NOT VIAB VIABLE

B6 Langham St, Burnley 160-200 -156 -281 197

NOT VIAB NOT VIAB MARGINAL

B7 Gorple Mill, Worsthorne 160-200 35 -97 392

NOT VIAB NOT VIAB VIABLE

B8 Albion Mill, Padiham 160-200 -314 -434 57

NOT VIAB NOT VIAB NOT VIAB

P1 Lob Lane Mill, Brierfield 135-175 -1,282 -1,547 -514

NOT VIAB NOT VIAB NOT VIAB

P2 Richard St, Brierfield 160-200 -701 -863 -226

NOT VIAB NOT VIAB NOT VIAB

P3 Lamberts Woodyard, Nelson 160-200 -580 -747 -88

NOT VIAB NOT VIAB NOT VIAB

P4 J Nelson Sports Club, Nelson 80-120 48 -82 401

NOT VIAB NOT VIAB VIABLE

P5 Spen Brook Mill, Spen Brook 160-200 227 -1 871

VIABLE NOT VIAB VIABLE

P6 Glen Mill, Colne 135-175 -124 -261 243

NOT VIAB NOT VIAB VIABLE

P7 Warehouse Lane, Foulridge 10-100 271 115 687

VIABLE VIABLE VIABLE

P8 Garage Site, Earby 175-215 -276 -437 177

NOT VIAB NOT VIAB MARGINAL

Source: Affordable Housing Update Fordham Research 2010

3.14 Were there to be a further fall of 10% in prices relative to costs, only one site would still be viable at

10%. The improvement in prices in the second half of 2009 made the prospect of a further significant

fall in prices less likely. However the improvement is not universally accepted to be the beginning of a

steady recovery; there has been no clear pattern to price movements in 2010. At present many

commentators believe a downwards adjustment is a strong possibility in the immediate short term.

3.15 On the other hand over the longer term it is reasonable to expect that market conditions will improve

significantly. Over the length of the LDF plan period, land values are likely to recover to at least their

position at the 2007 market peak.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 16

3.16 The results for a return to the ‘market peak’ price/cost relationship show that 10% affordable housing

could reasonably be sought in both Burnley and Pendle. Altogether nine sites are viable, and two

marginal.

3.17 This underlines the importance of a flexible approach to target setting, which will allow a significant

improvement in prices to be reflected in the affordable target as and when such an improvement is

manifested.

4. Threshold model l ing: resu l ts

Page 17

4. Threshold modelling: results

Introduction

4.1 This chapter sets out how viability assessments of model sites were prepared to provide guidance on

the threshold issue, and presents the appraisal results of the model sites.

Modelling variations in scheme size

4.2 Of the AHSVS sites, P7 Warehouse Lane (12 dwellings) is the only site of fewer than 15 dwellings,

and can therefore provide only limited guidance on viability for sites below the national guidance

threshold.

4.3 In order to provide more robust support on the scope for reducing thresholds in either Borough area, it

was necessary to look at model sites. In order to provide a full picture of how viability varied between

five and 15 dwellings, we created a suite of model sites with the same characteristics as the greenfield

site P7. It was felt that, with only a few exceptions considered below, assumptions from the actual site

could reasonably be carried over to the model sites; otherwise, that meant that the model sites were

greenfield, on agricultural land, with a built form of 100% two storey houses.

4.4 Firstly, we recognised that as site size declines it may be increasingly difficult to achieve the same site

utilisation efficiency. Therefore as site size varied we allowed the development density (sq ft

floorspace per acre/sq m per ha) to vary, increasing above 12 dwellings though at a declining rate,

and decreasing below 12 dwellings, at an increasing rate. Since the average floor area of the

dwellings remained constant this was achieved by varying the site area (i.e. so that it did not vary fully

pro rata with dwelling numbers).

4.5 Secondly, we built in loadings for the build cost which varied with scheme size but were consistent

with the 3% loading for 12 dwellings in the AHSVS and referred to 2.23.

4.6 Thirdly, we considered whether the developer contribution assumption should vary to reflect some

minimum contributions threshold. Whilst In Pendle the contribution would reduce below 10 dwellings,

in Burnley it would not. Taking a ‘worse case’ approach it was decided to leave the developer

contribution figure, used for the 12 dwellings at site P7, unchanged throughout.

4.7 Finally we considered whether as site size declined below 12 dwellings, values might at some point

improve to reflect a ‘non-estate’ type of location. However it was difficult to decide in the abstract

model situation where this might arise, and so no adjustments were made to values.

4.8 The variant floorspace densities and build costs are set out in the table below.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 18

Table 4.1 Variant assumptions for model

threshold sites

build cost No of dwgs

floorspace density

sq ft per acre + % loading £ per sq ft

15 13,800 0.00% 83.4

14 13,790 1.00% 84.3

13 13,775 2.00% 85.1

12 13,755 3.00% 85.9

11 13,730 4.00% 86.8

10 13,705 5.00% 87.6

9 13,675 6.00% 88.4

8 13,640 7.25% 89.5

7 13,600 8.50% 90.5

6 13,555 10.00% 91.8

5 13,500 12.00% 93.4

4 13,440 14.00% 95.1

3 13,350 16.00% 96.8

Source: Fordham Research derived from analysis of BCIS cost data

Viability results

4.9 Using the above assumptions, and deriving from the ‘actual site’ appraisals for Site P7, appraisals

were prepared for two suites of model sites.

4.10 The first used house prices at £185 per sq ft, i.e. consistent with site P7, representing a greenfield site

in a location equivalent to Warehouse Lane. The second used lower prices at £150 per sq ft, in line

with the urban sites with base market levels in Burnley and in Pendle. These two therefore provided

guidance on small sites respectively on rural and urban sites.

4.11 The results for the rural threshold model sites are set out below. They cover the full range of sites from

15 down to three dwellings.

4. Threshold model l ing: resu l ts

Page 19

Table 4.2 Appraisal outcomes: rural threshold sites

Value £k per acre Site Alt use

value No

affordable 10% 20% 30% 40%

model site 15 dwgs 10-100 382 303 228 146 64

VIABLE VIABLE VIABLE VIABLE MARGINAL

model site 14 dwgs 10-100 366 287 212 131 49

VIABLE VIABLE VIABLE VIABLE MARGINAL

model site 13 dwgs 10-100 351 275 198 117 36

VIABLE VIABLE VIABLE VIABLE MARGINAL

model site 12 dwgs 10-100 345 271 189 107 25

VIABLE VIABLE VIABLE VIABLE MARGINAL

model site 11 dwgs 10-100 329 255 174 92 10

VIABLE VIABLE VIABLE MARGINAL NOT VIAB

model site 10 dwgs 10-100 320 240 160 79 -4

VIABLE VIABLE VIABLE MARGINAL NOT VIAB

model site 9 dwgs 10-100 314 233 152 71 -13

VIABLE VIABLE VIABLE MARGINAL NOT VIAB

model site 8 dwgs 10-100 293 213 133 52 -31

VIABLE VIABLE VIABLE MARGINAL NOT VIAB

model site 7 dwgs 10-100 275 195 117 35 -47

VIABLE VIABLE VIABLE MARGINAL NOT VIAB

model site 6 dwgs 10-100 257 177 98 16 -67

VIABLE VIABLE MARGINAL MARGINAL NOT VIAB

model site 5 dwgs 10-100 231 153 72 -10 -92

VIABLE VIABLE MARGINAL NOT VIAB NOT VIAB

model site 4 dwgs 10-100 208 127 46 -37 -119

VIABLE VIABLE MARGINAL NOT VIAB NOT VIAB

model site 3 dwgs 10-100 178 99 19 -62 -144

VIABLE MARGINAL MARGINAL NOT VIAB NOT VIAB

Source: Burnley & Pendle Affordable Housing Site Viability Study, Fordham Research 2010

4.12 The table shows quite clearly how viability declines as the site size reduces. At 30% the site is viable

down to 12 dwellings, the actual size of Site P7. From 11 dwellings downwards the scheme is only

marginally viable, and it is unviable from five dwellings.

4.13 At 20% the scheme is viable down to seven dwellings. It is marginal from six dwellings down. A 10%

affordable requirement is viable all the way down to four dwellings, and only becomes marginal, just,

at three dwellings.

4.14 Comparable results for the urban threshold model are shown in the table below.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 20

Table 4.3 Appraisal outcomes: urban threshold sites

Value £k per acre Site Alt use

value No

affordable 10% 20% 30% 40%

model site 15 dwgs 10-100 65 16 -34 -84 -135

MARGINAL MARGINAL NOT VIAB NOT VIAB NOT VIAB

model site 14 dwgs 10-100 51 2 -48 -98 -149

MARGINAL NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 13 dwgs 10-100 38 -12 -61 -101 -162

MARGINAL NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 12 dwgs 10-100 26 -24 -74 -125 -176

MARGINAL NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 11 dwgs 10-100 11 -38 -89 -139 -190

MARGINAL NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 10 dwgs 10-100 -2 -52 -101 -151 -202

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 9 dwgs 10-100 -11 -61 -111 -162 -213

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 8 dwgs 10-100 -29 -78 -128 -178 -229

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 7 dwgs 10-100 -45 -93 -144 -193 -243

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 6 dwgs 10-100 -66 -115 -165 -215 -265

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 5 dwgs 10-100 -91 -141 -190 -240 -290

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 4 dwgs 10-100 -118 -168 -217 -267 -318

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

model site 3 dwgs 10-100 -143 -191 -240 -289 -339

NOT VIAB NOT VIAB NOT VIAB NOT VIAB NOT VIAB

Source: Burnley & Pendle Affordable Housing Site Viability Study, Fordham Research 2010

4.15 As could be anticipated, the viability results for urban threshold sites are not very good. As the site is

consistent with Site P7, it is a clean greenfield site, with wholly two storey dwellings – no flats or three

storey town houses. However values are at the levels prevailing over most of the two Boroughs’ urban

areas. Consequently, only the largest site, 15 dwellings, exceeds the threshold use value of £10k per

acre with 10% affordable housing, though only narrowly – it is not viable. With no affordable housing

at all, sites down to 11 dwellings are similarly marginal.

4. Threshold model l ing: resu l ts

Page 21

4.16 These results help to understand how viability might decline as the size threshold was reduced. The

‘tipping point’ will depend in each case on the target proportion of affordable housing in the policy.

However it is clear that on rural sites at least, there is some scope for reducing the threshold from the

national guidance level of 15 dwellings.

4.17 This issue is considered further along with the general target, in the next chapter.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 22

5. Study f ind ings

Page 23

5. Study findings

Introduction

5.1 The AHSVS study carried out in 2008 considered a range of sites across the two Boroughs

comprising the Burnley and Pendle Housing Market Area. Only one of the 16 sites, in Pendle,

was below the national guidance threshold of 15 dwellings.

5.2 The 2008 study was carried out during a prolonged downturn in both housing market and

general economic conditions, when house prices had fallen quite significantly. Its findings

reflected market conditions as at November 2008.

5.3 The two Councils commissioned additional work to provide an updated assessment of current

residential development viability, with additional analysis of viability on sites below the national

guidance threshold. It would also incorporate arrangements (‘Dynamic Viability’),

subsequently developed by Fordham Research, which would enable the affordable target to

be updated automatically from time to time, as viability changed/improved.

5.4 The findings and conclusions from the work are outlined below.

Results from update

5.5 The information from our market survey suggested that, though they might well have moved in

the intervening period, at June 2010 prices of market dwellings were very similar to the values

they had in November 2008. There had been a small improvement in the base prices for two

storey houses, whilst prices for town houses and flats were just about the same. There was

no reason to think that the threshold alternative use values had changed to any measurable

extent. Build costs had risen slightly, and we assumed that affordable prices had risen in line

with the Retail Price Index (RPI).

5.6 The overall impact was that the viability results reported in the 2008 AHSVS report had not

changed very significantly; residual values had improved just a little on some sites, and

dropped back slightly on others. Overall it remained the case that a large majority of the sites

would be unviable even with zero affordable housing; they would not proceed in current

market circumstances, with the sustainability requirements and developer contributions we

assumed.

5.7 This indicates that it would not be possible to set an affordable housing target, however low,

even 0%, to apply generally across the two Borough areas.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 24

5.8 On the other hand, in the rural parts of Pendle prices are significantly higher than in the main

towns and, as in 2008, it appears that an affordable target could reasonably be set for those

areas.

General target

5.9 This study has drawn upon the work of the 2008 AHSVS study to provide an updated

assessment of viability for residential development in Burnley and Pendle, and also to look at

the scope for reducing the affordable housing threshold from the national guidance figure of

15 dwellings. To do this the 2008 appraisals were updated, and appraisals have also been

prepared for two sets of model sites of fewer than 15 dwellings.

5.10 The results suggest that in current market conditions, no affordable target could be set to

apply generally across either Burnley or Pendle. Market conditions would need to improve

somewhat in order that a positive target could be set.

5.11 However an affordable target could be applied in the rural parts of Pendle where prices are

higher. We suggest a figure of 20% in current market conditions. The rural area in Burnley is

much smaller, with only one substantial settlement, and with the postcode level data available

from the AHSVS (Table A2.1) the evidence of a significant rural price premium for that

settlement is more limited. However if that could be established, then we feel a corresponding

policy initiative could be supported if the Council wished to consider it.

Thresholds

5.12 We have analysed viability on sites below the national guidance threshold. Viability has been

considered for both rural sites, and for urban sites. Both were assumed to be greenfield.

5.13 For rural sites in Pendle below 15 dwellings it appears that, as with larger sites, viability would

permit their bearing an affordable target. On the model site used for our analysis a target

consistent with the suggested 20% target for larger sites, could be borne on sites down to

seven dwellings. A site of five dwellings – the smallest that at 20% would generate a complete

dwelling – could not bear the full requirement, though by interpolation we suggest it could

carry 15%.

5.14 There are several possible policy responses. A simple approach would be to operate a lower

target, of 15%, on sites from five to nine dwellings, and the full target of 20% from ten

dwellings upwards. A more sophisticated approach would involve a graduated scale, taking

one third of a dwelling as affordable on every additional dwelling after four dwellings. By ten

dwellings the full 20% target would be reached.

5. Study f ind ings

Page 25

5.15 Both these approaches would involve fractions of a dwelling, which we envisage would be

taken as commuted sums. If this arrangement is felt to be unacceptable, the graduated scale

could be rounded to whole numbers. The three approaches are shown together for

comparison in the table below. .

Table 5.1 Graduated scale for20% rural target

Option A 15% to 10 Option B graduated scale Option C rounded scale

Affordable requirement Affordable requirement Affordable requirement No of dwgs in scheme

Dwgs % Dwgs % Dwgs %

4 0 0% 0 0% 0 0%

5 0.75 15% 0.33 7% 0.0 0%

6 0.9 15% 0.67 11% 1 17%

7 1.05 15% 1.00 14% 1 14%

8 1.2 15% 1.33 17% 1 13%

9 1.35 15% 1.67 18% 2 22%

10 2 20% 2.00 20% 2 20%

11 2.2 20% 2.2 20% 2 18%

12 2.4 20% 2.4 20% 2 17%

13 2.6 20% 2.6 20% 3 23%

14 2.8 20% 2.8 20% 3 21% Source: Fordham Research Strategic Housing Viability Study

5.16 We consider that if a rural 20% target were to be developed for Burnley a parallel set of

proposals could be justified.

5.17 Model appraisals were also produced for urban threshold sites. These suggested that even

with zero affordable housing, development was only marginally viable down to 11 dwellings.

No affordable housing could be produced.

5.18 This situation is to be expected since it is reflected in the larger (15 dwellings plus) urban

sites, which also could not provide any level of affordable housing and remain viable. Were

market conditions to improve to the point where a target of say 20% could be applied

generally in Burnley or Pendle, then it is possible that a reduction in the urban threshold might

be considered. However that situation is some way off, and the relevant analysis only applies

to clean greenfield sites of comparable density to Warehouse Lane. We would suggest that

any such initiative is not pursued at this time.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 26

Changes in market conditions

5.19 The recommendations on targets and thresholds set out above reflect current (June 2010)

market conditions. They also reflect other assumptions such as those on tenure split; grant

support (zero); developer contributions; and the Code for Sustainable Homes specification,

which in general have been carried over from the 2008 study.

5.20 These assumptions may change, and in doing so impact upon the appraisal results. The level

of general target that could be achieved viably could then increase, or conceivably decrease.

5.21 More generally, in the report’s final two chapters (one for Burnley, one for Pendle) we develop

an approach to target setting which allows for the impact of changes in market conditions

upon the deliverable target. The approach involves constructing a matrix which shows all the

possible percentage targets that result from different combinations of movements in prices,

costs, and alternative use values. The matrix is calculated using a single ‘benchmark site’

which is felt to be reasonably representative of development generally in each Council’s area.

Sufficiently favourable movements in prices relative to costs and alternative use values would

then enable a general affordable target greater than zero to be set in each Council area. The

target of 20% proposed for rural parts of Pendle would then increase in line with the general

target.

5.22 Generally speaking, most changes (in either market conditions or other key assumptions) that

can be envisaged, will be neutral as between sites above and below 15 dwellings; if so the

results will move up or down in step. Consequently our conclusion that a lower (rural)

threshold can be introduced would remain valid, though the level of target should then vary in

step with the 15 dwellings plus target.

6. Dynamic V iab i l i ty : Burn ley

Page 27

6. Dynamic Viability: Burnley

6.1 These final two chapters for Burnley and for Pendle take the results of the viability analysis, and

provide a basis for setting policy targets. This is achieved by allowing the affordable housing target to

vary through the plan period according to what is deliverable. Hence although a general Borough-wide

target cannot be set in either area under market conditions as they stood at June 2010, a favourable

change in those conditions would allow a target to be set subsequently.

What Dynamic Viability does

6.2 The Dynamic Viability model is designed to provide robust targets at all phases of the housing market

during the plan period. This is taken to mean that the full range of possibilities must be set out for the

Core Strategy Examination, so that its Inspector can consider and decide on the level of target setting

for the whole plan period.

6.3 The model begins with the viability assessment, based on the residual valuations carried out as part of

the main Viability Study (covering a total of eight sites characteristic of the Burnley area). Whilst

normally the initial target figure provides the starting point for the model, in this case there can be no

initial target figure. The target would in fact be less than zero in Burnley, since at zero affordable

housing a majority of sites are still unviable.

Benchmark Site

6.4 The Dynamic Viability approach requires that a single benchmark site is identified that reasonably

reflects the affordable target level that is deliverable in that area. This site should be representative of

future development in the council area concerned.

6.5 After careful consideration Site B5, Former Coal Yard Burnley, was selected. The site has the base

level of floorspace density, and with market peak prices (Table 3.4) it has a middling land value

performance.

6.6 Its alternative use value is given as industrial/warehouse (net of some necessary abnormals) valued at

£160k per acre/£395k per hectare. This value is then keyed to the national published index.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 28

The indices

6.7 Future change in target levels is purely dependent on published indexes. This means that the process

of target setting through the plan period is entirely transparent. The model is set up prior to the Core

Strategy Examination, is assessed and approved in whatever form during that Examination, and

afterwards is entirely dependent on three published indexes:

• Price change: We use the Halifax Price Index (HPI) but others are available

• Building costs change: The RICS building cost index based on tenders (BCIS) provides a

general index of building costs

• Alternative use value: The appropriate measure would depend on the specific alternative

use applying to the benchmark site but usually it is the Valuation Office Agency’s (VOA)

Industrial Land index

6.8 The set of indices is based on the assessment that, of all the many financial assumptions in the

appraisal that could change over time, there are three key variables which in practice dominate the

outcome. Price and build cost are the key figures which determine the residual value result, but

significant movements in alternative use value will also move the site into or out of viability.

6.9 The following table shows the figures and sources of indices for each of these three ‘dimensions’:

6. Dynamic V iab i l i ty : Burn ley

Page 29

Table 6.1 Indices for automatic updating of Dynamic Viability

Variable Proposed index Starting value

House Price Halifax House Price Index Quarterly North West Seasonally Adjusted Q1 2010 = 493.8

Halifax House Price Index (free, monthly)

http://www.lloydsbankinggroup.com/media1/research/halifax_hpi.asp

Build cost BCIS General Building Cost Index Q2 2009 = 295.9

BCIS Review Online (subscription only, monthly) Produced by the Royal Institute of Chartered Surveyors http://www.bcis.co.uk/online

Alternative use value

Value of industrial land for Manchester

Both the coverage and frequency of VOA’s Property Market Report have recently (July 2010) been reduced. They are now annual rather than six monthly, and as discussed at para 2.19, only cover the very largest regional centres – the nearest being Manchester Liverpool & Leeds. The Manchester figure is proposed for use as an index in updating the alternative use value; it is movements in the Manchester figure rather than its absolute value, which are important.

January 2010: Value of £650,000 -per ha

Valuation Office Agency: Property Market Reports (free, annual) http://www.voa.gov.uk/publications/property_market_report/pmr-jan-

2010/index.htm

Sources: As shown in the boxes of the table

Details of the outputs

6.10 A simplified appraisal is used to assess what affordable target is achievable for any given combination

of new values for price, cost and alternative use value that may emerge from future movements in the

indices. Clearly in theory there are an infinite number of combinations of these three. To make the

task manageable, we have to work in ranges, i.e. with rounded percentage increases, and also to

consider only the plausible range of future variations.

6.11 Even then, the required three-dimensional table has to be reduced to a series of two dimensional

tables in order to set it down on paper. The following illustrated table shows the achievable affordable

target varies with future changes in price and cost for one particular alternative use value, the starting

(‘base’) value. It is one of a set of eight such tables. The complete set is presented in Appendix 3.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 30

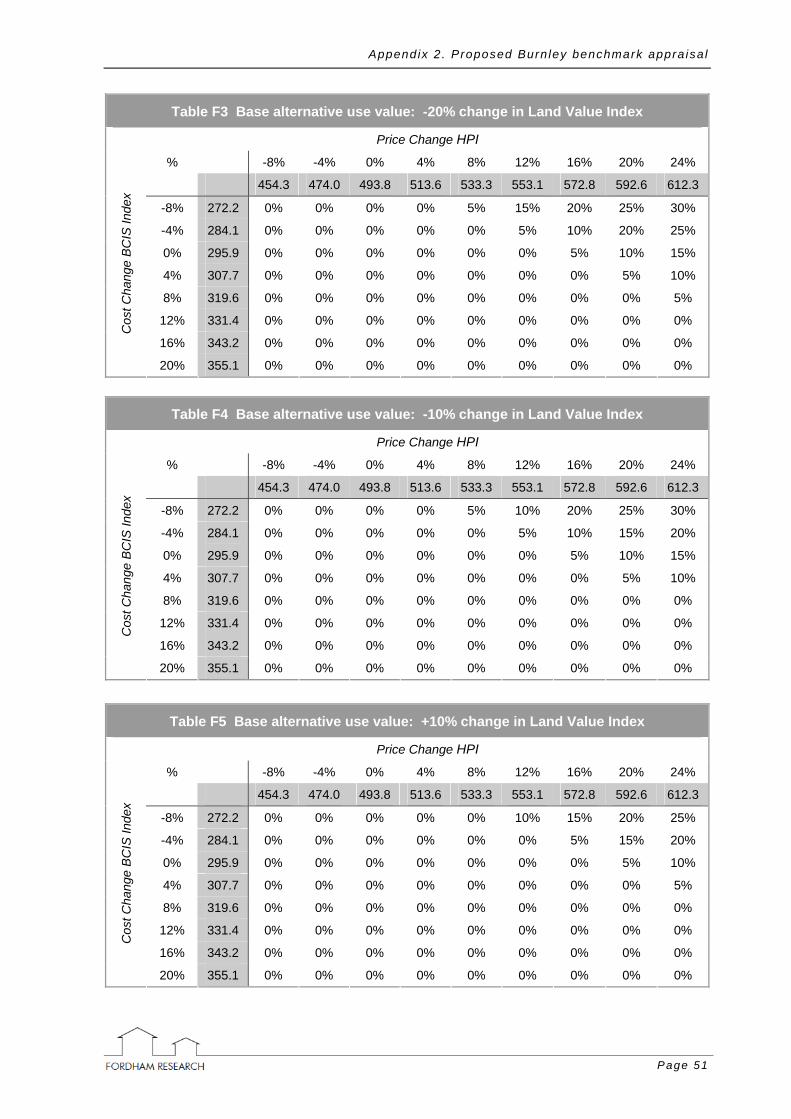

Table 6.2 Coarse Matrix for Burnley: base alternative use value

Price Change HPI

% -20% -10% 0% 10% 20% 30% 40% 50% 60%

395.0 444.4 493.8 543.2 592.6 641.9 691.3 740.7 790.1

-20% 236.7 0% 0% 15% 30% 40% 50% 55% 55% 55%

-10% 266.3 0% 0% 0% 10% 25% 35% 45% 50% 55%

0% 295.9 0% 0% 0% 0% 10% 20% 30% 40% 45%

10% 325.5 0% 0% 0% 0% 0% 5% 20% 25% 35%

20% 355.1 0% 0% 0% 0% 0% 0% 5% 15% 25%

30% 384.7 0% 0% 0% 0% 0% 0% 0% 5% 15%

40% 414.3 0% 0% 0% 0% 0% 0% 0% 0% 5%

Cos

t Cha

nge

BC

IS In

dex

50% 443.9 0% 0% 0% 0% 0% 0% 0% 0% 0% Note that the figure shows proposed % target for each cost/price combination, with 0% change in alternative use value. The

table also provides, inside the percentages, the actual values of the indexes, so that they can be read off in future Source: Table C1 of Appendix 2 below

6.12 The base value is the 0% price and 0% cost point: as can be seen this cell contains 0%, in line with

the maximum Borough-wide affordable housing target. (This cell shows the initial value for the two

indexes: 493.8 for price and 295.9 for build cost). For each combination of price and cost change, the

table shows what affordable target is achievable. If price moves sufficiently ahead of cost, so long as

alternative use value remains broadly at its present level, it will become possible to apply a general

affordable target across Pendle. For instance, with a 40% increase in price and only 10% cost

increase, a 20% affordable target will be achievable.

6.13 The set of eight tables, of which Table 7.2 is the first, together make up a Coarse Matrix. Appendix 3

also contains eight tables comprising a parallel Fine Matrix. The reason for there being two Matrices is

as follows:

• Coarse Matrix: This is calculated in 10% intervals of the indexes (all three). The result

provides broad coverage, but the change from one cell to another can produce large changes

in targets: e.g. from 20% to 35%. But this stage provides wide coverage.

• Fine Matrix: This takes the area around the chosen target and uses 4% intervals in the

indexes (the intervals can be varied). This produces results for the area around the chosen

target that yield much smaller target changes: mostly 5% intervals and sometimes 10%.

6. Dynamic V iab i l i ty : Burn ley

Page 31

Table 6.3 Fine Matrix for Burnley: base alternative use value

Price Change HPI

% -8% -4% 0% 4% 8% 12% 16% 20% 24%

454.3 474.0 493.8 513.6 533.3 553.1 572.8 592.6 612.3

-8% 272.2 0% 0% 0% 0% 0% 10% 15% 20% 25%

-4% 284.1 0% 0% 0% 0% 0% 0% 10% 15% 20%

0% 295.9 0% 0% 0% 0% 0% 0% 0% 10% 15%

4% 307.7 0% 0% 0% 0% 0% 0% 0% 0% 5%

8% 319.6 0% 0% 0% 0% 0% 0% 0% 0% 0%

12% 331.4 0% 0% 0% 0% 0% 0% 0% 0% 0%

16% 343.2 0% 0% 0% 0% 0% 0% 0% 0% 0%

Cos

t Cha

nge

BC

IS In

dex

20% 355.1 0% 0% 0% 0% 0% 0% 0% 0% 0% Source: Fordham Research: Source Table F1 of Appendix 3 below

6.14 The Fine Matrix is the operational level. It produces target changes of the order of 5%, which seems a

manageable level of change for a potentially annual shift. The Coarse Matrix in some cases shows

changes of 10% or more, which seems too large for an annual shift.

6.15 After a period of years it may well be that the indexes move beyond the range of the initial Fine Matrix.

This is not a problem, as the Fine Matrix can move within the Coarse Matrix. It is simply a ‘close up’ of

part of the Coarse Matrix. The following diagram shows the process as it may unfold.

Figure 6.1 Coarse and Fine Matrices related

Source: Fordham Research 2009: Affordable Housing Viability Study 2009

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 32

6.16 To provide further assistance in visualising how this system works, Figure 6.2 provides an operational

guide as to how the updating process goes.

Implementing Dynamic Viability

6.17 The Viability study which is the input into Dynamic Viability is likely to be done as part of the

preparation of the Core Strategy Affordable Housing Policy. There will then be a delay of months or

years until the actual Examination. During that period there may well be changes in the market. Thus it

is likely to be necessary to redo the base viability analysis at the time of the Core Strategy

Examination to ensure that the Dynamic Viability process starts from the period of the Examination.

6.18 Since the automatic target varying procedure cannot begin until approved by the Inspector’s Report, it

is desirable to have it as up to date as possible. Figure 6.2 indicates this process schematically.

Updating Dynamic Viability targets

6.19 The figure below sets out the updating sequence. It requires input from the report which we will have

provided. This includes, as an appendix, the following sets of tables containing indexes. In the same

appendix is a table listing the sources of the three indexes. The current values of the indexes, and the

sets of tables listed below, are all that is required for the updating process.

i) Coarse matrix of targets. This shows Halifax Price Index x BCIS (the RICS building cost

index). The indexes are shown by 10% gaps to provide affordable target numbers across a

very wide price/cost range. There are eight tables because the ‘third dimension’ of the

price/cost calculation is alternative use value. This is the value of the Benchmark Site in the

best alternative land uses to housing. The alternative use value may sometimes be higher

than housing for the Benchmark site (and so remove the affordable target, and sometimes it

may reduce the feasible target). This has to be checked as part of the procedure of updating.

ii) Fine matrix of targets. This parallels the Coarse Matrix (with eight tables) with narrower gap in

the indexes of 4%. It covers only part of the Coarse Matrix range, but as demonstrated in

Figure 7.1, can move around within that range. The affordable targets in adjoining cells of the

Fine Matrix are roughly at 5% intervals. This is about as big a target change as seems

feasible at the annual review point. The Coarse Matrix provides the background, and the Fine

matrix provides the operational targets. These alter as the prices and costs in the housing

market alter.

6. Dynamic V iab i l i ty : Burn ley

Page 33

Figure 6.2: Sequence of steps in updating the target

Step 1

The starting point is the Alternative Use Value Fine Matrix Table F1. Does the current value of the

Alternative use index mean that another page rather than the base page should be used? If so this is the

reference for the further steps.

Step 2

Using the appropriate Fine matrix table, decided by Step 1, check the changes in the HPI and the BCIS.

If either or both of these has changed by more than half the interval to the next step, then the target cell

will change. This may or may not involve a target change, since some of the targets will the same in

several cells.

Step 3

Publish the change in some suitable format such as the Annual Monitoring report.

Source: Fordham Research 2009: Affordable Housing Viability Study 2009

Figure 6.3 Implementing Dynamic Viability

Source: Fordham Research 2009: Affordable Housing Viability Study 2009

6.20 The diagram illustrates the possible change in viability between study and Core Strategy Examination,

after that, of course, the Dynamic Viability matrix will take account of future variations in viability. As

the diagram suggests, these could be downward as well as upward. The future course of the market is

uncertain.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 34

Conclusion: proposed target

6.21 The update study has confirmed that a general target, one covering the urban area of Burnley, could

not be set at the present time. However at some future point within the LDF plan period, if and when

prices move sufficiently ahead of costs, it will become possible to seek a target generally across

Burnley, as determined, from the Matrix tables, by movements of the published indices.

6.22 The analysis of viability, drawn from the AHSVS, does not provide sufficiently fine detail to confirm that

in current market conditions a target could be applied to the, more fragmentary, rural parts of the

Borough. Should such a target be established for some or all of the rural area, then when market

conditions improve to the point that a general target can be set through Dynamic Viability, viability will

also have improved in the rural areas sufficiently for a higher target to be deliverable. We therefore

recommend that any rural target moves up in step with the general target.

6.23 The analysis has suggested that in the rural areas, a reduced site threshold is justified. Clearly the

proposed target scale for small sites (set out at paragraph 5.16) ought also to move in step with any

rural target.

7. Dynamic V iab i l i ty : Pendle

Page 35

7. Dynamic Viability: Pendle

7.1 These final two chapters for Burnley and for Pendle take the results of the viability analysis, and

provide a basis for setting policy targets. This is achieved by allowing the affordable housing target to

vary through the plan period according to what is deliverable. Hence although a general Borough-wide

target cannot be set in either area under market conditions as they stood at June 2010, a favourable

change in those conditions would allow a target to be set subsequently.

What Dynamic Viability does

7.2 The Dynamic Viability model is designed to provide robust targets at all phases of the housing market

during the plan period. This is taken to mean that the full range of possibilities must be set out for the

Core Strategy Examination, so that its Inspector can consider and decide on the level of target setting

for the whole plan period.

7.3 The model begins with the viability assessment, based on the residual valuations carried out as part of

the main Viability Study (covering a total of eight sites characteristic of the Pendle area). Whilst

normally the initial target figure provides the starting point for the model, in this case there can be no

initial target figure. The target would in fact be less than zero in Pendle, since at zero affordable

housing a majority of sites are still unviable.

Benchmark Site

7.4 The Dynamic Viability approach requires that a single benchmark site is identified that reasonably

reflects the affordable target level that is deliverable in that area. This site should be representative of

future development in the council area concerned.

7.5 After careful consideration Site P6, Glen Mill Colne, was selected. The site has the base level of

floorspace density, and with market peak prices (Table 3.4) it has a middling land value performance.

7.6 Its alternative use value is given as industrial/warehouse (net of some necessary abnormals) valued at

£135k per acre/£335k per hectare. This value is then keyed to the national published index.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 36

The indices

7.7 Future change in target levels is purely dependent on published indexes. This means that the process

of target setting through the plan period is entirely transparent. The model is set up prior to the Core

Strategy Examination, is assessed and approved in whatever form during that Examination, and

afterwards is entirely dependent on three published indexes:

• Price change: We use the Halifax Price Index (HPI)

• Building costs change: The RICS building cost index (BCIS) provides a general index of

building costs

• Alternative use value: The appropriate measure would depend on the specific alternative

use applying to the benchmark site but usually it is the Valuation Office Agency’s (VOA)

Industrial Land index

7.8 The set of indices is based on the assessment that, of all the many financial assumptions in the

appraisal that could change over time, there are three key variables which in practice dominate the

outcome. Price and build cost are the key figures which determine the residual value result, but

significant movements in alternative use value will also move the site into or out of viability.

7.9 The following table shows the figures and sources of indices for each of these three ‘dimensions’:

7. Dynamic V iab i l i ty : Pendle

Page 37

Table 7.1 Indices for automatic updating of Dynamic Viability

Variable Proposed index Starting value

House Price Halifax House Price Index Quarterly North West Seasonally Adjusted Q1 2010 = 493.8

Halifax House Price Index (free, monthly)

http://www.lloydsbankinggroup.com/media1/research/halifax_hpi.asp

Build cost BCIS General Building Cost Index Q2 2009 = 295.9

BCIS Review Online (subscription only, monthly) Produced by the Royal Institute of Chartered Surveyors http://www.bcis.co.uk/online

Alternative use value

Value of industrial land for Manchester

Both the coverage and frequency of VOA’s Property Market Report have recently (July 2010) been reduced. They are now annual rather than six monthly, and as discussed at para 2.19, only cover the very largest regional centres – the nearest being Manchester Liverpool & Leeds. The Manchester figure is proposed for use as an index in updating the alternative use value; it is movements in the Manchester figure rather than its absolute value, which are important.

January 2010: Value of £650,000 -per ha

Valuation Office Agency: Property Market Reports (free, annual) http://www.voa.gov.uk/publications/property_market_report/pmr-jan-

2010/index.htm

Sources: As shown in the boxes of the table

Details of the outputs

7.10 A simplified appraisal is used to assess what affordable target is achievable for any given combination

of new values for price, cost and alternative use value that may emerge from future movements in the

indices. Clearly in theory there are an infinite number of combinations of these three. To make the

task manageable, we have to work in ranges, i.e. with rounded percentage increases, and also to

consider only the plausible range of future variations.

7.11 Even then, the required three-dimensional table has to be reduced to a series of two dimensional

tables in order to set it down on paper. The following illustrated table shows the achievable affordable

target varies with future changes in price and cost for one particular alternative use value, the starting

(‘base’) value. It is one of a set of eight such tables. The complete set is presented in Appendix 3.

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 38

Table 7.2 Coarse Matrix for Pendle: base alternative use value

Price Change HPI

% -20% -10% 0% 10% 20% 30% 40% 50% 60%

395.0 444.4 493.8 543.2 592.6 641.9 691.3 740.7 790.1

-20% 236.7 0% 0% 15% 30% 45% 50% 55% 55% 55%

-10% 266.3 0% 0% 0% 10% 25% 35% 45% 50% 55%

0% 295.9 0% 0% 0% 0% 10% 20% 30% 40% 45%

10% 325.5 0% 0% 0% 0% 0% 5% 20% 25% 35%

20% 355.1 0% 0% 0% 0% 0% 0% 5% 15% 25%

30% 384.7 0% 0% 0% 0% 0% 0% 0% 5% 15%

40% 414.3 0% 0% 0% 0% 0% 0% 0% 0% 5%

Cos

t Cha

nge

BC

IS In

dex

50% 443.9 0% 0% 0% 0% 0% 0% 0% 0% 0% Note that the figure shows proposed % target for each cost/price combination, with 0% change in alternative use value. The

table also provides, inside the percentages, the actual values of the indexes, so that they can be read off in future Source: Table C1 of Appendix 3 below

7.12 The base value is the 0% price and 0% cost point: as can be seen this cell contains 0%, in line with

the maximum Borough-wide affordable housing target. (This cell shows the initial value for the two

indexes: 493.8 for price and 295.9 for build cost). For each combination of price and cost change, the

table shows what affordable target is achievable. If price moves sufficiently ahead of cost, so long as

alternative use value remains broadly at its present level, it will become possible to apply a general

affordable target across Pendle. For instance, with a 40% increase in price and only 10% cost

increase, a 20% affordable target will be achievable.

7.13 The set of eight tables, of which Table 7.2 is the first, together make up a Coarse Matrix. Appendix 3

also contains eight tables comprising a parallel Fine Matrix. The reason for there being two Matrices is

as follows:

• Coarse Matrix: This is calculated in 10% intervals of the indexes (all three). The result

provides broad coverage, but the change from one cell to another can produce large changes

in targets: e.g. from 20% to 35%. But this stage provides wide coverage.

• Fine Matrix: This takes the area around the chosen target and uses 4% intervals in the

indexes (the intervals can be varied). This produces results for the area around the chosen

target that yield much smaller target changes: mostly 5% intervals and sometimes 10%.

7. Dynamic V iab i l i ty : Pendle

Page 39

Table 7.3 Fine Matrix for Pendle: base alternative use value

Price Change HPI

% -8% -4% 0% 4% 8% 12% 16% 20% 24%

454.3 474.0 493.8 513.6 533.3 553.1 572.8 592.6 612.3

-8% 272.2 0% 0% 0% 0% 5% 10% 15% 20% 25%

-4% 284.1 0% 0% 0% 0% 0% 0% 10% 15% 20%

0% 295.9 0% 0% 0% 0% 0% 0% 0% 10% 15%

4% 307.7 0% 0% 0% 0% 0% 0% 0% 0% 10%

8% 319.6 0% 0% 0% 0% 0% 0% 0% 0% 0%

12% 331.4 0% 0% 0% 0% 0% 0% 0% 0% 0%

16% 343.2 0% 0% 0% 0% 0% 0% 0% 0% 0%

Cos

t Cha

nge

BC

IS In

dex

20% 355.1 0% 0% 0% 0% 0% 0% 0% 0% 0% Source: Fordham Research: Source Table F1 of Appendix 3 below

7.14 The Fine Matrix is the operational level. It produces target changes of the order of 5%, which seems a

manageable level of change for a potentially annual shift. The Coarse Matrix in some cases shows

changes of 10% or more, which seems too large for an annual shift.

7.15 After a period of years it may well be that the indexes move beyond the range of the initial Fine Matrix.

This is not a problem, as the Fine Matrix can move within the Coarse Matrix. It is simply a ‘close up’ of

part of the Coarse Matrix. The following diagram shows the process as it may unfold.

Figure 7.1 Coarse and Fine Matrices related

Source: Fordham Research 2009: Affordable Housing Viability Study 2009

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 40

7.16 To provide further assistance in visualising how this system works, Figure 7.2 provides an operational

guide as to how the updating process goes.

Implementing Dynamic Viability

7.17 The Viability study which is the input into Dynamic Viability is likely to be done as part of the

preparation of the Core Strategy Affordable Housing Policy. There will then be a delay until the actual

Examination. During that period there may well be changes in the market. Thus it is likely to be

necessary to redo the base viability analysis at the time of the Core Strategy Examination to ensure

that the Dynamic Viability process starts from the period of the Examination. Only when the relevant

Development Plan Document has been approved will the automatic target varying procedure begin to

operate. However, it is desirable to have it as up to date as possible; Figure 7.3 indicates this process

schematically.

Updating Dynamic Viability targets

7.18 The figure below sets out the updating sequence. It requires input from the report which we will have

provided. This includes, as an appendix, the following sets of tables containing indexes. In the same

appendix is a table listing the sources of the three indexes. The current values of the indexes, and the

sets of tables listed below, are all that is required for the updating process.

i) Coarse matrix of targets. This shows Halifax Price Index x BCIS (the RICS building cost

index). The indexes are shown by 10% gaps to provide affordable target numbers across a

very wide price/cost range. There are eight tables because the ‘third dimension’ of the

price/cost calculation is alternative use value. This is the value of the Benchmark Site (Glen

Mill, Colne).in the best alternative land uses to housing. The alternative use value may

sometimes be higher than housing for the Benchmark site (and so remove the affordable

target, and sometimes it may reduce the feasible target). This has to be checked as part of the

procedure of updating.

ii) Fine matrix of targets. This parallels the Coarse Matrix (with eight tables) with a narrower gap

in the indexes of 4%. It covers only part of the Coarse Matrix range, but as demonstrated in

Figure 7.1, can move around within that range. The affordable targets in adjoining cells of the

Fine Matrix are roughly at 5% intervals. This is about as big a target change as seems

feasible at the annual review point. The Coarse Matrix provides the background, and the Fine

matrix provides the operational targets. These alter as the prices and costs in the housing

market alter.

7. Dynamic V iab i l i ty : Pendle

Page 41

Figure 7.2: Sequence of steps in updating the target

Step 1

The starting point is the Alternative Use Value Fine Matrix Table F1. Does the current value of the

Alternative use index mean that another page rather than the base page should be used? If so this is the

reference for the further steps.

Step 2

Using the appropriate Fine matrix table, decided by Step 1, check the changes in the HPI and the BCIS.

If either or both of these has changed by more than half the interval to the next step, then the target cell

will change. This may or may not involve a target change, since some of the targets will remain the same

in several cells.

Step 3

Publish the change in some suitable format such as the Annual Monitoring Report (AMR).

Source: Fordham Research 2009: Affordable Housing Viability Study 2009

Figure 7.3 Implementing Dynamic Viability

Source: Fordham Research 2009: Affordable Housing Viability Study 2009

Burn ley & Pendle Af fordable Housing Si te V iab i l i ty Update

Page 42

7.19 The diagram illustrates the possible change in viability between study and Core Strategy Examination,

after that, of course, the Dynamic Viability matrix will take account of future variations in viability. As

the diagram suggests, these could be downward as well as upward. The future course of the market is

uncertain.

Conclusion: proposed targets

7.20 The update study has confirmed that a general target, i.e. covering the urban and rural areas of

Pendle, could not be set at the present time. However at some future point within the LDF plan period,

if and when prices move sufficiently ahead of costs, it will become possible to seek a target generally

across Pendle, as determined, from the Matrix tables, by movements of the published indices.

7.21 The viability analysis indicates that in current market conditions a 20% target could be applied across

the rural areas of the Borough. When market conditions improve to the point that a general target can

be set through Dynamic Viability, viability will also have improved in the rural areas sufficiently for a

higher target to be deliverable. We therefore recommend that the rural target moves in step with the

general target, but 20% higher.

7.22 The analysis has suggested that in the rural areas of Pendle, a reduced site threshold is justified.

Clearly the proposed target scale for small sites (set out at paragraph 5.16) ought also to move in step