business finance ba303 michael dimond. michael dimond school of business administration bonds are...

TRANSCRIPT

Business FinanceBA303

Michael Dimond

Michael DimondSchool of Business Administration

• Bonds are long-term debt contracts used to raise capital

• Bonds are denominated in a set amount (most U.S. corporate bonds are $1,000) and can be bought and sold in a secondary market

• The bond indenture specifies the terms of the bond, including the rights and duties, the amounts and dates involved, standard debt provisions and restrictive covenants.

Bonds

Michael DimondSchool of Business Administration

Bonds: Linking terminology to TVM functions• PV = Price• FV = Face Value (also called “Par Value.” Usually $1,000)• n = Periods (usually semiannual)• i = Yield• PMT = Coupon Payment

• The Coupon Rate is only used to determine the coupon payment. For example, a 10% coupon rate on a $1,000 bond would give a $100 annual payment, which would be $50 semiannually.

Michael DimondSchool of Business Administration

Bond pricing, yields, etc.

• Bond terminology is what gives most students problems. Sometimes you need to make assumptions based on how the question is worded.

• Here’s a typical sort of a bond question:• XYZ Company has a 10% bond with semiannual payments which

matures in 12 years. The market rate for bonds of this risk is currently 8%. What is the price of this bond?

• The key to solving a question like this is to identify the relevant information and organize it:• PV = Price = Unknown. This is what we are solving for.• FV = Face Value = Not stated, so we assume $1,000.• n = Periods = Semiannual for 12 years. 12 x 2 = 24, :. n = 24.• i = Yield = Return demanded ÷ Periods per year = 8% ÷ 2 = 4%

semiannual• PMT = Coupon Payment = FV x Coupon Rate ÷ Periods per year =

1,000 x 10% ÷ 2 = 50, :. PMT = 50. The expression “10% bond” means a bond with a 10% coupon annual rate.

Michael DimondSchool of Business Administration

Bond pricing, yields, etc.

• Entering this information in a financial calculator lets us find an answer.• PV = Price = Unknown. This is what we are solving for.• FV = $1,000.• n = 24 semiannual• i = 4% semiannual• PMT = 50 semiannual• Solve for PV = -1,152.4696

• Notice n, i and PMT are all semiannual values. These must all be in the same scale: Annual, semiannual, etc.

• The answer appears negative because it is a cash outflow. The price will be $1,152.47

• Here’s another bond question:• XYZ Company has a 10% semiannual bond which matures in 12

years and is selling for $1,050. What is the yield of this bond?

Michael DimondSchool of Business Administration

Bond pricing, yields, etc.

• Let’s try another. Entering this information in a financial calculator lets us find an answer, but it will be a semiannual answer.• PV = -1,050 (remember, the price is a cash outflow, so it has a minus

sign)• FV = 1,000 • n = 24 semiannual• i = Unknown. This is what we are solving for.• PMT = 50 semiannual• Solve for i = 4.6499%

• Remember, n, i and PMT are all semiannual values. The result the calculator gives is the semiannual interest rate. To annualize it, multiply it by 2:• Yield = 2 x semiannual i = 2 x 4.6499% = 9.2998%

Michael DimondSchool of Business Administration

Bond pricing, yields, etc.

• Here’s one more:• XYZ Company has a 10% bond with semiannual payments which

matures in 12 years and is selling for $1,000. What is the yield of this bond?

• In this case, the price and the face value are both 1,000. This means the bond is selling at par, which means the yield will equal the coupon rate (10%). To test this:• PV = -1,000• FV = 1,000 • n = 24 semiannual• PMT = 50 semiannual• Solve for i = 5.0000% semiannual• Yield = 2 x semiannual i = 2 x 5.0000% = 10%

Michael DimondSchool of Business Administration

More about bonds

• Provisions of bonds• Convertability: A conversion feature allows bondholders to exchange the bond

for a certain number of shares of stock.• Callability: A call feature allows the bond issuer to repurchase the bonds

before they mature (for a premium above the face value)• Warrants: A “sweetener” which allows the bondholders to purchase a certain

number of shares of stock at a specific price & time.

• Current Yield vs Yield to Maturity vs Yield to Call• Current Yield: Annual Payment ÷ Price• YTM: Solve for i using the number of periods until the bond matures

(remember to annualize if appropriate)• YTC: Solve for i using the number of periods until the bond can be called

(remember to annualize if appropriate)

• The “approximation formula” (PMT+((FV-PV)/n))/((FV+PV)/2)

works only when bonds are selling close to par

Michael DimondSchool of Business Administration

Interest rates

• The coupon rate and the yield of a bond both reflect interest rates.

• The coupon rate reflects the interest which the market was demanding at the time the bond was planned.• Risk determines the rate of return which investors will bear. What risks do

bondholders face?

• The yield reflects the interest which the market requires right now. Again, this is based on the risk faced by holders of this bond.• Can the riskiness of a company change between the time a bond is issued

and the time it matures?

• The yield of a bond is the interest demanded by the market and is the “Cost of Debt” (Kd).

Michael DimondSchool of Business Administration

Capital: How a firm finances its assets• All assets are backed by either equity or debt:

A = L + SE• Each type of capital has a different required rate of return

• Debt has a yield demanded by investors (e.g. Bondholders)• Common stock (equity) has a return demanded by investors• Preferred stock (equity) has a return demanded by investors

• Each type of capital bears a different amount of risk• Debt has the most structured arrangement• Common stock has the least structured arrangement• Because of risk, Kd < Kpfd < Ke

• Capital Structure is the mixture of capital used in a company

Michael DimondSchool of Business Administration

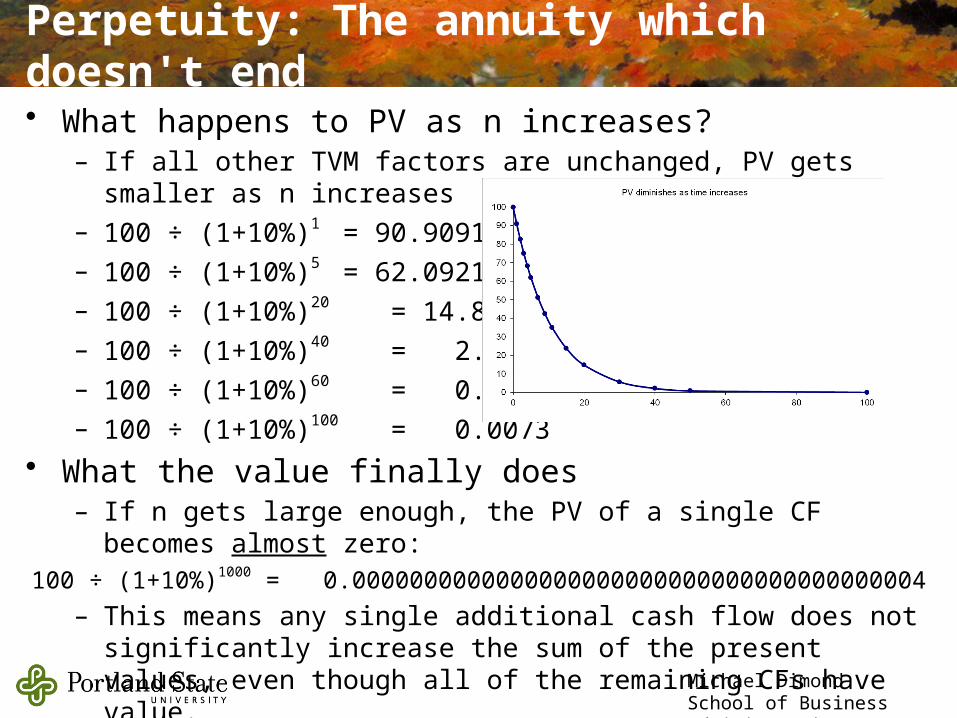

Perpetuity: The annuity which doesn't end• What happens to PV as n increases?

– If all other TVM factors are unchanged, PV gets smaller as n increases

– 100 ÷ (1+10%)1 = 90.9091– 100 ÷ (1+10%)5 = 62.0921– 100 ÷ (1+10%)20 = 14.8644– 100 ÷ (1+10%)40 = 2.2095– 100 ÷ (1+10%)60 = 0.3284– 100 ÷ (1+10%)100 = 0.0073

• What the value finally does– If n gets large enough, the PV of a single CF becomes almost zero:100 ÷ (1+10%)1000 = 0.0000000000000000000000000000000000000004

– This means any single additional cash flow does not significantly increase the sum of the present values, even though all of the remaining CFs have value.

• With a little math, the discounting of a perpetuity simplifies to:

PVperp = CF/r

Michael DimondSchool of Business Administration

• Consider a $100 annual perpetuity (“$100 per year forever”).– What if you require a 12% annual return?

Rather than trying to discount a infinite number of cash flows, we use the perpetuity formula.

• The value of a perpetuity: PVperp = CF/r– 100 ÷ 0.12 = 833.3333 :. You would be willing to pay $833.33 right

now to receive $100 per year “forever.”– What would happen if your required rate of return was higher (15%)?– What would happen if your required rate of return was higher (8%)?

Valuing a perpetuity

0 1 2 3 4

PV?

i = 12% APR

100100 100 100

The timeline for a perpetuity has an arrow at the right end to indicate there is no end

to the timeline

Michael DimondSchool of Business Administration

• Consider a $100 annual perpetuity which grows 10% each year.– What if you require a 12% annual return?

• As long as the percent growth rate is constant, this formula will give the present value: PVperp = CF/(r – g)– PVperp = 100 ÷ (0.12 – 0.10) = 100 ÷ 0.02 = 5,000– Expected growth has value– There is a rule: r > g– Notice this formula still works for a non-growing perpetuity. When

growth = 0%, PVperp = CF/(r – 0) = CF/r

Growing perpetuities

0 1 2 3 4

PV?

i = 12% APRg = 10%

110100 121 133.10

Michael DimondSchool of Business Administration

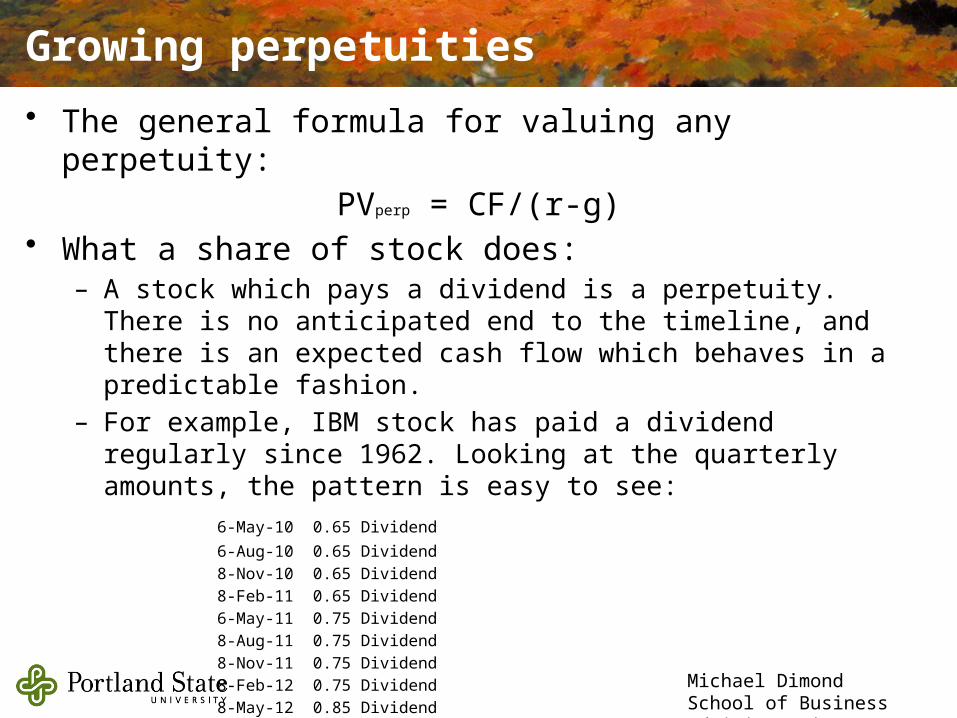

Growing perpetuities

• The general formula for valuing any perpetuity:

PVperp = CF/(r-g)• What a share of stock does:

– A stock which pays a dividend is a perpetuity. There is no anticipated end to the timeline, and there is an expected cash flow which behaves in a predictable fashion.

– For example, IBM stock has paid a dividend regularly since 1962. Looking at the quarterly amounts, the pattern is easy to see:

6-May-10 0.65 Dividend

6-Aug-10 0.65 Dividend

8-Nov-10 0.65 Dividend

8-Feb-11 0.65 Dividend

6-May-11 0.75 Dividend

8-Aug-11 0.75 Dividend

8-Nov-11 0.75 Dividend

8-Feb-12 0.75 Dividend

8-May-12 0.85 Dividend

8-Aug-12 0.85 Dividend

– You could probably predict the next several dividends without much doubt.

Michael DimondSchool of Business Administration

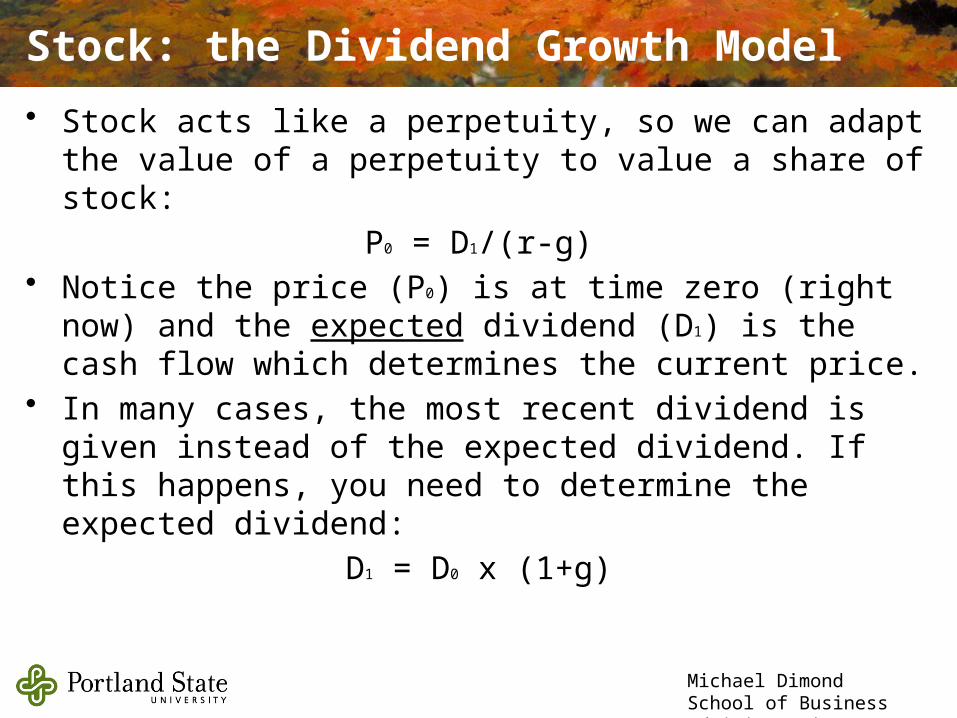

Stock: the Dividend Growth Model

• Stock acts like a perpetuity, so we can adapt the value of a perpetuity to value a share of stock:

P0 = D1/(r-g)• Notice the price (P0) is at time zero (right now) and the

expected dividend (D1) is the cash flow which determines the current price.

• In many cases, the most recent dividend is given instead of the expected dividend. If this happens, you need to determine the expected dividend:

D1 = D0 x (1+g)

Michael DimondSchool of Business Administration

Dividend Growth Model examples

• You require a 12% return on investment. If XYZ Company stock just paid a $1.00 dividend and dividends are expected to grow 4% per year forever, how much would you pay for a share of this stock?• D0 = 1.00 :. D1 = 1.00 x (1 + 4%) = 1.04• 1.04 ÷ (0.12 – 0.04) = 1.04 ÷ 0.08 = 13.00

:. You would be willing to pay $13.00 per share for XYZ Company

• If IBM stock has an expected annual dividend of $3.79 (four quarters of dividends), a growth rate of 14.9% and you require 16.8% return, what price would you pay for IBM stock?• 3.79 ÷ (0.168 – 0.149) = 3.79 ÷ 0.0190 = 199.4737

:. You would be willing to pay $199.47 per share for IBM

Michael DimondSchool of Business Administration

More about common stock

• Shares authorized vs issued vs outstanding• Classes of common stock (Class A vs Class B)• Voting rights & proxy ballots• Preemptive rights• Flotation• Foreign stock on the U.S. Market (ADRs)

Michael DimondSchool of Business Administration

About Preferred Stock

• Preferred stock is an ownership stake (equity) which comes with a contracted payout.

• The dividend is frequently a percentage of the par value of the stock.• For example, 5% preferred stock with a $10.00 par value would have an

annual dividend of $0.50.• Because it is a percent of the par value, the dividend does not grow.• The dividend is a perpetuity, so we use the perpetuity formula to value

preferred stock.

• XYZ Company has preferred stock with a $3.00 dividend and investors require a 9% return for this preferred equity. What is the market price?• D0 = 3.00 :. D1 = 3.00• 3.00 ÷ 0.09 = 33.3333

:. The market price is $33.33 per share for XYZ Company Preferred Stock.

Michael DimondSchool of Business Administration

More about preferred stock

• Dividend does not grow• Par value• Flotation & uses

Michael DimondSchool of Business Administration

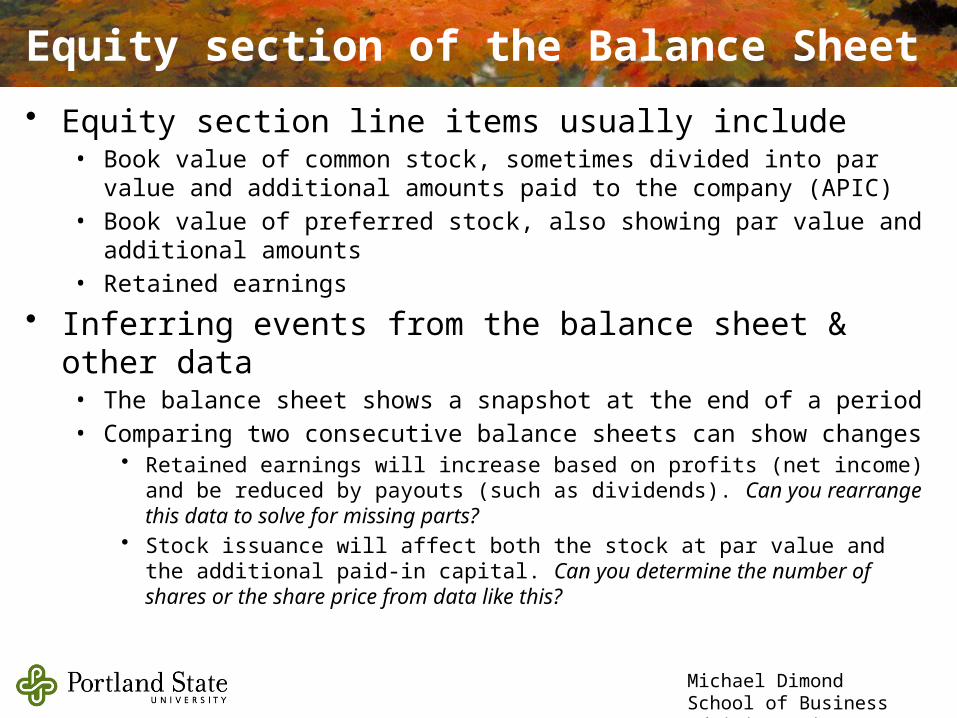

Equity section of the Balance Sheet

• Equity section line items usually include• Book value of common stock, sometimes divided into par value and additional

amounts paid to the company (APIC)• Book value of preferred stock, also showing par value and additional amounts• Retained earnings

• Inferring events from the balance sheet & other data• The balance sheet shows a snapshot at the end of a period• Comparing two consecutive balance sheets can show changes

• Retained earnings will increase based on profits (net income) and be reduced by payouts (such as dividends). Can you rearrange this data to solve for missing parts?

• Stock issuance will affect both the stock at par value and the additional paid-in capital. Can you determine the number of shares or the share price from data like this?

Michael DimondSchool of Business Administration

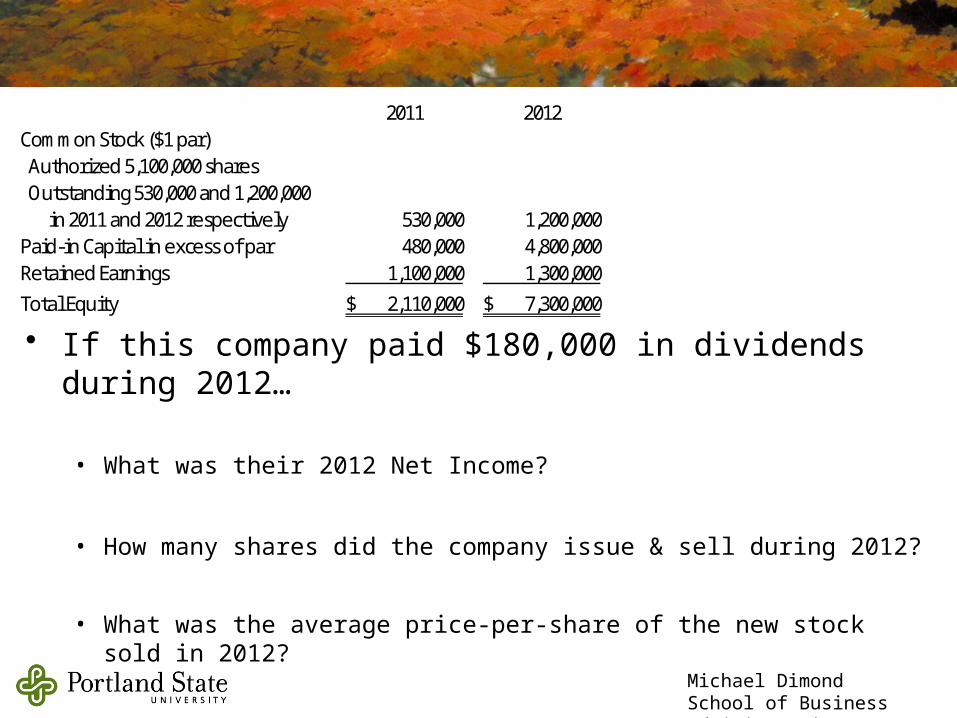

• If this company paid $180,000 in dividends during 2012…

• What was their 2012 Net Income?

• How many shares did the company issue & sell during 2012?

• What was the average price-per-share of the new stock sold in 2012?

2011 2012Common Stock ($1 par) Authorized 5,100,000 shares Outstanding 530,000 and 1,200,000 in 2011 and 2012 respectively 530,000 1,200,000 Paid-in Capital in excess of par 480,000 4,800,000 Retained Earnings 1,100,000 1,300,000

Total Equity 2,110,000$ 7,300,000$