business valuation - bangalore branch of sirc of the ... 8 business valuation is affected by •...

TRANSCRIPT

9/12/2009

1

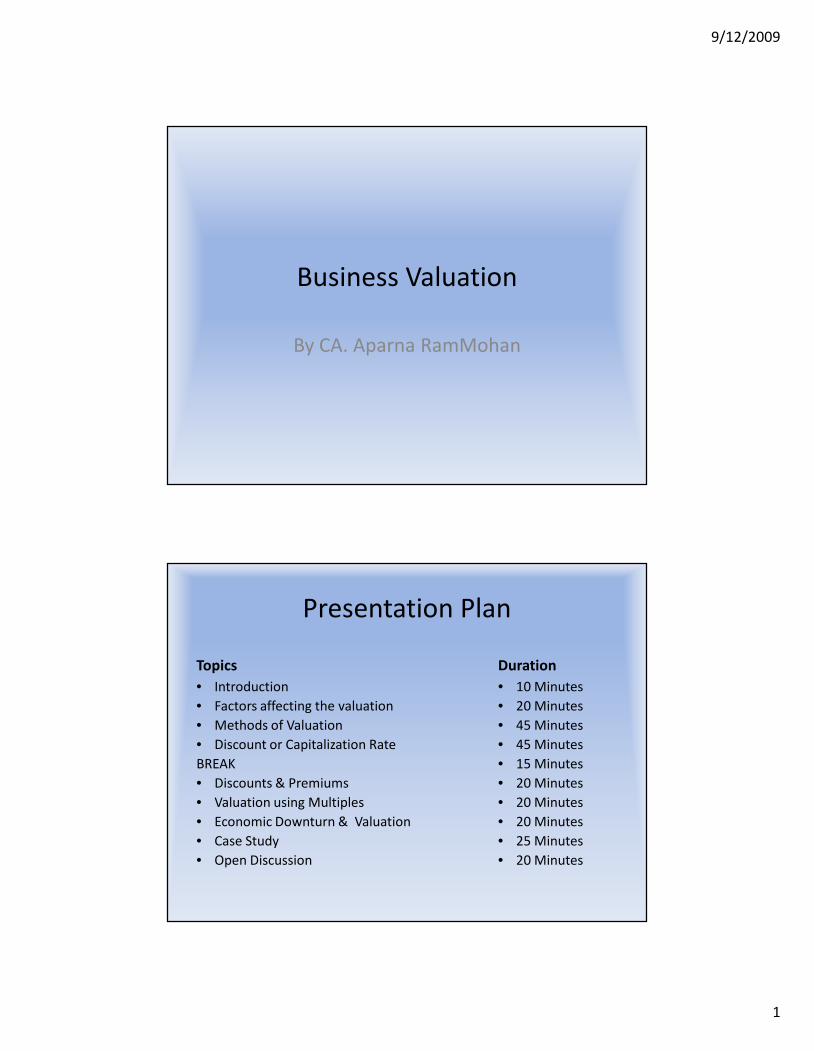

Business Valuation

By CA. Aparna RamMohan

Presentation Plan

Topics• Introduction• Factors affecting the valuation• Methods of Valuation• Discount or Capitalization RateBREAK• Discounts & Premiums• Valuation using Multiples• Economic Downturn & Valuation• Case Study• Open Discussion

Duration• 10 Minutes• 20 Minutes• 45 Minutes• 45 Minutes• 15 Minutes• 20 Minutes• 20 Minutes• 20 Minutes• 25 Minutes• 20 Minutes

9/12/2009

2

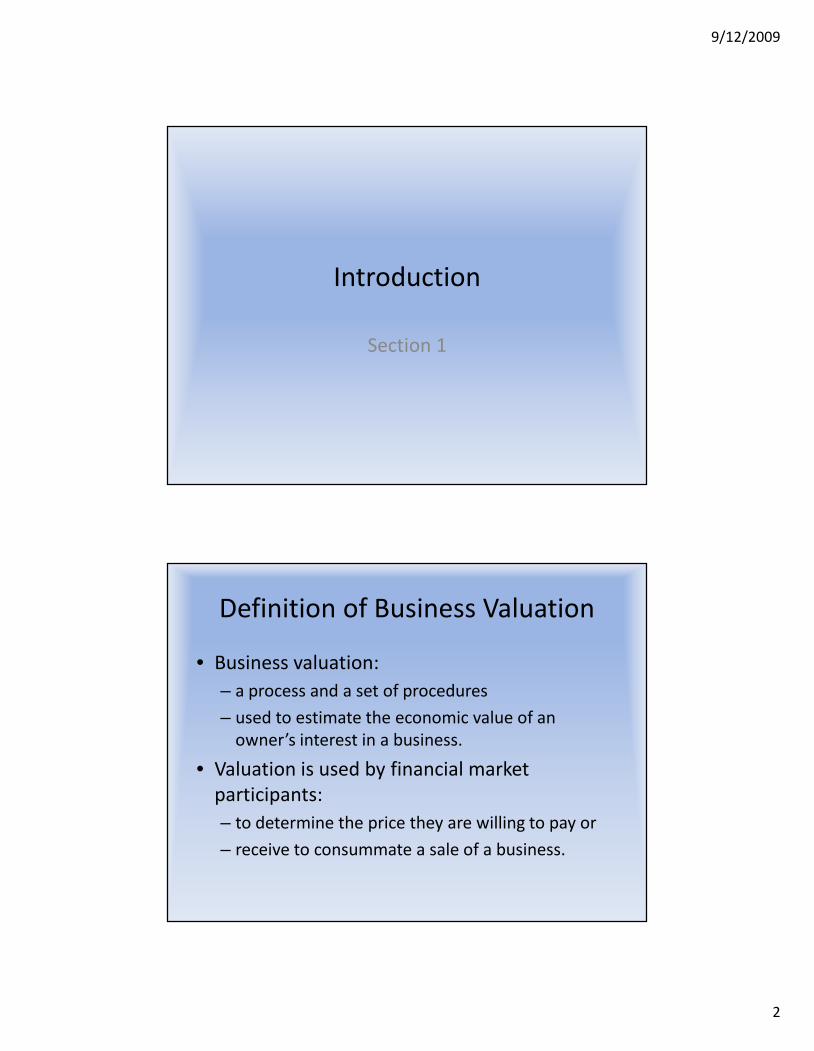

Introduction

Section 1

Definition of Business Valuation

• Business valuation:– a process and a set of procedures– used to estimate the economic value of an

owner’s interest in a business.

• Valuation is used by financial marketparticipants:– to determine the price they are willing to pay or– receive to consummate a sale of a business.

9/12/2009

3

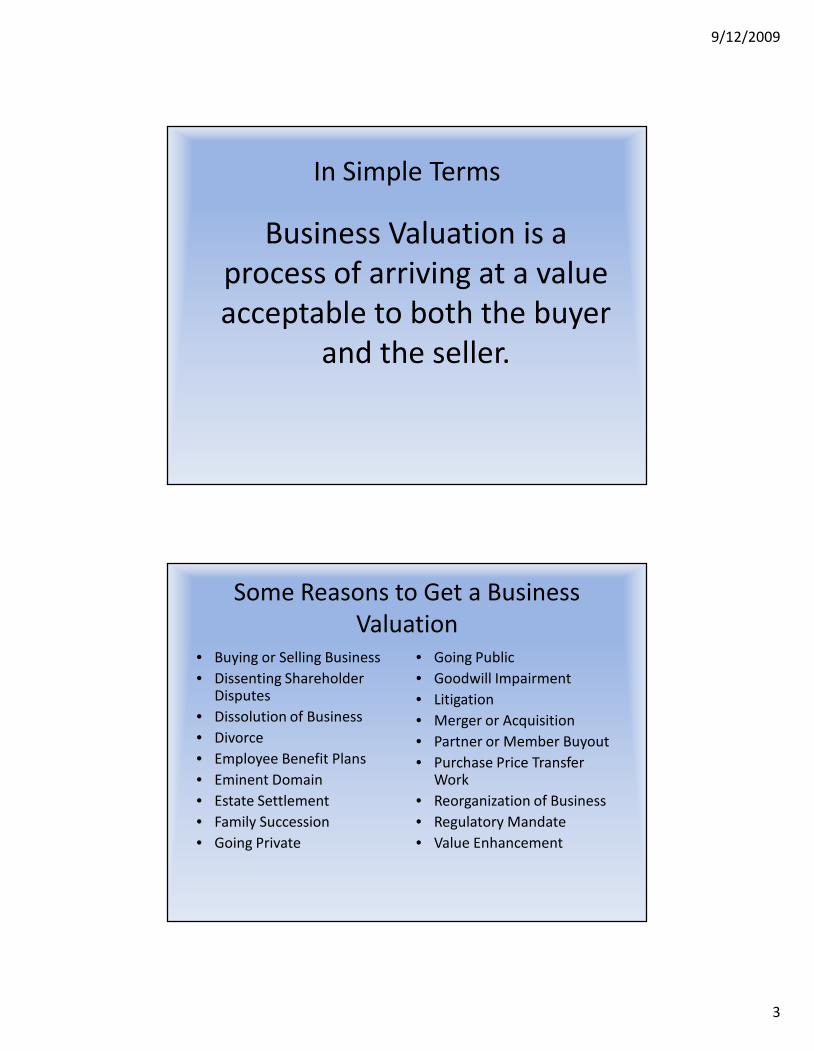

In Simple Terms

Business Valuation is aprocess of arriving at a valueacceptable to both the buyer

and the seller.

Some Reasons to Get a BusinessValuation

• Buying or Selling Business• Dissenting Shareholder

Disputes• Dissolution of Business• Divorce• Employee Benefit Plans• Eminent Domain• Estate Settlement• Family Succession• Going Private

• Going Public• Goodwill Impairment• Litigation• Merger or Acquisition• Partner or Member Buyout• Purchase Price Transfer

Work• Reorganization of Business• Regulatory Mandate• Value Enhancement

9/12/2009

4

What Does a Valuer Need to Know?

• Accounting• Best Practices• Capital Structure• Corporate Governance

Implications• Economics• Financial Statement

Analysis

• Growth Analysis• Industry Information• Legal Environment:

Federal, State, Local• Management Strategy• Regulatory Standards• Statistics• Taxes

What Affects Valuation Results?

• Approach / Model• Assumptions• Data• Purpose / Objectives• Regulations• Time Period

9/12/2009

5

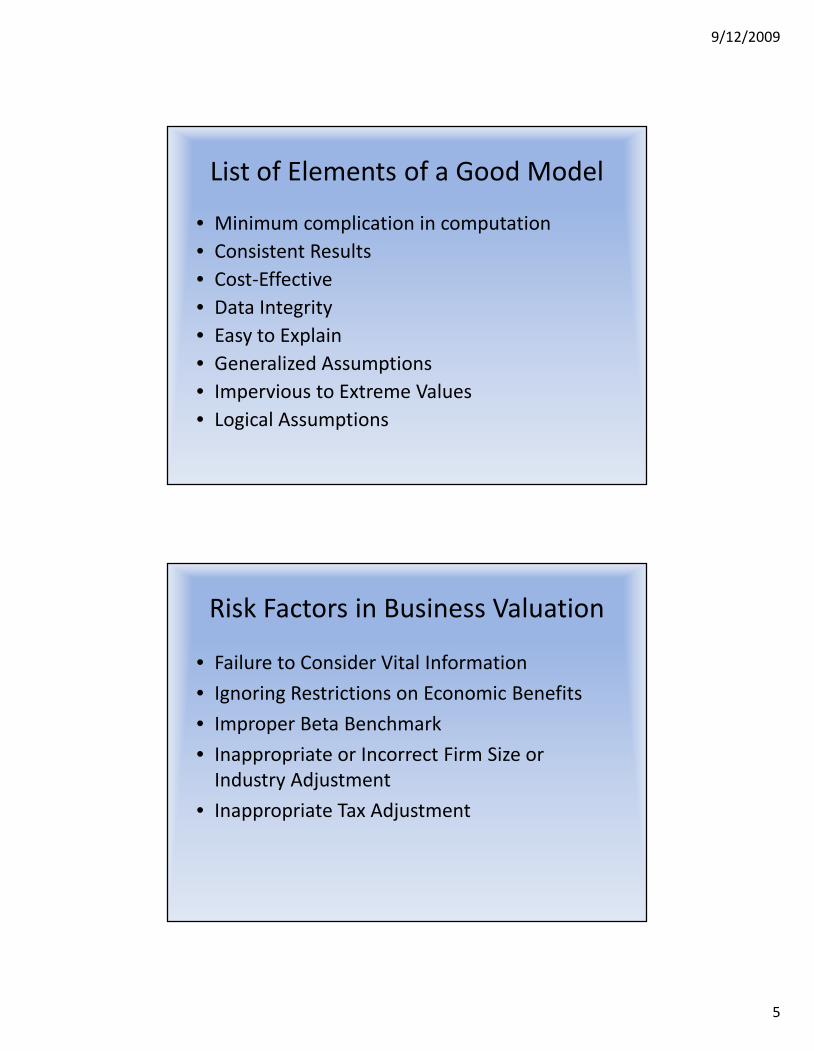

List of Elements of a Good Model

• Minimum complication in computation• Consistent Results• Cost-Effective• Data Integrity• Easy to Explain• Generalized Assumptions• Impervious to Extreme Values• Logical Assumptions

Risk Factors in Business Valuation

• Failure to Consider Vital Information• Ignoring Restrictions on Economic Benefits• Improper Beta Benchmark• Inappropriate or Incorrect Firm Size or

Industry Adjustment• Inappropriate Tax Adjustment

9/12/2009

6

Factors affecting Valuation

Section 2

Valuation Approaches

• Business valuation for going concern– It is important to understand the benefits,

business is able to generate in future out of itsexisting stock of assets although value of existingassets is not ignored by accountants

• Business valuation in case of liquidation– The emphasis is what can be fetched by selling the

assets either on piecemeal basis or taking as awhole

9/12/2009

7

Valuation in case of amalgamation

• The maximum price which a potentialpurchaser will be ready to pay will be:– Price = Value of (combined – existing) business

• Both tangible & intangible assets areconsidered for valuation

• Valuation = NRV of the surplus assets whichare to be sold + the PV of the additionalearnings / cash flows which will accrue to theacquirer as a result of the acquisition.

Valuation depends on

• Business Value Standard– The business value standard is the hypothetical

conditions under which the business will be valued.

• Premise of Value– The premise of value relates to the assumptions, such

as:• the business will continue forever in its current form (going

concern), or• the value of the business lies in the proceeds from the sale

of all of its assets minus the related debt.

9/12/2009

8

Business Valuation is affected by

• Economic Conditions• Financial Analysis• Normalization of financial statements

Economic Conditions

• National, regional and local economicconditions existing as of the valuation date

• The conditions of the industry in which thesubject business operates.

• A common source of economic informationare:– Publications by the Central and State Government,– Publications & Reports by Industry associations– Reports by Economists, Financial Analysts etc

9/12/2009

9

Financial Analysis• The financial statement analysis generally involves:

– ratio analysis (liquidity, turnover, profitability, etc.),– trend analysis and– industry comparative analysis– Size and volume analysis

• Industry Comparison helps in:– discovering trends affecting the company / the industry over time– risk assessment– Determination of the discount rate and– selection of market multiples

• Comparison in different time periods in viewing:– growth or decline in revenues or expenses,– changes in capital structure, or– other financial trends.

Normalization of Financial Statements

The most common normalization adjustmentsfall into the following four categories:• Comparability Adjustments• Non-operating Adjustments• Non-recurring Adjustments• Discretionary Adjustments

9/12/2009

10

Comparability Adjustments

• The valuer may adjust the subject company’sfinancial statements to facilitate acomparison:– with other businesses in the same industry– with other businesses in the same geography

• Intention of these adjustments are toeliminate the differences between:– published industry data presentation– company’s financial statements presentation

Non-operating Adjustments

Assume

• business weresold in ahypotheticalsales transaction

Then

• the seller wouldretain any assetswhich were notrelated to theproduction ofearnings or pricethose non-operating assetsseparately.

That’s Why

• non-operatingassets (such asexcess cash) areusuallyeliminated fromthe balancesheet.

9/12/2009

11

Non-recurring Adjustments

Non recurring adjustment are not expected to recur,such as:

• the purchase or sale of assets,• a lawsuit, or• an unusually large revenue or expense

These non-recurring items are adjusted so that thefinancial statements will better reflect themanagement’s expectations of future performance.

Discretionary Adjustments

• The owners ofprivate companiesmay be paid atvariance from themarket level ofcompensation thatsimilar executives inthe industry mightcommand.

At par withIndustry

• In order todetermine fairmarket value, theowner’scompensation,benefits, perquisitesand distributionsmust be adjusted toindustry standards.

Fair MarketValue

• Similarly, the rentpaid by the subjectbusiness for the useof property ownedby the company’sowners individuallymay be scrutinized.

MarketRate

9/12/2009

12

Factors considered by an investor• Risk vs. Reward –

– An Investor must evaluate a company from the viewpoint that it is risking its own capital tocapitalize another company.

– And for that risk and use of money, they deserve a reward.– The higher the risk of financial loss, the more reward will likely be asked of a potential

portfolio investment company.• How Much Capital is Needed? –

– An Investor will try to assess the amount of capital that a business needs in order to succeed.– Too little capital and the business risks failing.– Invest too much capital, and the Investor has tied up more money than it needed, thus losing

other potential investment earnings.• How Fast Will Revenues Grow? –

– Another factor that the investor must consider is the rate at which revenues are predicted toincrease until they can take out their “reward” or financial return.

– Some companies may take up to five years or more before they even see a profit and are ableto incorporate with an IPO.

– The longer that Investor money will be tied up, the more return they will ask for at their exitpoint.

Methods of Valuation

Section 3

9/12/2009

13

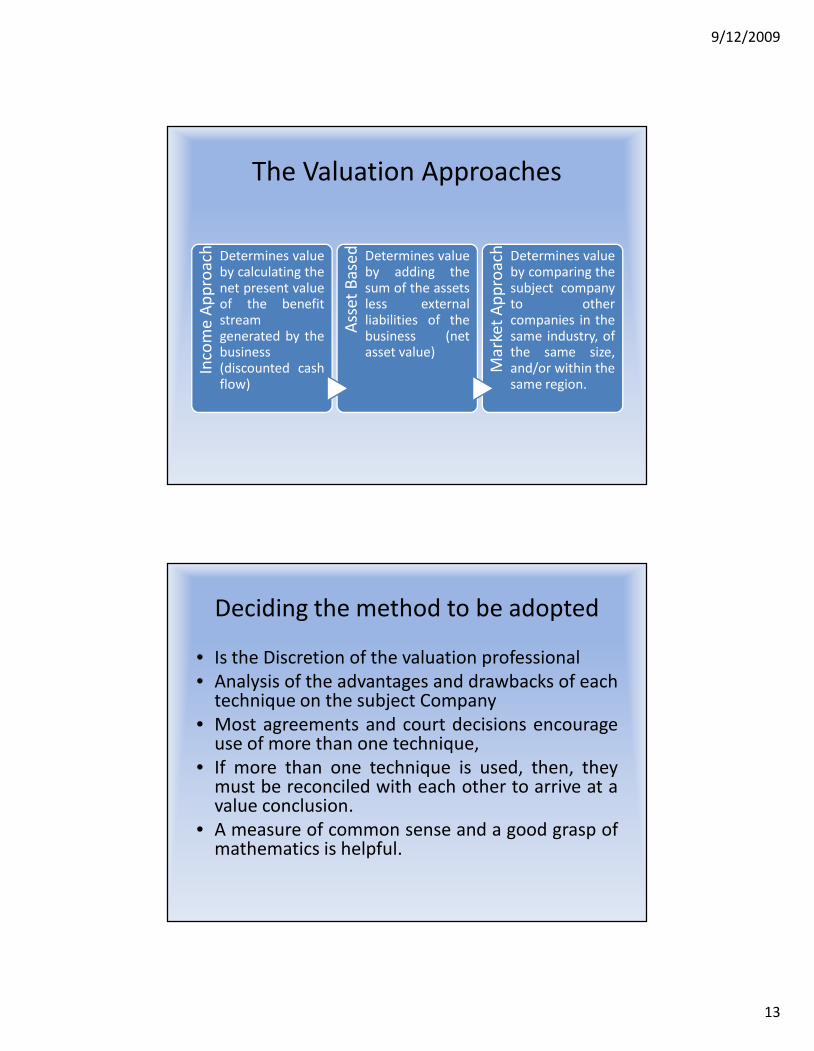

The Valuation ApproachesIn

com

e Ap

proa

ch Determines valueby calculating thenet present valueof the benefitstreamgenerated by thebusiness(discounted cashflow)

Asse

t Bas

ed Determines valueby adding thesum of the assetsless externalliabilities of thebusiness (netasset value)

Mar

ket A

ppro

ach Determines value

by comparing thesubject companyto othercompanies in thesame industry, ofthe same size,and/or within thesame region.

Deciding the method to be adopted

• Is the Discretion of the valuation professional• Analysis of the advantages and drawbacks of each

technique on the subject Company• Most agreements and court decisions encourage

use of more than one technique,• If more than one technique is used, then, they

must be reconciled with each other to arrive at avalue conclusion.

• A measure of common sense and a good grasp ofmathematics is helpful.

9/12/2009

14

Income Approach• Fair market value = net cash flow * discount or capitalization rate.• There are several income approaches, including:

– capitalization of earnings or cash flows,– discounted future cash flows (“DCF”), and– the excess earnings method (which is a hybrid of asset and income

approaches).• Only DCF requires data for multiple future periods.• Others look in single period historical data.• Income Approach results in the fair market value of:

– controlling interest --> since the entire benefit stream of the subjectcompany is most often valued

– marketable interest --> the capitalization and discount rates arederived from statistics concerning public companies.

Adjusted present value• APV is a business valuation method similar to the standard DCF Model.• Instead of WACC, cash flows would be discounted at the unlevered cost of

equity, and tax shields at the cost of debt.• APV is the net present value of a project if financed solely by ownership

equity plus the present value of all the benefits of financing.• The method is to calculate the NPV of the project as if it is all-equity

financed (so called base case). Then the base-case NPV is adjusted for thebenefits of financing.

• Usually, the main benefit is a tax shield resulted from tax deductibility ofinterest payments. Another benefit can be a subsidized borrowing at sub-market rates.

• The APV method is especially effective when a leveraged buyout case isconsidered since the company is loaded with an extreme amount of debt,so the tax shield is substantial.

• APV and the standard DCF approaches should give the identical result ifthe capital structure remains stable.

9/12/2009

15

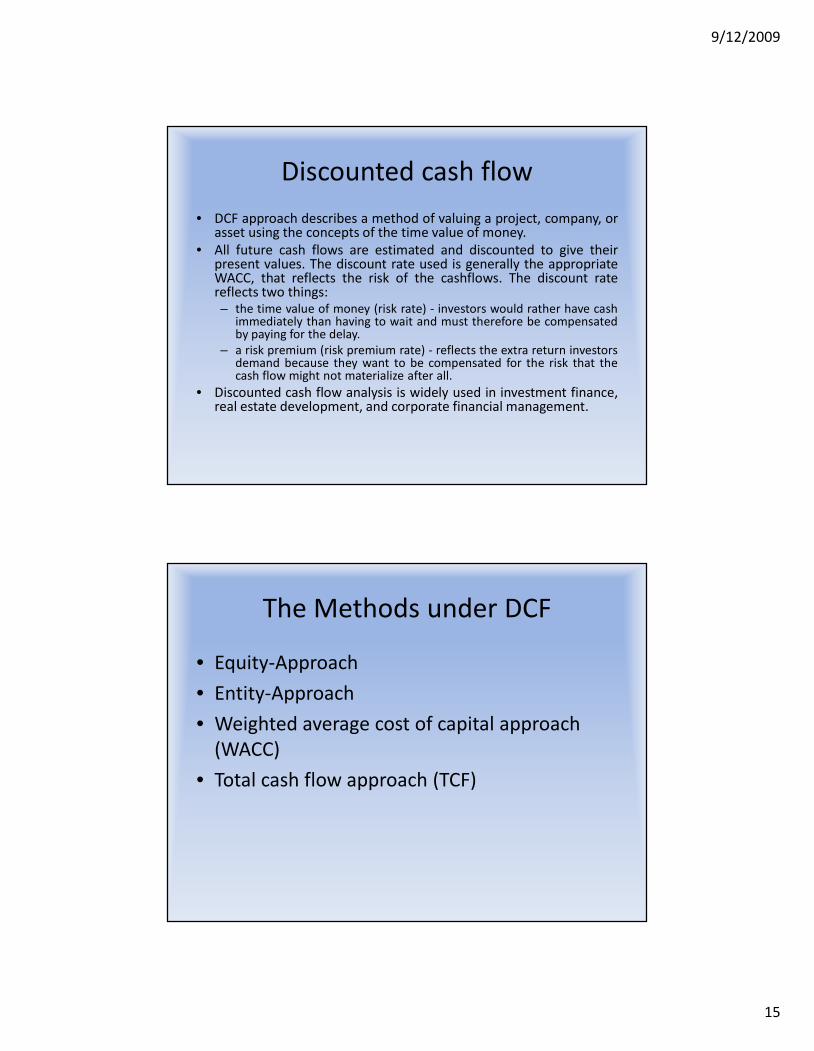

Discounted cash flow• DCF approach describes a method of valuing a project, company, or

asset using the concepts of the time value of money.• All future cash flows are estimated and discounted to give their

present values. The discount rate used is generally the appropriateWACC, that reflects the risk of the cashflows. The discount ratereflects two things:– the time value of money (risk rate) - investors would rather have cash

immediately than having to wait and must therefore be compensatedby paying for the delay.

– a risk premium (risk premium rate) - reflects the extra return investorsdemand because they want to be compensated for the risk that thecash flow might not materialize after all.

• Discounted cash flow analysis is widely used in investment finance,real estate development, and corporate financial management.

The Methods under DCF

• Equity-Approach• Entity-Approach• Weighted average cost of capital approach

(WACC)• Total cash flow approach (TCF)

9/12/2009

16

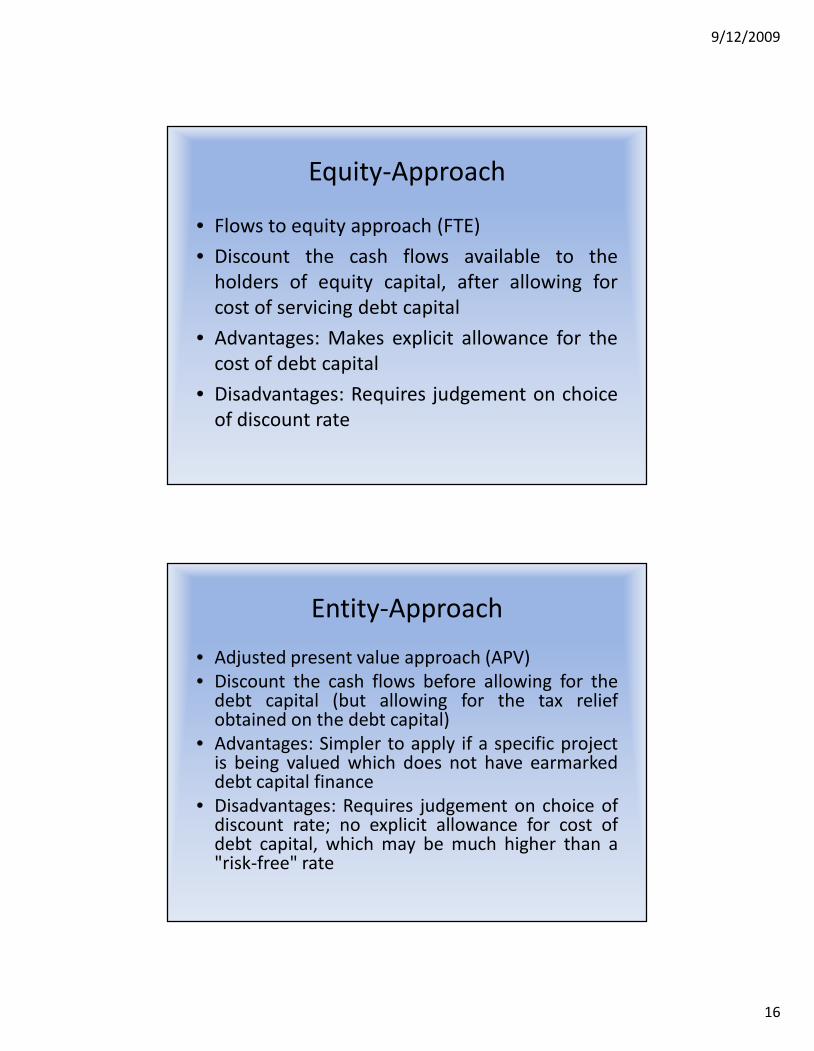

Equity-Approach

• Flows to equity approach (FTE)• Discount the cash flows available to the

holders of equity capital, after allowing forcost of servicing debt capital

• Advantages: Makes explicit allowance for thecost of debt capital

• Disadvantages: Requires judgement on choiceof discount rate

Entity-Approach• Adjusted present value approach (APV)• Discount the cash flows before allowing for the

debt capital (but allowing for the tax reliefobtained on the debt capital)

• Advantages: Simpler to apply if a specific projectis being valued which does not have earmarkeddebt capital finance

• Disadvantages: Requires judgement on choice ofdiscount rate; no explicit allowance for cost ofdebt capital, which may be much higher than a"risk-free" rate

9/12/2009

17

Weighted average cost of capitalapproach

• Derive a weighted cost of the capital obtainedfrom the various sources and use that discountrate to discount the cash flows from the project

• Advantages: Overcomes the requirement for debtcapital finance to be earmarked to particularprojects

• Disadvantages: Care must be exercised in theselection of the appropriate income stream. Thenet cash flow to total invested capital is thegenerally accepted choice.

Total cash flow approach (TCF)

• This distinction illustrates that the Discounted CashFlow method can be used to determine the value ofvarious business ownership interests. These caninclude equity or debt holders.

• Alternatively, the method can be used to value thecompany based on the value of total invested capital.In each case, the differences lie in the choice of theincome stream and discount rate.

• For example, the net cash flow to total invested capitaland WACC are appropriate when valuing a companybased on the market value of all invested capital.

9/12/2009

18

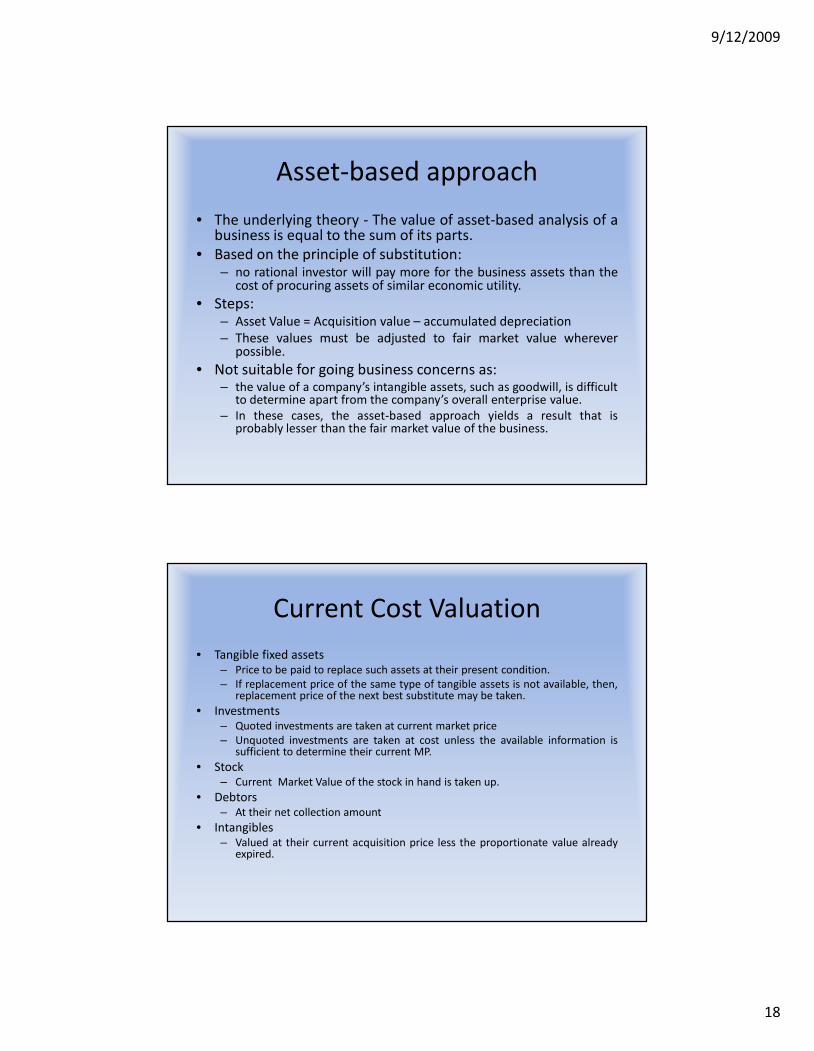

Asset-based approach• The underlying theory - The value of asset-based analysis of a

business is equal to the sum of its parts.• Based on the principle of substitution:

– no rational investor will pay more for the business assets than thecost of procuring assets of similar economic utility.

• Steps:– Asset Value = Acquisition value – accumulated depreciation– These values must be adjusted to fair market value wherever

possible.• Not suitable for going business concerns as:

– the value of a company’s intangible assets, such as goodwill, is difficultto determine apart from the company’s overall enterprise value.

– In these cases, the asset-based approach yields a result that isprobably lesser than the fair market value of the business.

Current Cost Valuation• Tangible fixed assets

– Price to be paid to replace such assets at their present condition.– If replacement price of the same type of tangible assets is not available, then,

replacement price of the next best substitute may be taken.• Investments

– Quoted investments are taken at current market price– Unquoted investments are taken at cost unless the available information is

sufficient to determine their current MP.• Stock

– Current Market Value of the stock in hand is taken up.• Debtors

– At their net collection amount• Intangibles

– Valued at their current acquisition price less the proportionate value alreadyexpired.

9/12/2009

19

Control of shareholders• Points to be considered:

– shareholder whose interest is being valued would have any authorityto access the value of the assets directly

– Controlling Shareholder– Non Controlling Shareholder

• Shareholders own shares in a corporation, but not its assets, whichare owned by the corporation.

• A controlling shareholder may have the authority to direct thecorporation to sell all or part of the assets it owns and to distributethe proceeds to the shareholder(s).

• The non-controlling shareholder, however, lacks this authority andcannot access the value of the assets.

• Value of a corporation's assets is rarely the most relevant indicatorof value to a shareholder who cannot avail himself of that value.

Income vs Asset Approach

• Income-based approaches– requires the valuation professional to make

subjective judgments about capitalization ordiscount rates

• Adjusted net book value method– is relatively objective, adjustment of current book

value to the fair market value

9/12/2009

20

Use of Asset-based approach• Adjusted net book value may be the most relevant

standard of value:– where liquidation is imminent or ongoing;– where a company earnings or cash flow are nominal,

negative or worth less than its assets;– or where net book value is standard in the industry in

which the company operates.• None of these situations applies to the Company which

is the subject of this valuation report. However, theadjusted net book value may be used as a “sanitycheck” when compared to other methods of valuation,such as the income and market approaches.

Market approach

• Based on the economic principle of competition:– that in a free market the supply and demand forces

will drive the price of business assets to a certainequilibrium.

• Buyers would not pay more for the business, andthe sellers will not accept less, than the price of acomparable business enterprise.

• It is similar in many respects to the “comparablesales” method that is commonly used in realestate appraisal.

9/12/2009

21

Indicators to Market approach• The market price of the stocks of publicly traded companies

engaged in the same or a similar line of business, whoseshares are actively traded in a free and open market, canbe a valid indicator of value when the transactions in whichstocks are traded are sufficiently similar to permitmeaningful comparison.

• The difficulty lies in identifying public companies that aresufficiently comparable to the subject company for thispurpose.

• Also, as for a private company, the equity is less liquid (inother words its stocks are less easy to buy or sell) than for apublic company, its value is considered to be slightly lowerthan such a market-based valuation would give.

Guideline Public Company method• The Guideline Public Company method entails a comparison of the subject

company to publicly traded companies.• The comparison is generally based on published data regarding the public

companies’ stock price and earnings, sales, or revenues, which isexpressed as a fraction known as a “multiple.”

• If the guideline public companies are sufficiently similar to each other andthe subject company to permit a meaningful comparison, then theirmultiples should be similar.

• The public companies identified for comparison purposes should besimilar to the subject company in terms of:– industry,– product lines,– market,– growth,– margins and– risk

9/12/2009

22

Guideline Transaction Method• Also known as Direct Market Data Method• Involves determination of market multiples by reviewing

published data regarding actual transactions involvingeither minority or controlling interests in either publiclytraded or closely held companies.

• In judging whether a reasonable basis for comparisonexists, the valuation analysis must consider:– the similarity of qualitative and quantitative investment and

investor characteristics;– the extent to which reliable data is known about the

transactions in which interests in the guideline companies werebought and sold; and

– whether or not the price paid for the guideline companies wasin an arms-length transaction, or a forced or distressed sale.

Discount or Capitalization Rate

Section 4

9/12/2009

23

Discount or capitalization rates• A discount rate or capitalization rate is used to determine

the present value of the expected returns of a business.• The discount rate and capitalization rate are closely related

to each other, but distinguishable.• The discount rate is composed of two elements:

– the risk-free rate, which is the return that an investor wouldexpect from a secure, risk-free investment, such as a highquality government bond; plus

– a risk premium that compensates an investor for the relativelevel of risk associated with a particular investment in excess ofthe risk-free rate.

• Most importantly, the selected discount or capitalizationrate must be consistent with stream of benefits to which itis to be applied.

Difference between D/R & C/R

• Discount Rate– is used to calculate the net present value of a

series of projected cash flows.

• Capitalization rate– is applied for a single period of time data

valuation

9/12/2009

24

Methods of calculating discount rate

METHODS

Capital Asset Pricing Model

Wei

ght A

vera

ge C

ost o

f Cap

ital

Built up Model

Capital Asset Pricing Model (“CAPM”)

• Determines the appropriate discount rate in businessvaluations.

• The CAPM method originated from the Nobel Prize winningstudies of Harry Markowitz, James Tobin and WilliamSharpe.

• Ke = Rf + Rp,• Rp = Beta*(Rm-Rf)• Beta is a measure of stock price volatility.• Beta is published by various sources for particular

industries and companies.• Beta is associated with the systematic risks of an

investment.

9/12/2009

25

Criticisms of CAPM Model• Beta is derived from the volatility of prices of publicly-

traded companies, which are likely to differ fromprivate companies in their:– capital structures,– diversification of products and markets,– access to credit markets,– size,– management depth,– and many other respects.

• CAPM method may be appropriate where privatecompanies can be shown to be sufficiently similar topublic companies.

Weighted Average Cost of Capital• Cost of capital = weighted average of the

company’s cost of debt and cost of equity.• Calculation of WACC is based on the subject

company’s:– existing capital structure,– the average industry capital structure, or– the optimal capital structure.

• WACC captures the risk of the subject business.• The existing or contemplated capital structures

are better choices for business valuation.

9/12/2009

26

Appropriate Match for WACC• Choices of applying the rate to an appropriate economic income streams:

– pretax cash flow,– aftertax cash flow,– pretax net income,– after tax net income,– excess earnings,– projected cash flow

• Appropriate choice is critical to the accuracy of the valuation results• Most chosen choice – After tax cash flow• Rationale for the choice:

– this earnings basis corresponds to the equity discount rate derived from theBuild-Up or CAPM models

– the returns obtained from investments in publicly traded companies can easilybe represented in terms of net cash flows.

– At the same time, the discount rates are generally also derived from the publiccapital markets data.

WACC Formula

9/12/2009

27

Built-Up Method

Determines the after-taxnet cash flow discountrate. It is called built upbecause it is the sum ofrisks associated withvarious classes of assets.

Principle --> investorswould require a greaterreturn on classes ofassets that are morerisky. First element is Rf,which is the min return.

Large-cap equity stocksare inherently more riskythan long-termgovernment bonds,requiring a greaterreturn. Second elementis equity risk premium.

Small cap stocks areriskier than blue-chipstocks, requiring agreater return, called thesize premium, the thirdelement (based onindustry reports)

Risk Factor in the Built-Up Method• In determining a company’s value, the long-horizon equity risk premium is

used because the Company’s life is assumed to be infinite.• Built up discount rate (systematic risk) for:

– Large Cap Equity Investors : Rate = Rf+ Rp– Small Cap Equity Investors : Rate = Rf+ Rp + Size Premium

• These three elements of the Build-Up discount rate are known collectivelyas the “systematic risks.”

• Discount Rate = Systematic Risks + Unsystematic Risks• Unsystematic Risks:

– Industry Risk Premium– specific company risk

9/12/2009

28

Butler Pinkerton Model (BPM)• Historically, no published data has been available to quantify specific

company risks.• However as of late 2006, new ground-breaking research has been able

to quantify, or isolate, this risk for publicly-traded stocks through theuse of Total Beta calculations, using a modified Capital Asset PricingModel ( CAPM) to calculate the company specific risk premium.

• Total Beta (CAPM Model) = Firm's beta + size premium + companyspecific risk premium

• The equality is then solved for the company specific risk premium asthe only unknown.

• The BPM is a relatively new concept and is gaining acceptance in thebusiness valuation community.

Rate for Small private companies• Capitalization rate for small, privately-held companies is significantly

higher than the return that an investor might expect to receive from othercommon types of investments, such as money market accounts, mutualfunds, or even real estate, due to higher risks.

• Those investments involve substantially lower levels of risk than aninvestment in a closely-held company.

• Depository accounts are insured by the government (up to certain limits);mutual funds are composed of publicly-traded stocks, for which risk canbe substantially minimized through portfolio diversification.

• Closely-held companies, on the other hand, frequently fail for a variety ofreasons too numerous to name.

• There are no government guarantees.• The risk of investing in a private company cannot be reduced through

diversification, and most businesses do not own the type of hard assetsthat can ensure capital appreciation over time.

9/12/2009

29

Discounts & Premiums

Section 5

Discounts and premiums• The valuation approaches yield the fair market value of the Company as a

whole.• In valuing a minority, non-controlling interest in a business, however, the

valuation professional must consider the applicability of discounts that affectsuch interests.

• Discussions of discounts and premiums frequently begin with a review of the“levels of value.”

• There are three common levels of value:– controlling interest,– marketable minority, and– non-marketable minority.

• The intermediate level, marketable minority interest, is lesser than thecontrolling interest level and higher than the non-marketable minority interestlevel.

• The marketable minority interest level represents the perceived value ofequity interests that are freely traded without any restrictions.

• These interests are generally traded on the stock exchanges where there is aready market for equity securities.

9/12/2009

30

Marketable Minority• The intermediate level, marketable minority interest, is lesser than

the controlling interest level and higher than the non-marketableminority interest level.

• The marketable minority interest level represents the perceivedvalue of equity interests that are freely traded without anyrestrictions.

• These interests are generally traded on the stock exchanges wherethere is a ready market for equity securities.

• These values represent a minority interest in the subject companies– small blocks of stock that represent less than 50% of thecompany’s equity.

• Controlling interest level is the value that an investor would bewilling to pay to acquire more than 50% of a company’s stock,thereby gaining the attendant prerogatives of control.

Controlling Interest Level• Controlling interest level is the value that an investor would be

willing to pay to acquire more than 50% of a company’s stock,thereby gaining the attendant prerogatives of control.

• Some of the prerogatives of control include:– electing directors, hiring and firing the company’s management and

determining their compensation;– declaring dividends and distributions, determining the company’s

strategy and line of business, and– acquiring, selling or liquidating the business.

• This level of value generally contains a control premium over theintermediate level of value, which typically ranges from 25% to50%.

• An additional premium may be paid by strategic investors who aremotivated by synergistic motives.

9/12/2009

31

Non-marketable minority level• Non-marketable, minority level is the lowest level on the chart, representing the

level at which non-controlling equity interests in private companies are generallyvalued or traded.

• This level of value is discounted because no ready market exists in which topurchase or sell interests.

• Private companies are less “liquid” than publicly-traded companies, andtransactions in private companies take longer and are more uncertain.

• Between the intermediate and lowest levels of the chart, there are restrictedshares of publicly-traded companies.

• Valuation discounts are actually increasing as the differences between public andprivate companies is widening .

• Publicly-traded stocks have grown more liquid in the past decade due to rapidelectronic trading, reduced commissions, and governmental deregulation.

• These developments have not improved the liquidity of interests in privatecompanies, however.

• Valuation discounts are multiplicative, so they must be considered in order.• Control premiums and their inverse, minority interest discounts, are considered

before marketability discounts are applied.

Discount for lack of control

• The first discount that must be considered is thediscount for lack of control, which in this instance isalso a minority interest discount.

• Minority interest discounts are the inverse of controlpremiums, to which the following mathematicalrelationship exists: MID = 1 – [1 / (1 + CP)].

• Mergerstat defines the “control premium” as thepercentage difference between the acquisition priceand the share price of the freely-traded public sharesfive days prior to the announcement of the M&Atransaction.

9/12/2009

32

Discount for lack of marketability• Marketability is defined as the ability to convert the business interest into

cash quickly, with minimum transaction and administrative costs, and witha high degree of certainty as to the amount of net proceeds.

• There is usually a cost and a time lag associated with locating interestedand capable buyers of interests in privately-held companies, becausethere is no established market of readily-available buyers and sellers.

• All other factors being equal, an interest in a publicly traded company isworth more because it is readily marketable, which is also true conversely.

• The discount for lack of control is separate and distinguishable from thediscount for lack of marketability.

• Several empirical studies have been published that attempt to quantifythe discount for lack of marketability. These studies include the restrictedstock studies and the pre-IPO studies. The aggregate of these studiesindicate average discounts of 35% and 50%, respectively. Some expertsbelieve the Lack of Control and Marketability discounts can aggregatediscounts for as much as ninety percent of a Company's fair market value,specifically with family owned companies.

Restricted stock studies• Restricted stocks are equity securities of public companies that are similar in all

respects to the freely traded stocks of those companies except that they carry arestriction that prevents them from being traded on the open market for a certainperiod of time, which is usually one year.

• This restriction from active trading, which amounts to a lack of marketability, is theonly distinction between the restricted stock and its freely-traded counterpart.

• Restricted stock can be traded in private transactions and usually do so at adiscount.

• The restricted stock studies attempt to verify the difference in price at which therestricted shares trade versus the price at which the same unrestricted securitiestrade in the open market as of the same date.

• The underlying data by which these studies arrived at their conclusions has notbeen made public. Consequently, it is not possible when valuing a particularcompany to compare the characteristics of that company to the study data.

• Still, the existence of a marketability discount has been recognized by valuationprofessionals and the Courts, and the restricted stock studies are frequently citedas empirical evidence. Notably, the lowest average discount reported by thesestudies was 26% and the highest average discount was 45%.

9/12/2009

33

Pre-IPO studies• Another approach to measure the marketability discount is

to compare the prices of stock offered in initial publicofferings (IPOs) to transactions in the same company’sstocks prior to the IPO.

• Companies that are going public are required to disclose alltransactions in their stocks for a period of 3 years prior tothe IPO.

• The pre-IPO studies are sometimes criticized because thesample size is relatively small, the pre-IPO transactions maynot be arm’s length, and the financial structure and productlines of the studied companies may have changed duringthe three year pre-IPO window.

Valuation using Multiples

Section 6

9/12/2009

34

Valuation using multiples• A method for determining the current value of a company by examining

and comparing the financial ratios of relevant peer groups, also oftendescribed as comparable company analysis .

• The most widely used multiple is the price-earnings ratio (P/E ratio) ofstocks in a similar industry. Using the average of multiple PERs improvesreliability but it can still be necessary to correct the PER for current marketconditions.

• Particular attention is paid to companies with P/E ratios substantiallyhigher or lower than the peer group.

• A P/E far below the average can mean (among other reasons) that the truevalue of a company has not been identified by the market, that thebusiness model is flawed, or that the most recent profits include, forexample, substantial one-off items.

Steps for valuation• Companies with P/E ratios substantially different from the peers (the

outliers) can be removed or other corrective measures used to avoid thisproblem.

• P/E multiples are popular in part due to their wide availability. The value ofa business should, however, be reflected in multiples based on enterprisevalue (EV/EBITDA, EV/EBIT, EV/NOPAT) of a company.

• These multiples reveal the rating of a business independently of its capitalstructure.– Determine Forecast Period– Identifying peer companies– Determining correct Price Earning Ratio (P/E)– Determining future company value– Determining discount rate / factor– Determining current company value

9/12/2009

35

More details• Identifying peer companies

– Important characteristics include: operating margin, company size, products,customer segmentation, growth rate, cash flow, number of employees, etc.

• Determining correct Price Earning Ratio (P/E)– The price earnings ratio (P/E) of each identified peer company can be

calculated as long as they are profitable. The P/E is calculated as: P/E = CurrentStock Price / (Net Profit / Number of shares)

• Determining discount rate / factor– Determine the appropriate discount rate and factor for the last year of the

forecast period based on the risk level associated with the target company• Determining current company value

– Calculate the current value of the future company value by multiplying thefuture business value with the discount factor. This is known as the time valueof money.

Enterprise value• Enterprise value (EV) = Total enterprise value (TEV) = Firm value

(FV).• It is an economic measure reflecting the market value of the whole

business.• It is a sum of claims of all the security-holders:

– debtholders,– preferred shareholders,– minority shareholders,– common equity holders, and others.

• Enterprise value is one of the fundamental metrics used in businessvaluation, financial modeling, accounting, portfolio analysis, etc.

• Enterprise value = common equity at equity value + debt at marketvalue + minority interest at market value - associate company atmarket value + preferred equity at market value - cash and cash-equivalents.

9/12/2009

36

More about Enterprise value• All the components are market, not book values.• Cash is subtracted because when it is paid out as a dividend, it reduces the

net cost to a potential purchaser. Therefore, the business was only worththe reduced amount to start with. The same effect is accomplished whenthe cash is used to pay down debt.

• Value of minority interest is added because it reflects the claim on assetsconsolidated into the firm in question.

• Value of associate companies is subtracted because it reflects the claim onassets consolidated into other firms.

• EV should also include such special components as unfunded pensionliabilities, executive stock options, environmental provisions,abandonment provisions, and so on, for they also reflect claims on thecompany's assets.

• EV can be negative in certain cases—for example, when there is too muchcash in the company.

• EV=NPV of the company.

Flow Chart

9/12/2009

37

How Has the Economic DownturnAffected Business Valuations?

Section 7

Expert’s Opinion

• In this section of business valuation, I havesummarized the opinion of an expert in thefield of business valuation.

• Mr Carlene Gaydosh talks about How Has theEconomic Downturn Affected BusinessValuations?

9/12/2009

38

Business Value• In today's difficult economic environment, are you finding that

businesses have lost value?– Yes, due to the uncertain economy people are less willing to take risk.– The level of risk an investor is willing to take directly drives the value

of a business when it is being considered, particularly when analyzingthe income stream and how much income one requires to generate offof a prospective investment.

• Is this a bad time to value and sell a business?– There is never a bad time to value a business or market it for sale: the

unique economic activity we are currently experiencing createsopportunities for investors and sellers.

– When someone finds himself or herself without a job, especially withhigh unemployment and few available jobs, they often look for self-employment opportunities and, many times, consider purchasing anexisting business.

Opportunities• Franchise and home-based business models do well in periods of

high unemployment, because people look to replace their incomeand, when they cannot find a job, they will look at a businessacquisition.

• Great opportunities available.– Small businesses are more attracted to acquiring other small

businesses, in an effort to diversify products or services and increaserevenue.

– There are some great opportunities now to purchase businesses thatcould benefit from the synergy of a complimentary fit with anotherbusiness in a similar industry or service sector.

• It is not just a good time to buy real estate, it is a buyers’ market forbusiness acquisition and that is where the greater opportunity is;however, the greater the unemployment rate, the greater thedemand for businesses that are available for sale.

9/12/2009

39

Challenges• The challenges of selling.

– Business owners that are considering selling their businessbecause it is failing due to declined sales and poor cashflow may find it challenging to market the business duringthese times because people are less inclined to assumethe risk.

– Potential buyers are finding it very difficult to borrowmoney to purchase a business that is healthy, let alone onethat is struggling, even though there are loans available, sothey say.

– If a buyer is going to borrow the money to purchase,lenders will look at a business valuation to determine theamount it is willing to loan.

Various Perspective

• Business valuations are necessary to demonstrate to apotential buyer the value, as well as provide a guide tothe seller what it is actually worth.

• Most business owners have an inflated perspective onwhat their business is worth because they have puttheir heart and soul into it, and entrepreneurs areeternal optimists.

• Sellers also need to have the knowledge of whatfactors drive the price of their business and managethose vital factors in a manner to package the businessand ready it for sale to maximize the selling price.

9/12/2009

40

Example• This is like getting a house ready for sale.• You need to complete maintenance items and freshen the paint,

landscaping and “image.”• A business is no different, in a sense – it needs to be cleaned up and

positioned within the market to make it more attractive to a potentialbuyer.

• Some examples of housekeeping would be to discount and sell off oldinventory and assets.

• This puts cash into the business and leaves good assets and inventory onthe books.

• Accounts receivable also need to be analyzed and uncollectable accountswritten off or reserved and sent to collections.

• Current assets are a real focus, because they reflect the liquidity of thebusiness and having old account receivables on the books negativelyimpacts the ratio analysis that will be conducted during a lender’svaluation.

Educating the Seller• The process of the business valuation will most importantly

educate the seller about the underlying drivers of the valueand get educated about steps that can be taken to increasethe value during the process.

• The exercise of having your business valued is veryeducational and insightful to owners, and sometimes theyeven decide not to sell the business during the process.

• Business valuations are performed for reasons other thanjust to sell the business, even though usually that is theprimary purpose.

• These reasons include transferring ownership to a familymember for tax reporting or due to the death, divorce ordisability of the owner (the three D’s).

9/12/2009

41

Case Study

Section 8

Objective of this case study

• The case study is designed to give prospectivebusiness acquirers, business owners,financiers, and advisors some insight into therole an independent business valuation mayhave in identifying mispricing of assets andgrounding expectations regarding price andvalue.

9/12/2009

42

Brief Background• XYZ is a local franchised restaurant and pub serving quality lunches at

reasonable prices at ten area locations.• The franchise is well-known throughout the region and has a strong

customer base, ranging from professionals on the go to retirees and localcollege students.

• XYZ's five area locations are organized as individual corporations whichare, in turn, owned and operated by ABC Holdings, Ltd, a local companythat also owns several other franchise restaurants, ice cream shops, andgourmet coffee houses.

• Mr A, Mr B, and Mr C own ABC Holdings, Ltd and are seeking to sell two ofthe XYZ locations that are outside their immediate territory.

• They had started the two locations about eighteen months ago as part ofan expansion plan incentive offered by XYZ’s parent company.

• Since then, ABC Holdings, Ltd declined the rights to additional franchisesin those outlying locations.

The financial aspect

• The two XYZ locations that ABC Holdings Ltd is seekingto sell had revenues of roughly $750,000 each in thelast fiscal year as compared to the other locations thateach generated revenues in excess of $1 million pa.

• Both locations have had trouble maintaining qualitystaff, and the managers have been largely unsuccessfulin running the business and controlling costs.

• However, the locations are in high traffic strip mallswhere rent is roughly $10,000 per month.

• These two locations experienced net losses for the lastfiscal year of roughly $50,000 each.

9/12/2009

43

Investing Proposition• MJ and DJ both work at one of the XYZ's more profitable

locations. Upon hearing rumors that ABC Holdings iscontemplating a sale of the two underperforming locations,they approach Mr A to discuss the possibility of purchasingthe franchises.

• All parties agree that this would be an ideal situation, givenMJ and DJ’s background with the XYZ and theircommitment to increasing the franchises' revenues throughadditional marketing and cost cutting initiatives.

• ABC Holdings offers to sell the two franchises for anaggregate price of $1,000,000. Mark and Diane agree, inprinciple, on the price. The deal is contingent upon theirability to secure financing for the acquisition.

Investors’ Projections• MJ and DJ consult ASC, a local business consultant and former head of the

state's Small Business Development Center who has extensive experiencein negotiating deals and working with entrepreneurs to develop a viablebusiness plan.

• After reviewing the tax return (which lacks a balance sheet) provided byABC Holding's accountants, ASC has several concerns over the viability ofthe plan.

• MJ and DJ believe that they will be able to:– increase sales by over $200,000 at each of the locations within twelve months.– In subsequent years, they anticipate sales to increase by 8% annually.– accomplish this through increased advertising initiatives having a marginal

cost of $10,000.– employee retention and training programs will help to reduce their turnover

expenses by roughly $20,000 per location– will be able to reduce their cost of sales from 35% to 30%, saving $50,000 at

each location, through better employee training and inventory management.• The other XYZ locations have cost of sales of roughly 32%.

9/12/2009

44

Valuation of the locations• As a way of assessing the acquisition of the XYZ locations and in

order to facilitate the lending process, ASC suggests that MJ and DJengage a business valuation firm to provide an estimate of the fairmarket value of the firm.

• They agree to this and feel this is an excellent way of obtaining animpartial opinion on the value of the business relative to the pricebeing paid.

• The valuation analyst receives the tax returns for the XYZ locations.• The valuation analyst utilizes an income approach and a market

approach to value these two locations.• Within these approaches, the valuation analyst employs the multi-

period discounted earnings method (income approach) and thedirect market data method (market approach). The final valueestimate for each of the XYZ locations is $300,000 for a total valueof $600,000 for the two locations.

Valuation Report• In arriving at this indication of value, the valuation analyst suggests

the following:– There is little to suggest that MJ and DJ will be able to reduce the cost of

sales at each location to 30%, a level that is below that of the other XYZlocations, particularly given that the cost of sales is now in excess of theaverage.

– The growth expectations for the two locations are higher than the currentand historic growth rates of the more established XYZ locations. The 8%growth rate is unlikely to be sustained indefinitely into the future.

– The valuation analyst states no opinion as to the likelihood of the marginalincrease in advertising to increase sales by such a disproportionateamount.

– After a visit to both locations, the valuation analyst does not believe thatthe local traffic is sufficient to support any dramatic increase in sales.

– Further, the analyst does not believe that the locations are conducive tothe business.

– The break-even point for each of the XYZ locations is roughly $1.1 million.

9/12/2009

45

Valuation Report (Contd..)– The ability of the firm to reach this level of sales is possible only under highly

optimistic projections.– In addition, MJ and DJ would likely be forced to make additional capital

contributions to the business in order to maintain operations until they reachbreak-even.

• In light of the comprehensive valuation report, MJ and DJ begin to reassesstheir acquisition of the two XYZ locations.

• ASC is glad that he arranged for the valuation to be conducted.• The bank is also glad to have the insight on the business in order to more fully

assess the loan request.• ABC Holdings is not pleased with the results of the valuation and its role in

killing the deal that would unload these two unprofitable assets that are adrain on the resources of the other XYZ locations. The ABC owners realize,however, that it is the job of the valuation analyst to provide an objectiveopinion of value, not to work toward a particular value that would get the dealdone.

Indications of the Case Study• The value-added nature of business valuations when entrepreneurs are

assessing the acquisition of an existing business.• The prospective owners benefit from the valuation of the firm which

reveals, in this case and in many others, that the companies beingacquired are underperforming assets that warrant a lower valuation thanthe contemplated transaction price.

• The valuation report may also serve as a reality check to the prospectivebuyers by providing an independent assessment regarding the futureearnings potential of the firm and the errors or overreaching in theirassumptions regarding future operations.

• In addition, the bank benefits from not making a loan to the prospectivebuyers whose business venture would likely be doomed from the start.

• Finally, ABC Holdings could also benefit by considering its options for thetwo underperforming locations—close the locations and liquidate thelimited assets, maintain existing operations that drain the other resourcesof the company, or sell the locations to MJ and DJ at a lower price that ismore reflective of fair market value.

9/12/2009

46

Thank You