bvz6a,bpg6c income tax law & practice-ii … · bvz6a,bpg6c –income tax law & practice-ii...

TRANSCRIPT

BVZ6A,BPG6C

INCOME TAX LAW &

PRACTICE-II

Unit : I - V

BVZ6A,BPG6C – Income tax law & practice-II

TM

BVZ6A,BPG6C – Income tax law & practice-II 02I

UNIT-I SYLLABUS

Capital assets

Meaning and kind

Procedure for computing Capital Gains

Cost of Acquisition

Exemption of Capital Gains

Laws under Head Capital Gains.

TM

BVZ6A,BPG6C – Income tax law & practice-II 03

CAPITAL GAINS

As per section 45 any profit or gain arising from transfer of a capital

asset effected in the previous year shall, save as otherwise provided in

specified sections, be chargeable to income-tax under the head

„Capital Gain‟.

• Capital gains attract tax liability only when the following essentials are satisfied:

• CAPITAL ASSET : Assessee should have a capital asset.

.• TRANSFER OF CAPITAL ASSET:

Capital asset held by the assessee.

• TRANSFER DURING THE YEAR :

Transfer of capital asset should have taken place during the

financial year.

PROFITS OR GAINS ON TRANSFER :

Asset transfer should have resulted in gain or profit

https://youtu.be/Lh2eznSn7BM

I

TM

BVZ6A,BPG6C – Income tax law & practice-II 04

EXEMPTION UNDER SPECIFIRED SECTIONS:

Such Capital Gains arising are not exempted under sections

54,54B,54D,54EC,54F,54G and 54GA

Meaning of Capital Assets

„Capital asset‟ is defined to include property of any kind, whether fixed or

circulating, movable or immovable tangible or intangible. Except a few

specified items, all other properties are capital assets.

Ignore repairs, since it is not a capital expenditure

The following assets are excluded from the definition of ‘Capital Assets

https://www.slideshare.net/Deepak1790/income-from-

capital-gain

TM

BVZ6A,BPG6C – Income tax law & practice-II 05

’.EXEMPTED ASSETS:

1.Stock in trade held for business or profession 2. Assets held for personal use3. Rural Agricultural land

4.Gold Bonds issued by the Government

5. Special Bearer Bonds

6. Gold Deposit Bonds.

Short Term Capital Assets:Capital Asset held by an assessee for not more than

36 months/ 3 years immediately preceding the date of transfer is a ‘Short Term

Capital Asset’.

All depreciable assets and fixed assets which are used by the organisation for

official purpose are treated as short term capital assets irrespective of its

holding

List of Short Term Capital Assets: Financial assets, are also short-term

capital assets if they are not held for more than 12 months.

1. Shares held in a company

2. Debentures held in a company

3. Units of Unit Trust of India

TM

06

4. Units of a Mutual fund

5. Any other securities listed in a stock exchange like Government securities

6. Zero coupon bonds

Long Term Capital Asset Capital asset held by an assessee for more than 36 months/ 3

years immediately preceding the date of transfer is a ‘Long Term Capital Gain’.

Determination of period of holding

• Shares and securities purchased through stock exchange

• Share and securities purchased and sold directly

• Shares and securities purchased and sold in several lots

• Transfer of securities by a depository

• Shares held in a company in liquidation

• When an asset is acquired by gift or will

• Shares becoming property in a scheme of Amalgamation

• Shares held in a demerged company

• Period of holding of bonus shares

• Period of holding of rights shares.

BVZ6A,BPG6C – Income tax law & practice-II

TM

BVZ6A,BPG6C – Income tax law & practice-II 07

Determining indexed cost of Acquisition and indexed cost of Improvement

Indexed cost of acquisition:

Indexed cost of acquisition means an amount which bears to be the cost of

acquisition the same proportion as cost inflation index for the year in which,

the assets is transferred bears to the cost inflation index for the first year in which

the asset was held by the assessee of for the year beginning on the 1st day of

April, 1981, whichever is later.

Indexed Cost of Improvement

Indexed Cost of Improvement‟ means an amount which bears to the cost of

improvement the same proportion as cost inflation index for the year in which

the asset is transferred bears to the cost inflation index for the year in which

the improvement to the asset took place.

Any additions or improvement made before 1.04.1981 should be ignored

Cost inflation Index

In relation to a previous year, means such index as the Central Government

having regard to 75% percent of average rise in the consumer price index,

for Urban non-manual employees for the previous year, by notification in the

official Gazette, specify in this behalf.

BVZ6A,BPG6C – Income tax law & practice-II

TM

08

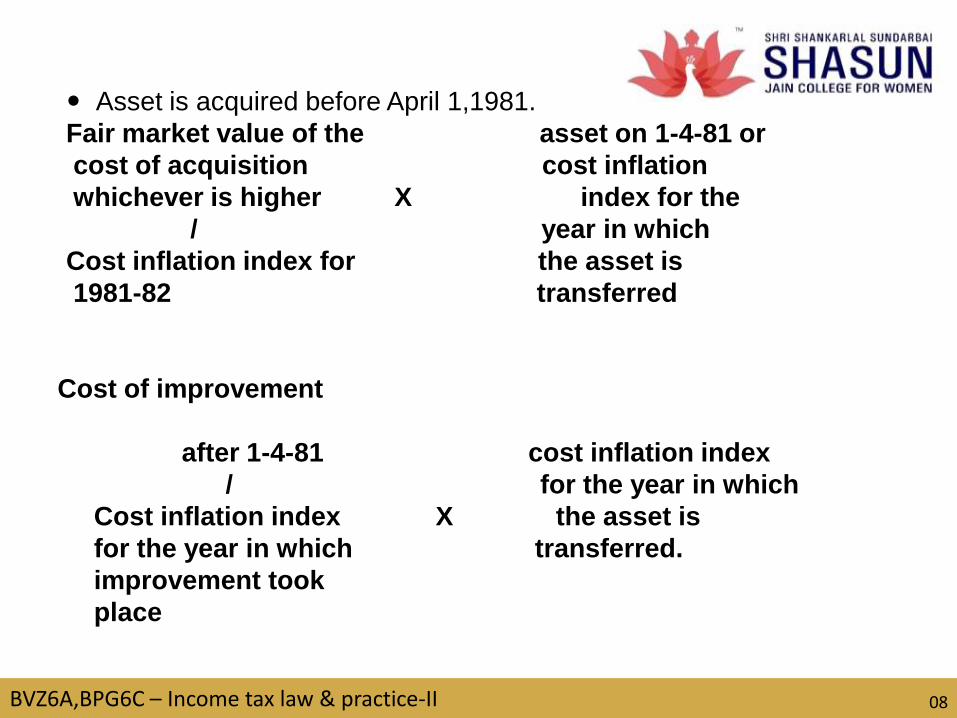

Asset is acquired before April 1,1981.

Fair market value of the asset on 1-4-81 or

cost of acquisition cost inflation

whichever is higher X index for the

/ year in which

Cost inflation index for the asset is

1981-82 transferred

Cost of improvement

after 1-4-81 cost inflation index

/ for the year in which

Cost inflation index X the asset is

for the year in which transferred.

improvement took

place

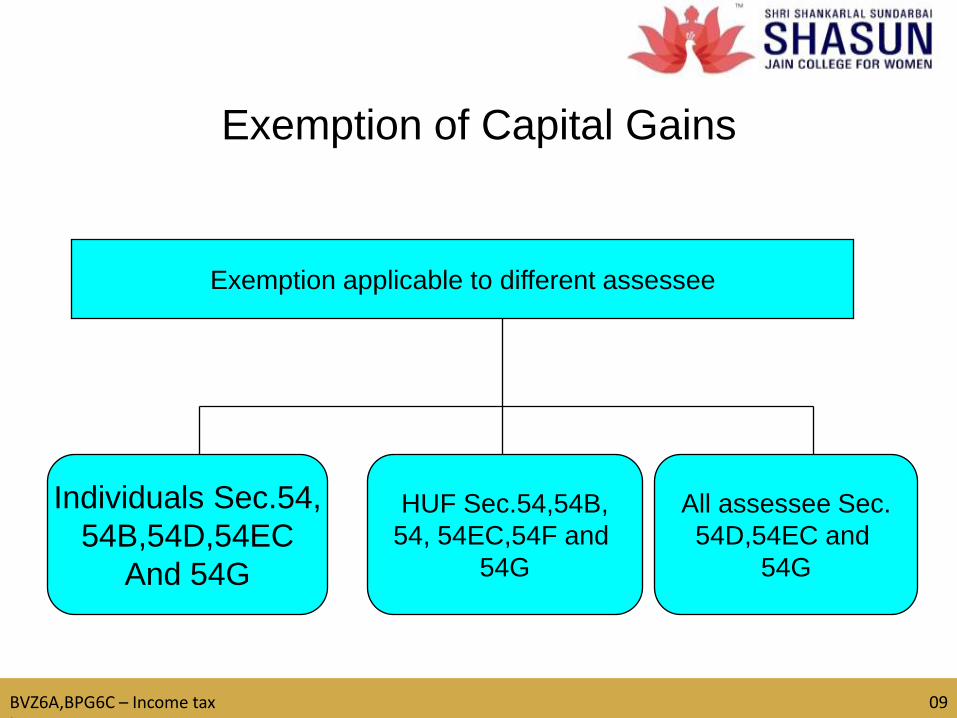

Exemption of Capital Gains

Exemption applicable to different assessee

Individuals Sec.54,

54B,54D,54EC

And 54G

HUF Sec.54,54B,

54, 54EC,54F and

54G

All assessee Sec.

54D,54EC and

54G

BVZ6A,BPG6C – Income tax law & practice-II

09

BVZ6A,BPG6C – Income tax law & practice-II

TM

10

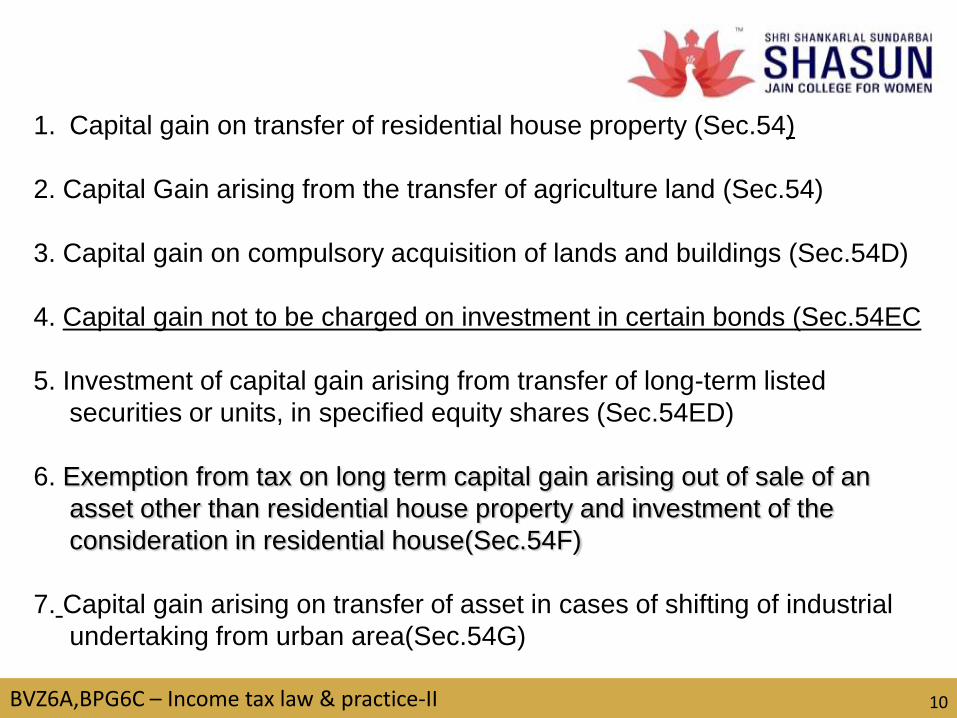

1. Capital gain on transfer of residential house property (Sec.54)

2. Capital Gain arising from the transfer of agriculture land (Sec.54)

3. Capital gain on compulsory acquisition of lands and buildings (Sec.54D)

4. Capital gain not to be charged on investment in certain bonds (Sec.54EC

5. Investment of capital gain arising from transfer of long-term listed

securities or units, in specified equity shares (Sec.54ED)

6. Exemption from tax on long term capital gain arising out of sale of an

asset other than residential house property and investment of the

consideration in residential house(Sec.54F)

7. Capital gain arising on transfer of asset in cases of shifting of industrial

undertaking from urban area(Sec.54G)

BVZ6A,BPG6C – Income tax law & practice-II

TM

11

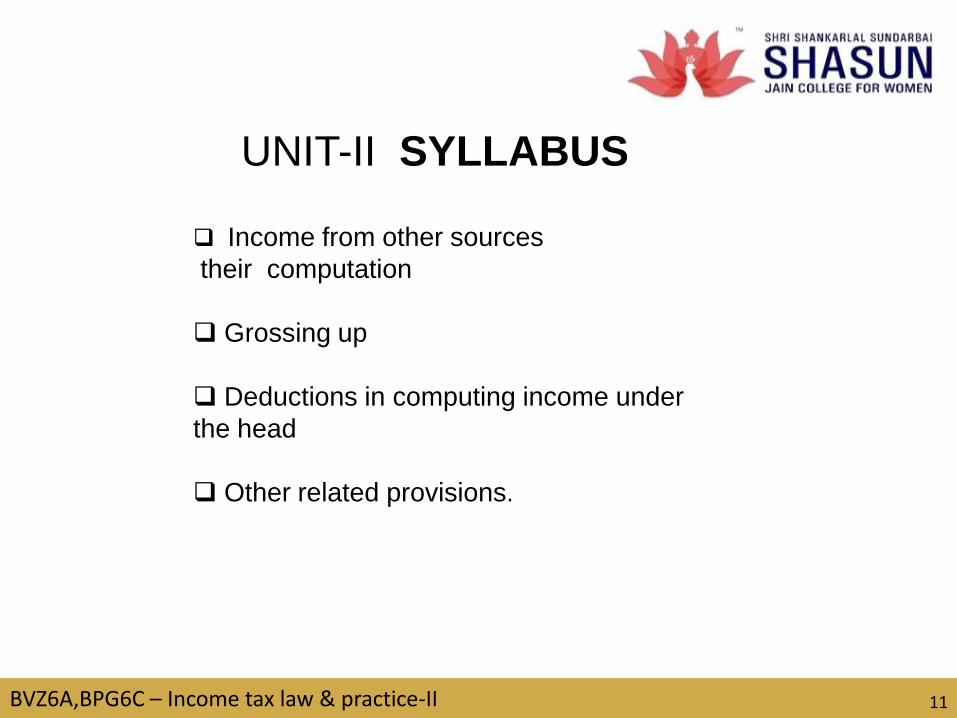

UNIT-II SYLLABUS

Income from other sources

their computation

Grossing up

Deductions in computing income under

the head

Other related provisions.

TM

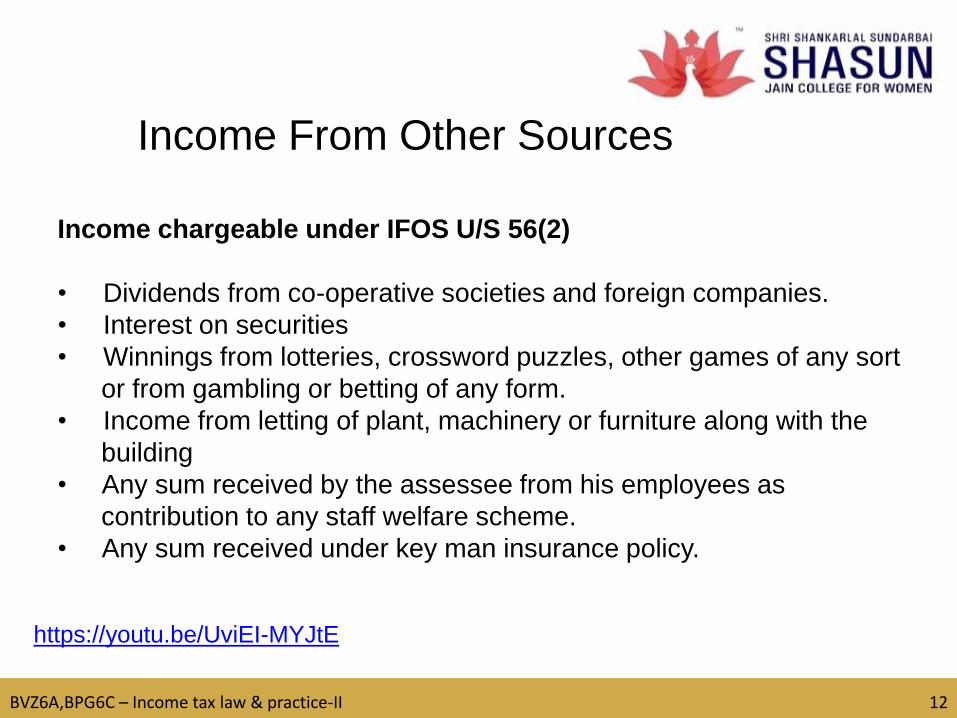

Income chargeable under IFOS U/S 56(2)

• Dividends from co-operative societies and foreign companies.

• Interest on securities

• Winnings from lotteries, crossword puzzles, other games of any sort

or from gambling or betting of any form.

• Income from letting of plant, machinery or furniture along with the

building

• Any sum received by the assessee from his employees as

contribution to any staff welfare scheme.

• Any sum received under key man insurance policy.

Income From Other Sources

https://youtu.be/UviEI-MYJtE

BVZ6A,BPG6C – Income tax law & practice-II 12

TM

BVZ6A,BPG6C – Income tax law & practice-II 13

• Fees or commission received by an employee from a person other

than his

employer

• Annuity paid under the provisions of the Annuity Deposit scheme

• Interest on bank deposits

• Directors fees

• Remuneration for examination work• Rent of land• Agricultural income• Royalty income• Interest on own contribution to URPF.• Remuneration received for writing.• Interest from co-operative society.• Family pension• NSS Deposit withdrawn• Director‟s commission• Gratuity received by a director

https://youtu.be/4fVNHtvkRqc

TM

BVZ6A,BPG6C – Income tax law & practice-II 14

Income by subletting

Income from undisclosed sources.

a) Unexplained cash credits

b) Unexplained Investments

c) Unexplain Receipts by cricketers money

d) Unexplained expenditure

e) Amount borrowed or repaid on Hundi

Kinds of Securities

Government Securities

• These securities are issued by state or central Govt.

• The amount received or due, shall be included in the total income.

• No tax is deducted at source.

Non government securities.

a) Tax free commercial securities are issued by a local authority or

statutory corporation or a company.

These securities are called „tax free‟, because the assessee is not to

pay tax on the interest, since tax is paid by the company on

assessee‟s behalf.

TM

BVZ6A,BPG6C – Income tax law & practice-II 15

b) Less tax commercial securities

Less tax securities are also called “taxable securities”.

Tax is deducted at source from the interest and balance of interest

after deduction of the income tax is paid to the security holder.

Casual Income

• Lottery winnings.

• Winnings from race including horse races.

• Winnings from card games.

• Winnings from crossword puzzles.

• Gambling or betting of any other nature.

• Grossing up: Net winnings * 100/100-30

• Casual incomes are subject to TDS at 30% if the income exceeds

Rs.5,000.

• Race winnings are subject to TDS at 30% if the income exceeds

RS. 2,500.

• No TDS on other race winnings, gambling and betting.

• Family pension received by widows or heirs of deceased

employees.

TM

BVZ6A,BPG6C – Income tax law & practice-II 16

Income from subletting.

Income from sub letting of house property or rent of vacant land is

income from other sources

Gifts

Gifts received from relatives are fully exempted.

Gifts received from unrelated persons are taxable as income from other

sources., Gifts received in kind is exempted

Property purchased for less than stamp duty value is taxable. (stamp

duty value more than consideration

Deduction U/S 57Bank commission on collection of taxable dividends and interest on securities in deductible.Interest on loan to acquire investment whose income is taxable is deductible.Standard deduction @1/3 of family pension or Rs.15,000 which ever is deductible.Depreciation, repairs, fire insurance premium, local taxes relating to letout plant and machinery along with building and furniture.

TM

BVZ6A,BPG6C – Income tax law & practice-II 17

UNIT-III SYLLABUS

Clubbing of Income

Deemed incomes

Provisions of the Act relating to clubbing

of income

Set off & Carry forward

Set off of losses

TM

BVZ6A,BPG6C – Income tax law & practice-II 18

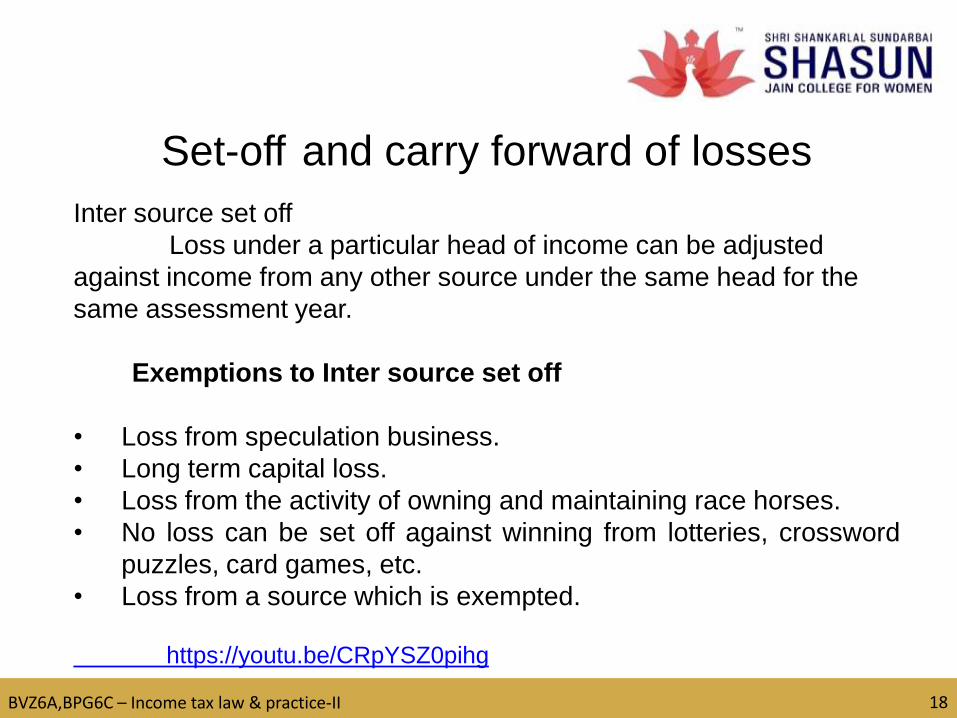

Set-off and carry forward of losses

Inter source set off

Loss under a particular head of income can be adjusted

against income from any other source under the same head for the

same assessment year.

Exemptions to Inter source set off

• Loss from speculation business.

• Long term capital loss.

• Loss from the activity of owning and maintaining race horses.

• No loss can be set off against winning from lotteries, crossword

puzzles, card games, etc.

• Loss from a source which is exempted.

https://youtu.be/CRpYSZ0pihg

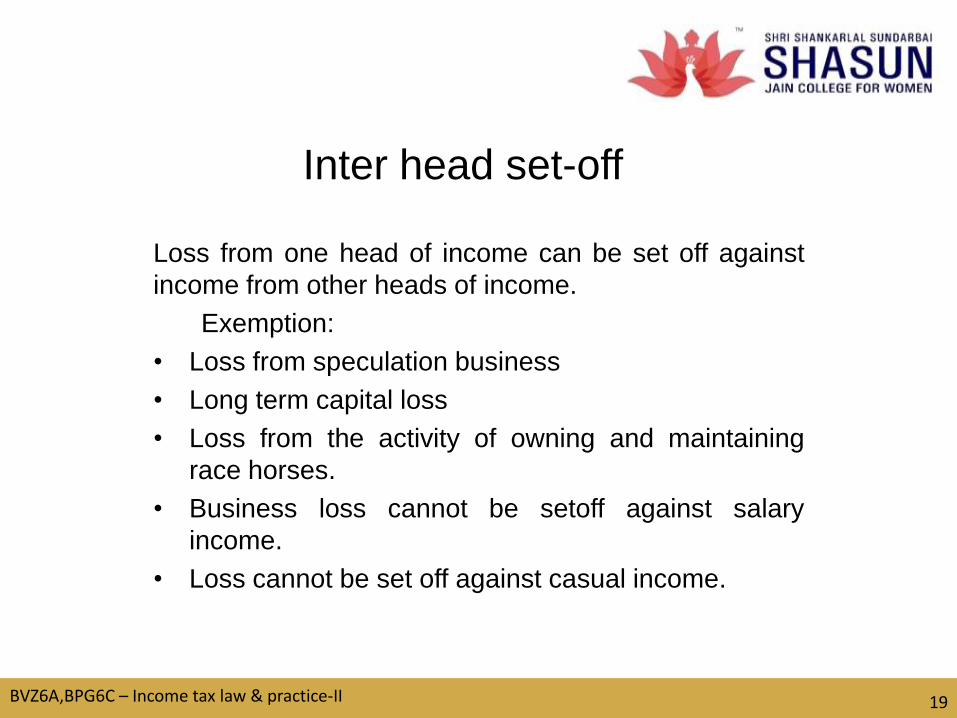

Inter head set-off

Loss from one head of income can be set off against

income from other heads of income.

Exemption:

• Loss from speculation business

• Long term capital loss

• Loss from the activity of owning and maintaining

race horses.

• Business loss cannot be setoff against salary

income.

• Loss cannot be set off against casual income.

BVZ6A,BPG6C – Income tax law & practice-II 19

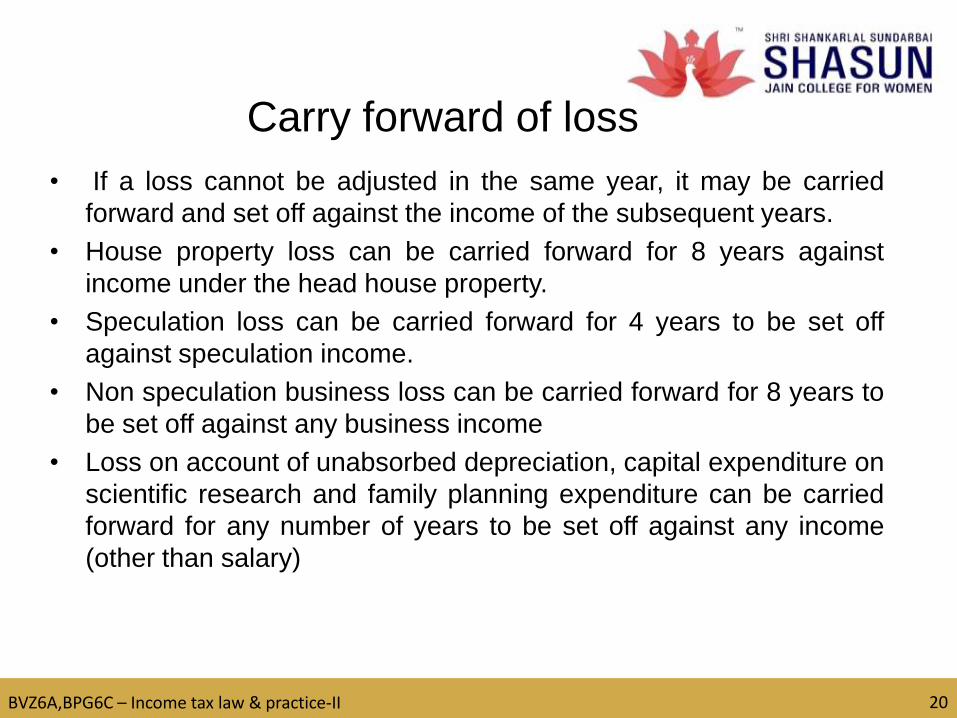

Carry forward of loss

• If a loss cannot be adjusted in the same year, it may be carried

forward and set off against the income of the subsequent years.

• House property loss can be carried forward for 8 years against

income under the head house property.

• Speculation loss can be carried forward for 4 years to be set off

against speculation income.

• Non speculation business loss can be carried forward for 8 years to

be set off against any business income

• Loss on account of unabsorbed depreciation, capital expenditure on

scientific research and family planning expenditure can be carried

forward for any number of years to be set off against any income

(other than salary)

BVZ6A,BPG6C – Income tax law & practice-II 20

Clubbing of income

Income of other persons to be included in

an assessee‟s total income. (Sec 60) • Transfer of income without transfer of an asset.

Such income is clubbed in the hands of the transferor

• Revocable transfer of assets by an assessee to another person.

It is clubbed in the hands of transferor.

• Irrevocable transfer of assets.

Income arises out of such transfer is taxable in the hands of

transferee.

BVZ6A,BPG6C – Income tax law & practice-II 21

Income of an individual to include spouse

income

• Remuneration of spouse:-

• Substantial interest is required.

• Husband and wife relationship should exist.

• Remuneration should be received in same concern.

• Remuneration should not be received out of professional

qualification.

BVZ6A,BPG6C – Income tax law & practice-II 22

Income from asset transferred to spouse• Direct or indirect transfer

• Transfer made without adequate consideration.

• Relationship of Husband and wife.

• Change in the identity of asset- taxable in the hands oftransferor.

• Sale or transfer of transferred asset- capital gain is taxablein the hands of transferor.

• Transferred Asset being invested in a business.

• Transferred asset being invested in a firm

• Acquisition of asset out of pin money – Taxable in the handsof transferee.

• Transfer of asset in connection with an agreement to liveapart – not taxable in the hands of transferor.

• Income arising to the spouse from the accretion totransferred asset cannot be clubbed with transferor.

BVZ6A,BPG6C – Income tax law & practice-II 23

Income of minor not to be clubbed

• Handicapped or disabled minor‟s income.

• Income earned by a minor out of any manual work.

• Income earned out of his skill, talent, or specialized knowledge

and experience.

• Exemption granted to parent u/s 10(32)

• Rs. 1500 is exempted in the hands of parent of each minor child

income.

Income of Minor child

• Income of a minor child shall be clubbed in the hands of parents.

• Minor‟s income should include with the income of parent whose

total income is greater.

BVZ6A,BPG6C – Income tax law & practice-II 24

Conversion of self acquired property into

Joint family property

• If a member of HUF transfers self acquired property to HUF

without adequate consideration. Income arising out of

transferred asset is clubbed in the hands of transferor.

Deemed Incomes

• Cash credits

• Unexplained investments.

• Unexplained money.

• Amount of investment not fully disclosed.

• Unexplained expenditure.

• Amount borrowed or repaid on Hundi

BVZ6A,BPG6C – Income tax law & practice-II 25

UNIT -IV SYLLABUS

Permissible deductions from gross total income

Sec. 80C,80CCC, 80CCCD, 80DD, 80DDB, 80E,

80G,80GG,80GGA, 80QQB, 80RRB, 80U

Assessment of Individual (Covering Capital gains, Income from

other sources including the above mentioned deductions –

Computation of Tax).

BVZ6A,BPG6C – Income tax law & practice-II 26

DEDUCTIONS

Deduction in respect of rent paid

[Sec 80 GG]• Allowed to Individuals:

Deduction in respect of rent paid is allowed to an individual

assessee who does not have any income by way of house rent allowance,

but who incurs expenditure by way of rent in respect of residential

accommodation occupied by him.

• Amount of deduction :

The amount of deduction is least of the following

(i) 25% of Adjusted Total Income

(ii) Excess of rent paid over 10 % of „Adjusted Total Income‟.

(iii) Rs. 2,000 per month.

• Conditions:

The assessee, his or her spouse or minor child or a HUF of which he/she is

a member, does not own any residential accommodation at the palace where

he ordinarily resides or performs duties of his office or employment or carries

on his business or professionBVZ6A,BPG6C – Income tax law & practice-II 27

Deduction in respect of income of Authors

(u/s 80QQB)• Allowed to individual being an author or joint author in literary,

artistic or scientific nature. Whose gross total income includes

royalty income. The amount of deduction is Rs. 3,00,000 or royalty

income whichever is less.

• Deduction in respect of royalty on patents (u/s 80 RRB)

The tax payer is an individual being a patentee or owner of patent

and in receipt of income being royalty, the amount of deduction is

Rs 3,00,000 or royalty income whichever is less.

BVZ6A,BPG6C – Income tax law & practice-II 28

Deduction in the case of physically

handicapped resident person[Sec 80U]

• A resident Individual who is totally blind or suffers from

permanent physical disability is entitled to a deduction of Rs

50,000 under Section 80U. A higher deduction of Rs.

1,00,000 with severe disability(having any disability over

80%) is allowed.

Person eligible for deduction:

• Deduction under Section 80U is available in the case of

resident Individual who is suffering from a permanent

physical disability, blindness, or subject to mental

retardation, specified in the rules made in this behalf by the

Board.

BVZ6A,BPG6C – Income tax law & practice-II 29

DEDUCTIONS UNDER SECTION 80C

PROVISIONS SPECIFIED UNDER SECTION 80C:

• Deductions under section 80C is allowed from the

gross total income.

• Deduction under section 80C is allowed to an

individual or a hindu undivided family.

• It is allowed on the basis of specified qualifying

investments/ deposits/ contribution/ payments made

by the assessee during the previous year.

• The maximum amount deductible under sections

80C, 80CCC and 80CCD cannot exceed Rs 1 lakh

as per section 80CCE.

BVZ6A,BPG6C – Income tax law & practice-II 30

COMPUTATION OF DEDUCTION

UNDER SECTION 80C• Computation of gross qualifying amount.

• Computation of net qualifying amount.

• Amount of deduction.

• Life insurance premium

• Non commutable deferred annuity

• Amount deducted for securing a deferred annuity

• Contribution to provident fund

• Contribution to public provident fund

• Contribution to an approved superannuation fund

• Subscription to national savings certificates

• Contribution made by an individual to the unit linked plan of UTI

• Contribution to unit linked insurance plan of the LIC mutual fund

• Payment made to effect annuity plan of LIC

BVZ6A,BPG6C – Income tax law & practice-II 31

COMPUTATION OF GROSS

QUALIFYING AMOUNT• Subscription to units of UTI or notified mutual fund

• Contribution to pension fund set up by a notified mutual fundor by UTI

• Subscription to home loan account scheme

• Subscription to any schemes

• Repayment of housing loan

• Any amount paid as tuition fee

• Investment in debentures and equity shares

• Term deposits with a bank

• Subscription to any notified bonds of NABARD

• Deposit made in 5 years time deposit scheme in post office

• Deposit made in senior citizens savings schemes rules 2004.

BVZ6A,BPG6C – Income tax law & practice-II 32

Deductions in respect of contribution to

certain pension funds- section 80CCC

• Allowed to individual assessee.

• The tax payer has paid a sum under an annuity plan of the LIC of

India or any other insurer for receiving pension.

• Amount of deduction is the least of the amount deposited or Rs.

100000.

• If the assessee receives any amount standing to the credit of theassessee in respect of which deduction under section 80ccc hasbeen allowed such amount shall be included in the total income of theassessee or his nominee in the year of receipt.

• The aggregate deduction under section 80ccc cannot exceed Rs100000.

BVZ6A,BPG6C – Income tax law & practice-II 33

Deduction in respect of contribution to

pension scheme of central government or

any other employer – section 80CCD

• The assessee is an individual.

• This deduction is applicable to central government or any other

employer.

• The assessee in the previous year paid or deposited any amount

in his amount under pension scheme notified by the central

government.

BVZ6A,BPG6C – Income tax law & practice-II 34

Deduction in respect of contribution to

pension scheme of central government or

any other employer – section 80CCD

• Employees contribution = 10%

• Contribution by the central government or any other employer

= 10%

• Self employed individual=upto 10% of his gross total income

in the previous year.

• The amount received from pension scheme along with

accretions will be taxed in the year of receipt by the

employee.

• The aggregate deduction under section 80ccd cannot exceed

Rs. 100000.

BVZ6A,BPG6C – Income tax law & practice-II 35

Deduction in respect of subscription to

long term infrastructure bonds – section

80CCF• Subscription during the year 2010-11 made to long term

infrastructure bonds to the extent of Rs. 20000 is allowed gross

total income of an individual or a HUF.

• Deduction under section 80CCF is in addition to Rs. 100000 under

section 80C, 80CCC and 80CCD.

Section 80 D

• Amount paid to GIC or Other insurer for health insurance or

mediclaim.

• Quantum of deduction:

• Actual amount paid or Rs 15,000 (W.E.L)

• In case of Senior citizen

• Actual amount paid or Rs. 20,000 (W.E.L)

Additional deduction on mediclaim taken on parentsBVZ6A,BPG6C – Income tax law & practice-II 36

Section 80DD

• Maintenance or treatment of Handicapped dependent .

Deposit with LIC or UTI for the benefit of Mentally retarded or

physically handicapped dependent.

• Quantum of deduction

• Rs.50,000

• In case of severe disability Rs.1,00,000

Section 80 DDB

• Amount incurred on treatment of notified disease of self or

dependent family members.

• Quantum of deduction

Actual amount paid or Rs. 40,000 (WEL)

In case of senior citizen : Actual amount or Rs. 60,000. (WEL)

BVZ6A,BPG6C – Income tax law & practice-II 37

SEC 80E - Deductions in respect of

interest on loan taken for higher education• Deduction under Section 80E is allowed to an individual assessee

who actually pays in the previous year any amount by way of interest

on loan taken from a Financial institution or from approved charitable

institution for the purpose of his higher education or for the purpose of

any education of spouse/any child the student for whom the individual

is the legal guardian.

• AMOUNT OF DEDUCTION:

Amount paid during the year towards interest.

• PERIOD OF DEDUCTION:

The deduction will be allowed for a

maximum of eight years , beginning from the year in which the

individual starts repaying the loan or interest or until the loan and

interest have been paid full whichever is earlier

BVZ6A,BPG6C – Income tax law & practice-II 38

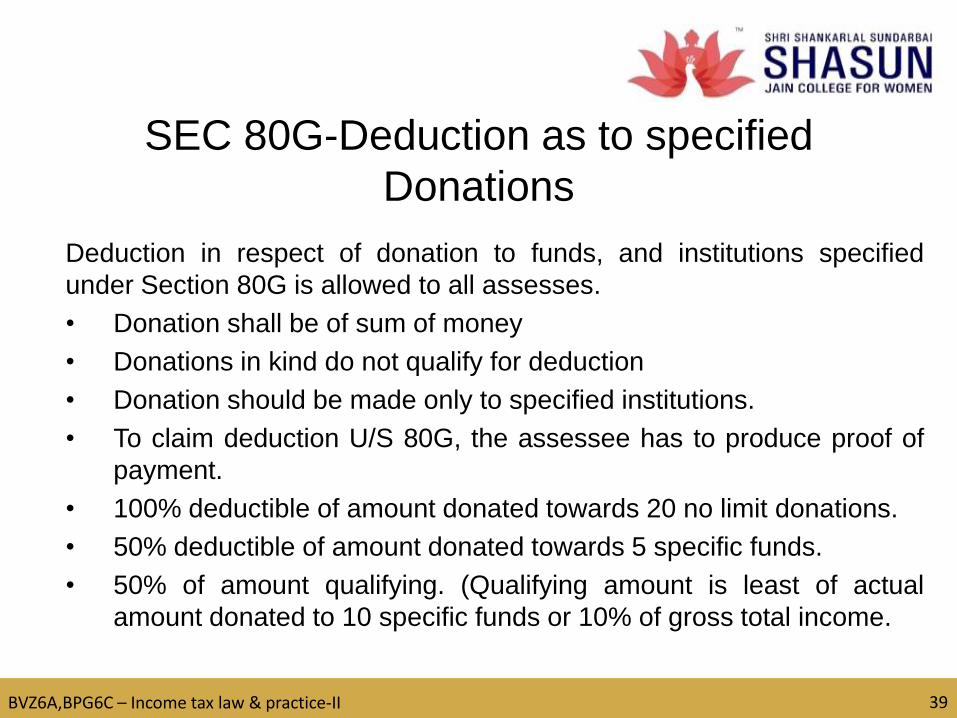

SEC 80G-Deduction as to specified

Donations

Deduction in respect of donation to funds, and institutions specified

under Section 80G is allowed to all assesses.

• Donation shall be of sum of money

• Donations in kind do not qualify for deduction

• Donation should be made only to specified institutions.

• To claim deduction U/S 80G, the assessee has to produce proof of

payment.

• 100% deductible of amount donated towards 20 no limit donations.

• 50% deductible of amount donated towards 5 specific funds.

• 50% of amount qualifying. (Qualifying amount is least of actual

amount donated to 10 specific funds or 10% of gross total income.

BVZ6A,BPG6C – Income tax law & practice-II 39

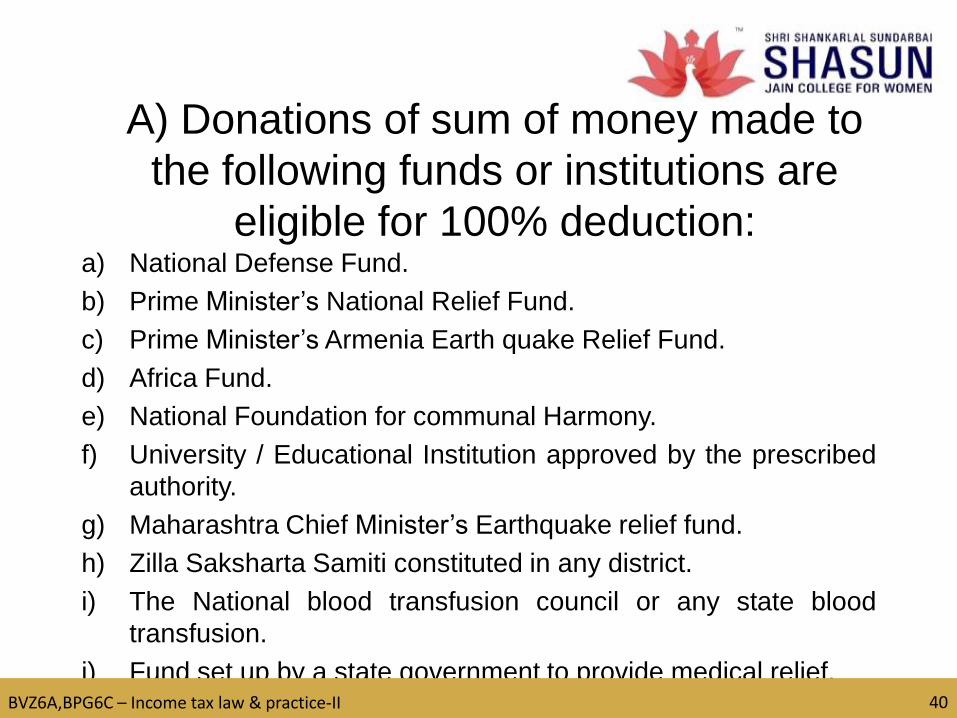

A) Donations of sum of money made to

the following funds or institutions are

eligible for 100% deduction:a) National Defense Fund.

b) Prime Minister‟s National Relief Fund.

c) Prime Minister‟s Armenia Earth quake Relief Fund.

d) Africa Fund.

e) National Foundation for communal Harmony.

f) University / Educational Institution approved by the prescribed

authority.

g) Maharashtra Chief Minister‟s Earthquake relief fund.

h) Zilla Saksharta Samiti constituted in any district.

i) The National blood transfusion council or any state blood

transfusion.

j) Fund set up by a state government to provide medical relief.BVZ6A,BPG6C – Income tax law & practice-II 40

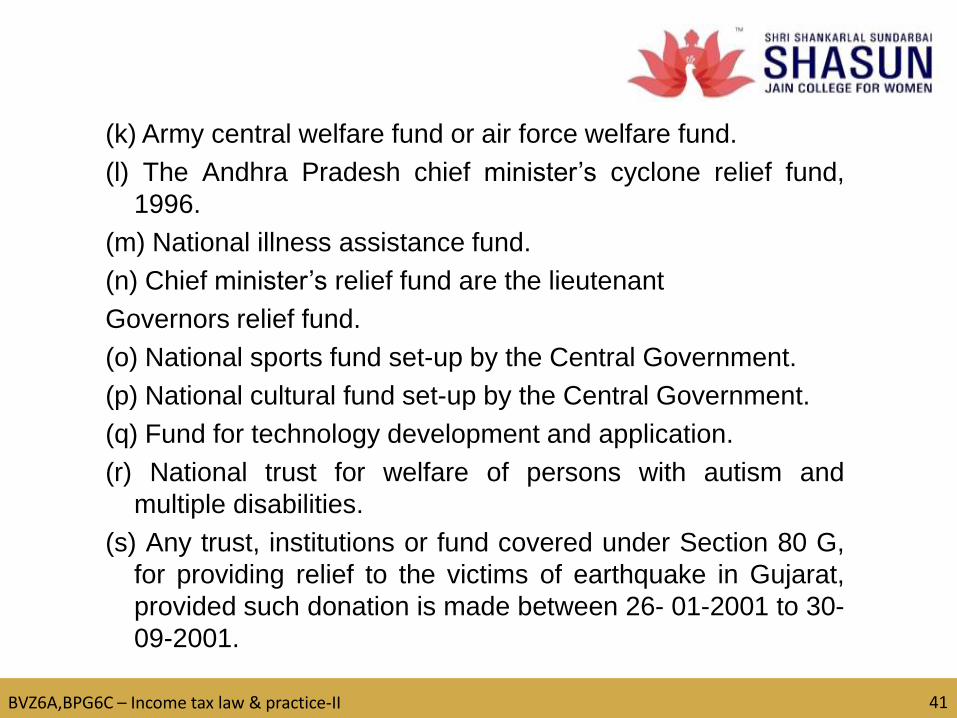

(k) Army central welfare fund or air force welfare fund.

(l) The Andhra Pradesh chief minister‟s cyclone relief fund,

1996.

(m) National illness assistance fund.

(n) Chief minister‟s relief fund are the lieutenant

Governors relief fund.

(o) National sports fund set-up by the Central Government.

(p) National cultural fund set-up by the Central Government.

(q) Fund for technology development and application.

(r) National trust for welfare of persons with autism and

multiple disabilities.

(s) Any trust, institutions or fund covered under Section 80 G,

for providing relief to the victims of earthquake in Gujarat,

provided such donation is made between 26- 01-2001 to 30-

09-2001.

BVZ6A,BPG6C – Income tax law & practice-II 41

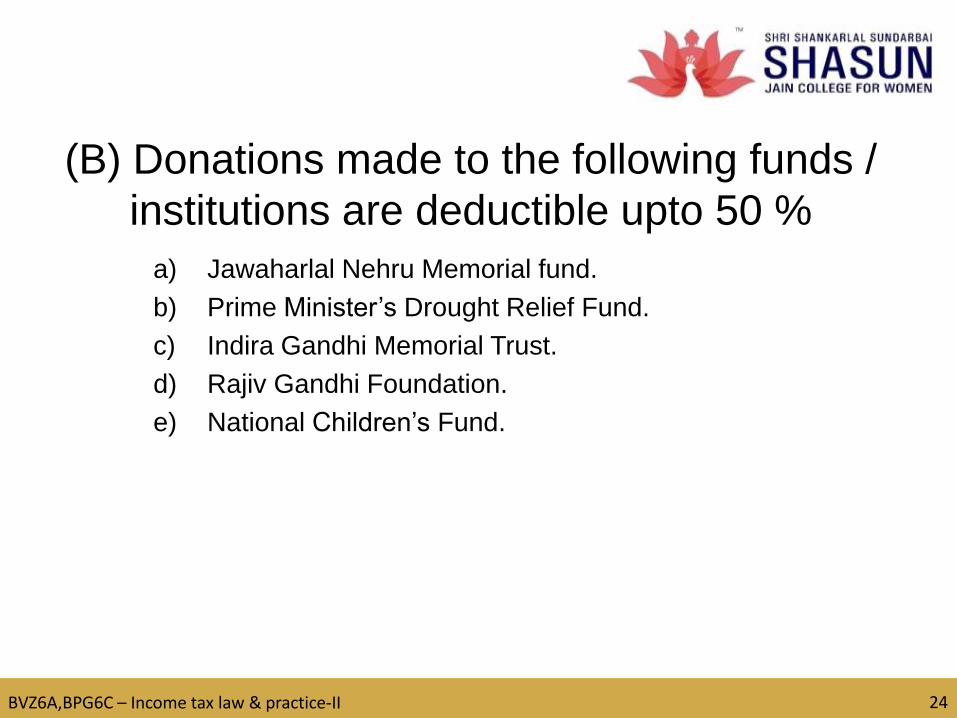

(B) Donations made to the following funds /

institutions are deductible upto 50 %

a) Jawaharlal Nehru Memorial fund.

b) Prime Minister‟s Drought Relief Fund.

c) Indira Gandhi Memorial Trust.

d) Rajiv Gandhi Foundation.

e) National Children‟s Fund.

BVZ6A,BPG6C – Income tax law & practice-II 24

(C) Restricted Donations

Donations to the following institutions or funds are restricted to

actual amount or 10 % of gross total income.

a) Approved charitable institutions.

b) Donation to government or any approved authority.

c) Any authority referred for satisfying the need for housing

accommodation or for the purpose of planning development or

improvement of cities.

d) Notified Temple, Mosque, Church, Gurudwara or other place notified

by the Central Government to be of historic or repair of such place.

e) Government or any approved local authority institution or association

to be utilized for the purpose of promoting family planning.

f) Indian Olympic association or to an institute notified under section 16

(23 G) for the development of infrastructure for sports and games in

India.

BVZ6A,BPG6C – Income tax law & practice-II 43

A. In the case of Category „C‟ qualifying amount is

B. restricted to the least of the following :

C. Actual amount donated

(OR)

A. b) 10% of Gross Total income (GTI-LTCG and

STCG on sale of listed shares – share from AOP –

deduction u/s 80C to 80U (but not Section 80G)

B. Amount deductible is 50% of qualifying amount but

in the case of amount paid for promotion of

planning and Indian Olympic Association full

amount is deductible.

BVZ6A,BPG6C – Income tax law & practice-II 44

Unit : V SYLLABUS

BVZ6A,BPG6C – Income tax law & practice-II 45

Income Tax Authorities

Powers of the central Board of Direct Taxes

(CBDT),

Commissioners of Income Tax and Income Tax

officers

Assessment Procedures

Self Assessment

Best Judgment Assessment

Income Escaping Assessment (Re assessment)

Advance payment of Tax

Meaning and Due dates

Deduction of Tax at source

Meaning.

BVZ6A,BPG6C – Income tax law & practice-II 46

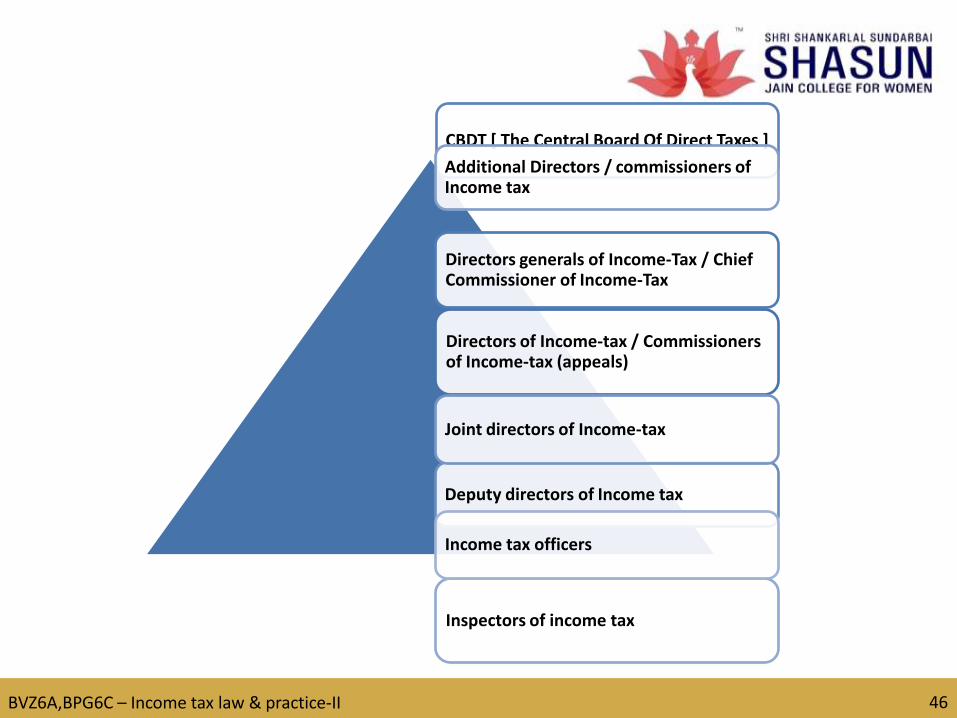

Directors of Income-tax / Commissioners of Income-tax (appeals)

Directors generals of Income-Tax / Chief Commissioner of Income-Tax

CBDT [ The Central Board Of Direct Taxes ]

Deputy directors of Income tax

Joint directors of Income-tax

Additional Directors / commissioners of Income tax

Inspectors of income tax

Income tax officers

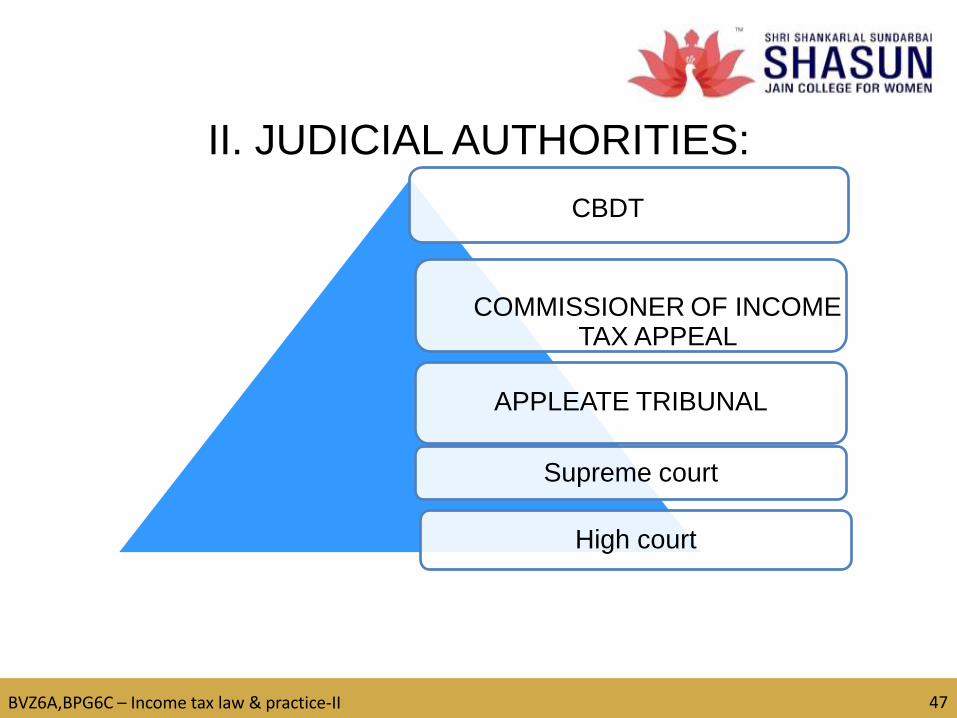

II. JUDICIAL AUTHORITIES:

BVZ6A,BPG6C – Income tax law & practice-II 47

APPLEATE TRIBUNAL

CBDT

COMMISSIONER OF INCOME TAX APPEAL

Supreme court

High court

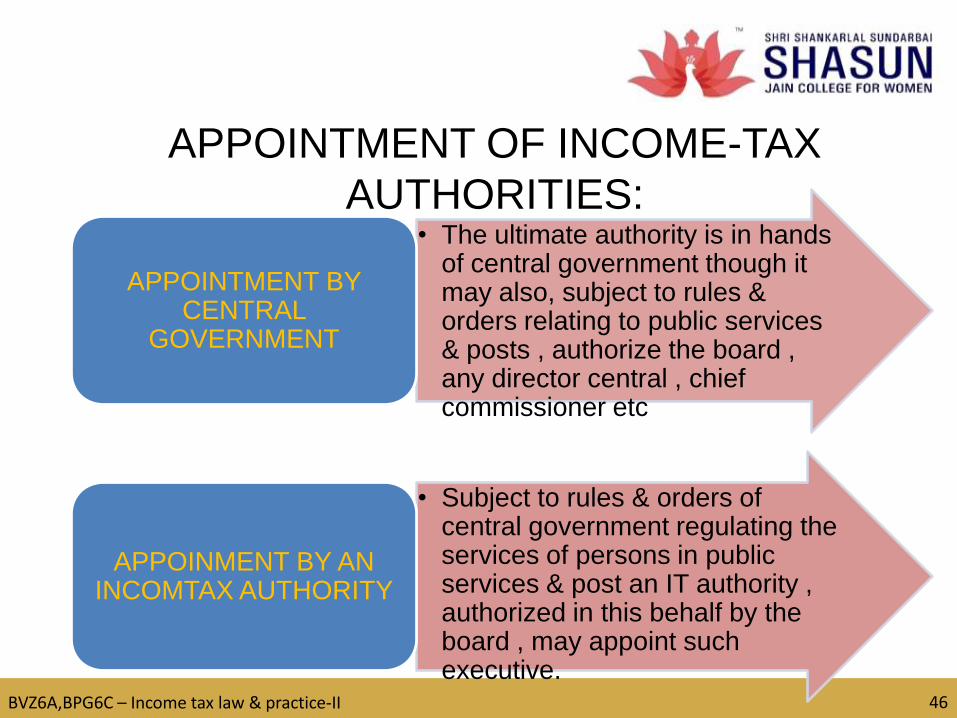

APPOINTMENT OF INCOME-TAX

AUTHORITIES:

BVZ6A,BPG6C – Income tax law & practice-II 46

• The ultimate authority is in hands of central government though it may also, subject to rules & orders relating to public services & posts , authorize the board , any director central , chief commissioner etc

APPOINTMENT BY CENTRAL

GOVERNMENT

• Subject to rules & orders of central government regulating the services of persons in public services & post an IT authority , authorized in this behalf by the board , may appoint such executive.

APPOINMENT BY AN INCOMTAX AUTHORITY

CENTRAL BOARD OF DIRECT

TAXES:

The CBDT is the highest executive authority powers

of ADMINISTRATION, SUPERVISION & CONTROL

extend over the whole IT department.

https://youtu.be/zRMNTg0HpKY

POWERS OF CBDT

BVZ6A,BPG6C – Income tax law & practice-II 49

BVZ6A,BPG6C – Income tax law & practice-II 50

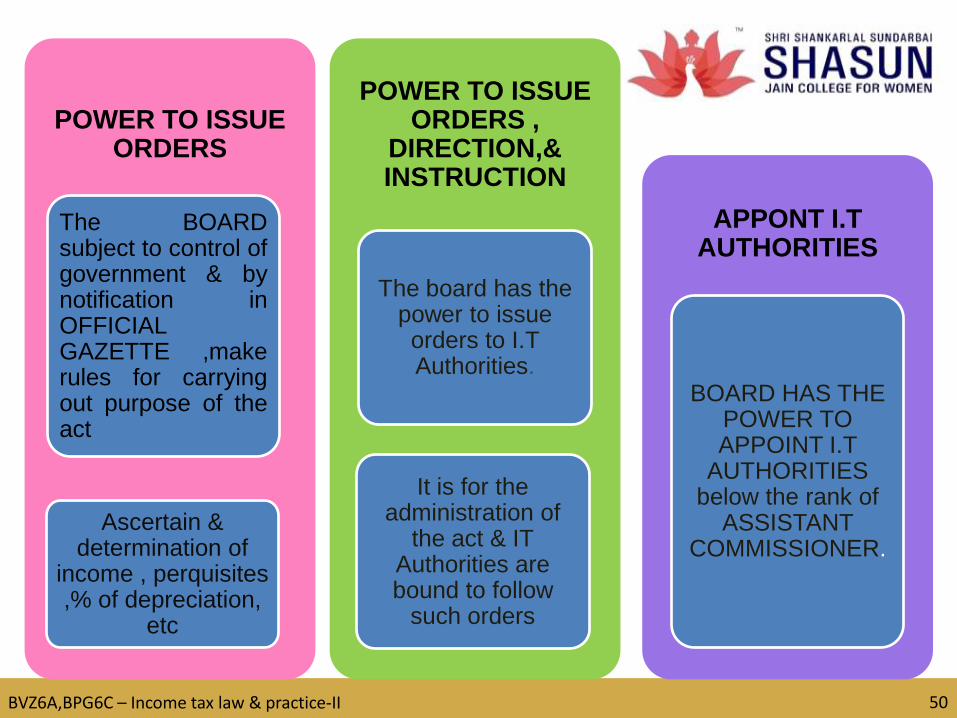

POWER TO ISSUE ORDERS

The BOARDsubject to control ofgovernment & bynotification inOFFICIALGAZETTE ,makerules for carryingout purpose of theact

Ascertain & determination of

income , perquisites ,% of depreciation,

etc

POWER TO ISSUE ORDERS ,

DIRECTION,& INSTRUCTION

The board has the power to issue orders to I.T Authorities.

It is for the administration of

the act & IT Authorities are bound to follow

such orders

APPONT I.T AUTHORITIES

BOARD HAS THE POWER TO APPOINT I.T

AUTHORITIES below the rank of

ASSISTANT COMMISSIONER.

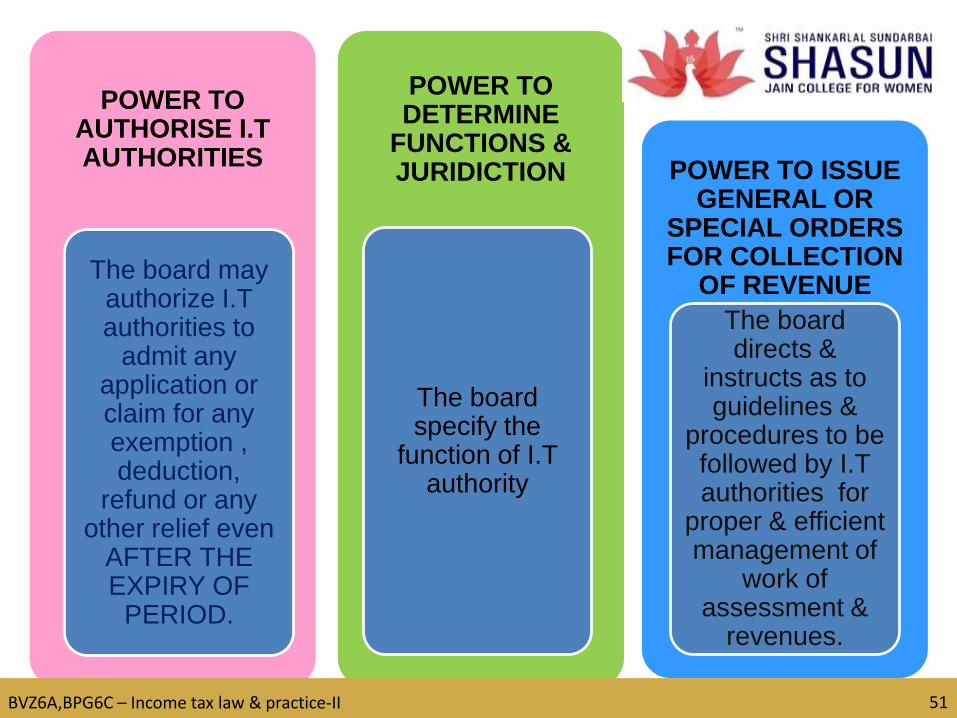

POWER TO AUTHORISE I.T AUTHORITIES

The board may authorize I.T authorities to

admit any application or claim for any exemption , deduction,

refund or any other relief even

AFTER THE EXPIRY OF

PERIOD.

POWER TO DETERMINE

FUNCTIONS & JURIDICTION

The board specify the

function of I.T authority

POWER TO ISSUE GENERAL OR

SPECIAL ORDERS FOR COLLECTION

OF REVENUE

The board directs &

instructs as to guidelines &

procedures to be followed by I.T authorities for

proper & efficient management of

work of assessment &

revenues.

BVZ6A,BPG6C – Income tax law & practice-II 51

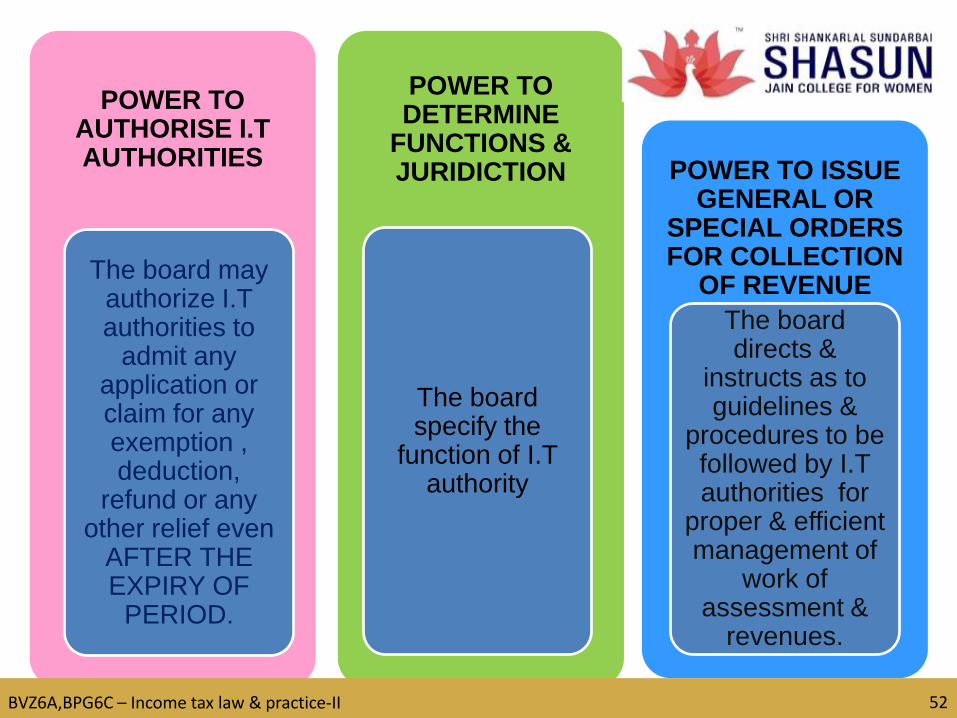

POWER TO AUTHORISE I.T AUTHORITIES

The board may authorize I.T authorities to

admit any application or claim for any exemption , deduction,

refund or any other relief even

AFTER THE EXPIRY OF

PERIOD.

POWER TO DETERMINE

FUNCTIONS & JURIDICTION

The board specify the

function of I.T authority

POWER TO ISSUE GENERAL OR

SPECIAL ORDERS FOR COLLECTION

OF REVENUE

The board directs &

instructs as to guidelines &

procedures to be followed by I.T authorities for

proper & efficient management of

work of assessment &

revenues.

BVZ6A,BPG6C – Income tax law & practice-II 52

Sub Code - Sub Name 53

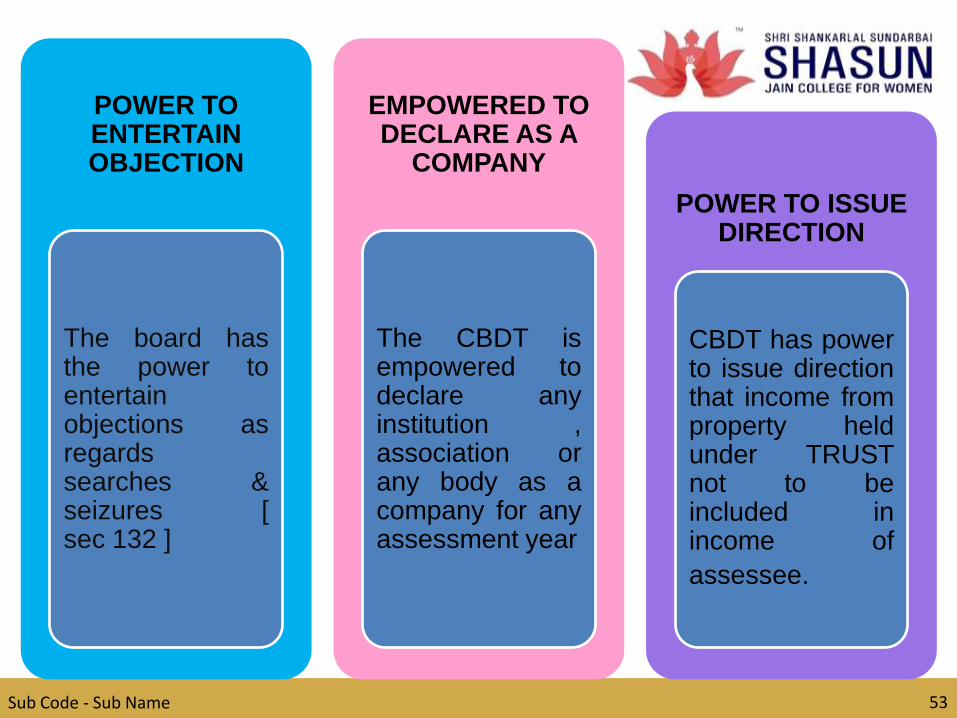

POWER TO ENTERTAIN OBJECTION

The board hasthe power toentertainobjections asregardssearches &seizures [sec 132 ]

EMPOWERED TO DECLARE AS A

COMPANY

The CBDT isempowered todeclare anyinstitution ,association orany body as acompany for anyassessment year

POWER TO ISSUE DIRECTION

CBDT has powerto issue directionthat income fromproperty heldunder TRUSTnot to beincluded inincome of

assessee.

BVZ6A,BPG6C – Income tax law & practice-II 54

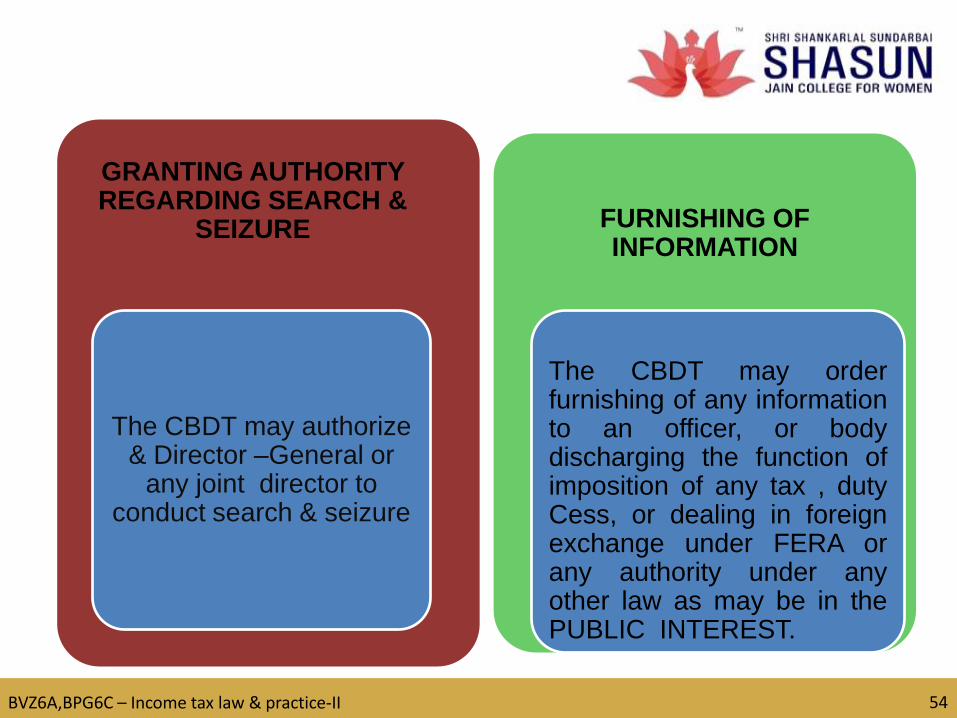

GRANTING AUTHORITY REGARDING SEARCH &

SEIZURE

The CBDT may authorize & Director –General or

any joint director to conduct search & seizure

FURNISHING OF INFORMATION

The CBDT may orderfurnishing of any informationto an officer, or bodydischarging the function ofimposition of any tax , dutyCess, or dealing in foreignexchange under FERA orany authority under anyother law as may be in thePUBLIC INTEREST.

BVZ6A,BPG6C – Income tax law & practice-II 55

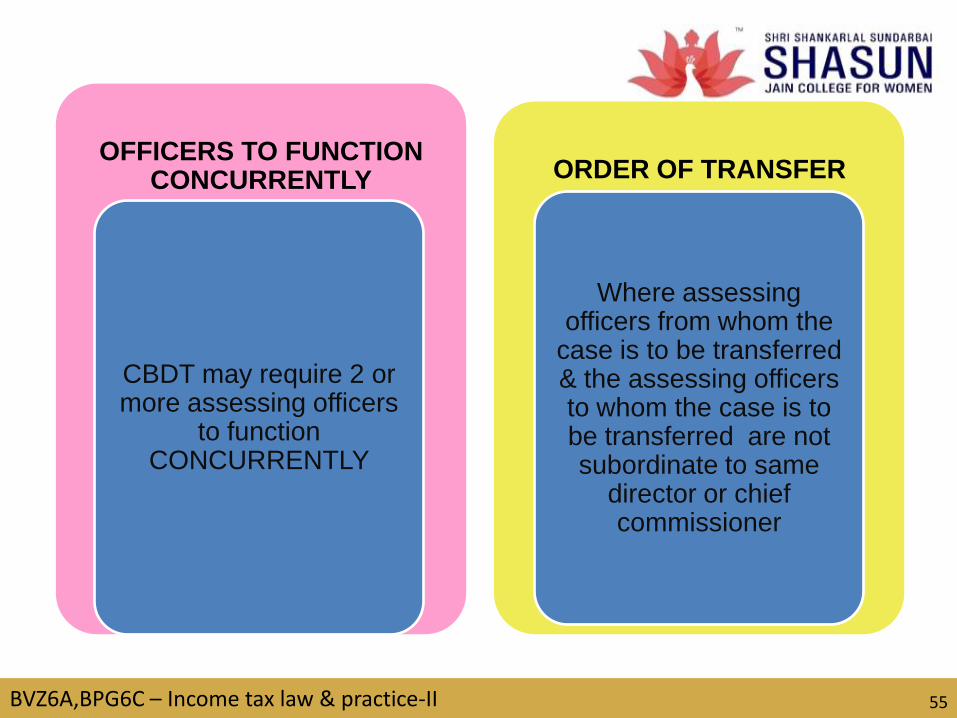

OFFICERS TO FUNCTION CONCURRENTLY

CBDT may require 2 or more assessing officers

to function CONCURRENTLY

ORDER OF TRANSFER

Where assessing officers from whom the

case is to be transferred & the assessing officers to whom the case is to be transferred are not subordinate to same

director or chief commissioner

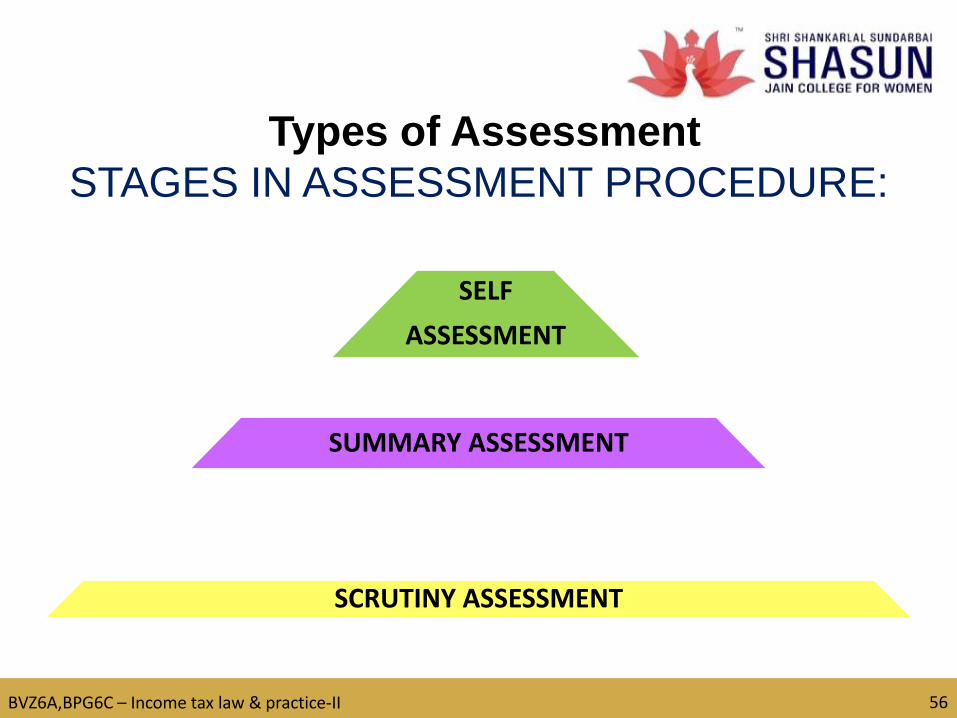

Types of Assessment

STAGES IN ASSESSMENT PROCEDURE:

BVZ6A,BPG6C – Income tax law & practice-II 56

SELF

ASSESSMENT

SUMMARY ASSESSMENT

SCRUTINY ASSESSMENT

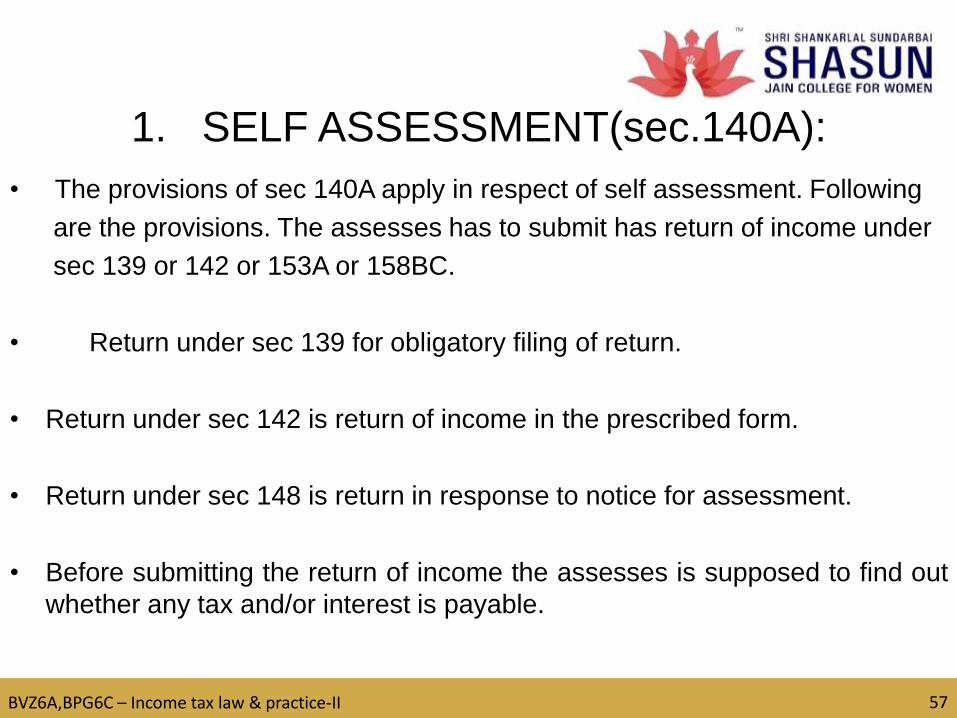

1. SELF ASSESSMENT(sec.140A):

• The provisions of sec 140A apply in respect of self assessment. Following

are the provisions. The assesses has to submit has return of income under

sec 139 or 142 or 153A or 158BC.

• Return under sec 139 for obligatory filing of return.

• Return under sec 142 is return of income in the prescribed form.

• Return under sec 148 is return in response to notice for assessment.

• Before submitting the return of income the assesses is supposed to find out

whether any tax and/or interest is payable.

BVZ6A,BPG6C – Income tax law & practice-II 57

BVZ6A,BPG6C – Income tax law & practice-IIv 58

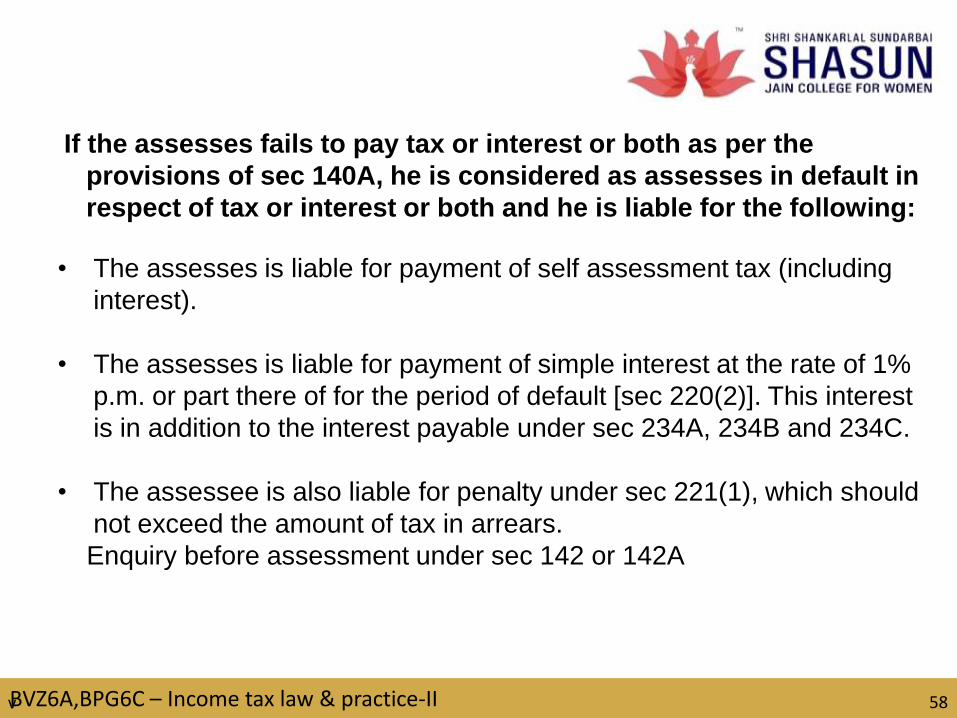

If the assesses fails to pay tax or interest or both as per the

provisions of sec 140A, he is considered as assesses in default in

respect of tax or interest or both and he is liable for the following:

• The assesses is liable for payment of self assessment tax (including

interest).

• The assesses is liable for payment of simple interest at the rate of 1%

p.m. or part there of for the period of default [sec 220(2)]. This interest

is in addition to the interest payable under sec 234A, 234B and 234C.

• The assessee is also liable for penalty under sec 221(1), which should

not exceed the amount of tax in arrears.

Enquiry before assessment under sec 142 or 142A

Provisions of sec 142 and 142A deals

with the following:

1. Giving notice to the assesses sec. 142(1):

• Return of income

• Documents and accounts

• Furnishing information

2. Conducting enquiry sec.142(2):

In order to obtain information in respect of income or loss of

any person the assessing officer may conduct such enquiry

as he considers necessary.

3. Special audit [sec. 142(2A) to 2D]:

The assessing officer may direct the assesses to get his

accounts audited by an accountant nominated by the chief

commissioner.

BVZ6A,BPG6C – Income tax law & practice-II 59

The following are the conditions to be

satisfied for direction of an audit:

• Directions for special audit can be given at any stage before the

completion of assessment.

• Direction for audit can be issued only if having regard to the nature

and complexity of the accounts of the assessee, the assessing

officer is of the opinion that it is necessary to conduct an audit.

• From A.Y. 1989-90 new procedure of regular assessment has

been prescribed.

• An assessing officer can accept the return filed by the assesses as

such and complete assessment accordingly.

In such case, he shall issue an intimation in the following

manner.

I. Intimation of demand.

II. Intimation of refund.

BVZ6A,BPG6C – Income tax law & practice-II 60

Exception:

In case there is no demand from or refund to the

assesses is due than there is no need to issue an

intimation. The acknowledgment copy of the return

of income filed by the assesses is itself demand to

be an intimation.

Time limit for intimation under sec 143(1)(1):

The intimation to the assesses should be sent

with in 1 year from the end of the financial year in

which return of income is made.

61

3. SCRUTINY ASSESSMENT UNDER

SEC 143(3):

Scrutiny assessment under sec 143(3) falls under the

following categories-

Scheme of scrutiny under sec 143(3):

The scheme of scrutiny is applicable as follows:

• A return of income or loss has been made by the

assesses.

• The assessing officer feels it necessary to ensure that

the assesses has not understated the income or over

stated the loss or has not under paid tax in any

manner.

BVZ6A,BPG6C – Income tax law & practice-II 62

• A notice shall be served on the assessee requiring

him produce any evidence which the assessee may

reply in support of the return. The notice shall be

sent on or before the expiry of 12 months from the

end of the month in which return is furnished.

• On the basis of evidence gathered by the assessing

officer from the assessee and other evidence the

assessing officer shall pass an assessment order in

writing determining.

I. The total income or loss of the assessee and

II. The sum payable by or to the assessee on the

basis of such assessment order.

Sub Code - Sub Name 63

DEDUCTION OF TAX AT SOURCE(TDS)

In certain specified cases of income ,tax should be

deducted at source by the person responsible for

making payment of such income.

The specified cases where income tax is deductible at

source are normally those cases where the income can

be calculated in advance i.e., the assessee can know

his income even before the expiry of the „previous

year‟.

BVZ6A,BPG6C – Income tax law & practice-II 64

The specified cases where tax is deducted at source

are as under:

Salaries[sec.192]

Interest on securities[sec.193]

Dividends[sec.194]

Winnings from lotteries ,crossword puzzles, horse races

and card games.[sec.56(2)]

Tax deduction at source on Rent.[sec194-i]

Tax deduction at source on commission etc. on sale of

lottery tickets[sec.194G].

BVZ6A,BPG6C – Income tax law & practice-II 65

DEDUCTION OF TAX AT SOURCE

FROM SALARY [SEC.192]

S BVZ6A,BPG6C – Income tax law & practice-II 66

Adjustment of tax

Liability of the employer

Deduction at the time of payment

Person responsible for deduction of tax at source

More than one employer

Relief u/s 89 (1)

Details of other income

Adjustment of loss from house property

In relevant columns provided inform No.16, if the amount of salary

paid or payable to the employee is more than Rs. 1,60,000 or

In form No:12BA, the amount of salary paid or payable to the

employee is more than Rs. 1,60,000 salary for the purpose shall have

the same meaning as is given in rule 3 of valuation of rent free

accommodation

• Any person responsible for paying any interest on securities is

required to deduct income tax at rates in force at the time of credit of

such income to the account of the payee.

•Tax rates: Tax is deduction at rate of 10 % in case of listed debentures

and at the rate of 10% in case of non-listed debentures if the recipient

is a resident.

BVZ6A,BPG6C – Income tax law & practice-II 67

Employer to furnish statement to

employee

TDS FROM INTEREST ON

SECURITIES[SEC.193]

Any person responsible for paying any interest on

securities is required to deduct income tax at rates in

force at the time of credit of such income to the

account of the payee.

Tax rates:

Tax is deduction at rate of 10 % in case of listed

debentures and at the rate of 10% in case of non-listed

debentures if the recipient is a resident.

BVZ6A,BPG6C – Income tax law & practice-II 68

•Tax not deductible from interest on securities;

The recipient can obtain a certificate in Form No.15AA authorizing

the payer to deduct tax or lower rates or deduct no tax as may be

appropriate.

Declaration to payer in Form No.154:

No deduction of tax is made from interest on securities in the case

of person if he furnishes a declaration in writing in duplication in Form

No .154

Debenture interest up to Rs 2500:

It is not necessary at source from any interest on debentures paid

to an individual who is resident in India.

BVZ6A,BPG6C – Income tax law & practice-II 69