by the numbers adding value to energy€¦ · by the numbers—adding value to energy 350, rue...

TRANSCRIPT

By the Numbers—Adding Value to Energy

350, rue Sparks Street, Bureau/Suite 805

Ottawa, Ontario K1R 7S8

T. 613 237-6215

Executive Summary

Canadian energy is a source of wealth creation con-

tributing to our quality of life. There are a range of

ways to further the contribution of energy in our

economy. Canada needs to develop and implement

policies that enhance the opportunities for extract-

ing maximum value from energy resources while re-

specting market principles and environmental sus-

tainability.

Energy comes in many forms, including electricity,

crude oil, natural gas and biomass. Canada can opti-

mize the value of its resources. Some energy can be

converted; some can be sequestered. The diversity

presented by moving some energy resources along

the energy value chain will enable Canadians to

share a much greater opportunity, while creating

additional wealth and jobs.

By the numbers – adding value to energy proposes

that energy resources offer an abundance of oppor-

tunities for Canada to become an energy super-

power, and also add to our economic diversity and

strength. What is envisaged is a strategy that seeks

to achieve a portfolio of energy development; some

exported, some upgraded, some consumed, some

converted.

Two strategic goals must be achieved by the joint

efforts of government and industry stakeholders:

first, to bring long-term balance to Canadian and

continental energy markets, and secondly, to add

value to at least some of our energy resources in the

most sustainable way possible to create wealth in

Canada.

Chemical manufacturing purchases 18% of gas, 5% of

oil and 3% of electricity demand in Canada. The en-

ergy is partly consumed and partly converted.

Chemical producers convert oil, gas, minerals and

electricity into value-added manufactured products,

adding 5, 10 or 20 times and more to the value of

the original energy input. In moving along re-

source value chains, Canada needs to consider

those factors that can enhance our global com-

petitiveness in adding value. Where there are du-

plicative and sometimes conflicting federal-

provincial regulations, regulatory streamlining

proposed for the energy sector projects should

also apply where business is seeking to add value

to resources, including energy.

Competitive access to resources for upgrading is a

crucial component of an integrated energy strat-

egy. Canadian chemical producers are concerned

about adequate and sustained access to a supply

of competitively-priced raw materials or feedstock

to run its plants and provide for future growth.

By the Numbers—Adding Value to Energy

i Chemistry Industry Association of Canada

Chemistry Industry Association of Canada ii

Table of Contents

Executive Summary………………………………………………………………………………………... i

Background…………………………………………………………………………………………………….1

Canada’s Economy is Closely Linked to Natural Resources…………………………...…4

Canada’s Chemical Sector – Chemistry Conversion and Value added……………...5

Petrochemicals………………………………………………………………………..7

Electrochemicals……………………………………………………………………..7

Making it Happen…………………………………………………………………… 7

A Broader Dialogue……………………………………………………….………..8

Conclusion……………………………………………………………………………………..…………….9

Chemistry Value Chains…………………………………………………………………………..…..10

Appendix 1……………………………………………………….……………………...……….………..11

Climate Change………………………..………………………………………….…11

Energy Use………………………..………………………………………………...…11

Appendix 2……………………………………………………………………………………………..…..12

By the Numbers—Adding Value to Energy

Illustration 3

goes further. It proposes that energy and other re-

sources offer a variety of opportunities and chal-

lenges. And, it recommends a portfolio approach

that recognizes the importance of not only responsi-

ble energy development, but also resource upgrad-

ing to create value-added products based on energy

inputs.

In 2007, COF released A Shared Vision for Energy in

Canada (http://www.councilofthefederation.ca/

pdfs/energystrategy_EN.pdf). In that document, the

vision and a seven point action plan were outlined.

The shared vision: a secure, sustainable, reliable and

competitively-priced supply of energy; a high stan-

dard of environmental and social responsibility (see

Appendix 1); and, continued economic growth and

prosperity. To achieve the vision, the action plan

called for the need to:

1. Promote energy efficiency and conservation.

2. Accelerate the development and deployment of

energy research and technologies that advance

more efficient production, transmission and use

of clean and conventional energy sources.

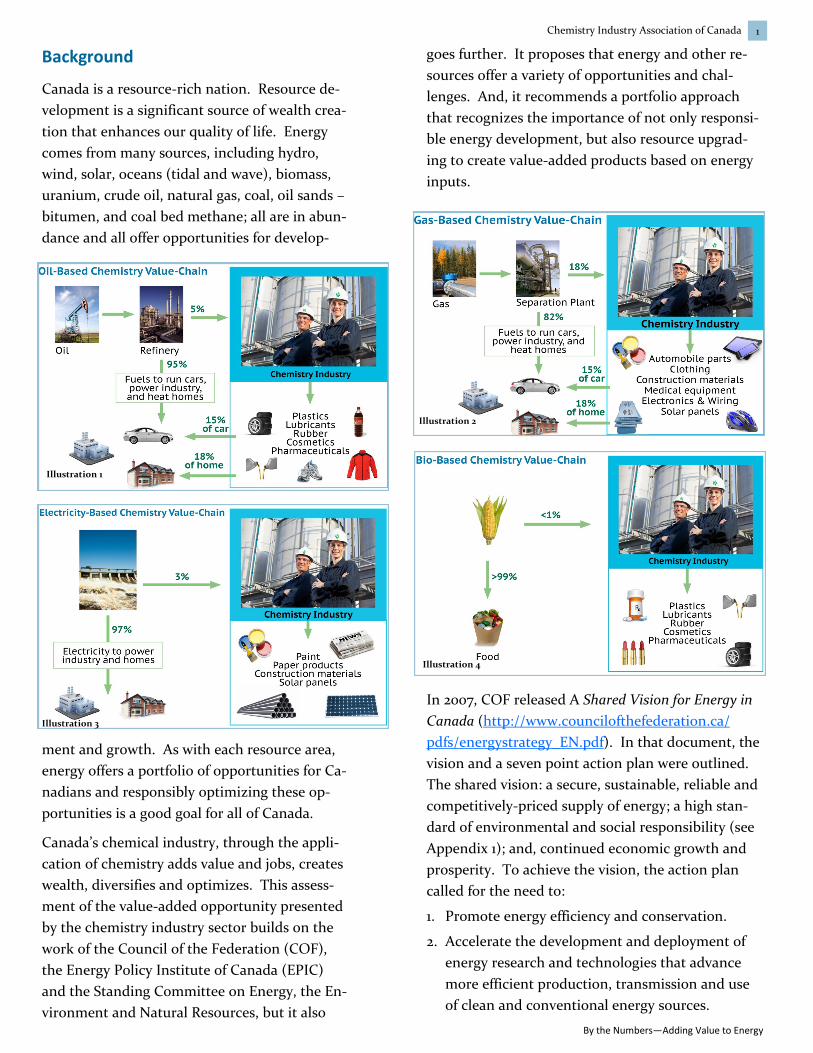

Background

Canada is a resource-rich nation. Resource de-

velopment is a significant source of wealth crea-

tion that enhances our quality of life. Energy

comes from many sources, including hydro,

wind, solar, oceans (tidal and wave), biomass,

uranium, crude oil, natural gas, coal, oil sands –

bitumen, and coal bed methane; all are in abun-

dance and all offer opportunities for develop-

ment and growth. As with each resource area,

energy offers a portfolio of opportunities for Ca-

nadians and responsibly optimizing these op-

portunities is a good goal for all of Canada.

Canada’s chemical industry, through the appli-

cation of chemistry adds value and jobs, creates

wealth, diversifies and optimizes. This assess-

ment of the value-added opportunity presented

by the chemistry industry sector builds on the

work of the Council of the Federation (COF),

the Energy Policy Institute of Canada (EPIC)

and the Standing Committee on Energy, the En-

vironment and Natural Resources, but it also

1 Chemistry Industry Association of Canada

Illustration 1

Illustration 2

Illustration 4

Illustration 3

By the Numbers—Adding Value to Energy

Chemistry Industry Association of Canada 2

By the Numbers—Adding Value to Energy

3. Facilitate the development of renewable, green

and/or cleaner energy sources to meet future

demand and contribute to environmental goals

and priorities.

4. Develop and enhance a modern, reliable, envi-

ronmentally safe, and efficient series of trans-

mission and transportation networks for domes-

tic and export/import sources of energy.

5. Improve the timeliness and certainty of regula-

tory approval decision-making processes while

maintaining rigorous protection of the environ-

ment and public interest.

6. Develop and implement strategies to meet en-

ergy-sector human resource needs now and well

into the 21st century.

7. Pursue formalized participation of provinces and

territories in international discussions and nego-

tiations on energy.

In July 2012, in Halifax, the COF took note of new

and urgent priorities that required renewal of this

strategy to ensure its continued relevance to Can-

ada’s energy challenges. They acknowledged the

need for sustainable energy development “that rec-

ognizes regional strengths and priorities and re-

spects provincial, territorial and legislative jurisdic-

tion over natural resources, a more integrated ap-

proach to climate change, reducing greenhouse gas

emissions and managing the transition to a lower

carbon economy.” They went on to identify a num-

ber of principles to guide collaborative action under

a renewed COF energy strategy (http://

www.councilofthefederation.ca/pdfs/Energy-

FINAL.pdf), including:

Maintain energy policies supported by effective,

efficient and transparent regulatory systems.

Recognize the importance of socially and envi-

ronmentally responsible development, transpor-

tation and use of energy and enabling technolo-

gies.

Affirm that intergovernmental cooperation is

essential, while respecting constitutional juris-

diction and optimizing the strengths of each

province/territory.

Governments be committed to transition to

lower-carbon alternatives and conservation to

meet future energy needs.

In the same time frame (August, 2012), EPIC re-

leased a “guide to building Canada’s future as a

global energy leader” titled A Canadian Energy

Strategy Framework (http://

www.canadasenergy.ca/canadian-energy-

strategy/). Specifically, this discussion paper

sought to collect and advance thinking in a num-

ber of areas: regulatory reform, innovation, con-

servation and literacy, market diversification and

carbon management. The document recom-

mended that decision-makers take action to cre-

ate a Canadian energy strategy that addresses

five key elements:

Respect the market as a primary determinant

of choices for energy production, transporta-

tion and its use.

Create economic development, enhance secu-

rity, grow energy production and ensure en-

ergy infrastructure.

Provide reliable and affordable energy to Ca-

nadians.

Enhance Canada’s competitiveness and econ-

omy through energy exports, technological

expertise and energy related services.

Improve energy efficiency and lower our car-

bon footprint.

Some further comments on the EPIC document

are provided in Appendix 1. Overall, it is our

view that in examining the energy sector and de-

veloping an energy strategy or framework, Cana-

dians need to broaden the dialogue and consider

our very integrated, resource-based economy.

A third study was considered in assessing the

role that value added resource upgrading should

play in a Canadian energy strategy. In July of

2012, the Standing Senate Committee on Energy,

3 Chemistry Industry Association of Canada

By the Numbers—Adding Value to Energy

the Environment and Natural Resources issued

a report culminating over three years of study

titled Now or Never: Canada Must Act Urgently

to Seize its Place in the New Energy World Order

(http://www.parl.gc.ca/Content/SEN/

Committee/411/enev/rep/rep04july12-e.pdf).

The core vision statement for this work was:

“Canada will be the most energy productive na-

tion in the world with the highest level of envi-

ronmental performance” and “responsible re-

source development” was set as the guiding

principle for this study. Rather than establish

specific end points, it identified 13 priorities or

focus points for action, all to be tested against

the guiding principle. The study noted that

“Development is responsible when it recognizes

the interests and values involved with energy

matters in four dimensions, namely economic,

environmental, social and energy security. A

change in one dimension affects the others.”

The committee believes the following 13 priori-

ties for action need to be addressed if Canada is

to be a world leader in energy production:

1. Canada must strive for collaborative energy

leadership

2. Advance nation-building through energy in-

frastructure

3. Natural gas: a game-changing fuel

4. Encourage energy efficiency and conserva-

tion from consumers

5. Frame a strong strategy for energy employ-

ment

6. Strengthen the foundation for energy inno-

vation

7. Pursue high-level environmental perform-

ance of non-renewable energy sources

8. Hydropower superpower: energy of the past

for the future

9. Foster renewable fuels

10. Regulatory reform

11. Guide responsible northern and arctic energy

exploration and development

12. Maintain strong support for Canada’s nuclear in-

dustry; and,

13. Speak for Canada.

Based on these studies, the following section elabo-

rates on optimizing energy use as a component part

of the development of an energy strategy for Canada.

Chemistry Industry Association of Canada 4

By the Numbers—Adding Value to Energy

Canada’s Economy is Closely Linked to

Natural Resources

While the Canadian economy is mature and appears

to be dominated by the service sector many of these

services are related to manufacturing and resource

development (Figure 1). Manufacturing is a very im-

portant component of our economy and figure 2 fur-

ther breaks down manufacturing into industries

based directly on resource upgrading and other

further-downstream industries.

A good illustration of the resource-manufacturing

linkage is chemical manufacturing which pur-

chases 18% of gas, 5% of oil and 3% of electricity

consumed in Canada.

Food

Wood

Paper

Chemicals

Primary metals

Fabricated metal

Other resource-based mfg

Plastics and rubber

Machinery

Transportation equipment

Other mfg

Canadian Manufacturing (GDP Comparison, 2011)

Resource-basedmanufacturing

Downstreammanufacturing

The chemistry industry consumes 18% of domestic gas, 5% of oil and 3% of electricity in adding value within the Canadian economy.

Figure 2

Services

Manufacturing

Agriculture

EnergyMining

Forestry Construction

Canadian Economy by Sector, 2011

Figure 1

5 Chemistry Industry Association of Canada

By the Numbers—Adding Value to Energy

Illustration 5

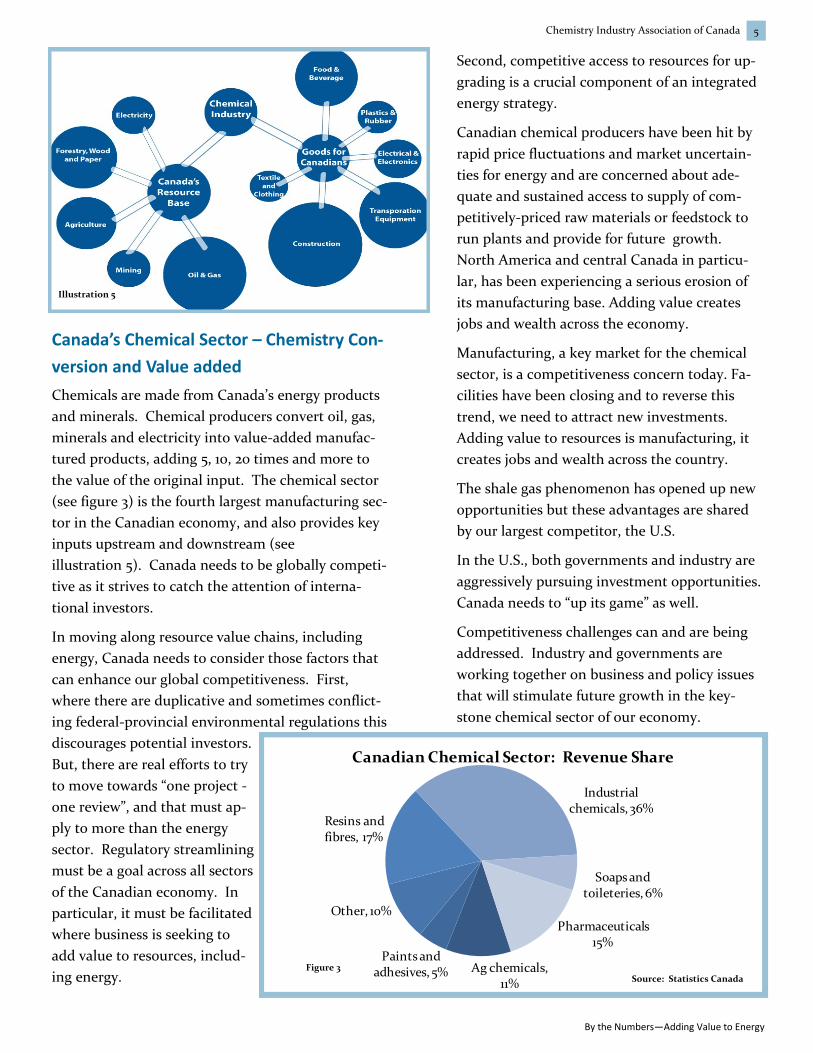

Canada’s Chemical Sector – Chemistry Con-

version and Value added

Chemicals are made from Canada’s energy products

and minerals. Chemical producers convert oil, gas,

minerals and electricity into value-added manufac-

tured products, adding 5, 10, 20 times and more to

the value of the original input. The chemical sector

(see figure 3) is the fourth largest manufacturing sec-

tor in the Canadian economy, and also provides key

inputs upstream and downstream (see

illustration 5). Canada needs to be globally competi-

tive as it strives to catch the attention of interna-

tional investors.

In moving along resource value chains, including

energy, Canada needs to consider those factors that

can enhance our global competitiveness. First,

where there are duplicative and sometimes conflict-

ing federal-provincial environmental regulations this

discourages potential investors.

But, there are real efforts to try

to move towards “one project -

one review”, and that must ap-

ply to more than the energy

sector. Regulatory streamlining

must be a goal across all sectors

of the Canadian economy. In

particular, it must be facilitated

where business is seeking to

add value to resources, includ-

ing energy.

Second, competitive access to resources for up-

grading is a crucial component of an integrated

energy strategy.

Canadian chemical producers have been hit by

rapid price fluctuations and market uncertain-

ties for energy and are concerned about ade-

quate and sustained access to supply of com-

petitively-priced raw materials or feedstock to

run plants and provide for future growth.

North America and central Canada in particu-

lar, has been experiencing a serious erosion of

its manufacturing base. Adding value creates

jobs and wealth across the economy.

Manufacturing, a key market for the chemical

sector, is a competitiveness concern today. Fa-

cilities have been closing and to reverse this

trend, we need to attract new investments.

Adding value to resources is manufacturing, it

creates jobs and wealth across the country.

The shale gas phenomenon has opened up new

opportunities but these advantages are shared

by our largest competitor, the U.S.

In the U.S., both governments and industry are

aggressively pursuing investment opportunities.

Canada needs to “up its game” as well.

Competitiveness challenges can and are being

addressed. Industry and governments are

working together on business and policy issues

that will stimulate future growth in the key-

stone chemical sector of our economy.

Ag chemicals, 11%

Paints and adhesives, 5%

Other, 10%

Resins and fibres, 17%

Industrial chemicals, 36%

Soaps and toileteries, 6%

Pharmaceuticals15%

Canadian Chemical Sector: Revenue Share

Figure 3 Source: Statistics Canada

Each chemistry industry job results in 5 additional jobs across the Canadian economy

Chemistry Industry Association of Canada 6

Canada can supply the world with value-added products.

Canada is a major source of all the necessary ingre-

dients (energy, minerals, skilled workers) to pro-

duce chemicals. Canada has the potential to be-

come the world’s best upgrader of natural resources

into value-added manufactured chemicals for do-

mestic and global markets through several routes,

but these require vision at a national as well as pro-

vincial level. An energy strategy can optimize and

secure opportunities for adding value in the petro-

chemicals area.

All of Canada’s resources offer opportunities for

adding value. Hydroelectric and major initiatives

to advance mineral production in Ontario and

Quebec create opportunities for inorganic chemical

production. Forest products and agriculture are

sources for making biochemicals. And sustainable

development in all resource sectors opens up new

and growing opportunities for chemistry solutions

and service providers.

An energy strategy must be more than facilitation

of energy project approvals and expeditious deliv-

ery of our energy to a broader suite of export mar-

kets. Our energy extraction and production must

also serve Canadians, serve them well and serve

them responsibly.

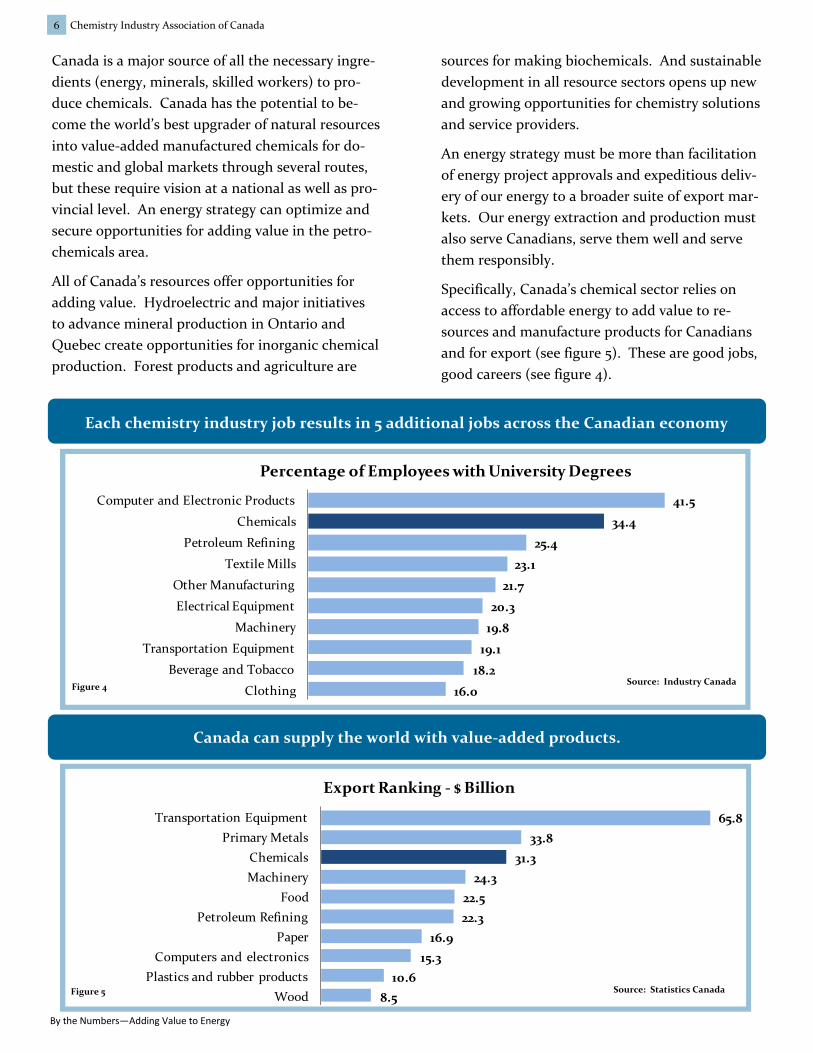

Specifically, Canada’s chemical sector relies on

access to affordable energy to add value to re-

sources and manufacture products for Canadians

and for export (see figure 5). These are good jobs,

good careers (see figure 4).

41.5

34.4

25.4

23.1

21.7

20.3

19.8

19.1

18.2

16.0

Computer and Electronic Products

Chemicals

Petroleum Refining

Textile Mills

Other Manufacturing

Electrical Equipment

Machinery

Transportation Equipment

Beverage and Tobacco

Clothing

Percentage of Employees with University Degrees

Figure 4 Source: Industry Canada

By the Numbers—Adding Value to Energy

65.8

33.8

31.3

24.3

22.5

22.3

16.9

15.3

10.6

8.5

Transportation Equipment

Primary Metals

Chemicals

Machinery

Food

Petroleum Refining

Paper

Computers and electronics

Plastics and rubber products

Wood

Export Ranking - $ Billion

Figure 5 Source: Statistics Canada

7 Chemistry Industry Association of Canada

By the Numbers—Adding Value to Energy

Petrochemicals

Chemical companies use energy as both a fuel

and as a raw material or feedstock for chemical

production. The energy may be oil, gas, elec-

tricity or bio-based materials (see illustrations

1,2,3 and 4).

For the petrochemical sub-sector, members

take energy products, mainly the natural gas

liquid ethane and convert it into a broad range

of petrochemicals such as ethylene glycol, sty-

rene and polyethylene and beyond into fabri-

cated products and formulations.

Feedstock or raw materials are core to the

competitiveness of chemical producers, to

move along the value chains (see figure 6).

Recently across Canada there have been

supply-side constraints to growth and even to

operating existing assets at capacity. Canada’s

business of chemistry consumes and converts

15%-20% of the domestic gas “barrel”, yet we

are still short of supply to operate existing

plants.

Electrochemicals

In the chemical sector, electricity is a raw ma-

terial for manufacturing electrochemicals.

Through electrolytic chemistry our members

produce necessary products such as chlo-

rine, hydrogen peroxide and sodium

chlorate for many applications including

water treatment and pulp and paper pro-

duction. Similar to oil and gas, these

manufactured goods represent 5 times to

10 times added value, along with added

jobs, added taxes for governments and a

diversification of our economy, in par-

ticular in B.C., Manitoba and Quebec.

Competitive pricing and reliable delivery

of electricity are essential for our mem-

bers and the factors driving these can

vary considerably from one province to

the next.

Making it Happen

Canada needs to develop and implement the policies

that enhance the opportunities for extracting maxi-

mum value from energy resources, while respecting

market principles. Extending the accelerated capital

cost allowance (ACCA) on a permanent basis for

manufacturing machinery and equipment will en-

hance the competitiveness of value-added projects for

Canada. Adjustments to royalties to “favour” resource

upgrading can pay big dividends for Canadians as and

when corporate income tax is applied to higher value

goods produced here. In turn, the resultant diversi-

fied economy smoothes out the government revenues

equation, could dampen resource-base swings and

could diversify employment and career opportunities

right across Canada. The chemical industry has po-

tential for further expansion and wealth creation, pro-

vided we realize our goal to access new energy and

feedstock supply.

Future feedstock sources could include northern gas

and new supplies from B.C., Saskatchewan and Al-

berta through a “Western Canada Energy Hub” in ad-

dition to continued growth in oil sands upgrading

capacity. For a review of competitiveness factors spe-

cific to the development of the chemical sector, refer

to the Chemistry Industry Association of Canada

Chemistry solutions can address Canada’s environmental issues.

124.5

26.8

19.7

16.6

11.1

10.9

9.7

9.4

8.3

8.2

6.9

2.7

0.6

Manufactured Products

Styrene

Ethylene

Propylene

Xylenes

Ethane

Gasoline

Propane

Natural Gas

Diesel Fuel

SCO

Bitumen

Coal/Coke

The hydrocarbon value chain

Value

multiplier

Upgrading &

Gasification

increase value of low grade fuels

Using Nat Gas to produce

bitumendecreases value

Figure 6 Source: Alberta Government (Adapted from Purvin & Gertz, March 20, 2004)

Chemistry Industry Association of Canada 8

By the Numbers—Adding Value to Energy

(CIAC) competitiveness scorecards and support-

ing texts (http://www.canadianchemistry.ca/

industrybrnbspcompetitiveness/

competitivenessbrscorecardsbr/tabid/81/ctl/

detail/mid/455/itemid/195/national-and-regional

-competitiveness-scorecards-for-2012-2013.aspx).

A Broader Dialogue

CIAC believes that energy

must become a matter of

Canadian priority, bringing

together the federal and

provincial governments and

energy stakeholders to de-

velop a modern, compre-

hensive energy framework.

This should be designed to

achieve two strategic goals:

first, to bring long-term bal-

ance to Canadian and conti-

nental energy markets; and

secondly, to add value to at

least a portion of our energy resources in the

most sustainable way possible to create Canadian

0%

20%

40%

60%

80%

100%

0

50

100

150

200

250

300

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Em

issi

on

s p

er u

nit

of

ou

tpu

t (1

99

2=10

0%

)

Em

issi

on

s in

Th

ou

san

d o

f T

on

nes

Total Emissions (Excluding Carbon Dioxide)

vs. Production

All Members Intensity

Current Members Intensity

All Members Emissions

Current Members Emissions

Projections

Source: “CIAC Report, Reducing Emissions 19”

wealth and jobs, products that improve everyday

living, and reduce our environmental footprint.

The chemistry industry is actively engaged in find-

ing solutions; our members are working with part-

ners in the energy sector to address emissions,

water use and site remediation issues (see figure 7

and Appendix 2).

Figure 7

MBSK

BC AB

QC

ON

9 Chemistry Industry Association of Canada

build our national economy and multiply the bene-

fits of our resources across the country.

2. Canada should recognize explicitly in any energy

strategy, framework or policy discussion that energy

cost, availability and access is a key to a highly com-

petitive and productive economy and can produce

huge value added manufacturing opportunities

throughout the country (i.e. chemistry, steel, petro-

leum products, aluminum, forest products) as well

as related service and technology sectors.

3. The chemistry industry is a key enabling sector that

can transform resources whether oil, gas, biomass,

and electricity into high value added products. It

should be recognized as an integral part of any en-

ergy strategy or framework at the federal or provin-

cial levels.

Across Canada, access to affordable and competitively-

priced energy drives economic growth and sustains

competitive advantage. Figure 8 illustrates where we

are located as we convert basic resources into products

for Canadians and for export. Competitive and

market-based access to energy for the chemical sector

is crucial to Canada’s value-added growth and capacity

for further value-added manufacturing.

Our industry is located across Canada, upgrading our resources

By the Numbers—Adding Value to Energy

Conclusion

CIAC supports policy initiatives that promote

sustainable development of diverse energy

supplies, energy conservation, and the concept

of using energy feedstock to produce high

value-added chemical products. At the same

time, energy development, environmental im-

provements and societal expectations should

advance cooperatively and not in conflict.

Chemistry solutions can address environ-

mental concerns and issues. Canada’s energy,

environmental and societal goals must be mu-

tually reinforcing and take industrial competi-

tiveness, value-added upgrading and sustain-

ability into account or risk creating significant

investment uncertainty.

Energy is a key component of economic well-

being and an essential input into an economy.

In summary:

1. Canada should take full advantage of our

abundant resources to maximize our re-

source development opportunities in the

energy industry in a sustainable and re-

sponsible way. As a nation we should take

full advantage of major projects that will

Figure 8

Chemistry Industry Association of Canada 10

By the Numbers—Adding Value to Energy

Chemistry Value Chains

By the Numbers—Adding Value to Energy

Chemistry Industry Association of Canada 11

Appendix 1

CIAC Comments on A Canadian Energy Strategy

Framework

To optimize a strategy one must carefully critique what is

presented and consider the issue in terms of overall bene-

fits to Canadians. An energy strategy is about more than

optimizing projects or profits or optimizing markets or

processes; it is also about achieving optimal quality of life

and overall public interest. In the EPIC document, the

core or fundamental principle is outlined on page 121,

paragraph 2:

“A fundamental principle in this discussion, however,

is that ultimately decisions about how Canadian en-

ergy resources should be developed, produced and

sold are best left to energy markets themselves, both

domestic and international, to resolve. Individual de-

cisions about who and where to sell an individual

firm’s energy production to and on what terms will

continue to be made by firms involved and different

market participants will have different opportunities,

with different views on which market opportunities

are most favourable for them. A critical role for gov-

ernments in this is to ensure that markets are enabled

to work efficiently, openly and fairly, while appropri-

ately safeguarding the environment and the rights of

all participants. This includes helping ensure that Ca-

nadian energy markets are open to global energy mar-

kets. And that in turn means, among other elements,

ensuring efficient, fair regulatory processes that can

expeditiously provide necessary energy transportation

infrastructure developed in a safe, environmentally

and socially responsible manner.”

While this optimizes development of primary energy, it

does not acknowledge the very real societal partnership

that is already taking place throughout the energy value

chain globally and the need to balance optimizing devel-

opment and markets with public interest. Decisions that

impact the nation require national consideration of op-

tions. The energy sector can and should provide solid

analysis and options and recommendations. The EPIC

paper does that. But energy, like any resource is a means

to an end. And any energy strategy is more than extrac-

tion and export optimization.

There is a portfolio approach to energy development

that sees some extraction and export, some upgrading

and some further refining into finished products.

Adding “some” further value to “some” basic re-

sources provides a diversity that optimizes opportuni-

ties for Canadians. That is portfolio development.

Climate Change

There are other areas that need serious debate and

coming back to the fundamental, the debate must

centre around optimizing; not just being fair or shar-

ing the pain. In the EPIC analysis, on page 27, carbon

management in the context of climate change is dis-

cussed. But, can the climate change issue be ad-

dressed by incrementality? If there is to be a global

solution to a global issue, then working at the mar-

gins is not enough and imposing costs our competi-

tors do not will hurt the economy and not help the

environment. Alberta is already imposing greater cli-

mate change obligations than nearly all other juris-

dictions and should not be looking to get even more

out of step by introducing additional requirements.

Along with continuous improvement we also need

breakthrough technologies, ones that are currently

unavailable or seem unattainable, must be sought and

found. In the meantime, a necessary alternative is

adaption. Globally every economy must invest in the

research and development that will provide future

solutions.

Energy Use

Beyond expanding energy markets, an energy strategy

for Canada must recognize that the use of energy

must also be included in discussions. Energy

(electricity, oil, gas, biomass, nuclear, wind, water,

solar) has many uses; consumption for its “energy”

value is just one use. Energy can be converted or se-

questered. CIAC will speak out on behalf of diversity.

This is about much more than market diversity; it is

about how Canadians can optimize the value of en-

ergy and any other resources. Moving along the value

chain adds value, wealth and opportunities for good

careers – the diversity it presents enables sharing a

bigger opportunity. Chemistry can add value across

energy and resource value chains across our country.

Chemistry Industry Association of Canada 12

By the Numbers—Adding Value to Energy

Appendix 2

Responsible Care® - Our Commitment to

Sustainability

CIAC is the national trade association of Canadian

chemical manufacturers, representing companies

that manufacture basic chemicals and resins.

Members range from family-owned companies to

affiliates of global enterprises. Together, these

companies generate revenues of more than $26

billion, representing over half of the total chemi-

cal sector which also includes fertilizers, pharma-

ceuticals and formulated products.

Responsible Care is the Association’s commitment

to sustainability – the betterment of society, the

environment and the economy. Our member op-

erations are bound and guided by the ethics and

principles of Responsible Care. A consequence of

these ethics, our members constantly innovate for

safer, more environmentally-friendly products and

processes, and work cooperatively to identify and

eliminate harm throughout the entire life cycle of

their products.

For a more complete description of the ethic and

the membership commitment to sustainable de-

velopment principles, visit

www.canadianchemistry.ca.

For Further information, please contact: David Podruzny Vice-President, Business and Economics Tel: (613) 237-6215 ext. 229 e-mail: [email protected]