c h a p t e r 5 operating budgets. learning objective 1 describe different types of budgeting and...

TRANSCRIPT

C H A P T E R 5

Operating BudgetsOperating Budgets

Learning Objective 1

Describe different types of budgeting and identify the purposes of budgeting.

What is Budgeting?

Budget: A quantitative expression of a plan of action that shows how a firm or an organization will acquire and use resources over some specified period of time.

The budget identifies and allocates resources necessary to effectively and efficiently carry out the mission of the organization.

Successful budgeting is absolutely critical to the success of a business.

Describe Three Types of Budgets

Strategic Plan: Broad, long-run planning, usually prepared by top management.

Capital Budget: Systematic plan for long-term investments in operating assets.

Operations (Master) Budget: Details the immediate goals for revenues, production, expenses, and cash for the next period. This budget is the most detailed and the most heavily used budget an organization has.

What are the Purposes of Budgeting ?

OVERALL PURPOSE:

To quantify a general plan so that performance in relation to a goal can be carefully monitored.

TWOFOLD PURPOSE

FIRST:To allow individuals or companies to develop a plan to meet a specified goal.

SECOND:To allow ongoing comparison between actual results and the plan in order to control operations or activities.

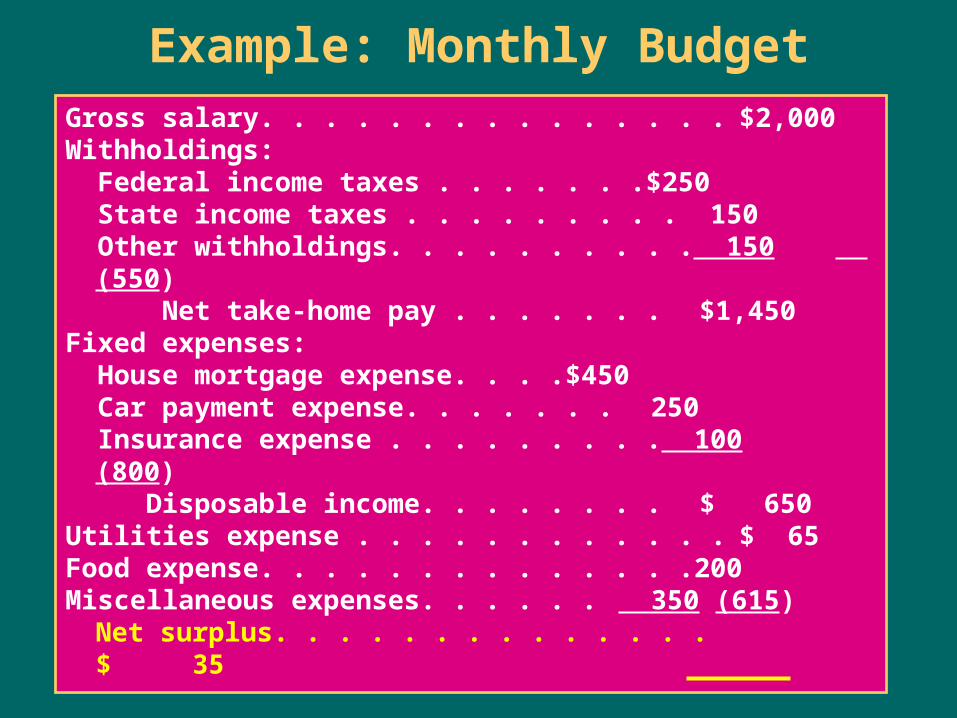

Example: Monthly Budget

Gross salary. . . . . . . . . . . . . . . $2,000 Withholdings: Federal income taxes . . . . . . . $250 State income taxes . . . . . . . . . 150 Other withholdings. . . . . . . . . . 150 (550) Net take-home pay . . . . . . . $1,450 Fixed expenses: House mortgage expense. . . . $450 Car payment expense. . . . . . . 250 Insurance expense . . . . . . . . . 100 (800) Disposable income. . . . . . . . $ 650 Utilities expense . . . . . . . . . . . . $ 65Food expense. . . . . . . . . . . . . . 200Miscellaneous expenses. . . . . . 350 (615)

Net surplus. . . . . . . . . . . . . . $ 35

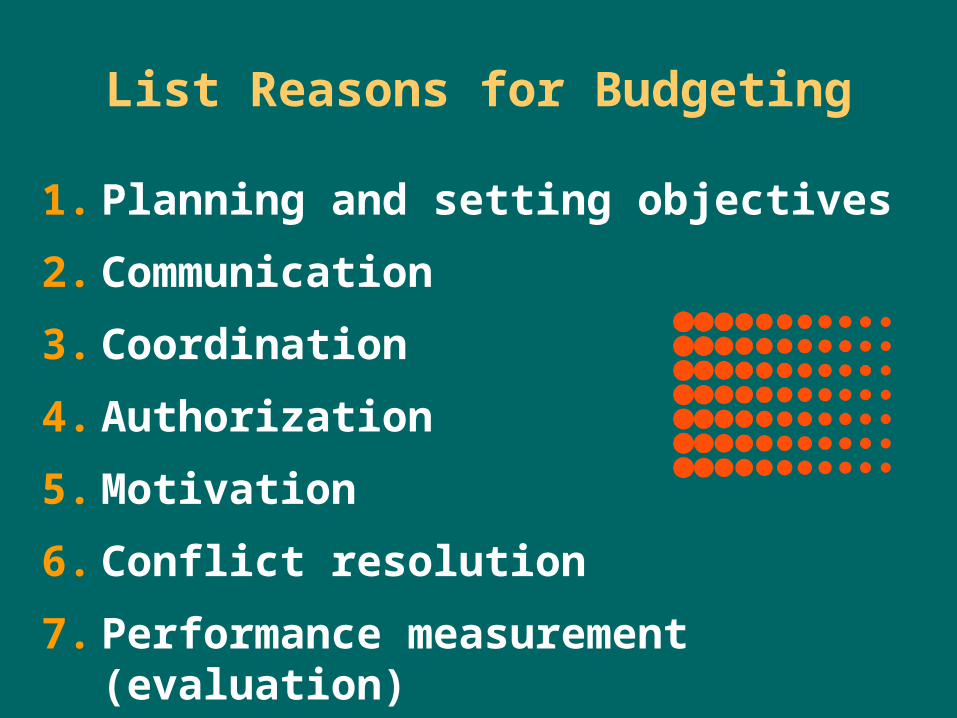

List Reasons for Budgeting

1. Planning and setting objectives

2. Communication

3. Coordination

4. Authorization

5. Motivation

6. Conflict resolution

7. Performance measurement (evaluation)

Learning Objective 2

Describe the budgeting process and its behavioral implications.

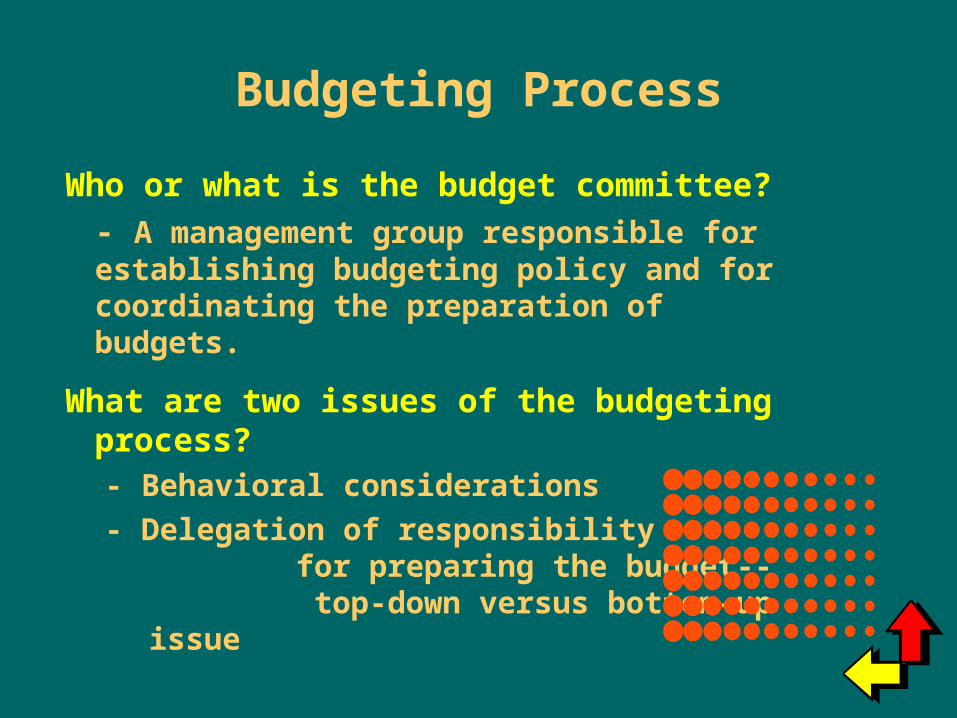

Budgeting Process

Who or what is the budget committee?

- A management group responsible for establishing budgeting policy and for coordinating the preparation of budgets.

What are two issues of the budgeting process?- Behavioral considerations

- Delegation of responsibility for preparing the budget-- top-down versus bottom-up issue

List Behavioral Considerations

1. Top management support

2. Employee participation

3. Addressing budget deviations

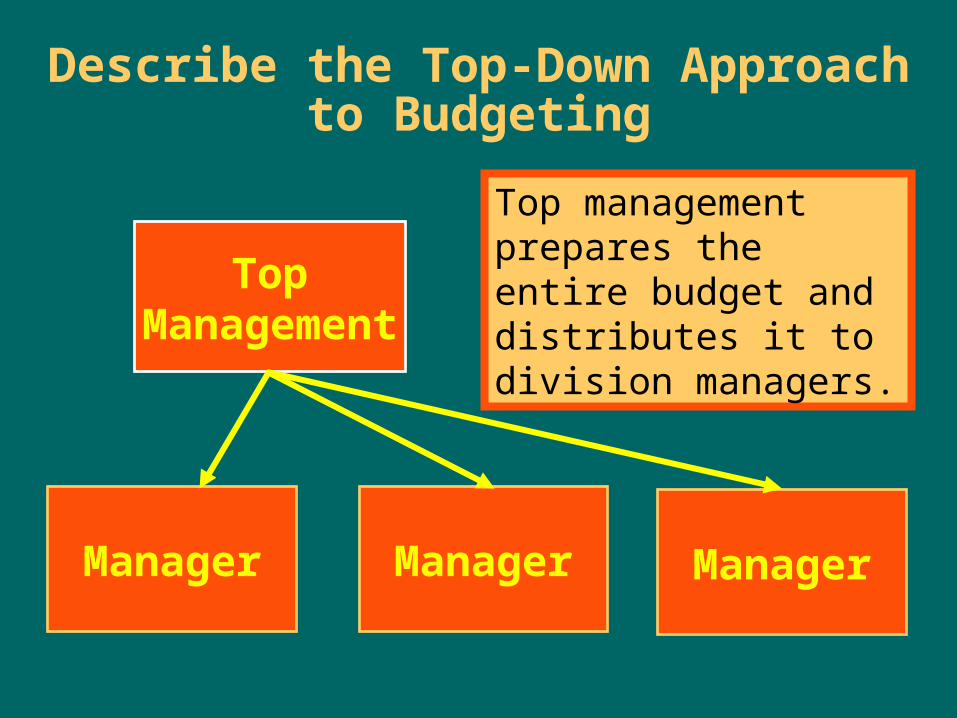

Describe the Top-Down Approach to Budgeting

TopManagement

Manager ManagerManager

Top management prepares the entire budget and distributes it to division managers.

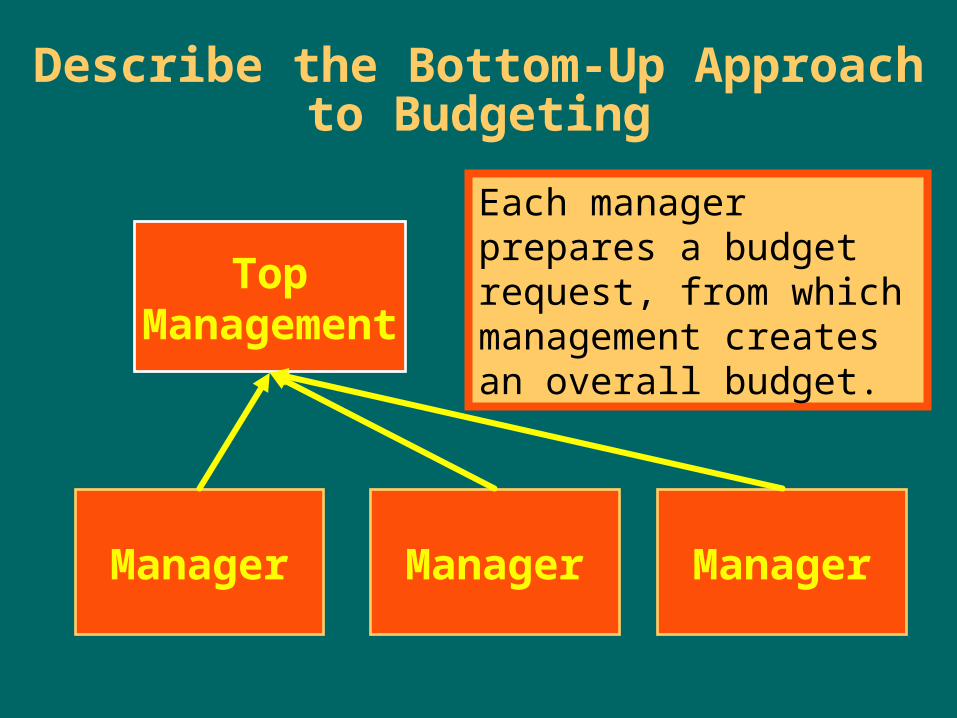

Describe the Bottom-Up Approach to Budgeting

TopManagement

Manager ManagerManager

Each manager prepares a budget request, from which management creates an overall budget.

Learning Objective 3

Explain the master budget and its components for manufacturing firms, merchandising firms, and service firms.

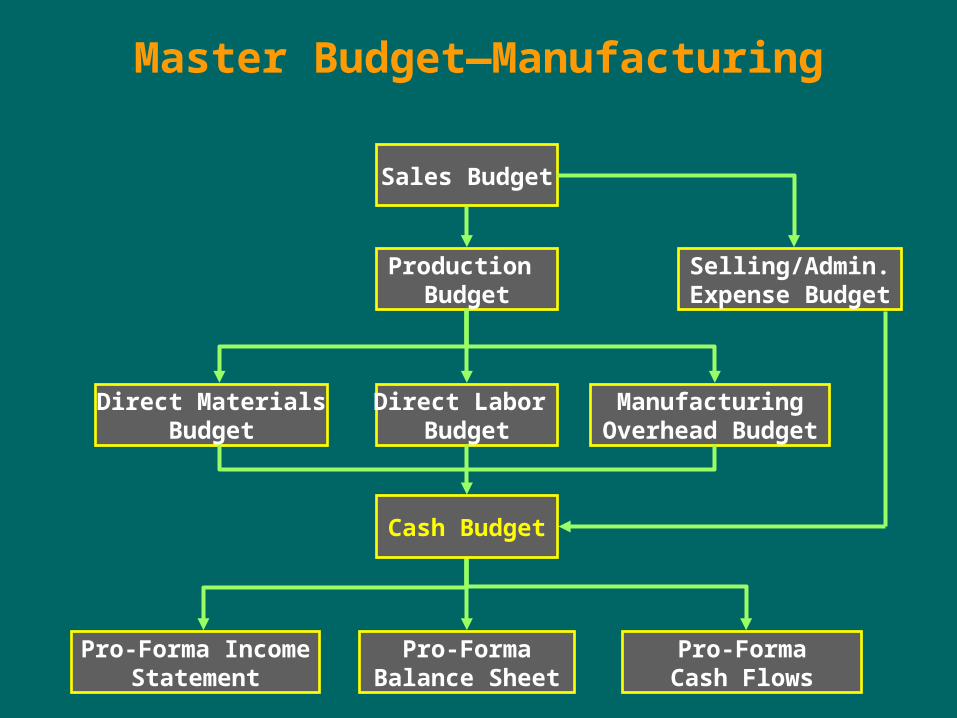

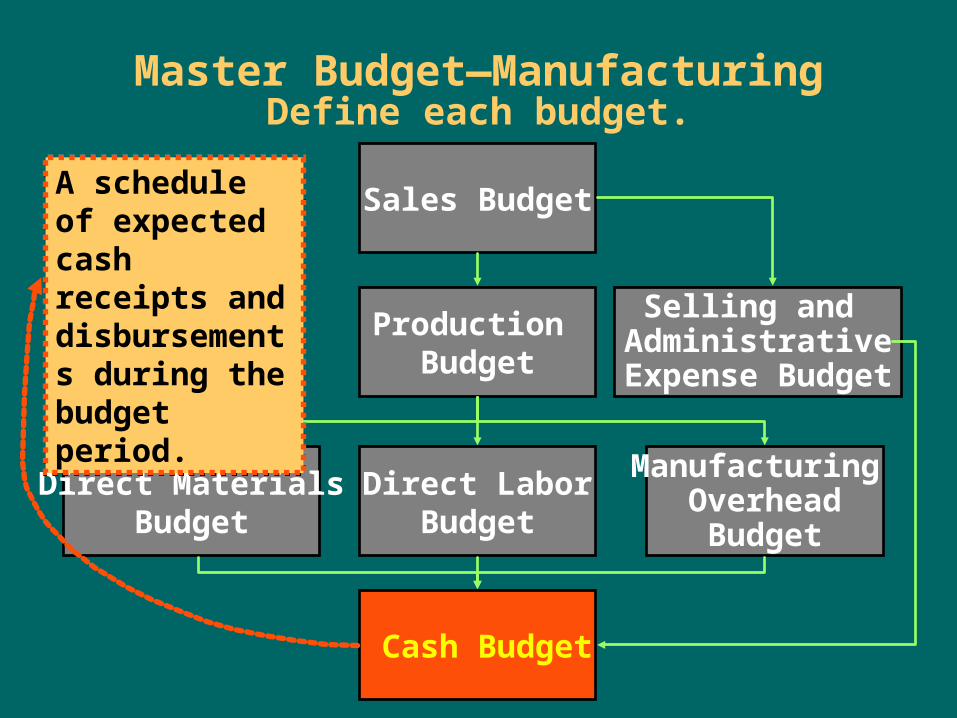

Master Budget—Manufacturing

Sales Budget

Selling/Admin.Expense Budget

Production Budget

Direct Labor Budget

ManufacturingOverhead Budget

Direct MaterialsBudget

Pro-Forma IncomeStatement

Pro-FormaBalance Sheet

Pro-FormaCash Flows

Cash Budget

Sales Budget

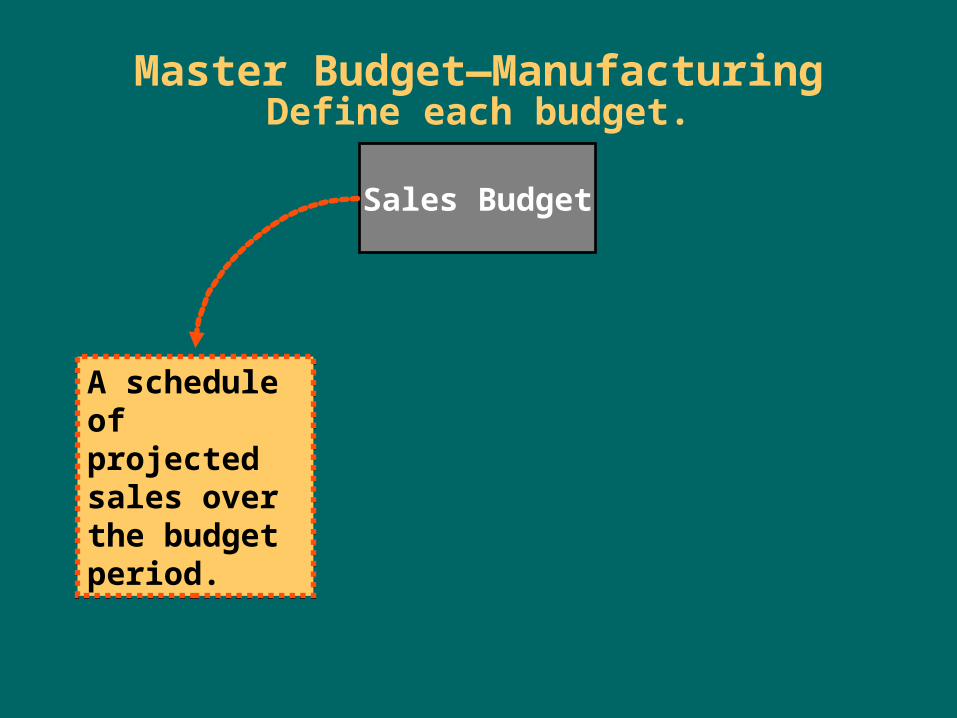

Master Budget—ManufacturingDefine each budget.

A schedule of projected sales over the budget period.

A schedule of projected sales over the budget period.

Example: Sales Budget

Selling price per bike . . . . . . $ 100

Expected sales (units). . . . . x 100

Expected revenues . . . . . . . $10,000

Selling price per bike . . . . . . $ 100

Expected sales (units). . . . . x 100

Expected revenues . . . . . . . $10,000

Sales Budget

Production Budget

Master Budget—ManufacturingDefine each budget.

A schedule of production requirements for the budget period.

A schedule of production requirements for the budget period.

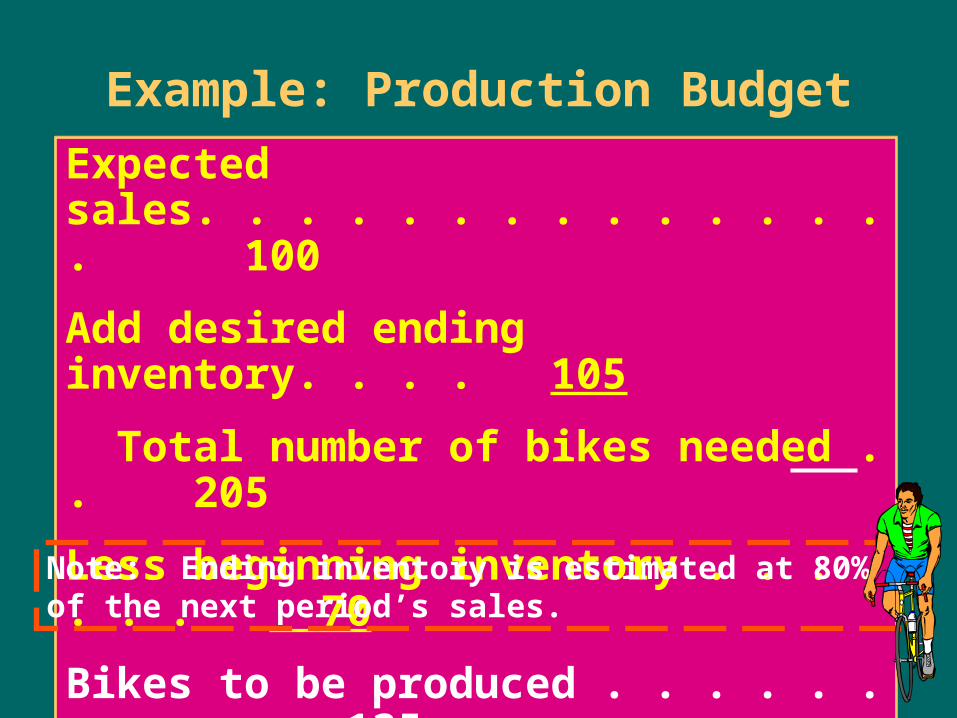

Example: Production Budget

Expected sales. . . . . . . . . . . . . . . 100

Add desired ending inventory. . . . 105

Total number of bikes needed . . 205

Less beginning inventory . . . . . . . 70

Bikes to be produced . . . . . . . . . . 135

Expected sales. . . . . . . . . . . . . . . 100

Add desired ending inventory. . . . 105

Total number of bikes needed . . 205

Less beginning inventory . . . . . . . 70

Bikes to be produced . . . . . . . . . . 135

Note: Ending inventory is estimated at 80% of the next period’s sales.

Sales Budget

Production Budget

Direct MaterialsBudget

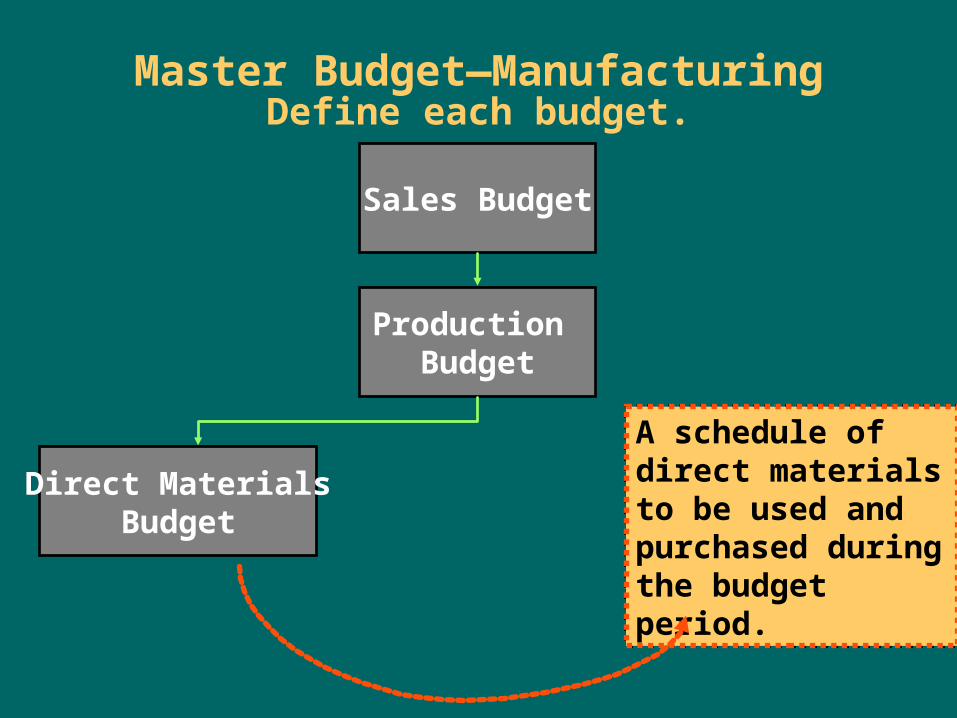

Master Budget—ManufacturingDefine each budget.

A schedule of direct materials to be used and purchased during the budget period.

A schedule of direct materials to be used and purchased during the budget period.

Example: Direct Materials Budget

Direct materials usage:

Direct Amount Unit TotalMaterials Required Cost Cost

Metal 2,700 lbs. $2.00/ft. $5,400

Plastic 405 lbs. $1.00/ft. $ 405

Direct materials usage:

Direct Amount Unit TotalMaterials Required Cost Cost

Metal 2,700 lbs. $2.00/ft. $5,400

Plastic 405 lbs. $1.00/ft. $ 405

Example: Direct Materials Budget

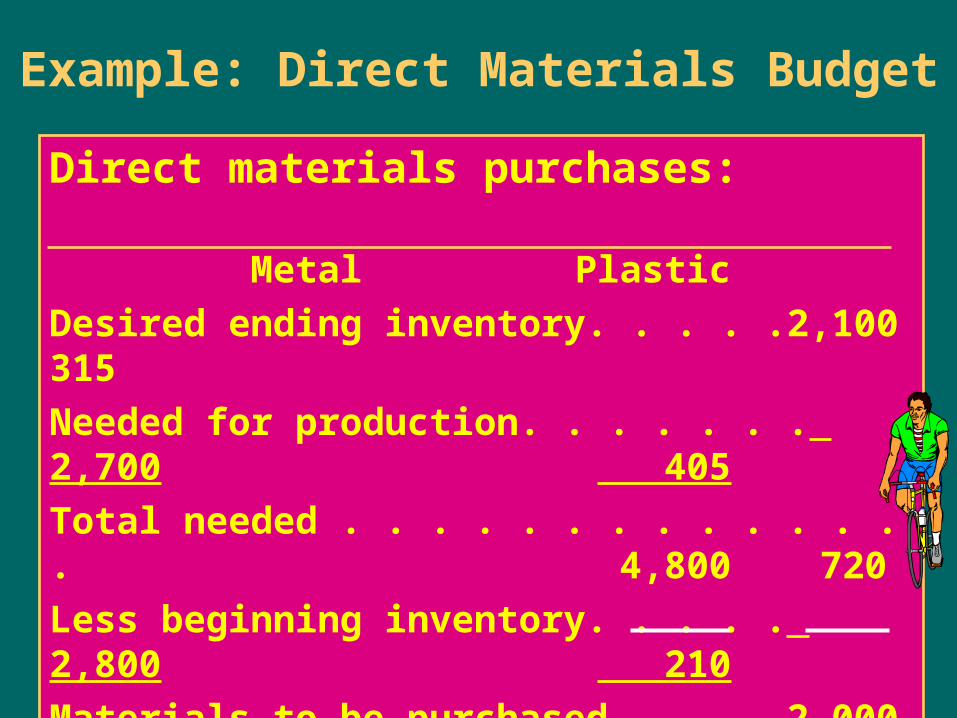

Direct materials purchases: Metal Plastic

Desired ending inventory. . . . . 2,100 315

Needed for production. . . . . . . 2,700 405

Total needed . . . . . . . . . . . . . . 4,800 720

Less beginning inventory. . . . . 2,800 210

Materials to be purchased . . . . 2,000 510

Unit cost. . . . . . . . . . . . . . . . . . x $2 x $1

Total cost . . . . . . . . . . . . . . . . $4,000 $ 510

Direct materials purchases: Metal Plastic

Desired ending inventory. . . . . 2,100 315

Needed for production. . . . . . . 2,700 405

Total needed . . . . . . . . . . . . . . 4,800 720

Less beginning inventory. . . . . 2,800 210

Materials to be purchased . . . . 2,000 510

Unit cost. . . . . . . . . . . . . . . . . . x $2 x $1

Total cost . . . . . . . . . . . . . . . . $4,000 $ 510

Sales Budget

Production Budget

Direct MaterialsBudget

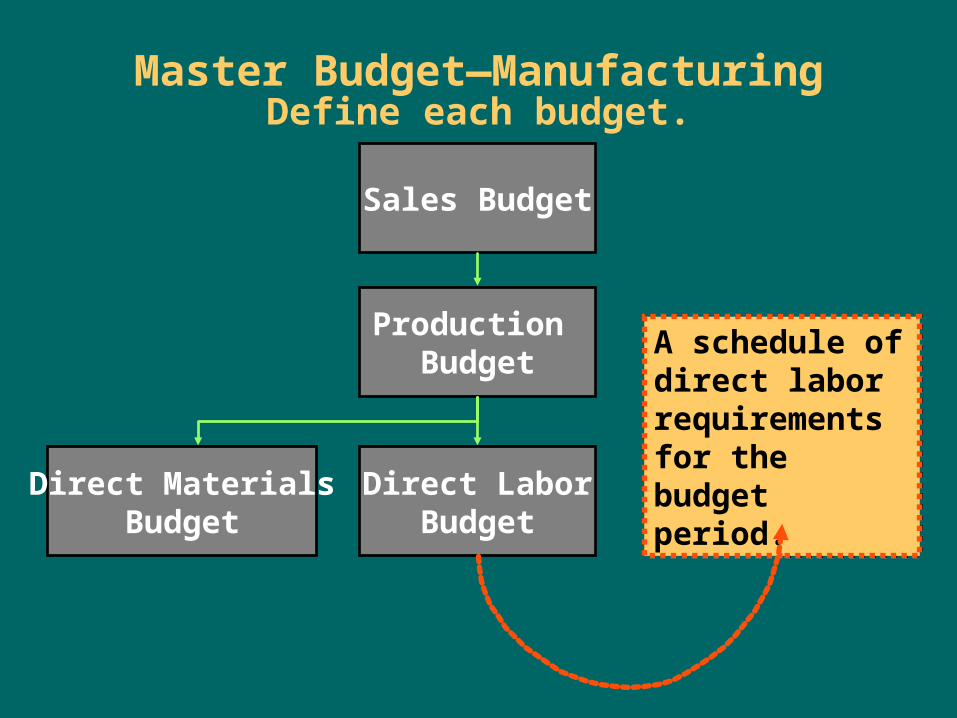

Direct LaborBudget

Master Budget—ManufacturingDefine each budget.

A schedule of direct labor requirements for the budget period.

A schedule of direct labor requirements for the budget period.

Example: Direct Labor Budget

Number of bikes to produce. . . . 135

Direct labor hours per bike. . . . .x 3

Total hours required. . . . . . . . . 405

Rate per hour. . . . . . . . . . . . . . . .x $5

Total direct labor cost. . . . . . . . $2,025

Number of bikes to produce. . . . 135

Direct labor hours per bike. . . . .x 3

Total hours required. . . . . . . . . 405

Rate per hour. . . . . . . . . . . . . . . .x $5

Total direct labor cost. . . . . . . . $2,025

Sales Budget

Production Budget

Direct MaterialsBudget

Direct LaborBudget

Manufacturing Overhead

Budget

Master Budget—ManufacturingDefine each budget.

A schedule of production costs other than those for direct labor and direct materials.

A schedule of production costs other than those for direct labor and direct materials.

Example: Manufacturing Overhead Budget

Variable costs:Indirect materials costs. . . . . . . . . $ 220Indirect labor costs . . . . . . . . . . . . 600 Total variable costs. . . . . . . . . . . $ 820

Fixed costs:Insurance expense. . . . . . . . . . . . 200Depreciation expense. . . . . . . . . . $ 600 Total fixed costs . . . . . . . . . . . . . $ 800

Total manufacturing overhead . . . $1,620

Variable costs:Indirect materials costs. . . . . . . . . $ 220Indirect labor costs . . . . . . . . . . . . 600 Total variable costs. . . . . . . . . . . $ 820

Fixed costs:Insurance expense. . . . . . . . . . . . 200Depreciation expense. . . . . . . . . . $ 600 Total fixed costs . . . . . . . . . . . . . $ 800

Total manufacturing overhead . . . $1,620

Sales Budget

Production Budget

Direct MaterialsBudget

Direct LaborBudget

Manufacturing Overhead

Budget

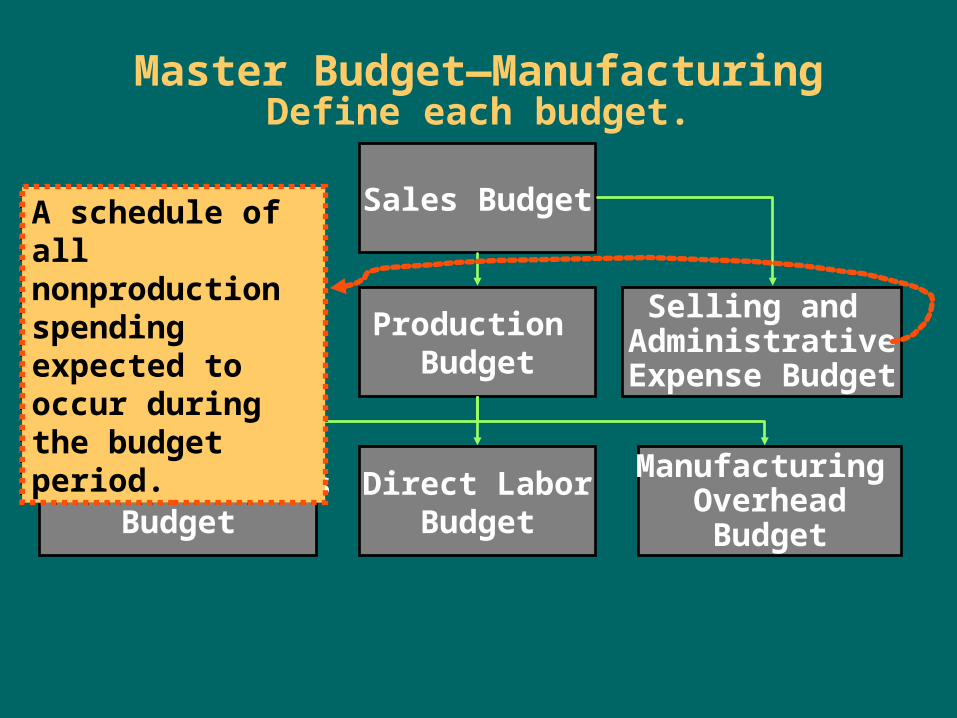

Master Budget—ManufacturingDefine each budget.

Selling and Administrative

Expense Budget

A schedule of all nonproduction spending expected to occur during the budget period.

A schedule of all nonproduction spending expected to occur during the budget period.

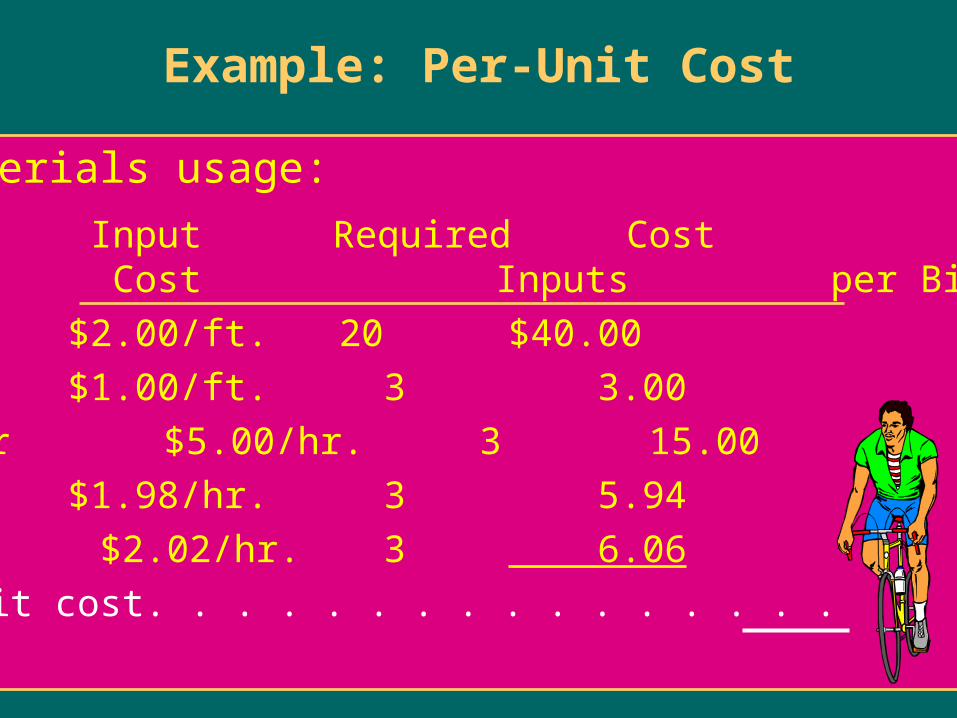

Example: Per-Unit Cost

Direct materials usage:

Input Required Cost Cost Inputs per Bike

Metal $2.00/ft. 20 $40.00

Plastic $1.00/ft. 3 3.00

Direct labor $5.00/hr. 3 15.00

Fixed OH $1.98/hr. 3 5.94

Variable OH $2.02/hr. 3 6.06

Total unit cost. . . . . . . . . . . . . . . . $70.00

Direct materials usage:

Input Required Cost Cost Inputs per Bike

Metal $2.00/ft. 20 $40.00

Plastic $1.00/ft. 3 3.00

Direct labor $5.00/hr. 3 15.00

Fixed OH $1.98/hr. 3 5.94

Variable OH $2.02/hr. 3 6.06

Total unit cost. . . . . . . . . . . . . . . . $70.00

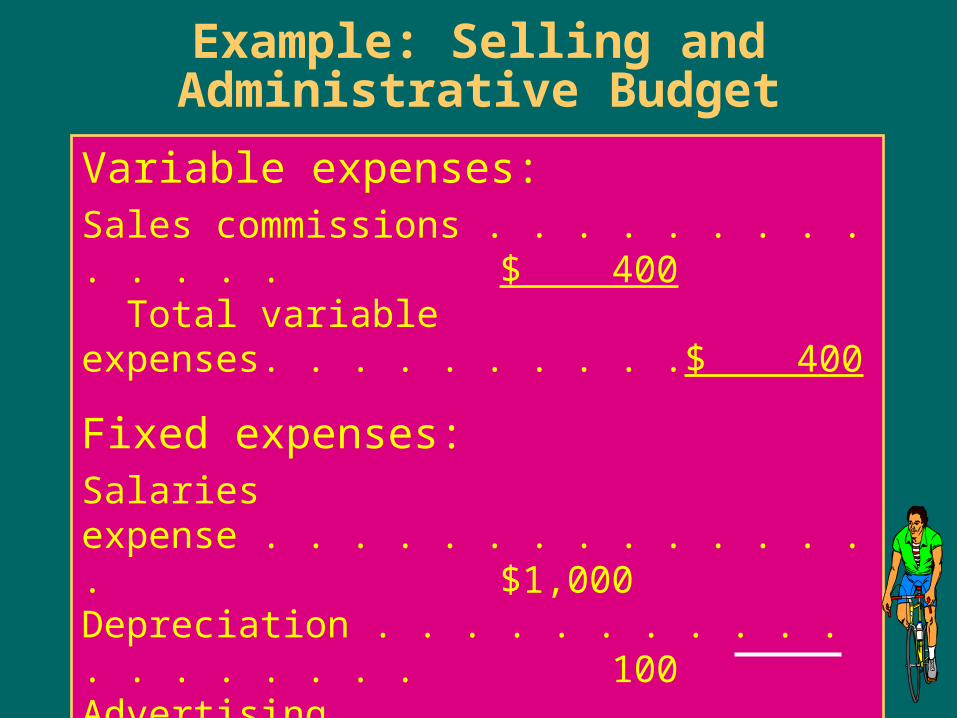

Example: Selling and Administrative Budget

Variable expenses:Sales commissions . . . . . . . . . . . . . . $ 400 Total variable expenses. . . . . . . . . . $ 400

Fixed expenses:Salaries expense . . . . . . . . . . . . . . . $1,000Depreciation . . . . . . . . . . . . . . . . . . . 100Advertising expense. . . . . . . . . . . . . 200 Total fixed expenses. . . . . . . . . . . . $1,300Total selling and administrative expenses. . . . . . . . . $1,700

Sales Budget

Production Budget

Direct MaterialsBudget

Direct LaborBudget

Manufacturing Overhead

Budget

Master Budget—ManufacturingDefine each budget.

Selling and Administrative

Expense Budget

Cash Budget

A schedule of expected cash receipts and disbursements during the budget period.

A schedule of expected cash receipts and disbursements during the budget period.

Example: Cash Budget

Cash balance, beginning . . . . . . . . . $ 4,900Add collections from customers . . . . 10,100(1)Total cash available. . . . . . . . . . $15,000Less disbursements for: Direct materials . . . . . . . . . . . . . $ 3,000 Direct labor. . . . . . . . . . . . . . . . . 2,000 Equipment purchase . . . . . . . . . 2,000(2)Total disbursements. . . . . . . . . . $ 7,000Minimum cash balance desired. . . . . 6,000Total cash needed. . . . . . . . . . . . . . . $13,000Excess (or deficiency) of cash available before financing. . . . . $ 2,000(3) Financing needed . . . . . . . . . . . 0

Ending cash balance [(1) – (2) + (3)] $ 2,000

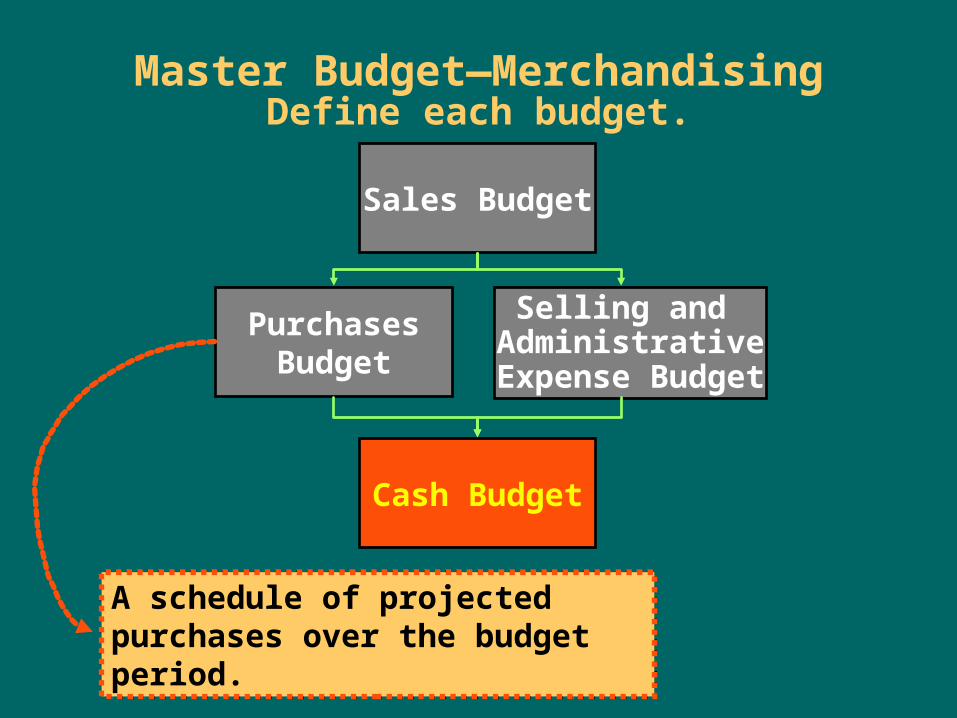

Sales Budget

PurchasesBudget

Cash Budget

Master Budget—MerchandisingDefine each budget.

Selling and Administrative

Expense Budget

A schedule of projected purchases over the budget period.A schedule of projected purchases over the budget period.

Master Budget—MerchandisingDefine each budget.

Sales Budget

PurchasesBudget

Cash Budget

Pro-FormaStatement ofCash Flows

Selling and Administrative

Expense Budget

Pro-FormaBalance

Sheet

Pro-FormaIncome

Statement

Pro-forma financial statements “budget” financial information for the coming period.

Pro-forma financial statements “budget” financial information for the coming period.

Master Budget—ServiceDefine each budget.

Pro-Forma IncomeStatement

Revenue Budget

Wages andSalaries Budget

Production Budget

Cash Budget

Pro-FormaBalance Sheet

Selling/Admin.Expense Budget

OverheadBudget

SuppliesBudget

Pro-Forma Statementof Cash Flows

A service entity’s budget that identifies how much revenue will be generated during a period.

Expanded MaterialLearning Objective 4

Prepare pro-forma financial statements.

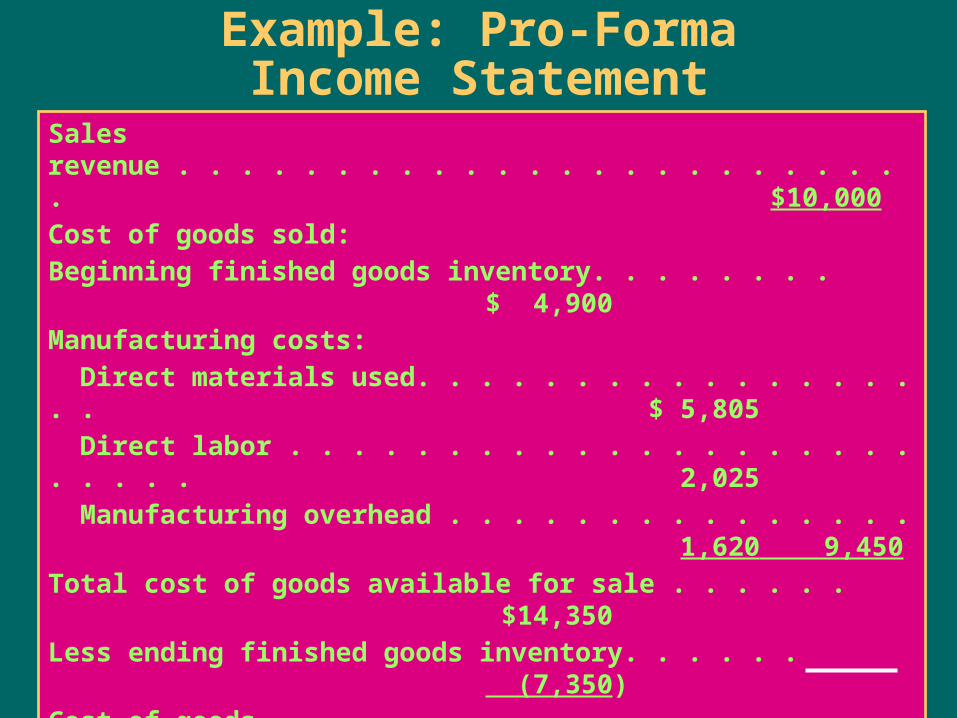

Example: Pro-FormaIncome Statement

Sales revenue . . . . . . . . . . . . . . . . . . . . . . . . $10,000 Cost of goods sold:Beginning finished goods inventory. . . . . . . . $ 4,900 Manufacturing costs: Direct materials used. . . . . . . . . . . . . . . . . . $ 5,805 Direct labor . . . . . . . . . . . . . . . . . . . . . . . . . 2,025 Manufacturing overhead . . . . . . . . . . . . . . . 1,620 9,450 Total cost of goods available for sale . . . . . . $14,350 Less ending finished goods inventory. . . . . . (7,350)Cost of goods sold. . . . . . . . . . . . . . . . . . . . . (7,000)Gross margin. . . . . . . . . . . . . . . . . . . . . . . . . $ 3,000 Selling and administrative expenses. . . . . . . 1,700 Operating income . . . . . . . . . . . . . . . . . . . . . $ 1,300 Interest expense . . . . . . . . . . . . . . . . . . . . . . 0 Income before taxes . . . . . . . . . . . . . . . . . . . $ 1,300

ASSETS

Current assets: Cash. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 15,000 Accounts receivable . . . . . . . . . . . . . . . . . . . . . . 3,000 Finished goods . . . . . . . . . . . . . . . . . . . . . . . . . . 7,350 $ 25,350Long-term operating assets: Equipment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .$ 12,000 Less accumulated depreciation. . . . . . . . . . . . . (3,300) 8,700

Total assets. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 34,050

Example: Pro-Forma Balance Sheet

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities: Accounts payable. . . . . . . . . . . . . . . . . . . . . . . . . $ 8,000 Notes payable . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,000 $ 15,000

Stockholders’ equity: Common stock. . . . . . . . . . . . . . . . . . . . . . . . . . . $ 11,850 Retained earnings . . . . . . . . . . . . . . . . . . . . . . . . 7,200 19,050

Total liabilities and stockholders’ equity. . . . . . . . . $ 34,050

Example: Pro-Forma Statement of Cash Flows

Cash flows from operating activities:Net income . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,300 Add (subtract) adjustments:

Depreciation . . . . . . . . . . . . . . . . . . . . . . . $ 700 Increase in finished goods . . . . . . . . . . . . (2,450)Increase in accounts receivable. . . . . . . . 5,550 3,800

Net cash provided by operating activities . . $ 5,100

Cash flows from investing activities:Purchase of equipment . . . . . . . . . . . . . . $(2,000)

Net cash used in investing activities . . . . (2,000)

Cash flows from financing activities:Cash obtained from borrowing . . . . . . . . $ 7,000

Net cash used in financing activities. . . . 7,000

Net increase in cash. . . . . . . . . . . . . . . . . . $ 10,100

Expanded MaterialLearning Objective 5

Distinguish between static and flexible budgets.

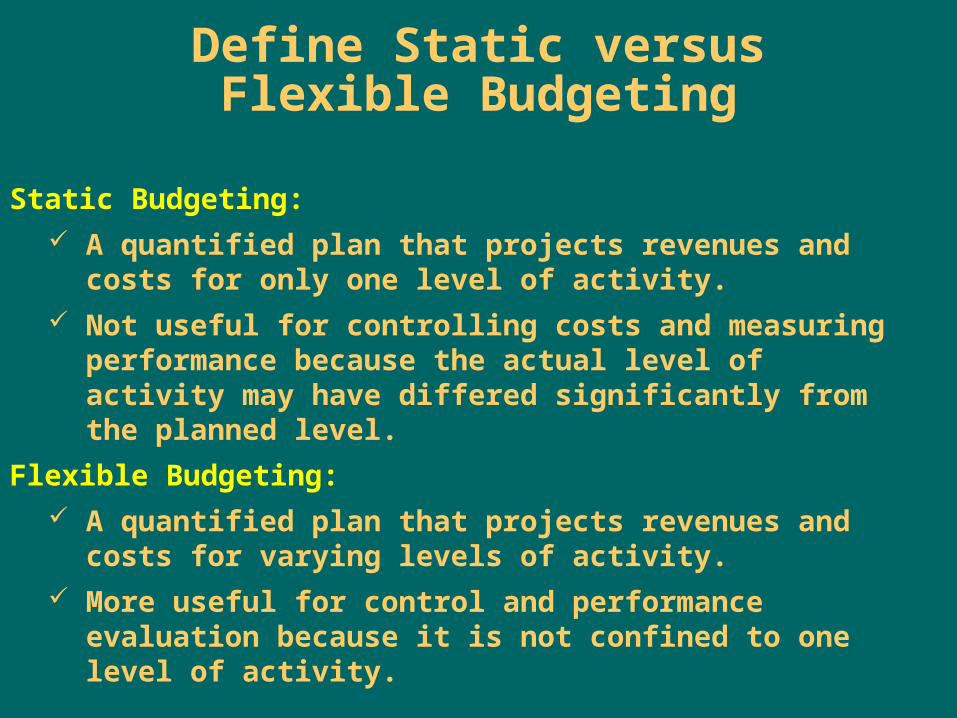

Define Static versusFlexible Budgeting

Static Budgeting: A quantified plan that projects revenues and costs for

only one level of activity. Not useful for controlling costs and measuring

performance because the actual level of activity may have differed significantly from the planned level.

Flexible Budgeting: A quantified plan that projects revenues and costs for

varying levels of activity. More useful for control and performance evaluation

because it is not confined to one level of activity.

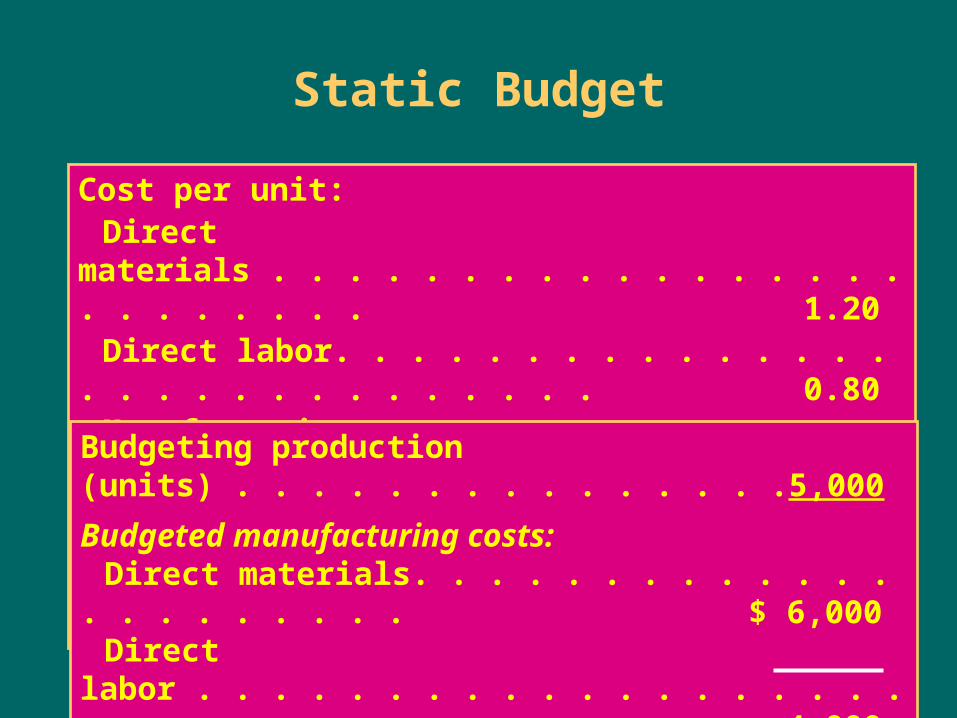

Static Budget

Cost per unit:Direct materials . . . . . . . . . . . . . . . . . . . . . . . . . 1.20Direct labor. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.80Manufacturing overhead . . . . . . . . . . . . . . . . . . 0.50

Total unit cost . . . . . . . . . . . . . . . . . . . . . . . . $2.50

Budgeting production (units) . . . . . . . . . . . . . . . 5,000

Budgeted manufacturing costs:Direct materials. . . . . . . . . . . . . . . . . . . . . . $ 6,000Direct labor . . . . . . . . . . . . . . . . . . . . . . . . . 4,000Manufacturing overhead. . . . . . . . . . . . . . . 2,500

Total manufacturing costs. . . . . . . . . . . . $12,500

Static Budget—Performance Report

Actual Budgeted Difference

Production (units) 4,800 5,000 (200)

Manufacturing costs:Direct materials. . . . . . . . .$ 5,500 $ 6,000 $ (500) Direct labor . . . . . . . . . . . . 3,800 4,000 (200) Manufacturing overhead . 2,450 2,500 (50)

Total actual and budgetedmanufacturing costs . . . . $11,750 $12,500 $ (750)

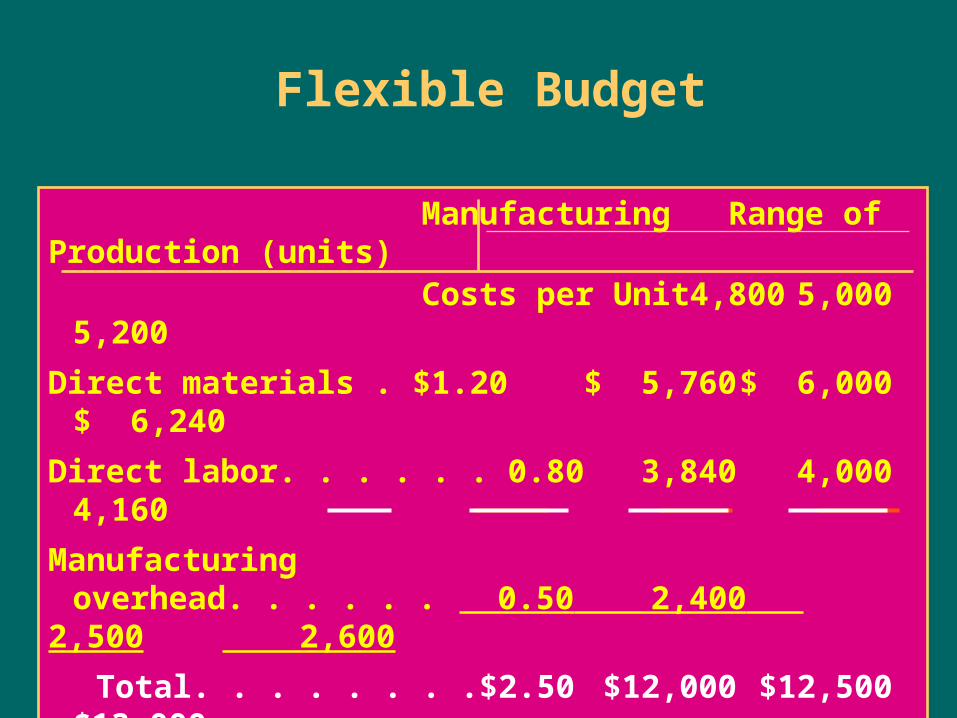

Flexible Budget

What are the three steps to prepare a

flexible budget?

Using the per-unit costs for each element, prepare a budget showing what costs are expected to be incurred at several points within the relevant range.

Analyze the projected manufacturing costs for the coming period.

Determine a relevant range over which production is expected to vary during the coming period.

Flexible Budget

Manufacturing Range of Production (units) Costs per Unit 4,800 5,000 5,200

Direct materials . $1.20 $ 5,760 $ 6,000 $ 6,240

Direct labor. . . . . . 0.80 3,840 4,000 4,160

Manufacturingoverhead. . . . . . 0.50 2,400 2,500 2,600

Total. . . . . . . . $2.50 $12,000 $12,500 $13,000

Flexible Budget—Performance Report

Actual production (units) . . . . . . . . . . . . . . . . . . 4,800 Budgeted production (units) . . . . . . . . . . . . . . . 5,000 Difference. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (200)

Actual Budgeted Difference

Direct materials. . . . . . . . . . $ 5,500 $ 5,760 $ (260) Direct labor . . . . . . . . . . . . . 3,800 3,840 (40) Manufacturing overhead . . 2,450 2,400 50

Total costs . . . . . . . . . . . . $11,750 $12,000 $ 250