c i d a d e d e s à o p a u l o indicadores · bibliografia. 1. são paulo (sp) – anuário 2....

TRANSCRIPT

E PESQUISAS DO TURISMO

C I D A D E D E S Ã O P A U L O

INDICADORES2008

*TOURISM INDICATORS AND RESEARCH IN THE CITY OF SÃO PAULO

*

E PESQUISAS DO TURISMO

C I D A D E D E S Ã O P A U L O

INDICADORES2008*TOURISM INDICATORS AND RESEARCH IN THE CITY OF SÃO PAULO

*

INDICADORES E PESQUISAS DO TURISMO DA CIDADE DE SÃO PAULOTOURISM INDICATORS AND RESEARCH IN THE CITY OF SÃO PAULO

[tradução BTS Traduções]

São Paulo : São Paulo Turismo, 2008.

Vários colaboradores.

Bibliografia.

1. São Paulo (SP) – Anuário

2. São Paulo (SP) – Descrição

3. São Paulo (SP) – Indicadores

4. São Paulo (SP) – Pesquisas

5. Turismo – São Paulo (SP)

I. Título: Tourism Indicators and Research in the City of São Paulo.

08-09495

CDD-918.1611

Índices para catálogo sistemático:

1. Indicadores e pesquisas do turismo : São Paulo : Cidade : Anuário

918.1611

As cores (cinza, preto e azul) desta publicação, incluindo a capa, foram adotadas com base em pesquisa de “Imagem do Turismo na Cidade de São Paulo”, realizada em 2008 pela SPTuris,

conforme opinião de turistas e moradores.

The colors (gray, black and blue) of this book, including the cover art, were chosen based on the survey carried out in 2008 by SPTuris, “Image of Tourism in the City of São Paulo” using the

opinions of both visitors and residents.

w w w . c i d a d e d e s a o p a u l o . c o m 3

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

Introdução / Foreword _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 5O maior destino turístico do país / The greatest tourism destination in the country _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 6Oferta turística / Tourism attractions _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 8

DEMANDA TURÍSTICA NA CIDADE DE SÃO PAULOTOURISM DEMAND IN THE CITY OF SÃO PAULO _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 10 DEMANDA TURÍSTICA NA CIDADE DE SÃO PAULO / TOURISM DEMAND IN THE CITY OF SÃO PAULO _ _ _ _ _ _ _ _ _ _ _ 11 CARACTERIZAÇÃO DA DEMANDA TURÍSTICA DOMÉSTICA / CHARACTERIZATION OF DOMESTIC TOURISM DEMAND _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 12 CARACTERIZAÇÃO DA DEMANDA TURÍSTICA INTERNACIONAL / CHARACTERIZATION OF INTERNATIONAL TOURISM DEMAND _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 16

ASPECTOS CONJUNTURAIS DO TURISMO PAULISTANOCONJUNCTURAL ASPECTS OF TOURISM IN SÃO PAULO _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 20 HOTELARIA / HOTEL INDUSTRY _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 21 FLUXO AÉREO / AIR TRAFFIC _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 25 TERMINAIS RODOVIÁRIOS / BUS TERMINALS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 27 VOLUME DO ISS / VOLUME OF ISS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 28 EVENTOS / EVENTS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 29

PESQUISAS EM EVENTOS DE GRANDE PORTESURVEYS IN HIGH PROFILE EVENTS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 32 ADVENTURE SPORTS FAIR / ADVENTURE SPORTS FAIR _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 33 BIENAL DO LIVRO / BOOK BIENNIAL _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 38 CARNAVAL / CARNIVAL _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 43 FRANCAL / FRANCAL _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 48 GP BRASIL DE FÓRMULA 1 / BRAZILIAN FORMULA 1 GP _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 53 HOSPITALAR / HOSPITALAR _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 58 PARADA DO ORGULHO GLBT / GLBT PARADE _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 63 SALÃO DO AUTOMÓVEL / AUTOMOBILE TRADE SHOW _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 68 VIRADA CULTURAL / VIRADA CULTURAL _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 73

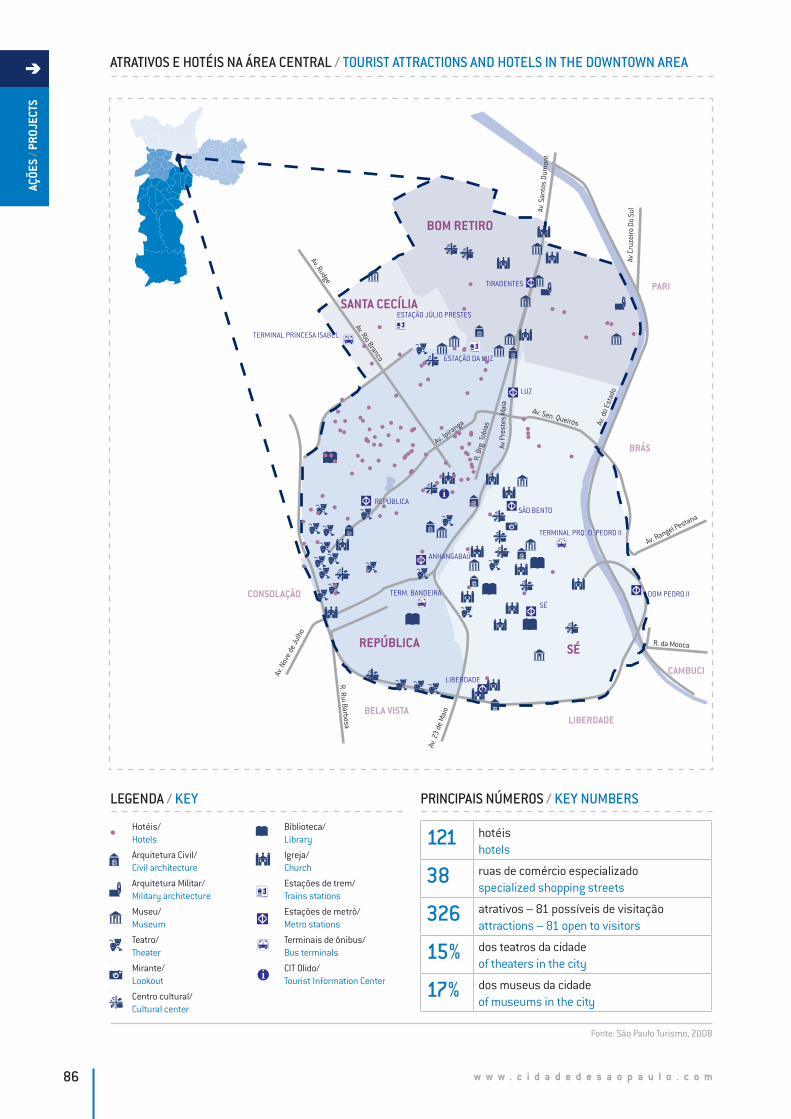

AÇÕES PARA O DESENVOLVIMENTO DO TURISMOPROJECTS FOR TOURISM DEVELOPMENT _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 79 CENTRAIS DE INFORMAÇÕES TURÍSTICAS - CITS / TOURIST INFORMATION CENTERS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 80 TURISMO NO CENTRO / TOURISM IN THE DOWNTOWN AREA _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 84

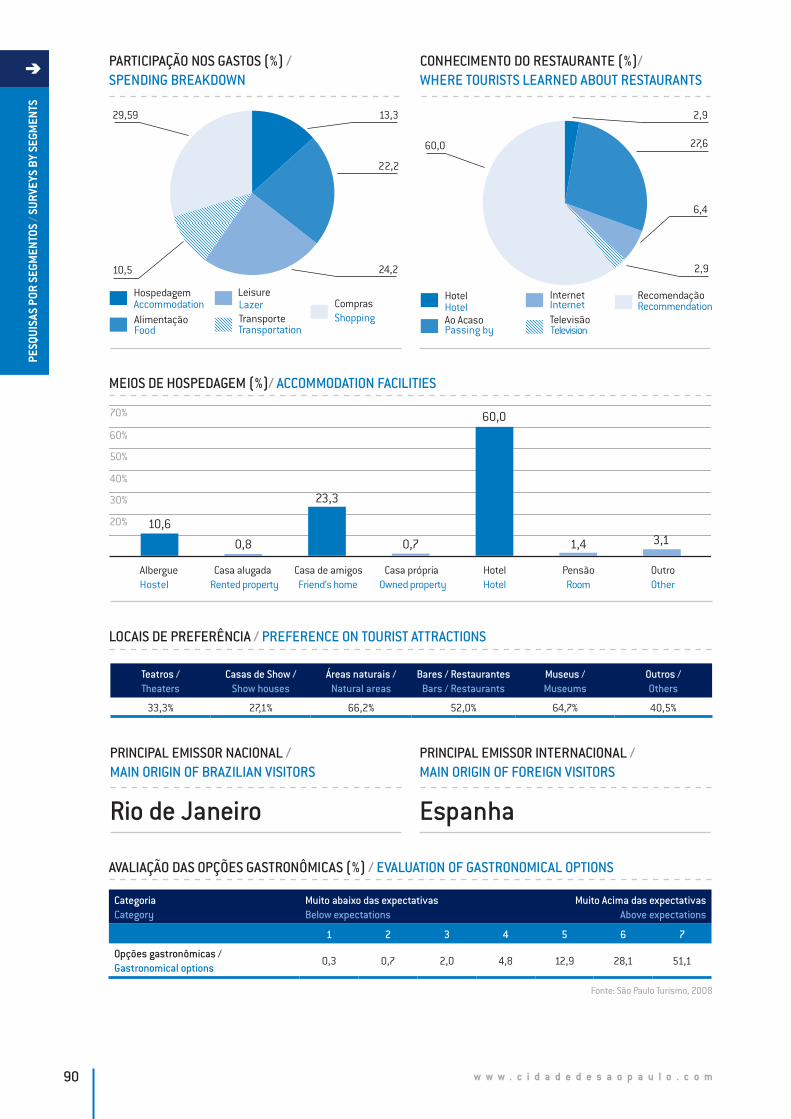

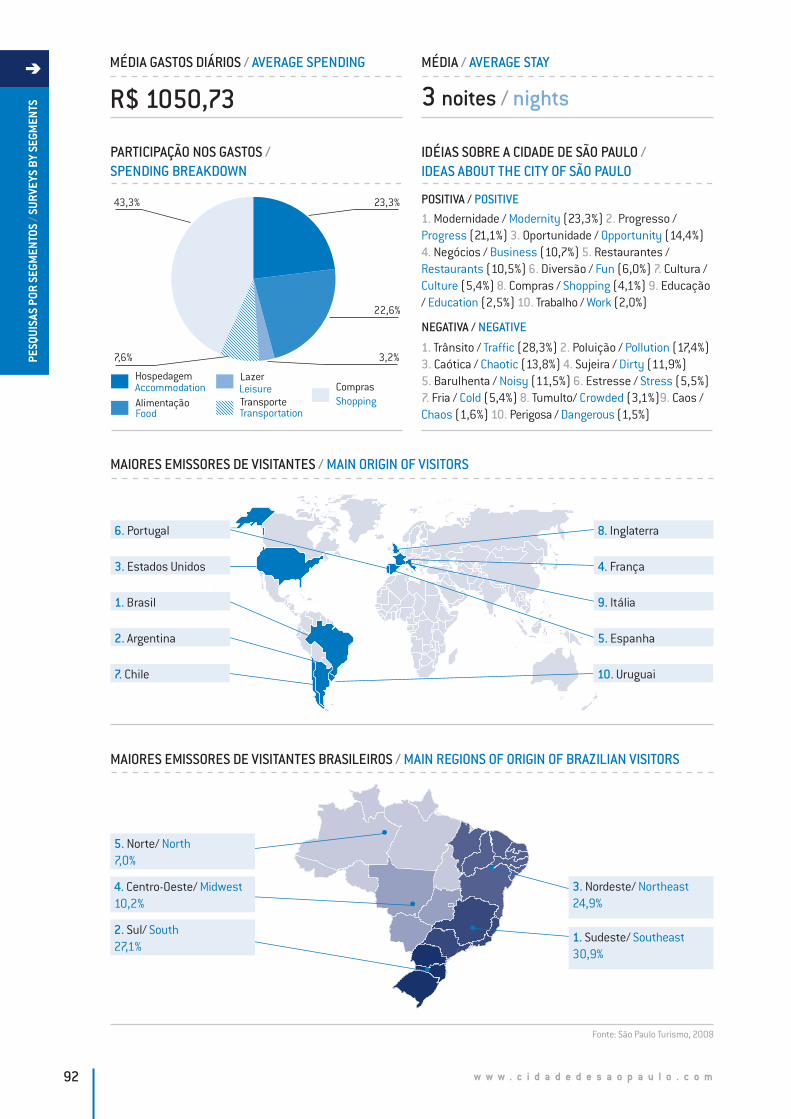

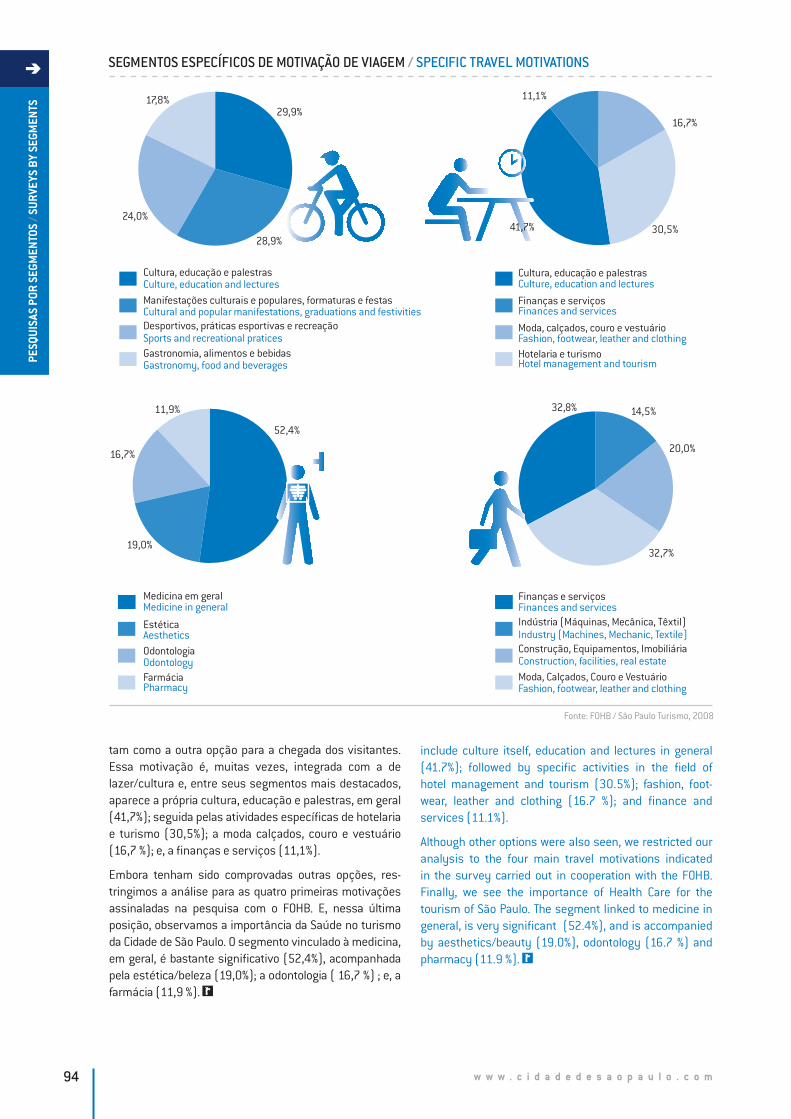

PESQUISAS POR SEGMENTOSURVEYS BY SEGMENTS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 88 GASTRONOMIA E CULTURA / GASTRONOMY AND CULTURE _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 89 NEGÓCIOS CORPORATIVOS / CORPORATE BUSINESS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 91 MOTIVAÇÃO DAS VIAGENS NOS HOTÉIS / TRAVEL MOTIVATION OF HOTEL GUESTS _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 93

Diagnósticos e Conclusões / Diagnoses and Conclusions _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 96Observações sobre a Metodologia / Remarks on the Methodology _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 98

Índi

ce

PREFEITO/MAYOR:

GILBERTO KASSAB

PRESIDENTE DA SÃO PAULO TURISMO/ PRESIDENT OF SÃO PAULO TURISMO:

CAIO LUIZ DE CARVALHO

DIRETORA DE TURISMO E ENTRETENIMENTO DA SÃO PAULO TURISMO / TOURISM AND ENTERTAINMENT DIRECTOR OF SÃO PAULO TURISMO:

LUCIANE LEITE

COORDENAÇÃO TÉCNICA / TECHNICAL COORDINATION:

BEATRIZ LAGE

DESIGN GRÁFICO / GRAPHIC DESIGN:

RENE PEROL

expe

dien

te

ASSISTENTE GRÁFICO / GRAPHIC ASSISTANT:

FÁBIO MONTANHEIRO

EQUIPE TÉCNICA / TECHNICAL TEAM:

BERNARDO IGNARRA FÁBIO MONTANHEIRO FABÍOLA BEMFEITO JULIANA CARRASCO MARÍLIA UINT MÁRIO LA TORRE FILHO

ESTAGIÁRIOS / TRAINEES:

ADRIANA GAMA ALESSANDRA TAMASHIRO ANA CAROLINA TEIXEIRA DE FREITAS FLORA RIBEIRO DA LUZ GEROLA MARIA FERNANDA PASSARELLI MARIANA ARA PESSÔA SAYEG MORITZ DIENEMANN SOLANGE VIEIRA MARQUES VINÍCIUS BRUNELLI BARBOSA

COLABORAÇÃO / COLLABORATION:

ADRIANA OMURO ADRIANO GOMES ALINE DELMANTO ANDRÉIA PIASON ANDREZZA SERRA CAMILA OCHOA CAROLINA NEGRI CRISTINA ROLLO EDILSON FRANCISCO CAVICHIA FERNANDA ASCAR DE ALBUQUERQUE JANAÍNA TRENTIN LÚCIA REGINA LUCIANA CANTO LUIS PASCUZZI MARISA MARROCOS RAQUEL VETTORI RODRIGO SUTÃO LIMA ALVES SÉRGIO PORTO THELMA GHOBRIL VANESSA JAENICK

REVISÃO DE TEXTOS / PROOFREADING OF TEXTS:

JUROTRANS TRADUÇÕES

TRADUÇÃO / TRANSLATION

BTS TRADUÇÕES

ENTIDADES ENVOLVIDAS / INSTITUTIONS INVOLVED

CONSELHO MUNICIPAL DE TURISMO DA CIDADE DE SÃO PAULO – COMTUR EMPRESA BRASILEIRA DE INFRA-ESTRUTURA AEROPORTUÁRIA – INFRAERO FÓRUM DOS OPERADORES HOTELEIROS DO BRASIL - FOHB FUNDAÇÃO INSTITUTO DE PESQUISAS ECONÔMICAS – FIPE INSTITUTO BRASILEIRO DE GEOGRAFIA E ESTATÍSTICA – IBGE INTERNATIONAL CONGRESS AND CONVENTION ASSOCIATION – ICCA SÃO PAULO CONVENTION & VISITORS BUREAU – SPC&VB SÃO PAULO TURISMO S/A – SPTURIS SECRETARIA MUNICIPAL DE FINANÇAS – SMF SECRETARIA MUNICIPAL DO VERDE E MEIO AMBIENTE – SMVMA SOCICAM – TERMINAL DE PASSAGEIROS

UNIÃO BRASILEIRA DE PROMOTORES DE FEIRAS – UBRAFE

INSTITUIÇÕES DE ENSINO SUPERIOR/ INSTITUTIONS OF HIGHER EDUCATION

CENTRO FEDERAL DE EDUCAÇÃO TECNOLÓGICA DE SÃO PAULO – CEFET-SP CENTRO UNIVERSITÁRIO NOVE DE JULHO – UNINOVE CENTRO UNIVERSITÁRIO SENAC – SP UNIVERSIDADE ANHEMBI MORUMBI – UAM UNIVERSIDADE CRUZEIRO DO SUL – UNICSUL UNIVERSIDADE PAULISTA – UNIP

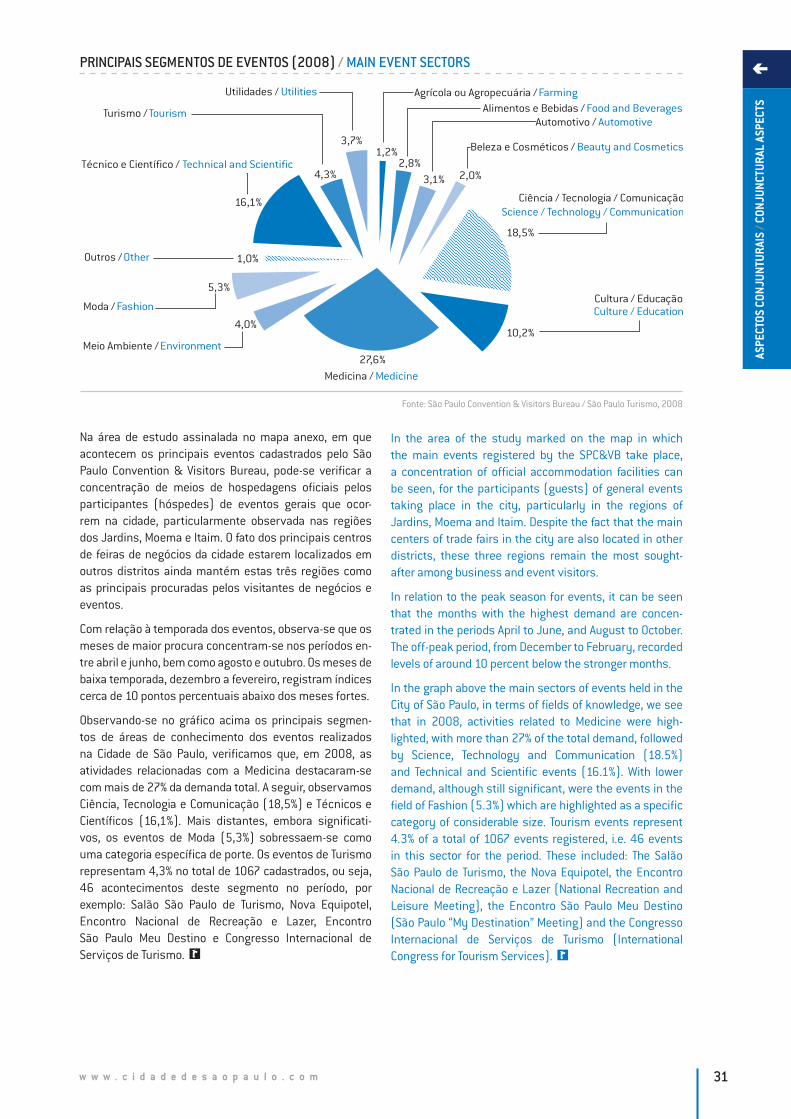

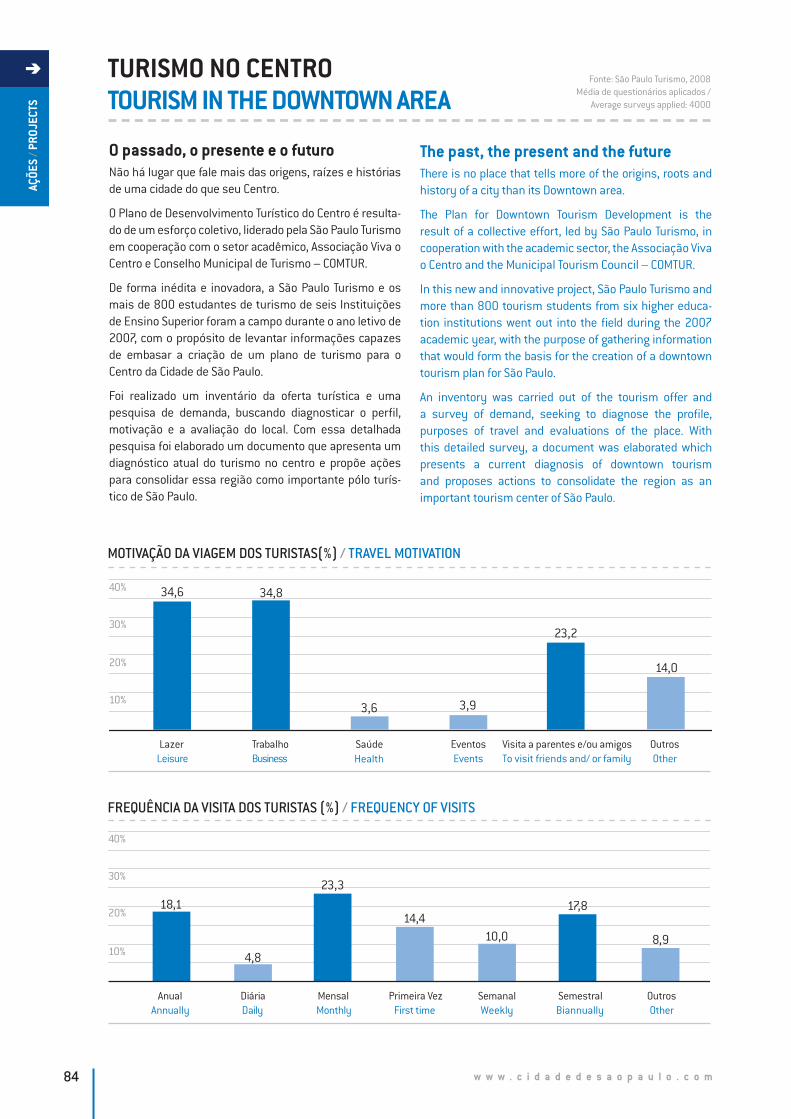

A publicação institucional “Indicadores e Pesquisas do Turismo na Cidade de São Paulo” é a primeira coletânea de resultados das pesquisas desenvolvidas pela São Paulo Turismo, de 2005 a 2008, abrangendo um conjunto de informações quantitativas e qualitativas sobre o desempenho do turismo na Cidade de São Paulo.

Permite uma visão espacializada da oferta turística em áreas selecionadas, como parques e áreas verdes, shoppings, museus, teatros e centros culturais.

Apresenta o dimensionamento e a caracterização da demanda turística da metrópole paulistana, e dos principais indicadores do desempenho do turismo no setor hoteleiro, no fluxo aéreo local, nos terminais rodoviários, no volume do ISS, nos eventos e feiras de negócios da capital.

Disponibiliza um conjunto de indicadores básicos sobre pesquisas realizadas nos megaeventos da Cidade de São Paulo. Também oferece informações sobre o desempenho de ações internas da empresa, destacando as Centrais de Informações Turísticas (CITs), o Plano de Desenvolvimento Turístico do Centro, concluindo com pesquisas de segmentos específicos.

Esta obra agrega um conjunto de variáveis comparativas sobre o turismo que mostra toda sua magnitude e relacionamento com os demais setores da Cidade de São Paulo.IN

TROD

UÇÃO

FORE

WOR

D

The institutional publication “Indicadores e Pesquisas do Turismo na Cidade de São Paulo” (Tourism Indicators and Research in the City of São Paulo) is the first collection of results of surveys carried out by São Paulo Turismo between 2005 and 2008, covering a range of quantitative and qualitative information about tourism performance in the City of São Paulo.

It gives a specialized view of thetourism related products in selected areas, such as parks and green areas, shopping centers, museums, theaters and cultural centers.

It presents the scale and nature of the tourism demand in the metropolitan area of the city, and the main tourism performance indicators for the hotel sector, use of the airports, the highway bus terminals, the volume of ISS (tax on services), and events and business fairs in the capital.

It provides a range of basic indicators derived from surveys carried out at mega-events in the City of São Paulo. It also offers information about the performance of internal actions of the company, highlighting the Tourist Information Centers (CITs) and the “Plano de Desenvolvimento Turistíco do Centro” (Plan for Downtown Area Tourism Development), and concludes with some surveys on specific sectors.

This work combines a set of comparative variables on tourism, which shows all its magnitude and interaction with the other economic sectors of the City of São Paulo.

w w w . c i d a d e d e s a o p a u l o . c o m6

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

O MAIOR DESTINO TURÍSTICO DO PAÍSA São Paulo Turismo (SPTuris) é a empresa de promoção turística e eventos da Cidade de São Paulo. Atua no plane-jamento turístico, em pesquisas, no incentivo à criação de novos produtos e roteiros, mapeamento de atrações, estímulo a novos eventos ou consolidação daqueles com potencial turístico, relacionamento com a cadeia produ-tiva do setor, promoção do destino no Brasil e no exterior, entre múltiplas ações integradas.

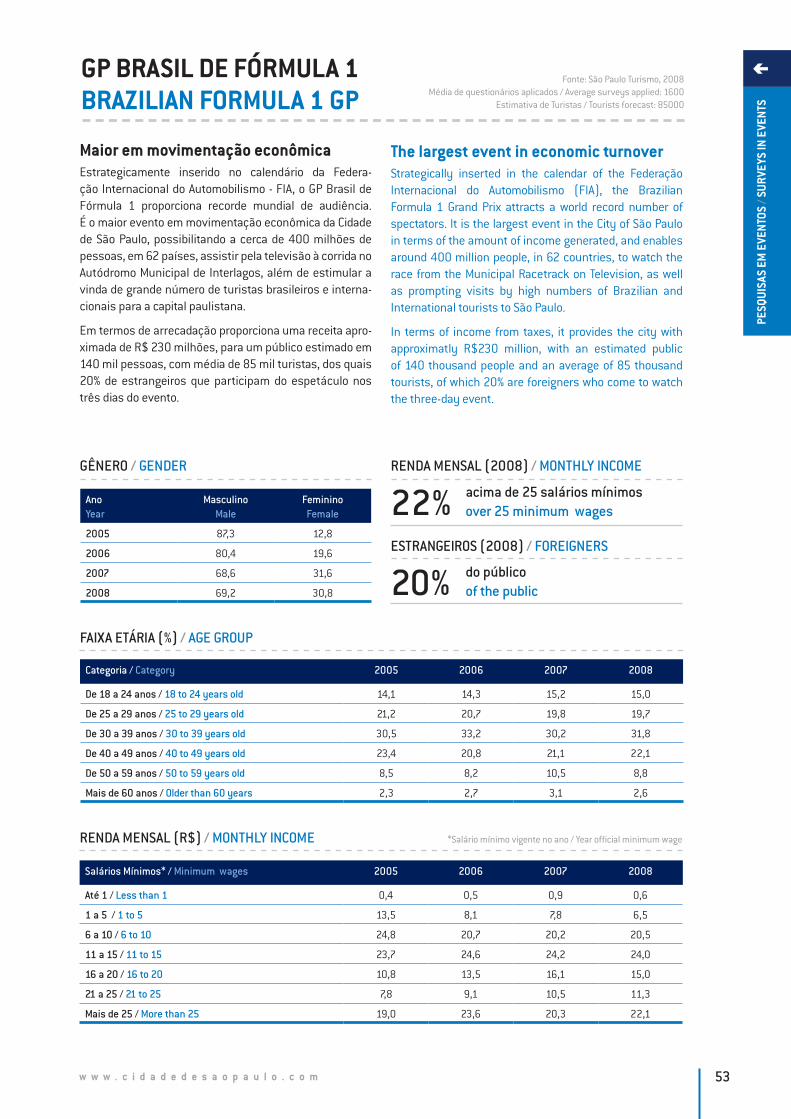

Com o posicionamento da cidade como grande pólo de lazer e entretenimento, a SPTuris contabiliza resultados favoráveis que revelam a grandeza de São Paulo como des-tino turístico. Chega ao final de 2008 com a perspectiva de receber 11 milhões de turistas anuais, e com indicado-res inéditos nas taxas de ocupação hoteleira, em média de 70%, e elevado crescimento na receita por quarto de hotel ocupado. Em termos de arrecadação anual de ISS, o setor turístico deste destino ultrapassou R$110 milhões, com um incremento de 97% desde o início da década.

São Paulo também ocupa, desde 2006, a liderança nas Américas entre as cidades que mais sediam eventos internacionais no mundo, oferecendo muitos produtos e programas na cidade como o “Turismetrô”, o “Fique Mais um Dia”, o “SP Tanque Cheio”, o “Plano de Desenvolvimento

Turístico do Centro”, o “Projeto de Capacidade a Taxistas e Guias de Turismo”, além do material de apoio para o trade como o “Manual de Capacitação Destino São Paulo”, o “São Paulo Saúde – Guia de Turismo Médico e Bem-Estar” e o “Manual Turismo de Negócios e de Incentivo”.

Como empresa de eventos, a São Paulo Turismo coor-dena a realização e, por vezes, também a infra-estrutura dos grandes eventos da maior cidade da América Latina. Entre eles o Carnaval, a Virada Cultural, o Natal Iluminado, o Réveillon na Paulista, além de dar suporte a outros acon-tecimentos tradicionais, como a Parada GLBT, o GP Brasil de Fórmula 1, a Virada Esportiva, a Maratona Internacional de SP e outros. É atuante em eventos importantes, como na organização da infra-estrutura na visita do Papa Bento 16 à Cidade de São Paulo em 2007, bem como na preparação do dossiê paulistano para a Copa Mundial de 2014.

É ainda a responsável pela administração do Anhembi Parque e de seus espaços, como o Pavilhão de Exposições, Palácio de Convenções, Sambódromo, Arena e Auditório Elis Regina, assim como do Autódromo de Interlagos.

Conheça mais sobre o turismo e os eventos em São Paulo nos sites: www.spturis.com, www.cidadedesaopaulo.com e www.anhembi.com.br.

São Paulo Turismo (SPTuris) is the tourism and events promotion company of the City of São Paulo. Its activities include tourism planning, surveys, providing incentives for the creation of new products and sightseeing, mapping the attractions, promoting new events or consolidating those with tourism potential, liaising with the production chain of the sector and promoting the destination in Brazil and abroad, among many other integrated actions. With the city’s position as the capital of leisure and entertainment, SPTuris has seen favorable results that demonstrate the greatness of São Paulo as a tourism destination. By the end of 2008, the city expects to have received 11 million tourists per year, with all-time high indicators with regard to hotel occupancy rates – around 70% - and a high growth rate in view of income per occupied hotel room. The amounts collected annually in ISS for the tourism sector in this destination was worth more than R$110 million, with an increase of 97% since the start of the decade.

São Paulo has also occupied, since 2006, the leading position in the Americas in the world-wide ranking of cities hosting the highest number of international events, offering more products and programs in the city, such as “Turismetrô”, “Fique Mais um Dia”, “SP Tanque Cheio”, the Downtown Area Tourism Development plan, and the Project to train Taxi Drivers and Tour Guides, and provi-ding support material for the trade, such as the “Manual

de Capacitação Destino São Paulo” (Destination São Paulo Training Manual), and “São Paulo Saúde – Guia de Turismo Médico e Bem-Estar” (São Paulo Health – Guide to Medical and Well-Being Tourism).

As an event company, São Paulo Turismo coordinates the organization and sometimes also the infrastructure for major events held in Latin America’s largest city. These include the Carnival, the “Virada Cultural”, the Christmas Lights, and the New Year celebrations in the capital, as well as providing support for other traditional events, such as the GLBT Parade, the Brazilian Formula 1 Grand Prix, the “Virada Esportiva” sporting event, the São Paulo Inter- national Marathon, and others. São Paulo Turismo was involved in major events, such as the organization of infrastructure for the visit of Pope Benedict XVI to the City of São Paulo in 2007, and the preparations of São Paulo’s bid dossier for the 2014 World Cup. It is also responsible for administrating the Anhembi Parque convention center and its different spaces, including the Pavilhão de Exposições, the Palácio de Convenções, Sambadrome, the Arena and the Elis Regina Auditorium, as well as the Inter-lagos Race Track.

Learn more about tourism and events in São Paulo, at the following websites: www.spturis.com, www.cidadedesaopaulo.com and www.anhembi.com.br.

THE GREATEST TOURISM DESTINATION IN THE COUNTRY

w w w . c i d a d e d e s a o p a u l o . c o m 7

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

1

1

2

3

4

1

7

6

5

23

10

45

6

10

7

9 814

13

12

11

19

20181716

15

23 2221

25 24

26

11

9

81

23

7 8

1

2

3

4

5

6

78

9

1011

1213

21

22

23

2420

25

26

27

28 31

1914

18 8

30

15

1716

9

105

46

2

3

4

6

7

8

9

10

12

13

14

15

16

17

18115

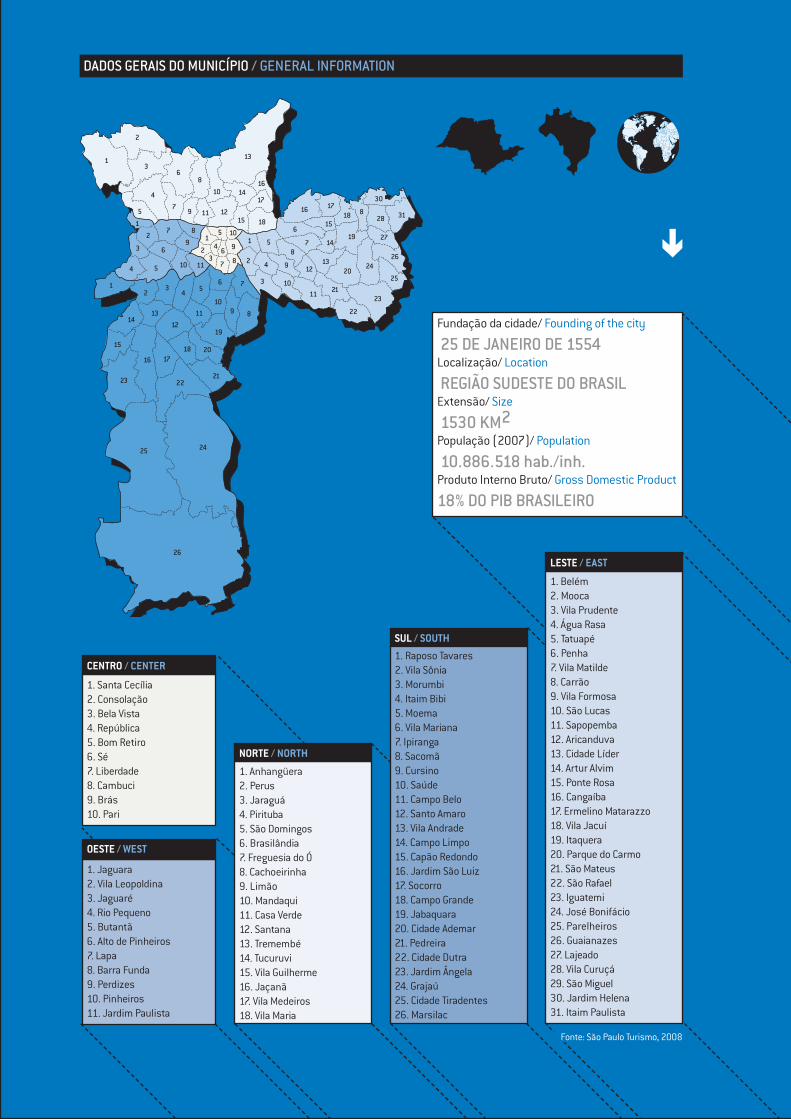

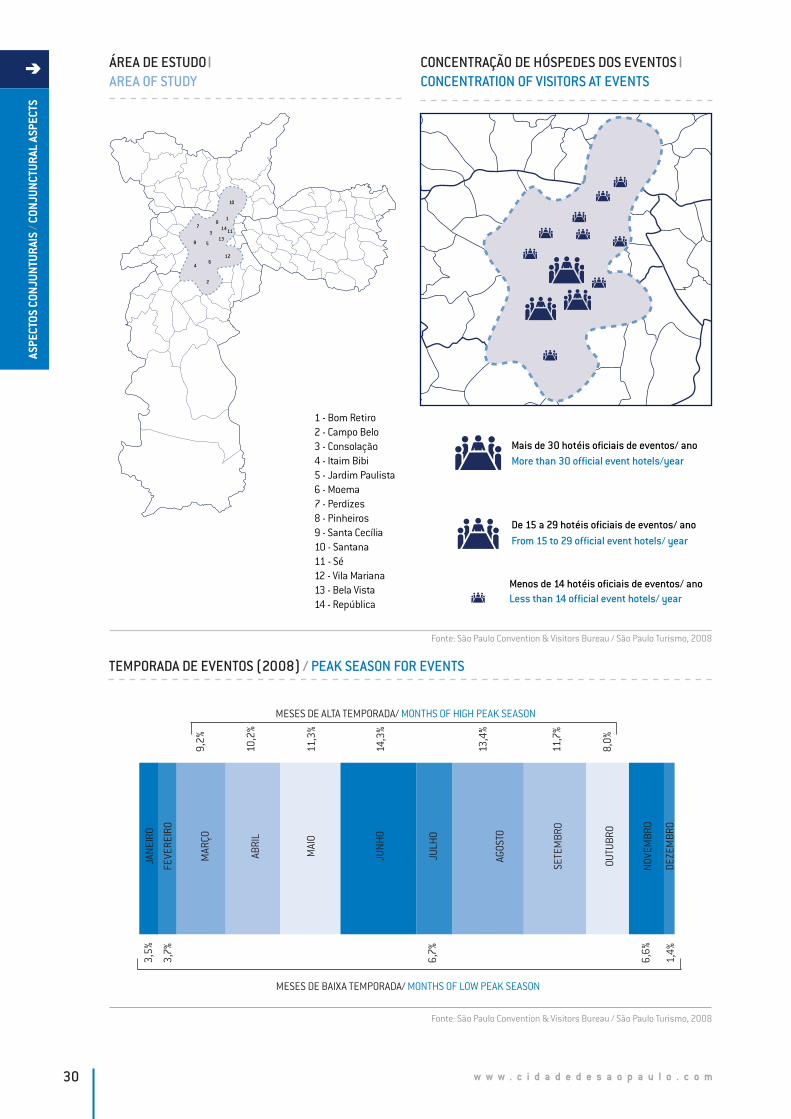

DADOS GERAIS DO MUNICÍPIO / GENERAL INFORMATION

1. Belém 2. Mooca 3. Vila Prudente 4. Água Rasa 5. Tatuapé 6. Penha 7. Vila Matilde 8. Carrão 9. Vila Formosa 10. São Lucas 11. Sapopemba 12. Aricanduva 13. Cidade Líder 14. Artur Alvim 15. Ponte Rosa 16. Cangaíba 17. Ermelino Matarazzo 18. Vila Jacuí 19. Itaquera 20. Parque do Carmo 21. São Mateus 22. São Rafael 23. Iguatemi 24. José Bonifácio 25. Parelheiros 26. Guaianazes 27. Lajeado 28. Vila Curuçá 29. São Miguel 30. Jardim Helena 31. Itaim Paulista

1. Raposo Tavares 2. Vila Sônia 3. Morumbi 4. Itaim Bibi 5. Moema 6. Vila Mariana 7. Ipiranga 8. Sacomã 9. Cursino 10. Saúde 11. Campo Belo 12. Santo Amaro 13. Vila Andrade 14. Campo Limpo 15. Capão Redondo 16. Jardim São Luiz 17. Socorro 18. Campo Grande 19. Jabaquara 20. Cidade Ademar 21. Pedreira 22. Cidade Dutra 23. Jardim Ângela 24. Grajaú 25. Cidade Tiradentes 26. Marsilac

1. Anhangüera 2. Perus 3. Jaraguá 4. Pirituba 5. São Domingos 6. Brasilândia 7. Freguesia do Ó 8. Cachoeirinha 9. Limão 10. Mandaqui 11. Casa Verde 12. Santana 13. Tremembé 14. Tucuruvi 15. Vila Guilherme 16. Jaçanã 17. Vila Medeiros 18. Vila Maria

1. Santa Cecília 2. Consolação 3. Bela Vista 4. República 5. Bom Retiro 6. Sé 7. Liberdade 8. Cambuci 9. Brás 10. Pari

1. Jaguara 2. Vila Leopoldina 3. Jaguaré 4. Rio Pequeno 5. Butantã 6. Alto de Pinheiros 7. Lapa 8. Barra Funda 9. Perdizes 10. Pinheiros 11. Jardim Paulista

Fundação da cidade/ Founding of the city

25 DE JANEIRO DE 1554Localização/ Location

REGIÃO SUDESTE DO BRASILExtensão/ Size

1530 KM2População (2007)/ Population

10.886.518 hab./inh.Produto Interno Bruto/ Gross Domestic Product

18% DO PIB BRASILEIRO

CENTRO / CENTER

OESTE / WEST

NORTE / NORTH

SUL / SOUTH

LESTE / EAST

Fonte: São Paulo Turismo, 2008

w w w . c i d a d e d e s a o p a u l o . c o m8

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

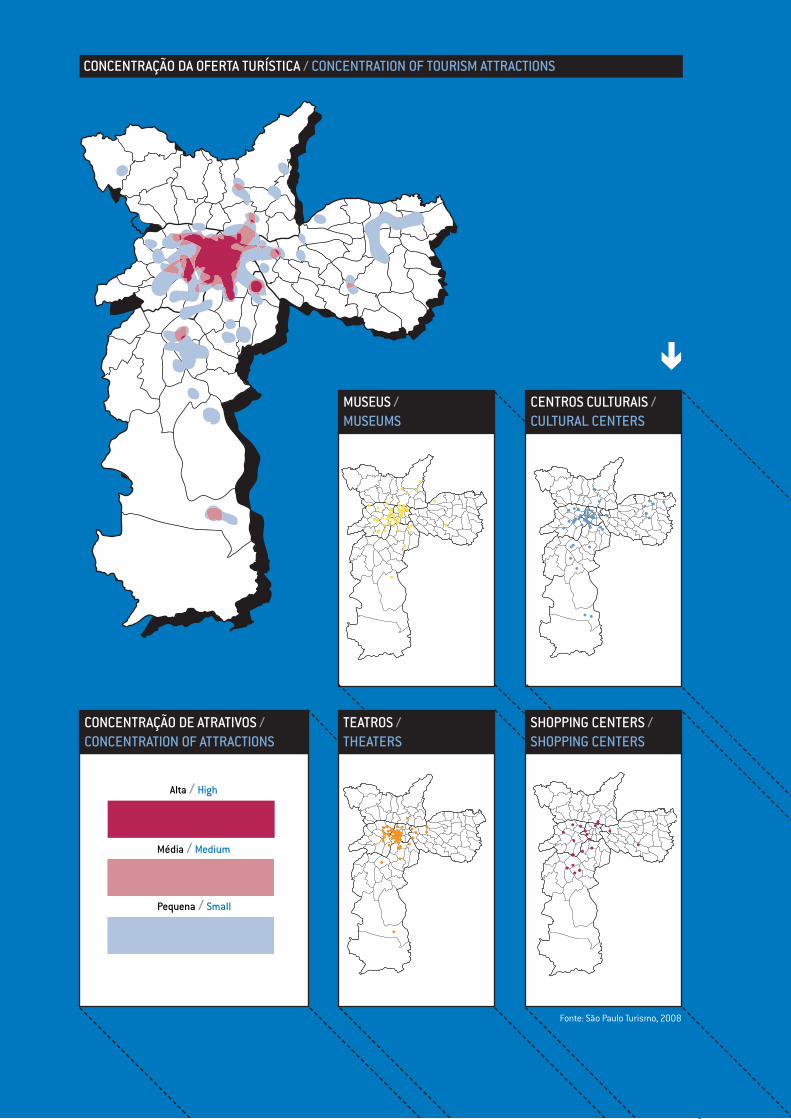

Um bem-sucedido destino turísticoSão Paulo não é apenas o maior centro econômico da América Latina. É a capital da cultura, da moda, do entretenimento e conhecimento da região. Formada por mais de 70 nacionalidades com brasileiros de todas as regiões, a capital paulista é constituída por uma diver-sidade turística. Sua oferta é composta por atrativos diferenciados e dirigida aos principais segmentos de visi-tantes, com equipamentos e serviços dos mais completos, além de uma infra-estrutura de apoio adequada tanto aos moradores quanto a todos que a visitam.

Hoje, a cidade é reconhecida como um dos destinos mun-diais da sofisticação, do entretenimento e da gastrono-mia. Reúne multiculturalismo, requinte, agitação e uma infinidade de atrações que agradam qualquer tipo de visitante. Dentre as várias opções da sua oferta turística, apresentam-se mapeados alguns de seus componentes, selecionados por sua expressiva participação no contexto geral dessa megalópole.

A successful tourism destinationSão Paulo is not only the largest economic center in Latin America, it is also the capital of culture, fashion, entertainment and knowledge of the region. Comprised of more than 70 nationalities, with Brazilians from all regions, the capital receives a wide diversity of tourists. Its offer consists of differentiated attractions and is focused on the main visitor segments, with a complete range of facilities and services, as well as a good support infra-structure both for the local inhabitants and for visitors to the city.

Today, São Paulo is recognized as a world class destina-tion for sophistication, entertainment and gastronomy. It combines multiculturalism, sophistication, liveliness, and an infinite range of attractions to suit all types of visitors. Of the various options of the city’s tourism offer, some of its components are selected and mapped due to their important role within the general context of this urban conglomeration.

45 SHOPPING CENTERSQue recebem mais de 90 milhões de pessoas por mês.

45 SHOPPING CENTERSReceiving more than 90 million people per month.

59 RUAS DE COMÉRCIO ESPECIALIZADO Do comércio luxuoso da Rua Oscar Freire e adjacentes ao comércio mais popular da Rua 25 de Março que chega a receber mais de 1 milhão de pessoas em um único dia.

59 SPECIALIZED SHOPPING STREETS From the luxurious shopping area of Rua Oscar Freire to the more popular shopping of Rua 25 de Março, which receives over a million people in a single day.

160 TEATROS Capital brasileira dos musicais, estes espetáculos realiza-dos em São Paulo recebem, em média, 25% de visitantes de várias cidades do Estado de São Paulo.

160 THEATERSAs the Brazilian capital of musicals, the shows receive on average 25% visitors from various cities of Brazil and the State

67 PARQUES E ÁREAS VERDESSão Paulo ganhou muito lazer com 12 novos parques municipais nos últimos quatro anos, e com tradicionais espaços verdes, como a área de proteção ambiental (APAs Capivari Monos e Bororé Colônia) em quase um quinto da Cidade de São Paulo.

67 PARKS AND GREEN AREAS São Paulo has gained lots of leisure areas, with 12 new municipal parks over the past four years, as well as traditional green spaces, such as the Environmental Protection Areas (EPAs) of Capivari Monos and Bororé Colônia covering almost a fifth of the city.

110 MUSEUS O Museu do Futebol criado em 2008, no Pacaembu, será um dos museus mais visitados do país. Já o Museu da Língua Portuguesa, desde a sua inauguração, vem rece-bendo mais de 1,3 milhões de visitantes.

110 MUSEUMS The Museum of Football created in 2008 in Pacaembu will become one of the most visited museums in the country, and the Museum of the Portuguese Language already is, with more than 1.3 million visitors since it first opened.

OFERTA TURÍSTICA TOURISM ATTRACTIONS

w w w . c i d a d e d e s a o p a u l o . c o m 9

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

CONCENTRAÇÃO DE ATRATIVOS / CONCENTRATION OF ATTRACTIONS

TEATROS / THEATERS

SHOPPING CENTERS / SHOPPING CENTERS

MUSEUS / MUSEUMS

CENTROS CULTURAIS / CULTURAL CENTERS

Fonte: São Paulo Turismo, 2008

Alta / High

Média / Medium

Pequena / Small

CONCENTRAÇÃO DA OFERTA TURÍSTICA / CONCENTRATION OF TOURISM ATTRACTIONS

w w w . c i d a d e d e s a o p a u l o . c o m10

THE EXTENT AND CHARACTERIZATION OF THE LEISURE AND NON-LEISURE DEMAND IN THE CITY OF SÃO PAULO IS DIVIDED INTO TWO SEGMENTS: DOMESTIC TOURISM COMING FROM CITIES WITHIN THE STATE OF SÃO PAULO AND THE REST OF BRAZIL; AND INTERNATIONAL TOURISM. A TRUE PICTURE OF THE NUMBER AND PROFILE OF THE PEOPLE WHO ARRIVE AND STAY TEMPORARILY IN THE CITY OF SÃO PAULO, ATTRACTED BY ONE OR MORE INTERESTS, CAN CONTRIBUTE A LOT TO THE PLANNING PROCESS AIMED AT THE GROWTH AND DEVELOPMENT OF TOURISM IN THIS MAJOR METROPOLIS. THE PRESENTED INFORMATION ON CHAPTER I REFFERS TO THE RESEARCH PRODUCED BY “FUNDAÇÃO INSTITUTO DE PESQUISAS ECONÔMICAS – FIPE” FOR SÃO PAULO TURISMO – SPTURIS.

DEMANDA TURÍSTICA NA CIDADE DE SÃO PAULOTOURISM DEMAND IN THE CITY OF SÃO PAULO

REPRESENTADO PELO DIMENSIONAMENTO E PELA CARACTERIZAÇÃO DA DEMANDA POR LAZER E NÃO-LAZER NA CIDADE DE SÃO PAULO, DIFERENCIADA EM DOIS SEMENTOS: O TURISMO DOMÉSTICO ORIUNDO DE CIDADES EMISSORAS DO ESTADO DE SÃO PAULO E DO BRASIL; E O TURISMO INTERNACIONAL. O CONHECIMENTO REAL DO NÚMERO E DO PERFIL DAS PESSOAS QUE CHEGAM E PER-MANECEM TEMPORARIAMENTE NA CIDADE DE SÃO PAULO, ATRAÍDAS POR UM OU MAIS INTERESSES, EM MUITO CON-TRIBUIRÁ PARA O PROCESSO DE PLANEJAMENTO DIRECIO-NADO AO CRESCIMENTO E DESENVOLVIMENTO TURÍSTICO DESSA GRANDE METRÓPOLE. OS DADOS APRESENTADOS NO CAPÍTULO I REFEREM-SE À PESQUISA REALIZADA PELA FUNDAÇÃO INSTITUTO DE PESQUISAS ECONÔMICAS – FIPE PARA A SÃO PAULO TURISMO – SPTURIS.

I/CAPÍTULO / CHAPTER

w w w . c i d a d e d e s a o p a u l o . c o m 11

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

DEMANDA TURÍSTICA DA CIDADE DE SÃO PAULOTOURISM DEMAND IN THE CITY OF SÃO PAULO

DEMANDA TURÍSTICA DA CIDADE DE SÃO PAULO (em milhões) / TOURISM DEMAND IN THE CITY OF SÃO PAULO (in millions)

Fonte de dados brutos: FIPE / São Paulo Turismo, 2008

Fonte: São Paulo Turismo, 2008

* Estimativa / Forecast

* *Estimativa / Forecast

* Assumindo US$ 1.00 = R$ 1,9015 (cotação média de 2008) / Considering US$ 1.00 = R$ 1,9015 (2008 average rate)

1,27,0 8.0 1,4 1,58,7 9,1 9,3 1,7

11,010,710,2

9,48,2

1,6

2006 2008*20072004 2005

brasileiros / Brazilians estrangeiros / foreigners total / total

11,0 milhões de turistas em São PauloA demanda turística é representada pelo conjunto de pessoas que se deslocam e pernoitam na Cidade de São Paulo por várias motivações, procedentes de outras localidades, nacionais e internacionais.

Na pesquisa do dimensionamento da demanda turística paulistana, para o período de 2005 a 2008, a São Paulo Turismo adotou como critério de avaliação a média de UH disponíveis na cidade, o número de hóspedes por apar-tamento e as taxas de ocupação assinaladas no próximo capítulo . Com base nos indicadores médios de permanên-cia, de gastos diários per capita e dos meios de hospeda-gem fornecidos por pesquisa da Fundação Instituto de Pesquisas Econômicas - FIPE “Caracterização e Dimen-sionamento da Demanda Turística do Município de São Paulo” realizada em 2008, obtidos por dados secundários, estimou-se que a demanda total da cidade (doméstica e internacional), no presente ano, foi de 11,0 milhões de turistas, com a geração de uma receita estimada em R$ 6,2 bilhões.

11.0 million tourists in São PauloTourism demand is represented by the set of people coming from other national and international locations, who travel and spend the night in the City of São Paulo for different reasons.

In the research on the size of the tourism demand in São Paulo, for the period from 2004 to 2008, São Paulo Turismo adopted, as its evaluation criteria, the average number of available Accommodation Units in the city, the number of guests per apartment and the occupancy rates given in the next chapter. Based on the average indicators for length of stay, average daily spending per capita, and types of accommodation found in the “Fundação Institu-to de Pesquisas Econômicas - FIPE” survey entitled “Characterization and Size of Tourism Demand in the City of São Paulo”, carried out in 2008 and obtained from secon-dary data, it is estimated that the total demand of the city (both domestic and international) for the current year, is 11.0 million tourists, with generation of receipts estimated at R$ 6.2 billion.

RECEITA TURÍSTICA DA CIDADE DE SÃO PAULO (em bilhões de R$) / TOURISM RECEIPTS IN THE CITY OF SÃO PAULO (in billions of R$)

1,7*3,0 3,4 1,9* 2,0*3,7 3,8 3,9 2,3*

6,26,05,3

5,74,7

2,2*

2006 2008**20072004 2005

brasileiros / Brazilians estrangeiros / foreigners total / total

w w w . c i d a d e d e s a o p a u l o . c o m12

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

CARACTERIZAÇÃO DA DEMANDA TURÍSTICA DOMÉSTICACHARACTERIZATION OF DOMESTIC TOURISM DEMAND

9,3 milhões de turistas em São PauloO estudo sobre a demanda turística doméstica da Cidade de São Paulo, apresentado pela São Paulo Turismo (SP TURIS), está baseado na pesquisa “Caracterização e Dimensionamento do Turismo Doméstico no Brasil”, rea-lizada pela Fundação Instituto de Pesquisas Econômicas - FIPE, em 2006.

O objetivo é destacar as principais características dos turistas em suas viagens domésticas para o destino pau-listano, com pelo menos um pernoite, desconsideradas as viagens de excursão e as rotineiras. São apresentados dados provenientes da amostragem de 825 casos em que São Paulo foi o principal destino da viagem comparados com outros destinos brasileiros

Com estas informações fundamentais para os investi-mentos públicos e privados do setor, com ineditismo, a Cidade de São Paulo passa a ter um amplo conhecimento da dimensão e caracterização de sua importante deman-da turística doméstica.

9.3 million tourists in São PauloThe study on domestic tourism demand in the City of São Paulo, presented by São Paulo Turismo (SPTURIS), is based on the survey “Caracterização e Dimensionamento do Turismo Doméstico no Brasil” (Characterization of the Size of Domestic Tourism in Brazil) carried out by the Fundação Instituto de Pesquisas Econômicas - FIPE, in 2006.

The objective is to highlight the main characteristics of the tourists in their domestic trips to São Paulo, staying at least one night, not including excursion and routine trips. Data is given from the sample of 825 cases, in which São Paulo was the main travel destination, compared with other Brazilian destinations.

With this basic information for public and private investments in the sector, for the first time, the City of São Paulo has a more complete picture of the size and characterization of its important domestic tourism demand.

RENDA MENSAL (R$) / MONTHLY INCOME

Salários Mínimos / Minimum wages

Até 1 / Less than 1 3,5

1 a 5 / 1 to 5 30,9

6 a 10 / 6 to 10 35,3

11 a 15 / 11 to 15 12,9

16 a 20 / 16 to 20 8,6

21 a 25 / 21 to 25 5,3

Mais de 25 / More than 25 3,5

FAIXA ETÁRIA (%) / AGE GROUP

ACOMPANHANTES (%) / COMPANIONS

Categoria / Category

De 18 a 24 anos / 18 to 24 years old 5,0

De 25 a 29 anos / 25 to 29 years old 10,9

De 30 a 39 anos / 30 to 39 years old 17,7

De 40 a 49 anos / 40 to 49 years old 25,6

De 50 a 59 anos / 50 to 59 years old 27,9

Mais de 60 anos / Older than 60 years 12,9

Categoria / Category

Sozinho / Alone 43,6

Parentes / Family members 20,6

Cônjuge / Spouse 15,9

Cônjuge e filhos / Spouse and children 13,1

Outros / Others 6,9

GÊNERO / GENDER

Fonte: Fundação Instituto de Pesquisas Econômicas (FIPE), 2006/ São Paulo Turismo, 2008Observações do banco de dados / Extract from database : 825

45,1%

54,9%

8,6 noites / nights

MÉDIA PERNOITES / AVERAGE STAY Masculino / Male Feminino / Female

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

w w w . c i d a d e d e s a o p a u l o . c o m 13

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

Outros meios de transporte/ Other means of transportation: 12,7%

MEIO DE TRANSPORTE / MEANS OF TRANSPORTATION

MEIOS DE HOSPEDAGEM (%) / ACCOMMODATION FACILITIES

Casa de amigos/ parentesHome of friends/ family

Hotel econômicoStandard hotel

Hotel midscale/ luxoMidscale/ luxury hotel

PousadaInn/ lodge

Imóvel próprio/ alugadoOwn/ rented home

OutroOther

64,1

1,1

60%

40%

20% 10,52,9

17,0

5,3

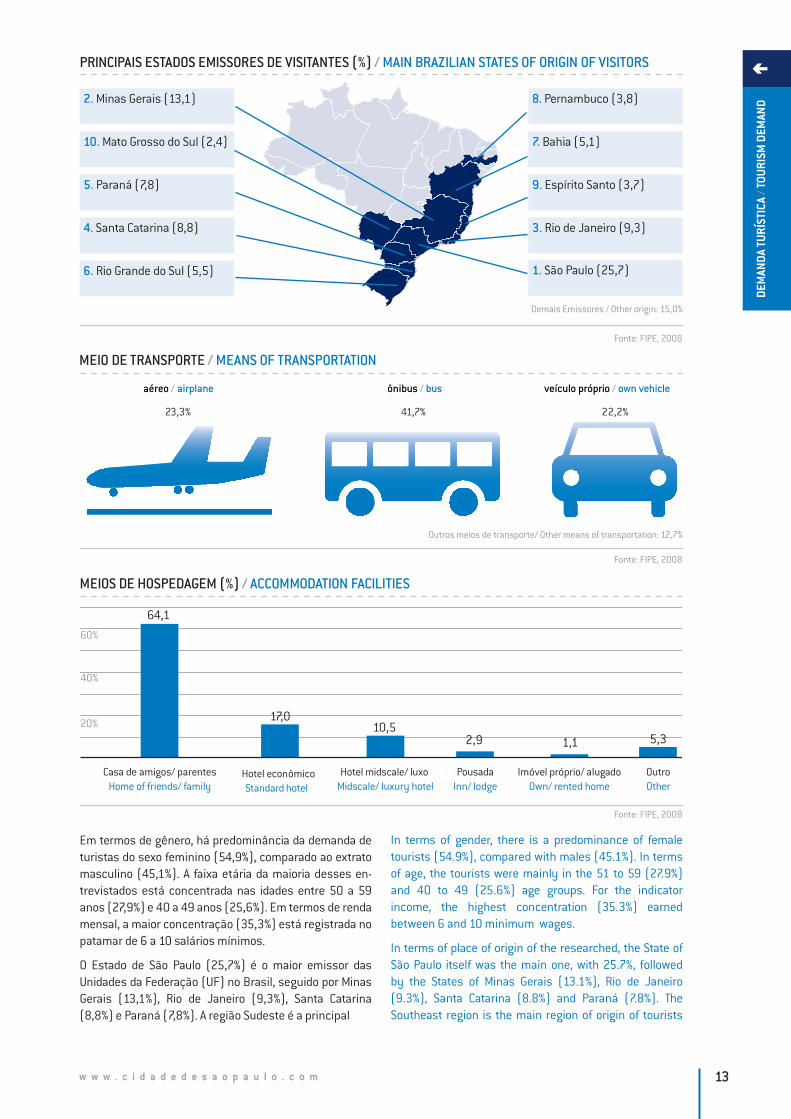

PRINCIPAIS ESTADOS EMISSORES DE VISITANTES (%) / MAIN BRAZILIAN STATES OF ORIGIN OF VISITORS

2. Minas Gerais (13,1)

10. Mato Grosso do Sul (2,4)

5. Paraná (7,8)

4. Santa Catarina (8,8)

6. Rio Grande do Sul (5,5)

8. Pernambuco (3,8)

7. Bahia (5,1)

9. Espírito Santo (3,7)

3. Rio de Janeiro (9,3)

1. São Paulo (25,7)

Demais Emissores / Other origin: 15,0%

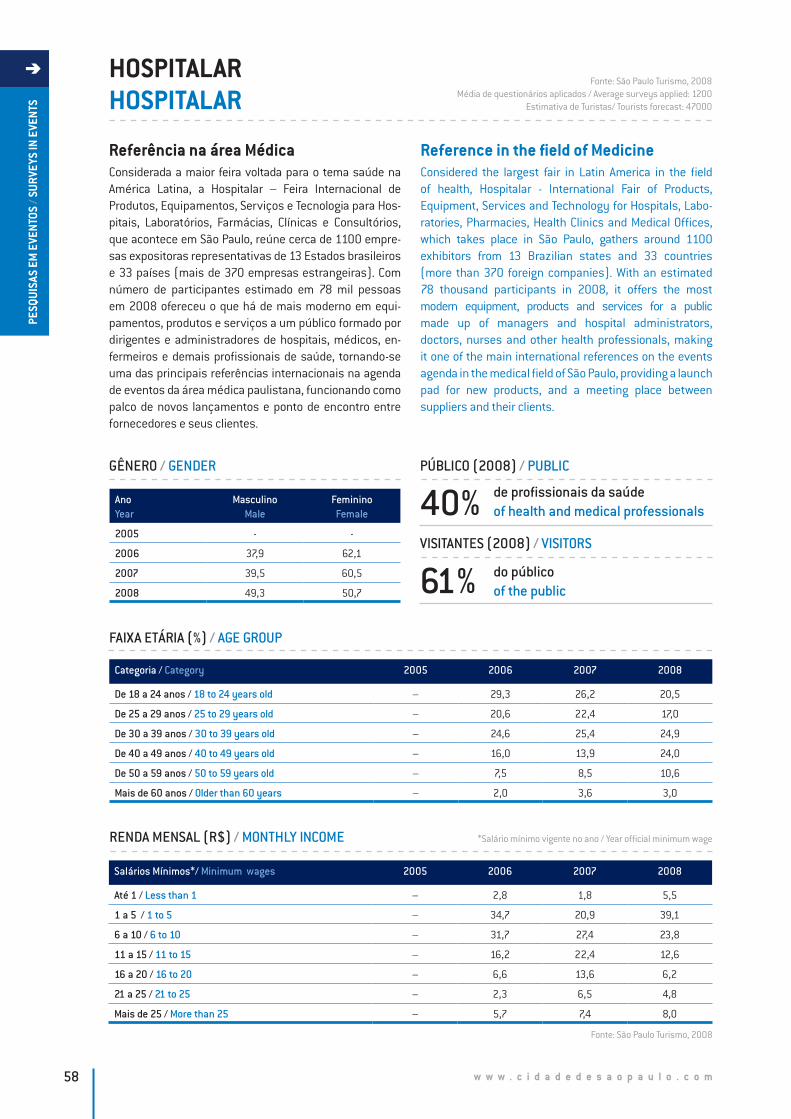

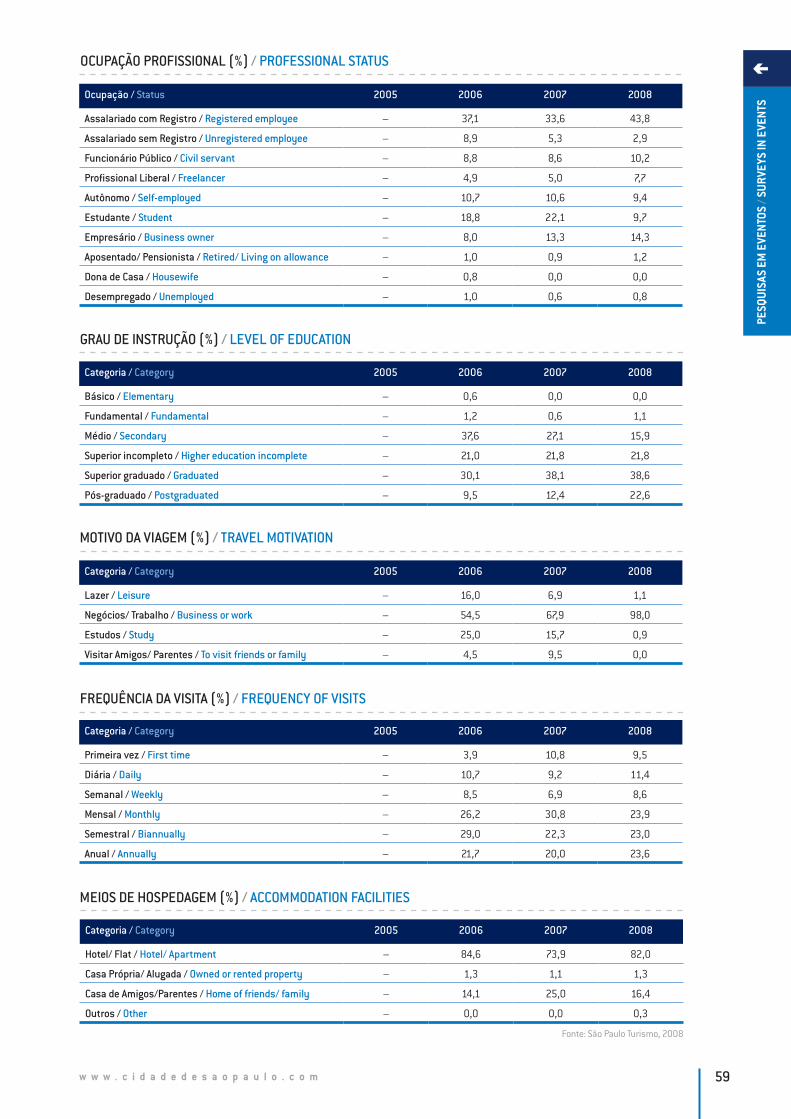

Em termos de gênero, há predominância da demanda de turistas do sexo feminino (54,9%), comparado ao extrato masculino (45,1%). A faixa etária da maioria desses en- trevistados está concentrada nas idades entre 50 a 59 anos (27,9%) e 40 a 49 anos (25,6%). Em termos de renda mensal, a maior concentração (35,3%) está registrada no patamar de 6 a 10 salários mínimos.

O Estado de São Paulo (25,7%) é o maior emissor das Unidades da Federação (UF) no Brasil, seguido por Minas Gerais (13,1%), Rio de Janeiro (9,3%), Santa Catarina (8,8%) e Paraná (7,8%). A região Sudeste é a principal

In terms of gender, there is a predominance of female tourists (54.9%), compared with males (45.1%). In terms of age, the tourists were mainly in the 51 to 59 (27.9%) and 40 to 49 (25.6%) age groups. For the indicator income, the highest concentration (35.3%) earned between 6 and 10 minimum wages.

In terms of place of origin of the researched, the State of São Paulo itself was the main one, with 25.7%, followed by the States of Minas Gerais (13.1%), Rio de Janeiro (9.3%), Santa Catarina (8.8%) and Paraná (7.8%). The Southeast region is the main region of origin of tourists

aéreo / airplane ônibus / bus veículo próprio / own vehicle

22,2%41,7%23,3%

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

w w w . c i d a d e d e s a o p a u l o . c o m14

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

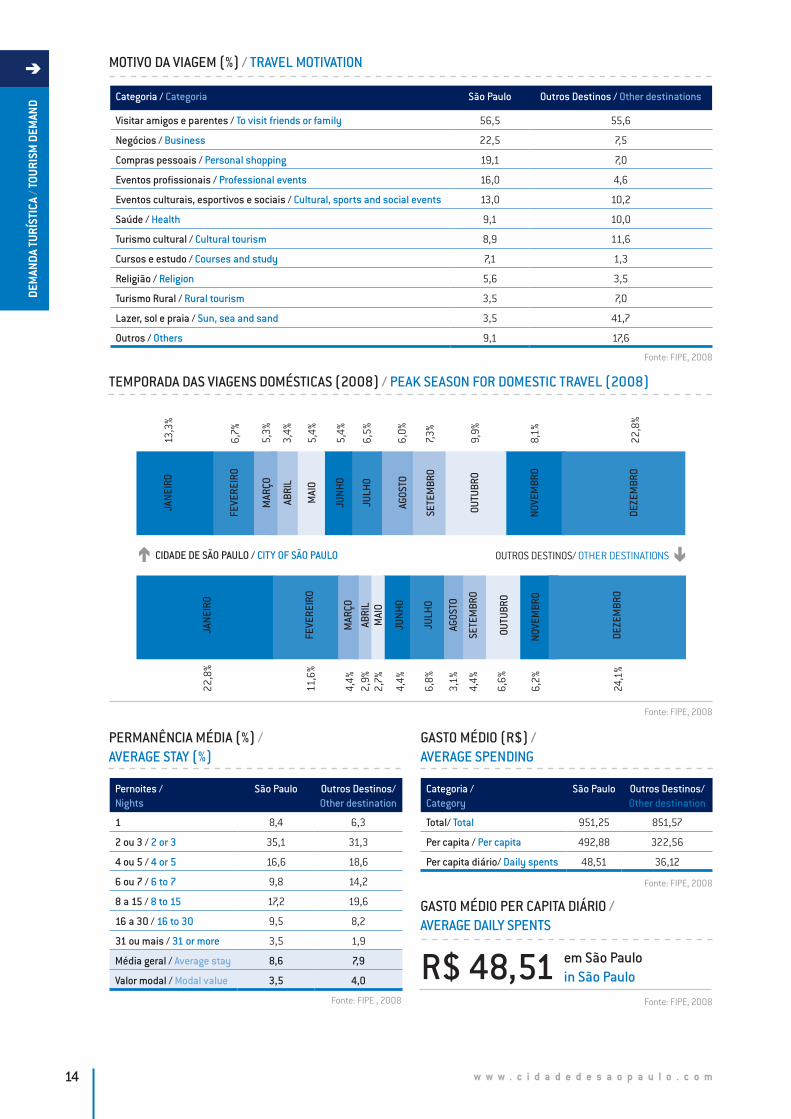

PERMANÊNCIA MÉDIA (%) / AVERAGE STAY (%)

GASTO MÉDIO (R$) / AVERAGE SPENDING

Pernoites / Nights

São Paulo Outros Destinos/Other destination

1 8,4 6,3

2 ou 3 / 2 or 3 35,1 31,3

4 ou 5 / 4 or 5 16,6 18,6

6 ou 7 / 6 to 7 9,8 14,2

8 a 15 / 8 to 15 17,2 19,6

16 a 30 / 16 to 30 9,5 8,2

31 ou mais / 31 or more 3,5 1,9

Média geral / Average stay 8,6 7,9

Valor modal / Modal value 3,5 4,0

Categoria / Category

São Paulo Outros Destinos/Other destination

Total/ Total 951,25 851,57

Per capita / Per capita 492,88 322,56

Per capita diário/ Daily spents 48,51 36,12

GASTO MÉDIO PER CAPITA DIÁRIO / AVERAGE DAILY SPENTS

R$ 48,51

MOTIVO DA VIAGEM (%) / TRAVEL MOTIVATION

Categoria / Categoria São Paulo Outros Destinos / Other destinations

Visitar amigos e parentes / To visit friends or family 56,5 55,6

Negócios / Business 22,5 7,5

Compras pessoais / Personal shopping 19,1 7,0

Eventos profissionais / Professional events 16,0 4,6

Eventos culturais, esportivos e sociais / Cultural, sports and social events 13,0 10,2

Saúde / Health 9,1 10,0

Turismo cultural / Cultural tourism 8,9 11,6

Cursos e estudo / Courses and study 7,1 1,3

Religião / Religion 5,6 3,5

Turismo Rural / Rural tourism 3,5 7,0

Lazer, sol e praia / Sun, sea and sand 3,5 41,7

Outros / Others 9,1 17,6

TEMPORADA DAS VIAGENS DOMÉSTICAS (2008) / PEAK SEASON FOR DOMESTIC TRAVEL (2008)

JANE

IRO

FEVE

REIR

O

MAR

ÇO

ABRI

LM

AIO

JUNH

O

JULH

O

AGOS

TO

SETE

MBR

O

OUTU

BRO

NOVE

MBR

O

DEZE

MBR

O

JANE

IRO

FEVE

REIR

O

MAR

ÇO

ABRI

L

MAI

O

JUNH

O

JULH

O

AGOS

TO

SETE

MBR

O

OUTU

BRO

NOVE

MBR

O

DEZE

MBR

O

OUTROS DESTINOS/ OTHER DESTINATIONSCIDADE DE SÃO PAULO / CITY OF SÃO PAULO

13,3

%

6,7%

5,3%

3,4%

5,4%

5,4%

6,0%

7,3%

6,5%

9,9%

22,8

%

8,1%

22,8

%

11,6

%

4,4%

2,9%

2,7%

4,4%

3,1%

4,4%

6,8%

6,6%

24,1

%

6,2%

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE , 2008 Fonte: FIPE, 2008

em São Pauloin São Paulo

w w w . c i d a d e d e s a o p a u l o . c o m 15

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

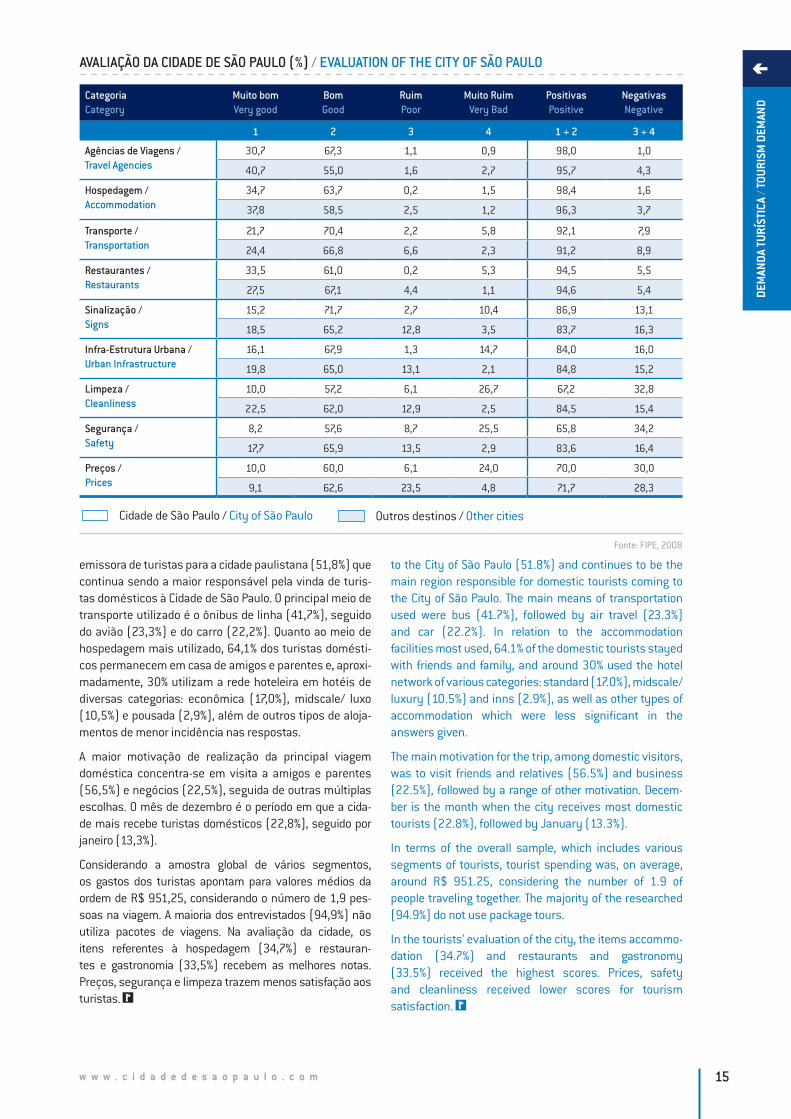

CategoriaCategory

Muito bomVery good

BomGood

RuimPoor

Muito RuimVery Bad

PositivasPositive

NegativasNegative

1 2 3 4 1 + 2 3 + 4

Agências de Viagens / Travel Agencies

30,7 67,3 1,1 0,9 98,0 1,0

40,7 55,0 1,6 2,7 95,7 4,3

Hospedagem / Accommodation

34,7 63,7 0,2 1,5 98,4 1,6

37,8 58,5 2,5 1,2 96,3 3,7

Transporte / Transportation

21,7 70,4 2,2 5,8 92,1 7,9

24,4 66,8 6,6 2,3 91,2 8,9

Restaurantes / Restaurants

33,5 61,0 0,2 5,3 94,5 5,5

27,5 67,1 4,4 1,1 94,6 5,4

Sinalização / Signs

15,2 71,7 2,7 10,4 86,9 13,1

18,5 65,2 12,8 3,5 83,7 16,3

Infra-Estrutura Urbana / Urban Infrastructure

16,1 67,9 1,3 14,7 84,0 16,0

19,8 65,0 13,1 2,1 84,8 15,2

Limpeza / Cleanliness

10,0 57,2 6,1 26,7 67,2 32,8

22,5 62,0 12,9 2,5 84,5 15,4

Segurança / Safety

8,2 57,6 8,7 25,5 65,8 34,2

17,7 65,9 13,5 2,9 83,6 16,4

Preços / Prices

10,0 60,0 6,1 24,0 70,0 30,0

9,1 62,6 23,5 4,8 71,7 28,3

AVALIAÇÃO DA CIDADE DE SÃO PAULO (%) / EVALUATION OF THE CITY OF SÃO PAULO

emissora de turistas para a cidade paulistana (51,8%) que continua sendo a maior responsável pela vinda de turis-tas domésticos à Cidade de São Paulo. O principal meio de transporte utilizado é o ônibus de linha (41,7%), seguido do avião (23,3%) e do carro (22,2%). Quanto ao meio de hospedagem mais utilizado, 64,1% dos turistas domésti-cos permanecem em casa de amigos e parentes e, aproxi-madamente, 30% utilizam a rede hoteleira em hotéis de diversas categorias: econômica (17,0%), midscale/ luxo (10,5%) e pousada (2,9%), além de outros tipos de aloja-mentos de menor incidência nas respostas.

A maior motivação de realização da principal viagem doméstica concentra-se em visita a amigos e parentes (56,5%) e negócios (22,5%), seguida de outras múltiplas escolhas. O mês de dezembro é o período em que a cida-de mais recebe turistas domésticos (22,8%), seguido por janeiro (13,3%).

Considerando a amostra global de vários segmentos, os gastos dos turistas apontam para valores médios da ordem de R$ 951,25, considerando o número de 1,9 pes-soas na viagem. A maioria dos entrevistados (94,9%) não utiliza pacotes de viagens. Na avaliação da cidade, os itens referentes à hospedagem (34,7%) e restauran-tes e gastronomia (33,5%) recebem as melhores notas. Preços, segurança e limpeza trazem menos satisfação aos turistas.

Cidade de São Paulo / City of São Paulo Outros destinos / Other cities

to the City of São Paulo (51.8%) and continues to be the main region responsible for domestic tourists coming to the City of São Paulo. The main means of transportation used were bus (41.7%), followed by air travel (23.3%) and car (22.2%). In relation to the accommodation facilities most used, 64.1% of the domestic tourists stayed with friends and family, and around 30% used the hotel network of various categories: standard (17.0%), midscale/luxury (10.5%) and inns (2.9%), as well as other types of accommodation which were less significant in the answers given.

The main motivation for the trip, among domestic visitors, was to visit friends and relatives (56.5%) and business (22.5%), followed by a range of other motivation. Decem-ber is the month when the city receives most domestic tourists (22.8%), followed by January (13.3%).

In terms of the overall sample, which includes various segments of tourists, tourist spending was, on average, around R$ 951.25, considering the number of 1.9 of people traveling together. The majority of the researched (94.9%) do not use package tours.

In the tourists’ evaluation of the city, the items accommo- dation (34.7%) and restaurants and gastronomy (33.5%) received the highest scores. Prices, safety and cleanliness received lower scores for tourism satisfaction.

Fonte: FIPE, 2008

w w w . c i d a d e d e s a o p a u l o . c o m16

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

CARACTERIZAÇÃO DA DEMANDA TURÍSTICA INTERNACIONALCHARACTERIZATION OF INTERNATIONAL TOURISM DEMAND

Fonte: Fundação Instituto de Pesquisas Econômicas (FIPE), 2008/ São Paulo Turismo, 2008Observações do banco de dados / Extract from database: 2897

1,7 milhões de turistas internacionaisO detalhamento dos resultados específicos sobre a demanda turística internacional da Cidade de São Paulo está baseado na pesquisa “Caracterização e Dimensiona-mento do Turismo Internacional no Brasil” realizada pela Fundação Instituto de Pesquisas Econômicas - FIPE, em 2006, estimando 15% de estrangeiros, em média. Objeti-va destacar dados provenientes da amostragem de 2897 casos em que São Paulo foi o destino principal da viagem comparada a outros destinos brasileiros.

1.7 million international touristsThe specific results for international tourism demand in the City of São Paulo are based on the survey “Caracte-rização e Dimensionamento do Turismo Internacional no Brasil” (Characterization and Size of International Tourism in Brazil), carried out by the Fundação Instituto de Pesquisas Econômicas - FIPE, in 2006, estimating 15% of all foreigners. Its objective is to highlight data from a sample of 2,897 cases in which São Paulo was the main destination of the trip, compared with other Brazilian des-tinations.

RENDA MENSAL (US$) / MONTHLY INCOME

Categoria / Category São Paulo

Familiar / Family 5537.45

Individual / Individual 4583.24

Categoria / Category Outros destinos / Other destination

Familiar / Family 3950.10

Individual / Individual 3037.81

FAIXA ETÁRIA (%) / AGE GROUP

Categoria / Category

De 18 a 24 anos / 18 to 24 years old 5,9

De 25 a 29 anos / 25 to 29 years old 20,3

De 30 a 39 anos / 30 to 39 years old 29,6

De 40 a 49 anos / 40 to 49 years old 26,1

De 50 a 59 anos / 50 to 59 years old 11,9

Mais de 60 anos / Older than 60 years 6,2

GÊNERO / GENDER

PERMANÊNCIA MÉDIA / AVERAGE STAY

8,5 noites / noites

77,4%

22,6%

PERMANÊNCIA MÉDIA (%) / AVERAGE STAY (%)

Pernoites / Nights

São Paulo Outros destinos / Other destination

1 7,2 3,2

2 to 5 / 2 oto 5 46,1 27,1

6 to 10 / 6 to 10 22,7 30,3

11 a 30 / 11 to 30 18,4 30,8

31 ou mais / 31 or more 5,7 8,7

Brasil / Brazil 13,6 19,2

São Paulo principal destino / Main destination

11,1 15,7

São Paulo destino secundário / Secondary destination

8,5 10,1

GASTO MÉDIO (US$) / AVERAGE SPENDING

São Paulo principal destino / Main destination

São Paulo Outros destinos/Other destination

Per capita / Per capita 957.37 856.59

Per capita diário/ Daily spents 86.25 54.56

MEIO DE ACESSO À CIDADE DE SÃO PAULO / MEANS OF ACCESS TO THE CITY OF SÃO PAULO

96,1% aéreo / airplane

Masculino / Male Feminino / Female

Fonte: FIPE, 2008

Fonte: FIPE, 2008 Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008Fonte: FIPE, 2008

w w w . c i d a d e d e s a o p a u l o . c o m 17

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

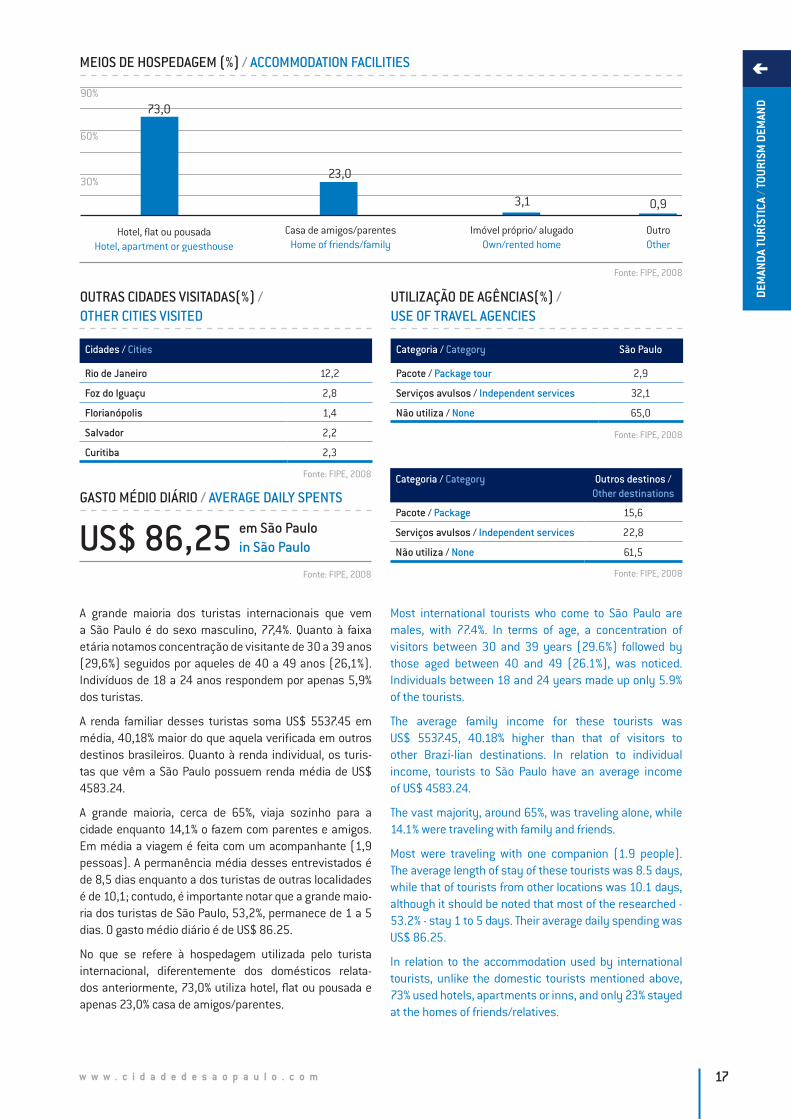

MEIOS DE HOSPEDAGEM (%) / ACCOMMODATION FACILITIES

Casa de amigos/parentesHome of friends/family

Hotel, flat ou pousadaHotel, apartment or guesthouse

Imóvel próprio/ alugadoOwn/rented home

OutroOther

73,0

3,1

90%

60%

30%23,0

0,9

A grande maioria dos turistas internacionais que vem a São Paulo é do sexo masculino, 77,4%. Quanto à faixa etária notamos concentração de visitante de 30 a 39 anos (29,6%) seguidos por aqueles de 40 a 49 anos (26,1%). Indivíduos de 18 a 24 anos respondem por apenas 5,9% dos turistas.

A renda familiar desses turistas soma US$ 5537.45 em média, 40,18% maior do que aquela verificada em outros destinos brasileiros. Quanto à renda individual, os turis-tas que vêm a São Paulo possuem renda média de US$ 4583.24.

A grande maioria, cerca de 65%, viaja sozinho para a cidade enquanto 14,1% o fazem com parentes e amigos. Em média a viagem é feita com um acompanhante (1,9 pessoas). A permanência média desses entrevistados é de 8,5 dias enquanto a dos turistas de outras localidades é de 10,1; contudo, é importante notar que a grande maio-ria dos turistas de São Paulo, 53,2%, permanece de 1 a 5 dias. O gasto médio diário é de US$ 86.25.

No que se refere à hospedagem utilizada pelo turista internacional, diferentemente dos domésticos relata-dos anteriormente, 73,0% utiliza hotel, flat ou pousada e apenas 23,0% casa de amigos/parentes.

Most international tourists who come to São Paulo are males, with 77.4%. In terms of age, a concentration of visitors between 30 and 39 years (29.6%) followed by those aged between 40 and 49 (26.1%), was noticed. Individuals between 18 and 24 years made up only 5.9% of the tourists.

The average family income for these tourists was US$ 5537.45, 40.18% higher than that of visitors to other Brazi-lian destinations. In relation to individual income, tourists to São Paulo have an average income of US$ 4583.24.

The vast majority, around 65%, was traveling alone, while 14.1% were traveling with family and friends.

Most were traveling with one companion (1.9 people). The average length of stay of these tourists was 8.5 days, while that of tourists from other locations was 10.1 days, although it should be noted that most of the researched - 53.2% - stay 1 to 5 days. Their average daily spending was US$ 86.25.

In relation to the accommodation used by international tourists, unlike the domestic tourists mentioned above, 73% used hotels, apartments or inns, and only 23% stayed at the homes of friends/relatives.

OUTRAS CIDADES VISITADAS(%) / OTHER CITIES VISITED

UTILIZAÇÃO DE AGÊNCIAS(%) / USE OF TRAVEL AGENCIES

Cidades / Cities

Rio de Janeiro 12,2

Foz do Iguaçu 2,8

Florianópolis 1,4

Salvador 2,2

Curitiba 2,3

Categoria / Category São Paulo

Pacote / Package tour 2,9

Serviços avulsos / Independent services 32,1

Não utiliza / None 65,0

Categoria / Category Outros destinos / Other destinations

Pacote / Package 15,6

Serviços avulsos / Independent services 22,8

Não utiliza / None 61,5

GASTO MÉDIO DIÁRIO / AVERAGE DAILY SPENTS

US$ 86,25 em São Pauloin São Paulo

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

w w w . c i d a d e d e s a o p a u l o . c o m18

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

CategoriaCategory

Muito bomVery good

BomGood

RuimPoor

Muito RuimVery Bad

PositivasPositive

NegativasNegative

1 2 3 4 1 + 2 3 + 4

Limpeza/ Cleanliness

7,6 58,9 27,7 5,8 66,5 33,5

22,4 58,5 16,1 3,0 80,9 19,1

Segurança pública / Public safety

5,1 56,6 27,8 10,5 61,7 38,3

18,8 61,0 15,8 4,4 83,6 16,4

Serviço de táxi / Taxi service

21,0 72,5 5,1 1,4 93,5 6,5

21,2 67,5 9,0 2,3 88,7 11,3

Transporte público / Public transportation

20,7 59,7 14,8 4,8 80,4 19,6

21,9 61,7 12,0 4,4 83,6 16,4

Telefonia e internet / Telephone and internet

15,9 64,9 15,6 3,7 80,8 19,2

15,6 62,6 16,6 5,2 78,2 21,8

Sinalização / Signs

7,9 58,8 27,2 6,2 66,7 33,4

14,7 61,2 18,8 5,2 75,9 24,1

Aeroporto / Airport

14,3 72,6 1,4 11,6 86,9 13,0

17,7 68,0 11,7 2,7 85,7 14,4

Rodovias / Highways

9,1 53,5 31,1 6,3 62,6 37,4

11,1 53,5 26,2 9,3 64,6 35,5

Restaurantes / Restaurants

47,2 50,9 1,7 0,3 98,1 1,9

31,4 62,9 5,2 0,6 94,3 5,7

Alojamento / Accommodation

42,4 55,2 2,1 0,3 97,6 2,4

37,7 57,0 4,8 0,5 94,7 5,3

Diversão Noturna / Nightlife

41,5 55,3 2,8 0,4 96,8 3,2

33,4 55,4 9,2 2,0 88,8 11,2

Guias de turismo / Tourism guides

22,1 64,3 9,9 3,6 86,4 13,5

32,5 58,1 7,7 1,7 90,6 9,4

Informações turísticas / Tourist information

16,2 66,9 14,2 2,7 83,1 16,9

22,5 63,2 11,9 2,4 85,7 14,3

Hospitalidade do povo / Hospitality of the people

62,7 36,0 1,1 0,2 98,7 1,3

62,0 35,9 1,8 0,3 97,9 2,1

Gastronomia / Gastronomy

54,3 43,8 1,6 0,4 98,1 1,9

43,6 50,7 5,2 0,5 94,3 5,7

Preços / Prices

15,3 57,3 23,0 4,4 72,6 27,4

13,9 53,5 26,3 6,4 67,4 32,7

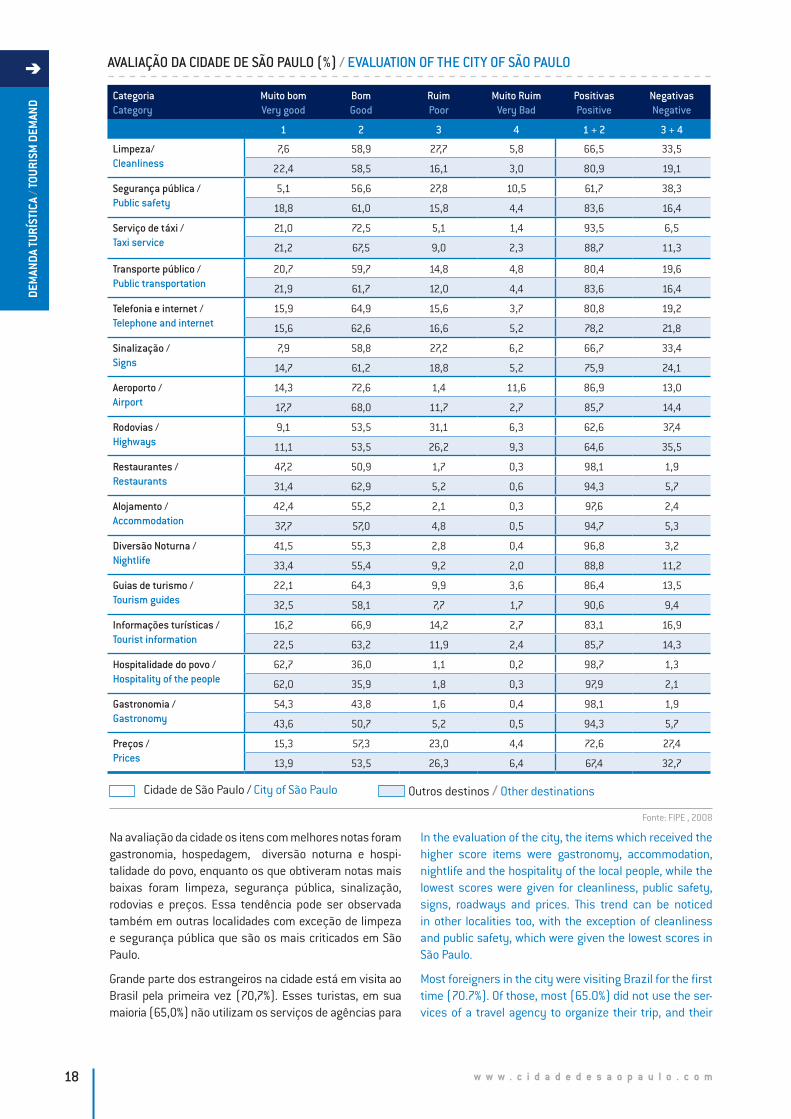

AVALIAÇÃO DA CIDADE DE SÃO PAULO (%) / EVALUATION OF THE CITY OF SÃO PAULO

In the evaluation of the city, the items which received the higher score items were gastronomy, accommodation, nightlife and the hospitality of the local people, while the lowest scores were given for cleanliness, public safety, signs, roadways and prices. This trend can be noticed in other localities too, with the exception of cleanliness and public safety, which were given the lowest scores in São Paulo.

Most foreigners in the city were visiting Brazil for the first time (70.7%). Of those, most (65.0%) did not use the ser-vices of a travel agency to organize their trip, and their

Na avaliação da cidade os itens com melhores notas foram gastronomia, hospedagem, diversão noturna e hospi-talidade do povo, enquanto os que obtiveram notas mais baixas foram limpeza, segurança pública, sinalização, rodovias e preços. Essa tendência pode ser observada também em outras localidades com exceção de limpeza e segurança pública que são os mais criticados em São Paulo.

Grande parte dos estrangeiros na cidade está em visita ao Brasil pela primeira vez (70,7%). Esses turistas, em sua maioria (65,0%) não utilizam os serviços de agências para

Cidade de São Paulo / City of São Paulo Outros destinos / Other destinations

Fonte: FIPE , 2008

w w w . c i d a d e d e s a o p a u l o . c o m 19

DEM

ANDA

TUR

ÍSTI

CA /

TOUR

ISM

DEM

AND

MAIORES EMISSORES DE ESTRANGEIROS / MAIN COUNTRIES OF ORIGIN OF FOREIGN VISITORS

10. México

8. Inglaterra

5. Chile

2. Argentina

1. Estados Unidos

6. Itália

3. Alemanha

5. Portugal

7. Espanha

4. França

MOTIVO DA VIAGEM (%) / TRAVEL MOTIVATION

MOTIVAÇÕES LIGADAS AO LAZER (%) / MOTIVATIONS RELATED TO LEISURE

Categoria / Category

São Paulo Outros Destinos/Other destination

Negócios ou trabalho / Business or work 57,2 17,6

Visitar amigos ou parentes / To visit friends or family 20,7 25,6

Lazer / Leisure 13,6 50,3

Congressos,feiras e convenções / Congresses, fairs and conventions 4,4 3,2

Outros / Other 3,1 3,4

Categoria / Category

São Paulo Outros Destinos/Other destination

Cultura / Culture 36,3 14,8

Lazer, sol e praia / Sun, sea and sand 28,2 57,4

Natureza ou ecoturismo / Nature or ecotourism 18,4 19,6

Esportes / Sports 9,8 2,7

Diversão Noturna / Nightlife 3,6 1,3

Viagem de incentivo / Incentive trip 0,9 1,2

Outros / Other 2,8 2,9

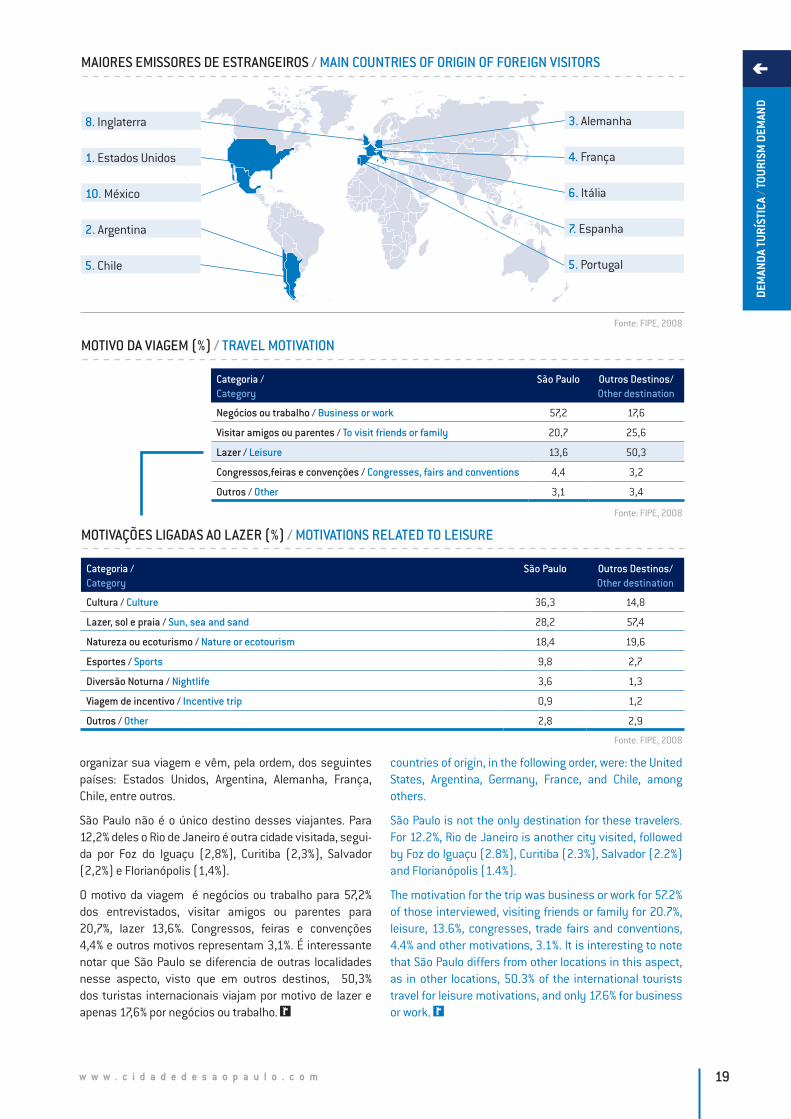

organizar sua viagem e vêm, pela ordem, dos seguintes países: Estados Unidos, Argentina, Alemanha, França, Chile, entre outros.

São Paulo não é o único destino desses viajantes. Para 12,2% deles o Rio de Janeiro é outra cidade visitada, segui-da por Foz do Iguaçu (2,8%), Curitiba (2,3%), Salvador (2,2%) e Florianópolis (1,4%).

O motivo da viagem é negócios ou trabalho para 57,2% dos entrevistados, visitar amigos ou parentes para 20,7%, lazer 13,6%. Congressos, feiras e convenções 4,4% e outros motivos representam 3,1%. É interessante notar que São Paulo se diferencia de outras localidades nesse aspecto, visto que em outros destinos, 50,3% dos turistas internacionais viajam por motivo de lazer e apenas 17,6% por negócios ou trabalho.

countries of origin, in the following order, were: the United States, Argentina, Germany, France, and Chile, among others.

São Paulo is not the only destination for these travelers. For 12.2%, Rio de Janeiro is another city visited, followed by Foz do Iguaçu (2.8%), Curitiba (2.3%), Salvador (2.2%) and Florianópolis (1.4%).

The motivation for the trip was business or work for 57.2% of those interviewed, visiting friends or family for 20.7%, leisure, 13.6%, congresses, trade fairs and conventions, 4.4% and other motivations, 3.1%. It is interesting to note that São Paulo differs from other locations in this aspect, as in other locations, 50.3% of the international tourists travel for leisure motivations, and only 17.6% for business or work.

Fonte: FIPE, 2008

Fonte: FIPE, 2008

Fonte: FIPE, 2008

w w w . c i d a d e d e s a o p a u l o . c o m20

CONSIDERED WITH REGARD TO THE EVOLUTION OF KEY INDICATORS OF THE SÃO PAULO HOTEL INDUSTRY (OCCUPANCY RATE, AVERAGE DAILY RATES, REVENUE PER AVAILABLE ROOM); MOVEMENT OF PASSENGERS AND AIRCRAFT AT THE CONGONHAS AND GUARULHOS AIRPORTS; MOVEMENT OF PASSENGERS AND VEHICLES AT THE TIETÊ, BARRA FUNDA AND JABAQUARA BUS TERMINALS; AND THE VOLUME OF SERVICE TAXES (ISS) PAID IN BY “GRUPO 13” COMPANIES, WHICH INCLUDE THE ACTIVITIES OF TOURISM, LODGING, EVENTS, AND THE LIKE. CONTAINING ALSO INFORMATION ON THE EVENTS THAT OCCUR ANNUALLY FROM 2005 TO 2008, THE CHAPTER PROVIDES A CONJUNCTURAL SCENARIO OF SOME OF THE MOST SIGNIFICANT FACTORS OF THE TOURISM SECTOR IN THE CITY OF SÃO PAULO.

ASPECTOS CONJUNTURAIS DO TURISMO PAULISTANOCONJUNCTURAL ASPECTS OF TOURISM IN SÃO PAULO

II/

CONSIDERADO PELA EVOLUÇÃO DOS PRINCIPAIS INDICA-DORES DA HOTELARIA PAULISTANA (TAXA DE OCUPAÇÃO, DIÁRIA MÉDIA, REVENUE PER AVAILABLE ROOM); DOS FLUXOS DE PASSAGEIROS E AERONAVES NOS AEROPORTOS DE CONGONHAS E GUARULHOS; DOS TERMINAIS RODOVIÁ-RIOS DE TIETÊ, BARRA FUNDA E JABAQUARA; E, DO VOLUME DO ISS ARRECADADO PELO GRUPO 13 COMPREENDIDO PELAS ATIVIDADES DE TURISMO, HOSPEDAGEM, EVENTOS E ASSEMELHADOS. TAMBÉM COM INFORMAÇÕES SOBRE OS EVENTOS QUE OCORREM ANUALMENTE, DE 2005 A 2008, O CAPÍTULO OFERECE UM CENÁRIO CONJUNTURAL DE ALGUNS DOS FATORES MAIS SIGNIFICATIVOS DO SETOR TURÍS-TICO DA CIDADE DE SÃO PAULO.

CAPÍTULO / CHAPTER

w w w . c i d a d e d e s a o p a u l o . c o m 21

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

HOTELARIAHOTEL INDUSTRY

Ocupação com crescimento inéditoA ocupação hoteleira na Cidade de São Paulo vem alcan-çando índices positivos, próximos ou superiores a 70% durante a maior parte do ano. Para se ter uma idéia, vale citar os resultados dos meses de abril, maio e junho de 2008, respectivamente 70,3%, 70,0% e 74,7%. Em 2007 os índices também foram semelhantes.

O atual desempenho diferencia-se da realidade ao final dos anos 90 e nos primeiros anos desta década, quando a ocupação mensal ficava em torno de 40%, com peque-nas variações. Nesse período, a capacidade dos hotéis da cidade era muito maior que a demanda e havia uma ociosi-dade de mais de 50% dos apartamentos disponíveis.

E, ainda, aos fins de semana, quando há tradicionalmente menos eventos e feiras de negócios na cidade, os hotéis procuram alternativas para a demanda de lazer com pa-cotes promocionais.

Confirmando o momento favorável da hotelaria paulistana, basta olhar o desempenho do setor nos últimos anos. O período de maior baixa em 2008, mais especificamente em janeiro (54,8%), representa uma taxa de ocupação pró-xima à maior alta registrada em 2004, em agosto (58,3%).

Occupancy shows record growthHotel occupancy rates in the City of São Paulo have been reaching positive levels, close to or higher than 70% for most of the year. To give an idea, the results for April, May and June 2008 were 70.3%, 70.0%, and 74.7%, respecti-vely, and the rates for 2007 were similar.

This scenario is quite different from that seen around the end of the 1990s and early years of this decade, when monthly occupancy rates were around 40%, with small fluctuations. In that period, the city’s hotel capacity was far higher than the demand, with more than 50% of hotel apartments remaining empty.

On weekends, when there are traditionally fewer events and trade fairs in the city, hotels are looking for alterna-tive sources of leisure demand, offering promotional packages.

The sector’s performance in recent years confirms the favorable trend in the São Paulo hotel industry. The period with the lowest rate in the sector for 2008 - January (54.8%), represented an occupancy rate which was close to the highest rate recorded in August 2004 (58.3%).

2005

100.0

120.0

140.0

80.0

2006 2008*2007

79,17 89,57 109,25108,56Média anual:Annual average:

REVENUE PER AVAILABLE ROOM (REVPAR EM R$) / REVENUE PER AVAILABLE ROOM

Fonte: São Paulo Turismo, 2008

2004 2005

60.0

70.0

80.0

50.0

2006 2008*2007

55,2 58,7Média anual:Annual average: 64,7 68,567,058,7

TAXA DE OCUPAÇÃO HOTELEIRA (EM %) / HOTEL OCCUPANCY RATE

Fonte: São Paulo Turismo, 2008

* Estimativa / forecast

* Estimativa / forecast

w w w . c i d a d e d e s a o p a u l o . c o m22

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

AnoYear

ZonaZone

DadoData

JanJan

FevFeb

MarMar

AbrApr

MaiMay

JunJun

JulJul

AgoAug

SetSep

OutOct

NovNov

DecDec

ZSTO 43,2 45,0 57,2 58,6 60,5 63,8 62,0 64,3 70,0 64,9 64,2 52,4

DM 147,7 147,3 142,3 161,0 163,6 157,0 158,4 143,5 150,3 135,5 154,4 148,6

ZNTO 25,9 29,1 53,5 59,5 59,7 61,3 46,6 63,5 60,3 48,3 42,0 42,5

DM 150,8 119,1 116,8 111,0 99,4 106,1 136,6 115,0 133,3 108,0 98,7 97,2

ZLTO 45,8 56,6 57,2 56,1 53,7 52,6 57,1 58,4 58,8 57,5 58,0 49,1

DM 102,3 106,3 101,0 102,3 101,4 107,9 109,5 102,9 112,8 105,1 115,0 107,9

CETO 52,3 49,3 57,1 58,3 56,4 58,0 68,6 60,8 66,1 61,1 67,1 50,3

DM 83,4 88,3 101,6 94,9 102,7 95,5 77,6 121,3 109,0 87,3 92,5 84,9

ZOTO 47,9 58,5 70,5 73,0 69,0 70,0 67,1 73,9 78,4 67,8 75,9 63,9

DM 219,1 153,2 153,3 162,4 164,8 144,1 145,4 159,8 101,2 149,9 147,0 154,6

ZSTO 42,2 43,1 55,7 59,0 61,1 60,4 62,1 65,9 71,3 62,4 65,8 53,4

DM 150,4 145,4 145,0 158,3 161,6 159,7 157,7 140,3 155,7 133,3 155,9 145,0

ZNTO 24,4 29,1 54,6 61,4 56,8 60,4 44,5 67,8 60,2 49,7 39,4 43,3

DM 149,3 120,4 117,2 111,1 97,5 106,9 137,5 115,5 133,3 104,2 99,1 99,2

ZLTO 47,7 59,0 59,7 55,1 55,5 57,4 59,7 60,5 55,7 56,7 59,7 50,8

DM 100,4 108,0 98,6 104,4 100,5 105,7 107,5 101,7 114,4 103,9 116,0 106,5

CETO 54,3 51,0 56,7 57,4 55,7 59,3 70,4 61,3 67,9 62,3 68,4 51,3

DM 84,2 89,8 102,3 96,5 104,3 97,5 77,5 122,3 106,5 90,6 90,4 86,2

ZOTO 50,9 60,0 71,2 70,6 69,8 76,7 69,0 75,8 80,9 70,6 73,5 65,7

DM 215,4 154,6 153,5 162,4 166,0 143,2 146,7 155,5 160,8 102,3 152,5 150,6

ZSTO 56,3 55,9 72,2 67,9 69,4 68,4 67,0 66,8 68,0 73,8 68,4 64,6

DM 154,3 161,7 181,3 179,6 168,5 159,5 169,3 166,0 166,7 188,4 176,1 176,7

ZNTO 52,5 44,5 48,3 55,3 60,2 64,7 63,0 64,6 68,7 54,0 57,1 57,9

DM 129,7 123,5 144,1 150,6 137,5 123,0 153,1 156,0 124,5 137,8 112,8 123,3

ZLTO 66,6 53,5 70,4 62,3 71,6 63,0 62,0 60,1 65,6 63,3 64,7 56,0

DM 123,4 126,9 123,4 156,5 126,8 130,3 131,6 129,5 130,6 139,0 129,5 133,1

CETO 57,0 81,0 64,0 66,1 68,1 62,1 63,0 64,0 57,8 68,3 65,6 60,7

DM 119,7 120,2 105,5 109,7 109,0 105,0 107,6 105,5 110,8 120,3 118,8 106,3

ZOTO 56,3 62,4 78,7 71,7 77,8 72,8 71,2 70,6 73,8 74,8 78,1 59,0

DM 186,8 136,7 225,6 140,6 132,7 148,2 203,1 167,0 141,0 148,1 142,6 141,4

ZSTO 55,4 59,9 68,1 71,5 71,3 75,7 68,1 72,8 80,4 81,8* 83,2* 84,3*

DM 177,6 182,1 167,8 174,4 184,7 185,5 181,1 182,4 194,2 197,6* 201,1* 204,1*

ZNTO 50,9 41,5 35,6 58,0 67,9 59,5 76,8 63,6 60,9 62,3* 63,9* 65,4*

DM 160,0 153,1 189,9 150,9 143,8 181,2 174,1 123,0 134,6 139,1* 145,4* 151,2*

ZLTO 56,7 54,1 67,4 72,3 64,0 74,5 59,7 82,9 76,4 75,4* 74,5* 73,6*

DM 138,1 140,3 141,7 140,0 142,4 140,2 131,7 115,7 135,6 137,2* 138,1* 140,1*

CETO 51,0 57,5 67,8 64,7 66,3 67,5 64,5 78,8 58,2 59,9* 61,8* 63,8*

DM 114,4 138,7 126,0 130,2 128,8 139,2 162,6 185,6 149,1 152,1* 151,1* 159,7*

ZOTO 55,9 70,1 76,1 73,7 68,9 78,7 64,5 61,3 76,4 74,4* 72,5* 70,6*

DM 190,6 165,7 189,8 179,6 198,0 175,5 140,5 134,5 186,8 188,1* 181,1* 190,1*

TAXA DE OCUPAÇÃO HOTELEIRA (%) E DIÁRIA MÉDIA (R$) POR REGIÃO / HOTEL OCCUPANCY RATE AND AVERAGE DAILY RATE BY CITY REGION

20

08

20

07

20

06

20

05

Fonte: São Paulo Turismo, 2008

*Estimativa / ForecastTO - Taxa de ocupação / Occupancy rate

ZS - Zona Sul / South region

ZN - Zona Norte / North region

ZL - Zona Leste / East region

CE - Centro / Downtown Area

ZO - Zona Oeste / West region

DM - Diária média / Average daily rates

w w w . c i d a d e d e s a o p a u l o . c o m 23

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

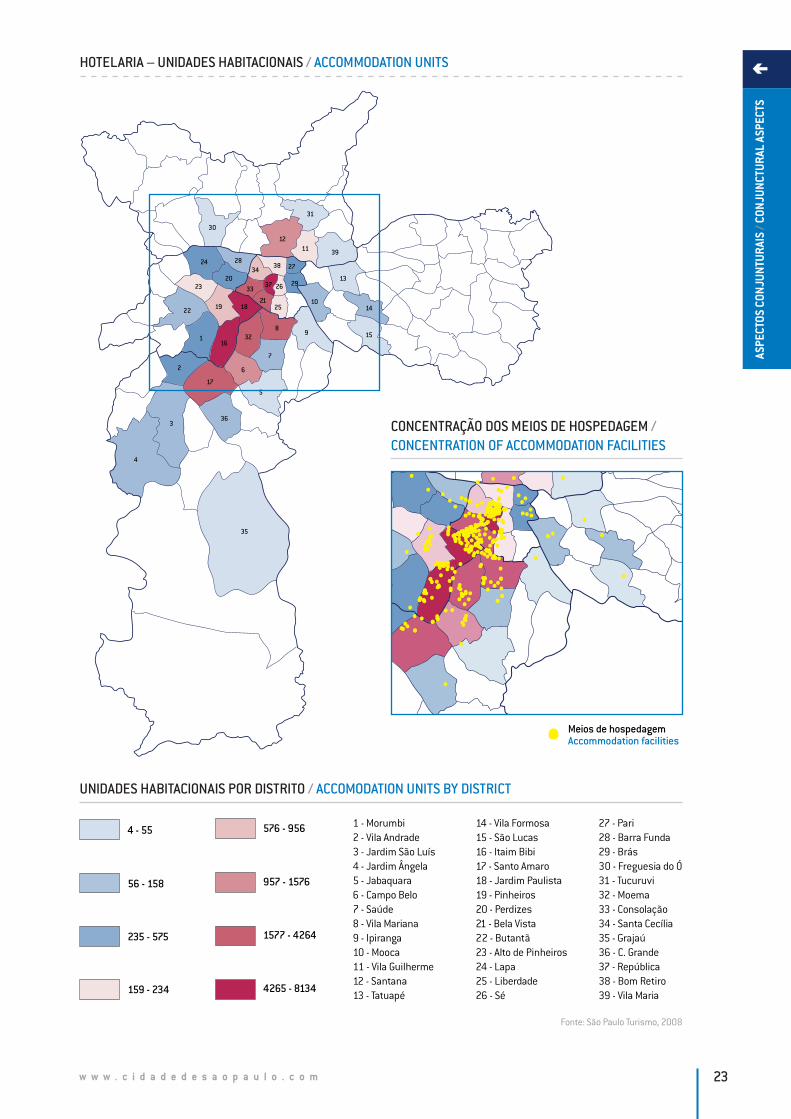

HOTELARIA – UNIDADES HABITACIONAIS / ACCOMMODATION UNITS

CONCENTRAÇÃO DOS MEIOS DE HOSPEDAGEM / CONCENTRATION OF ACCOMMODATION FACILITIES

35

4

3

5

19

2

7

6

8

17

10

12

22

36

39

30

24

1615

31

32

13

19 14

23

11

20

18

2838

33

34

25

27

29

21

37 26

1 - Morumbi2 - Vila Andrade3 - Jardim São Luís4 - Jardim Ângela5 - Jabaquara6 - Campo Belo7 - Saúde8 - Vila Mariana9 - Ipiranga10 - Mooca11 - Vila Guilherme12 - Santana13 - Tatuapé

14 - Vila Formosa15 - São Lucas16 - Itaim Bibi17 - Santo Amaro18 - Jardim Paulista19 - Pinheiros20 - Perdizes21 - Bela Vista22 - Butantã23 - Alto de Pinheiros24 - Lapa25 - Liberdade26 - Sé

27 - Pari28 - Barra Funda29 - Brás30 - Freguesia do Ó31 - Tucuruvi32 - Moema33 - Consolação34 - Santa Cecília35 - Grajaú36 - C. Grande37 - República38 - Bom Retiro39 - Vila Maria

4 - 55

56 - 158

235 - 575

576 - 956

957 - 1576

1577 - 4264

4265 - 8134159 - 234

Meios de hospedagemAccommodation facilities

UNIDADES HABITACIONAIS POR DISTRITO / ACCOMODATION UNITS BY DISTRICT

Fonte: São Paulo Turismo, 2008

w w w . c i d a d e d e s a o p a u l o . c o m24

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

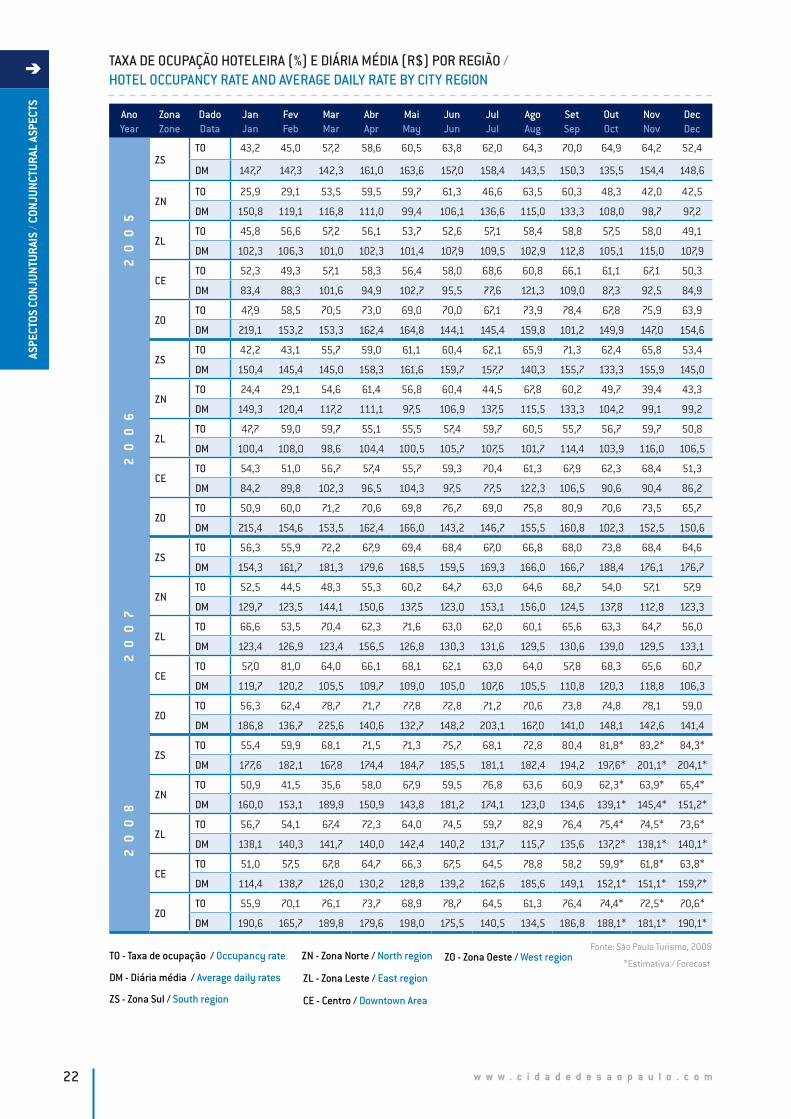

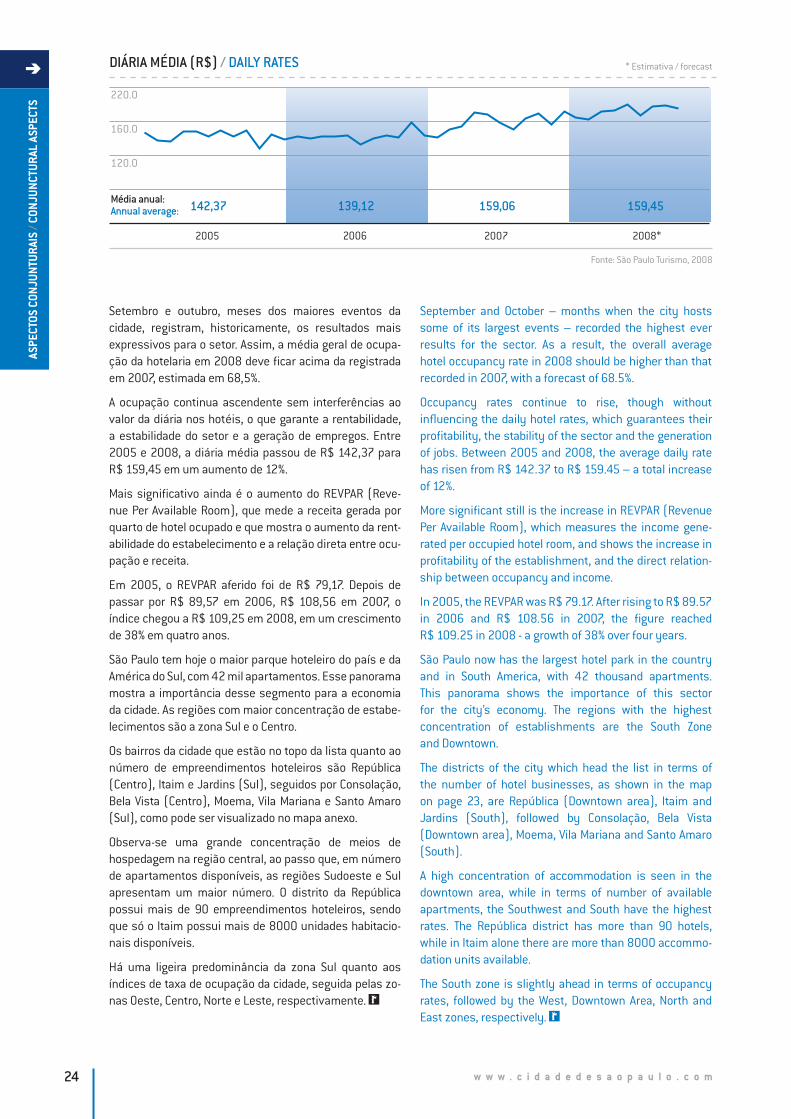

Setembro e outubro, meses dos maiores eventos da cidade, registram, historicamente, os resultados mais expressivos para o setor. Assim, a média geral de ocupa-ção da hotelaria em 2008 deve ficar acima da registrada em 2007, estimada em 68,5%.

A ocupação continua ascendente sem interferências ao valor da diária nos hotéis, o que garante a rentabilidade, a estabilidade do setor e a geração de empregos. Entre 2005 e 2008, a diária média passou de R$ 142,37 para R$ 159,45 em um aumento de 12%.

Mais significativo ainda é o aumento do REVPAR (Reve-nue Per Available Room), que mede a receita gerada por quarto de hotel ocupado e que mostra o aumento da rent-abilidade do estabelecimento e a relação direta entre ocu-pação e receita.

Em 2005, o REVPAR aferido foi de R$ 79,17. Depois de passar por R$ 89,57 em 2006, R$ 108,56 em 2007, o índice chegou a R$ 109,25 em 2008, em um crescimento de 38% em quatro anos.

São Paulo tem hoje o maior parque hoteleiro do país e da América do Sul, com 42 mil apartamentos. Esse panorama mostra a importância desse segmento para a economia da cidade. As regiões com maior concentração de estabe-lecimentos são a zona Sul e o Centro.

Os bairros da cidade que estão no topo da lista quanto ao número de empreendimentos hoteleiros são República (Centro), Itaim e Jardins (Sul), seguidos por Consolação, Bela Vista (Centro), Moema, Vila Mariana e Santo Amaro (Sul), como pode ser visualizado no mapa anexo.

Observa-se uma grande concentração de meios de hospedagem na região central, ao passo que, em número de apartamentos disponíveis, as regiões Sudoeste e Sul apresentam um maior número. O distrito da República possui mais de 90 empreendimentos hoteleiros, sendo que só o Itaim possui mais de 8000 unidades habitacio-nais disponíveis.

Há uma ligeira predominância da zona Sul quanto aos índices de taxa de ocupação da cidade, seguida pelas zo-nas Oeste, Centro, Norte e Leste, respectivamente.

September and October – months when the city hosts some of its largest events – recorded the highest ever results for the sector. As a result, the overall average hotel occupancy rate in 2008 should be higher than that recorded in 2007, with a forecast of 68.5%.

Occupancy rates continue to rise, though without influencing the daily hotel rates, which guarantees their profitability, the stability of the sector and the generation of jobs. Between 2005 and 2008, the average daily rate has risen from R$ 142.37 to R$ 159.45 – a total increase of 12%.

More significant still is the increase in REVPAR (Revenue Per Available Room), which measures the income gene-rated per occupied hotel room, and shows the increase in profitability of the establishment, and the direct relation-ship between occupancy and income.

In 2005, the REVPAR was R$ 79.17. After rising to R$ 89.57 in 2006 and R$ 108.56 in 2007, the figure reached R$ 109.25 in 2008 - a growth of 38% over four years.

São Paulo now has the largest hotel park in the country and in South America, with 42 thousand apartments. This panorama shows the importance of this sector for the city’s economy. The regions with the highest concentration of establishments are the South Zone and Downtown.

The districts of the city which head the list in terms of the number of hotel businesses, as shown in the map on page 23, are República (Downtown area), Itaim and Jardins (South), followed by Consolação, Bela Vista (Downtown area), Moema, Vila Mariana and Santo Amaro (South).

A high concentration of accommodation is seen in the downtown area, while in terms of number of available apartments, the Southwest and South have the highest rates. The República district has more than 90 hotels, while in Itaim alone there are more than 8000 accommo-dation units available.

The South zone is slightly ahead in terms of occupancy rates, followed by the West, Downtown Area, North and East zones, respectively.

160.0

220.0

120.0

2005 2006 2008*2007

142,37 139,12 159,45159,06Média anual:Annual average:

DIÁRIA MÉDIA (R$) / DAILY RATES

Fonte: São Paulo Turismo, 2008

* Estimativa / forecast

w w w . c i d a d e d e s a o p a u l o . c o m 25

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

FLUXO AÉREOAIR TRAFFIC

Passageiros transferidos: CGH para GRUAs grandes mudanças ocorridas na malha aérea pau-listana nos últimos tempos podem ser observadas nos números de pousos e decolagens nos dois principais aeroportos da cidade, bem como no fluxo de passageiros. Juntos, Congonhas (CGH) e Guarulhos (GRU) apresenta-ram um aumento de mais de 800 mil passageiros no ano de 2007, em relação ao ano anterior.

Porém, observa-se uma transferência de passageiros e aeronaves do aeroporto de Congonhas (queda de 17,4% no movimento de passageiros) para Guarulhos (aumento de 18,7% no número de passageiros), a partir das mudanças advindas principalmente em função do acidente aéreo da TAM em julho de 2007.

Congonhas registrou uma queda de 11,7% no fluxo entre 2006 e 2007. Em conseqüência, Guarulhos obteve um incremento de 17%. No entanto, o número de pousos e decolagens de Guarulhos em 2007 não superou o de Congonhas, mesmo com todas as alterações.

Transfer of passengers: From CGH to GRUThe main changes that have taken place in the airline industry of São Paulo in recent times are seen in the number of airplanes landing and taking off in the main airports of the city, and in the flow of passengers. Together, Congonhas (CGH) and Guarulhos (GRU) presented an increase of more than 800 thousand passengers in 2007, in relation to the previous year.

However, a transfer of passengers and aircraft from Congonhas airport (a decrease of 17.4% in passenger movement) to Guarulhos (increase of 18.7% in the number of passengers) can be seen, following the chang-es instigated after the TAM aircraft accident in July 2007.

Congonhas recorded a drop of 11.7% in passenger flow between 2006 and 2007. As a consequence, Guarulhos saw an increase of 17%. However, despite the changes, the number of aircrafts landing and taking off at Guarulhos in 2007 did not surpass that of Congonhas.

FLUXO DE AERONAVES / AIR TRAFFIC

25.000

10.000

5.000

20.000

2005 2006 20082007

CongonhasGuarulhos

Fonte: INFRAERO, 2008

FLUXO DE PASSAGEIROS (em milhares) / NUMBER OF PASSENGERS (in thousands)

1.500

1.000

500

2.000

2.500

3.000

2005 2006 20082007

CongonhasGuarulhos

Fonte: INFRAERO, 2008

GUARULHOS 2007 - PASSAGEIROS / PASSENGERS

18,7 milhões / millions

CONGONHAS 2007 - PASSAGEIROS / PASSENGERS

15,2 milhões / millions

w w w . c i d a d e d e s a o p a u l o . c o m26

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

Caracas

Miami

Dallas

México

Washington, DCNew York

Toronto

La Paz

FrankfurtAmsterdãLondres

Paris

MadriLisboa

Assunção

Lima

Bogot á

Montevidéu

Joanesburgo

DubaiDoha

Roma

São PauloSantiago

Buenos Aires

Pequim

Tóquio

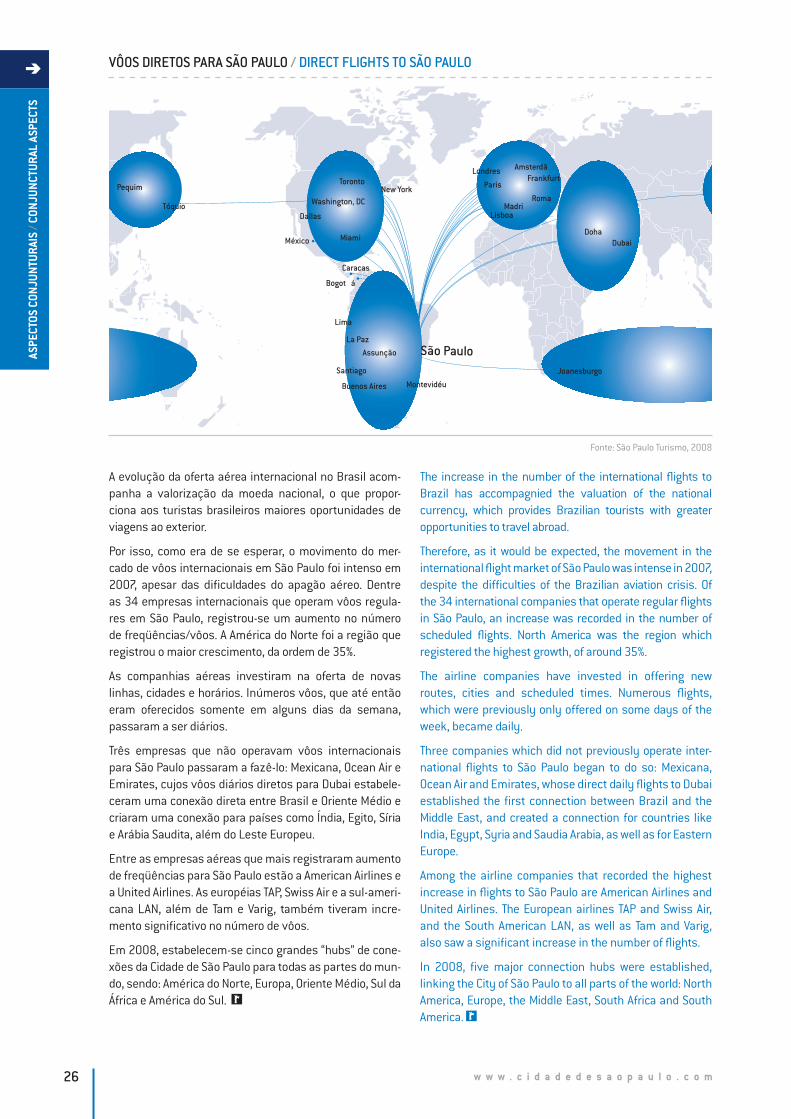

VÔOS DIRETOS PARA SÃO PAULO / DIRECT FLIGHTS TO SÃO PAULO

Fonte: São Paulo Turismo, 2008

A evolução da oferta aérea internacional no Brasil acom-panha a valorização da moeda nacional, o que propor-ciona aos turistas brasileiros maiores oportunidades de viagens ao exterior.

Por isso, como era de se esperar, o movimento do mer-cado de vôos internacionais em São Paulo foi intenso em 2007, apesar das dificuldades do apagão aéreo. Dentre as 34 empresas internacionais que operam vôos regula-res em São Paulo, registrou-se um aumento no número de freqüências/vôos. A América do Norte foi a região que registrou o maior crescimento, da ordem de 35%.

As companhias aéreas investiram na oferta de novas linhas, cidades e horários. Inúmeros vôos, que até então eram oferecidos somente em alguns dias da semana, passaram a ser diários.

Três empresas que não operavam vôos internacionais para São Paulo passaram a fazê-lo: Mexicana, Ocean Air e Emirates, cujos vôos diários diretos para Dubai estabele-ceram uma conexão direta entre Brasil e Oriente Médio e criaram uma conexão para países como Índia, Egito, Síria e Arábia Saudita, além do Leste Europeu.

Entre as empresas aéreas que mais registraram aumento de freqüências para São Paulo estão a American Airlines e a United Airlines. As européias TAP, Swiss Air e a sul-ameri-cana LAN, além de Tam e Varig, também tiveram incre-mento significativo no número de vôos.

Em 2008, estabelecem-se cinco grandes “hubs” de cone-xões da Cidade de São Paulo para todas as partes do mun-do, sendo: América do Norte, Europa, Oriente Médio, Sul da África e América do Sul.

The increase in the number of the international flights to Brazil has accompagnied the valuation of the national currency, which provides Brazilian tourists with greater opportunities to travel abroad.

Therefore, as it would be expected, the movement in the international flight market of São Paulo was intense in 2007, despite the difficulties of the Brazilian aviation crisis. Of the 34 international companies that operate regular flights in São Paulo, an increase was recorded in the number of scheduled flights. North America was the region which registered the highest growth, of around 35%.

The airline companies have invested in offering new routes, cities and scheduled times. Numerous flights, which were previously only offered on some days of the week, became daily.

Three companies which did not previously operate inter-national flights to São Paulo began to do so: Mexicana, Ocean Air and Emirates, whose direct daily flights to Dubai established the first connection between Brazil and the Middle East, and created a connection for countries like India, Egypt, Syria and Saudia Arabia, as well as for Eastern Europe.

Among the airline companies that recorded the highest increase in flights to São Paulo are American Airlines and United Airlines. The European airlines TAP and Swiss Air, and the South American LAN, as well as Tam and Varig, also saw a significant increase in the number of flights.

In 2008, five major connection hubs were established, linking the City of São Paulo to all parts of the world: North America, Europe, the Middle East, South Africa and South America.

w w w . c i d a d e d e s a o p a u l o . c o m 27

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

TERMINAIS RODOVIÁRIOSBUS TERMINALS

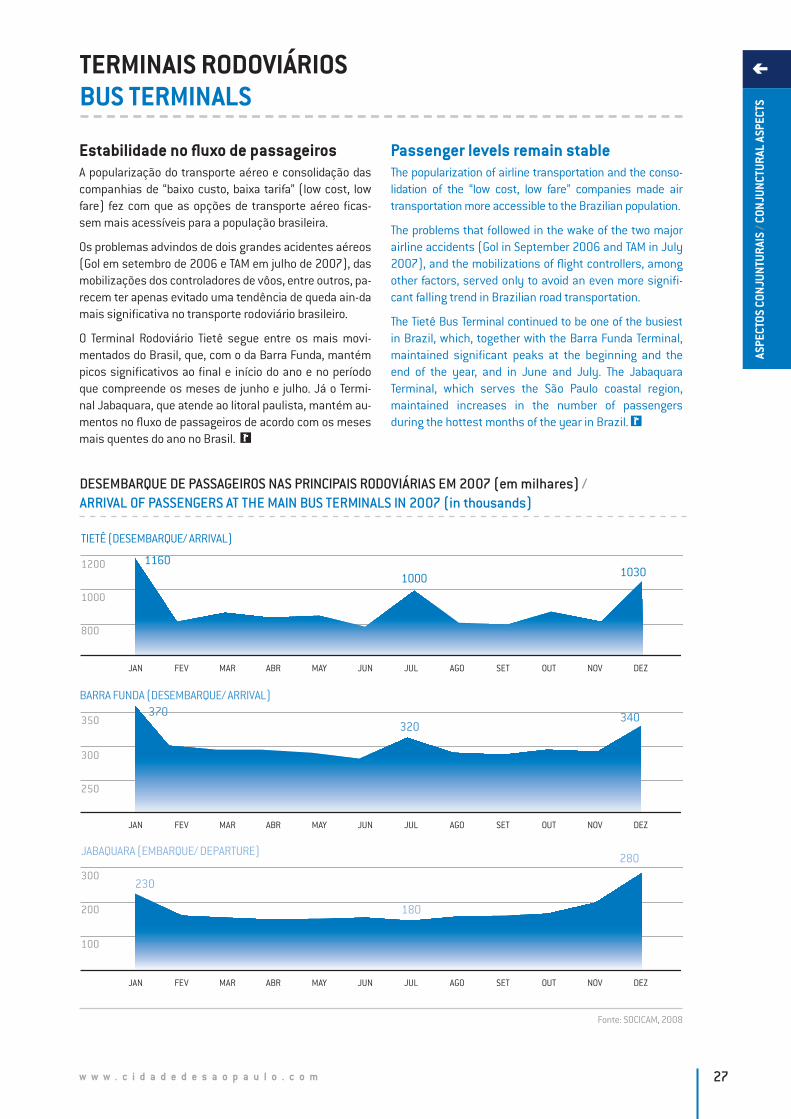

Estabilidade no fluxo de passageirosA popularização do transporte aéreo e consolidação das companhias de “baixo custo, baixa tarifa” (low cost, low fare) fez com que as opções de transporte aéreo ficas-sem mais acessíveis para a população brasileira.

Os problemas advindos de dois grandes acidentes aéreos (Gol em setembro de 2006 e TAM em julho de 2007), das mobilizações dos controladores de vôos, entre outros, pa-recem ter apenas evitado uma tendência de queda ain-da mais significativa no transporte rodoviário brasileiro.

O Terminal Rodoviário Tietê segue entre os mais movi-mentados do Brasil, que, com o da Barra Funda, mantém picos significativos ao final e início do ano e no período que compreende os meses de junho e julho. Já o Termi-nal Jabaquara, que atende ao litoral paulista, mantém au-mentos no fluxo de passageiros de acordo com os meses mais quentes do ano no Brasil.

Passenger levels remain stableThe popularization of airline transportation and the conso- lidation of the “low cost, low fare” companies made air transportation more accessible to the Brazilian population.

The problems that followed in the wake of the two major airline accidents (Gol in September 2006 and TAM in July 2007), and the mobilizations of flight controllers, among other factors, served only to avoid an even more signifi-cant falling trend in Brazilian road transportation.

The Tietê Bus Terminal continued to be one of the busiest in Brazil, which, together with the Barra Funda Terminal, maintained significant peaks at the beginning and the end of the year, and in June and July. The Jabaquara Terminal, which serves the São Paulo coastal region, maintained increases in the number of passengers during the hottest months of the year in Brazil.

DESEMBARQUE DE PASSAGEIROS NAS PRINCIPAIS RODOVIÁRIAS EM 2007 (em milhares) / ARRIVAL OF PASSENGERS AT THE MAIN BUS TERMINALS IN 2007 (in thousands)

JAN FEV MAR ABR MAY JUN JUL AGO SET OUT NOV DEZ

100

300

200

JABAQUARA (EMBARQUE/ DEPARTURE)

230

180

280

JAN FEV MAR ABR MAY JUN JUL AGO SET OUT NOV DEZ

250

350

300

BARRA FUNDA (DESEMBARQUE/ ARRIVAL)370

320340

JAN FEV MAR ABR MAY JUN JUL AGO SET OUT NOV DEZ

800

1200

1000

TIETÊ (DESEMBARQUE/ ARRIVAL)

1160

1000 1030

Fonte: SOCICAM, 2008

w w w . c i d a d e d e s a o p a u l o . c o m28

ASPE

CTOS

CON

JUNT

URAI

S / C

ONJU

NCTU

RAL

ASPE

CTS

VOLUME DO ISSVOLUME OF ISS

Mais um indicador favorávelMaior pólo receptor de visitantes do país, a Cidade de São Paulo apresenta bons resultados em diversos segmentos relacionados ao turismo, particularmente na arrecadação do ISS – Imposto Sobre Serviços.

Levando-se em conta os últimos quatro anos, o aumento na arrecadação foi de 39,8%, correspondente a uma taxa anual de crescimento de 10%, em média. A estimativa para 2008 representa uma média de 2,6% do volume total de arrecadação do município com os impostos.

O levantamento foi feito pela Secretaria Municipal de Fi-nanças e contabiliza os resultados do Grupo 13 (Turismo) que concentra valores arrecadados com Hospedagens, Pacotes Turísticos e Eventos. Importante destacar, porém, que neste grupo não está incluído o montante significa-tivo de outros setores que recebem impacto do turismo – 52 no total, segundo a Organização Mundial do Turismo (OMT), entidade vinculada à Organização das Nações Unidas (ONU).

Another positive indicatorNumber one incoming destination in Brazil, the City of São Paulo presents good results in various sectors related to tourism, as seen in the city’s income from ISS – Tax On Services.