c ountry report - cpmaicpmaindia.com/pdf/apic_countrypaper2011_korea.pdf · c ountry report from ko...

TRANSCRIPT

C o u n try R e p o rt

F ro m

K O R EA

Korea Petrochemical Industry Association(KPIA)

Asia Petrochemical Industry Conference 2011

May 26~27, 2011

Japan

CONTENTS

. Country ReportⅠ ··································································3

; The Petrochemical Industry In Korea

II. For Committee Meeting ··············································19

1. General Matters & Raw Materials Committee ··············19

2. Polyolefins Committee ······························································28

3. Styrenics Committee ··································································33

4. PVC Committee ············································································37

5. Synthetic Rubber Committee ················································40

6. Synthetic Fiber Raw Materials Committee ······················43

7. Chemicals Committee ·······························································49

. Country Report

2011 Asia Petrochemical Industry Conference - Korea

The Petrochemical Industry in Korea

1. The Korean Economy: Present Status and Outlook

Korea's economy is expected to grow 4% in 2011 just as the world

economy. Though the manufacturing sector will lead economic growth thanks

to an increase in export and equipment investment, the domestic demand will

remain weak. Especially, private consumption will grow slowly due to low

buying power resulted from price rising.

While aggravated trade conditions limit consumption recovery, investment

in construction will be weak as the construction industry undergoes

restructuring. This year's consumer price rise will slow down after the 2nd

quarter as raw material prices are stabilized, and will remain at the latter half

of 3%.

<Table 1> The forecast of Korean domestic economy

(Unit : %/yr)

2010

2011

1Q 2Q 3Q 4Q Y

S1) H2) S H S H S H S H

GDP(%) 6.2 4.1 3.1 3.4 3.5 4.2 4.0 5.3 5.8 4.3 4.1Private

Consumption(%) 4.1 3.6 2.9 3.7 3.0 3.5 3.1 4.2 4.8 3.7 3.5

ConstructionInvestment(%) -1.4 -6.9 0.3 -0.7 3.1 2.3 0.1 3.4 0.0 -0.1 0.9

EquipmentInvestment(%) 25.0 13.0 4.5 6.1 1.5 4.2 2.8 10.2 7.0 8.2 3.9

Note : 1) SERI (Samsung Economy Research Institute), Forecast for 2011 World

Economy and Korea's Economy (April 2011)

2) HANAIF (Hana Institute of Finance), Forecast for 2011 Finance and

Economy(November 2010)

Country Report

2. Petrochemical Industry Overviews

[2010 Situations]

Despite of no new line addition and decrease in export to China,

production of 2010 (based on three major areas) grew 1.0% to mark

21,201,000 tons compared to the previous year thanks to improvement in the

operating rate driven by domestic demand recovery.

The domestic market grew 6.0% to mark 10,232,000 tons compared to

the previous year thanks to recovery of frontline industries such as automobile,

home appliance and chemical fiber, and the export market fell 2.4% to

11,822,000 tons compared to the previous year due to insufficient export

capacity as resources were channeled to meet the growing domestic demand.

<Figure 1> The trend of Growth rate of Domestic demand for Petrochemicals

The domestic demand, especially for synthetic resin and materials, has

stalled or fallen since 2002. The demand for synthetic resin was weakened as

2011 Asia Petrochemical Industry Conference - Korea

the home appliance industry became streamlined and transferred facilities to

other countries, and the demand for synthetic materials was reduced as

Korea's chemical fiber facilities were moved to other countries and

uncompetitive facilities were scrapped.

A big rise in 2009 compared to 2008 should be understood as a base

effect but could not be seen as an expansion of the domestic market.

Continuous growth in 2010 resulted from the global competitiveness

improvement of frontline industries such as automobile and home appliance.

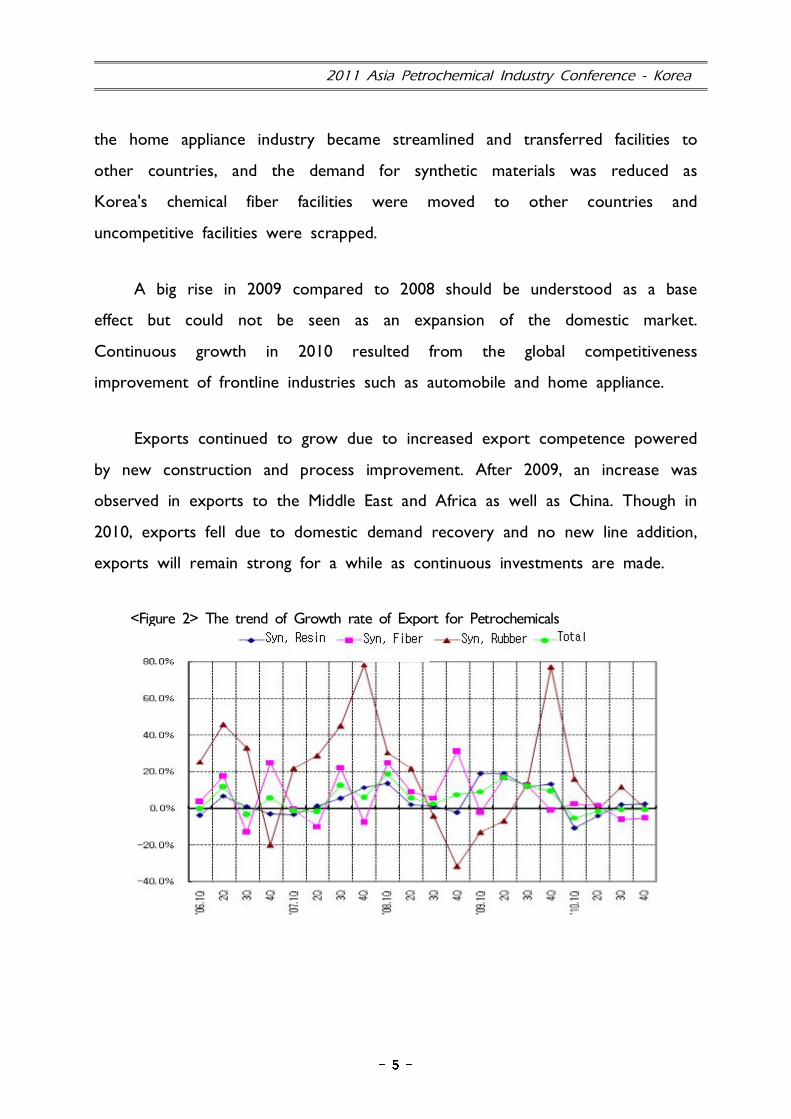

Exports continued to grow due to increased export competence powered

by new construction and process improvement. After 2009, an increase was

observed in exports to the Middle East and Africa as well as China. Though in

2010, exports fell due to domestic demand recovery and no new line addition,

exports will remain strong for a while as continuous investments are made.

<Figure 2> The trend of Growth rate of Export for Petrochemicals

Country Report

[2011 Forecast]

Though large-scale investment is not planned for 2011, debottlenecking and

improved operation in some lines will enable production to grow 1.4% to mark

21,507,000 tons. As the frontline industry slows down, the domestic demand will

grow 2.9% to mark 10,525,000 tons and exports will rise 0.2%.

<Table 2> Supply and Demand for Major Petrochemicals

(Unit : 1,000MT, %/yr)

20092010

2011(P)1H 2H Y

G·R G·R G·R G·R G·R

Synth.

Resin

Prod. (-0.5) (1.1)

Exp. (2.1) (-3.7) (0.1)

Imp. (8.8) (40.7) (4.2)

Dem. (2.5) (5.6) (2.6)

Synth.

Fiber

Prod. (-0.8) (2.6) (0.8)

Exp. (-2.8) (-1.3) (-2.0)

Imp. (16.5) (1.9) (1.2)

Dem. (3.0) (6.2) (3.3)

Synth.

Rubber

Prod. (4.4) (5.8) (12.9)

Exp. (4.4) (5.3) (18.3)

Imp. (2.9) (14.5) (-4.2)

Dem. (4.6) (8.2) (1.8)

Total

Prod. (1.1) (1.0) (1.4)

Exp. (0.4) (-2.4) (0.2)

Imp. (13.5) (9.7) (1.3)

Dem. (2.9) (6.0) (2.9)

2011 Asia Petrochemical Industry Conference - Korea

(1) Supply and demand by sector

Synthetic Resins

[2010 Situations]

Production fell 0.5% to mark 11,738,000 tons as there was no new line addition

and low operation rate in some products (HDPE). The domestic demand grew 5.6%

to mark 4,970,000 tons thanks to a boost in the frontline industry.

Based on accumulated data from January to October, the demand for

LDPE/HDPE for wire sheathes, PS/ABS for home appliances, and PP for impact,

random and compound grew significantly. Also, LDPE replaced LLDPE on the market

actively.

Exports fell 3.7% compared to the previous year due to insufficient export

capacity as resources were channeled to meet the growing domestic demand. Though

exports to China plunged, exports to India, Vietnam, Japan, Russia and Turkey

increased.

[2011 Forecast]

Production in 2011 will grow only 1.1% to mark 11,865,000 tons due to an

increase in regular maintenance though new lines are added for some products

(LDPE). The domestic demand in 2011 will grow 2.6% to mark 5,097,000 tons as

frontline industries grow slowly.

Thanks to efforts to diversify overseas markets, exports will grow 0.1%

compared to 2010.

Country Report

<Table 3> The trend of Supply and Demand for Synthetic Resins1)

(Unit : 1,000MT, %/yr)

20092010

2011(P)1H 2H Y

G·R G·R G·R G·R G·R

LDPE

Prod.Exp.

Imp.Dem.

HDPE

Prod.Exp.

Imp.

Dem.

PP

Prod.

Exp.Imp.

Dem.

PVC

Prod.Exp.

Imp.Dem.

P S

Prod.Exp.

Imp.

Dem.

PS

Prod.

Exp.Imp.

Dem.

EPS

Prod.Exp.

Imp.Dem.

ABS

Prod.Exp.

Imp.

Dem.

Total

Prod.

Exp.Imp.

Dem.

(NOTE) 1) Based on PE, PP, PS, ABS, PVC

2011 Asia Petrochemical Industry Conference - Korea

Synthectic Fiber Raw Materials

[2010 Situations]

Production in 2010 grew 2.6% to mark 8,586,000 tons thanks to a rise in

frontline industry's demand though there was no investment.

The domestic demand in 2010 grew 6.2% to mark 4,864,000 tons thanks to a

rise in demand for polyester and nylon(8.6% increase, 1,463,000 tons).

Exports in 2010 fell 1.3% to mark 4,312,000 due to insufficient export capacity

as resources were channeled to meet the growing domestic demand. Though exports

to China went down, exports to India, Thailand, Japan, Taiwan, Russia and Brazil

soared significantly.

[2011 Forecast]

In spite of new line addition (TPA), production in 2011 will grow only 0.8% to

mark 8,652,000 tons compared to 2010 as new lines will be completed in the fourth

quarter.

Thanks to line addition (Daehan Synthetic Fiber, Hyosung, Kum Kang), the

domestic demand will grow 3.3% to mark 5,023,000 tons compared to 2010.

In spite of efforts to diversify global markets, exports in 2011 will drop 2.0%

compared to 2010 due to insufficient export capacity.

Country Report

<Table 4> The trend of Supply and Demand for Synthetic Fiber Raw Materials1)

(Unit : 1,000MT, %/yr)

20092010

2011(P)1H 2H Y

G.R G.R G.R G.R G.R

TPA

Prod.

Exp.

Imp.

Dem.

DMT

Prod.

Exp.

Imp.

Dem.

EG

Prod.

Exp.

Imp.

Dem.

AN

Prod.

Exp.

Imp.

Dem.

CPLM

Prod.

Exp.

Imp.

Dem.

Total

Prod.

Exp.

Imp.

Dem.

(NOTE) 1) Based on AN, CPLM, DMT, EG, TPA

2011 Asia Petrochemical Industry Conference - Korea

Synthectic Rubbers

[2010 Situation]

Production in 2010 grew 5.8% to mark 877,000 tons thanks to increased

production capacity powered by continuous line addition.

The domestic demand grew 8.2% to mark 398,000 tons thanks to a boom in

the tire industry supported by the automobile industry's growth (tire production grew

26.3% to mark 95,322,000 tires), and exports grew 5.3% to mark 552,000 tons.

[2011 Forecast]

Production in 2011 will grow 12.9% thanks to increased production capacity

powered by continuous line addition compared to 2010.

The domestic demand in 2011 will grow 1.8% thanks to frontline industry

growth and higher demand for local exports, and exports will grow 18.3% thanks to

increased export capacity.

<Table 5> The trend of Supply and Demand for Synthetic Rubbers1)

(Unit : 1,000MT, %/yr)

20092010

2011(P)1H 2H Y

G.R G.R G.R G.R G.R

SBR

Prod.

Exp.

Imp.Dem.

BR

Prod.Exp.

Imp.Dem.

Total

Prod.

Exp.Imp.

Dem.

(NOTE) 1) Based on SBR, BR

Country Report

Basic Petrochemicals Ethylene

[2010 Situation]

Production in 2010 fell 0.2% to mark 7,362,000 tons due to regular maintenance

of a number of facilities and accidents in some facilities. The domestic demand grew

only 1.8% to mark 7,003,000 tons due to a decrease in PE and EG.

[2011 Forecast]

Production in 2011 will grow 2.7% to mark 7,560,000 tons thanks to new line

addition and reoperation, and the domestic demand will drop 0.1% to mark 6,995,000

tons due to no new line addition.

<Table 6> The trend of Supply and Demand for Basic Petrochemicals(Ethylene)

(Unit : 1,000MT, %/yr)

20092010

2011(P)1H 2H Y

G.R G.R G.R G.R G.R

Ethylene

Prod. (3.9)

Exp.

Imp.

Dem.

2011 Asia Petrochemical Industry Conference - Korea

<Table 7> Turnaround Schedule of NCC

(Unit : 1,000MT, %/yr)

Capacity Regular Maintenance Line Addition

K o r e a

P e t r o ch em i c a l

Ind. Co., Ltd.

470 April N/A

Samsung Total

Petrochemica ls

Co., Ltd.

900 April 26 ~ Early June (+)120,000 tons

YEOCHUN NCC

Co., Ltd.#1, 857 #1, April 5 ~ May 4 N/A

LG Chem, Ltd.Daesan,

760Daesan, March 17 ~ April 20 (+)100,000 tons

Honam Petrochemical

Corp.

Daesan,

1,000April N/A

Yeosu, 750 October N/A

SK Global

Chemical Co., Ltd.760 N/A N/A

(4) Environment/Health & Safty

As the environmental regulations are getting stricter around the world, Korea's

petrochemical industry is making proactive efforts to meet such global requirements.

As well as enhanced activities related to climate change and environmental safety,

increased efforts of interested parties and compliance with relevant regulations,

Korea's petrochemical companies are taking proactive measures such as responsible

care programs.

Regarding the Climatic Change Convention, the Korean government enforced

Basic Act for Low Carbon Green Growth to provide various policies. Thus, Korea's

petrochemical industry centralized its efforts with its association, requesting proper

climate change policies to create the environment for spontaneous green management

and improving its capability to respond to climate change.

For environment conservation, pertrochemical plants are monitoring contaminants

at major outlets in real time, and making efforts to reduce discharged chemicals by

Country Report

signing the chemical reduction agreement with the Ministry of Environment in 2004.

Also, since May 2008, they have begun to release information on discharged

hazardous chemicals to locals and interested parties for a better understanding.

To improve the petrochemical industry's image and regain trust, the responsible

care program is in place to protect environments and people's health over all

production processes and enhance environment/safety/health levels continuously.

Raising awareness of environment, safety and health as well, the responsible care

program started in 2003 to help children to understand the petrochemical industry.

Also, the chemistry frontier festival is held for high school students to motivate them,

and various seminars are held to share information.

3. Major Outstanding Issues

(1) Advancement of the Petrochemical Industry and Enhancement of

Competitiveness

Due to new players rising from Middle East, high oil prices and stricter

regulations on greenhouse gases, the growth fundamental is weakening fast. Thus,

major companies are increasing the gap with their advanced technology and new

players are trying to close the gap with large investments.

Especially, severe environmental regulations have a great impact on the

petrochemical industry as it consumes energy and emits greenhouse gases significantly.

To secure fundamental competitiveness and reduce greenhous gas emissions, the

pertrochemial complex is being converted into green facilities. This will contribute to

better energy efficiency of the petrochemical industry and national energy savings,

resulting in enhanced competitiveness.

2011 Asia Petrochemical Industry Conference - Korea

(2) Increased Attention to the Future Growth Business

To cope with structural oversupply and maintain sustainable growth momentum,

the pertrochemical industry has felt the needs for future growth businesses.

Thus, for a brighter future of the petrochemical industry, Korea's pertrochemical

companies endeavor to develop polysilicon, monosilane, flims, solar energy materials

and secondary batteries as well as add new lines.

(3) Climate Change Convention

The international community is discussing how to control greenhouse gas

emissions when the Kyoto Protocol expires in 2012. Korea will be obliged to reduce

greenhouse gas emissions from the 2nd commitment period 2013.

Thus, the Korean government enforced Basic Act for Low Carbon Green

Growth to prepare for greenhouse gas reduction obligation. In November 2009, the

national greenhouse gas reduction target was set to be 30% against BAU by 2020.

And detailed greenhouse reduction targets will be decided for each business sector.

Therefore, to enable Korea's petrochemical industry to remain as Korea's core

industry in the future while maintaining its current scale, there should be the

greenhouse gas policy based on the industry's international competitiveness. Korea's

petrochemical industry is preparing the plan to comply with greenhouse reduction

regulations by combining their resources through its association.

Country Report

<Table 8> New Construction and expansion

Company ProductProduction

CapacityNew Line Location

Operation Start

Period

Kumho PolychemCo., Ltd.

EPDM 95 60 Yeosu Q4, 2013.

Tong SuhPe t ro ch em i c a lCorp., Ltd.

AN 300 245 Ulsan #4 Q4, 2012

S a m s u n gPe t ro ch em i c a lCo., Ltd.

TPA 1,800 200 Ulsan Sep. 2011

Samsung TotalPetrochemical sCo., Ltd.

Ethylene 850 120

Daesan

Nov. 2011Propylene 680 100

Butadiene 105 15

Benzene 680 120Sep. 2012

PX 600 100

YEOCHUN NCCCo., Ltd. Ethylene 1,910 300 Yeosu 2012

H a n w h aC h e m i c a lCorporation

EVA 86 40 Ulsan Dec. 2012

H o n a mPe t ro ch em i c a lCorp.

Ethylene 750 250

Yeosu 2012HDPE 380 250

PP 400 200

Ebonic Carbon BlackKorea

C a r b o n

Black230 40 Yeosu 2nd Half, 2012

HC PetrochemBenzene 120 115

Daesan Sep. 2013PX 380 800

2011 Asia Petrochemical Industry Conference - Korea

<Table 9> Major Development Related to Petrochemical Industry Restructuring

Merger

- Tonsg Suh Petchem. transferred its all the stake, 100% to Asahi Kasei ’98. 5

- Hyosung T&C, Hyosung Corporation, Hyosung LivingIndustry and Hyosung Industries consolidated into HyosungCorporation

’98.11

- Korea BASF Urethane, Korea BASF Styrenic, BASF Koreaconsolidated into BASF Korea

’99.1

- Kohap, Kohap Chemical, Kohap Petrochemical consolidatedinto Kohap

’99.3

- Korea Steel Petrochemical transferred to Oriental chemicalindustry

’00. 3

- Kumho Chemical transferred to Kumho Petrochemical ’01. 1

- SK Evertec transferred to SKC ’01.11

- Samsung General Chemicals transferred the stake, 50% to

Atofina’03.8

- KP Chemical transferred to Honam Petrochemical ’04.11

- LG Daesan Petrochemical transferred to LG chemicals ’06. 1

- CCC transferred to DCC ’06. 3

- Kolon Chemical transferred to Kolon ’07. 6

- LG Petrochemical transferred to LG Chemical ’07.11

- Honam Petrochemical bought Titan Chemicals of Malaysia. '10

- LG Chemical bought LG Polycarbonate. '11.4

Business

Integration

- Daelim Industrial and Hanwha Chemical established YeochunNCC

’99.10

- Daelim Industrial : PP, HDPE- Hanwha Chemical : LDPE, LLDPE

’99.10

- SK Chemical and Samyang established Hubis runningpolyester businsess

’00.10

- LG Chemical divided into 3 companies, LGCI, LG chemical,LG House hold and Health care

’00.12

- Kohap divided into KP chemical(TPA, PET Chip, PA) andKohap(Chemical fiber)

’01.12

- Kolon established Kolon Plastic integrating Its plasticdepartment and KTP

’08.6

- LG Chemical diveded into 2 companies, LG chemical, LGHausys

’09.4

- Hyundai Oil Bank founded HC Petrochem to produce and sell BTX(Hyundai Oil Bank: Cosmo Oil = 50:50)

'09.11

- SK Total Chemical was separated from SK Innovation. '11

Country Report

Business

transfer

- Dainong Petrochemical Industry transferred the stake toYongsan Chemicals

’97. 5

- Hanyang Chemical transferred the stake, 50% to BASF- Change the name to Hanwha BASF Urethane

’97.12

- Hyosung transferred the stake, 50% to BASF- Change the name to Hyosung BASF Styrenenics

’98. 3

- Hanwha Chemical transferred H2O2 to Kemira(Finland) ’98. 7

- Hanwha Chemical transferred PMMA to ElfAtochem(France)

’98.10

- LG Chemical transferred Carbon black toDegussa(German)

’98.11

- Dongsung Chemical transferred Polyol to BASF(German) ’98.12

- Hyosung transferred Polyacetal Rodia(France) ’99.1

- Kumho Chemical transferred Carbon black to CICC ’99.2

- Daelim and Phillips(USA) established Joint venture,K-Resin Copolymer

’00.2

- Daelim and Montell established Joint venture, Polymirae ’00.9

- Hyundai Petrochemical transferred PVC to LG Chemical ’00.11

- Samsung General Chemicals transferred TPA to SamsungPetrochemical

’00.12

- SK Evertec transferred SM #2 to BASF Korea ’01.7

- Korea PTG transferred the stake 54.8% to Yongsan

Chemicals’02.12

- Hyundai Petrochemical transferred its all the stake to the

consortium of Honam Petrochemical and LG Chemicals’03.6

- Inchon Oilbank transferred to SK ’05.12

- SK Chemical transferred Petrochemical Business to SKPetrochemical

’05.12

- OCI transferred PA/DOP to Hanwha Chemical ’08.6

- Korea Basf transferred SM to SK Energy ’08.8

- Kolon transferred SAP to LG Chemicals ’08.9

. For Committee Meeting

1. General Matters & Raw Materials

Committee

General Matters & Raw Materials Committee

General Matters & Raw Materials Committee

1. Olefins (Ethylene, Propylene, Butadiene)

ITEM : Ethylene

1) The 2010 Results

The domestic ethylene production was decreased by 0.2% compare to previous

year to be 7,396 thousand tons. Total ethylene demand was increased by 0.2%

compare to previous year to be 7,557 thousand tons. The export was decreased by

16% compare to previous year to be 554 thousand tons due to new expansion in

China.

2) The 2011 Forecast

In 2011, total ethylene demand is expected to grow up about 2-3% to be 7,760

thousand tons due to increase export in India and Southeast Asia.

The domestic ethylene production will increase about 2.2% to be 7,560 thousand tons

caused by small amount of expansion from LG Chem.

ITEM : Propylene

1) The 2010 Results

The balance of supply/demand was tight because the domestic propylene market

showed a good condition due to strong demand of downstream products. Korean

total supply of propylene was grown by 2.2% compare to previous year to be 5,982

thousand tons and total demand of propylene was grown by 1.9% compare to

previous year to be 5,948 thousand tons.

2011 Asia Petrochemical Industry Conference - Korea

2) The 2011 Forecast

It is expected that supply of propylene will be short due to the Japan

earthquake and annual turnaround of Taiwan in 1H of 2011. As Korean maker’s

annual turnaround will be converged on March and April, so supply/demand balance

will be tight temporarily. However Hyundai Oil bank RFCC(150~300thousand tons)

will be newly started up in the middle of May then tight balance will be soften

somewhat.

ITEM : Butadiene

1) The 2010 Results

With recovery of Automobile market, downstream demand was steadily

increased.

The domestic production was grown by 4.6% compare to previous year to be 1,144

thousand tons due to increase synthetic rubber’s alternative demand effect, which is

caused by rising price of natural rubber.

Total demand was grown by 4.9% compare to previous year to be 1,456 thousand

tons due to strong demand of domestic market.

2) The 2011 Forecast

There is no large scale of new capacity expansion and butadiene demand will be

increased by highly using BR and ABS due to the continued growing demand in the

home electronics and tire.

Honam petrochemical increased additional Butadiene 150 thousand tons at the end of

last year and KPC(BR 120 thousand tons) will be started up in 2011.

General Matters & Raw Materials Committee

(Unit : 1,000MT)

2009 20102011

(Prospect)

Ethylene

Supply

Production 7,380 7,396 7,560

Import 160 196 200

Total 7,540 7,592 7,760

Demand

Domestic 6,882 7,003 6,995

Export 659 554 765

Total 7540 7,557 7,760

Year-end Capacity 7,440 7,610 7,770

Propylene

SupplyProduction 5,642 5,702 5,690Import 249 280 250Total 5,891 5,982 6,040

DemandDomestic 4,003 5,389 5,308Export 665 559 655Total 4,668 5,948 5,963

Year-end Capacity 5,641 5,726 5,801

Butadiene

SupplyProduction 869 1,144 1,180Import 291 318 383Total 1,160 1,462 1,563

DemandDomestic 1,160 1,224 1,318Export 228 232 262Total 1,388 1,456 1,580

Year-end Capacity 1,107 1,107 1,257

2011 Asia Petrochemical Industry Conference - Korea

2. Aromatics(Benzene, Toluene, Xylene)

ITEM : Benzene

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Production 4,175 4,388 4,400

Demand 3,132 3,248 3,380

Balance +1,043 +1,140 +1,020

1) The 2010 Results

In 2010 Production in Korea was 4,388 thousand tons, which is 5% increase

from 2009. The Domestic Demand was 3,248 thousand tons, which is slightly

increased from 2009.

Export volume to US in 2010 was approximately 537 thousand tons, which

contributed towards healthier benzene Supply/Demand Balance in Asia.

2) The 2011 Forecast

Korean production in 2011 is forecasted to be 4,400 thousand tons, which is

very similar to 2010 production even though new addition of huge paraxylene

capacity, which carry large scale co-product benzene suppply. It is mainly caused by

heavy scheduled maintenance of naptha crackers and aromatics plants.

Demand in 2011 is expected to increase due to the demand of derivatives such

as SM, Phenol, however Korea will continue to have a large surplus and will remain a

major net exporter.

Based on the supply/demand forecast of 2011, it is anticipated that benzene price may

pass by the peak during the early 3rd Quarter and shall be weak through the 4th Quarter.

General Matters & Raw Materials Committee

ITEM : Toluene

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 2,022 2,058 2,090

Import 209 272 330

Total 2,231 2,330 2,420

Demand

Domestic 1,328 1,492 1,620

Export 903 837 800

Total 2,231 2,329 2,420

1) The 2010 Results

In 2010 Production in Korea was 2,058 thousand tons, which is similar to 2009.

The Domestic Demand was 1,492 thousand tons, which is 10% increase from 2009.

Export volume in 2010 was approximately 837 thousand tons with a 7%

decrease from previous year (903 thousand tons in 2009). Import in 2010 was 272

thousand tons with a 30% increase from previous year (209 thousand tons in 2009).

2) The 2011 Forecast

Korean production in 2011 will be pretty similar compared to last year so that

there would not be any expansion plan.

Toluene Supply/Demand balance of Korea was forecasted as pretty long balace

due to China's mixed aromitics import and GS Caltex's MTPX Turn-around. But from

Japan's earthquake Toluene Market is very tight because of gasoline demand of Japan

and healthy demand of TDP. Furthermore as US toluene Price has been very strong,

the arbitrage is opened from Asia to US.

In spite of GSC's MTPX turn-around toluene balance might be healthy till 3rd

Quarter.

2011 Asia Petrochemical Industry Conference - Korea

ITEM : Mixed Xylene

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Production 5,636 5,898 6,228

Demand 5,608 6,094 6,458

Balance 28 -196 -230

(NOTE) Sourced by CMAI

1) The 2010 Results

In 2010 Production in Korea was around 5,898 thousand tons with 4.5% annual

growth rate from previous year (5,636 thousand tons in 2009). The Domestic

Demand was 6,094 thousand tons, which is 9% increase from 2009 due to PX

demand.

Export volume in 2010 was approximately 12% decrease compared to 2009, on

the other hand, Import volume in 2010 was approximately 10% increase compared to

2009.

2) The 2011 Forecast

Korean production in 2011 will be sharply increase compare to last year and

Domestic Demand will be increased about 5% as well.

Based on the supply/demand forecast of 2011, MX price will maintain a fairly

stable level throughout the year, however due to the Japan earthquake in March, the

recent price is thought to be its peak around and with the addition of PX Capacity,

MX-PX Spread in 2nd Half is expected to shrink compared to 1st Quarter"

General Matters & Raw Materials Committee

ITEM : Para Xylene

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Production 4,240 4,509 4,800

Demand 4,217 4,332 4,450

Balance 23 177 350

1) The 2010 Results

"In 2010 Production in Korea was 4,019 thousand tons, which is 5% decrease

from 2009. Whereas, China's PX consumption grew at 14.3% in 2010. (Global

consumption growth for 2010 is 10.4%)

In 2010 1st Half, PX Price was downward trend because of the increased

Supply by new PX plants in China. Whereas, there were PX plant troubles in China

and Middle East and the cotton crops were in bad condition through 4th Quarter.

For this reason, 2nd Half PX Price turned bullish.

2) The 2011 Forecast

"In 1st Quarter, Increased PTA Operation due to the recovery of Asia

Economy led to increase demand for PX and due to the Japan earthquake, PX Price

of March was higher than $1,800/MT around.

Even though S-Oil & Urumqi remains on target for 2011 1st Half starting up of

its new plant, Demand growth remains close to trend due to some plants T/A and

the increase of new PTA plants in China. It means that PX markets appear to have

slightly stronger prospects.

2011 Asia Petrochemical Industry Conference - Korea

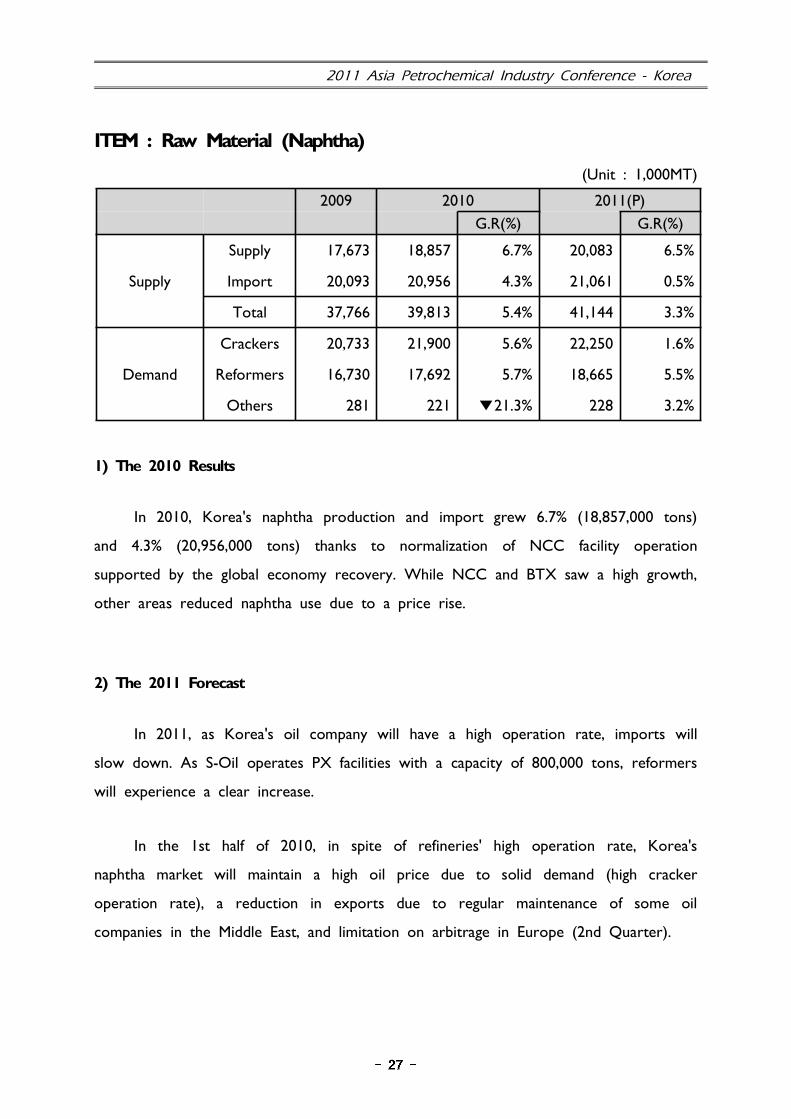

ITEM : Raw Material (Naphtha)

(Unit : 1,000MT)

2009 2010 2011(P)

G.R(%) G.R(%)

Supply 17,673 18,857 6.7% 20,083 6.5%

Supply Import 20,093 20,956 4.3% 21,061 0.5%

Total 37,766 39,813 5.4% 41,144 3.3%

Crackers 20,733 21,900 5.6% 22,250 1.6%

Demand Reformers 16,730 17,692 5.7% 18,665 5.5%

Others 281 221 21.3%▼ 228 3.2%

1) The 2010 Results

In 2010, Korea's naphtha production and import grew 6.7% (18,857,000 tons)

and 4.3% (20,956,000 tons) thanks to normalization of NCC facility operation

supported by the global economy recovery. While NCC and BTX saw a high growth,

other areas reduced naphtha use due to a price rise.

2) The 2011 Forecast

In 2011, as Korea's oil company will have a high operation rate, imports will

slow down. As S-Oil operates PX facilities with a capacity of 800,000 tons, reformers

will experience a clear increase.

In the 1st half of 2010, in spite of refineries' high operation rate, Korea's

naphtha market will maintain a high oil price due to solid demand (high cracker

operation rate), a reduction in exports due to regular maintenance of some oil

companies in the Middle East, and limitation on arbitrage in Europe (2nd Quarter).

2. Polyolefins Committee

2011 Asia Petrochemical Industry Conference - Korea

Polyolefins Committee

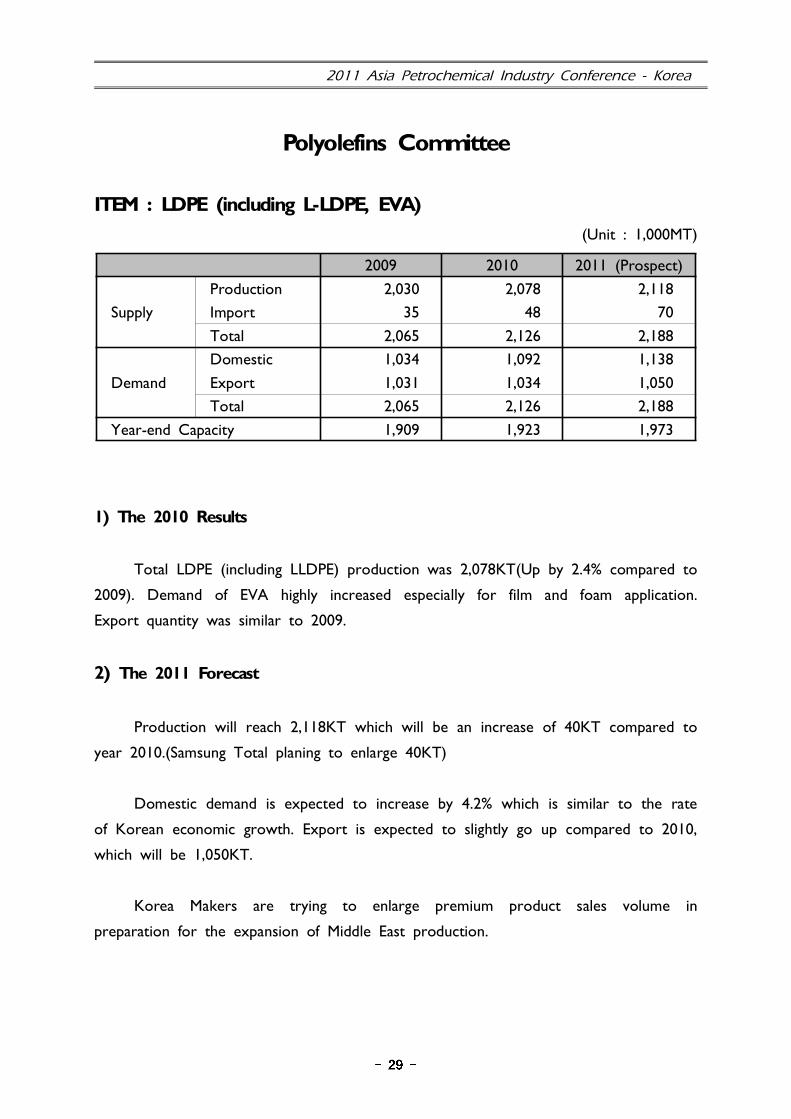

ITEM : LDPE (including L-LDPE, EVA)

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 2,030 2,078 2,118

Import 35 48 70

Total 2,065 2,126 2,188

Demand

Domestic 1,034 1,092 1,138

Export 1,031 1,034 1,050

Total 2,065 2,126 2,188

Year-end Capacity 1,909 1,923 1,973

1) The 2010 Results

Total LDPE (including LLDPE) production was 2,078KT(Up by 2.4% compared to

2009). Demand of EVA highly increased especially for film and foam application.

Export quantity was similar to 2009.

2) The 2011 Forecast

Production will reach 2,118KT which will be an increase of 40KT compared to

year 2010.(Samsung Total planing to enlarge 40KT)

Domestic demand is expected to increase by 4.2% which is similar to the rate

of Korean economic growth. Export is expected to slightly go up compared to 2010,

which will be 1,050KT.

Korea Makers are trying to enlarge premium product sales volume in

preparation for the expansion of Middle East production.

Polyolefins Committee

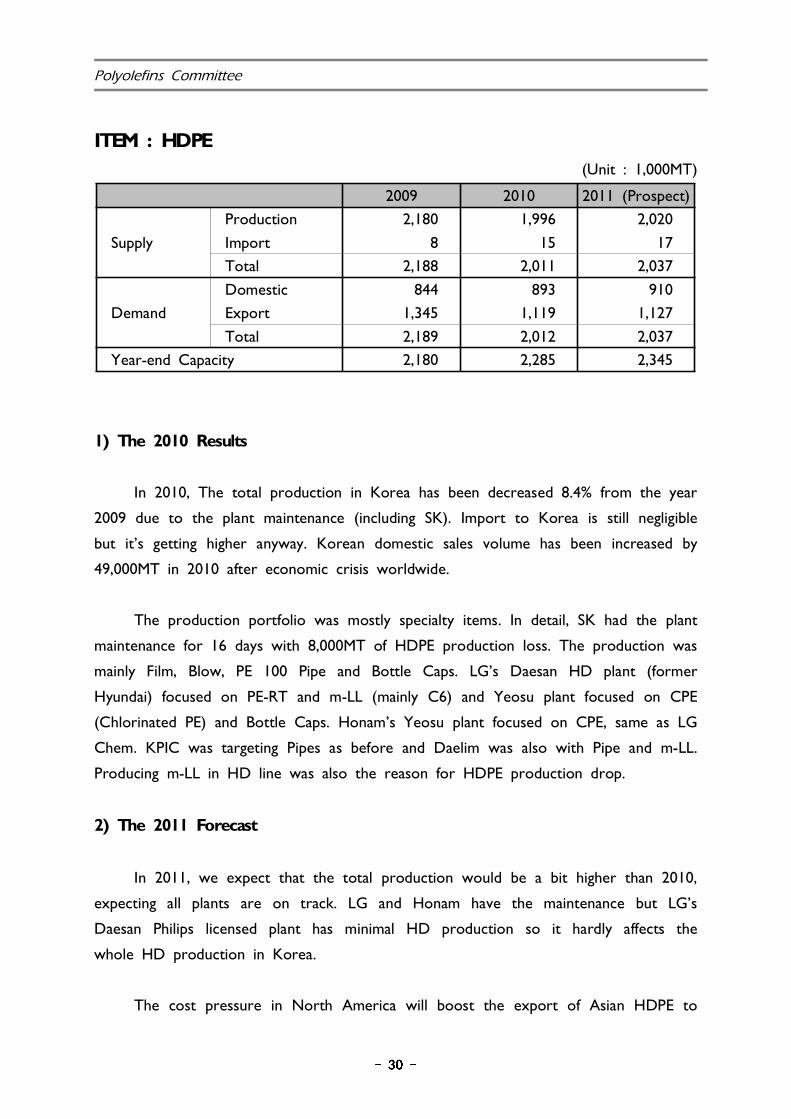

ITEM : HDPE

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 2,180 1,996 2,020

Import 8 15 17

Total 2,188 2,011 2,037

Demand

Domestic 844 893 910

Export 1,345 1,119 1,127

Total 2,189 2,012 2,037

Year-end Capacity 2,180 2,285 2,345

1) The 2010 Results

In 2010, The total production in Korea has been decreased 8.4% from the year

2009 due to the plant maintenance (including SK). Import to Korea is still negligible

but it’s getting higher anyway. Korean domestic sales volume has been increased by

49,000MT in 2010 after economic crisis worldwide.

The production portfolio was mostly specialty items. In detail, SK had the plant

maintenance for 16 days with 8,000MT of HDPE production loss. The production was

mainly Film, Blow, PE 100 Pipe and Bottle Caps. LG’s Daesan HD plant (former

Hyundai) focused on PE-RT and m-LL (mainly C6) and Yeosu plant focused on CPE

(Chlorinated PE) and Bottle Caps. Honam’s Yeosu plant focused on CPE, same as LG

Chem. KPIC was targeting Pipes as before and Daelim was also with Pipe and m-LL.

Producing m-LL in HD line was also the reason for HDPE production drop.

2) The 2011 Forecast

In 2011, we expect that the total production would be a bit higher than 2010,

expecting all plants are on track. LG and Honam have the maintenance but LG’s

Daesan Philips licensed plant has minimal HD production so it hardly affects the

whole HD production in Korea.

The cost pressure in North America will boost the export of Asian HDPE to

2011 Asia Petrochemical Industry Conference - Korea

Latin America and other area. The price gap between China and non-China is huge

now but we expect that it will be synchronized from 2nd half of the year.

Korean producers are still targeting specialty items but in commodity side, looks

like it also has the merit in this year. As a whole, the year 2011 will be another

good year for producers in HDPE aspects.

ITEM : P P

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 3,677 3,806 3,790

Import 21 22 22

Total 3,698 3,828 3,812

Demand

Domestic 1,353 1,497 1,540

Export 2,376 2,308 2,272

Total 3,729 3,805 3,812

Year-end Capacity 3,748 3,818 3,958

1) The 2010 Results

In 2010, production and sales volume were 3,806 thousand tons, 3,805 thousand

tons each. It is increased 129 thousand tons and 76 thousand tons respectively from

the previous year. In 2009, production was 3,677 thousand tons and domestic and

export sales was 3,709 thousand ton.

The domestic sales volume of 2010 recorded 1,497 thousand tons, rising 12.3%

comparing with previous year's 1,333 thousand tons. Especially Co-polymer sales of

domestic reached 815 thousand ton, increasing by 24% from previous year's 659

thousand ton due to the growth automotive and electric and electronics.

The export volume in 2010 reached 2,308 thousand tons, falling 2.9% from the

previous year's 2,376 thousand tons.

Polyolefins Committee

2) The 2011 Forecast

In 2011, production volume will be 3,790 thousand tons, falling 0.4% from the

previous year's 3,806 thousand tons due to the turnaround. It will be historically a

large number of plant turnaround, including Honam Petrochemical, LG Chemical,

Samsung Total, etc.

It is expected that the growth of downstream industry (Automotive, Home

appliance etc) will be slowed down in 2011. It will cause the domestic sales growth

slowdown, from 12% in 2010 to 3% in 2011.

In 2011, STC and LG Chemical is planning to expand PP plant capacity. Hence,

the year-end capacity will be increased by 3,963 thousand tons. It is nearly 4%

increase compare to the previous year.

3. Styrenics Committee

Styrenics Committee

Styrenics Committee

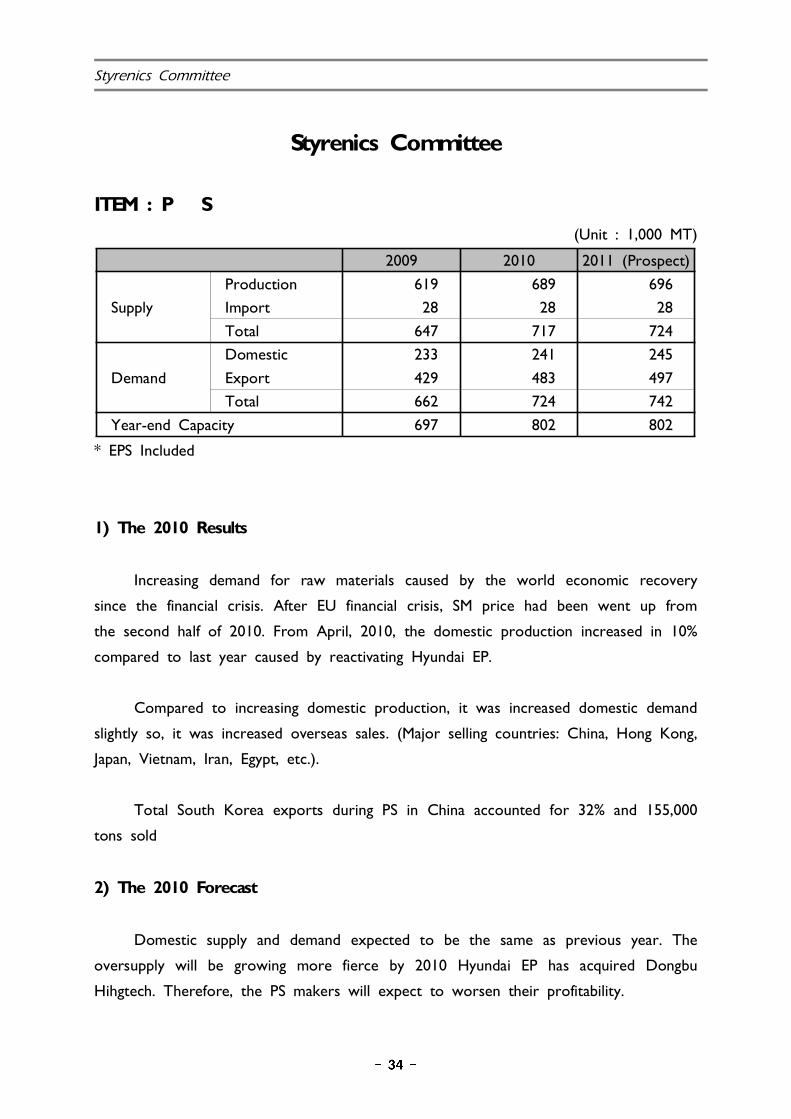

ITEM : P S

(Unit : 1,000 MT)

2009 2010 2011 (Prospect)

Supply

Production 619 689 696

Import 28 28 28

Total 647 717 724

Demand

Domestic 233 241 245

Export 429 483 497

Total 662 724 742

Year-end Capacity 697 802 802

* EPS Included

1) The 2010 Results

Increasing demand for raw materials caused by the world economic recovery

since the financial crisis. After EU financial crisis, SM price had been went up from

the second half of 2010. From April, 2010, the domestic production increased in 10%

compared to last year caused by reactivating Hyundai EP.

Compared to increasing domestic production, it was increased domestic demand

slightly so, it was increased overseas sales. (Major selling countries: China, Hong Kong,

Japan, Vietnam, Iran, Egypt, etc.).

Total South Korea exports during PS in China accounted for 32% and 155,000

tons sold

2) The 2010 Forecast

Domestic supply and demand expected to be the same as previous year. The

oversupply will be growing more fierce by 2010 Hyundai EP has acquired Dongbu

Hihgtech. Therefore, the PS makers will expect to worsen their profitability.

2009 Asia Petrochemical Industry Conference - Korea

As the world economy to survive, PS demand will be solved a little bit because

of consumer demand increased and extending China's domestic stimulus. The domestic

PS makers switch to HIPS, ABS with a high value. (LG Chemical: Some PS line switch

to ABS line / Cheil: only produce HIPS) In particular, the domestic PS makers seek a

high value product through HIPS rather than the general GP.

ITEM : A B S

(Unit : 1,000 MT)

2009 2010 2011 (Prospect)

Supply

Production 1,404 1,493 1,500

Import 6 7 7

Total 1,410 1,500 1,507

Demand

Domestic 160 216 230

Export 1,250 1,284 1,277

Total 1,410 1,500 1,507

Year-end Capacity 1,520 1,520 1,596

1) The 2010 Results

The production was 1,493 thousand tons, 6.4 % higher than that in 2009

resulted from enhancement of operation rate. There has been no additional

investment in Korea.

The demand was 216 thousand tons, 35% higher than last year mainly with high

growth of household appliances like refrigerator and washing machine and flat TV.

Demand for health care appliance like water purifier, videt, humidifier etc. was also

increased in 2010.

2) The 2011 Forecast

The production will be slightly increased comparing to the last year with the

increase of domestic demand.

Styrenics Committee

Domestic demand is expected to increase by 6.5% comparing to that of 2010

with the expectation of increase in demand from E/E applications.

ITEM : S M

(Unit : 1,000 MT)

2009 2010 2011 (Prospect)

Supply

Production 2,767 2,810 2,791

Import 759 755 800

Total 3,526 3,565 3,591

Demand

Domestic 2,221 2,255 2,261

Export 1,305 1,310 1,330

Total 3,526 3,565 3,591

Year-end Capacity 3,383 3,383 3,383

1) The 2010 Results

The SM production and capacity in Korea was almost similar to that of 2009.

Import and export wasn’t changed compare to that of 2009.

2) The 2011 Forecast

Capacity growth in Korea will be minimal in the near future. Honam will

increase their Daesan plant by 9% in 2011(80kta).

Production of SM in 2011 is expected to be 2791 thousand tons cause of there

will be turn around.

4. PVC Committee

PVC Committee

ITEM : P V C

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 1,439 1,404 1,410

Import 31 55 50

Total 1,470 1,459 1,460

Demand

Domestic 775 787 793

Export 685 630 642

Total 1,460 1,417 1,435

Year-end Capacity 1,380 1,380 1,380

1) The 2010 Results (Unit: 1,000MT)

2011 Asia Petrochemical Industry Conference - Korea

5. Synthetic Rubber Committee

2011 Asia Petrochemical Industry Conference - Korea

Synthetic Rubber Committee

(Unit : 1,000 MT)

2009 2010 2011 (Prospect)

SBR

Supply

Production 525 571 596

Import 39 49 46

Total 564 620 642

Demand

Domestic 164 203 212

Export 408 416 429

Total 572 619 641

Year-end Capacity 616 616 616

BR

SupplyProduction 306 323 432Import 23 22 24Total 329 345 456

DemandProduction 94 111 122Import 231 229 337Total 325 340 459

Year-end Capacity 322 322 522

* SBR / BR (SBR : E-SBR+S-SBR, BR : HBR + LBR)

* Production : based on Shipment

* Capacity : excluding S-SBR

1) The 2010 Results

a. Due to the global economic recovery, Korean auto and tire production grew.

As a result, both demand and production increased.

b. In 2010, Korean tire makers produced 94,200 k unit compared to 75,467 k

unit in 2009. The growth rate of 2009-2010 was 25% which was the highest record

for last 10 years.

c. After US imposed a tariff on tires from China in Sep. 2009, (35 % in the

first year, 30% in the second year and 25% in the third year), 2010 was the first

year which this decision started to take effect. This move accelerated the export of

Korean tire to US and resulted in the increase of tire production.

Synthetic Rubber Committee

d. The demand of S-SBR especially grew over the world because of Green Tire

trend which favors the eco-friendly tire with low rolling resistance. The domestic

demand of S-SBR increased as well.

2) The 2011 Forecast

a. In 2010, the operation rate was almost 100% for both SBR and BR.

Therefore, it looks difficult for SBR production to be increased more in 2011. In case

of BR, the domestic production will increase 38% due to the expansion of production

capacity in Korea.

b. As Chinese and Indian Auto & Tire industries continue to grow annually

based on motorization, the global demand of SBR and BR will show steady growth in

2011, especially in Asia.

c. Natural rubber price remains high due to tight supply and it will especially

affect the growth of demand for BR which can replace natural rubber.

6. Synthetic Fiber Raw Materials

Committee

Synthetic Fiber Raw Materials Committee

Synthetic Fiber Raw Materials Committee

ITEM : A N

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 532 595 582

Import 82 88 95

Total 614 683 677

Demand

Domestic 450 490 520

Export 172 183 157

Total 622 673 677

Year-end Capacity 550 550 565

1) The 2010 Results

AN total demand was increased by 8%, comparing with 2009. AN demand

from acrylic fibre was 50KT, the same as the last year and operation rate was 100%.

That is because shortly balanced and highly priced cottons have been triggering

increased acrylic fiber demand.

Additionally, AN demand from ABS resin sector was increased by 8% thanks to

booming electrics and chemical industries wide.

In the mean time, AN supply has been improved by 11% to cover up the

increased demand. TSPC issued no T/A in 2010 which helped to increase total

production by 12%.

2) The 2011 Forecast

Basically, there seems to be no capacity change in Acrylic Fibre. On the

contrary, capacity increases and D/Ns from major ABS makers will lead 6% of AN

demand increase in domestic.

However, AN export volume will be decreased by 13% due to shortage caused

2011 Asia Petrochemical Industry Conference - Korea

by TSPC's annual T/A.

As a result, total demand will be expanded slightly to reach 677KT. Domestic

production will be decreased by 2% and reached at 582KT reflecting turnarounds

from both of TK and TSPC in March and May, respectively. To compensate domestic

production, import will be expected to be increased by 7KT and touched at 95KT.

Accordingly, total supply would be decreased by 1% whereas a D/N helped to ramp

up year-end capacity by 3%.

ITEM : Caprolactam(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 258 275 276

Import 28 47 52

Total 286 322 328

Demand

Domestic 254 303 317

Export 32 19 11

Total 286 322 328

Year-end Capacity 270 270 270

1) The 2010 Results

Production of CPL was increased by 6.6% from previous year thanks to global

economy recovery and booming exports.

Export of CPL was decreased by 40.6% from previous year due to good

domestic demand and CPL shortage.

Import quantity of CPL was increased by 67.9%.

CPL demand from Textile, Engineering Plastic, Film was good. CPL demand in

Korea made a plus growth for two years in a row.

Synthetic Fiber Raw Materials Committee

2) The 2011 Forecast

Production of CPL is expected to increase by 0.4% from 2010 year.

Domestic CPL consumption for 2011 year is expected to increase by 4.6%

thanks to global economy recovery and booming exports.

CPL demand from textile and engineering plastics is expected to be strong.

CPL export quantity will be reduced due to increasing domestic sales.

ITEM : E G

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 1,177 1,153 1,067

Import 466 445 460

Total 1,643 1,598 1,527

Demand

Domestic 1,117 1,137 1,260

Export 526 461 267

Total 1,643 1,598 1,527

Year-end Capacity 1,340 1,340 1,352

1) The 2010 Results

MEG demand in Korea was about 1,137 thousand tons in 2010, slightly

increased by 2% compared with previous year’s 1,117 thousand tons. The improved

polyester margins compare to previous year was main reason behind the strong global

growth for polyester fiber, partially due to cotton supply constraints

The existing 3 MEG supplier produced about 1,153 thousand tons, similar to

last year.

2011 Asia Petrochemical Industry Conference - Korea

The total MEG import figures were decreased to 445 thousand tons, 4% lower

compared with previous year.

To cope with demand increase in domestic, MEG producers have decided to

increase domestic supply at the expense of reducing export volume. The total MEG

export figures were decreased to 461 thousand tons, which was 11% lower figures

compared to the year of 2009.

2) The 2011 Forecast

On the demand side, restarts at two polyester units and an expected increase

in operating rates of existing polyester facilities would in turn drive up domestic MEG

demand.

At the same time, severe competition along with numerous polyester capacity

expansion in both China and Korean domestic, cast gloom over the outlook of

demand growth.

On the Production side, MEG production will be decreased by 86 thousand

tons, mainly due to MEG rationalization plans including the conversion of glycols

capacity into HPEO and downstream HPEO derivatives.

As per price outlook, MEG prices staged downward correction in the past

weeks because of delayed turnaround schedule at major plants and China’s tightening

monetary policy. In the long run, however, MEG prices are expected to trend up,

because of no additional expansion plans until 2013 and steady demand growth in

polyester industry.

Synthetic Fiber Raw Materials Committee

ITEM : T P A

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 6,305 6,535 6,535

Import 0 0 0

Total 6,305 6,535 6,535

Demand

Domestic 2,708 2,885 2,885

Export 3,618 3,651 3,651

Total 6,326 6,536 6,536

Year-end Capacity 6,380 6,390 6,390

1) The 2010 Results

In the first half of 2010, the PTA price fell due to a price recession caused by

the PIGS Europe finance crisis. Spread was still strong and the anti-dumping issue was

a big issue for the Korea PTA maker, so they tried to make BIZ by exporting to

other countries such as India. As a result, China's import of Taiwan PTA has

increased rapidly.

In second half of 2010, Korea PTA export to China normalized due to the

most recent anti-dumping issue decision. The increased demand of downstream made

the PTA Spread very strong, as Polyester purchase increased as a result of high

priced raw cotton.

2) The 2011 Forecast

In the first half of 2011, the end of 2010's atmosphere will be maintained

because of increased Polyester demand. The China market will increasingly prefer

imported PTA, as a result of the currency exchange rate.

In the second half of 2011, PET demand will be stabilized as predicted by raw

cotton price, so PTA spread also will be steadily maintained.

7. Chemicals Committee

Chemicals Committee

Chemicals Committee

ITEM : 2-Ethyl Hexanol

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 416 404 410

Import 5 14 10

Total 421 418 420

Demand

Domestic 304 319 320

Export 117 99 100

Total 421 418 420

Year-end Capacity 400 400 400

1) The 2010 Results

Demand of 2-EH in Asia had gradually increased on 2010 as Global economy

recession had been slowly recovered since 2008.

Domestic demand(including self-consumption) also had increased to over 319KT which

is 5% higher than 2009.

The Profitability of 2-EH had improved its return on 2010 by widening the gap with

the feedstock(C3) to $522/mt from $200/mt on 2009.

The main reason of the bullish Domestic demand and bearish export trend was

increased self-consumption for Acrylic products such as 2EHA

And the demand of Plasticizers in Asia was continuous weak.

2) The 2011 Forecast

Plasticizers Demand in 2011 is still expected to be bearish, but Domestic

Demand of 2EH is expected, a slight increase, 325KT which is higher than 2009 due

2011 Asia Petrochemical Industry Conference - Korea

to Acrylic family of products' (2EHA) booming domestic demand for self-consumption,

while Export volume of 2EH is expected, a slight decrease, 95KT which is lower than

2009.

Intensive Shut-down in the first half of 2011 in Asia and Japan earthquake affected the

strength to maintain international current 2EH, but China's tightening policy and

authentic appearance from newly-organized facilities in Asia in the second half will

affect the relative ease of international supply, which will lead to switch weakness.

The gap between 2EH and the feedstock(C3) is expected under 2010's level($522/mt).

ITEM : Phenol

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 608 620 660

Import 48 96 90

Total 656 716 750

Demand

Domestic 533 575 601

Export 127 132 150

Total 660 707 751

Year-end Capacity 595 595 620

Chemicals Committee

1) The 2010 Results

Recovery to the healthy global market from economy crisis & bad market

demand in 2009. Due to US / EU manufaturer's unexpected troubles, reducing the

operating rates of producers caused to suffer from lack of supply

Some major supplier in Asia faced against the unplanned S/D, even twice.

(Mar~Apr, Aug~Sep) Delaying new Phenol projects to escalate tight supply situation.

(Sinopec-Tainjin : 1Q -> 2Q, SABIC : 3Q -> End of year)

Improvement in main end user applications such as construction and automotive,

taking place with a good global growth, such as BPA and Phenolic resins.

2) The 2011 Forecast

Generally, keeping out for high price amid a bullish outlook.

Phenol price remains bullish, in tandem with escalating feedstock, upstream

Benzene and Propylene valuses and T/A at regional facilities. Tight regional supply that

is getting more serious, after a deadly earthquake and tsunami struck Japan.

In US / EU phenol's case, the restricted availability of Cumene continues to

dictate the operating rates of US phenol producers, to supply very limited volume to

Asian market.

As one of main downstreams, BPA, new players (PTT, Sinopec-MCC) start the

new operating of plants. (Keeping strong and healthy demand)

Continuance to escalate upstream values, coupled with the volatility in crude

futures amid political turmoil in the Middle East, contribute to a positive outlook in

the rest of this year.

2011 Asia Petrochemical Industry Conference - Korea

ITEM : Phthalic Anhydride

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 330 330 330

Import 2 1 1

Total 332 331 331

Demand

Domestic 36 30 29~31

Export 160 160 160

Total 196 190 189~191

Year-end Capacity 340 340 340

1) The 2010 Results

Due to the sluggish construction industry, UPR and Paint parts entered the

phase of stagnation. So PA local demand showed no increase even some decline. The

imported cargo also slowed down due to the growing competition between

manufacturers

UPR: volatile demand by each product line.

Paints: Alkyd demand was encroached by Water based paints demand increase.

The industry definitely depends on the local market because the export is not easy,

and its demand usually comes from the renovation instead of new construction.

2) The 2011 Forecast

The recovery of construction industry along with the real estate market will be

one of the key factors for the market demand. It is very hard to expect the

short-term improve of the local construction market, but the reposition of local

products portfolio and the industry reorganizing are expected to follow and

strengthen the local competitiveness at last.

The imported cargo is expected to stay stable and more competition for new

application development for using PA will come out.

Chemicals Committee

ITEM : Acetic Acid

(Unit : 1,000MT)

2009 2010 2011 (Prospect)

Supply

Production 464 500 488

Import 51 48 71

Total 515 548 559

Demand

Domestic 450 480 500

Export 67 71 57

Total 517 551 557

Year-end Capacity 470 490 570

1) The 2010 Results

Domestic demand of acetic acid was 480,300 tons, larger than 2009. Demand

from all the derivatives of AA eg. PTA, VAM, EA & Solvents improved.

Supply was 547,600 tons which is increased by 33,200 tons in line with demand

increase & D/B of SSBP

2) The 2011 Forecast

Domestic demand from PTA, VAM, & EA/BA are stable to firm. PTA maintained

full operation with high margin in 1Q. SBP supply will be tight throughout the year

due to TAR from Sep. thru Oct.