caam funds emerging internal demand page 1 caam funds emerging internal demand a domestic growth...

Post on 19-Dec-2015

217 views

TRANSCRIPT

Page 1 CAAM Funds Emerging Internal Demand

CAAM Funds Emerging Internal Demand

A domestic growth thematic fund

Page 2 CAAM Funds Emerging Internal Demand

Contents

Summary p. 3

1. Why focus on " Internal Demand " in Emerging Countries now? p. 4

1.1 Historical overview of economic development

1.2 An important contributor to world growth

1.3 Strong macro-economic fundamentals

1.4 Decreasing sensitivity of emerging markets to the US economy

2. The strong drivers of Internal Demand in Emerging Countries p. 12

2.1 Household consumption: the emergence of a gigantic middle class

2.2 Corporate investments: strong support from private investments,

infrastructure spending and urbanisation

3. CAAM Funds Emerging Internal Demand p. 20

3.1 CAAM Funds Emerging Internal demand: concept & attractiveness

3.2 Fund key features

3.3 Investment philosophy, robust process & risk monitoring

3.4 Track- record of Global Emerging funds managed by the team

3.5 Strengths of CAAM expertise

Page 3 CAAM Funds Emerging Internal Demand

A winning theme in the current market environment:

Growth engine of the world economy in the years to come

Better economic health of emerging countries should translate into more resilient internal demand than in the

past

A way to invest in Emerging Markets with a targeted lower volatility

Some protection from the slowdown of developed economies

Summary

Emerging internal demand: why now?

1. Why focus on Internal Demand

in Emerging Countries now?

Page 5 CAAM Funds Emerging Internal Demand

United KingdomUnited StatesFranceGermanySwedenJapanRussiaItalyCanadaAustraliaTaiwanSouth KoreaMexicoArgentina

Take-off BrazilTurkey

March towards technology maturity ChinaThailand

Mass consumption India

1780 1800 1820 1840 1900 19201860 1880 1940 1960

United KingdomUnited StatesFranceGermanySwedenJapanRussiaItalyCanadaAustraliaTaiwanSouth KoreaMexicoArgentinaBrazilTurkeyChinaThailandIndiaIndonesiaPhilippinesVietnam

1980 2000 2020 2040

1.1 Historical overview of economic development

Large Emerging countries are entering mass consumption phase

Analysis of Rostow in 1960 (updated in 1990), « The Stages of Economic Growth », economica,3e edition

Our vision

Page 6 CAAM Funds Emerging Internal Demand

Retail Sales growth over last 12 months (6 months average, mio $)

0

4000

8000

12000

16000

20000

24000

août

-98

févr

-99

août

-99

févr

-00

août

-00

févr

-01

août

-01

févr

-02

août

-02

févr

-03

août

-03

févr

-04

août

-04

févr

-05

août

-05

févr

-06

août

-06

févr

-07

United States China

Growth in retail sales are already higher in current dollars in China than in the United States

1.2 Internal Demand in Emerging countries: an important contributor to world growth (1/2)

Source : CAAM

Page 7 CAAM Funds Emerging Internal Demand

Differential between Emerging and Developed Countries

-5,0-4,0-3,0-2,0-1,00,01,02,03,04,0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

source : EIU, MSCI, CAAMGDP (real, %yoy) Average

GDP growth in emerging countries consistently above the one of developed countries (except for 1998)

Growth looks set to remain strong due to improvement in fundamentals

1.2 Internal Demand in Emerging countries: an important contributor to world growth (2/2)

Page 8 CAAM Funds Emerging Internal Demand

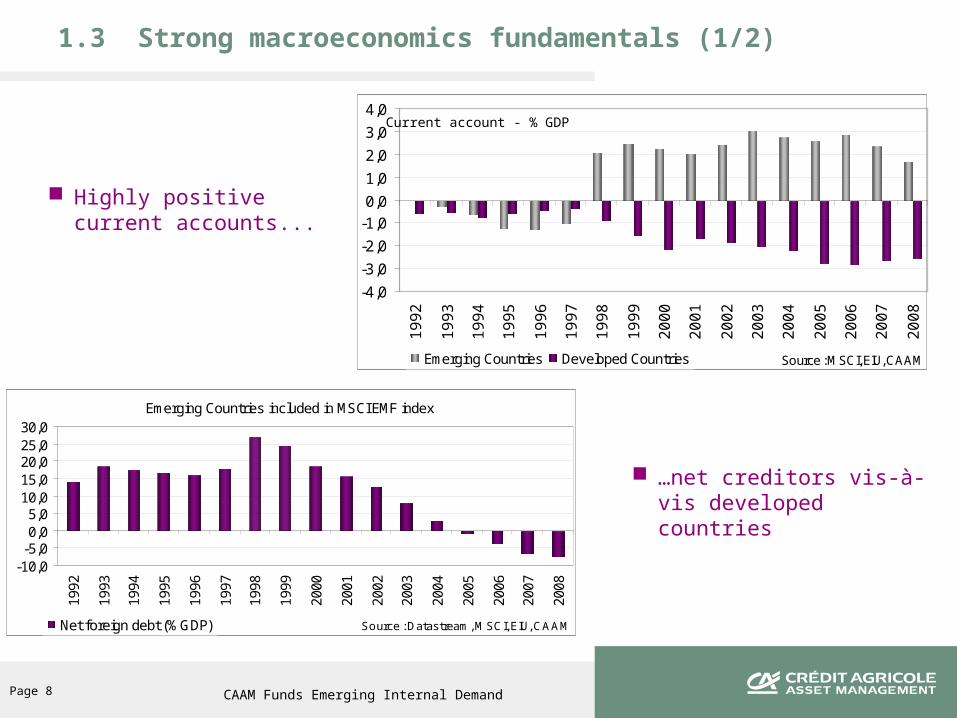

1.3 Strong macroeconomics fundamentals (1/2)

Highly positive current accounts...

-4,0

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Source : MSCI, EIU, CAAMEmerging Countries Developed Countries

Emerging Countries included in MSCI EMF index

-10,0-5,00,05,0

10,015,020,025,030,0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Source : Datastream, MSCI, EIU, CAAMNet foreign debt (%GDP)

Current account - % GDP

…net creditors vis-à-vis developed countries

Page 9 CAAM Funds Emerging Internal Demand

Comparison of different bond spreads

0

200

400

600

800

1000

1200

1400

1600

1800

jan

v.-

98

ma

i-9

8

se

pt.-9

8

jan

v.-

99

ma

i-9

9

se

pt.-9

9

jan

v.-

00

ma

i-0

0

se

pt.-0

0

jan

v.-

01

ma

i-0

1

se

pt.-0

1

jan

v.-

02

ma

i-0

2

se

pt.-0

2

jan

v.-

03

ma

i-0

3

se

pt.-0

3

jan

v.-

04

ma

i-0

4

se

pt.-0

4

jan

v.-

05

ma

i-0

5

se

pt.-0

5

jan

v.-

06

ma

i-0

6

se

pt.-0

6

jan

v.-

07

ma

i-0

7

Source : CAAM London

Emerging Markets Bond Index Lehman Brothers High Yield Merrill Lynch BBB Index

Difference in rating between emerging and developed countries set to tighten further

10 years of macroeconomic adjustment and budget discipline:

historically low and less volatile spreads

1.3 Strong macroeconomics fundamentals (2/2)

S&P Ratings of countries included in the MSCI Emerging Markets (w eighted according to equity country w eight)

-1

0

1

2

3

4

5

6

7

8

9

Sep

-96

Mar

-97

Sep

-97

Mar

-98

Sep

-98

Mar

-99

Sep

-99

Mar

-00

Sep

-00

Mar

-01

Sep

-01

Mar

-02

Sep

-02

Mar

-03

Sep

-03

Nov

-03

Jan-

04

Mar

-04

May

-04

Jul-0

4

Sep

-04

Nov

-04

Jan-

05

Mar

-05

May

-05

Jul-0

5

Sep

-05

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep

-06

Nov

-06

Jan-

07

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% Investment Grade (right) Av. grade for MSCI EMF (left)

Exit of Greece

Outperformance of non investment grade country leading to a lower rating

S&P upgraded Russia to "investment grade"

S&P upgraded India to "investment grade"

Downgrade of South Korea & exit of Portugal

Source : CAAM

Page 10 CAAM Funds Emerging Internal Demand

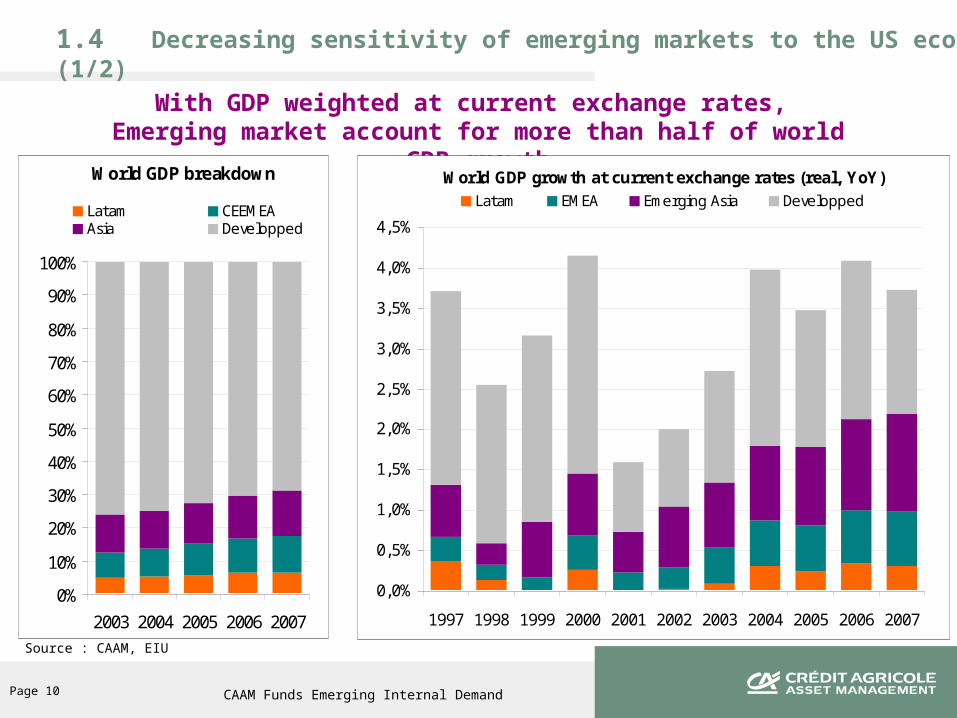

With GDP weighted at current exchange rates, Emerging market account for more than half of world GDP growth

Source : CAAM, EIU

World GDP breakdown

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007

Latam CEEMEAAsia Developped

World GDP growth at current exchange rates (real, YoY)

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Latam EMEA Emerging Asia Developped

1.4 Decreasing sensitivity of emerging markets to the US economy (1/2)

Page 11 CAAM Funds Emerging Internal Demand

With GDP weighted at purchasing power parity, Emerging market account for 80% of world GDP growth

Source : CAAM, EIU

World GDP breakdown

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002 2003 2004 2005 2006

Latam EMEAEmerging Asia Developped

World GDP growth at current exchange rates (real, YoY)

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Latam EMEA Emerging Asia Developped

1.4 Decreasing sensitivity of emerging markets to the US economy (2/2)

2. The strong drivers of Internal Demand

in Emerging Countries

Page 13 CAAM Funds Emerging Internal Demand

0

10

20

30

40

50

60

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 11000 12000 13000 14000 15000 16000

Inc

om

e p

erc

en

tile

2000

Source : Nomura, July 2007« China consumer – The great Leap Upwards »

An accelerator effect beyond a certain level of development…

2.1 Household consumption: the emergence of a gigantic middle class (1/3)

< 3000$ : low incomes, subsistence consumption (strong share of food and clothing)

> 3000$: decent incomes allowing savings and consumption (cars, white goods, education, etc.)

0

10

20

30

40

50

60

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 11000 12000 13000 14000 15000 16000

Inc

om

e p

erc

en

tile

2000 2005

0

10

20

30

40

50

60

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 11000 12000 13000 14000 15000 16000

Inc

om

e p

erc

en

tile

2000 2005 2010

0

10

20

30

40

50

60

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 11000 12000 13000 14000 15000 16000

Inc

om

e p

erc

en

tile

2000 2005 2010 2015

Distribution of urban Chinese income

Percentage of households with income higher than 3000$ pa

2000 2005 2010 2015Urban revenu /capita 731 1235 1911 3000Growth 69% 55% 57%Nbr of people over 47 179 419Growth 281% 134%

Average GDP growth : 9%Average increase in number of people over 3000$ : 24%

Page 14 CAAM Funds Emerging Internal Demand

Source : Rostow, Goldman Sachs

2.1 Household consumption: the emergence of a gigantic middle class (2/3)

0

100

200

300

400

500

600

700

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Germany

US

Japan

Korea

Russia

Brazil

China

India

Nb of cars per 1000 habitants

Acceleration effect : for example, the car industry

Private car penetration

Log scale

Japan

Italy

Germany

France

UK

Canada

United States

Nb of habitants per car

Nb

of c

ars

per

1000

hab

itant

s

Page 15 CAAM Funds Emerging Internal Demand

Expansion of a middle-class population :

population size will considerably impact emerging countries

In 10 years time, 800 million people will cross the 3000$ threshold, i.e. a greater population compared to the US, Europe and Japan put together

Massive middle-class population expansion in highly-populated countries

Middle class in Brazil, Russia, India & China

0

0,5

1

1,5

2

2,5

3

3,5

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Nb of people with income above3000$ pa (bn)

Dramatic rise in China's and India's middle class

0

200

400

600

800

1000

1200

1400

1600

2005 2015 2025 2035 2045

China

India

Sources : Goldman Sachs

2.1 Household consumption: the emergence of a gigantic middle class (3/3)

Page 16 CAAM Funds Emerging Internal Demand

2.2 Corporate investments: strong support from private investments

Healthy balance sheets should translate into higher capex

High levels of capacity utilization

0

10

20

30

40

50

60

70

80

90

100

2000 2001 2002 2003 2004 2005 2006E

0

10

20

30

40

50

60

70

80

90

100

Asia Pacific Free Cash Flow * (LHS) Asia Pacific Net Debt-to-Equity Ratio* (RHS)

%US$bn

70

72

74

76

78

80

82

84

86

Q2

19

95

Q4

19

95

Q2

19

96

Q4

19

96

Q2

19

97

Q4

19

97

Q2

19

98

Q4

19

98

Q2

19

99

Q4

19

99

Q2

20

00

Q4

20

00

Q2

20

01

Q4

20

01

Q2

20

02

Q4

20

02

Q2

20

03

Q4

20

03

Q2

20

04

Q4

20

04

Q2

20

05

Q4

20

05

Q2

20

06

Q4

20

06

Q2

20

07

Computation : average of Brazil, Thailand, Korea, Mexico, India, China Source : OECD, CAAM

Capacity utilization ratio

Source: Merrill Lynch

Page 17 CAAM Funds Emerging Internal Demand

2.2 Government spending: strong support from infrastructure

Governments infrastructure spending plans for 2007 to 2009

Source : Merrill Lynch, World Bank

Country Investment estimated Sectors targeted

China400bn$(12% GDP)

Energy, transportation (rail, highways), environment protection.2008 Olympics is a reason for sustained spending

India110bn$(9,7% GDP)

Roads, ports, oil and gas, power generation.

Indonesia45bn$ (10,5% GDP)

Roads, power generation, ports & water treatmentHas been reduced given slow regulatory reform and efforts to combat corruption

Russia185bn$(15,6% GDP)

Projects to facilitate exports of commodities (pipeline, ports)

Central & Eastern Europe25bn$ (3,5% GDP)

Spending target trans-European transport network (high speed motorways, rail lines)

South Africa60bn$(23%)

Will focus on electricity generation and transportation (rail freight)2010 world cup is the objective

Brazil100bn$(7,7% GDP)

Will apply to a wide range of sectors: oil, power generation, telecommunications, transportation, engineering and construction

Mexico60bn$(6,8%)

Natural gas, electricity, oil, roads, highways, home building

Total 985bn$ (10,8% GDP)

Page 18 CAAM Funds Emerging Internal Demand

Infrastructure needs are a major boost to investment

Example: India

Golden Quadrilateral was a huge

success: more roads built in India

over the past 5 years than there were

over the previous 50 years combined

Road / Highways- Development is

two-fold:

Expanding the 4 lane GQ network to 6

lanes

North/South & East/West corridors

linking the entire country

Source : CAAM Hong Kong

Page 19 CAAM Funds Emerging Internal Demand

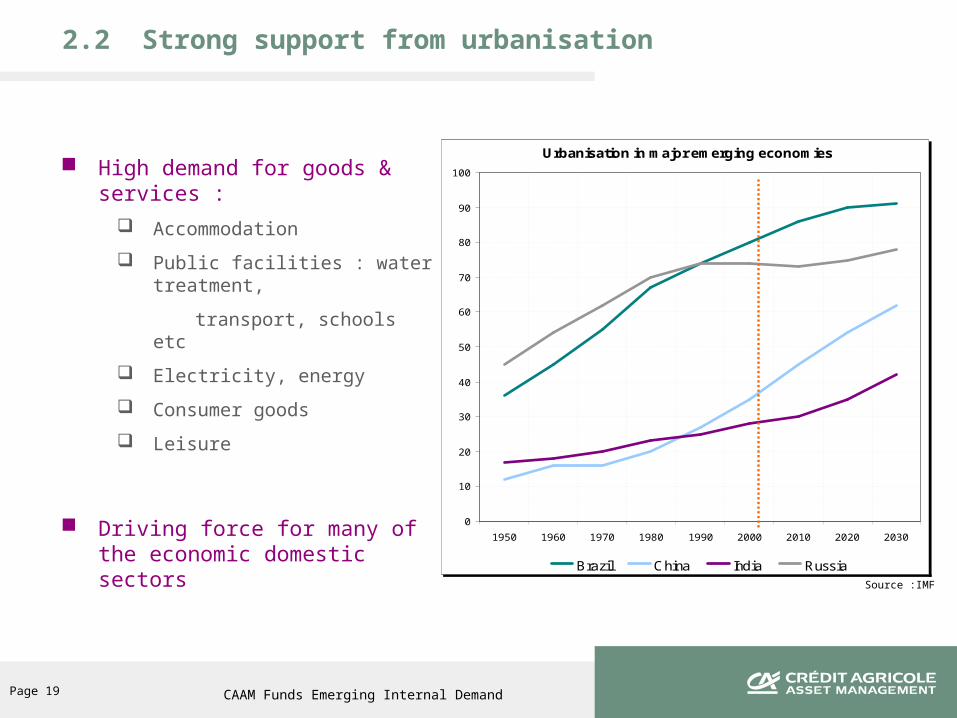

2.2 Strong support from urbanisation

High demand for goods & services :

Accommodation

Public facilities : water treatment,

transport, schools etc

Electricity, energy

Consumer goods

Leisure

Driving force for many of the economic domestic sectors

Urbanisation in major emerging economies

0

10

20

30

40

50

60

70

80

90

100

1950 1960 1970 1980 1990 2000 2010 2020 2030

Brazil China India Russia

Source :IMF

3. CAAM Funds Emerging Internal Demand

Page 21 CAAM Funds Emerging Internal Demand

An important contributor to world growth

Strong fundamentals supportive of a high and stable growth : Increasing purchasing power and demographics supportive of an increase in consumption Huge investments requirements compared to developed countries

Should provide investors with some protection from slowing developed economies

Internal Demand in emerging countries: an opportunity for investors…

3.1 CAAM Funds Emerging Internal demand: concept & attractiveness

Internal Demand: an economic concept…

Household consumption

Corporate investments

Government spending

DOMESTIC DEMAND = + +

CAAM Funds Emerging Internal Demand Focus on companies exposed to emerging domestic demand

Using tested investment philosophy and process

Page 22 CAAM Funds Emerging Internal Demand

3.2 CAAM Funds Emerging Internal Demand key features (1/2)

Fund objective:

Outperform the MSCI Emerging Markets by benefiting from the growth potential of emerging countries' growing domestic demand

Focus on companies that sell most of their goods and services to Emerging Countries

Favor sectors catering to Internal Demand

Consumer Discretionary, Consumer Staples, Finance, Industry, Telecom and Public Utilities

Sectors most likely to be underweight are those most linked to developed economies :

Technology, Healthcare, Energy, Materials

Page 23 CAAM Funds Emerging Internal Demand

CAAM Funds Emerging Internal Demand should be less volatile than other GEM funds

Source: CAAM

3.2 CAAM Funds Emerging Internal Demand key features (2/2)

Volatility 3 years (monthly performance)

10%

15%

20%

25%

30%

35%

40%

févr

.-9

7

ao

ût-

97

févr

.-9

8

ao

ût-

98

févr

.-9

9

ao

ût-

99

févr

.-0

0

ao

ût-

00

févr

.-0

1

ao

ût-

01

févr

.-0

2

ao

ût-

02

févr

.-0

3

ao

ût-

03

févr

.-0

4

ao

ût-

04

févr

.-0

5

ao

ût-

05

févr

.-0

6

ao

ût-

06

févr

.-0

7

ao

ût-

07

MSCI EMF Domestic sectors MSCI EMF External sectors

MSCI EMF MSCI Bric

Page 24 CAAM Funds Emerging Internal Demand

3.3 Tested investment philosophy

Our convictions

Fundamental analysis and judgemental decisions

Anticipating changes

Arbitraging prospects vs. valuations vs. risks

3 sources of alpha generation: country selection, sector allocation & stock picking

Exposure to small/mid cap stocks

Risk diversification

Medium term investments

Average 18 months holding

Page 25 CAAM Funds Emerging Internal Demand

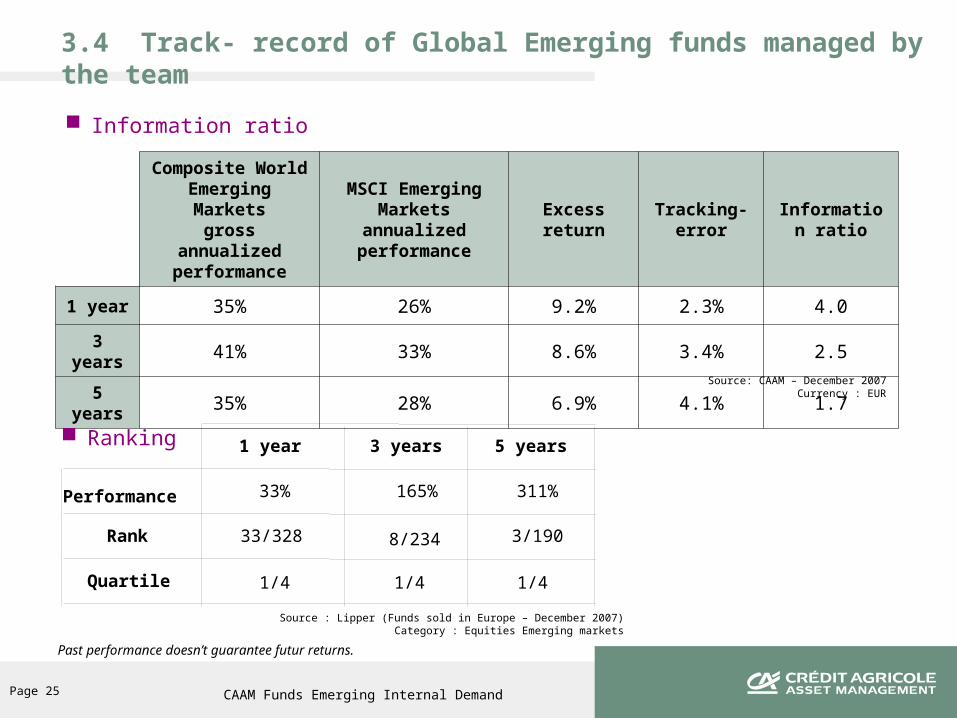

Information ratio

Composite World Emerging Marketsgross annualized

performance

MSCI Emerging Markets annualized

performance

Excess return

Tracking-error

Information ratio

1 year 35% 26% 9.2% 2.3% 4.0

3 years 41% 33% 8.6% 3.4% 2.5

5 years 35% 28% 6.9% 4.1% 1.7

Source: CAAM – December 2007Currency : EUR

3.4 Track- record of Global Emerging funds managed by the team

Source : Lipper (Funds sold in Europe – December 2007)Category : Equities Emerging markets

1 year 3 years 5 years

Performance 33% 165% 311%

Rank 33/328 8/234 3/190

Quartile 1/4 1/4 1/4

Ranking

Past performance doesn’t guarantee futur returns.

Page 26 CAAM Funds Emerging Internal Demand

3.5 Strengths of CAAM expertise

A team of 7 investment professionnals dedicated to emerging equity management with complementary skills

Latin America managers: Patrice Lemonnier (CFA) and Lionel Bernard Emerging Asia: Philippe Guigny and Mickaël Tricot (CFA) Emerging Europe, Middle East and Africa: Nina de Martinis (CFA) Analysts: Hélène Ecalle and Qian Jang

Recognised for its expertise and good track-record* Lipper Funds Awards (2008)

Award Trophy for CAAM Funds Latin America Equities C Cap (USD)-Equity Emerging Markets Latin America, over 3, 5 and 10 years in Switzerland / Best fund in Spain over 3 years for « Equity Emerging Markets Latin America » : CAAM Funds Latin America Equities C Cap (USD).

Lipper Funds Awards (2007)Best fund over 10 years in the category « Equity Emerging Latin America » in Italy, Spain, France, Austria, North Countries, Germany and Switzerland for CAAM Latin America Equities C Cap

La Tribune-Standard&Poor’s (march 2007)1st place over 1 year and the 2nd place over 3 and 5 years in the category « emerging countries equities » for a french domiciled fund.

Mieux VivreVotre Argent (march 2007)Excellence Label for a french domiciled fund and Regularity Label for a french domiciled Global Emerging Equity fund.

With a large product range Global emerging equity funds Latin America equity fund Europe emerging equity fund

More than €2 billion under management (as at 31/12/2007)

* Past performance doesn’t guarantee future returns.

Page 27 CAAM Funds Emerging Internal Demand

CAAM Funds Emerging Internal Demand – Fund information

Classic (C) Institutional (I) Classic S* (S)

Management company Crédit Agricole Asset Management Luxembourg S.A.

Investment manager Crédit Agricole Asset Management

Custodian CACEIS Bank Luxembourg

Reference currency USD

Minimum recommended period 5 years

Countries registered for sales as at 14/04/2008

Austria, Belgium, Finland, France, Germany, Hong Kong, Irland, Italy, Luxembourg, The Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, United Kingdom

Isin Code Accumulation :

LU0319685854

Distribution :

LU0319686076

Accumulation :

LU0319685342

Distribution :

LU00319685425

LU0319686159

Minimum initial subscription None USD 500 000** None

Share categories Accumulation / Distribution Accumulation

Frequency of NAV calculation Daily

Cut off for dealing times Luxembourg dealing days before 2pm***

Maximum initial charge 4.50% 2.50% 3.00%

Maximum annual management fee 1.60% 1.00% 2.00%

Annual administration fee 0.50% 0.40% 0.50%

Performance fee None

Maximum conversion fee 1.00%

Maximum redemption fee None

Not all share classes and, as the case may be, share categories are registered for sales in all countries

* Only for distributors authorised by Board of Directors.** Or equivalent in another currency.*** Or, as the case may be, an earlier cut off time applicable by the relevant distributor.

Page 28 CAAM Funds Emerging Internal Demand

Disclaimer

This document which is not contractual and not part of documents usually certified by statutory auditors, is provided solely for information purposes by Crédit Agricole Asset Management, based on sources that we consider to be reliable. Crédit Agricole Asset Management can in no way be held responsible for any decision made on the basis of information contained in this document.

The information contained in this document doesn’t constitute a recommendation, a request for proposal or an invitation to purchase, sell or switch shares in the funds (Organismes de Placement Collectif en Valeurs Mobilières or OPCVM, UCITS) described herein, and should in no case be interpreted as such. The information contained in this document may be modified without prior notice. Additional information is available upon request. The information contained in this document is disclosed to you on a confidential basis and you agree it shall not be copied, reproduced, or distributed to a third party without our prior written approval. The information contained in this document is not intended for all categories of customers.

Your attention is drawn to the fact that units or shares in these UCITS may not be purchased if the regulations of your country of origin or any other applicable regulation forbid such purchase. As a consequence, it is your responsibility, prior to subscribing to any shares, to ensure that such purchase is permitted by applicable laws and regulations, as well as to inform yourself as to the fiscal consequences of such investment. It is also your responsibility to read the legal documents in force for each UCITS, in particular the prospectus as approved by the AMF (French Regulatory Authority) and the CSSF (Luxembourg Regulatory Authority) which are available upon request.

Past performance does not prejudge future results, nor is it a guarantee of future returns. The value of units or shares in UCITS may fluctuate according to market conditions and as a result the value of initial investments may rise as well as fall.

Document issued by Crédit Agricole Asset Management , a limited company ( “ French société anonyme”) with a registered capital of € 546 162 915, head office : 90 Boulevard Pasteur, 75 015 PARIS, 437 574 452 RCS Paris.Crédit Agricole Asset Management is a portfolio management company approved by the AMF (Autorité des Marchés Financiers), the French Securities Regulator under n° GP 04000036www.caam.com

This document contains information about CAAM Funds Emerging Internal Demand (the “Sub-Funds”), a sub-fund of CAAM Funds (the “Sicav”), an undertaking for collective investment in transferable securities existing under Part I of the Luxembourg law of 20 December 2002, organised as a société d’investissement à capital variable and registered with the Luxembourg Trade and Companies Register under number B68.806. The Sicav has its registered office at 5, Allée Scheffer, l-2520 Luxembourg.The Sub-Fund has been authorised for public sale by the Commision de Surveillance du Secteur Financier in Luxembourg. The Sicav comprises other sub-funds which are described in the Sicav’s full and simplified prospectus. Not all sub-funds will be necessarily be registered or authorised for sales in all jurisdictions or be available to all investors. Subscriptions in the Sub-Funds will only be accepted on the basis of the Sicav’s latest complete and simplified prospectuses and its latest annual and semi-annual reports that may be obtained, at the registered office of the Sicav or at its local representative. The name of the local representative may be obtained at the Sicav's registered office.Consideration should be given to whether the risks attached to an investment in the Sub-Funds are suitable for prospective investors who should ensure that they fully understand the contents of this document. In case of doubt, it is advised to consult a professional advisor to determine whether an investment in the Sub-Funds is suitable.The value of, and any income from, an investment in the Sub-Funds can decrease as well as increase. The Sub-Funds have no guaranteed performance. Further, past performance is not a guarantee or a reliable indicator for future returns.This document does not constitute an offer to buy nor a solicitation to sell in any country where it might be considered as unlawful, nor does it constitute public advertising or investment advice.This document is solely for the attention of institutional, professional or sophisticated investors and is not to be distributed to the general public.