caixabank - the leading force in spanish retail banking · peer group includes: bbva, bkia, popular...

TRANSCRIPT

CaixaBank - the leading force in Spanish retail banking May 2012 Corporate presentation

2

Important note

The purpose of this presentation is purely informative. In particular, regarding the data provided by third parties, neither CaixaBank, S.A. (“CaixaBank”) as a legal entity, nor any of its administrators, directors or employees, is obliged, either explicitly or implicitly, to vouch that these contents are exact, accurate, comprehensive or complete, nor to keep them updated, nor to correct them in the case that any deficiency, error or omission were to be detected. Moreover, in reproducing these contents in any medium, CaixaBank may introduce any changes it deems suitable, may omit partially or completely any of the elementsof this document, and in the case of any deviation between such a version and this one, assumes no liability for any discrepancy.

This document has at no time been submitted to the Comisión Nacional del Mercado de Valores (CNMV – the Spanish Stock Markets regulatory body) for approval or scrutiny. In all cases its contents are regulated by the Spanish law applicable at time of writing, and it is not addressed to any person or legal entity located in any other jurisdiction. For this reason it may not necessarily comply with the prevailing norms or legal requisites as required in other jurisdictions.

This presentation on no account should be construed as a service of financial analysis or advice, nor does it aim to offer any kind of financial product or service. In particular, it is expressly remarked here that no information herein contained should be taken as a guarantee of future performance or results.

Without prejudice to legal requirements, or to any limitations imposed by CaixaBank that may be applicable, permission is hereby expressly refused for any type of use or exploitation of the contents of this presentation, and for any use of the signs, trademarks and logotypes which it contains. This prohibition extends to any kind of reproduction, distribution, transmission to third parties, public communication or conversion into any other medium, for commercial purposes, without the previous express permission of CaixaBank and/or other respective proprietary title holders. Any failure to observe this restriction may constitute a legal infraction which may be sanctioned by the prevailing laws in such cases.

• 3rd financial group in Spain • Assets: €277.6 bn • Business volume: €429.5bn (€183.9bn loans + €245.6bn customer funds)

CaixaBank at a glance

• 10.4 million customers serviced by a segmented business model • Multi-channel platform: branches (5,172); ATMs (7,979); online and mobile banking • Excellence in customer service and highly-rated brand

• Diversified and good quality loan portfolio • NPL Ratio: 5.25%; Coverage ratio 61% (138% with mortgage guarantees)

• Comfortable liquidity position: €29.4 bn • Solid base of capital: core capital of 12.4% (BIS II), ~ 10.5% Core capital (BIS III,

fully phased-in)

Figures as of March 2012

A flagship institution

Ranked 1st in retail banking in Spain

Sound Risk profile

Robust financial metrics

3

1. CaixaBank overview

“la Caixa” Group Reorganisation

4

Real Estate assets

New structure

81.1%1

Retail Banking & Insurance Other industrial

portfolio

(former Criteria, Listed)

Repsol + Telefonica

100%

(1) Does not take into account the mandatory convertible bond of €1.5 Bn (2) Book Value as of June 2011

International Banking portfolio

Welfare Projects

CaixaBank Book Value2: €21.6 bn

CaixaHolding Book Value2: €10.3 bn

(Not listed)

5

Strategic rationale

Consolidates CaixaBank’s leadership position in Spanish banking

Increases number of core markets with dominant position (#1 player in 5 regions)

Leads to c. 15% market share in key retail products

€540 M of expected annual cost synergies by 2014; 12.5% of total combined costs

NPV of cost synergies of €1.8 Bn

€1.1 Bn of net restructuring costs

Material income synergies to be expected

€3.41 bn business combination fair value adjustments, implying a zero cost of risk for the acquired loan book.

The combined entity will have 82% NPL coverage

Sound capital (>10% FY12E Core Capital) and liquidity position

Solid balance sheet metrics maintained

Improves competitive

position

Enhances profitability

(1) Includes €2.8 bn of adjustments in the loan portfolio, €0.3 bn of real estate adjustments and €0.3 bn of other adjustments

EPS accretive from 2013 and +20% by 2014

Strengthens CaixaBank dividend policy in the medium term

Sustainable RoE improvement (PF 2011 ROE of 7% vs. 5% CABK)

ROIC ~ 20% by 2014

Increases Shareholder

value

Integration agreement with Banca Cívica

Significant asset clean-up to result from the transaction

6 6

As a result, the combined entity will have a sound balance sheet, with 82% NPL coverage level, significantly above the 58.2% sector average

Fair value adjustment – €3.4 Bn

A fair value adjustment will be made against BCIV’s reserves:

No P&L impact: offset against any potential gain arising from acquiring BCIV below book value

This significant effort will imply a reduction in future provisioning requirements, leading to related improvements in future net profits

These adjustments are on top of €2Bn fair value adjustments of BCIV made July 2011.

2.8

0.30.3

Loan portfolio

Real Estate1

Other

(1) Includes €0.2 bn of adjustments related to foreclosed assets + €0.1 bn of other adjustments

Balance Sheet: Integration agreement with Banca Cívica

128%

82%67%

60% 54% 48% 45% 45% 44%

BCIV PF CABK + BCIV PF

BCIV CABK Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

7

The combination results in one of the best levels of asset quality

NPL loans ratio well below the sector average

4.9% 4.9%5.5% 5.5%

5.9% 6.0%

7.4% 7.6%

CABK Peer 1 CABK + BCIV PF

Peer 2 Peer 3 Peer 4 BCIV Peer 5

Sector Average: 7.62%

NPL coverage significantly above the sector average

Sector Average: 58.2%

Peer group includes: BBVA, BKIA, Popular + Pastor, Sabadell and Grupo Santander Spain Banca Cívica pro forma for the extraordinary provisioning Information as of December 2011 except for NPL loans of Popular + Pastor PF (July 2011) . BBVA excluding Unnim & Sabadell excluding CAM (NPL loans and coverage are not homogeneous due to APS – Asset Protection Scheme)

NPL loans (%) NPL coverage (%)

Balance Sheet: Integration agreement with Banca Cívica

Banca Cívica was Spain’s 10th largest financial institution based on total assets

Banca Cívica: key figures

Resulting from the merger of Caja Navarra, CajaSol, Caja Burgos and Caja Canarias

45%

11%

12%

16%

16%

Free float

Caja Canarias

CAN

CajaSol

Caja de Burgos Shareholders agreement

55%

Shareholding structure

Assets

Net loans

Deposits1

Shareholder’s funds

Core Capital2

Branches

Customers

Employees

€72 Bn

€49 Bn

€38 Bn

€2.9 Bn

9.0%

1,394

3.9 M

7,800

Information as of December 2011 (1) Excluding “cédulas multicedentes” (2) FROB included

8

2.3% market share by total assets

Integration agreement with Banca Cívica

A market leader in complementary regions

9 Information as of December 2011 Source FRS

Leading market shares in core regions Market share (%)

3.1% market share in deposits and

loans

Branch network focused in core regions Branches by CCAA

174

634

125

206

1,394 branches, o/w 80% in core regions

25.7

16.0

10.1

4.5

34.5

17.6

8.7 7.1

40.4

20.6

12.4

7.2

Navarra Canarias Andalucía C. León

Branches Loans Deposits

Integration agreement with Banca Cívica

A retail oriented bank with 3.9 million customers

49% 40%

11%

Demand deposits

Other

Time deposits

In % In %

46%

17%

25% Corporate & SMEs

Consumer

Retail mortgages

8%

RE Developers & construction

10

Total deposits1 €38 bn Total net loans €49 bn

Deposits breakdown Loan book breakdown

Information as of December 2011 (1) Excluding “cédulas multicedentes”

4%

Public sector

Integration agreement with Banca Cívica

11

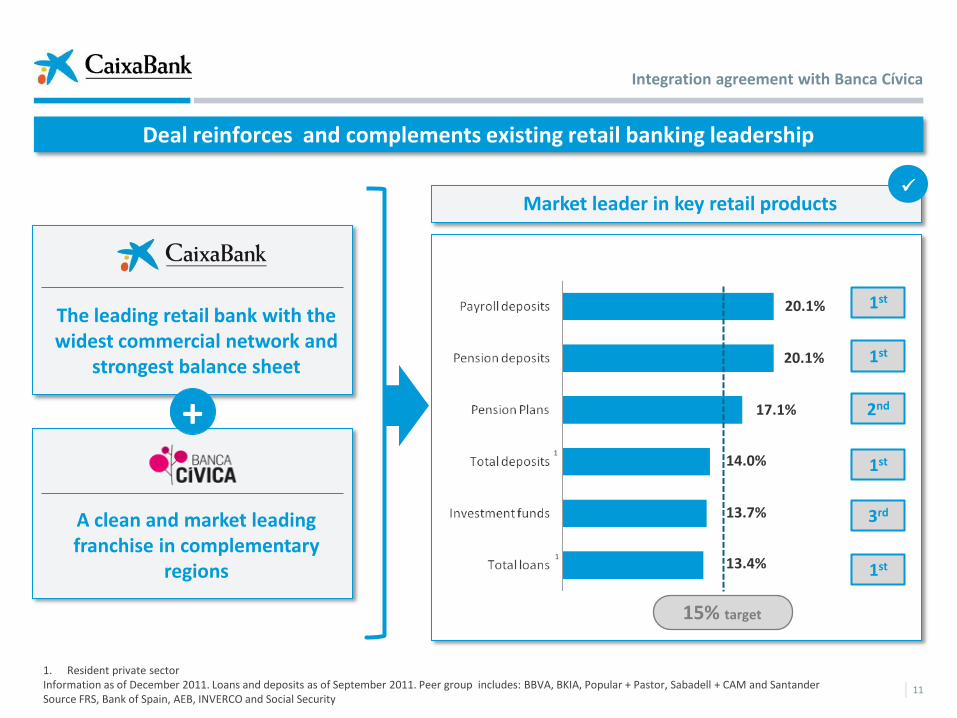

Deal reinforces and complements existing retail banking leadership

A clean and market leading franchise in complementary

regions

Market leader in key retail products

1. Resident private sector Information as of December 2011. Loans and deposits as of September 2011. Peer group includes: BBVA, BKIA, Popular + Pastor, Sabadell + CAM and Santander Source FRS, Bank of Spain, AEB, INVERCO and Social Security

The leading retail bank with the widest commercial network and

strongest balance sheet

+

15% target

20.1%

20.1%

17.1%

14.0%

13.7%

13.4%

1st

1st

2nd

1st

3rd

1st

1

1

Integration agreement with Banca Cívica

12

Deal consolidates retail banking leadership across key performance indicators

Total assets - € Bn

Deposits(1) - € Bn

Net loans to customers - € Bn

BCIV: 72

CABK: 270

342 339 338

306

171 161

1st

BCIV: 50

CABK: 129

179 174 155

134 108

96

1st

BCIV: 49

CABK: 182

231 227 218 186

120 118

1st

Market share by branches(2) (%)

BCIV: 3.5%

CABK: 12.7%

16.2%

11.3%

9.7% 8.9% 6.0% 5.6%

1st

Information as of December 2011. Peer group includes: BBVA (Spain) + Unnim, BKIA, Popular + Pastor, Sabadell + CAM and Grupo Santander Spain (1) Deposits as shown in financial reports (2) Market share information based on branches as of December 11 (CABK + BCIV – before network optimisation)

Integration agreement with Banca Cívica

Credit quality still mostly driven by developer book

13 (1) Includes Servihabitat and other subsidiaries of Caja de Ahorros y Pensiones de Barcelona, CaixaBank’s major shareholder (2) Includes contingent liabilities

Increase in total NPL ratio mostly explained by real estate developers

Limited deterioration in other segments; in line with expectations

Loans to individuals

Residential mortgages

Consumer credit

Loans to businesses

Corporate and SMEs

Real estate developers

ServiHabitat and other “la Caixa” Group subs1

Public sector

Total loans

Loan book and NPL by segments

93.7

69.7

24.0

81.0

55.5

22.4

3.1

11.3

186.0

1.82%

1.48%

2.81%

9.54%

3.49%

25.84%

0.00%

0.40%

4.90%

€bn NPL ratio2

31st December 2011

92.5

69.1

23.4

79.8

55.0

21.7

3.1

11.6

183.9

1.95%

1.57%

3.07%

10.37%

3.93%

28.16%

0.00%

0.66%

5.25%

€bn NPL ratio2

31st March 2012

Solid balance sheet

Uptick in NPLs in line with 2011 trends but supported by higher coverage

14

NPLs and NPL ratio (€MM) Provisioning effort to reinforce high NPL coverage

NPLs

NPL ratio

NPL Coverage ratio

Credit Provisions

Sector:

8.16% (Feb’12)

Sector:

57% (Feb’12)

(1) €1.9 bn additions and €1.3 bn derecognitions from NPLs, of which €156 M correspond to loan write offs

(1)

Solid balance sheet

Exposure to real estate developers continues to decline

15

28% reduction in balance of real estate developer loans since December 2008

Real estate developer loan breakdown (€ bn)

€12.7bn

€2.9bn

€6.1bn

(1) Source: Bank of Spain (Table 4.18 “Actividades inmobiliarias”) (2) Impacted by the acquisition of Caixa Girona

€21.7 bn Coverage (%)

€4.5 bn provisions

for RE developers

Provisions required by Royal Decree 2/12 reinforce RE coverage ratios

Real estate developer loan evolution: CaixaBank vs sector1

-7%

-28%

Performing

Substandard

NPL

7.0%

41.1%

40.2%

Solid balance sheet

Building Center1 Repossessed real estate assets

Intense commercial activity with low losses on sales prove fair assets valuations

16

31st March

Net

amount %

coverage

RE assets from loans to construction and RE development

1,200 37%

Finished buildings 884 25%

Buildings under construction 54 44%

Land 262 59%

RE assets from mortgage loans to households

343 30%

Other repossessed assets 31 21%

(1) The real estate holding company of CaixaBank, S.A. (2) Data from Dec 31st 2011 to April 5th 2012 (3) Calculated as selling price minus direct selling and administrative expenses (4) Total stock of rental assets: €141 M for Building Center

Inflows of foreclosures in line with aggressive management of developer book

1,574

36% coverage of portfolio (inc. write-downs)

All assets appraised in 2011

Limited land exposure

36%

16

Building Center 2012 commercial activity2

TOTAL (NET)

Sales

€318M

Rental Assets4

Commitments

€M

4.9% Yield on

rental sales

-4.2% Margin on

sales3 1,707 units

Solid balance sheet

17

Real estate: problematic assets and total exposure coverage

Real Estate problematic assets coverage Total Real Estate exposure coverage

Total assets

Foreclosed1

NPLs

Substandard

Performing

RE provisions

Foreclosed

NPLs

Substandard

Performing

Total RE exposure coverage

RE problematic assets

Foreclosed1

NPLs

Substandard

RE provisions

Foreclosed

NPLs

Substandard

Performing

RE problematic exposure coverage

24.1

2.4

6.1

2.9

12.7

5.3

0.9

2.4

1.2

0.8

22%

24.3

1.8

5.8

3.0

13.7

2.9

0.6

1.8

0.5

0.0

12%2

11.4

2.4

6.1

2.9

10.6

1.8

5.8

3.0

5.3

0.9

2.4

1.2

0.8

2.9

0.6

1.8

0.5

0.0

27%2

Dec’11 Mar’12 Billion euros Dec’11 Mar’12 Billion euros

1. Loan equivalent 2. Does not include generic provision

47% 22%

Solid balance sheet

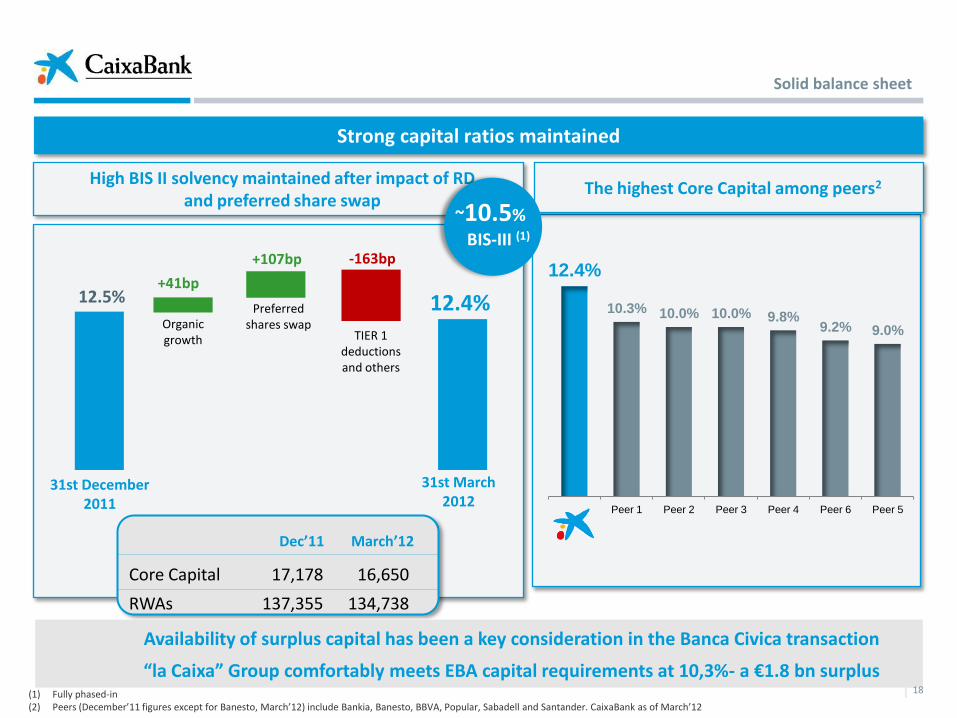

Strong capital ratios maintained

18 (1) Fully phased-in (2) Peers (December’11 figures except for Banesto, March’12) include Bankia, Banesto, BBVA, Popular, Sabadell and Santander. CaixaBank as of March’12

Availability of surplus capital has been a key consideration in the Banca Civica transaction

“la Caixa” Group comfortably meets EBA capital requirements at 10,3%- a €1.8 bn surplus

17,178

137,355

31st December 2011

31st March 2012

Organic growth

Preferred shares swap

+41bp

+107bp

12.5% 12.4% ~10%

BIS-III (1)

Dec’11

16,650

134,738

March’12

Core Capital

RWAs

The highest Core Capital among peers2 High BIS II solvency maintained after impact of RD

and preferred share swap

TIER 1 deductions and others

-163bp

~10.5%

BIS-III (1)

12.4%

10.3% 10.0% 10.0% 9.8% 9.2% 9.0%

Peer 1 Peer 2 Peer 3 Peer 4 Peer 6 Peer 5

Solid balance sheet

+ 71 bp

+ 51 bp- 39 bp - 45 bp- 26 bp

- 218 bp

12.5% 12.1%

10.4%

Dec 11 Hybrid debtbuy-back(CABK)

Dec 11Pro formaHyb. debt

buy-back CABK

Capitalincrease

TransactionGoodwill

Restructuringcosts

Capitalrequirements

Hybrid debtbuy-back

(BCIV)

Dec 11CABK + BCIV PF

Balance Sheet: Integration agreement with Banca Cívica

19

Core Capital BIS II

Resulting in a more efficient capital base (10.4% PF Dec 11 BIS II Core Capital)

Capital impact: 167 bps

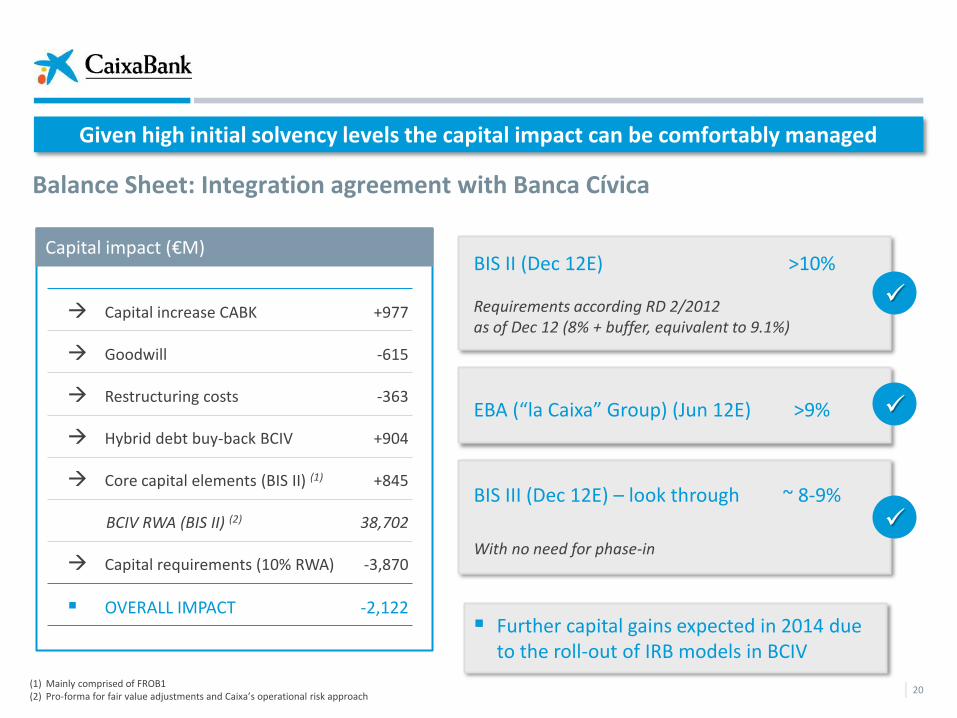

Given high initial solvency levels the capital impact can be comfortably managed

20

BIS II (Dec 12E) >10%

Requirements according RD 2/2012 as of Dec 12 (8% + buffer, equivalent to 9.1%)

EBA (“la Caixa” Group) (Jun 12E) >9%

BIS III (Dec 12E) – look through ~ 8-9%

With no need for phase-in

Capital increase CABK

Goodwill

Restructuring costs

Hybrid debt buy-back BCIV

Core capital elements (BIS II) (1)

BCIV RWA (BIS II) (2)

Capital requirements (10% RWA)

OVERALL IMPACT

+977

-615

-363

+904

+845

38,702

-3,870

-2,122

Capital impact (€M)

(1) Mainly comprised of FROB1 (2) Pro-forma for fair value adjustments and Caixa’s operational risk approach

Further capital gains expected in 2014 due to the roll-out of IRB models in BCIV

Balance Sheet: Integration agreement with Banca Cívica

21

Liquidity flexiblity remains a key tool for balance sheet management

(1) Includes cash, interbank deposits, accounts at central banks and short duration unencumbered Spanish sovereign debt.

€29.4bn 10.6%

CaixaBank Assets

€20.9bn

Unused ECB discount facility

Balance sheet liquidity1

Solid balance sheet

€20.9bn

Unused ECB discount facility

Balance sheet liquidity1

€19.6bn

7.7% CaixaBank

Assets

1st ECB 3YR facility: €12.4 bn, used to:

o Anticipate 2012 maturities o Replace LCH repo funding o Provide additional liquidity cushion

2t ECB 3YR facility: €6.08 bn, used to:

o Anticipate 2013 maturities

€ 19.6bn

22

(1) Defined as: gross loans (€183,886 M) net of loan provisions (€6,203 M) (total loan provisions excluding those corresponding to contingent guarantees) and excluding pass-through funding from multilateral agencies (€5,900 M) / retail funds (deposits, retail issuances) (€133,211 M)

(2) From April to December 2012

Wholesale maturities remain at comfortable levels

Wholesale maturities (€bn)

1Q12: €0.4 bn redeemed and €1.0 bn issued

LTD ratio(1) reduced by 4 pp over the year

Net loans declined by 1.6% and retail customer funds increased by 1.7%

129%

2

11.1

1.0

9.8

2.1

Dec 2011

23

Total liquidity: €24 Bn

~ 7.0% CABK + BCIV

PF Assets 65%

12%

23%

Client funds

Net Interbank Deposits

and repos

Wholesale funding

Current liquidity covers future maturities

Manageable maturity profile

Total Financing: €259 Bn

Information as of December 2011 (1) Includes collateral that can be included in the facility (2) Mortgage and public sector covered bonds

€12.2 Bn ECB discount

facility(1)

€11.9 Bn Balance sheet

liquidity

(€ Bn)

Additional issuance

capacity(2): 31.7 Bn

2.3

6.16.9

4.3

1.91.36.6

8.0 8.2

2012 2013 2014

Liquidity levels to remain comfortably high after the proposed deal

BCIV

CABK

BCIV

CABK

BCIV

CABK

Liquidity level Financing structure Wholesale maturities

Balance Sheet: Integration agreement with Banca Cívica

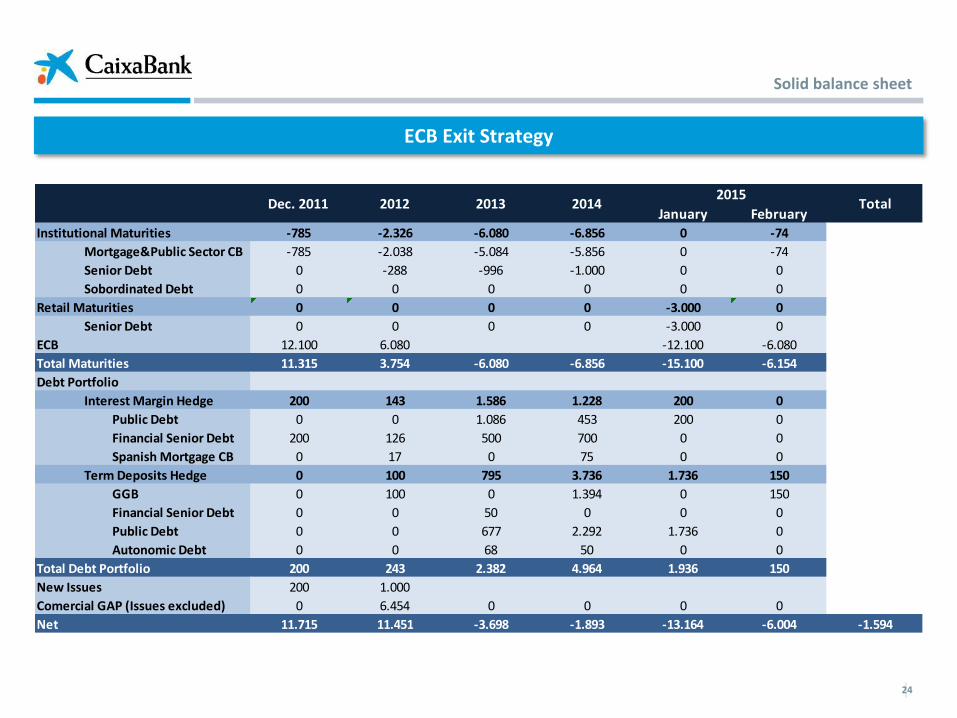

ECB Exit Strategy

24

2015

January February

Institutional Maturities -785 -2.326 -6.080 -6.856 0 -74

Mortgage&Public Sector CB -785 -2.038 -5.084 -5.856 0 -74

Senior Debt 0 -288 -996 -1.000 0 0

Sobordinated Debt 0 0 0 0 0 0

Retail Maturities 0 0 0 0 -3.000 0

Senior Debt 0 0 0 0 -3.000 0

ECB 12.100 6.080 -12.100 -6.080

Total Maturities 11.315 3.754 -6.080 -6.856 -15.100 -6.154

Debt Portfolio

Interest Margin Hedge 200 143 1.586 1.228 200 0

Public Debt 0 0 1.086 453 200 0

Financial Senior Debt 200 126 500 700 0 0

Spanish Mortgage CB 0 17 0 75 0 0

Term Deposits Hedge 0 100 795 3.736 1.736 150

GGB 0 100 0 1.394 0 150

Financial Senior Debt 0 0 50 0 0 0

Public Debt 0 0 677 2.292 1.736 0

Autonomic Debt 0 0 68 50 0 0

Total Debt Portfolio 200 243 2.382 4.964 1.936 150

New Issues 200 1.000

Comercial GAP (Issues excluded) 0 6.454 0 0 0 0

Net 11.715 11.451 -3.698 -1.893 -13.164 -6.004 -1.594

Dec. 2011 2012 2013 2014 Total

Solid balance sheet

25

Encumbered vs Unencumbered Assets: Remaining Issuing Capacity

LOAN PORTFOLIO as of March 31st 2012 TOTAL COVERED BONDS RMBS/ABS

AVAILABLE FOR

SENIOR DEBT

USED COLLATERAL UNUSED

MORTGAGES PORTFOLIO 117.533 49.846 49.495 18.193

PUBLIC SECTOR PORTFOLIO 12.413 7.714 4.684 15

OTHER LOAN PORTFOLIO 43.130 - - 4.007 39.123

LOANS TO CUSTOMERS 173.077 57.560 54.179 22.215 39.123

ENCUMBERED ASSETS (REPOS) 4.612

INSURANCE COMPANIES ASSETS 24.843

REST OF ASSETS 75.078 75.078

TOTAL ASSETS as of March 31st 2012 277.610 57.560 54.179 22.215 114.202

As of March 31st 2012 PUBLIC ISSUANCE

RETAINED /

ECB COLLATERAL TOTAL USED

MORTGAGES COVERED BONDS (€49,633 collateral) (*) 39.252 625 39.877

PUBLIC SECTOR COVERED BONDS (€7,714 collateral) (*) 1.400 4.000 5.400

RMBS/ABS 22.215 22.215

SENIOR DEBT 5.000 5.000

TOTAL issued 45.653 26.840 72.492

(*) Used Collateral = Issued amount of Cédulas Hipotecarias divided by 0.80

and Issued amount of Cédulas Territoriales divided by 0.70

26

CaixaBank Covered Bond Issuing Capabities (as of March 31st 2012)

18,193 15 18,208

Mortgages Public Sector Total

LOAN PORTFOLIO 117,534 12,413 131,824

Used in RMBS/ABS <18,193> <15> <18,208>

Total Collateral for Covered Bonds 99,341 12,398 111,249

Elligible Portfolio (1) 71,822 12,398

Cedulas

Hipotecarias

Cedulas

Territoriales

Used Collateral (2) 49,846 7,714

Covered Bond Issued Amount 39,877 5,400

Over Collaterization 249% 230%

Available Collateral (1-2) 21,976 4,684

REMAINING ISSUING CAPACITY (*) 17,581 3,279 20,860 Available Issuing Capacity

(*) Issuing Capacity= 80% of Collateral Available for C. Hipotecarias and 70% for Cedulas Territoriales

27

CaixaBank: Institutional and Retail Issues: Maturity Profile

Overview Balance per LTV-band

Specific Loan and Borrower

characteristics

CATALONIA 35.8%

VALENCIA 7.0%

ANDALUSIA 12.7%

MADRID 15.9%

Main Country regional Distribution

Cover Pool Information (ex-securitizations) – Residential Assets, as of March 2012

WA Seasoning (in months) 60.4

BALEARIC I.

5%

(*) Regions with weight >5.0% 28

Total Mortgage Loans (ex securitization) (€ mll) 68,791,100

Number of loans 870,901

Average Loan balance 78,988

Number of Borrowers 739,442

Number of properties 818,329

WA Seasoning in months 66

WA Remaining term in months 277

Avg LTV (%) 48%

WA LTV (%) 59.5%

% of Floating Rate loans: 99.7%

WA Interest Rate (Floating Rate loans) 2.98%

WA Interest Rate (Fixed Rate loans) 5.33%

17%

12%

16%

23%21%

4% 4% 3%1% 0% 0%

0%

5%

10%

15%

20%

25%

6%

9%

6%

19%

59%

< 12

≥12-<24

≥24-<36

≥36-<60

≥60

First Home91%

2nd Home6%

Rented2%

Other1%

Overview Balance per LTV-band

CATALONIA 29.7%

VALENCIA 6.5%

ANDALUSIA 16.0%

MADRID 24.6%

Main Country regional Distribution

Cover Pool Information (ex-securitizations) – Commercial Assets as of March 2012

Loan Maturity

(*) Regions with weight >5.0%

29

Total Mortgage Loans (ex securitization) (€ mll) 30,549,914

Number of loans 153,562

Average Loan balance 198,942

Number of Borrowers 59,517

Number of properties 161,919

WA Seasoning in months 54

WA Remaining term in months 202

Average LTV (%) 46.7%

WA LTV (%) 59.6%

% of Floating Rate loans: 98.7%

WA Interest Rate (Floating Rate loans) 3.17%

WA Interest Rate (Fixed Rate loans) 4.94%

18%14%

18%

24%

14%

2% 2% 2% 4%0% 2%

0%

5%

10%

15%

20%

25%

30%

18%

15%

14%

16%

37%

≤ 5

>5 - ≤10

>10 - ≤15

>15 - ≤25

>25 - ≤50

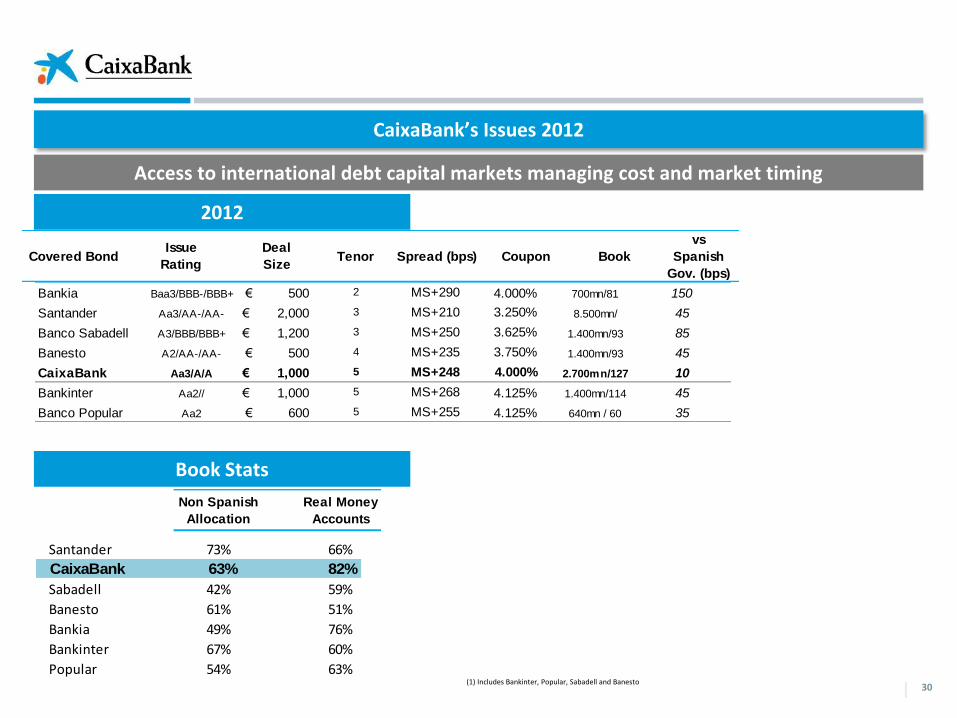

CaixaBank’s Issues 2012

30

Access to international debt capital markets managing cost and market timing

2012

Book Stats

Covered BondsRating

Emisión

Deal

Size

Plazo

añosSpread Cupón Demanda

vs

Spanish Gov

Bankia Baa3/BBB-/BBB+ 500€ 2 MS+290 4.000% 700mn/81 150

Santander Aa3/AA-/AA- 2,000€ 3 MS+210 3.250% 8.500mn/ 45

Banco Sabadell A3/BBB/BBB+ 1,200€ 3 MS+250 3.625% 1.400mn/93 85

Banesto A2/AA-/AA- 500€ 4 MS+235 3.750% 1.400mn/93 45

CaixaBank Aa3/A/A 1,000€ 5 MS+248 4.000% 2.700mn/127 10

Bankinter Aa2// 1,000€ 5 MS+268 4.125% 1.400mn/114 45

Banco Popular Aa2 600€ 5 MS+255 4.125% 640mn / 60 35

Non Spanish

Allocation

Real Money

Accounts

Santander 73% 66%

CaixaBank 63% 82%

Sabadell 42% 59%

Banesto 61% 51%

Bankia 49% 76%

Bankinter 67% 60%

Popular 54% 63%(1) Includes Bankinter, Popular, Sabadell and Banesto

Covered BondIssue

Rating

Deal

SizeTenor Spread (bps) Coupon Book

vs

Spanish

Gov. (bps)

CaixaBank 63% 82%

31

Ratings

Ratings

(1) Ratings on review for possible downgrade

Moody’s Investors Service A3

BBB+

A-

P-2

A-2

F2

(1)

(1)

(1)

Long term

Short term

Outlook Cédulas Hipotecarias

AA+

Aa2

Repsol and Telefonica provide revenue diversification and a potential capital cushion

32

Income diversification: two international leaders in defensive sectors

Financial flexibility: very liquid stakes

Potential capital buffer

Value: solid fundamentals, excellent track record and high dividend yield

Profitability: attractive return

Low regulatory capital consumption

Tax-efficient (≥ 5%)

Geographical diversification: ~65% generated outside Spain

5.1%2

12.8%2

Market value1: €5.8 bn

(1) As of March 31st 2012 (2) 12.8% stake in Repsol: 156,509,448 shares; 5.1% stake in Telefónica; 233,844,420 shares

Investment diversification

33

CaixaBank, the leading retail banking player in Spain

o Commercial strengh with sustained market share gains across the board

Solid balance sheet

o Excellent level of liquidity (€29.4bn): a key tool for balance sheet management

o Low NPL Ratio (5.25%) compared with Spanish banks combined with solid coverage (61%)

o Coverage reinforced by taking the full hit of the RDL 2/12 provisions

o Solid capital (12.4% core capital BIS II and ~10.5% core capital1 BIS III look-through 2019 in 2012)

The transaction with BCIV

o Consolidates CaixaBank’s leadership position in Spanish banking

o Increases shareholder value with sustainable increases in ROE and EPS, while maintaining strong balance sheet metrics and solvency

Key takeaways

(1) Proforma post preferred shares swap, fully phased-in. (2) Figures as of December 2011

Final remarks

APENDIX

34

35

Financial Sector Reform

Additional Provisions & Capital Buffers (1st and 2nd Stages)

Exitings

provisions

+

60% + 20%

Problematic

Assets 50% + 15%

(€176.000Mn)

Exitings

provisions

as of Jan

2012

Land

(€ 25 bn)0%

Building under

Construction

(€ 16 bn)

0%

Funished

Buildings

( € 60 bn)

0%

Personal

Guarantee

& 2nd mortgage

(€ 20.7 bn)

0%

unchanged

35% 0%+

2nd DecreeMay 2012

Generic Provisions Generic Provisions

1st DecreeFeb 2012

Generic Provisions

35%

28%

25% unchanged

unchanged

7%

7%

7%

7%

2nd DecreeMay 2012

1st DecreeFeb 2012

14%

52%

Capital

Buffer

Specific

Provisions

as of Jan

2012

Performing

Assets

(€121,7.000Mn)

Land

(€73 bn)

Building under

Construction

(€ 15 bn)

Funished

Buildings

( € 88 bn)

52%

29%

36

FULL ABSORPTION OF THE 1ST ROYAL DECREE

IMPACT ON Q1 RESULTS

CaixaBank Royal Decree Impact

PROVISION´S IMPACT ABSORVED AGAINST THE

€ 3.4 bn MERGED ADJUSTMENT IMPOSED ON ITS BOOKS.

2.700

4.722

1.800

2.102

1.287

3.305

325

2.166

2.300

1.600

1.830

Total (gross)

5.000

6.552

3.966

3.714

4.905

Total (net of Taxes)

3.500

4.586

2.776

P&L:1.471 R/E: 1.128

P&L: 2.814 R/E: 619

Pending Impact

(con Pastor)

0

857 761 1.618 1.132

412 1.607 2.019 P&L: 1.413 R/E: n.d.

Millions €

Impacto RDL 18/2012 en principales competidores

+

+

+

+

+

+

+

+

2nd Decree New

Reuirements

1st Decree Pending

to be booked

FROB

Entities oblidged to increase their capital as a consequence of being unable to cope with the new

stablished provisions, will have raise capital or apply for FROB`s financial asistance.

The FROB would be able to inject Capital via Common Equity or via Contingent Convertibles.

Contingent Convertibles would have a maturity of 5 years.

Entities asking for FROB´s support will have to present a Restructuring Plan

FROB’s Financial Capabilities of €42.000Mn (€27.300Mn still available):

Available Liquidity: €5.300Mn

Credit Facility: €3.000Mn

Capital not disbursed: €6.000Mn

Additional Issuance Cappacity (i) €13.000Mn (explicit, unconditional and irrevocable)

Total: €27.300Mn

(i) With current Government Authorization

38

FROB – Fund for Orderly Bank Restructuring

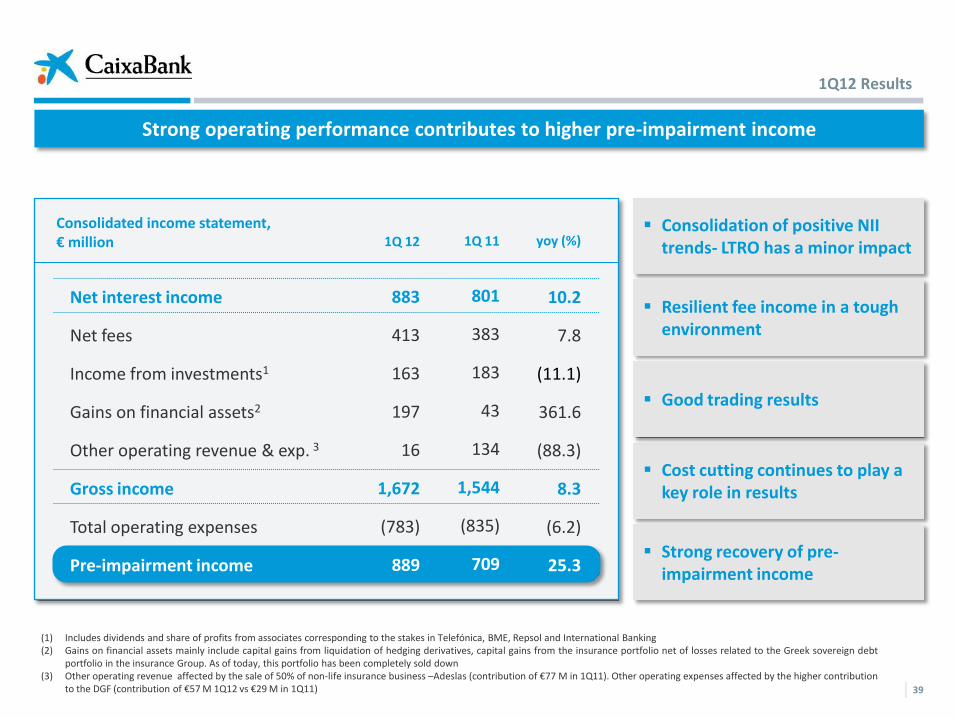

Strong operating performance contributes to higher pre-impairment income

39

1Q 11 yoy (%) Consolidated income statement, € million 1Q 12

Consolidation of positive NII trends- LTRO has a minor impact

(1) Includes dividends and share of profits from associates corresponding to the stakes in Telefónica, BME, Repsol and International Banking (2) Gains on financial assets mainly include capital gains from liquidation of hedging derivatives, capital gains from the insurance portfolio net of losses related to the Greek sovereign debt

portfolio in the insurance Group. As of today, this portfolio has been completely sold down (3) Other operating revenue affected by the sale of 50% of non-life insurance business –Adeslas (contribution of €77 M in 1Q11). Other operating expenses affected by the higher contribution

to the DGF (contribution of €57 M 1Q12 vs €29 M in 1Q11)

Resilient fee income in a tough environment

Cost cutting continues to play a key role in results

Strong recovery of pre-impairment income

Net interest income

Net fees

Income from investments1

Gains on financial assets2

Other operating revenue & exp. 3

Gross income

Total operating expenses

Pre-impairment income

801

383

183

43

134

1,544

(835)

709

10.2

7.8

(11.1)

361.6

(88.3)

8.3

(6.2)

25.3

883

413

163

197

16

1,672

(783)

889

Good trading results

1Q12 Results

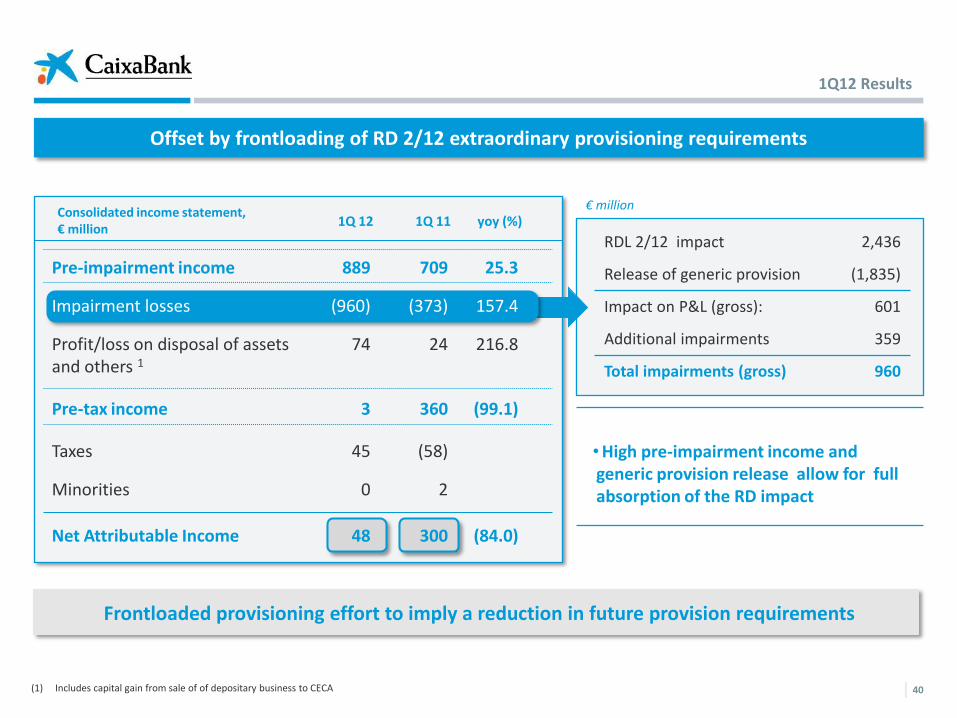

Offset by frontloading of RD 2/12 extraordinary provisioning requirements

40

Frontloaded provisioning effort to imply a reduction in future provision requirements

RDL 2/12 impact 2,436

Release of generic provision (1,835)

Impact on P&L (gross): 601

Additional impairments 359

Total impairments (gross) 960

1Q 11 yoy (%) Consolidated income statement, € million 1Q 12

• High pre-impairment income and generic provision release allow for full absorption of the RD impact

Pre-impairment income

Impairment losses

Profit/loss on disposal of assets and others 1

Pre-tax income

Taxes

Minorities

Net Attributable Income

889

(960)

74

3

45

0

48

709

(373)

24

360

(58)

2

300

25.3

157.4

216.8

(99.1)

(84.0)

€ million

(1) Includes capital gain from sale of of depositary business to CECA

1Q12 Results

€ million

Net interest income still supported by repricing of mortgage portfolio and increased loan spreads

Net interest income reflects repricing trends

41

Net interest margin increases by 9bs YoY

1Q11 2Q11 3Q11 4Q11 1Q12

+10.2%

+3.9%

1Q12 Results

Stable customer spread despite higher deposit yields

1Q11 2Q11 3Q11 4Q11

42

1Q12

Front book credit spreads

improve

Spreads in front book

time deposits

deteriorate as rates fall

YoY mortgage yields variation (bps) Customer spread

Repricing of mortgage loan

book tones down

Loans and credits Customer spread Customer deposits

1Q12 Results

43

Strong increase in fee income in a tough environment as franchise proves its worth

1Q’ 12 YoY(%)

Banking Services 311 11.8%

Mutual funds 38 0%

Insurance and pension plans

49 15.5%

Custody and distribution fees(1) 15 (40.0%)

Net Fees

€ million

Net fees break-down

Increased banking service fees a good indication of business health

413 7.8%

(1) Includes distribution fees for regional government securities

€ million

Net Fees

+7.8%

-2.8%

1Q12 Results

44

€ million

Strong capacity of generating pre-impairment income Cost-cutting discipline plays a significant role and leads to improved efficiency

Strong efforts in cost reduction

(1) Trailing 12 months including depreciation (2) On a non-consolidated basis to exclude impact of ADESLAS.

Operational improvements + cost cutting = strong pre-impairment income : €889 M (+25.3%)

Cost-to-income ratio falling below 50%1

No of branches: 5,172 (-105 yoy)

CaixaBank employees: 24,893 (-289 yoy)2

%

Trend is impacted by the deconsolidation of the non-life insurance business (ADESLAS).

In line for -3% annual reduction in recurring expenses

Personnel

General

Amortization

835 783

-6.2%

-2.3%

-13.4%

-15.1%

1Q12 Results

Expect €540 M of cost synergies by 2014 with an NPV of €1.8 bn

45 45

Annual gross costs savings (€ M)

12.5% of total combined costs

€540 M of annual costs savings achieved by 2014

€1.1 Bn of net restructuring costs

NPV of €1.8 Bn equals 1.8x price paid

Proven integration skills of CaixaBank

2011 PF cost-to-income ratio 49% (7 pp lower than combined ratio)

Cost/income expectations for 2014 in line with previously reported guidance

270

540

54

2012E 2013E 2014E

2011 Cost-to-income ratio (%)

51%

78%56% 49%

CABK BCIV CABK + BCIV PF

(exc. synergies)

CABK + BCIV PF

(100% synergies)

Information as of December 2011 (based on reported statutory accounts)

Integration agreement with Banca Cívica

140113

BCIV CABK

557438

BCIV CABK

In addition we are targeting material income synergies

46 46 Information as of December 2011. CaixaBank gross margin adjusted for income from stakes. Comparable number of clients. (1) BCIV time deposit base of €18.5 bn, according to public information as of December (excluding “cédulas multicedentes”)

Substantial income synergies:

Reduction in time deposit1 costs:

25-30 bps p.a. could be reduced over

time

High potential to improve profitability

per client (reaching CABK levels)

Cross-selling potential based on CABK

leadership in key retail products (e.g.

Mutual funds, pension plans, life

insurance, mortgages)

1.3x

1.2x

Commissions / client (€)

Gross margin / client (€)

Integration agreement with Banca Cívica

Leading platform: existing scale advantage

M&A not a “need”, but an opportunity

As such, will only consider value-creating opportunities

Minimum thresholds:

o Return on investment > Cost of equity by year 3

o EPS accretive by year 3

o Maintain financial strength (core 8%-9% Basel-3)

Transaction is consistent with CaixaBank’s M&A policy as stated to the market

ROIC ~ 20% by 2014

ROI substantially higher

Positive EPS impact from 2013 >20% EPS accretion by 2014

Core Basel-III (Fully phased-in) ~8-9%

Room for both organic and M&A growth

Indicative criteria for M&A

47 47

Inaugural Analyst Presentation (Feb. 2011)

Integration agreement with Banca Cívica

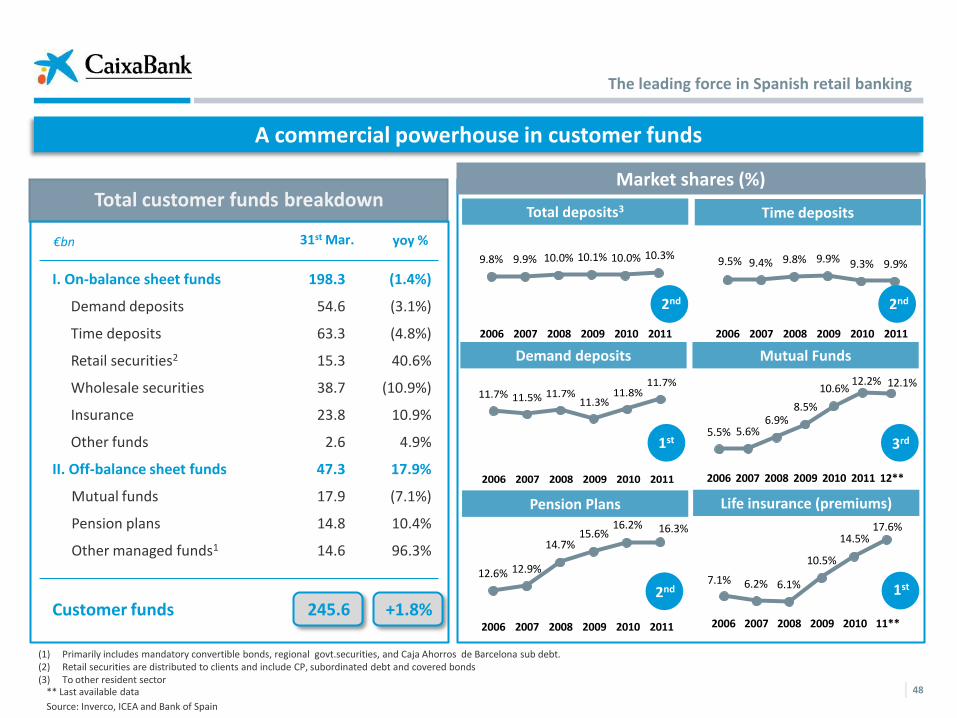

48

Total customer funds breakdown Total customer funds breakdown

A commercial powerhouse in customer funds

Total deposits3 Time deposits

9.8% 9.9% 10.0% 10.1% 10.0% 10.3%

2006 2007 2008 2009 2010 2011

9.5% 9.4% 9.8% 9.9% 9.3% 9.9%

2006 2007 2008 2009 2010 2011

Mutual Funds

12.6% 12.9%

14.7%15.6%

16.2% 16.3%

2006 2007 2008 2009 2010 2011

Pension Plans

7.1% 6.2% 6.1%

10.5%

14.5%17.6%

2006 2007 2008 2009 2010 11**

11.7% 11.5% 11.7%11.3%

11.8%11.7%

2006 2007 2008 2009 2010 2011

Life insurance (premiums)

Demand deposits

2nd 2nd

2nd

3rd

1st

1st

Market shares (%)

** Last available data

Source: Inverco, ICEA and Bank of Spain

(1) Primarily includes mandatory convertible bonds, regional govt.securities, and Caja Ahorros de Barcelona sub debt. (2) Retail securities are distributed to clients and include CP, subordinated debt and covered bonds (3) To other resident sector

5.5% 5.6%6.9%

8.5%

10.6%12.2% 12.1%

2006 2007 2008 2009 2010 2011 12**

31st Mar.

I. On-balance sheet funds

Demand deposits

Time deposits

Retail securities2

Wholesale securities

Insurance

Other funds

II. Off-balance sheet funds

Mutual funds

Pension plans

Other managed funds1

Customer funds

198.3

54.6

63.3

15.3

38.7

23.8

2.6

47.3

17.9

14.8

14.6

(1.4%)

(3.1%)

(4.8%)

40.6%

(10.9%)

10.9%

4.9%

17.9%

(7.1%)

10.4%

96.3%

€bn yoy %

+1.8% 245.6

The leading force in Spanish retail banking

Management of loan book to adapt to market environment

(1) To other resident sector

** Last available data

Source: SWIFT, Bank of Spain and Factoring Spanish association 49

Loan Book Breakdown

9.0% 9.1%9.6% 10.0%

10.6%10.6%

2006 2007 2008 2009 2010 2011

Total loans1 Mortgages

11.1%11.0%10.9%10.5%11.0%11.1%10.6%

2006 2007 2008 2009 2010 2010 12**

Commercial loans

6.0% 6.5%7.8%

8.9% 9.5% 9.9%

2006 2007 2008 2009 2010 11**

1st 1st

2nd 7.2% 7.3% 8.1%

11.6%13.3%

15.4%

2006 2007 2008 2009 2010 jul-05

Factoring & Confirming

5.1% 5.7%

9.4%

14.2%17.1%

2007 2008 2009 2010 2011

Foreign trade - exports

9.6% 10.3%12.7% 13.0% 14.0%

2007 2008 2009 2010 2011

Foreign trade- imports

3rd

Market shares (%)

Loan balances to real estate developers continue to decline at a greater pace than the market

Exposure to businesses (ex-developers) increases by 1.3%

31st Mar.

I. Loans to individuals

Residential mortgages

Consumer credit

II. Loans to businesses

Non RE business

Real Estate developers

ServiHabitat & other RE subsidiaries

III. Public sector

Total loans

92.5

69.1

23.4

79.8

55.0

21.7

3.1

11.6

(1.8%)

(1.2%)

(3.8%)

(5.0%)

1.3%

(15.1%)

(26.1%)

11.1%

€bn, gross yoy %

-2.5% 183.9

The leading force in Spanish retail banking

50

Reinforced by a premium brand reputation

“la Caixa”: the financial brand

with the best reputation

In 2011, reduction in the number of complaints: 17%

Leading institution in reputation and interest in operating (FRS

Inmark 2011 – individuals) and customer retention in business

segment (FRS Inmark 2011 - businesses)

The first institution for 36% of business clients (internal survey

among 3,385 companies)

The most highly rated online service in all segments (individuals

and businesses) (Aqmetrix)

Quality of service – Brand reputation

The leading force in Spanish retail banking

Av. Diagonal, 621 08028 Barcelona

www.CaixaBank.com

+34 93 411 75 03

Institutional Investors & Analysts Contact

contact us, please call or write to us at the following email address and telephone number: We are at your entire disposal for any questions or suggestions you may wish to make. To