calling all employers employment tax and pensions workshop may 2014

TRANSCRIPT

Calling all employersEmployment Tax and Pensions workshopMay 2014

Today’s workshop

Alastair Wilson - Introduction

Mark Parkinson – Workplace Pensions

Claire Brown – Payroll

Clair Williams – Salary sacrifice

Alastair Wilson – A quick 2014 Budget round up

Questions

Before we start – Growth Vouchers

Mark ParkinsonWealth Management & Workplace Pensions

Why has auto enrolment come about?

Six million people in the UK have no retirement savings

Auto enrolment criteria

All employers regardless of size – 1.3m employers in UK.

Minimum income aligned to income tax threshold (£10,000 2014/15) but pay on income earned between the lower and upper NI thresholds (£5,772 - £41,865 2014/15).

Age 22 – SPA, can opt in if aged between 16 -21 or SPA to 74. Employer contributes if employee has qualifying earnings.

Individuals can opt in, if earning less, employer contributes on income over the lower NI threshold.

Optional 3 month waiting period (employee can opt in earlier and employer must pay).

The SME market

What do employers need to do? Provide a qualifying workplace pension scheme

Assess workforce every pay reference period

Automatically enrol eligible workers

Administer opt out processes

Provider information to employees including:o Telling eligible jobholders they have the right to opt outo Notifying non-eligible jobholders and entitled workers they have the right to opt ino Notifying workers if using a postponement period

Arrange membership of a pension scheme for entitled workers who choose to opt in

Pay contributions to the pension scheme

Keep records about their workers and the pension scheme

Hopefully you’re all familiar with this?

And this?

Preparing for the challenge ahead

Compliance & Employer Fines

Compliance & Employer Fines – Dunelm Furniture Case StudyBackground

Dunelm had a Staging Date of 1st April 2013. They were due to complete registration to confirm they had complied with employer duties, by 31st July 2013.

The Pensions Regulator investigated and discovered that Dunelm had breached the rules in several instances.

- Failure to enrol members of four weekly payroll on time. Members enrolled a month late- Failure to enrol certain members of monthly payroll on time. These members were enrolled 3 months

later- Failure to pay across to the pension provider a significant level of contributions due to the above

failuresRegulatory Action

Due to the significant amount of pension contributions and in order to protect the benefits of the employees of Dunelm, The Pensions Regulator served an Unpaid Contributions Notice pursuant to section 37 of the Pensions Act 2008.

Outcome

Dunelm were ordered to pay across the total amount of contributions owed to members, £108,000.

The Auto Enrolment ‘Tsunami’

Source: www.accountingweb.co.uk – 30/07/2013

In 2014 around 38,000 employers will stage

In 2015 around 70,000 employers will stage

In 2016 around 450,000 employers will stage

In 2017 around 850,000 employers will stage

Staging Dates – part 1

Staff on payroll Staging Date120,000 or more 1 October 2012

50,000 - 119,999 1 November 2012

30,000 - 49,999 1 January 2013

20,000 - 29,999 1 February 2013

10,000 - 19,999 1 March 2013

6,000 - 9,999 1 April 2013

4,100 - 5,999 1 May 2013

4,000 - 4,099 1 June 2013

3,000 - 3,999 1 July 2013

2,000 - 2,999 1 August 2013

1,250 - 1,999 1 September 2013

800 - 1,249 1 October 2013

500 - 799 1 November 2013

350 - 499 1 January 2014

250 - 349 1 February 2014

160 - 249 1 April 2014

90 - 159 1 May 2014

62 – 89 1 July 2014

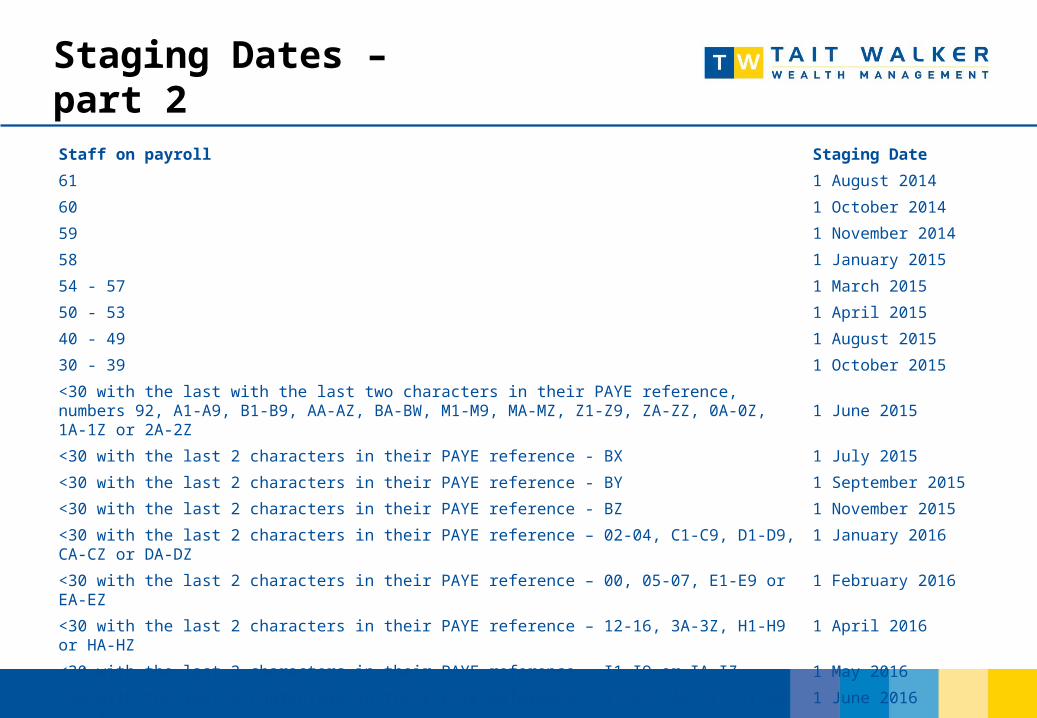

Staging Dates – part 2

Staff on payroll Staging Date

61 1 August 2014

60 1 October 2014

59 1 November 2014

58 1 January 2015

54 - 57 1 March 2015

50 - 53 1 April 2015

40 - 49 1 August 2015

30 - 39 1 October 2015

<30 with the last with the last two characters in their PAYE reference, numbers 92, A1-A9, B1-B9, AA-AZ, BA-BW, M1-M9, MA-MZ, Z1-Z9, ZA-ZZ, 0A-0Z, 1A-1Z or 2A-2Z 1 June 2015

<30 with the last 2 characters in their PAYE reference - BX 1 July 2015

<30 with the last 2 characters in their PAYE reference - BY 1 September 2015

<30 with the last 2 characters in their PAYE reference - BZ 1 November 2015

<30 with the last 2 characters in their PAYE reference – 02-04, C1-C9, D1-D9, CA-CZ or DA-DZ 1 January 2016

<30 with the last 2 characters in their PAYE reference – 00, 05-07, E1-E9 or EA-EZ 1 February 2016

<30 with the last 2 characters in their PAYE reference – 12-16, 3A-3Z, H1-H9 or HA-HZ 1 April 2016

<30 with the last 2 characters in their PAYE reference – I1-I9 or IA-IZ 1 May 2016

<30 with the last 2 characters in their PAYE reference – 17-22, 4A-4Z, J1-J9 or JA-JZ 1 June 2016

<30 with the last 2 characters in their PAYE reference – 23-29, 5A-5Z, K1-K9 or KA-KZ 1 July 2016

Staging Dates – part 3

Staff on payroll Staging Date

<30 with the last 2 characters in their PAYE reference – 30-37, 6A-6Z, L1-L9 or LA-LZ 1 August 2016

<30 with the last 2 characters in their PAYE reference – N1-N9 or NA-NZ 1 September 2016

<30 with the last 2 characters in their PAYE reference – 38-46, 7A-7Z, 01-09 or 0A-0Z 1 October 2016

<30 with the last 2 characters in their PAYE reference – 47-57, 8A-8Z, Q1-Q9, R1-R9, S1-S9, T1-T9, QA-QA, RA-RZ, SA-SZ or TA-TZ

1 November 2016

<30 with the last 2 characters in their PAYE reference – 58-59, 9A-9Z, U1-U9, V1-V9, W1-W9, UA-UZ, VA-VZ or WA-WZ

1 January 2017

<30 with the last 2 characters in their PAYE reference – 70-83, X1-X9, Y1-Y9 XA-XZ or YA-YZ 1 February 2017

<30 with the last 2 characters in their PAYE reference – P1-P9 or PA-PZ 1 March 2017

<30 with the last 2 characters in their PAYE reference – 84-91 or 93-99 1 April 2017

<30 unless otherwise described 1 April 2017

Employer who does not have a PAYE scheme 1 April 2017

New Employer (PAYE income first payable between 1 April 2012 and 31 March 2013) 1 May 2017

New Employer (PAYE income first payable between 1 April 2013 and 31 March 2014) 1 July 2017

New Employer (PAYE income first payable between 1 April 2014 and 31 March 2015) 1 August 2017

New Employer (PAYE income first payable between 1 April 2015 and 31 December 2015) 1 October 2017

New Employer (PAYE income first payable between 1 January 2016 and 30 September 2016) 1 November 2017

New Employer (PAYE income first payable between 1 October 2016 and 30 June 2017) 1 January 2018

New Employer (PAYE income first payable between 1 July 2017 and 30 September 2017) 1 February 2018

NEST – The government’s answer to Automatic Enrolment

Maximum contribution £4,600 (2014/15)

Limited investment choice

No transfers in or out until 2017

0.3% annual management charge + 1.8% contribution charge

There are currently 6 different levels of access that can be given by

employers to scheme administrators:

Read-only access

Payment access

Enrolment delegate

General access

Schedule access

Full access

Phasing in contributions

Period (#) Minimum employer

Minimum employee (*)

Tax Relief (*) Minimum Total

1st Oct to 30th Sept 2017 1% 0.8% 0.2% 2%

1st Oct 2017 to 30th Sept 2018 2% 2.4% 0.6% 5%

October 2018 onwards 3% 4% 1% 8%

(#) Depending on the company’s Staging Date (*) Assuming employer pays the minimum allowed

NB – the above is based on a percentage of ‘qualifying earnings’ = NI threshold earnings

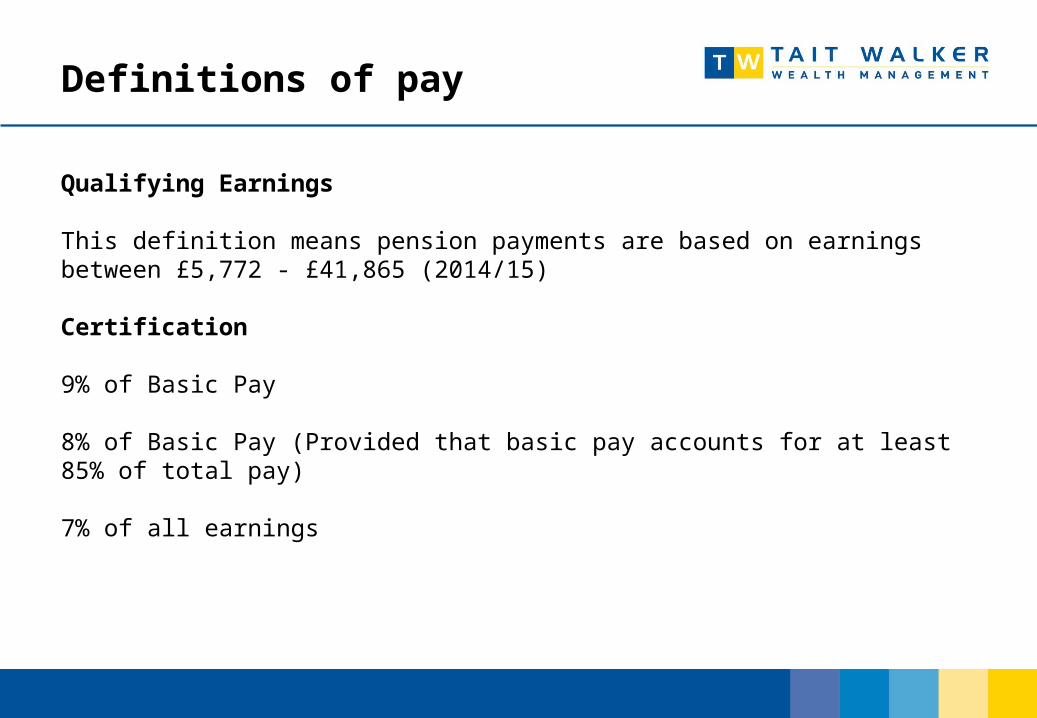

Definitions of pay

Qualifying Earnings

This definition means pension payments are based on earnings between £5,772 - £41,865 (2014/15)

Certification

9% of Basic Pay

8% of Basic Pay (Provided that basic pay accounts for at least 85% of total pay)

7% of all earnings

How are SME businesses responding?

Cost

“In house” work needed

“Bespoke” pension

What makes Tait Walker different?

Our recent implementations

Our Clients Staff Numbers Staging Date

Residential Care Home 635 1st November 2013

Aerospace Manufacturer 320 1st February 2014

National Charity (1) 230 1st April 2014

National Charity (2) 325 1st April 2014

Regional Legal Firm 297 1st April 2014

Manufacturing Firm 167 1st May 2014

Engineering Firm 138 1st May 2014

Distribution Firm 112 1st May 2014

Real Life Stories and Lessons

Maintaining compliance

Opt Ins

Successful communication strategies

Pitfalls of communication

Sourcing schemes for clients

Charge caps

Types of queries from employees

Concluding thoughts

Automatic Enrolment is a four party project as it brings together:

The EmployerThe AdviserThe Pensions ProviderThe Payroll Provider

In our role as advisers, Tait Walker can offer guidance for employers on the best way to proceed and project manage the process using its 3 steps

StrategyImplementationOn-going support & Compliance

Tax and legislation are likely to change. The information given here is based on Tait Walker Wealth Management’s understanding of law and HMRC practice at the date of presentation

Tait Walker Wealth Management is a trading style of Tait Walker Financial Services Ltd which is authorised and regulated by the Financial Conduct Authority (FCA)

Automatic Enrolment is not regulated by the FCA .

Tait Walker Chartered Accountants is not regulated by the FCA.

Claire BrownPayroll

Auto Enrolment

What will your Pension Provider do for you!

Who will issue postponement letters?Who will issue new joiner packs?How will the data be uploaded?Will data be duplicated at the start?Is there more than 1 scheme reference?

Scottish Widows Middleware: Assist Me

Auto Enrolment

Sage (or equivalent software) Scottish Widows – Assist Me

Assesses entire workforce Issue Postponement letters if applicable

Auto enrol eligible workers

Calculate & deduct correct pension amounts

Export File from Sage into Assist Me Triggers communication which will be sent out to employees

Authorise payment and direct debit

Send opt out notifications to employer

Process Opt outs notifications

Calculate refunds and refund via payroll

Do not assume the pension provider will do everything

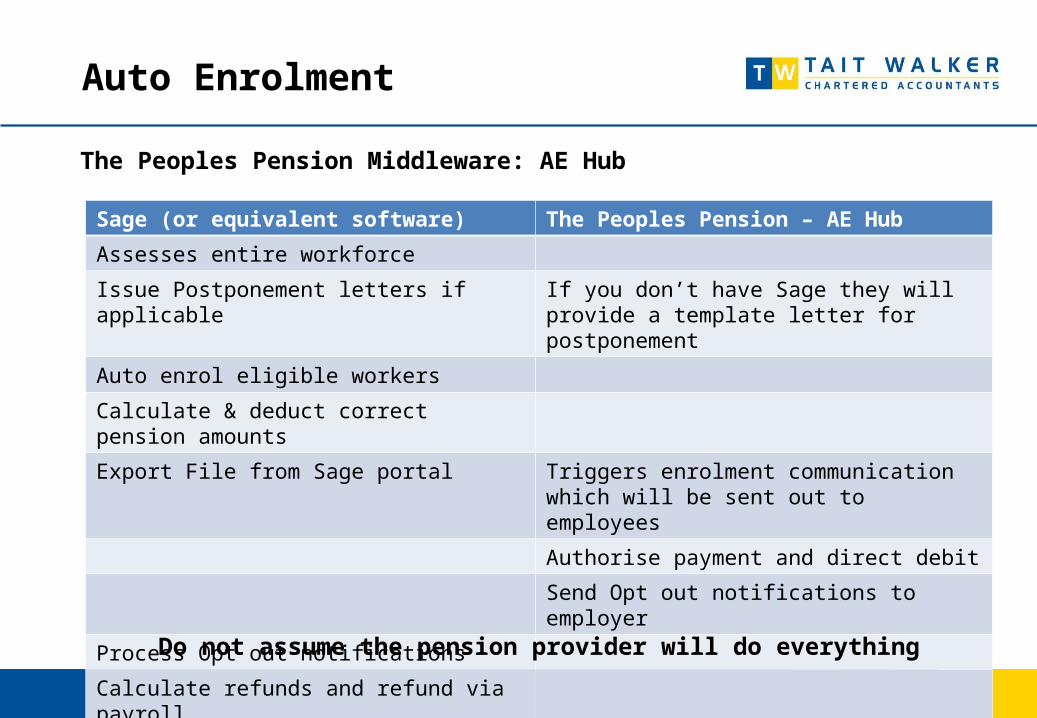

The Peoples Pension Middleware: AE Hub

Auto Enrolment

Sage (or equivalent software) The Peoples Pension – AE Hub

Assesses entire workforce

Issue Postponement letters if applicable If you don’t have Sage they will provide a template letter for postponement

Auto enrol eligible workers

Calculate & deduct correct pension amounts

Export File from Sage portal Triggers enrolment communication which will be sent out to employees

Authorise payment and direct debit

Send Opt out notifications to employer

Process Opt out notifications

Calculate refunds and refund via payroll

Do not assume the pension provider will do everything

NEST Middleware: NEST

Auto Enrolment

Sage (or equivalent software) NEST

Assesses entire workforce

Issue Postponement letters if applicable

Auto enrol eligible workers

Calculate & deduct correct pension amounts

Export File from Sage portal Triggers enrolment communication which will be sent out to employees

Authorise payment and direct debit

Send Opt out notifications to employer

Process Opt out notifications

Calculate refunds and refund via payroll

Do not assume the pension provider will do everything

Auto Enrolment

Planning is CRUCIAL

Compliant software Understanding your rolePay reference periods & Tax monthsPay elementsAgreeing the best definition of pensionable payTesting Data with provider

Auto Enrolment

Pay reference period example (4 weekly payroll)

Staging date 1 February 2014Employer wants to postpone for the maximum 3 months Employer assumes deferral date 30 April (End of Postponement)Employer assumes deductions to be deducted from May payroll : WRONG!

The legislation states that contributions must be deducted from the first time the employees get paid after the assessment date. See the example below;

Assessment date: 21st April - the first day of the 4 weekly pay reference period (PRP) that includes the 1st May (ie. The day after the postponement period has ended) PRP: runs from 21st April to 19th May

When do you deduct the premium? First date that an employee gets paid after the 21st April is 25th April so despite these earnings relating to the earnings from 23rd March to 20th April, it is from this pay that they must deduct a premium.

Auto Enrolment

Pay reference period example (4 weekly payroll)

The legislation states that contributions must be deducted from the first pay date, after the assessment date and as they were paid on the 25th this falls into the previous period.

Pay Reference Period

23rd March To 20th April

Paid to employees on 25th April

Pay Reference Period

21st April

25th To 19th May

End of Postponement 30 April

Auto Enrolment

Planning is CRUCIAL

Compliant software Understanding your rolePay reference periods & Tax monthsPay elementsAgreeing the best definition of pensionable payTesting Data with provider

Auto Enrolment

Payroll issues

Statutory Sick PayStatutory Maternity PayStatutory Paternity PayExisting Pension SchemesEmployees HandbookRecord Keeping

Clair WilliamsSalary sacrifice for pensions

Salary sacrifice for pensions

What is salary sacrifice?An agreement between an employer and employee that an element of salary will be sacrificed in return for employer provided benefits… in this case – additional employer pension contributionPension contributions made by employees receive income tax relief therefore saving = NI (both employer and employee) on the amount of salary sacrificedTotal required contributions set at a certain level - expected to be split between the employer and employee but this is not prescribedEmployee proportion is subject to NI for both employer and employee

Salary sacrifice for pensions

Example based on qualifying earnings

Salary sacrifice for pensions

ExampleBasic rate employee currently making a net pension contribution of £400 pa

− Salary sacrifice is based on gross pension contribution of £500− Employee NI saving = £60− Employer NI saving = £69

Income tax relief achieved directly via salary sacrifice

Easy to see how savings grow as more employees sign upEmployer NI saving 10 employees = £690 pa 50 employees = £3,450 paUsing this example with 50 employees money saved in Y1 would cover a lot of the costs of implementing pensions auto-enrolment

NI saving can either:− Increase employee’s net take-home pay (pension contributions remain the same)− Increase the pension contribution made (take-home pay remains the same)

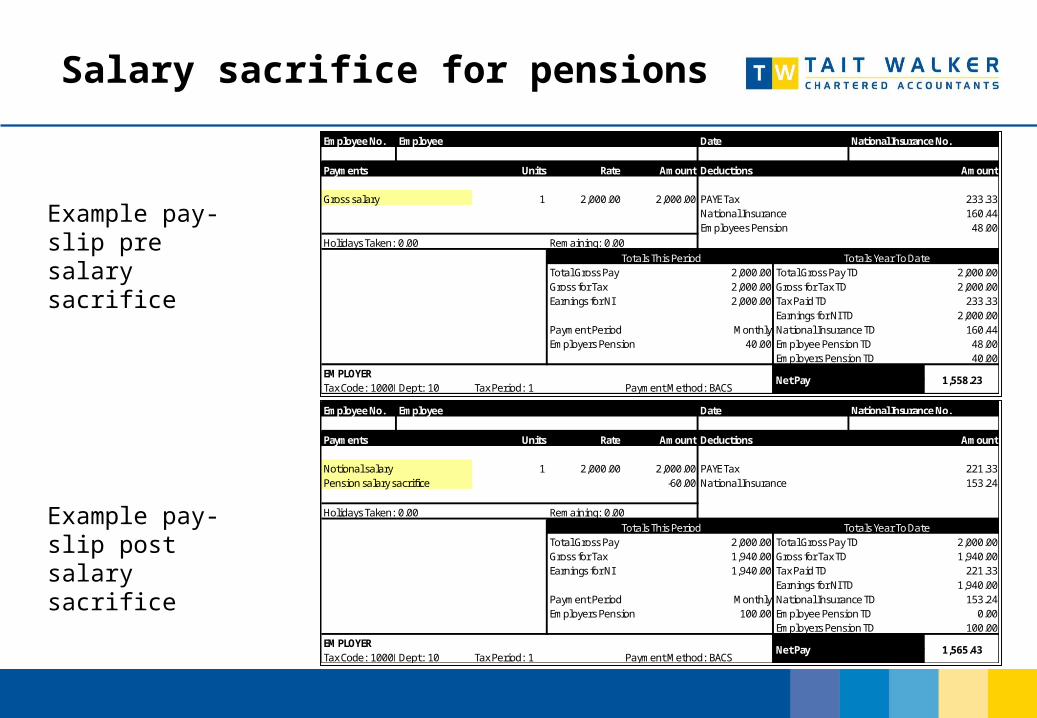

Salary sacrifice for pensions

Example pay-slip pre salary sacrifice

Example pay-slip post salary sacrifice

Employee No. Employee Date

Payments Units Rate Amount Deductions Amount

Notional salary 1 2,000.00 2,000.00 PAYE Tax 233.33National Insurance 160.44Employees Pension 48.00

Holidays Taken: 0.00 Remaining: 0.00

Total Gross Pay 2,000.00 Total Gross Pay TD 2,000.00Gross for Tax 2,000.00 Gross for Tax TD 2,000.00Earnings for NI 2,000.00 Tax Paid TD 233.33

Earnings for NI TD 2,000.00Payment Period Monthly National Insurance TD 160.44Employers Pension 40.00 Employee Pension TD 48.00

Employers Pension TD 40.00EMPLOYERTax Code: 1000L Dept: 10 Tax Period: 1 Payment Method: BACS

National Insurance No.

Totals This Period Totals Year To Date

1,558.23Net Pay

Employee No. Employee Date

Payments Units Rate Amount Deductions Amount

Notional salary 1 2,000.00 2,000.00 PAYE Tax 221.33Pension salary sacrifice -60.00 National Insurance 153.24

Holidays Taken: 0.00 Remaining: 0.00

Total Gross Pay 2,000.00 Total Gross Pay TD 2,000.00Gross for Tax 1,940.00 Gross for Tax TD 1,940.00Earnings for NI 1,940.00 Tax Paid TD 221.33

Earnings for NI TD 1,940.00Payment Period Monthly National Insurance TD 153.24Employers Pension 100.00 Employee Pension TD 0.00

Employers Pension TD 100.00EMPLOYERTax Code: 1000L Dept: 10 Tax Period: 1 Payment Method: BACS

National Insurance No.

Totals This Period Totals Year To Date

Net Pay 1,565.43

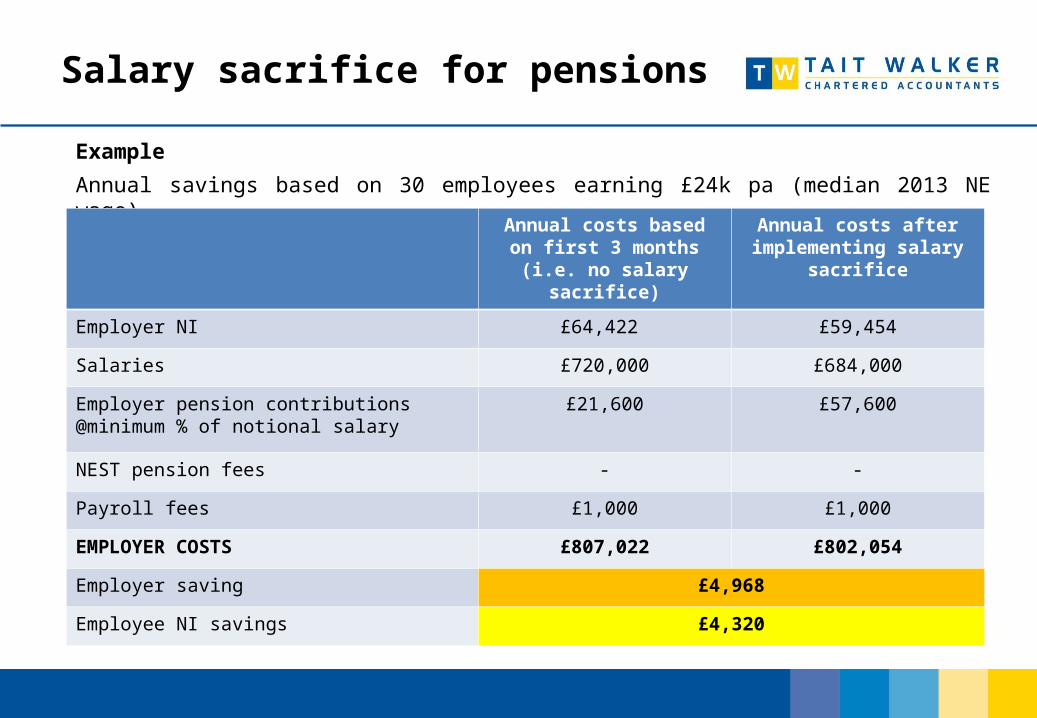

Salary sacrifice for pensions

Example

Annual savings based on 30 employees earning £24k pa (median 2013 NE wage)

Annual costs based on first 3 months (i.e. no salary

sacrifice)

Annual costs after implementing salary sacrifice

Employer NI £64,422 £59,454

Salaries £720,000 £684,000

Employer pension contributions @minimum % of notional salary

£21,600 £57,600

NEST pension fees - -

Payroll fees £1,000 £1,000

EMPLOYER COSTS £807,022 £802,054

Employer saving £4,968

Employee NI savings £4,320

Salary sacrifice for pensions

TimingsPension providers are requesting that the implementation of salary sacrifice is deferred until 3-4 months after a company’s staging date so that:

− any opt-outs have been processed and reversals in respect of payroll deductions have been reflected

− any employees remaining within the scheme 3-4 months after the staging date are likely to continue in the pension scheme

Deferral is possible but communication with employees becomes more complex as:− For first 3-4 months in pension scheme employee’s take-home pay will be reduced by the net

employee pension contributions made− When salary sacrifice commences employee’s take-home pay will be increased as the net

employee pension contribution will no longer be deducted and they will be subject to tax and NI on the reduced gross salary (or pension contributions will increase)

Communicate to employees before staging date so set expectations and explain reason for changes to pay-slips

Salary sacrifice for pensions

Practicalities to observe when implementing salary sacrificeA formal variation to the employees’ contracts of employment must be agreed Salary sacrifice schemes cannot reduce an employees wage < NMW or LEL

− Current NMW = £6.31ph / £11,485pa (35 hour week), Current LEL = £5,772 per annum− For 1% pension contribution via salary sacrifice employee > £11,600 (£11,950 – Oct 2014)− Most payroll software will flag ongoing

Once a salary sacrifice scheme is implemented employer only pension contributions will be paid− Employer must notify pension provider that salary sacrifice is being operated− Contributions must be input to pension middleware as employer contributions− If employee contributions continue in error then pension provider will continue to claim tax

relief within pension scheme too!The employees’ pay-slips will change - ‘Basic Pay’ is replaced by ‘Notional Pay’ from which a contribution is taken

− equivalent to previous gross pension contributions (increasing net take-home pay)− to result in the same net take-home pay (increasing pension contributions)

Salary sacrifice for pensions

Example pay-slip pre salary sacrifice

Example pay-slip post salary sacrifice

Employee No. Employee Date

Payments Units Rate Amount Deductions Amount

Gross salary 1 2,000.00 2,000.00 PAYE Tax 233.33National Insurance 160.44Employees Pension 48.00

Holidays Taken: 0.00 Remaining: 0.00

Total Gross Pay 2,000.00 Total Gross Pay TD 2,000.00Gross for Tax 2,000.00 Gross for Tax TD 2,000.00Earnings for NI 2,000.00 Tax Paid TD 233.33

Earnings for NI TD 2,000.00Payment Period Monthly National Insurance TD 160.44Employers Pension 40.00 Employee Pension TD 48.00

Employers Pension TD 40.00EMPLOYERTax Code: 1000L Dept: 10 Tax Period: 1 Payment Method: BACS

National Insurance No.

Totals This Period Totals Year To Date

1,558.23Net Pay

Employee No. Employee Date

Payments Units Rate Amount Deductions Amount

Notional salary 1 2,000.00 2,000.00 PAYE Tax 221.33Pension salary sacrifice -60.00 National Insurance 153.24

Holidays Taken: 0.00 Remaining: 0.00

Total Gross Pay 2,000.00 Total Gross Pay TD 2,000.00Gross for Tax 1,940.00 Gross for Tax TD 1,940.00Earnings for NI 1,940.00 Tax Paid TD 221.33

Earnings for NI TD 1,940.00Payment Period Monthly National Insurance TD 153.24Employers Pension 100.00 Employee Pension TD 0.00

Employers Pension TD 100.00EMPLOYERTax Code: 1000L Dept: 10 Tax Period: 1 Payment Method: BACS

National Insurance No.

Totals This Period Totals Year To Date

Net Pay 1,565.43

Salary sacrifice for pensions

Communication of salary sacrifice and TW servicesCommunicate salary sacrifice to employees as part of Auto-enrolment implementationCommunicate before staging date showing difference between pre and post salary sacrifice pay-slipsTW can help the employer to communicate salary sacrifice to employees - this could include written communications, face-to-face presentations and/or drop-in sessions for employeesTW can prepare a tailored employee communication booklet which explains salary sacrifice to your employees. This will include examples of how salary sacrifice works, explains the impact of salary sacrifice on statutory payments (e.g. redundancy, maternity, sick pay) and answer other salary sacrifice FAQs

TW can prepare calculations, employee letters and variations to the terms of employees’ contractsThe salary sacrifice scheme must be communicated to HMRC once implementedMaintenance of scheme – e.g. new employee calculations, annual updates regarding changes to tax rates and periodic review the pension filings submitted to the pension provider

Alastair WilsonGeneral updates

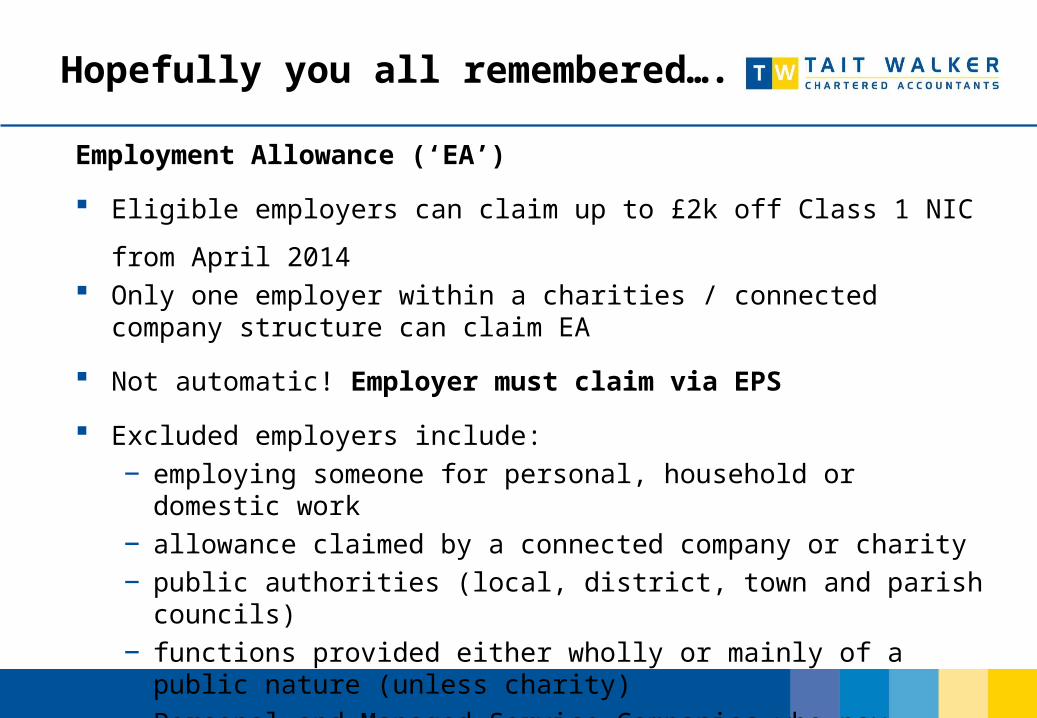

Hopefully you all remembered….

Employment Allowance (‘EA’)

Eligible employers can claim up to £2k off Class 1 NIC from April 2014 Only one employer within a charities / connected company structure can claim

EA

Not automatic! Employer must claim via EPS

Excluded employers include:− employing someone for personal, household or domestic work− allowance claimed by a connected company or charity− public authorities (local, district, town and parish councils)− functions provided either wholly or mainly of a public nature (unless charity)− Personal and Managed Service Companies who pay contract fees instead of

wages and salaries

General updates from the Budget

Benefits and expenses reporting

Office of Tax Simplification - proposals to simplify dealing with taxable benefits1. Voluntary payrolling of taxable benefits2. PSAs – employers to settle any tax liability on benefits and expenses3. An exemption for qualifying business expenses paid for or reimbursed by an employer4. Abolition of the £8,500 threshold5. Simple ‘principles based’ definition of a trivial benefit, incorporating a per item cap (e.g. £50)6. Travel and subsistence - clarification regarding permanent workplaces, homeworking, scale rate

subsistence payments and updates to HMRC guidance7. Simplifying NICs – 2 suggestions:

− apply Class 1 NICs to all employee remuneration (whether cash or benefits in kind)− alignment of the underlying definitions of income and expenses for income tax and NI

8. This would represent a fundamental policy review− But the employer must still know what is and what is not a taxable benefit?− whether the way a benefit is provided should determine how much tax is paid on it− whether non-taxable items can be excluded from charge to tax

Any Questions? Next workshop will be in September…..