can investors do well by doing good? sébastien pouget toulouse school of economics

TRANSCRIPT

Can investors do well by doing good?

Sébastien POUGET

Toulouse School of Economics

Co-director of the research center on Sustainable Finance and Responsible Invesments

Chaire « Finance Durable et Investissement Responsable »

Can investors do well by doing good?

Sébastien POUGET

Toulouse School of Economics

Chaire « Finance Durable et Investissement Responsable »

“The Washing Machine”: Investment Strategies and Corporate Behavior

with Socially Responsible Investors

Christian Gollierand

Sébastien POUGET

Socially Responsible Investments

Complements financial analysis by taking into account Environmental, Social, and Governance (ESG) factors

ESG factors (externalities): pollution, working conditions, employee relations, product safety, transparency of decisions…

SRI represents today between 5% and 15% of assets under management in Europe and the USA

Several trillions of euros (3.7 trillion$ in the US according to US SIF and 0.4 trillion€ in France according to Novethic)

5

Sébastien Pouget

What is SRI?

6

Source: US SIF, Sustainable and Responsible Investing in the United States 2012

Pension funds (CALPERS, TIAA-CREF, APG, FRR…)

Sovereign funds (Norway GPF, CDC…)

Institutional investors are major promoters of SRI (see e.g., the UN-backed Principles for Responsible Investment)

Numerous asset management companies are also proposing SRI funds (for example, Calvert in the US, and all the sponsors of the Chaire FDIR in France)

More than 250 funds in France

7

Sébastien Pouget

Players in SRI

8

Source: Novethic, Chiffres 2013 de l’investissement responsable en France

There are 3 main types of strategies

Exclusion

Boycott sectors that are jugged as irresponsible

Best in Class

Invest more in companies with best ESG performance

Engagement

Change corporate behavior by exerting voice

Other strategies: microcredit, thematic funds…9

Sébastien Pouget

SRI strategies

10

Source: EuroSIF, European SRI Study 2012

Why could it be important to foster Corporate Social Responsibility?

Milton Friedman (1970): corporate social responsibility is to maximize firm value

According to Benabou and Tirole (2010):

Quid if there are missing markets and thus externalities? Delegated Philanthropy

Quid if firm value does not reflect long term items? Bonus culture (Benabou and Tirole, 2014) may be dampened by using ESG performance to evaluate firms (extra-financial rating agencies)

11

Sébastien Pouget

Why SRI?

Necessary conditions : market failures (due to externalities) and government failures (due to territorial limits in juridical influence or to transaction costs)

SRI motivations:

Creating economic value in the long run

Being ethical

Institutional investors and asset managers often cite both due to:

Fiduciary responsibility that imposes financial objectives

Reputational risks that call for acceptable behaviors12

Sébastien Pouget

Why SRI?

13

Sébastien Pouget

Pourquoi capitalisme devient solidaire?

14

Sébastien Pouget

Pourquoi capitalisme devient solidaire?

15

Sébastien Pouget

Pourquoi capitalisme devient solidaire?

Norwegian GPF has more than 800 billion $ of AUM

The Fund launches enquiries regarding the behavior of companies on the field

The list of excluded companies is made publicly available online

Its choices are followed by a lot of asset owners and managers

16

Sébastien Pouget

Why SRI?

17

Sébastien Pouget

Why SRI?

18

63 companies are currently excluded by the Norwegian Fund

Excluded sectors: non-conventional weapons, tobacco, severe violations to human rights, severe degradation of environment

In France, Safran and Airbus Group are excluded due to their implication in nuclear weapon production

Sébastien Pouget

Why SRI?

Provide some theoretical underpinnings for SRI industryFinancial performance?

Change within companies?

Analyze the practical implications for SRI industryWhat type of funds?

With which strategy?

Can investors do well by doing good?

Our approach

Set up an asset pricing model for socially responsible assets

Study the link between financial markets and corporate decisions via shareholders’ voting decisions

Propose a business model for SRI funds that associates financial performance and changes in corporate behavior

Within the SRI industry, engagement strategies and private equity funds can display abnormal returns at equilibrium

The “washing machine” investment strategy

Profitable SRI?

Proposing a model in which SRI investors outperform traditional ones is challenging

Consider that CSR pays at the company level, i.e., virtuous firms display higher (long term) earnings than vicious firms

If one considers that financial markets are informationally efficient

Both SRI and traditional investors overweight virtuous firms

These investors display identical performances

If one considers that financial markets are inefficientBoth SRI and traditional investors try and collect information to spot the firms that are mispriced

Again, these investors display identical performances

Profitable SRI

There are at least three reasons why SRI might outperform traditional investment funds

SRI may be better at spotting the most promising companies because of expertise in extra-financial analysis

SRI may be better at anticipating new trends in corporate social responsibility and benefit from the subsequent enthusiasm

SRI may implement the “washing machine” strategy we characterize in this paper

Related literature

Other pricing models for socially responsible assets include Heinkel, Kraus, and Zechner (2001), Barnea, Heinkel, and Kraus (2005), and Barnea, Heinkel, and Kraus (2009)

These models feature investors with private benefits from firms’ responsible policies but there is no voting issues

Existing models of voting in firms include Gromb (1993), Burkart, Gromb, and Panunzi (1997, 2000), At, Burkart, and Lee (2011)

Gromb and ABL study the optimal design of security-voting structure and optimal allocation of control rights

Closest paper is BGP (2000) that features conflict of interest among shareholders but no voting on strategic decisions

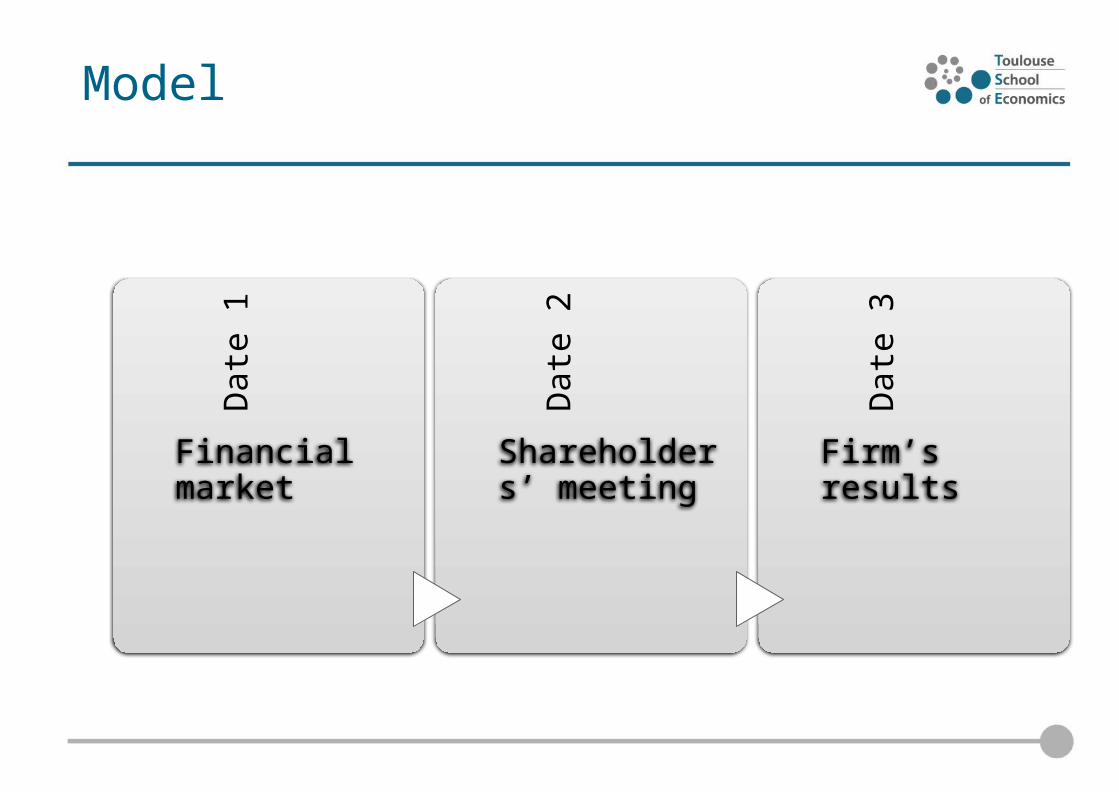

ModelD

ate

1

Financial market

Dat

e 2Shareholders’ meeting

Dat

e 3

Firm’s results

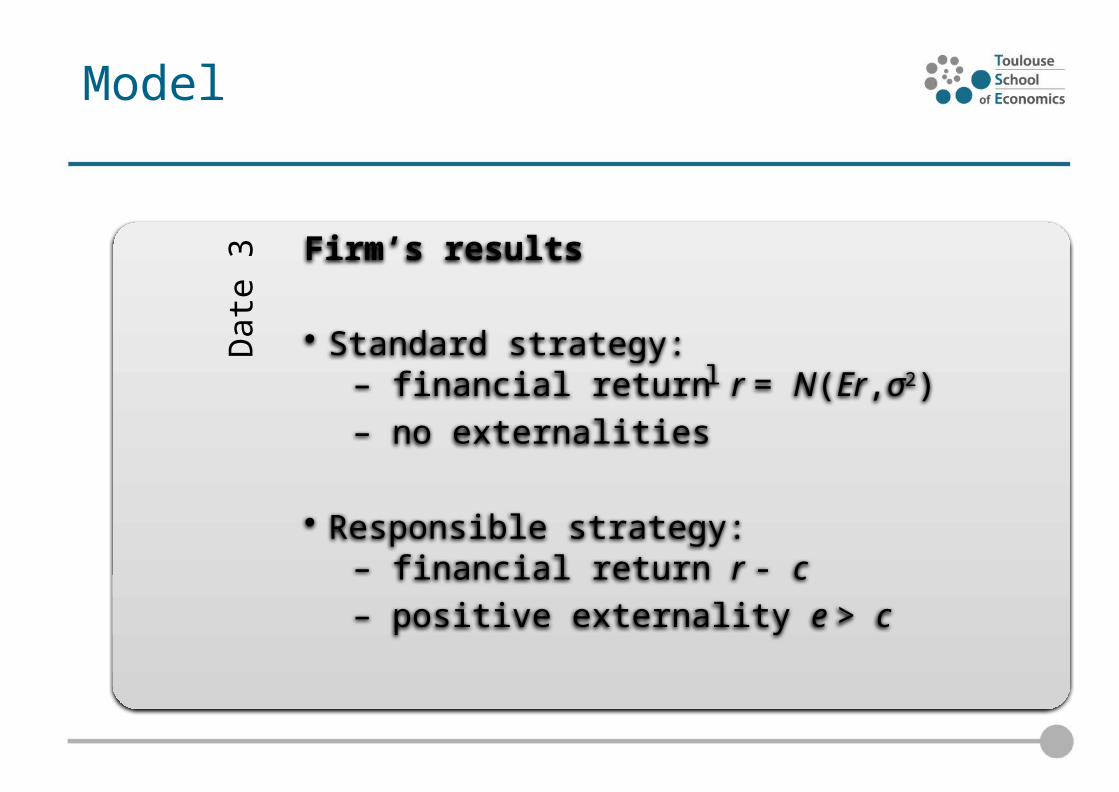

ModelD

ate

3 Firm’s results

• Standard strategy: – financial return r = N(Er,σ2)

– no externalities

• Responsible strategy:

– financial return r - c

– positive externality e > c

l

ModelD

ate

2 Shareholders’ meeting

• Strategy choice: standard vs. responsible

• Vote: simple majority

• One share = One vote

ModelD

ate

1 Financial market

• An initial owner sells his shares

ModelD

ate

1 Financial market

• An initial owner sells his shares• Socially responsible investors: – value

r, c and e• – proportion π

ModelD

ate

1 Financial market

• An initial owner sells his shares• Socially responsible investors: – value

r, c and e• – proportion π• Traditional investors:

– value r, and c only

ModelD

ate

1 Financial market

• An initial owner sells his shares• Socially responsible investors: – value

r, c and e• – proportion π• Traditional investors:

– value r, and c only• Trading at price P

Rational expectations equilibrium

Corporate strategy?

Investors’ demand?

Share price?Investors’ holdings?

Shareholders’ vote?

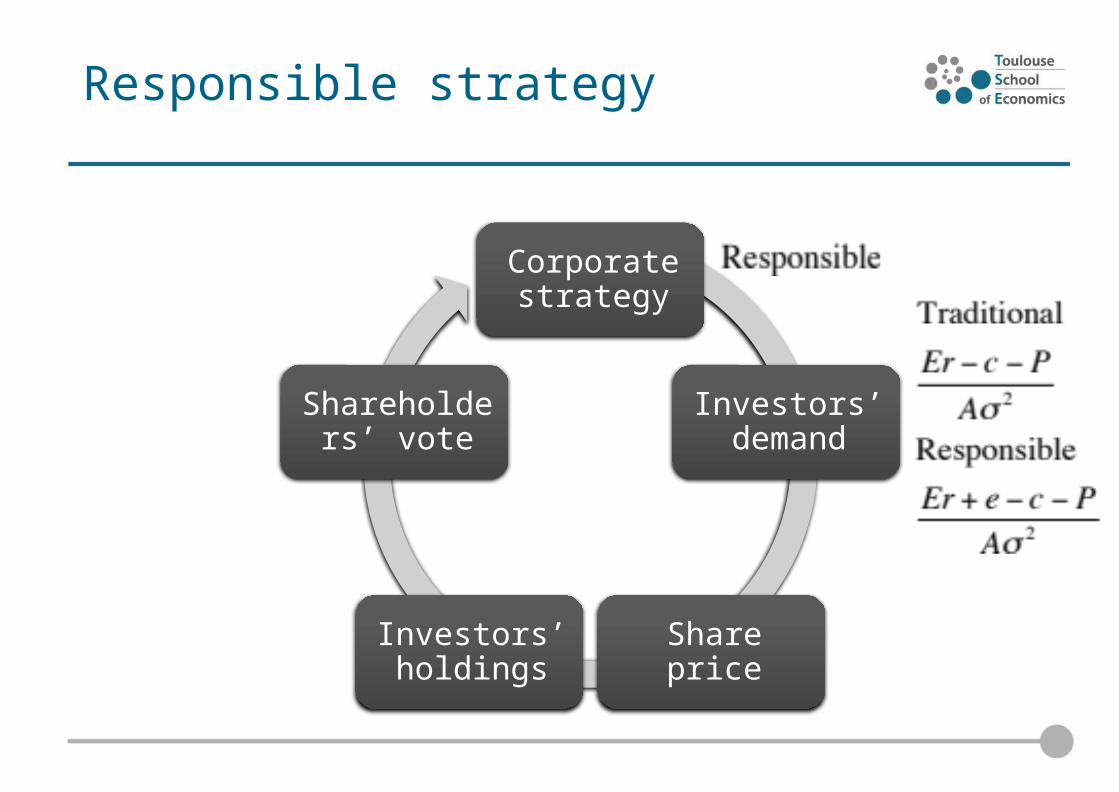

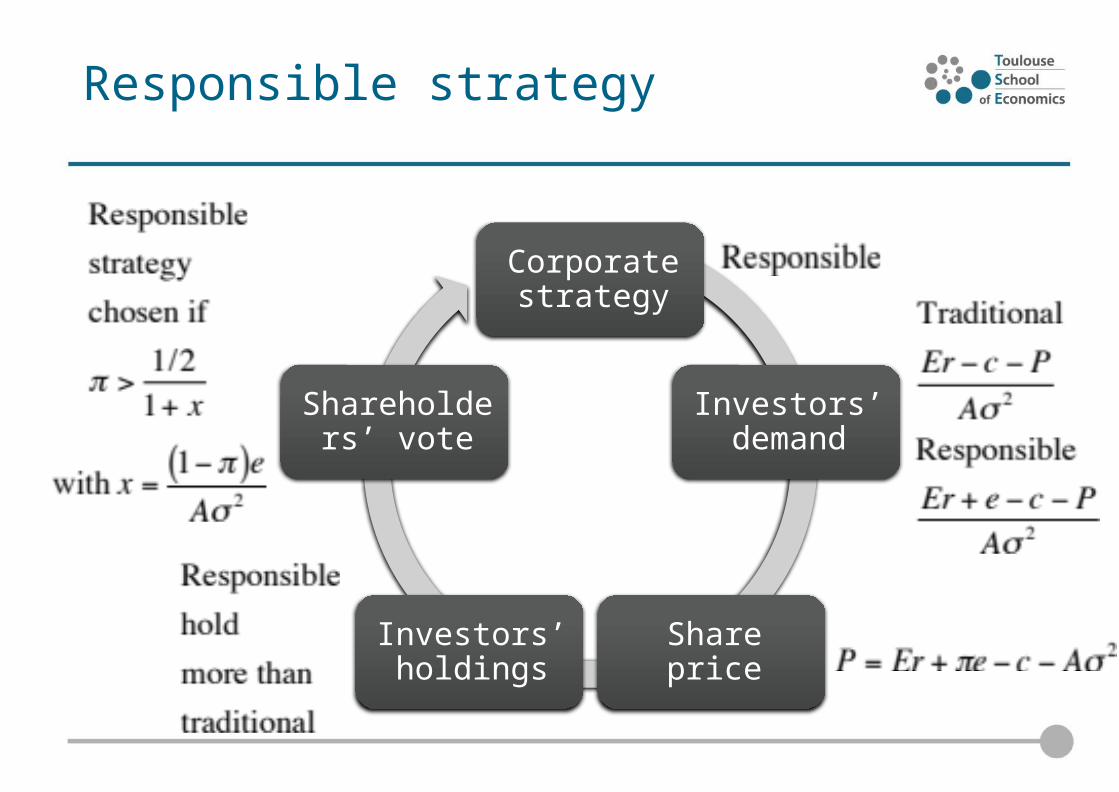

Corporate strategy

Investors’ demand

Share priceInvestors’ holdings

Shareholders’ vote

Standard strategy

Corporate strategy

Investors’ demand

Share priceInvestors’ holdings

Shareholders’ vote

Responsible strategy

Corporate strategy

Investors’ demand

Share priceInvestors’ holdings

Shareholders’ vote

Responsible strategy

Corporate strategy

Investors’ demand

Share priceInvestors’ holdings

Shareholders’ vote

Responsible strategy

Corporate strategy

Investors’ demand

Share priceInvestors’ holdings

Shareholders’ vote

Responsible strategy

Corporate strategy

Investors’ demand

Share priceInvestors’ holdings

Shareholders’ vote

Responsible strategy

Results so far

The responsible strategy is adopted when π > (1/2)/(1+x)

Responsible company offers a lower risk-adjusted return than the standard company

In line with Hong and Kacperczyk (2009)

Responsible companies market cap is higher than the one of standard companies when πe > c

Helps explaining why event studies on CSR are unclear – see, for example, Krüger (2014)

Value creation thanks to engagement

When π < (1/2)/(1+x) and πe > c, …

… responsible investors do not hold a majority of shares (the standard strategy is adopted)…

… and the firm is undervalued (with respect to the situation in which the responsible strategy would be chosen)

Potential for value creation (both financial and social)

Intervention of a raiderD

ate

0

Takeover

Dat

e 1

Financial market

Dat

e 2

Share-holders’ meeting

Dat

e 3

Firm’s results

Intervention of a raiderD

ate

0 Takeover

• Raider makes a take-it or leave-it offer to the initial owner

Dat

e 1 Financial market

• Raider sells back its shares to investors

Raider’s strategy

At date 0, raider offers a low price Er-Aσ2 at which the initial owner accepts to sell his shares

At date 1, raider could be tempted to sell back all its shares at high a price of Er+πe-c-Aσ2 (greater than Er-Aσ2)

This strategy is not feasible because, if it sells back all its shares, responsible investors do not have a majority

The raider has to keep a part α of the shares such that the responsible strategy is adopted

Raider’s behavior

We assume that the raider is risk-neutral and internalizes a part θ of the externality

Its expected utility is: (1-α)P1*+α(μ+θe-c)-P0*

Raider sells back 1-α shares if c/e<θ<πIts expected utility is: Aσ2+θe-c+(π-θ) 2e2/(4Aσ2)

Last term: the raider reaps the responsibility premium

Pure financial returns can be higher than for a traditional raider

Raider prefers to keep all the sharesIf θ<c/e: votes against responsible strategy and it is less risk averse than other investors (expected utility is Aσ2)

If θ>π: votes for the responsible strategy and it finds that the price is not high enough despite the responsibility premium (Aσ2+θe-c)

Raider’s commitment for CSR

This strategy is not credible unless the raider votes, at the shareholders’ meeting, in favor of the responsible strategy

If it focuses on financial returns only, it will always favor the standard strategy

Hence, a traditional raider cannot intervene and restructure the firm

Only a socially responsible raider can at the same time change the strategy of the firm and benefit financially from this change

Relation with empirical evidence

There is a responsibility premium:Hong and Kacperczyk (2009) on sin stocks

Bauer and Hann (2010) on green companies and credit spreads

Bauer, Derwall, Hann (2009) on employee relationships and spreads

Chava (2011) on green companies and bank loans

Dimson, Karakas and Li (2012) show that investment strategies based on engagement on environmental and social issues can generate positive abnormal return

Activism profitable on governance issues: Brav et al. (2006), Becht et al. (2009)

Relation with empirical evidence

An emerging strategy

The “Washing Machine” strategy has not yet been implemented

However, a fund, Tau Investment Management, is currently being set up in New York that follows the same principles

Objective (“NY firm sees investment opportunity in garment factories”, Reuters, 9/27/2013):

Invest in garment factories in emerging countries (i.e., Bengladesh, Vietnam…)

Be a very active minority shareholder

Transform companies mainly by improving labor conditions (compensation, security, training…) and supply chain organization

Resell shares on stock markets

Conclusion

To benefit from the “washing machine” strategy, SRI should:

Invest in non responsible firms and turn them into responsible

Have a long-term orientation

Have a credible orientation towards social responsibility

Strategy can be implementedAlone by SRI private equity or hedge funds

In group by SRI mutual funds or pension funds

Two remarks:Investing in non responsible firms raises a reputation issue for SRI

Traditional raiders can profit from targeting some CSR-oriented firms

Research center on

Sustainable Finance and Responsible Invesments

www.idei.fr/fdir

THANKS FOR YOUR ATTENTION!