can the german automotive industry lead again? · pdf filecan the german automotive industry...

TRANSCRIPT

GLOBAL INSIGHT AUTOMOTIVE SEMINAR

13-14 SEPTEMBER 2007 • FRANKFURT

Can the German Automotive Industry Lead Again?

Christoph StürmerDirector Product Development

Copyright © 2007 Global Insight, Inc. 2

• Bad News:– Sluggish Domestic Sales– Corporate Unrest– Regulatory Pressures

• Good News: – Booming Domestic Production – Aggressive International Growth– New Cooperative Spirit

• Conclusions

Structure of Presentation

Copyright © 2007 Global Insight, Inc. 3

2.0

2.5

3.0

3.5

4.0

4.51/

1998

7/19

98

1/19

99

7/19

99

1/20

00

7/20

00

1/20

01

7/20

01

1/20

02

7/20

02

1/20

03

7/20

03

1/20

04

7/20

04

1/20

05

7/20

05

1/20

06

7/20

06

1/20

07

7/20

07

Mill

ions

SAARSAAR Trend

Sluggish Domestic Sales

Current SAAR rate has recovered to 3.28 million units – but trend remains fixed at 3.14 million

Current SAAR rate has recovered to 3.28 million units – but trend remains fixed at 3.14 million

VAT increase

Copyright © 2007 Global Insight, Inc. 4

Private New Registrations Breaking Off

0

20

40

60

80

100

120

140

160

180

1/20

02

4/20

02

7/20

02

10/2

002

1/20

03

4/20

03

7/20

03

10/2

003

1/20

04

4/20

04

7/20

04

10/2

004

1/20

05

4/20

05

7/20

05

10/2

005

1/20

06

4/20

06

7/20

06

10/2

006

1/20

07

4/20

07

7/20

07

Thou

sand

s

PRIVATE AUTO RETAIL BUSINESS RENTAL FLEETS VEHICLE PRODUCTION OTHERS

VAT increase

Copyright © 2007 Global Insight, Inc. 5

2007 Sales Forecast Now Adjusted to 3.21 Million

2.0

2.5

3.0

3.5

4.0

4.519

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

Mill

ions

-30%

-20%

-10%

0%

10%

20%

30%

40%

CARS Growth

Year-on-year sales change for 2007 now forecast at -7% due to very high Q4 comparison base

Year-on-year sales change for 2007 now forecast at -7% due to very high Q4 comparison base

Copyright © 2007 Global Insight, Inc. 6

Corporate Unrest at Key Manufacturers

• New management at Volkswagen– The Audi way introduced in Wolfsburg– Dissolution of brand groups and repositioning of VW – Increasing influence of Porsche

• Unravelling of Daimler and Chrysler: – Re-evaluation of long-term platform strategy– Re-adjustment of management structures

• New management at BMW– Re-evaluation of business model– Increasing financial pressures

• New supplier giant– Continental taking over VDO from Siemens– Threat or opportunity for OEM clients?

Copyright © 2007 Global Insight, Inc. 7

CO2 Reduction Remains Complex Political Issue

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008140

145

150

155

160

165

170

175

180

185

190

195CO2 in g/km

Benzin

Gesamt

Diesel

Total emissions

172.5 g/ km

Gasoline

Total

Source: KBA

Urgency of issue is underlined by immediate impact on German car sales

Urgency of issue is underlined by immediate impact on German car sales

Copyright © 2007 Global Insight, Inc. 8

German Brands Dominate the Domestic Market

0%

20%

40%

60%

80%

100%

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

IND

SRB

CHN

CHE

AUT

MYS

N/K

RUS

ROM

GBR

SWE

ESP

ITA

KOR

CZE

USA

FRA

JPN

DEU

Sales Shares

Copyright © 2007 Global Insight, Inc. 9

0%

20%

40%

60%

80%

100%

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

SRB

PRT

CHE

AUT

CHN

IND

TWN

MYS

RUS

N/K

ROM

SWE

GBR

KOR

JPN

ITA

USA

DEU

FRA

German Brands Battle for First Place in West Europe

Sales Shares

Copyright © 2007 Global Insight, Inc. 10

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Mill

ions

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

CARS Growth

2007 Production Forecast Points to Historical High

Production Units

Full-year production forecast now at +4.5% due to weakness of domestic marketFull-year production forecast now at +4.5% due to weakness of domestic market

Copyright © 2007 Global Insight, Inc. 11

Among the Top-Ten Brand Origins, Germany Will Keep Its Global Position

0

10

20

30

40

50

60

70

80

90

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Mill

ions SWE

CZE

IND

RUS

ITA

CHN

FRA

KOR

DEU

USA

JPN

Production Units, World

Copyright © 2007 Global Insight, Inc. 12

German Brands Look Well-Prepared to Defend Their Global Competitive Position

0%

20%

40%

60%

80%

100%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

ZAFYUGUZBUKRSVKCHEAUTBRABLRPOLPAKSRBTURN/KMYSAUSIRNTWNROMESPGBRSWECZEINDRUSITACHNFRAKORDEUUSAJPN

Production Shares, World

Copyright © 2007 Global Insight, Inc. 13

The Segment Profile of German Brands Has Become Increasingly Diverse and Will Continue

Production Units, German Brands, World

0

2

4

6

8

10

12

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Mill

ions others

A

SUV-E

MVAN

MPV-C

D1

E1

C2

B

D2

C1

Copyright © 2007 Global Insight, Inc. 14

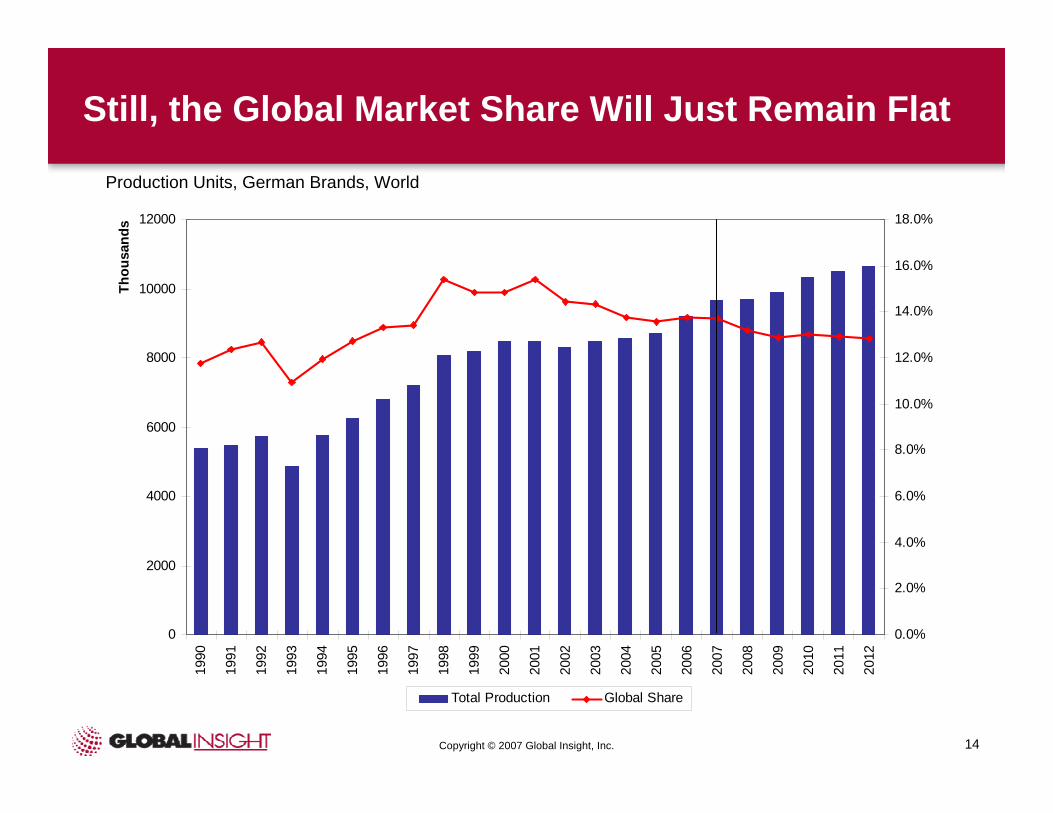

Still, the Global Market Share Will Just Remain Flat

0

2000

4000

6000

8000

10000

1200019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Total Production Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 15

The Proverbial “S-Class Segment” Will See Some Infringement From Japanese and U.S. Brands

0

50

100

150

200

250

300

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

E2 Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 16

In Spite of Rising Competition, the E1 Segment Offers Additional Potential for German Brands

0

200

400

600

800

1000

1200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

E1 Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 17

The C2 Segment Offers Premium Capabilities in a Subcompact Package – Brand Strength Is Key

0

200

400

600

800

1000

1200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

C2 Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 18

In the D2 Segment, High-Tech Appeal Combines with Sporty Driving – German Engineering Reigns

0

200

400

600

800

1000

1200

1400

160019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

D2 Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 19

Although Late to Start, German Brands Were Quick to Understand the Compact MPV Concept

0

100

200

300

400

500

60019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

MPV-C Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 20

While Frequently Overlooked, the MVAN Sector Accounts for Stable and Profitable Volume

0

100

200

300

400

500

600

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

MVAN Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 21

Entering a Mature Market, German Brands Established a Stronghold in Upscale SUV

0

50

100

150

200

250

300

350

400

450

500

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

SUV-E Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 22

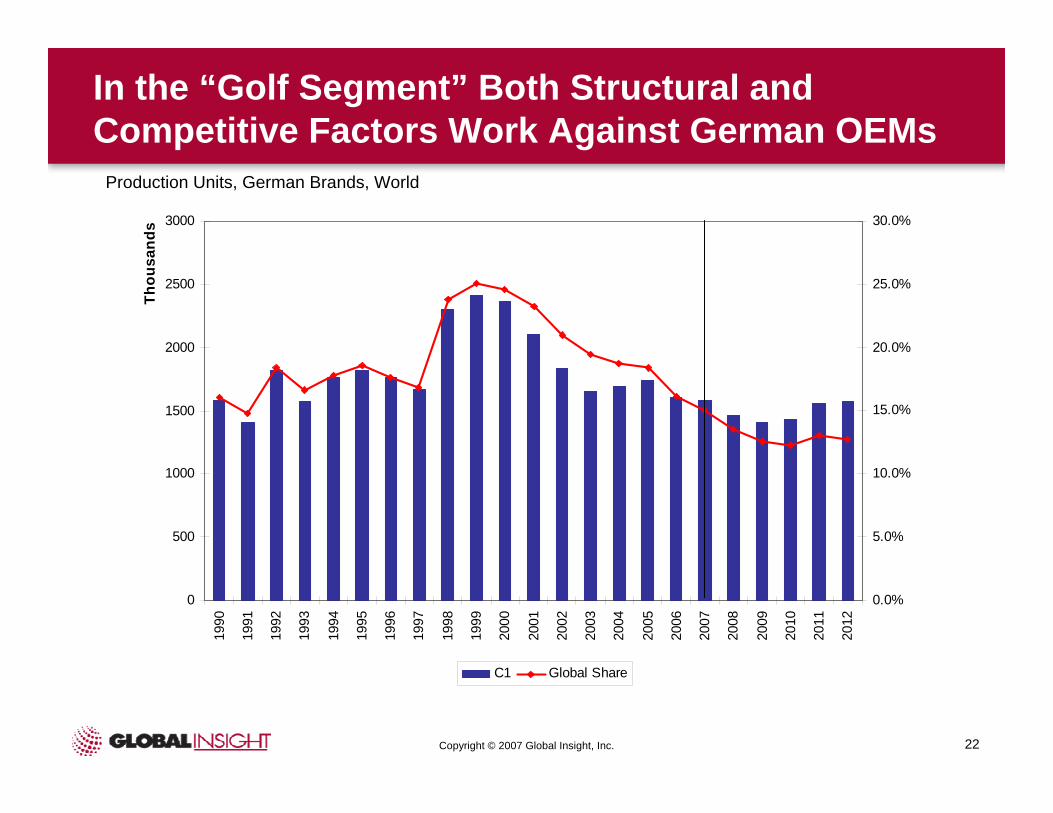

In the “Golf Segment” Both Structural and Competitive Factors Work Against German OEMs

0

500

1000

1500

2000

2500

300019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

s

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

C1 Global Share

Production Units, German Brands, World

Copyright © 2007 Global Insight, Inc. 23

Segment Analyis - Conclusions

• In the largest production segments, German Brands are not the largest manufacturers– possible competitive risk

• The segments with the highest German brand shares are rather small, but offer high product prices– possible imitation risk

• With their German-based brands alone, German manufacturers run the risk of limiting their growth potential – International acquisitions become a strategic necessity

• New segments tend to be small, so they are a natural habitat forGerman OEMs– New inventions or entry into new segments only make sense when

market leadership is achievable

Copyright © 2007 Global Insight, Inc. 24

0

1

2

3

4

5

6

7

8

9

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Mill

ions

50%

52%

54%

56%

58%

60%

62%

64%JPN

ITA

GBR

SWE

USA

DEU

DEUShare

Within the Premium Market, German Brands Will Defend Their Top Spot, but Lose on ShareProduction Units

Copyright © 2007 Global Insight, Inc. 25

Increasingly, the German Automotive Industry Is Acting As a Unified Entity

• New role of VDA vs OEMs– Integration of political and technical action

• Coordinated financial action: – Bail-out of Peguform– Support of BBS – Joint venture fund to support defaulting suppliers

• Understanding of Cluster Strength: – Joint promotion of engineering jobs– Recommendation towards German buyer of VDO– Careful moves towards increased technical cooperation:

• Bluetec (o.k, was cancelled afterwards)• Hybrid drivetrain, Bio-Fuels• Mercedes-Benz and BMW – “Brothers in Fate”

Copyright © 2007 Global Insight, Inc. 26

Can the German Car Industry Lead Again?

• In Global Terms – NO: – Not the largest companies, markets, output, growth.... – But that would assume an Auto Industry in which everybody

competes with everybody about everything– Largest segments are not the ones with the largest German brand

shares

• In Specific Terms – YES: – Largest producer of Premium Vehicles– Dominating role in Home Market, and leading within Europe– Largest future increase of production efficiency – Increasing integration with world-leading supplier base– Largest spender on auto-specific R&D

GLOBAL INSIGHT AUTOMOTIVE SEMINAR

13-14 SEPTEMBER 2007 • FRANKFURT

Thank You

Christoph StürmerDirector Product Development

E-mail: [email protected]