canada, montreal

DESCRIPTION

urbanism, brain powered economyTRANSCRIPT

GREATER MONTRÉAL

ATTRACTIVENESS INDICATORS 2011-2012

A BRAINPOWEREDECONOMY

SET-UP OR EXPANSION PROJECT IN GREATER MONTRÉAL?

As a one-stop organization, Montréal International (MI) offers a wide range of customized, free and confi dential services. The organization relies on the expertise of some fi fty professionals, all of whom are specialists in their respective fi eld.

OUR MISSION:

MI is a non-profi t organization created in 1996 as a result of a private-public partnership. Its mission is to contribute to the economic development of Greater Montréal and enhance its international status. MI is funded by some 100 mem-bers from the private and institutional sectors, as well as the Governments of Canada and Québec, the Communauté Métropolitaine de Montréal and the City of Montréal.

OUR MANDATES:

/ Attract, retain and expand foreign direct investment

/ Attract, retain and expand international organizations

/ Attract, welcome and retain foreign talent

/ Promote and reinforce Greater Montréal’s economic attractiveness and international status

MONTRÉAL INTERNATIONAL’S SERVICES

STRATEGIC SUPPORT

Public-private partnership, MI provides foreign compa-nies with valuable assistance for setting-up, expansion or

strategic alliance projects. They benefi t from expert advice to help them take full advantage of business opportunities that will power the deve lopment of their company.

KNOWLEDGE OF THE FINANCIAL AND FISCAL PROGRAMS

Companies setting-up in Greater Montréal can benefi t from various government programs. MI can provide

guidance in identifying the fi nancial and tax incentives that are right for your project as well as various potential funding sources.

INTERNATIONAL MOBILITY

MI assists companies and organizations seeking to hire foreign strategic workers particularly by

providing assistance with paperwork and easing the settlement process for these individuals and their families in Greater Montréal.

SECTORIAL EXPERTISE

We enjoy a unique expertise in Greater Montréal’s com-petitive clusters. In addition to coordinating the vari-

ous services required to the advance promising projects, MI provides foreign companies contemplating a move to the area with information and advice on high technology sectors such as aerospace, life science and health technologies, information and communications technology and cleantech.

SITE SELECTION DATA

MI can provide a full range of comparative key informa-tion on Greater Montréal’s business environment

(availability of talent, innovation, operat-ing costs, quality of life, taxes, etc.).

GOVERNMENT RELATIONS

You will benefi t from the privileged relations that we maintain with many federal, provincial

and municipal partners, business and fi nancial networks, universities and research centres.

TABLE OF CONTENTSSUMMARY 4

01 / MARKET ACCESS

Greater Montréal – An Integral Part of the North American Market

Highlights 61.1 Information on the Area 71.2 Canada – A Natural Springboard

to the North American Market 101.3 Greater Montréal –

Strategic Transportation Infrastructure 11

02 / WORKFORCE

Greater Montréal – A Wide Array of Talent for Business and Industry

Highlights 122.1 Greater Montréal –

Canada’s University Capital 132.2 A Solid and Flexible Labour Market 152.3 A Multicultural Labour Force 172.4 A Linguistic Mosaic 18

03 / COSTS

Greater Montréal – The Most Competitive Operating Costs of Any Large North American Metropolitan Area

Highlights 193.1 Total Operation Costs 203.2 Labour Costs 213.3 Facilities Costs 223.4 Electricity Costs 23

04 / TAXES AND INCENTIVES

Greater Montréal – A Tax Burden among the Most Competitive in North America

Highlights 244.1 Corporate Taxes 254.2 Main Corporate Financial

and Tax Incentives 27

05 / INNOVATION

Greater Montréal – A Unique Blend of Creativity, Diversity and High Technology

Highlights 33 5.1 Solid High Technology Clusters 34 5.2 A Critical Mass of High

Technology Talent 35 5.3 Major Foreign Investment

in High Technology 36 5.4 An Ideal R&D Environment

for Businesses 37 5.5 A Thriving North American

Venture Capital Market 38

06 / QUALITY OF LIFE

Greater Montréal – A City with a Human Dimension and a Great Place to Live, Work and Enjoy Life

Highlights 39 6.1 An Exceptional Quality of Life 40 6.2 Superior Purchasing Power 42

APPENDICES

Appendix A: Sample of Announced Private-Sector Industrial Investment Projects 44

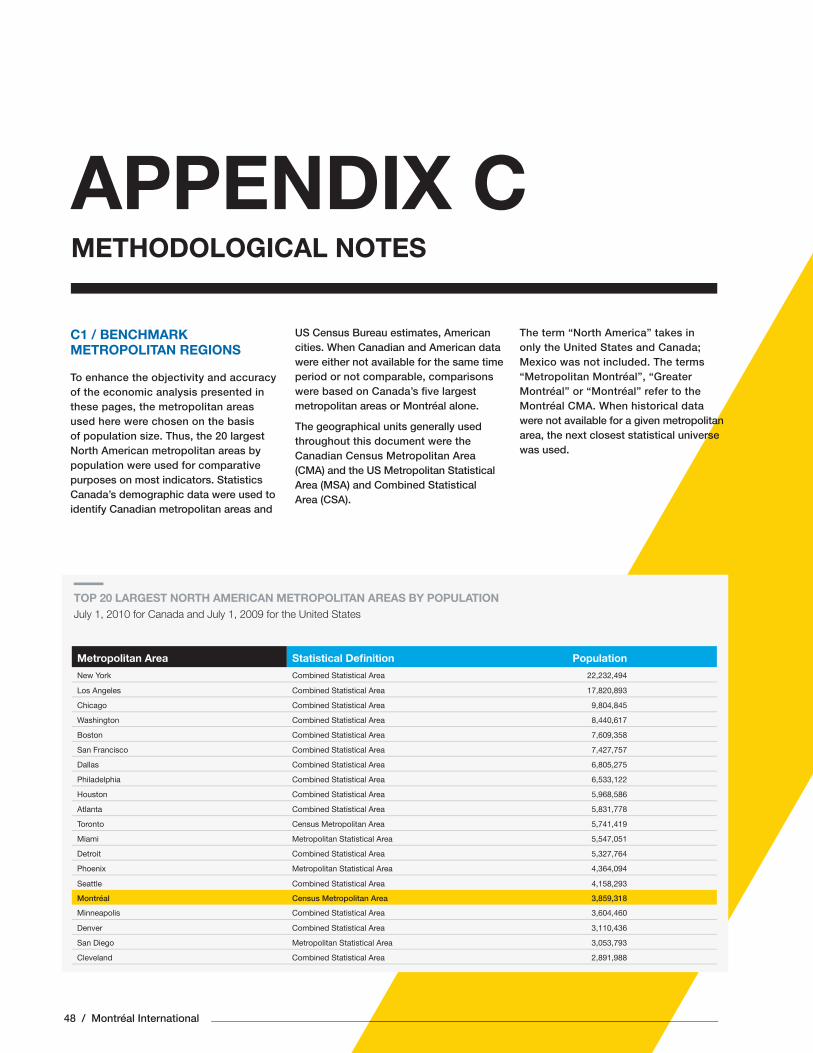

Appendix B: Sources 46 Appendix C: Methodological Notes 48

CREDITS 54

TABLE OF CONTENTSSUMMARY 4

01 / MARKET ACCESS

Greater Montréal – An Integral Part of the North American Market

Highlights 61.1 Information on the Area 71.2 Canada – A Natural Springboard

to the North American Market 101.3 Greater Montréal –

Strategic Transportation Infrastructure 11

02 / WORKFORCE

Greater Montréal – A Wide Array of Talent for Business and Industry

Highlights 122.1 Greater Montréal –

Canada’s University Capital 132.2 A Solid and Flexible Labour Market 152.3 A Multicultural Labour Force 172.4 A Linguistic Mosaic 18

03 / COSTS

Greater Montréal – The Most CompetitiveOperating Costs of Any Large North AmericanMetropolitan Area

Highlights 193.1 Total Operation Costs 203.2 Labour Costs 213.3 Facilities Costs 223.4 Electricity Costs 23

04 / TAXES AND INCENTIVES

Greater Montréal – A Tax Burden among the Most Competitive in North America

Highlights 244.1 Corporate Taxes 254.2 Main Corporate Financial

and Tax Incentives 27

05 / INNOVATION

Greater Montréal – A Unique Blend of Creativity, Diversity and High Technology

Highlights 335.1 Solid High Technology Clusters 345.2 A Critical Mass of High

Technology Talent 355.3 Major Foreign Investment

in High Technology 365.4 An Ideal R&D Environment

for Businesses 375.5 A Thriving North American

Venture Capital Market 38

06 / QUALITY OF LIFE

Greater Montréal – A City witha Human Dimension and a Great Place to Live, Work and Enjoy Life

Highlights 396.1 An Exceptional Quality of Life 406.2 Superior Purchasing Power 42

APPENDICES

Appendix A: Sample of Announced Private-Sector Industrial Investment Projects 44

Appendix B: Sources 46 Appendix C: Methodological Notes 48

CREDITS 54

4 / Montréal International

This sixth annual edition of Greater Montréal’s Attractiveness Indicators is designed to meet the information needs of foreign investors contemplating a move to the area. It highlights the latest data on the region’s performance in North America along the six key elements that characterize a business hub:

SUMMARY

01 / MARKET ACCESS

An Integral Part of the North American Market

/ A strategic location in North America – under two hours from Boston, New York and Toronto by air, less than an hour from the American border by road

/ Direct access to the North American Free Trade Agreement (NAFTA) market and its 460 million consumers

/ The United States – Greater Montréal’s most important trading partner

/ Strategic transportation infrastructure, including two international airports and one of North America’s busiest ports.

02 / WORKFORCE

A Wide Array of Talent for Business and Industry

/ The largest pool of university graduates in Canada with over 40,000 new gradu-ates every year

/ A stable labour market – 1st among large North American metropolitan regions with a 1.7% increase in jobs during the 2008-2010 economic downturn

/ More than 50% of the population is bilingual (French/English) and nearly 20% master three or more languages

/ Some 120 cultural commu nities are present in the area.

03 / COSTS

The Most Competitive Operating Costs of Any Large North American Metropolitan Area

/ Total operating costs are 5% lower than the average for other large North American metropolitan areas

/ A 14% average cost advantage for R&D sectors

/ Potential for substantial savings particularly for:

• Labour

• Space

• Electricity.

GREATER MONTRÉAL A BRAIN POWERED ECONOMY

Attractiveness Indicators 2011-2012 / 5

04 / TAXES AND INCENTIVES

A Tax Burden among the Most Competitive in North America

/ The region’s tax burden for R&D companies is the most favourable among large international metropolitan areas due in large part to generous R&D tax credits offered by the govern-ments of Canada and Québec

/ The lowering of the federal corporate income tax rate from 22% to 15% by 2012 means that Canada will enjoy the most competitive corporate revenue taxation rate among the G7 countries

/ An important array of targeted and highly competitive government-backed incentives provide technology companies with stable support.

05 / INNOVATION

A Unique Blend of Creativity, Diversity and High Technology

/ Constant interplay between technology, science, art and culture explains the success, among other things, of Montréal’s high technology clusters, video game industry and creative enterprises such as the Cirque du Soleil

/ Major high technology clusters responsible for one out of ten jobs are: aerospace, information and communi-cations technologies (ICT), life science and health technologies (LSHT) and Cleantech

/ A network of universities with the largest share of research funding in Canada and a broad range of expertise in several hundred research centres

/ Effective intellectual property protec-tion backed by international treaties.

06 / QUALITY OF LIFE

A City with a Human Dimension and a Great Place to Live, Work and Enjoy Life

/ Greater Montréal is a cosmopolitan, bilingual and international city, with a distinct personality serving as a bridge between North America and Europe

/ An excellent quality/cost ratio with superior purchasing power

/ A safe environment with competitive health and transportation infrastructure

/ A green city known around the world for its cultural, recreational and sports scene as well as its talent and technology.

Po

rt o

f M

ont

réal

MARKET ACCESSGREATER MONTRÉAL –

AN INTEGRAL PART OF THE

NORTH AMERICAN MARKET

01/ A strategic location in North America –

under two hours from Boston, New York and Toronto by air, less than an hour from the American border by road

/ Direct access to the North American Free Trade Agreement (NAFTA) market and its 460 million consumers

/ The United States – Greater Montréal’s most important trading partner

/ Effi cient transportation infrastructure, including two international airports and one of North America’s busiest ports.

Attractiveness Indicators 2011-2012 / 7

1 Source: The Conference Board of Canada and Statistics Canada2 Source: Unless otherwise indicated, $ and ¢ signs refer to CA $3 Source: The Brookings Institution, London School of Economics and Political Science and Deutsche Bank Research, City of Montréal

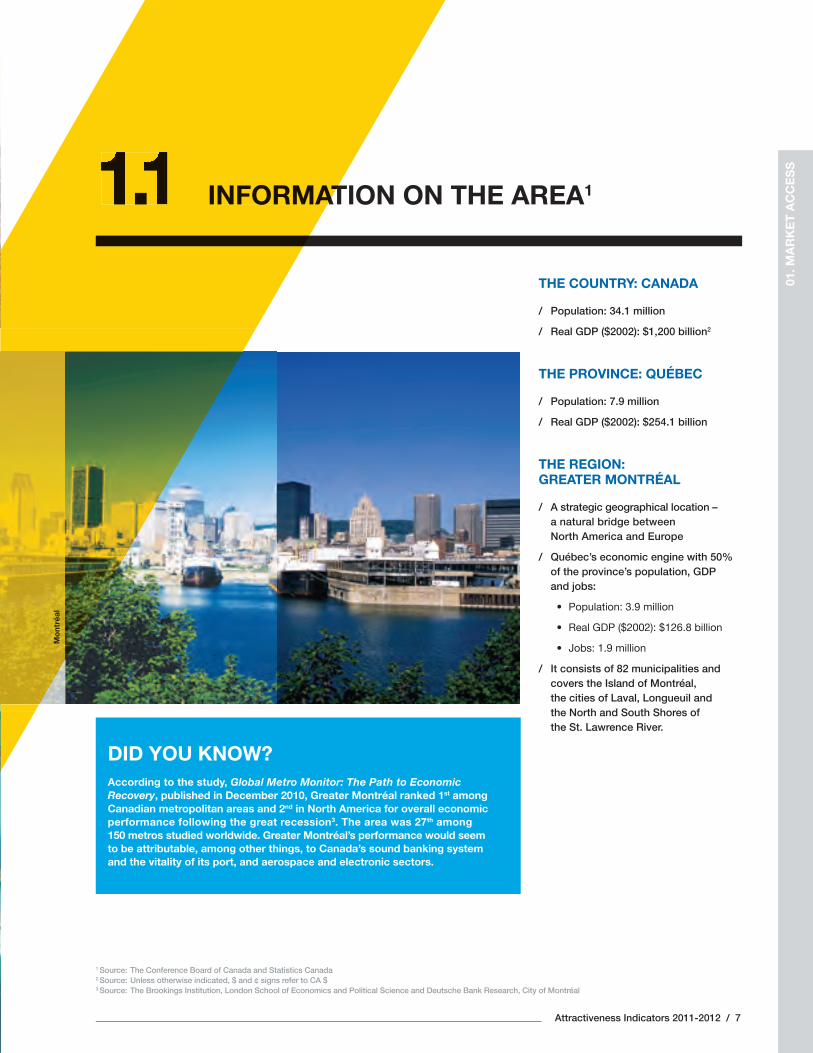

INFORMATION ON THE AREA11.11.1THE COUNTRY: CANADA

/ Population: 34.1 million

/ Real GDP ($2002): $1,200 billion2

THE PROVINCE: QUÉBEC

/ Population: 7.9 million

/ Real GDP ($2002): $254.1 billion

THE REGION: GREATER MONTRÉAL

/ A strategic geographical location – a natural bridge between North America and Europe

/ Québec’s economic engine with 50% of the province’s population, GDP and jobs:

• Population: 3.9 million

• Real GDP ($2002): $126.8 billion

• Jobs: 1.9 million

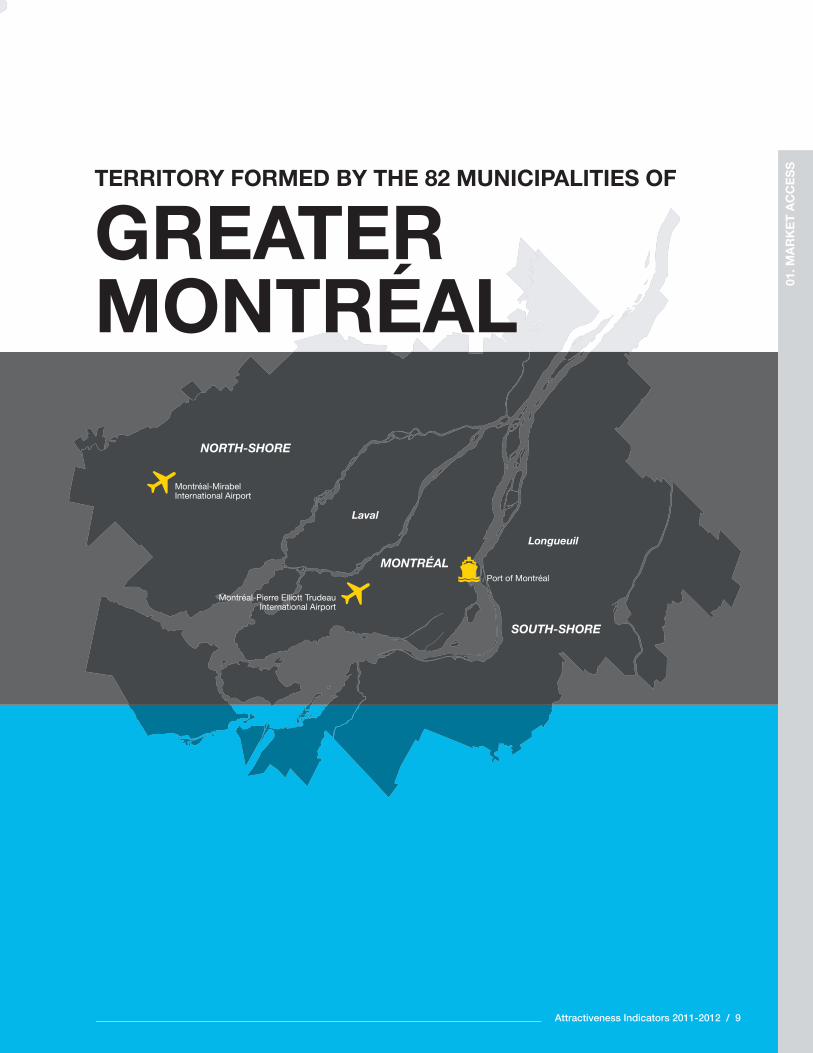

/ It consists of 82 municipalities and covers the Island of Montréal, the cities of Laval, Longueuil and the North and South Shores of the St. Lawrence River.

INFORMAT1.11.1

01. M

AR

KE

T A

CC

ES

S

DID YOU KNOW?According to the study, Global Metro Monitor: The Path to Economic Recovery, published in December 2010, Greater Montréal ranked 1st among Canadian metropolitan areas and 2nd in North America for overall economic performance following the great recession3. The area was 27th among 150 metros studied worldwide. Greater Montréal’s performance would seem to be attributable, among other things, to Canada’s sound banking system and the vitality of its port, and aerospace and electronic sectors.

Mo

ntré

al

8 / Montréal International

FLIGHT TIME FROM MONTRÉAL

HOUSTON

MONTRÉAL

OTTAWABOSTON

NEW YORK

PHILADELPHIA

WASHINGTON

ATLANTA

DALLAS

CLEVELAND

MINNEAPOLIS

TORONTO

MIAMI

BOSTON: 1 H 20

TORONTO: 1 H 20

NEW YORK: 1 H 53

CHICAGO: 2 H 21

LOS ANGELES: 6 H 28

LONDON: 6 H 40

PARIS: 6 H 49

CHICAGO

DENVER

PHOENIX

SAN DIEGO

LOS ANGELES

SAN FRANCISCO

VANCOUVERCALGARY

DETROIT

SEATTLE

NORTH AMERICA

Attractiveness Indicators 2011-2012 / 9

TERRITORY FORMED BY THE 82 MUNICIPALITIES OF

GREATER MONTRÉAL

NORTH-SHORE

SOUTH-SHORE

MONTRÉAL

Montréal-Mirabel International Airport

Montréal-Pierre Elliott Trudeau International Airport

Port of Montréal

Longueuil

Laval

01. M

AR

KE

T A

CC

ES

S

Mo

ntré

al-T

rud

eau

Air

po

rt

10 / Montréal International

“

CANADA – A NATURAL SPRINGBOARD TO THE NORTH AMERICAN MARKET 1.2

DIRECT ACCESS TO THE NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) MARKET

/ Approximately 460 million consumers and a GDP of US$17 trillion4

A FREE FLOW OF GOODS ACROSS NATIONAL BORDERS

/ One of the most effi cient border inspection systems in the world – usual wait time of less than ten minutes5.

THE UNITED STATES – GREATER MONTRÉAL’S LARGEST TRADING PARTNER6

/ The value of Greater Montréal’s exports to the United States (US) was over $30 billion in 2007, or nearly 60% of all of Québec’s exports to the US

/ The value of Greater Montréal’s exports to European Union (EU): almost $6 billion in 2007, or 70% of all of Québec’s exports to the EU

DIVERSIFICATION OF FREE-TRADE AGREEMENTS

/ The signing of free trade agreements between Canada and several countries (or groups of countries): the European Free Trade Association (EFTA), Chile, Columbia, Costa Rica, Israel, Jordan, Panama and Peru.

4 Source: Invest in Canada5 Source: Invest in Canada6 Source: Institut de la statistique du Québec

”

Medtech, Specialist in Surgical Assistive Robots

We wanted to get closer to the North American market, particularly the Northeast. The choice of Montréal is based not only on its cultural affi nity with France, but on the fact that it is a video game hub and the visualisation and surgical planning software technology that is of particular interest to us is readily available here.

Mr. Bertin NahumPresident and FounderMedtech

U

ENTS

agreementseveral countries

es): the European tion (EFTA), Chile,

Rica, Israel, Jordan, ru.

Attractiveness Indicators 2011-2012 / 11

GREATER MONTRÉAL – STRATEGIC TRANSPORTATION INFRASTRUCTURE 1.3

7 Source: Aéroports de Montréal8 Source: Port of Montréal9 Source: The World Economic Forum and Invest in Canada

GREATER MTRANSPO1.3

DID YOU KNOW?Canada is known for9:

/ The most favourable business environment forecast for 2011-2015: 1st among G7 countries and 7th among 82 countries (The Economist Intelligence Unit, 2011)

/ Market access, border management, transportation and communications infrastructure and business environment:1st among G7 countries and 8th among 125 countries measured on the Enabling Trade Index in 2010 (The World Economic Forum, 2010)

/ The least amount of paperwork required for exporting goods: 2nd among 125 countries (The World Economic Forum, 2010)

/ The fewest procedures required for creating an enterprise: 1st among 183 countries (The World Bank, 2010).

TWO MAJOR INTERNATIONAL AIRPORTS7

/ Montréal-Pierre-Elliott Trudeau International Airport

• Main Canadian airport east of the Great Lakes

• Natural hub for traffi c between North America and Europe

• Over 40 airlines, most of which are major North American or European carriers present

• 130 non-stop destinations in Canada, the United States and around the world

• Nearly 13 million passengers in 2010, a 6.1% increase over the year 2009.

/ Montréal-Mirabel International Airport

• A 24-hour, all-cargo airport

• Some of the best operating condi-tions in the American Northeast – no curfew, no congestion

• Regularly used by some 20 carriers and traffi c is growing

Nearly 200,000 of metric tons of goods transit through these two airports annually.

THE PORT OF MONTRÉAL – ONE OF THE WORLD’S BUSIEST8

/ Located on the Saint Lawrence River, 1,600 km from the Atlantic Ocean

/ The most important container port in Eastern Canada and 9th largest in North America

/ Served by seven of the world’s ten largest container lines

/ Recognized for its effi ciency in container transfer to and from ships, trains and trucks

/ Annual cargo volume of 25.9 metric tons in 2010, up by 5.7% over 2009.

01. M

AR

KE

T A

CC

ES

S

WORKFORCE GREATER MONTRÉAL –

A WIDE ARRAY OF TALENT

FOR BUSINESS AND INDUSTRY

02/ The largest pool of university graduates

in Canada with over 40,000 new gradu-ates every year

/ A highly diverse and competent workforce due to the presence of head offi ces of many local companies and foreign subsidiaries

/ A stable labour market – 1st among large North American metropolitan regions with a 1.7% increase in jobs during the 2008-2010 economic downturn

/ More than 50% of the population is bilingual (French/English) and nearly 20% master three or more languages

/ Some 120 cultural communities are present in the area.

McG

ill U

nive

rsit

y

Attractiveness Indicators 2011-2012 / 13

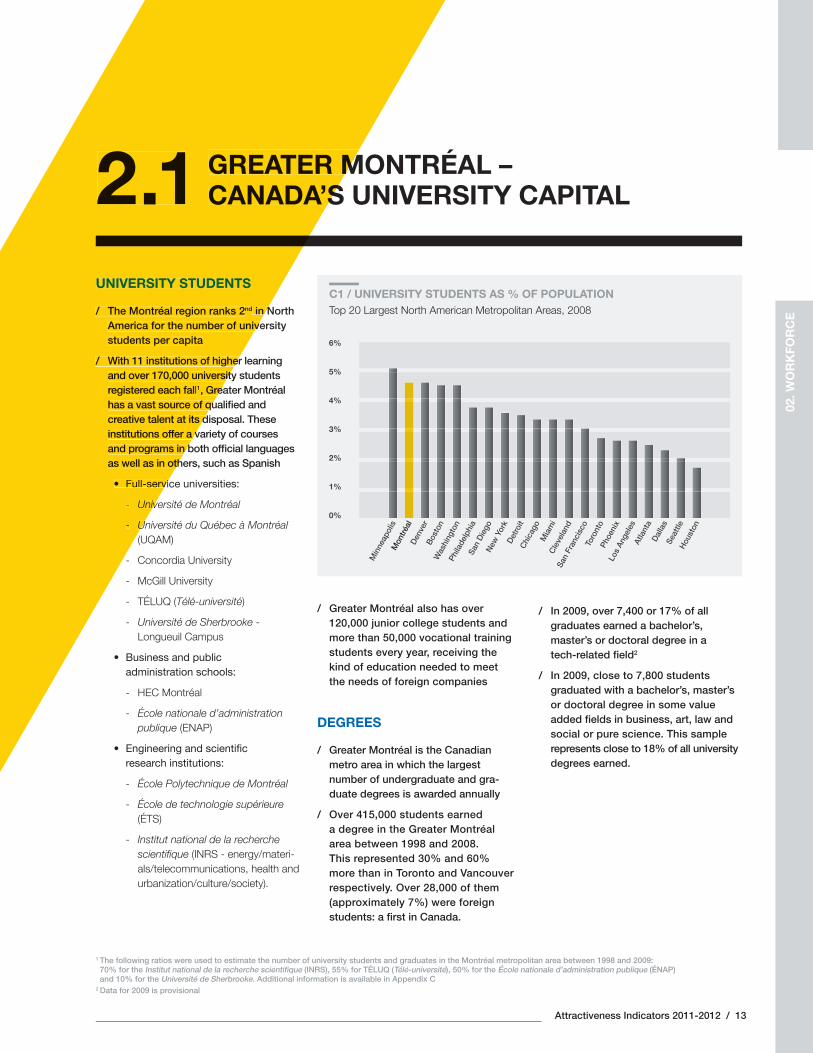

GREATER MONTRÉAL – CANADA’S UNIVERSITY CAPITAL 2.1

6%

5%

4%

3%

2%

1%

0%

Min

neap

olis

Mon

tréal

D

enve

rB

osto

nW

ashi

ngto

nPh

ilade

lphi

aSa

n D

iego

New

Yor

kD

etro

itC

hica

goM

iam

iC

leve

land

San

Fran

cisc

oTo

ront

o Ph

oeni

xLo

s An

gele

sAt

lant

aD

alla

sSe

attle

Hou

ston

C1 / UNIVERSITY STUDENTS AS % OF POPULATIONTop 20 Largest North American Metropolitan Areas, 2008

/ Greater Montréal also has over 120,000 junior college students and more than 50,000 vocational training students every year, receiving the kind of education needed to meet the needs of foreign companies

DEGREES

/ Greater Montréal is the Canadian metro area in which the largest number of undergraduate and gra-duate degrees is awarded annually

/ Over 415,000 students earned a degree in the Greater Montréal area between 1998 and 2008. This represented 30% and 60% more than in Toronto and Vancouver respectively. Over 28,000 of them (approximately 7%) were foreign students: a fi rst in Canada.

/ In 2009, over 7,400 or 17% of all graduates earned a bachelor’s, master’s or doctoral degree in a tech-related fi eld2

/ In 2009, close to 7,800 students graduated with a bachelor’s, master’s or doctoral degree in some value added fi elds in business, art, law and social or pure science. This sample represents close to 18% of all university degrees earned.

UNIVERSITY STUDENTS

/ The Montréal region ranks 2nd in North America for the number of university students per capita

/ With 11 institutions of higher learning and over 170,000 university students registered each fall1, Greater Montréal has a vast source of qualifi ed and creative talent at its disposal. These institutions offer a variety of courses and programs in both offi cial languages as well as in others, such as Spanish

• Full-service universities:

- Université de Montréal

- Université du Québec à Montréal (UQAM)

- Concordia University

- McGill University

- TÉLUQ (Télé-université)

- Université de Sherbrooke - Longueuil Campus

• Business and public administration schools:

- HEC Montréal

- École nationale d’administration publique (ENAP)

• Engineering and scientifi c research institutions:

- École Polytechnique de Montréal

- École de technologie supérieure (ÉTS)

- Institut national de la recherche scientifi que (INRS - energy/materi-als/telecommunications, health and urbanization/culture/society).

02. W

OR

KFO

RC

E

1 The following ratios were used to estimate the number of university students and graduates in the Montréal metropolitan area between 1998 and 2009: 70% for the Institut national de la recherche scientifi que (INRS), 55% for TÉLUQ (Télé-université), 50% for the École nationale d’administration publique (ÉNAP) and 10% for the Université de Sherbrooke. Additional information is available in Appendix C

2 Data for 2009 is provisional

GREATER MCANADA’S2.1

UNIVERSITY STUDENTS

/ The Montréal region ranks 2nd in NAmerica for the number of univestudents per capita

/ With 11 institutions of higherand over 170,000 universityregistered each fall1, Grehas a vast source of qucreative talent at its dinstitutions offer a vand programs in bas well as in oth

• Full-servi

- Univ

- U

14 / Montréal International

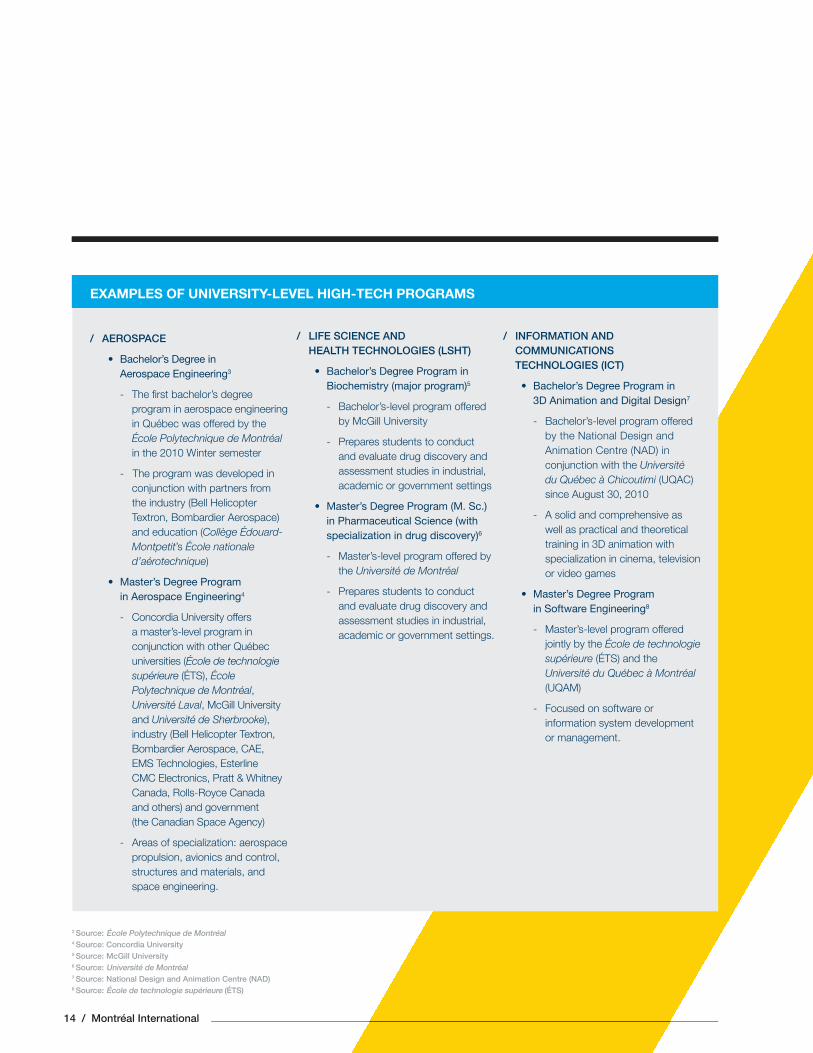

3 Source: École Polytechnique de Montréal4 Source: Concordia University5 Source: McGill University6 Source: Université de Montréal7 Source: National Design and Animation Centre (NAD)8 Source: École de technologie supérieure (ÉTS)

/ AEROSPACE

• Bachelor’s Degree in Aerospace Engineering3

- The fi rst bachelor’s degree program in aerospace engineering in Québec was offered by the École Polytechnique de Montréal in the 2010 Winter semester

- The program was developed in conjunction with partners from the industry (Bell Helicopter Textron, Bombardier Aerospace) and education (Collège Édouard-Montpetit’s École nationale d’aérotechnique)

• Master’s Degree Program in Aerospace Engineering4

- Concordia University offers a master’s-level program in conjunction with other Québec universities (École de technologie supérieure (ÉTS), École Polytechnique de Montréal, Université Laval, McGill University and Université de Sherbrooke), industry (Bell Helicopter Textron, Bombardier Aerospace, CAE, EMS Technologies, Esterline CMC Electronics, Pratt & Whitney Canada, Rolls-Royce Canada and others) and government (the Canadian Space Agency)

- Areas of specialization: aerospace propulsion, avionics and control, structures and materials, and space engineering.

/ LIFE SCIENCE AND HEALTH TECHNOLOGIES (LSHT)

• Bachelor’s Degree Program in Biochemistry (major program)5

- Bachelor’s-level program offered by McGill University

- Prepares students to conduct and evaluate drug discovery and assessment studies in industrial, academic or government settings

• Master’s Degree Program (M. Sc.) in Pharmaceutical Science (with specialization in drug discovery)6

- Master’s-level program offered by the Université de Montréal

- Prepares students to conduct and evaluate drug discovery and assessment studies in industrial, academic or government settings.

/ INFORMATION AND COMMUNICATIONS TECHNOLOGIES (ICT)

• Bachelor’s Degree Program in 3D Animation and Digital Design7

- Bachelor’s-level program offered by the National Design and Animation Centre (NAD) in conjunction with the Université du Québec à Chicoutimi (UQAC) since August 30, 2010

- A solid and comprehensive as well as practical and theoretical training in 3D animation with specialization in cinema, television or video games

• Master’s Degree Program in Software Engineering8

- Master’s-level program offered jointly by the École de technologie supérieure (ÉTS) and the Université du Québec à Montréal (UQAM)

- Focused on software or information system development or management.

EXAMPLES OF UNIVERSITY-LEVEL HIGH-TECH PROGRAMS

Attractiveness Indicators 2011-2012 / 15

Toro

nto

New

Yor

kM

ontré

alLo

s An

gele

sC

hica

goB

osto

nVa

ncou

ver

San

Fran

cisc

oPh

ilade

lphi

aAt

lant

aD

alla

sSa

n D

iego

Hou

ston

Mia

mi

Min

neap

olis

Was

hing

ton

Den

ver

Phoe

nix

Seat

tleD

etro

it

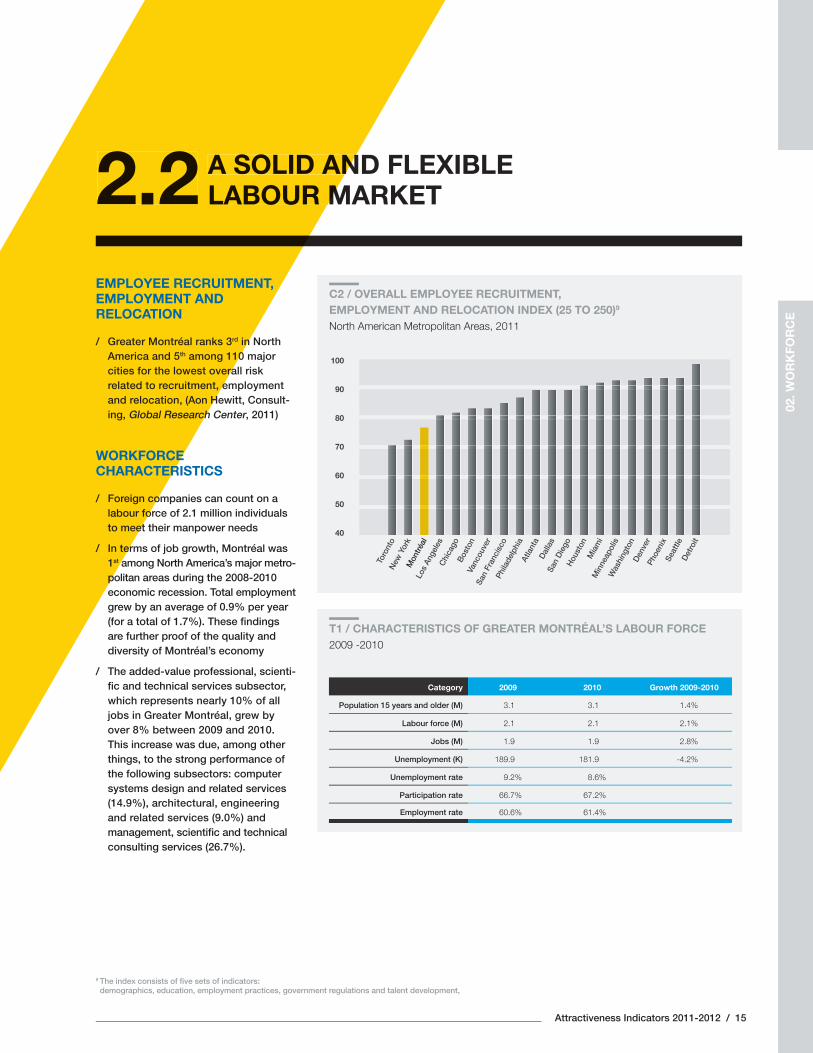

A SOLID AND FLEXIBLE LABOUR MARKET2.2

C2 / OVERALL EMPLOYEE RECRUITMENT, EMPLOYMENT AND RELOCATION INDEX (25 TO 250)9 North American Metropolitan Areas, 2011

Category 2009 2010 Growth 2009-2010

Population 15 years and older (M) 3.1 3.1 1.4%

Labour force (M) 2.1 2.1 2.1%

Jobs (M) 1.9 1.9 2.8%

Unemployment (K) 189.9 181.9 -4.2%

Unemployment rate 9.2% 8.6%

Participation rate 66 .7% 67.2%

Employment rate 60.6% 61.4%

T1 / CHARACTERISTICS OF GREATER MONTRÉAL’S LABOUR FORCE2009 -2010

9 The index consists of fi ve sets of indicators: demographics, education, employment practices, government regulations and talent development,

A SOLID ANLABOUR M2.2

EMPLOYEE RECRUITMENT, EMPLOYMENT AND RELOCATION

/ Greater Montréal ranks 3rd in North America and 5th among 110 major cities for the lowest overall risk related to recruitment, employment and relocation, (Aon Hewitt, Consult-ing, Global Research Center, 2011)

WORKFORCE CHARACTERISTICS

/ Foreign companies can count on a labour force of 2.1 million individuals to meet their manpower needs

/ In terms of job growth, Montréal was 1st among North America’s major metro-politan areas during the 2008-2010 economic recession. Total employment grew by an average of 0.9% per year (for a total of 1.7%). These fi ndings are further proof of the quality and diversity of Montréal’s economy

/ The added-value professional, scienti-fi c and technical services subsector, which represents nearly 10% of all jobs in Greater Montréal, grew by over 8% between 2009 and 2010. This increase was due, among other things, to the strong performance of the following subsectors: computer systems design and related services (14.9%), architectural, engineering and related services (9.0%) and management, scientifi c and technical consulting services (26.7%).

02. W

OR

KFO

RC

E

100

90

80

70

60

50

40

Qua

ys o

f th

e O

ld P

ort

, Mo

ntré

al

16 / Montréal International

FOREIGN SUBSIDIARY EMPLOYMENT

/ Foreign subsidiaries established in Greater Montréal contribute to the development of human capitaland growth of Greater Montréal’s international competitiveness

/ They represent:

• Over 1,900 foreign subsidiaries operating some 2,100 facilities

• Over 165,000 direct and 100,000 indirect jobs, over 50% of which in facilities with 250 or more employees

• 9% of all jobs and 13% of private sector jobs

• Over 20% of the region’s GDP ($26 billion in annual expenditures)

• An important magnet for investment: in 2009, nearly one out of every three non-residential private investment dollars originated with a foreign subsidiary ($3.3 billion).

4%

2%

0%

-2%

-4%

-6%

-8%

C3 / VARIATION IN TOTAL EMPLOYMENT (%)Top 20 Largest North American Metropolitan Areas, 2008-2010

Mon

tréal

Toro

nto

Hou

ston

Dal

las

Min

neap

olis

Bos

ton

Phoe

nix

Seat

tleW

ashi

ngto

nN

ew Y

ork

San

Die

goPh

ilade

lphi

aM

iam

iC

leve

land

Chi

cago

Den

ver

San

Fran

cisc

oLo

s An

gele

sD

etro

itAt

lant

a

Attractiveness Indicators 2011-2012 / 17

A MULTICULTURAL LABOUR FORCE

/ The richness and diversity of Greater Montréal’s workforce is due to the meeting between the Anglophone and Francophone communities and integration of over 120 immigrant cultural groups

/ With an international migration balance of nearly 44,000 between July 2008 and June 2009, Greater Montréal ranks 7th in North America in that category. From a percentage of total population perspective, it comes in 2nd among top North American metro areas. These numbers underline the fact that the region is becoming increasingly attractive to immigrants and particularly foreign strategic talent.

2.3

1.6%

1.4%

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

0.0%

Toro

nto

Mon

tréal

Mia

mi

San

Fran

cisc

oPh

oeni

xN

ew Y

ork

Los

Ange

les

Hou

ston

Dal

las

Was

hing

ton

Atla

nta

Bos

ton

Chi

cago

San

Die

goSe

attle

Den

ver

Min

neap

olis

Phila

delp

hia

Det

roit

Cle

vela

nd

C4 / INTERNATIONAL MIGRATION BALANCE AS % OF TOTAL POPULATION Top 20 Largest North America Metropolitan Areas, 2008-2009

A MULTICULLABOUR F

/ The richness and diversity of GreatMontréal’s workforce is due to themeeting between the Anglophonand Francophone communitieintegration of over 120 immigcultural groups

/ With an international migbalance of nearly 44,00July 2008 and June 2Montréal ranks 7th inin that category. Fof total populatiit comes in 2nd

American menumbers unregion is battractivparticu

2.3

02. W

OR

KFO

RC

E

Ub

iso

ft, M

ont

réal

18 / Montréal International

“

“ ””

A LINGUISTIC MOSAIC

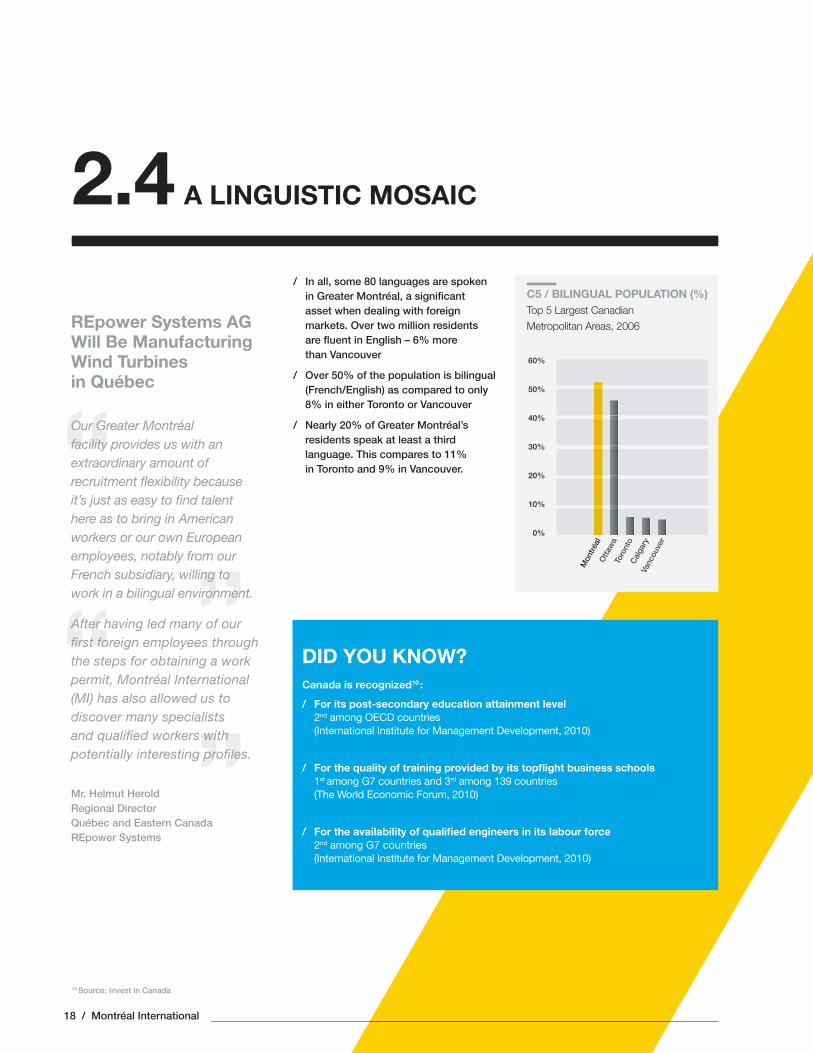

/ In all, some 80 languages are spoken in Greater Montréal, a signifi cant asset when dealing with foreign markets. Over two million residents are fl uent in English – 6% more than Vancouver

/ Over 50% of the population is bilingual (French/English) as compared to only 8% in either Toronto or Vancouver

/ Nearly 20% of Greater Montréal’s residents speak at least a third language. This compares to 11% in Toronto and 9% in Vancouver.

2.4

10 Source: Invest in Canada

REpower Systems AG Will Be Manufacturing Wind Turbines in Québec

Our Greater Montréal facility provides us with an extraordinary amount of recruitment fl exibility because it’s just as easy to fi nd talent here as to bring in American workers or our own European employees, notably from our French subsidiary, willing to work in a bilingual environment.

After having led many of our fi rst foreign employees through the steps for obtaining a work permit, Montréal International (MI) has also allowed us to discover many specialists and qualifi ed workers with potentially interesting profi les.

Mr. Helmut HeroldRegional DirectorQuébec and Eastern CanadaREpower Systems

DID YOU KNOW?Canada is recognized10 :

/ For its post-secondary education attainment level 2nd among OECD countries

(International Institute for Management Development, 2010)

/ For the quality of training provided by its topfl ight business schools 1st among G7 countries and 3rd among 139 countries

(The World Economic Forum, 2010)

/ For the availability of qualifi ed engineers in its labour force 2nd among G7 countries

(International Institute for Management Development, 2010)

Mon

tréal

Otta

wa

Toro

nto

Cal

gary

Vanc

ouve

r

C5 / BILINGUAL POPULATION (%) Top 5 Largest Canadian

Metropolitan Areas, 2006

60%

50%

40%

30%

20%

10%

0%

COSTS GREATER MONTRÉAL –

THE MOST COMPETITIVE

OPERATING COSTS OF ANY

LARGE NORTH AMERICAN

METROPOLITAN AREA

03/ Total operating costs are 5% lower

than the average for other large North American metropolitan areas

/ An average cost advantage of 14% in R&D sectors

/ Potential for substantial savings particularly for:

• Labour

• Space

• Electricity

Pal

ais

des

con

grè

s d

e M

ontr

éal

(Mo

ntré

al C

onv

enti

on

Cen

tre)

20 / Montréal International

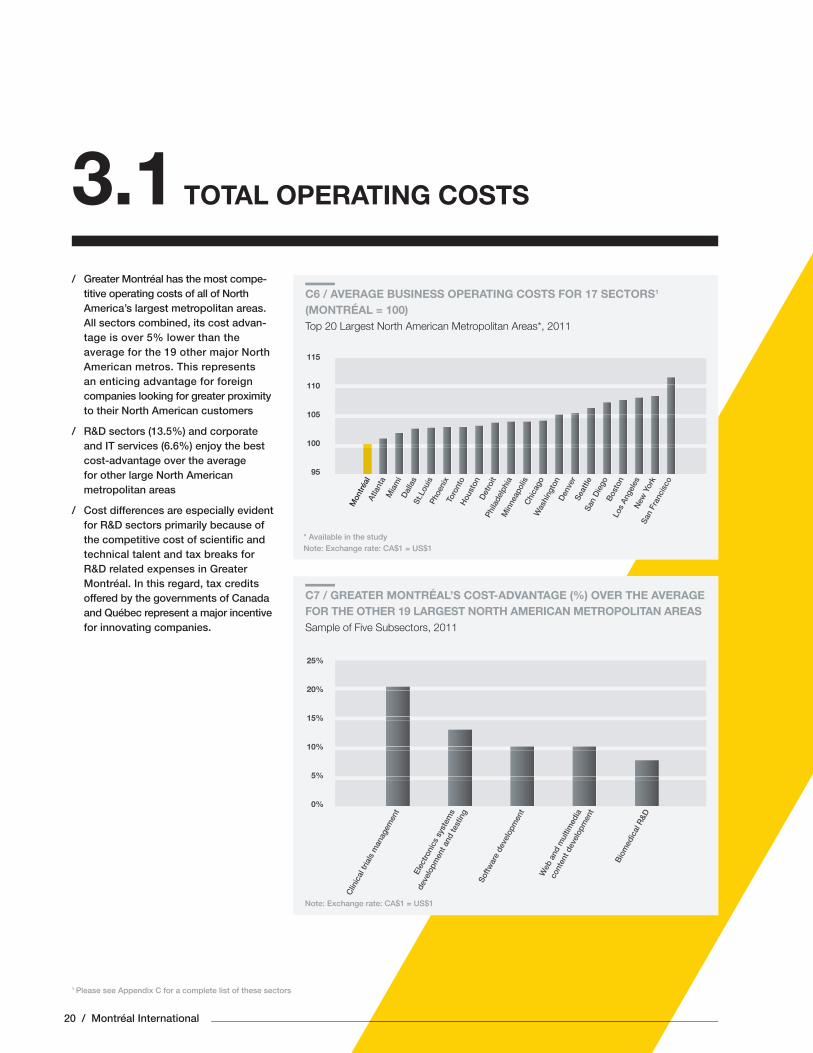

TOTAL OPERATING COSTS3.1/ Greater Montréal has the most compe-

titive operating costs of all of North America’s largest metropolitan areas. All sectors combined, its cost advan-tage is over 5% lower than the average for the 19 other major North American metros. This represents an enticing advantage for foreign companies looking for greater proximity to their North American customers

/ R&D sectors (13.5%) and corporate and IT services (6.6%) enjoy the best cost-advantage over the average for other large North American metropolitan areas

/ Cost differences are especially evident for R&D sectors primarily because of the competitive cost of scientifi c and technical talent and tax breaks for R&D related expenses in Greater Montréal. In this regard, tax credits offered by the governments of Canada and Québec represent a major incentive for innovating companies.

1 Please see Appendix C for a complete list of these sectors

25%

20%

15%

10%

5%

0%

Clin

ical

tria

ls m

anag

emen

t

Elec

troni

cs s

yste

ms

deve

lopm

ent a

nd te

stin

g

Softw

are

deve

lopm

ent

Web

and

mul

timed

ia

cont

ent d

evel

opm

ent

Bio

med

ical

R&D

C7 / GREATER MONTRÉAL’S COST-ADVANTAGE (%) OVER THE AVERAGE FOR THE OTHER 19 LARGEST NORTH AMERICAN METROPOLITAN AREASSample of Five Subsectors, 2011

Note: Exchange rate: CA$1 = US$1

C6 / AVERAGE BUSINESS OPERATING COSTS FOR 17 SECTORS1 (MONTRÉAL = 100)Top 20 Largest North American Metropolitan Areas*, 2011

115

110

105

100

95

Mon

tréal

Atla

nta

Mia

mi

Dal

las

St.L

ouis

Phoe

nix

Toro

nto

Hou

ston

Det

roit

Phila

delp

hia

Min

neap

olis

Chi

cago

Was

hing

ton

Den

ver

Seat

tleSa

n D

iego

Bos

ton

Los

Ange

les

New

Yor

kSa

n Fr

anci

sco

* Available in the study Note: Exchange rate: CA$1 = US$1

Attractiveness Indicators 2011-2012 / 21

03. C

OS

TS

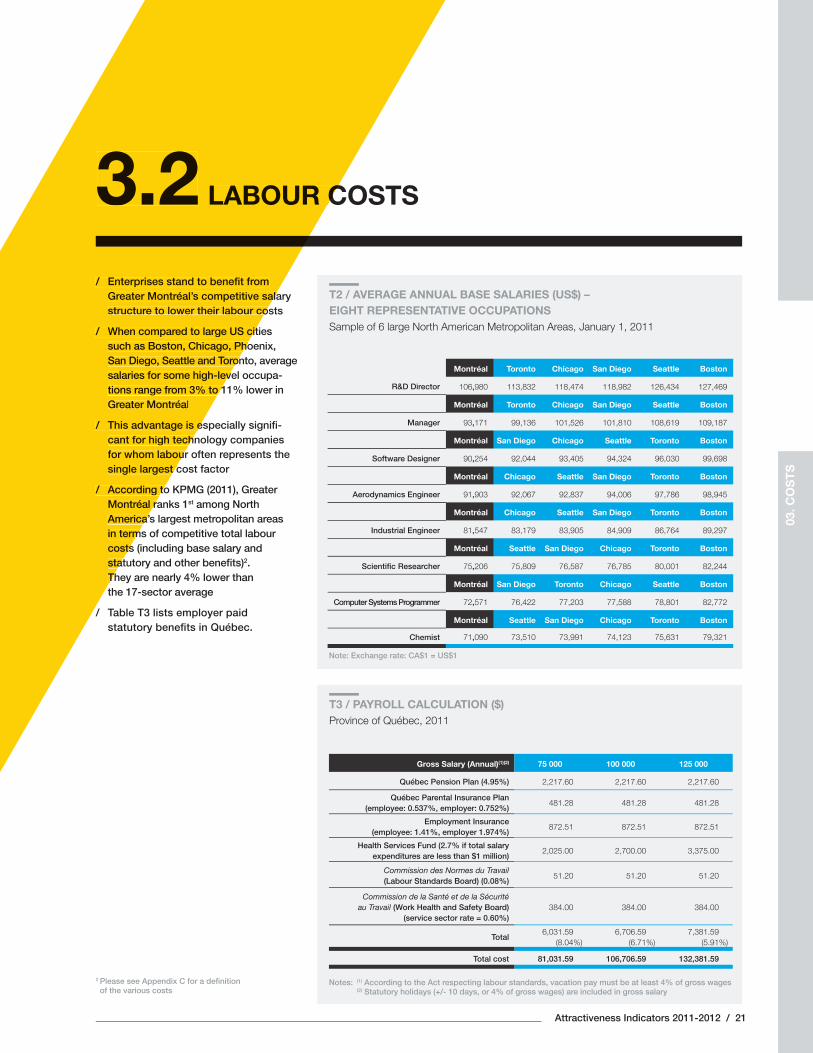

LABOUR COSTS3.2/ Enterprises stand to benefi t from

Greater Montréal’s competitive salary structure to lower their labour costs

/ When compared to large US cities such as Boston, Chicago, Phoenix, San Diego, Seattle and Toronto, average salaries for some high-level occupa-tions range from 3% to 11% lower in Greater Montréal

/ This advantage is especially signifi -cant for high technology companies for whom labour often represents the single largest cost factor

/ According to KPMG (2011), Greater Montréal ranks 1st among North America’s largest metropolitan areas in terms of competitive total labour costs (including base salary and statutory and other benefi ts)2. They are nearly 4% lower than the 17-sector average

/ Table T3 lists employer paid statutory benefi ts in Québec.

Gross Salary (Annual)(1)(2) 75 000 100 000 125 000

Québec Pension Plan (4.95%) 2,217.60 2,217.60 2,217.60

Québec Parental Insurance Plan (employee: 0.537%, employer: 0.752%)

481.28 481.28 481.28

Employment Insurance (employee: 1.41%, employer 1.974%)

872.51 872.51 872.51

Health Services Fund (2.7% if total salary expenditures are less than $1 million)

2,025.00 2,700.00 3,375.00

Commission des Normes du Travail (Labour Standards Board) (0.08%)

51.20 51.20 51.20

Commission de la Santé et de la Sécurité au Travail (Work Health and Safety Board)

(service sector rate = 0.60%)384.00 384.00 384.00

Total6,031

(8.59.04%)

6,706 (6

.59

.71%)7,381

(5.59.91%)

Total cost 81,031.59 106,706.59 132,381.59

Montréal Toronto Chicago San Diego Seattle Boston

R&D Director 106,980 113,832 118,474 118,982 126,434 127,469

Montréal Toronto Chicago San Diego Seattle Boston

Manager 93,171 99,136 101,526 101,810 108,619 109,187

Montréal San Diego Chicago Seattle Toronto Boston

Software Designer 90,254 92,044 93,405 94,324 96,030 99,698

Montréal Chicago Seattle San Diego Toronto Boston

Aerodynamics Engineer 91,903 92,067 92,837 94,006 97,786 98,945

Montréal Chicago Seattle San Diego Toronto Boston

Industrial Engineer 81,547 83,179 83,905 84,909 86,764 89,297

Montréal Seattle San Diego Chicago Toronto Boston

Scientifi c Researcher 75,206 75,809 76,587 76,785 80,001 82,244

Montréal San Diego Toronto Chicago Seattle Boston

Computer Systems Programmer 72,571 76,422 77,203 77,588 78,801 82,772

Montréal Seattle San Diego Chicago Toronto Boston

Chemist 71,090 73,510 73,991 74,123 75,631 79,321

T3 / PAYROLL CALCULATION ($)Province of Québec, 2011

T2 / AVERAGE ANNUAL BASE SALARIES (US$) – EIGHT REPRESENTATIVE OCCUPATIONS Sample of 6 large North American Metropolitan Areas, January 1, 2011

Note: Exchange rate: CA$1 = US$1

Notes: (1) According to the Act respecting labour standards, vacation pay must be at least 4% of gross wages (2) Statutory holidays (+/- 10 days, or 4% of gross wages) are included in gross salary

2 Please see Appendix C for a defi nition of the various costs

LABOUR C3.2/ Enterprises stand to benefi t from

Greater Montréal’s competitive salastructure to lower their labour co

/ When compared to large US citsuch as Boston, Chicago, PhoSan Diego, Seattle and Toronsalaries for some high-levtions range from 3% to 1Greater Montréal

/ This advantage is ecant for high techfor whom laboursingle largest c

/ According toMontréal rAmerica’in termcostsstatTh

22 / Montréal International

FACILITIES COSTS3.3/ Offi ce and industrial space is

available at extremely competitive rates throughout Greater Montréal. This is true in the downtown core as well as adjacent locations on the North and South Shores of the St. Lawrence River

/ In 2010, Cushman & Wakefi eld (2011) assessed these costs at approximately US$19 sq ft/year for a Class A building in Greater Montréal’s core business district. This compared to an average US$43.20 sq ft/year in the 11 other large North American metropolitan areas included in the survey

/ According to Cushman & Wakefi eld (2011), leasing costs for industrial space was US$4.90 sq ft/year in Greater Montréal as compared to US$7.00 sq ft/year in the 12 other large North American metros included in the study.

C9 / AVERAGE INDUSTRIAL RENTAL RATE (US$/SQ FT/YEAR)13 Largest North American Metropolitan Areas, 2010

Notes: (1) Los Angeles County (2) Silicon Valley/San Jose

The US average corresponds to the gross rental rate. The exchange rate used in the survey: CA$1 = US$1.0063 (December 31, 2010)

16

12

8

4

0

Atla

nta

Toro

nto

Mon

tréal

Dal

las

Chi

cago

Hou

ston

Phila

delp

hia

Seat

tleLo

s An

gele

s (1

)

Mia

mi

Den

ver

Bos

ton

San

Fran

cisc

o (2

)

C8 / AVERAGE OFFICE RENTAL RATE (US$/SQ FT/YEAR)12 Largest North American Metropolitan Areas, 2010

80

60

40

20

0

Mon

tréal

Toro

nto

Atla

nta

Phila

delp

hia

Hou

ston

Chi

cago

San

Fran

cisc

oLo

s An

gele

s (1

)

Mia

mi

Bos

ton

New

Yor

k (2

)

Was

hing

ton

Notes: (1) West (2) Downtown

Average rent does not include service charges and local taxes. Except for Los Angeles and New York, the data are for offi ce space located in the central business district. The exchange rate used in the survey: CA$1 = US$1.0063 (December 31, 2010)

Attractiveness Indicators 2011-2012 / 23

“

”

THQ, Video Game Industry Leader, Comes to Montréal

Government support, in the form of reimbursable tax credits and other incentives, enabled Montréal to stand out as offering the best combination of creative talent and favourable economic conditions among the cities that we considered for our new studio.

Mr. Dave GatchelGeneral ManagerTHQ Montréal

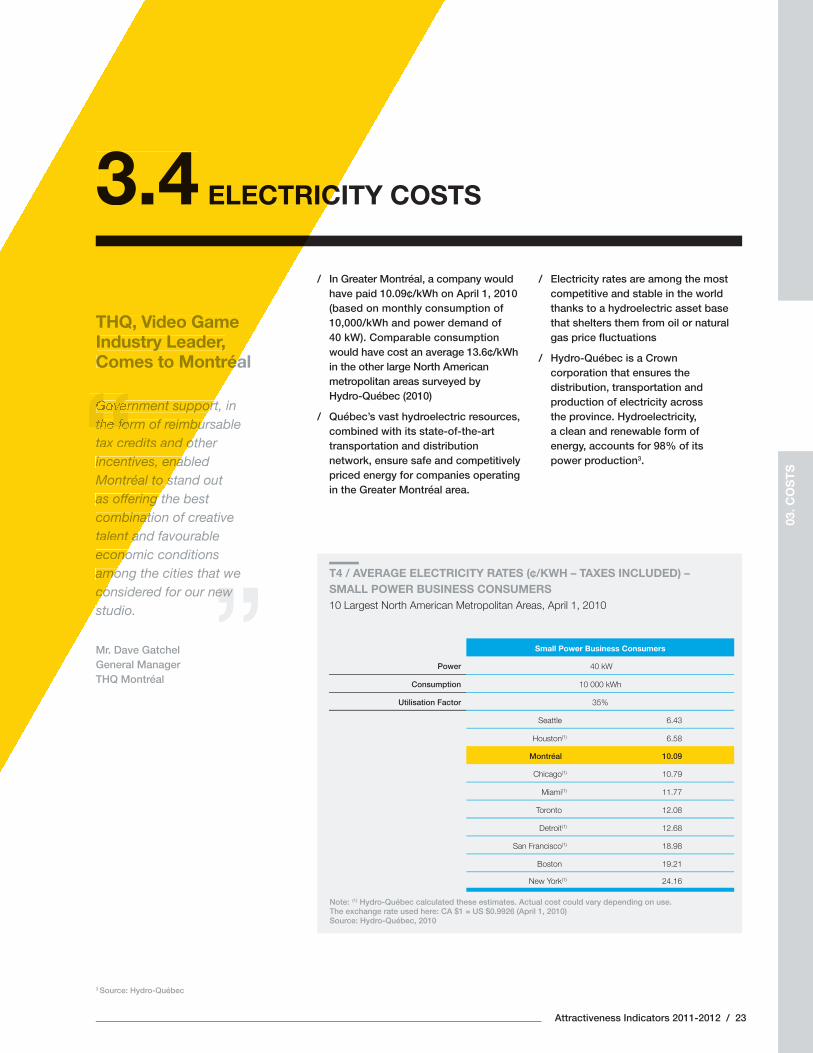

ELECTRICITY COSTS3.4/ In Greater Montréal, a company would

have paid 10.09¢/kWh on April 1, 2010 (based on monthly consumption of 10,000/kWh and power demand of 40 kW). Comparable consumption would have cost an average 13.6¢/kWh in the other large North American metropolitan areas surveyed by Hydro-Québec (2010)

/ Québec’s vast hydroelectric resources, combined with its state-of-the-art transportation and distribution network, ensure safe and competitively priced energy for companies operating in the Greater Montréal area.

/ Electricity rates are among the most competitive and stable in the world thanks to a hydroelectric asset base that shelters them from oil or natural gas price fl uctuations

/ Hydro-Québec is a Crown corporation that ensures the distribution, transportation and production of electricity across the province. Hydroelectricity, a clean and renewable form of energy, accounts for 98% of its power production3.

Small Power Business Consumers

Power 40 kW

Consumption 10 000 kWh

Utilisation Factor 35%

Seattle 6.43

Houston(1) 6.58

Montréal 10.09

Chicago(1) 10.79

Miami(1) 11.77

Toronto 12.08

Detroit(1) 12.68

San Francisco(1) 18.98

Boston 19.21

New York(1) 24.16

T4 / AVERAGE ELECTRICITY RATES (¢/KWH – TAXES INCLUDED) – SMALL POWER BUSINESS CONSUMERS10 Largest North American Metropolitan Areas, April 1, 2010

Note: (1) Hydro-Québec calculated these estimates. Actual cost could vary depending on use. The exchange rate used here: CA $1 = US $0.9926 (April 1, 2010)Source: Hydro-Québec, 2010

3 Source: Hydro-Québec

“THQ, Video Game Industry Leader,Comes to Montréa

rnment suppor

““the form of reimbu““tax credits and oincentives, enaMontréal to sas offering combinattalent aneconoamoco

ELECTRIC3.4

03. C

OS

TS

24 / Montréal International

TAXES AND INCENTIVES A TAX BURDEN AMONG

THE MOST COMPETITIVE

IN NORTH AMERICA

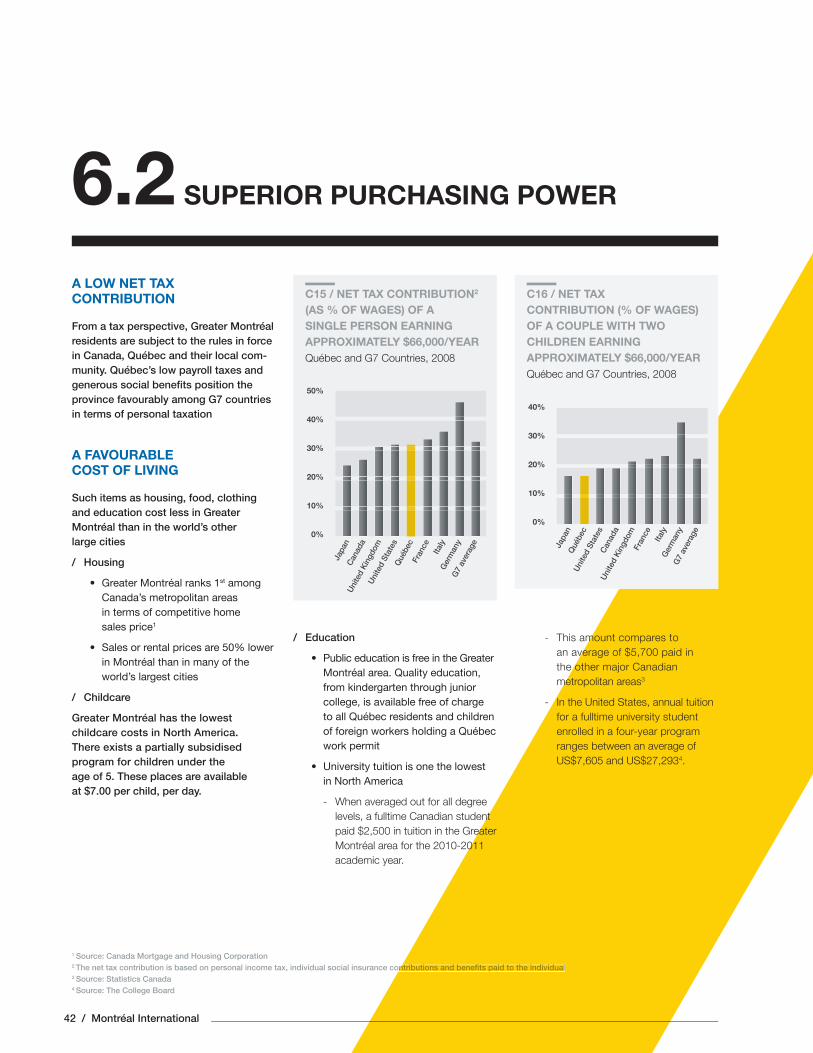

04/ The region’s tax burden for R&D

companies is the most favourable among large international metropolitan areas due in large part to generous R&D tax credits offered by the governments of Canada and Québec

/ The lowering of the federal corporate income tax rate from 22% to 15% by 2012 means that Canada will enjoy the most competitive corporate revenue taxation rate among the G7 countries

/ An important array of targeted and highly competitive government-backed incentives provide technology companies with stable support.

Do

wnt

ow

n, M

ont

réal

Attractiveness Indicators 2011-2012 / 25

“”

Danone Expands Its Boucherville Facility

Montréal International’s involvement greatly contributed to bringing the DanActive project to fruition in the Montréal area. Their support helped us obtain the fi nancial aid needed to ensure the implementation of our investment project.

Mr. Louis FrenettePresident and CEODanone Canada

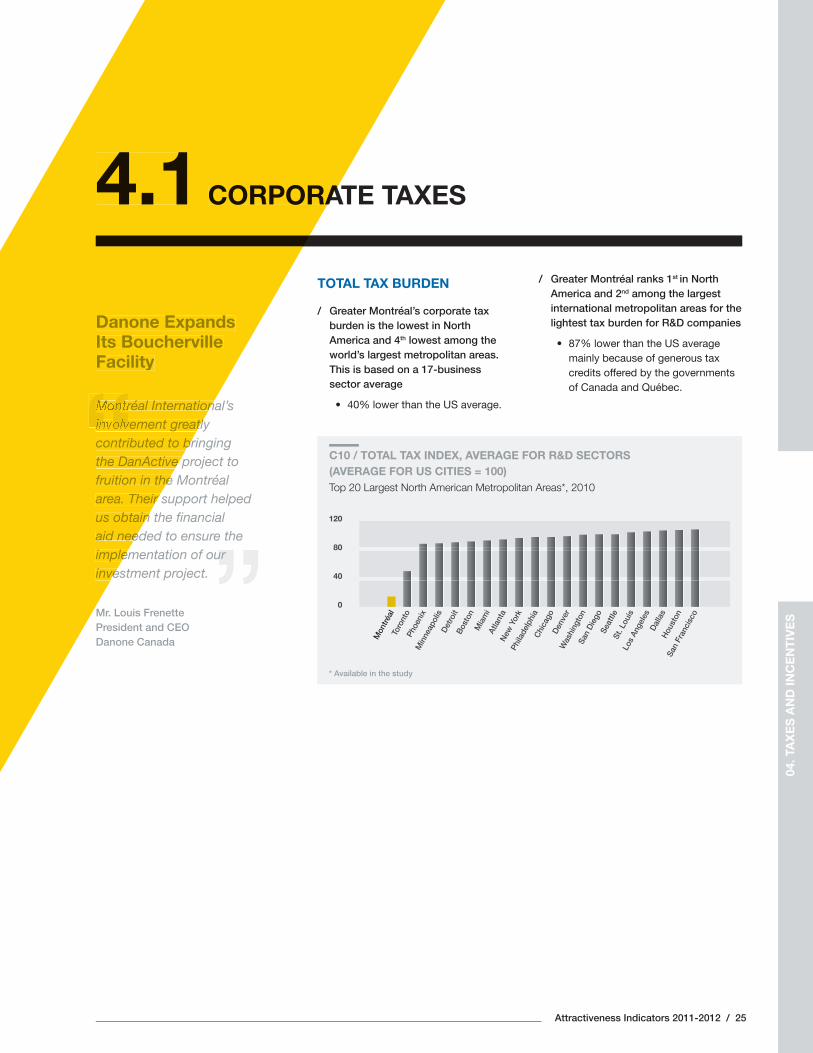

CORPORATE TAXES4.1

04. T

AX

ES

AN

D IN

CE

NT

IVE

S

C10 / TOTAL TAX INDEX, AVERAGE FOR R&D SECTORS (AVERAGE FOR US CITIES = 100)Top 20 Largest North American Metropolitan Areas*, 2010

120

80

40

0

Mon

tréal

Toro

nto

Phoe

nix

Min

neap

olis

Det

roit

Bos

ton

Mia

mi

Atla

nta

New

Yor

kPh

ilade

lphi

a C

hica

goD

enve

rW

ashi

ngto

nSa

n D

iego

Seat

tleSt

. Lou

isLo

s An

gele

sD

alla

sH

oust

onSa

n Fr

anci

sco

“Danone ExpandsIts BouchervilleFacility

réal Internation

““involvement greatly““contributed to brthe DanActive pfruition in thearea. Their us obtainaid needimpleminve

CORPORA4.1TOTAL TAX BURDEN

/ Greater Montréal’s corporate tax burden is the lowest in North America and 4th lowest among the world’s largest metropolitan areas. This is based on a 17-business sector average

• 40% lower than the US average.

/ Greater Montréal ranks 1st in North America and 2nd among the largest international metropolitan areas for the lightest tax burden for R&D companies

• 87% lower than the US average mainly because of generous tax credits offered by the governments of Canada and Québec.

* Available in the study

26 / Montréal International

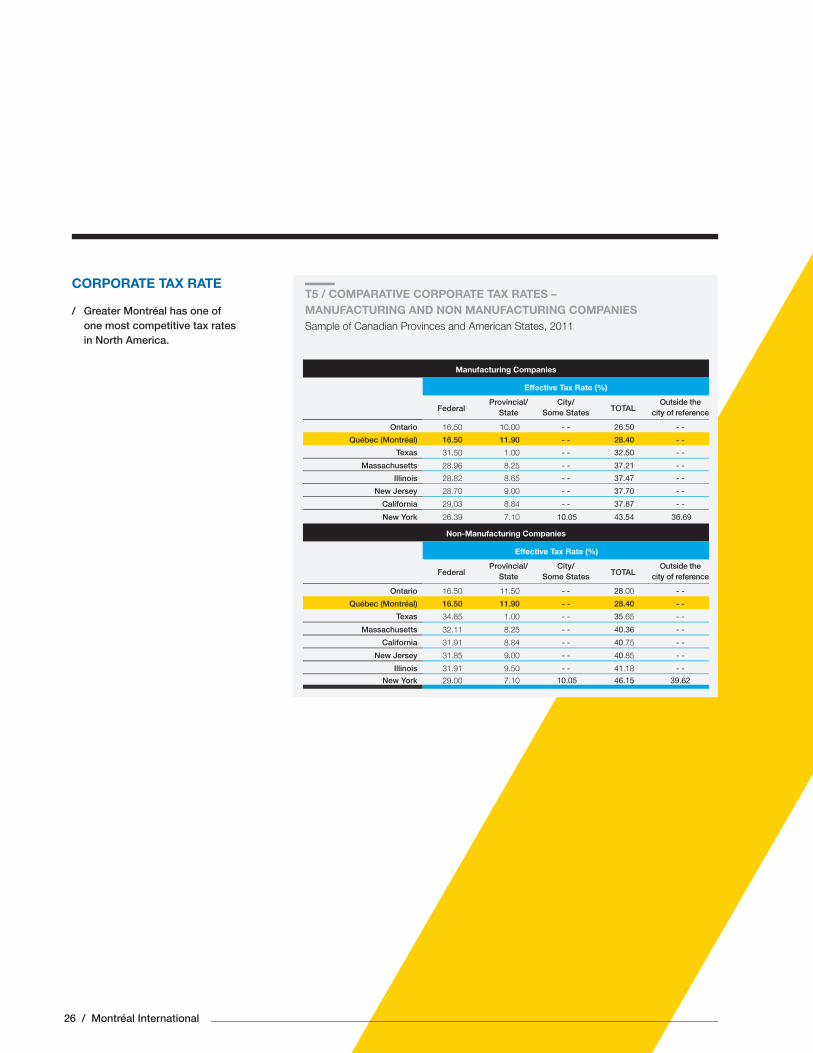

T5 / COMPARATIVE CORPORATE TAX RATES – MANUFACTURING AND NON MANUFACTURING COMPANIES Sample of Canadian Provinces and American States, 2011

Manufacturing Companies

Effective Tax Rate (%)

FederalProvincial/

State City/

Some States TOTALOutside the

city of reference

Ontario 16.50 10.00 - - 26.50 - -

Québec (Montréal) 16.50 11.90 - - 28.40 - -

Texas 31.50 1.00 - - 32.50 - -

Massachusetts 28.96 8.25 - - 37.21 - -

Illinois 28.82 8.65 - - 37.47 - -

New Jersey 28.70 9.00 - - 37.70 - -

California 29.03 8.84 - - 37.87 - -

New York 26.39 7.10 10.05 43.54 36.69

Non-Manufacturing Companies

Effective Tax Rate (%)

FederalProvincial/

State City/

Some States TOTALOutside the

city of reference

Ontario 16.50 11.50 - - 28.00 - -

Québec (Montréal) 16.50 11.90 - - 28.40 - -

Texas 34.65 1.00 - - 35.65 - -

Massachusetts 32.11 8.25 - - 40.36 - -

California 31.91 8.84 - - 40.75 - -

New Jersey 31.85 9.00 - - 40.85 - -

Illinois 31.91 9.50 - - 41.18 - -

New York 29.00 7.10 10.05 46.15 39.62

CORPORATE TAX RATE

/ Greater Montréal has one of one most competitive tax rates in North America.

RESEARCH/INNOVATION/HIGH TECHNOLOGY

R&D Tax Credit

/ The governments of Canada and Québec have been offering R&D tax credits since the mid-1980s

/ The Government of Canada currently offers a 20% tax credit and the Government of Québec a 17.5% refundable tax credit

/ Together, these two measures lower R&D-related taxes by more than 50%

RESEARCH/INNOVATION/HIGH TECHNOLOGY

R&D Tax Credit

/ The governments of CanadaQuébec have been offeringtax credits since the mid

/ The Government of Cacurrently offers a 20%and the Governmea 17.5% refundab

/ Together, theselower R&D-rethan 50%

Attractiveness Indicators 2011-2012 / 27

MAIN CORPORATE FINANCIAL AND TAX INCENTIVES14.2

Assumption:• Private, foreign-controlled company• 20 eligible employees @ $50,000/year• 100% of employee work related to eligible activities• Subcontractor: $200,000• Equipment: $150,000

Federal Québec Total

Wages 1,000,000 1,000,000

Prescribed proxy amount @ 65%

650,000

Subcontractors(1) 200,000 100,000

Equipment 150,000

Québec SR&ED tax credit(2) -192,500

1,807,500 1,100,000

Federal tax credit @ 20% and Québec tax credit @ 17.5%

361,500 192,500 554,000

T6 / EXAMPLE ($): SCIENTIFIC RESEARCH AND EXPERIMENTAL DEVELOPMENT (SR&ED) TAX INCENTIVE PROGRAM, 2011

Notes: (1) Only 50% of the amount paid to a subcontractor is eligible for the Québec tax credit. In Québec, only R&D-related wages are considered eligible for the R&D tax credit; expenditures for materials, equipment and overhead are not covered

(2) In calculating the combined credit, the federal tax credit is reduced by the provincial tax credit receivable

1 Sources: the City of Montréal, Deloitte, Emploi-Québec, Industrial Technologies Offi ce, International Financial Centre Montréal, Investissement Québec, Ministère du Développement économique, de l’Innovation, de l’Exportation du Québec, Montréal International, National Research Council Canada, Québec Film and Television Council, Raymond Chabot Grant Thornton

04. T

AX

ES

AN

D IN

CE

NT

IVE

S

Nat

iona

l Res

earc

h C

oun

cil C

anad

a (N

RC

)

Bel

l Can

ada

28 / Montréal International

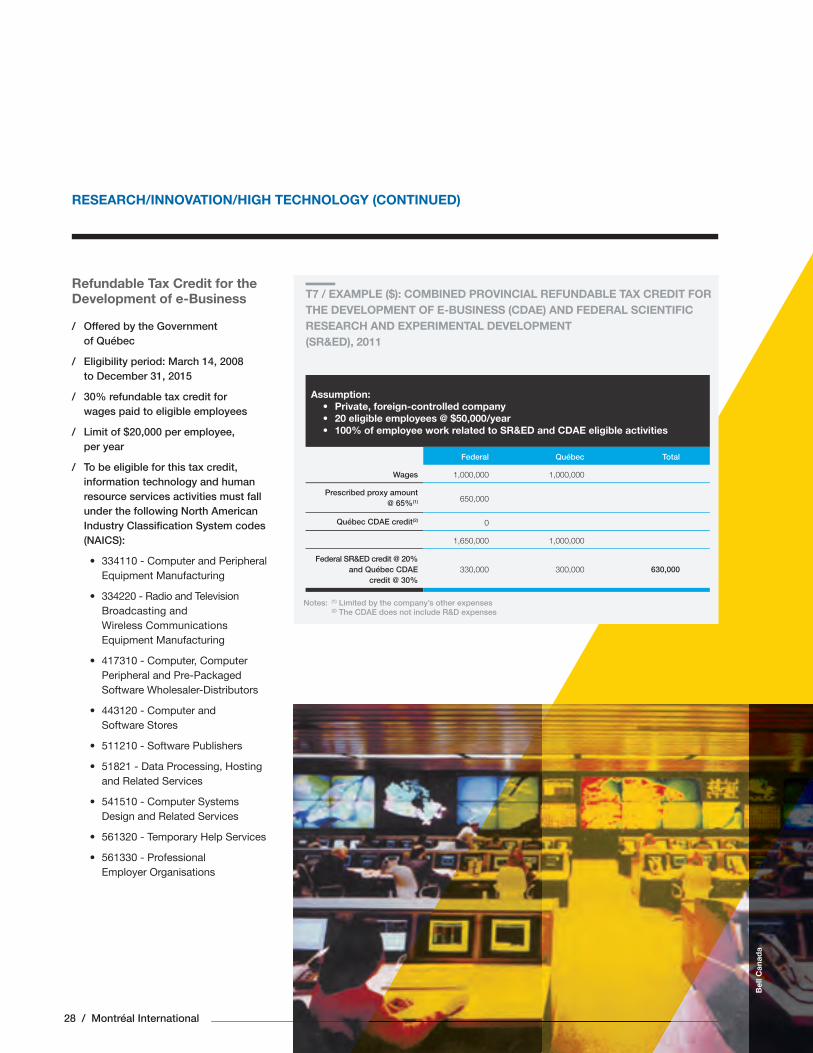

Refundable Tax Credit for the Development of e-Business

/ Offered by the Government of Québec

/ Eligibility period: March 14, 2008 to December 31, 2015

/ 30% refundable tax credit for wages paid to eligible employees

/ Limit of $20,000 per employee, per year

/ To be eligible for this tax credit, information technology and human resource services activities must fall under the following North American Industry Classifi cation System codes (NAICS):

• 334110 - Computer and Peripheral Equipment Manufacturing

• 334220 - Radio and Television Broadcasting and Wireless Communications Equipment Manufacturing

• 417310 - Computer, Computer Peripheral and Pre-Packaged Software Wholesaler-Distributors

• 443120 - Computer and Software Stores

• 511210 - Software Publishers

• 51821 - Data Processing, Hosting and Related Services

• 541510 - Computer Systems Design and Related Services

• 561320 - Temporary Help Services

• 561330 - Professional Employer Organisations

T7 / EXAMPLE ($): COMBINED PROVINCIAL REFUNDABLE TAX CREDIT FOR THE DEVELOPMENT OF E-BUSINESS (CDAE) AND FEDERAL SCIENTIFIC RESEARCH AND EXPERIMENTAL DEVELOPMENT (SR&ED), 2011

Notes: (1) Limited by the company’s other expenses (2) The CDAE does not include R&D expenses

Assumption:• Private, foreign-controlled company• 20 eligible employees @ $50,000/year• 100% of employee work related to SR&ED and CDAE eligible activities

Federal Québec Total

Wages 1,000,000 1,000,000

Prescribed proxy amount @ 65%(1) 650,000

Québec CDAE credit(2) 0

1,650,000 1,000,000

Federal SR&ED credit @ 20% and Québec CDAE

credit @ 30%330,000 300,000 630,000

RESEARCH/INNOVATION/HIGH TECHNOLOGY (CONTINUED)

Attractiveness Indicators 2011-2012 / 29

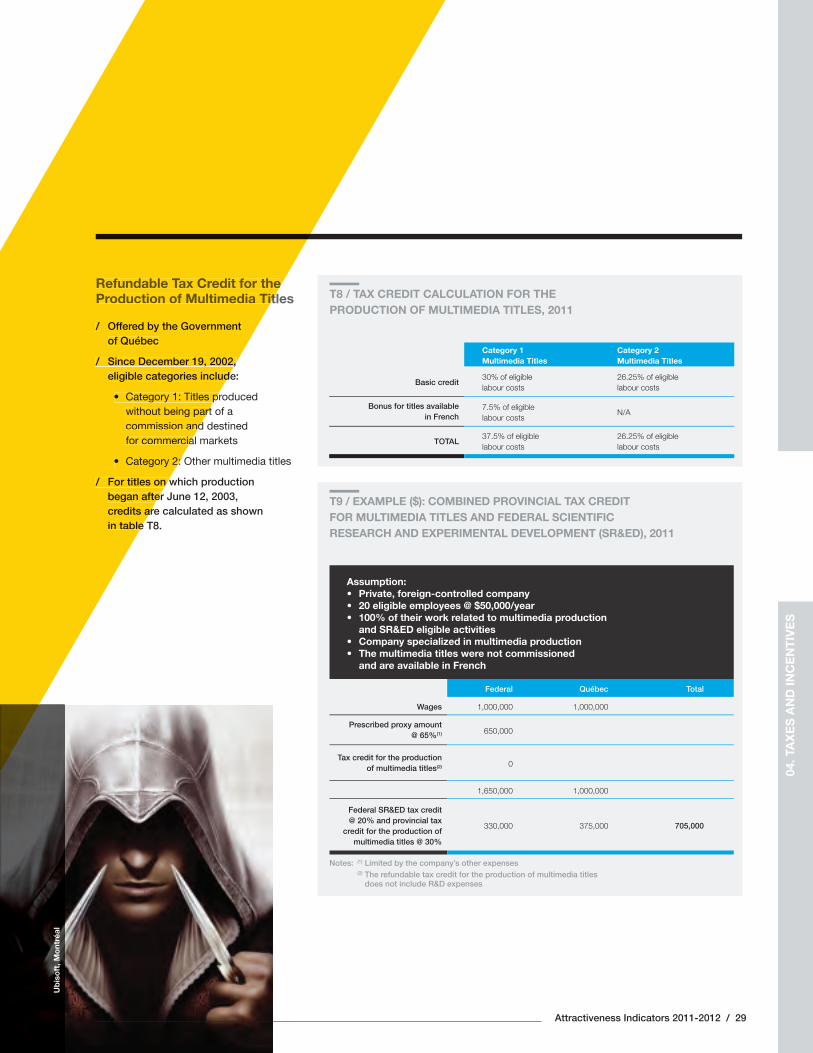

Refundable Tax Credit for the Production of Multimedia Titles

/ Offered by the Government of Québec

/ Since December 19, 2002, eligible categories include:

• Category 1: Titles produced without being part of a commission and destined for commercial markets

• Category 2: Other multimedia titles

/ For titles on which production began after June 12, 2003, credits are calculated as shown in table T8.

T8 / TAX CREDIT CALCULATION FOR THE PRODUCTION OF MULTIMEDIA TITLES, 2011

T9 / EXAMPLE ($): COMBINED PROVINCIAL TAX CREDIT FOR MULTIMEDIA TITLES AND FEDERAL SCIENTIFIC RESEARCH AND EXPERIMENTAL DEVELOPMENT (SR&ED), 2011

Category 1 Multimedia Titles

Category 2 Multimedia Titles

Basic credit30% of eligible labour costs

26.25% of eligible labour costs

Bonus for titles available in French

7.5% of eligible labour costs

N/A

TOTAL37.5% of eligible labour costs

26.25% of eligible labour costs

Notes: (1) Limited by the company’s other expenses (2) The refundable tax credit for the production of multimedia titles

does not include R&D expenses

Assumption:• Private, foreign-controlled company• 20 eligible employees @ $50,000/year• 100% of their work related to multimedia production and SR&ED eligible activities • Company specialized in multimedia production• The multimedia titles were not commissioned and are available in French

Federal Québec Total

Wages 1,000,000 1,000,000

Prescribed proxy amount @ 65%(1) 650,000

Tax credit for the production of multimedia titles(2) 0

1,650,000 1,000,000

Federal SR&ED tax credit @ 20% and provincial tax

credit for the production of multimedia titles @ 30%

330,000 375,000 705,000

Ub

iso

ft, M

ont

réal

Refundable Tax Credit for theProduction of Multimedia Tit

/ Offered by the Government of Québec

/ Since December 19, 2002,eligible categories include

• Category 1: Titles pwithout being partcommission andfor commercia

• Category 2:

/ For titles on wbegan aftercredits arin table

04. T

AX

ES

AN

D IN

CE

NT

IVE

S

30 / Montréal International

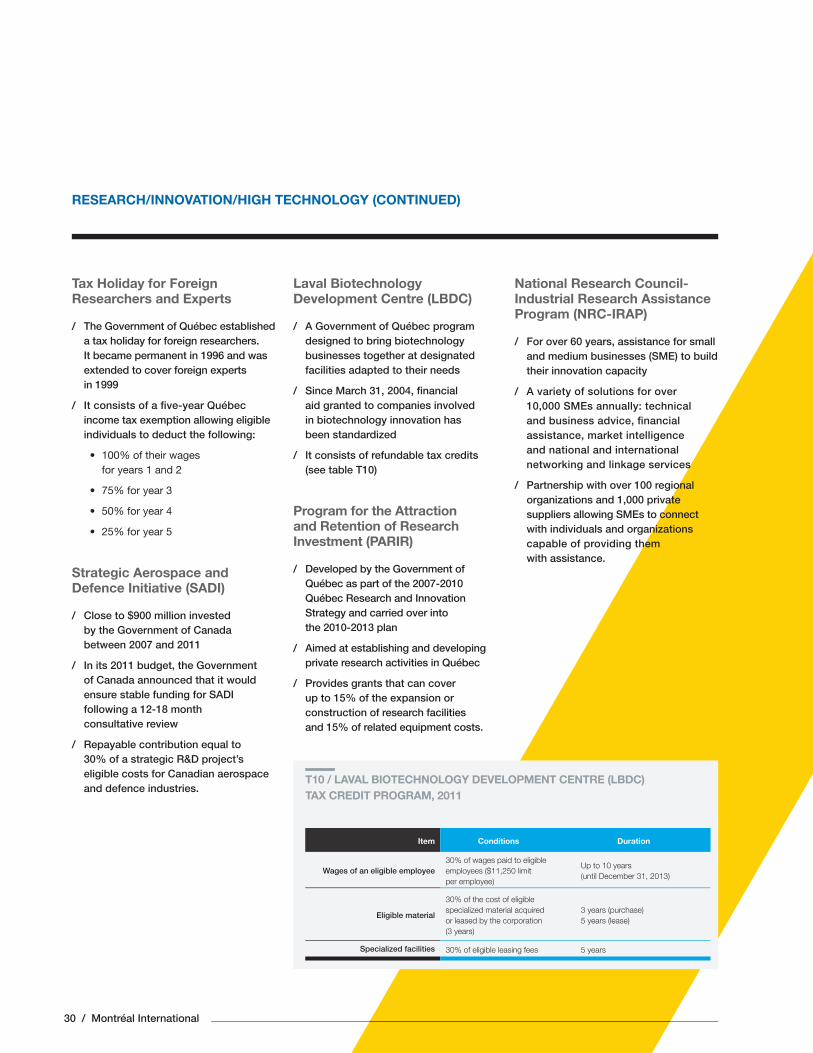

Tax Holiday for Foreign Researchers and Experts

/ The Government of Québec established a tax holiday for foreign researchers. It became permanent in 1996 and was extended to cover foreign experts in 1999

/ It consists of a fi ve-year Québec income tax exemption allowing eligible individuals to deduct the following:

• 100% of their wages for years 1 and 2

• 75% for year 3

• 50% for year 4

• 25% for year 5

Strategic Aerospace and Defence Initiative (SADI)

/ Close to $900 million invested by the Government of Canada between 2007 and 2011

/ In its 2011 budget, the Government of Canada announced that it would ensure stable funding for SADI following a 12-18 month consultative review

/ Repayable contribution equal to 30% of a strategic R&D project’s eligible costs for Canadian aerospace and defence industries.

Laval Biotechnology Development Centre (LBDC)

/ A Government of Québec program designed to bring biotechnology businesses together at designated facilities adapted to their needs

/ Since March 31, 2004, fi nancial aid granted to companies involved in biotechnology innovation has been standardized

/ It consists of refundable tax credits (see table T10)

Program for the Attraction and Retention of Research Investment (PARIR)

/ Developed by the Government of Québec as part of the 2007-2010 Québec Research and Innovation Strategy and carried over into the 2010-2013 plan

/ Aimed at establishing and developing private research activities in Québec

/ Provides grants that can cover up to 15% of the expansion or construction of research facilities and 15% of related equipment costs.

National Research Council-Industrial Research Assistance Program (NRC-IRAP)

/ For over 60 years, assistance for small and medium businesses (SME) to build their innovation capacity

/ A variety of solutions for over 10,000 SMEs annually: technical and business advice, fi nancial assistance, market intelligence and national and international networking and linkage services

/ Partnership with over 100 regional organizations and 1,000 private suppliers allowing SMEs to connect with individuals and organizations capable of providing them with assistance.

T10 / LAVAL BIOTECHNOLOGY DEVELOPMENT CENTRE (LBDC) TAX CREDIT PROGRAM, 2011

Item Conditions Duration

Wages of an eligible employee30% of wages paid to eligible employees ($11,250 limit per employee)

Up to 10 years (until December 31, 2013)

Eligible material

30% of the cost of eligible specialized material acquired or leased by the corporation (3 years)

3 years (purchase) 5 years (lease)

Specialized facilities 30% of eligible leasing fees 5 years

RESEARCH/INNOVATION/HIGH TECHNOLOGY (CONTINUED)

Attractiveness Indicators 2011-2012 / 31

INVESTMENT

Strategic Support for Investment (PASI)

/ A program created by the Government of Québec in 2004

/ Assistance in the form of interest-free loans, equity-type loans, loans with interest repayable through royalties, contributions repayable through royalties or loans guarantee – a non-repayable contribution is also a possibility

/ Two types of eligible projects:

• Investments

• Development of unique products

/ Some targeted sectors: manufactur-ing, software publishing, call centres and waste recovery and processing

/ A loan guarantee can cover up to 70% of an investment’s net loss.

/ The minimum amount required is $5 million for investments and $2 million for product development projects; the Government of Québec’s Economic Project Support Program (PSPE) remains an attractive option for projects worth less these amounts

/ Government fi nancial assistance shall not exceed 50% of a project’s total cost

/ Duration of fi nancial support shall not to exceed 10 years.

T11 / TERMS OF REFERENCE FOR THE TAX HOLIDAY FOR THE COMMERCIALIZATION OF INTELLECTUAL PROPERTY, 2009

Exemption - 100% on corporate income

Duration - First ten years following incorporation

Eligible corporations- Established in Québec - Incorporated in Canada - Must derive at least 90% of income from commercialization activities

Eligible activities- The making of goods whose value stems from intellectual property- The selling of goods whose value stems from intellectual property

Eligible intellectual property- Intellectual property developed in Québec universities

and public research centres

Tax Holiday for the Commercialisation of Intellectual Property

/ Applicable to new eligible corporations dedicated to the commercialization of intellectual property developed in Québec universities and public research centres

/ To be eligible, a company must have been (or be) incorporated in Canada between March 19, 2009 and April 1, 2014 and have started to carry on an eligible commercial ization business within 12 months of its incorporation

WORKFORCE

Financial Assistance for Job Creation and Training

/ Since 1998, Government of Québec technical and fi nancial assistance has been available to help businesses meet their need for new talent

/ This assistance can consist of:

• Up to 25% of eligible costs for the implementation of a training program

• Up to 50% of costs incurred for the creation of a human resource department

/ A special fund exists for job-creation “major economic initiatives”. To be eligible for and benefi t from, among other things, the above mentioned contributions, a company must:

• Submit a project that will have a signifi cant impact on regional employment or one that comes on the heels of a major investment, or

• Create 50 new full-time, lasting jobs over a 24-month period.

04. T

AX

ES

AN

D IN

CE

NT

IVE

S

32 / Montréal International

REAL ESTATE

PR@M-Industry

/ A program created in 2008; its eligibility period ends on December 31, 2012

/ The City of Montréal offers owners of non-residential buildings a fi ve-year general property tax rebate on the increase in property value resulting from the construction, conversion or expansion of an industrial building

/ How it works:

• A subsidy paid over a period of fi ve years as follows: 100% - 100% - 100% - 80% - 80%

• An annual subsidy ceiling of $1 million

• A three-year deadline for project completion after the eligibility date

• Eligible activities include: manufac-turing (in general); fi lm and video production; information system design; packaged software design; call centres; head offi ces (and related activities); physical science, engineering and life science R&D; architecture, engineering, specialized design and environmental consulting services; the performing arts and theatre and museum operation.

FINANCE

Refundable Tax Credits for Inter national Finance Centres (IFC)

/ Created in 1986 by the Government of Québec and amended in its 2010-2011 budget

/ Provides an annual refundable tax credit of 30% on wages paid to eligible employees

/ An IFC must have at least six employees

/ Employees must work full-time for the IFC and 75% of their duties must be devoted to carrying out qualifi ed inter-national fi nancial transactions (QIFT)

/ A refundable tax credit is allowed up to a maximum of $20,000 per employee, per year

/ Foreign specialists employed by an eligible corporation operating an IFC can claim a deduction on their Québec income tax for a period of fi ve years – the annual deduction is: 100% for years one and two, and 75%, 50% and 37.5% for years three, four and fi ve, respectively.

FILM

Tax Credit for Film Production Services

/ Tax credits available for this sector from both Canada and Québec since 1998

/ A Government of Québec 25% refund-able tax credit and a Government of Canada 16% tax credit2

/ At the provincial level, it currently applies to all eligible production costs incurred within the province (all-spend concept)

/ At the federal level, it applies to eligible labour costs

/ Québec adds a 20% tax credit enhancement for digital special effects (VFX) and computer animation (on extended eligible labour3) – fi lming in front of a green screen is included in the credit enhancement

/ Total tax credits for production services can amount to 44%.

2 In calculating the combined credit, the federal tax credit is reduced by the provincial tax credit receivable3 Foreign workers hired by a Québec company can be eligible for the assistance program4 Source: Invest in Canada

nce

es

ax creditgital special

omputer animation gible labour3) –

of a green screen is e credit enhancement

edits for production can amount to 44%.

x credit receivablem

DID YOU KNOW?Canada is known4

/ For its sound banking system 1st among 139 countries

(The World Economic Forum, 2010)

/ For its ranking on the Access to Capital Index

1st among 122 countries (The Milken Institute, 2010)

INNOVATIONGREATER MONTRÉAL –

A UNIQUE BLEND OF

CREATIVITY, DIVERSITY

AND HIGH TECHNOLOGY

05/ Constant interplay between

techno logy, science, art and culture explains the success, among other things, of Montréal’s high technology clusters, video game industry and creative enterprises such as the Cirque du Soleil

/ An industrial economy built on high technology clusters such as aerospace, information and communications technologies (ICT), life science and health technologies (LSHT), and cleantech

/ A critical mass of workers in higher knowledge sectors (1 out of 10 jobs)

/ A network of universities with the largest share of research funding in Canada and a broad range of expertise in hundreds of research centres

/ Effective intellectual property protection backed by international treaties.

Can

adia

n S

pac

e A

gen

cy

34 / Montréal International

SOLID HIGH TECHNOLOGY CLUSTERS5.1AEROSPACE

/ Over 40,000 jobs in 230 companies

/ Over $11 billion in annual sales

/ Nearly 70% of all research and development expenditures in Canada

/ Main leaders: Air Canada, Bell Helicopter Textron, Bombardier Aerospace, CAE, Esterline CMC Electronics, General Electric, Goodrich, Héroux-Devtek, Honeywell, L-3 Communications MAS, MDA Space, Messier-Dowty, Pratt & Whitney Canada, Rolls-Royce Canada, Sonaca Montréal, Thales Canada and Turbomeca Canada

/ Cluster secretariat: Aéro Montréalwww.aeromontreal.ca

CLEANTECH

/ Over 400 innovative companies in Québec in energy (34%), water (16%), waste (16%), air (13%), land (13%) and other (10%) technologies

/ Some 200 research organizations and university chairs

/ Over $220 million in research invest-ment between 2000 and 2007

/ Cluster secretariat: Écotech Québec www.ecotechquebec.com

LIFE SCIENCE AND HEALTH TECHNOLOGIES (LSHT)

/ Over 43,000 jobs in 620 organizations, including 150 research centres

/ Nearly half of Canada’s biopharmaceu-tical industry and most of its basic and clinical research are concentrated in Québec and the Greater Montréal area

/ The Canadian headquarters of some 20 multinational pharmaceutical companies are located in Montréal

/ Main leaders: Algorithme Pharma, AstraZeneca, Boehringer Ingelheim, Bristol-Myers Squibb, GlaxoSmith-Kline, Johnson & Johnson, Merck, Novartis, Pfi zer, Pharmanet, Sanofi and Theratechnologies

/ Cluster secretariat: Montréal InVivo www.montreal-invivo.com

INFORMATION AND COMMUNICATIONS TECHNOLOGIES (ICT)

/ Nearly 120,000 jobs in some 5,000 companies

/ A critical mass of enterprises in fi ve major sectors: computer services, entertainment, interactive and digital content, manufacturing, software and telecommunications and wireless technologies

/ Because of the spectacular growth of the video games industry, the interactive and digital content and entertainment segment expe-rienced the greatest expansion of any ICT sector

/ Main leaders: Accenture, Autodesk, Bell Canada, Compuware, Dassault Systems, DMR/Fujitsu, Eidos, Electronic Arts, Ericsson, Funcom, CGI, GFI, IBM, Morgan Stanley, Positron, SAP, Telus, THQ, Ubisoft, Videotron, and Warner Bros. Interactive Entertainment

/ Cluster secretariat: TechnoMontréal www.technomontreal.com

ustry,ntent

t expe-nsion of

ure, Autodesk, uware, Dassault

ujitsu, Eidos,Ericsson, Funcom,

, Morgan Stanley, P, Telus, THQ, Ubisoft,

and Warner Bros. ve Entertainment

r secretariat: TechnoMontréal w.technomontreal.com

“”

Attractiveness Indicators 2011-2012 / 35

05. I

NN

OVA

TIO

N

A CRITICAL MASS OF HIGH TECHNOLOGY TALENT5.2

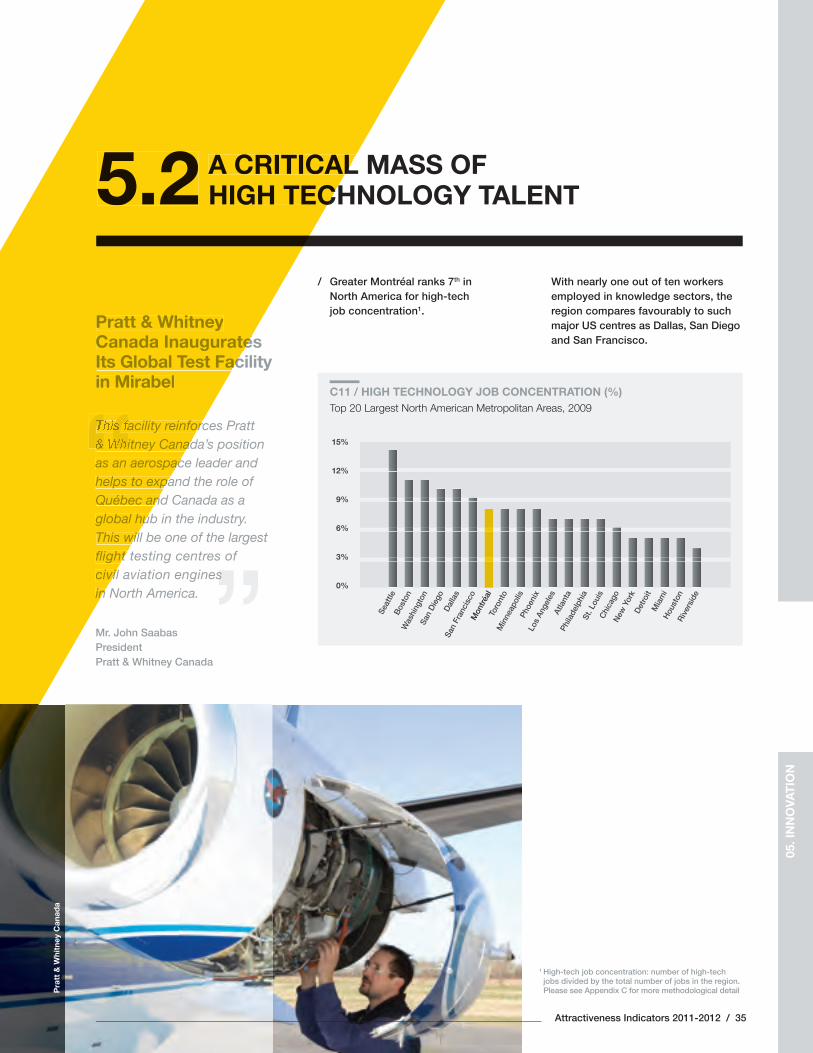

/ Greater Montréal ranks 7th in North America for high-tech job concentration1.

With nearly one out of ten workers employed in knowledge sectors, the region compares favourably to such major US centres as Dallas, San Diego and San Francisco.

1 High-tech job concentration: number of high-tech jobs divided by the total number of jobs in the region. Please see Appendix C for more methodological detail

15%

12%

9%

6%

3%

0%

Seat

tleB

osto

nW

ashi

ngto

nSa

n D

iego

Dal

las

San

Fran

cisc

oM

ontré

alTo

ront

oM

inne

apol

isPh

oeni

xLo

s An

gele

sAt

lant

aPh

ilade

lphi

aSt

. Lou

isC

hica

goN

ew Y

ork

Det

roit

Mia

mi

Hou

ston

Riv

ersi

de

C11 / HIGH TECHNOLOGY JOB CONCENTRATION (%) Top 20 Largest North American Metropolitan Areas, 2009

Pratt & Whitney Canada Inaugurates Its Global Test Facilityin Mirabel

This facility reinforces Pratt & Whitney Canada’s position as an aerospace leader and helps to expand the role of Québec and Canada as a global hub in the industry. This will be one of the largest fl ight testing centres of civil aviation engines in North America.

Mr. John SaabasPresidentPratt & Whitney Canada

“

A CRITICALHIGH TECH5.2

Pratt & Whitney Canada InaugurateIts Global Test Facin Mirabel

facility reinforc

““& Whitney Canad““as an aerospachelps to expaQuébec anglobal huThis wilfl ight civilin

Pra

tt &

Whi

tney

Can

ada

La v

itri

ne,

Mo

ntré

al

36 / Montréal International

MAJOR FOREIGN INVESTMENT IN HIGH TECHNOLOGY5.3

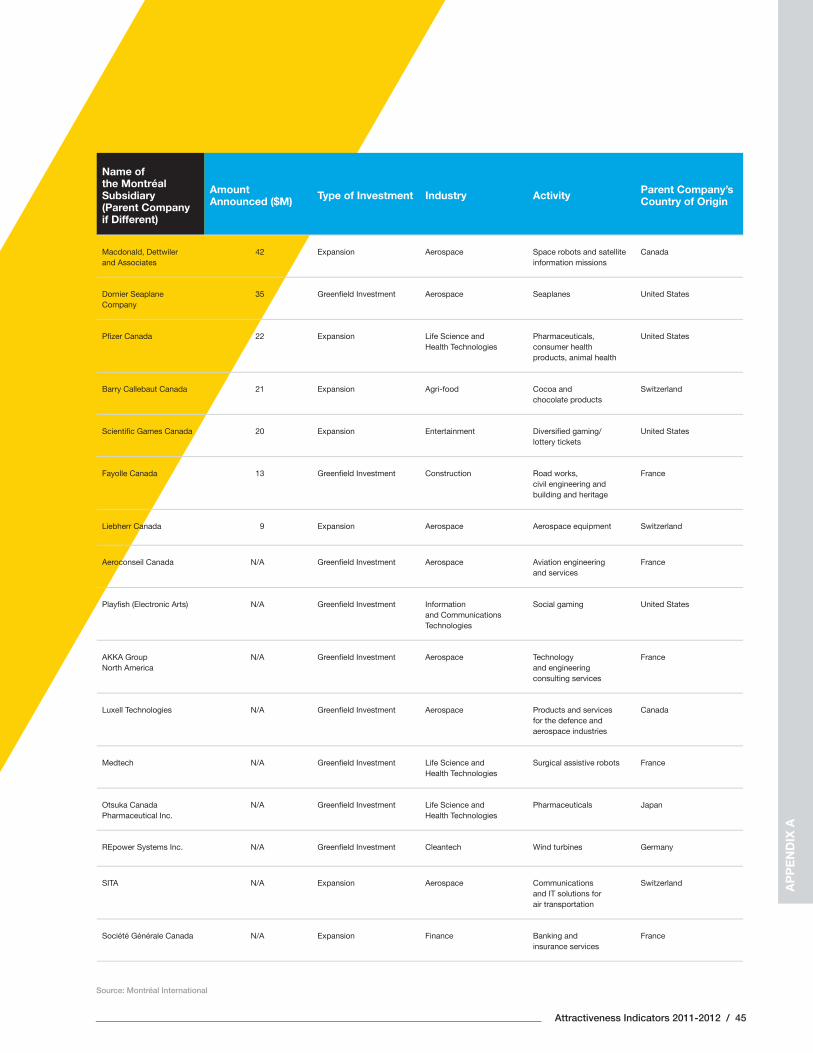

2 Please see Appendix A for a partial list of private sector investments announced in 2010-2011 for Greater Montréal

FOREIGN INVESTORS2

/ Montréal International’s (MI) foreign investment data demonstrate the importance of aerospace, Information and communications technologies (ICT) and life science and health tech-nologies (LSHT) in Greater Montréal

/ From 2006 to 2010, MI has helped to attract over $3 billion in foreign investment, 80% of which was in one of the three main high-tech sectors

/ These three areas represent 40% of the 165,000 jobs generated by Greater Montréal’s 1,900 foreign subsidiaries.

ICT ($1,819M - 58%)

OTHER ($726M - 23%)

LSHT ($305M - 10%)

AEROSPACE ($275M - 9%)

C12 / FOREIGN INVESTMENT BY HIGH TECHNOLOGY SECTOR ($M - %) Montréal International Results, 2006-2010

Attractiveness Indicators 2011-2012 / 37

AN IDEAL R&D ENVIRONMENT FOR BUSINESSES5.4 AN IDEAL RFOR BUSIN5.4

Mon

tréal

Toro

nto

Vanc

ouve

rO

ttaw

aC

alga

ry

C13 / UNIVERSITY RESEARCH FUNDING ($M)Top 5 Largest Canadian Metropolitan

Areas, 2005-2009

6,000

5,000

4,000

3,000

2,000

1,000

PRIVATE SECTOR AND UNIVERSITY-BASED RESEARCH

/ According to the Institut de la statistique du Québec, the private sector spends more than $3.5 billion annually on in-house R&D

/ Several well-known multinationals conducting R&D in the area are listed among RE$EARCH Infosource’s Top 100 companies with the largest R&D budgets in Canada in 2009. Included among them are BCE, Bombardier, CAE, Ericsson, GlaxoSmithKline, IBM, Novartis, Pratt &Whitney, Sanofi and Telus

/ Montréal’s main university-based research centres had over $5 billion in research funds at their disposal between 2005 and 2009. This repre-sented nearly 20% of the total for the entire country: a fi rst in Canada.

RESEARCH CENTRES

/ The following lists some of Greater Montréal’s main research centres that work in partnership with the private sector and reinforce its expertise:

• Aerospace: Canadian Space Agency, McGill University’s Aerospace Materials and Alloy Development Centre, NRC Institute for Aerospace Research, Aerospace Technology Manufacturing Centre, Centre techno-logique en aérospatiale du collège Édouard-Montpetit, Consortium for Research and Innovation in Aerospace in Québec (CRIAQ)

• LSHT: University hospital research centres, Montréal Heart Institute (MHI), INRS-Institut Armand-Frappier, Institut de recherches cliniques de Montréal (IRCM), NRC Biotechnology Research Institute (BRI)

• ICT: Centre de recherche informa-tique de Montréal (CRIM), Centre de recherches mathématiques (CRM), Centre for Advanced Systems and Technologies in Communications (SYTACom), INRS-Énergie, Matéri-aux et Télécommunications (INRS-EMT), Microsystems Strategic Alliance of Québec (ReSMiQ).

INTELLECTUAL PROPERTY PROTECTION

/ The Canadian Intellectual Property Offi ce (CIPO) lists several legal measures relating to the creation of intellectual property:

• The Government of Canada grants intellectual property protection up to a maximum of 20 years after the day on which a patent application was fi led

• Several countries, including Canada, have signed the Paris Convention for the Protection of Industrial Property. This treaty recognizes a right of priority, which means that an application fi led in one of the signatory countries shall bear the same fi lling date as the others provided that the applicant submit a request in all of the other countries within 12 months of the initial fi ling date. By virtue of the Paris Convention, a company can fi le an application fi rst in a foreign country, then in Canada

• A patent application can also be fi led in Canada by virtue of the Patent Cooperation Treaty and it shall be valid in any of the 137 member-countries. This pro-cedure is simpler because an applicant need not fi le separately in every country.

05. I

NN

OVA

TIO

N

38 / Montréal International

A THRIVING NORTH AMERICAN VENTURE CAPITAL MARKET 5.5

/ In an economy centred on high technology clusters, access to venture capital is essential for stimulating innovation.

/ Over $5 billion in venture capital was invested in the region between 2000 and 2010. This represented 20% of all Venture Capital funding in Canada. It is worth noting that Greater Montréal’s life sciences sector attracted almost 35% of this money: a fi rst in Canada.

/ Greater Montréal ranked 2nd for the largest amount of investment money among Canadian metropolitan areas in 2010 with a total of $292 million or 26% of the total for the entire country.

3 Source: MONTRÉAL F1RST, 2011

DID YOU KNOW?Greater Montréal is the source of many innovations. Here are 12 compelling examples3:

/ In April 2008, CAE designed and built the fi rst A380 simulator for Airbus, which obtained a D level certifi cation, the highest awarded for fl ight simulators

/ In April 2009, a team at the Université de Montréal’s Institut de recherche en immunologie et en cancérologie (IRIC) succeeded in producing a large quantity of laboratory stem cells from a small number of blood stem cells obtained from bone marrow

/ Genia Photonics has developed a new generation of fi bre-optic based pulsed laser system that offer the capability to switch rapidly between imaging, diagnostic and treatment functions

/ Sensio Technologies led the way in making the 2010 FIFA World Cup available in live 3D in theatres around the world

/ Object Research System (ORS) designed ORS Visual, a software solution that allows the review and analysis of images generated by different medical scanning devices

/ Effenco’s patented Head system can convert new and used trucks into hybrid vehicles and generate a 15% to 25% reduction in fuel consumption per vehicle

/ Longueuil-based D-BOX Techno-logies designs and manufactures leading edge high technology motion systems mainly suited to the needs of the entertainment industry

/ Caprion Proteomics developed CellCarta, a unique proteomic platform for profi ling proteins in solid tissues and plasma and pre-dicting drug treatment effectiveness

/ The City of Montréal’s BIXI is the world’s fi rst self-serve, solar energy powered bicycle system

/ René Roy, professor and researcher in the Department of Chemistry of the Université du Québec à Montréal (UQAM), and his team developed and marketed a synthetic vaccine for meningitis and pneumonia

/ The Montréal company, gsmprjct°, invented an interactive electronic high resolution telescope, Tellscope, which is currently installed on the 124th-fl oor observatory of the world’s tallest building, the Burj Khalifa, in Dubai

/ To decontaminate underground water, Golder Associates installed a reactive barrier in the soil, made up of shafts into which they injected iron powder suspended in a liquid mixture consisting of, among other things, soy milk and food additives.

Attractiveness Indicators 2011-2012 / 39

QUALITY OF LIFE GREATER MONTRÉAL –

A CITY WITH A HUMAN

DIMENSION AND A GREAT

PLACE TO LIVE, WORK

AND ENJOY LIFE

06/ Greater Montréal, a cosmopolitan,

bilingual and international city, with a distinct personality serving as a bridge between North America and Europe

/ An excellent quality/cost ratio providing its workforce with superior purchasing power

/ A cultural, recreational, sports and green city whose talent and technology are recognized around the globe.

St-

Den

is s

tree

t, M

ont

réal

40 / Montréal International

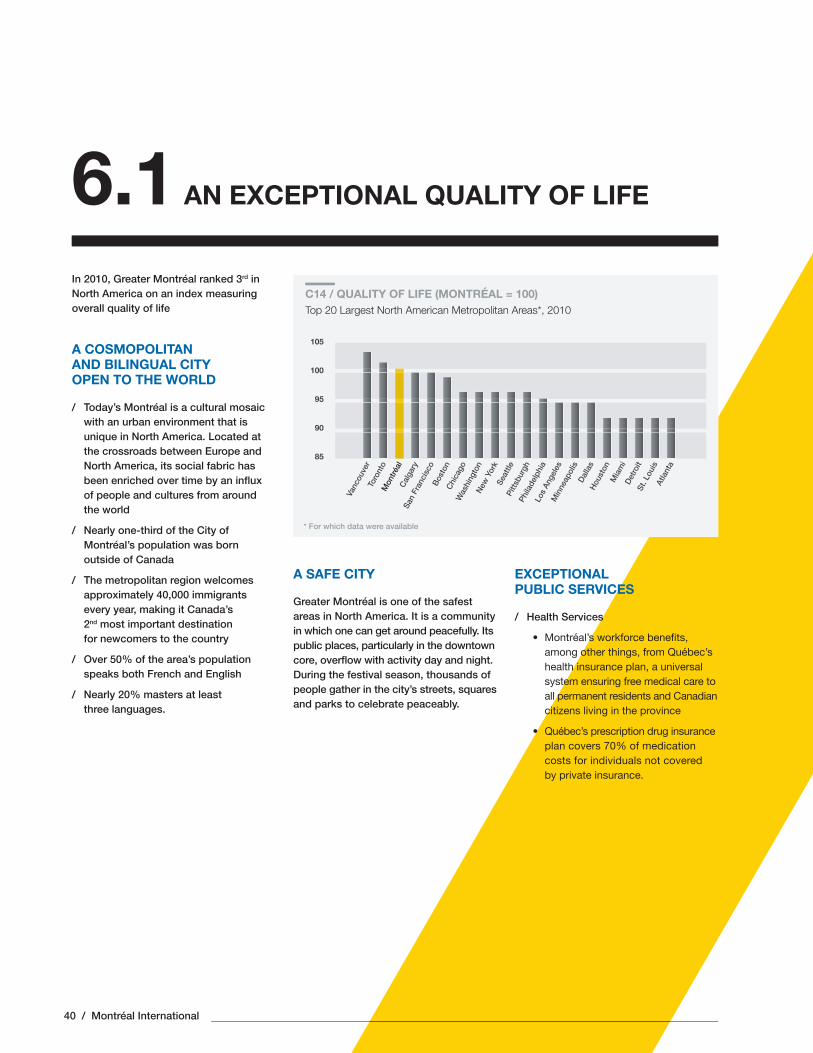

AN EXCEPTIONAL QUALITY OF LIFE6.1In 2010, Greater Montréal ranked 3rd in North America on an index measuring overall quality of life

A COSMOPOLITAN AND BILINGUAL CITY OPEN TO THE WORLD

/ Today’s Montréal is a cultural mosaic with an urban environment that is unique in North America. Located at the crossroads between Europe and North America, its social fabric has been enriched over time by an infl ux of people and cultures from around the world

/ Nearly one-third of the City of Montréal’s population was born outside of Canada

/ The metropolitan region welcomes approximately 40,000 immigrants every year, making it Canada’s 2nd most important destination for newcomers to the country

/ Over 50% of the area’s population speaks both French and English

/ Nearly 20% masters at least three languages.

C14 / QUALITY OF LIFE (MONTRÉAL = 100)Top 20 Largest North American Metropolitan Areas*, 2010

Vanc

ouve

rTo

ront

oM

ontré

alC

alga

rySa

n Fr

anci

sco

Bos

ton

Chi

cago

Was

hing

ton

New

Yor

kSe

attle

Pitts

burg

hPh

ilade

lphi

aLo

s An

gele

sM

inne

apol

isD

alla

sH

oust

onM

iam

iD

etro

itSt

. Lou

isAt

lant

a

* For which data were available

A SAFE CITY