canada research canadian tire corporation - raymond · pdf filecanada research published by...

TRANSCRIPT

Canada Research Published by Raymond James Ltd.

Please read domestic and foreign disclosure/risk information beginning on page 44 and Analyst Certification on page 43. Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Canadian Tire Corporation April 29, 2015 CTC.A-TSX Company Report - Initiation of Coverage Kenric S. Tyghe MBA | 416.777.7188 | [email protected]

Krisztina Katai (Associate) | 416.777.7060 | [email protected]

Consumer & Retail

Switching to Summer Tires and Expecting Better Traction

Recommendation We are initiating coverage of Canadian Tire Corporation (CTC) with an Outperform rating and $145.00 target price. Our Outperform rating is reflective of the underlying momentum within both key segments and select banners. While continued share gains in sport and better levering (though eCanadian Tire Money attached loyalty analytics) of its iconic brands underpin the growth strategy, it is the changes in the bench, ethos, and focus that support our positive bias. We are mindful of CTC’s misses (against select performance targets through 2014), but we are of the opinion that on the new mantra (and changes to the bench across key businesses), CTC through 2017E will prove to be a far more agile and adept player. While we are not expecting a series of home runs, we believe that as confidence builds on fewer strikeouts (relative to performance targets), that CTC’s ticket price will move higher (on further multiple expansion). The strategic partnerships with both Scotiabank and the SCENE loyalty program are, in our opinion, right on the money in terms of CTC’s brand positioning with a younger (target) demographic.

Analysis As the Tim Hortons of Canadian Retail, there exists in We the North a tremendous

affinity for and loyalty to CTC, which we believe is (finally) being better leveraged. In an always on world the dumb (but beloved) paper money in a smart money retail loyalty landscape was particularly expensive (but has finally been addressed).

In increasingly competitive markets, playing to your strengths (brand, footprint, home field advantage) is a better strategy than playing your competitors’ games. In automotive, compete on service competitors can’t offer; in living, on national brands, and in sport, on a this-is-our-game basis. We think CTC is increasingly on the money.

With the recent exit of a key competitor likely giving new entrants pause, it’s time for CTC to swing for the fences, and reassert its iconic status (across all banners). With a new dealer agreement and the requisite technology and talent in the game, we believe that CTC is likely better positioned than at any point in the last decade.

Valuation

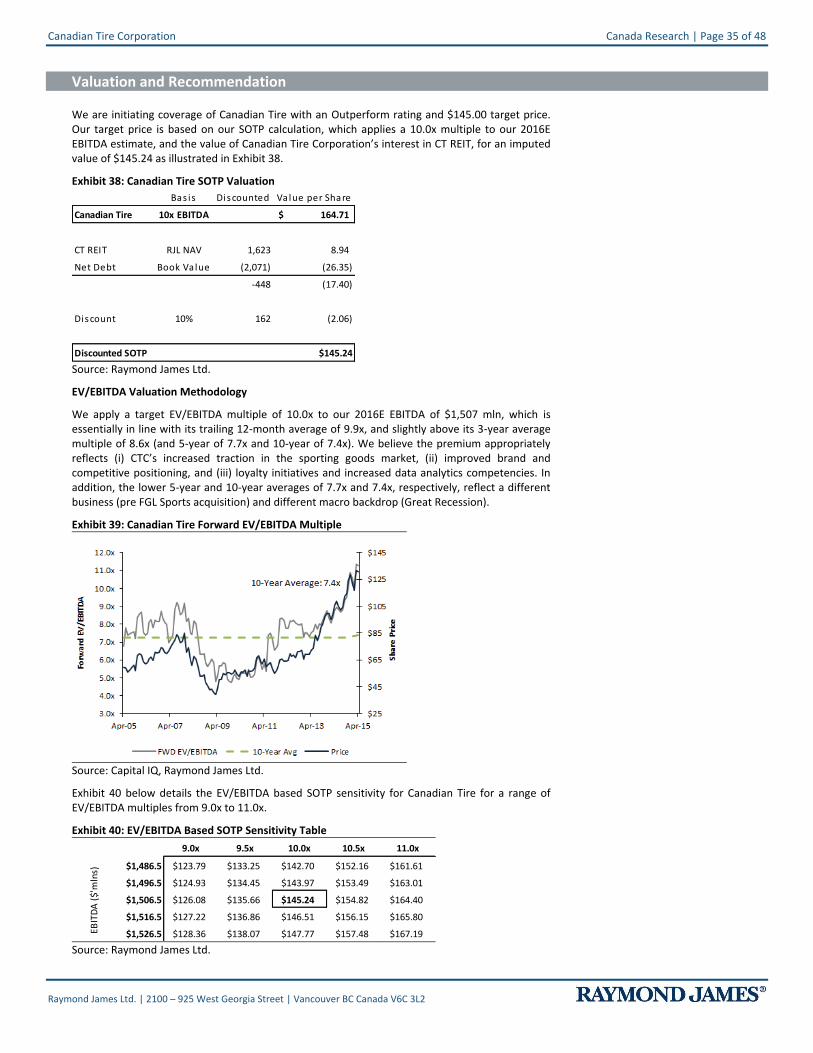

Our $145.00 target price is based on our SOTP calculation (see Exhibit 38), which applies a 10.0x multiple to our 2016E EBITDA, and the value of Canadian Tire Corporation’s interest in CT REIT. Our target multiple is essentially in line with CTC’s trailing 12-month average of 9.9x, and slightly above its 3-year average multiple of 8.6x. We believe the premium appropriately reflects (i) CTC’s increased traction in the sporting goods market, (ii) improved brand and competitive positioning, and (iii) loyalty initiatives and increasing data analytics competencies.

EPS 1Q 2Q 3Q 4Q Full Revenue EBITDA Mar Jun Sep Dec Year (mln) (mln)

2014A US$0.88 US$2.26 US$2.17 US$2.65 US$7.94 US$12,463 US$1,376

2015E 0.91 2.34 2.24 2.80 8.28 12,746 1,422

2016E 0.97 2.48 2.36 3.11 8.92 13,315 1,507

Source: Raymond James Ltd., Thomson One

Outperform 2

C$145.00 target price

Current Price ( Apr-24-15 ) C$131.54 Total Return to Target 12% 52-Week Range C$137.48 - C$100.01 Suitability Growth

Market Data Market Capitalization (mln) C$10,341 Current Net Debt (mln) C$2,071 Enterprise Value (mln) C$12,413 Shares Outstanding (mln, f.d.) 79.0 10 Day Avg Daily Volume (000s) 146 Dividend/Yield C$2.10/1.6%

Key Financial Metrics 2014A 2015E 2016E

P/E 16.6x 15.9x 14.8x

EV/EBITDA 9.0x 8.7x 8.2x

Company Description Canadian Tire Corporation (CTC), with approximately 1,700 retail and gasoline outlets (and Financial Services and CT REIT segments), is one of Canada’s largest and most iconic retailers.

Canada Research | Page 2 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Table of Contents

Executive Summary ............................................................................................................................................. 4

Company Overview .............................................................................................................................................. 5

Investment Thesis ................................................................................................................................................ 7

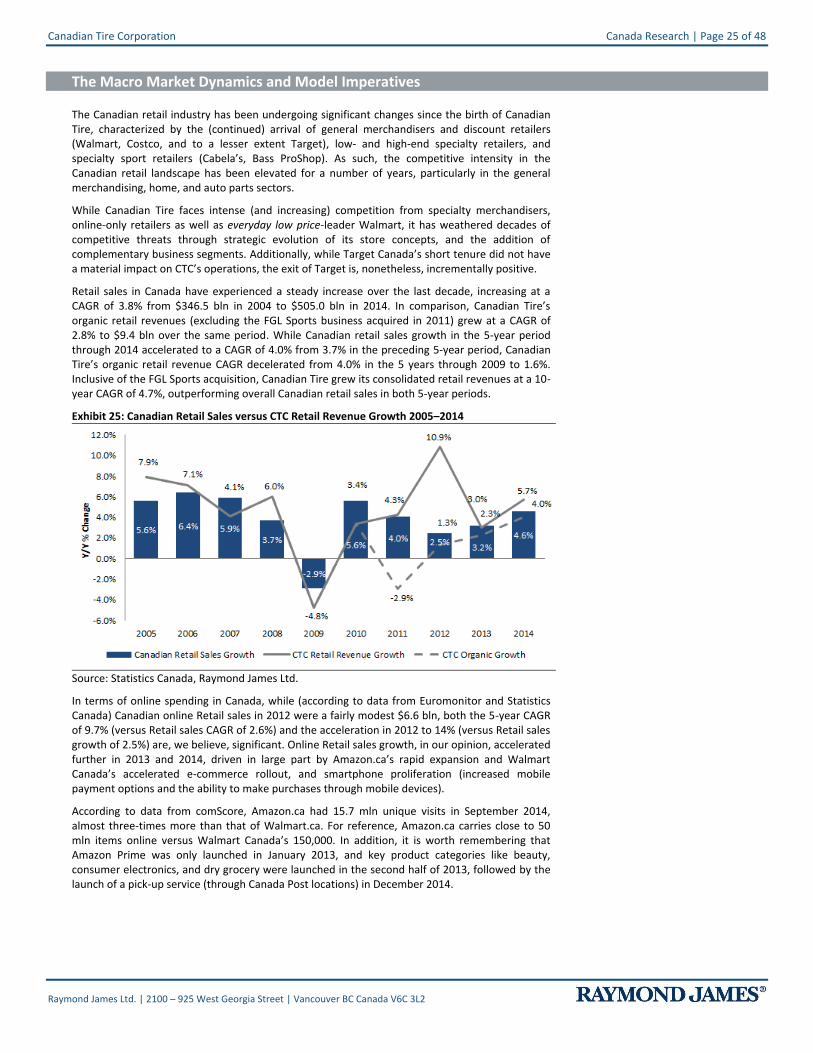

The Macro Market Dynamics and Model Imperatives ......................................................................................... 25

Corporate Structure, Financial Analysis, and Outlook ......................................................................................... 33

Valuation and Recommendation ......................................................................................................................... 35

Appendix A: Financial Statements ....................................................................................................................... 37

Appendix B: Management and Board of Directors .............................................................................................. 40

Risks ..................................................................................................................................................................... 41

Canadian Tire Corporation Canada Research | Page 3 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Canadian Tire Tear Sheet

CANADIAN TIRE TSX:CTC.A

F2012A F2013A F2014A F2015E F2016E

Price $131.54 Financial Summary 12/31/2012 12/31/2013 12/31/2014 12/31/2015 12/30/2016

Target Price $145.00

52-week Range $100.01 $137.48 EPS (Diluted) $6.10 $7.02 $7.94 $8.28 $8.92

Return to Target 11.8% DPS $1.40 $1.75 $2.10 $2.10 $2.10

Market Cap (mln) $10,341 BVPS $58.50 $67.57 $71.31 $78.08 $86.27

Valuation Metrics

Price/Sales 0.9x 0.9x 0.8x 0.8x 0.8x

P/E 21.6x 18.8x 16.6x 15.9x 14.8x

Price/BV 2.2x 1.9x 1.8x 1.7x 1.5x

FCF Yield 4.6% 4.8% 0.5% 2.7% 4.1%

Dividend Yield 2.0% 1.8% 1.7% 1.6% 1.6%

EV/Sales 1.3x 1.2x 1.2x 1.1x 1.1x

EV/Adj. EBITDA 10.9x 10.0x 9.0x 8.7x 8.2x

EV/EBIT 17.9x 16.2x 14.4x 13.4x 12.7x

81.4 80.7 79.0 77.0 76.6

Top 10 Institutional Holders Shares (mln) % Held Income Statement (C$ mln)

Beutel Goodman & Company Ltd. 1.53 1.97% Sales $11,427 $11,786 $12,463 $12,746 $13,315

Manulife Asset Management Limited 1.48 1.91% EBITDA (Adj) $1,139 $1,236 $1,376 $1,422 $1,507

Albikin Management Inc 1.44 1.86% EBIT $803 $890 $1,004 $1,075 $1,134

Ctc Dealer Holdings Ltd 1.41 1.82% Pre-Tax Profit $677 $785 $895 $983 $1,047

Tire N Me Pty. Ltd 1.40 1.81% Net Income (Adj) $499 $569 $632 $644 $690

Canadian Tire Corporation, Ltd. Profit-Sharing Plan 1.20 1.55% Cash Flow (C$ mln)

BlackRock, Inc. 1.07 1.38% CFO $702 $901 $586 $1,047 $1,093

RBC Global Asset Management Inc. 1.03 1.33% CAPEX $222 $404 $539 $770 $665

Mackenzie Financial Corporation 0.74 0.96% Free Cash Flow (FCF) $479 $497 $47 $277 $428

TD Asset Management, Inc. 0.72 0.93% Dividends $98 $112 $141 $163 $162

Δ in Working Capital -$429 $270 -$84 -$16 -$34

Balance Sheet (C$ mln)

Cash and Equivalents $1,016 $643 $662 $565 $946

Total Assets $13,229 $13,630 $14,553 $14,946 $15,740

Long Term Debt $2,336 $2,339 $2,132 $1,867 $1,867

Total Liabilities $8,464 $8,180 $8,922 $8,932 $9,134

Net Debt $2,068 $2,037 $2,071 $1,904 $1,523

Investment Highlights Key Company Metrics

SSS Growth

CTR 0.6% 1.4% 2.1% 2.6% 2.8%

FGL Sports 4.8% 8.8% 7.0% 5.9% 7.3%

Mark's 3.8% 4.4% 3.5% 3.6% 1.8%

Retail Sales Growth

CTR 0.9% 2.6% 4.3% 2.9% 3.0%

FGL Sports 3.9% 6.8% 11.2% 9.2% 8.9%

Mark's 4.0% 4.8% 4.5% 4.9% 4.4%

Sales per sq. ft.

Rating Outperform CTR $385.0 $389.0 $398.0 $408.3 $417.3

Target Price $141.15 FGL Sports N/M $275.0 $284.8 $304.1 $313.8

SALES ($'mln) $12,749 Mark's $305.3 $315.3 $328.3 $342.7 $353.3

EBITDA ($'mln) $1,411

EPS $7.95 ROE 10.9% 11.2% 12.0% 12.2% 11.9%

ROA 3.9% 4.3% 4.7% 4.8% 4.9%

Market

Price Cap.

Company Name Apr-24-15 (mln) LFY FY1E FY2E LFY FY1E FY2E1000 1001 1002 1000 1001 1002

Canadian Tire Corp. Ltd. $131.54 $10,341 $12,413 TSX:CTC.A 16.6x 15.9x 14.8x 9.0x 8.7x 8.2x

US Home Improvement Retailers

The Home Depot, Inc. $113.70 $147,623 $163,097 HD 24.1x 21.8x 19.0x 13.8x 12.7x 11.7x

Lowe's Companies Inc. $73.16 $69,627 $80,403 LOW 27.0x 22.1x 18.6x 13.0x 11.8x 10.8x

Group Average 25.6x 21.9x 18.8x 13.4x 12.2x 11.2x

Canadian Home Improvement Retailers/Distributors

Richelieu Hardware Ltd. $63.35 $1,241 $1,234 TSX:RCH 24.1x 21.5x 19.5x 16.2x 14.3x 13.1x

Rona Inc. $16.13 $1,743 $2,098 TSX:RON 29.3x 17.9x 16.6x 10.9x 8.1x 7.7x

Group Average 26.7x 19.7x 18.0x 13.6x 11.2x 10.4x

US General Merchandizers

Costco Wholesale Corporation $148.12 $65,169 $62,965 COST 31.9x 28.2x 26.0x 14.9x 13.3x 12.4x

Target Corp. $82.70 $53,072 $63,658 TGT 21.6x 18.2x 16.5x 9.4x 8.7x 8.4x

Wal-Mart Stores Inc. $79.84 $257,524 $303,923 WMT 16.1x 16.2x 15.4x 8.3x 8.3x 8.1x

The TJX Companies, Inc. $66.29 $45,307 $44,216 TJX 21.0x 20.2x 17.9x 10.9x 10.6x 9.8x

Group Average 22.6x 20.7x 19.0x 10.9x 10.2x 9.7x

US Auto Parts Aftermarket

Advance Auto Parts Inc. $148.61 $10,872 $12,426 AAP 22.1x 17.4x 15.3x 10.0x 9.3x 8.5x

AutoZone, Inc. $702.00 $22,270 $26,561 AZO 22.2x 19.6x 17.4x 13.1x 12.3x 11.7x

O'Reilly Automotive Inc. $229.35 $23,244 $24,167 ORLY 31.2x 26.4x 23.3x 17.0x 14.9x 13.8x

Group Average 25.2x 21.1x 18.7x 13.4x 12.2x 11.3x

US Sporting Goods Retailers

Cabela's Incorporated $54.19 $3,879 $7,609 CAB 19.3x 17.2x 15.0x 17.0x 15.3x 13.5x

Callaway Golf Co. $9.89 $767 $838 ELY 49.5x 247.3x 38.6x 16.1x 23.8x 14.3x

Dick's Sporting Goods Inc. $56.59 $6,693 $6,478 DKS 19.9x 17.8x 15.9x 8.8x 8.1x 7.5x

Hibbett Sports, Inc. $48.97 $1,219 $1,134 HIBB 17.1x 16.1x 14.5x 8.7x 8.4x 7.7x

Group Average 26.4x 74.6x 21.0x 12.7x 13.9x 10.8x

Total Group Average 25.3x 31.6x 19.1x 12.8x 12.0x 10.7x

OUTPERFORM 2

Canadian Tire Corporation, with approximately 1,700 retail and gasoline

locations, is one of Canada's largest and most iconic retailers. Our

constructive thesis is supported by the underlying momentum within key

segments and banners. While continued share gains in sport and better

levering of its iconic brands are supportive of continued growth, it is the

changes in the bench, ethos and focus that support our positive thesis. In

addition, the strategic partnerships with both Scotiabank and the SCENE

loyalty program are, in our opinion, right on the money, particularly in the

context of CTC's brand positioning with a younger (target) demographic.

Consensus

Enterprise

Value

(mln)

EV/ EBITDA RatiosPrice/Earnings Ratios

0

1

2

3

4

5

6

7

8

85

100

115

130

145

160

175

190

205

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15V

olu

me

(m

ln)

CTC

& S

&P

TSX

Re

bas

ed

CTC S&P TSX

Source: Canadian Tire Corporation, Capital IQ, Raymond James Ltd.

Canada Research | Page 4 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Executive Summary

Canadian Tire Corporation (CTC), with 493 dealer-owned Canadian Tire stores, 436 FGL Sports banner stores, 297 gasoline outlets, and 383 Mark’s stores, is one of Canada’s largest and most iconic retailers. While CTC’s core business is Retail with Canadian Tire Retail (CTR) as its core platform, the generational shift CTC is embarking on places increased focus on FGL Sports, with Sport Chek as its super brand.

Building a Sport(chek) Empire

With the August 2011 acquisition of the Forzani Group (FGL Sports), Canadian Tire emerged as the largest sporting goods retailer in Canada, commanding an approximate 31.5% of the sporting goods market. FGL Sports’ largest banner, Sport Chek, accounted for approximately 11.4% of the sporting goods market in Canada, followed by its Sports Experts banner at 4.3% at the end of 2012, both of which increased market share through 2014. The acquisition not only served to reinforce CTC’s leadership position within the Canadian sporting goods market, but to also stave off (or at a minimum materially delay) the entrance of US-based Dick’s Sporting Goods. The Canadian sporting goods industry is relatively concentrated with the 10 largest sporting goods retailers commanding an estimated 54.2% of the market, versus the more competitive US market, where the top 10 retailers represent approximately 40.6%. Within the sporting goods market, the apparel and footwear segments are poised to see the fastest growth rate through 2017E. According to estimates by Trendex North America, sales of sports apparel are expected to grow at an annual CAGR of 2.7%, followed by the sports footwear industry at a CAGR of 2.5%.

CTC has leveraged its existing position in the sporting goods market, and continues to gain momentum in both key growth segments and demographics. The planned 12-14 HERO stores (and additional Sport Chek flagship stores), and the efficacy of the cascading of the learnings from these stores across the broader base, will be key determinants of the momentum trends.

Show Me the (e)Canadian Tire Money

While Canadian Tire has long had a loyalty program in place through Canadian Tire Money (in fact it is Canada’s oldest loyalty program), it lagged those offered by key peers, as it was a paper versus smart currency. Given the competitive dynamics (and increased competitive intensity), every basis point of market share is that much more valuable, which further highlights the imperative that is a compelling, data analytics underpinned loyalty program. dunnhumby was an integral player in the initial loyalty program analytics design and specification. Following an Oct-28-14 national rollout, CTC customers can earn and redeem either digital or paper Canadian Tire Money (paper Canadian Tire ‘Money’, remains in circulation).

e-Canadian Tire Money (just like the paper Canadian Tire Money in your sock drawer and glove box) has no expiry date and can be shared with other members. In addition (in a similar vein to key competitor programs), customers who use their Canadian Tire Options MasterCard collect 10x the e-Canadian Tire ‘Money’ across Canadian Tire’s family of companies. Canadian Tire e-Money is a critical, and long overdue evolution of Canadian Tire’s loyalty offering, in a smart always on world, where real-time insights and digital rewards fulfillment are critical elements of the customer experience. Further complementing CTC’s loyalty initiatives, and most importantly the resonance of its banners with the (younger) target demographic, are key strategic initiatives attached to the SCENE Loyalty program.

Automotive – The Heart and the Margin

While sport is the cornerstone of growth, and loyalty analytics the powerful glue that not only holds the model together but makes it stronger (the currency is a means to and end), Automotive is the not-so-little engine that could. Automotive and Living are the two largest categories for Canadian Tire. With the increase in the competitive intensity within these categories (and the imperative that is an acceleration of organic growth), CTC has allocated significant capital over the last 5-plus years to these categories. While the Automotive category represents approximately 34% of Canadian Tire’s Point of Sale (POS), versus the Living category at approximately 33%, Automotive is the heart (and margin).

The single biggest change within Automotive is, in our opinion, the placing of service (versus product) at the centre of Canadian Tire’s offering, as the service element (done right) will create an ever-larger moat around this invaluable crown jewel. We are cautiously optimistic that after a number of false starts in Automotive, the team, the tools, and alignment of interests are such that CTC is poised to get back on offence (versus defense) through 2017E.

Canadian Tire Corporation Canada Research | Page 5 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Company Overview

Canadian Tire Corporation (CTC), with approximately 1,700 retail and gasoline outlets (and Financial Services and CT REIT segments), is one of Canada’s largest and most iconic retailers. While CTC’s core business is Retail and its core platform is Canadian Tire Retail (CTR), the relatively recent shift in strategic priorities places increased focus on FGL Sports (specifically, the Sport Chek banner) as the proverbial tip of the spear for CTC.

CTC has six business categories – Automotive, Living, Fixing, Playing (Sport), Apparel, and Financial Services – all positioned to prepare Canadians for the jobs and joys of everyday living in Canada (to paraphrase a management mantra). The CTR operated network comprises 584 (including 91 corporate PartSource) dealer-operated stores representing 20.5 mln sq. feet of retail space.

The FGL and Mark’s banners comprise 436 (7.2 mln sq. feet) and 383 stores (3.5 mln sq. feet), respectively. Canadian Tire Gas bar locations currently number 297.

Exhibit 1: CTC Business Categories – 2014 Revenues

Source: Canadian Tire Corporation, Raymond James Ltd.

The evolution (20-years in the making) of CTR’s store concepts continues. The most recent iteration began in 2008, with a focus on Smart Stores. As of December-2014, CTR has converted 337 (68.4%) and 22 (4.5%) of its base to the Smart Store and Small Market Store concepts, respectively. The Smart Store format integrates a number of new store features designed to enhance operating productivity and improve the customer experience. What we believe is worth noting (based on discussions with management), in terms of the evolution of the footprint, is the tighter focus on working formats versus experimenting with all manner of formats. The stores feature a racetrack layout, easier-to-read navigational signage, customer help buttons, price check stations, and additional customer assistance desks in key areas of the store, in addition to CTC banner stores-within-stores and ProShops. The Smart Store concept is capital light and converted stores have demonstrated a modest improvement in same-store sales performance (relative to traditional Canadian Tires stores).

Exhibit 2: Canadian Tire Retail (CTR) SSS Performance

Source: Canadian Tire Corporation, Raymond James Ltd.

Canada Research | Page 6 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

While CTC commands leading market shares in numerous key product lines, and is a leading sporting goods retailer with particular strength in Automotive, consistency of its financial performance (despite its extensive reach and scale) has been challenging.

CTC’s strategic objectives serve as the foundation for meeting targeted financial aspirations. Where CTC previously provided 5-year targets, effective 2015E, it is now providing 3-year targets. Given the accelerating pace of change in the Canadian retail landscape, and the challenged history in meeting targets, the shift to 3-year aspirations appears prudent. Through 2017E, CTC has outlined 3 strategic priorities, namely to: (i) attract and retain world class talent; (ii) develop best- in-class digital and analytics capabilities; and, (iii) leverage the strength of its brand. Exhibit 3 details Canadian Tire’s financial aspirations for the periods: 2005-2009; 2010-2014, and 2015-2017.

Exhibit 3: CTC Aspirations

2015-2017 Target 2015E 2016E 2017E RJL Est.

Retail Sales growth

Canadian Tire 3%+ 3.1% 3.0% 2.8% 2.9%

FGL Sports 9%+ 10.5% 9.7% 9.3% 9.8%

Mark's 5%+ 5.1% 5.4% 5.8% 5.4%

ROIC 9% 9.5% 9.4% 9.6% 9.5%

EPS growth 8%-10% 5.8% 7.0% 8.8% 7.2%

CTFS Return on Receivables 6%+ 7.6% 7.6% 7.4% 7.5%

2010-2014 Target 2010 2011 2012 2013 2014 Actual

Retail Sales growth 3%-5% 1.4% 2.0% 0.8% 2.5% 4.4% 2.4%

Return to shareholders 10%-12% 19.8% -1.7% 6.8% 46.5% 24.3% 17.5%

ROIC 10%+ 8.0% 7.7% 7.4% 8.1% 8.1% 8.1%

Adj. EPS growth 8%-10% 18.5% 5.3% 6.9% 13.5% 10.0% 13.3%

CTFS Return on Receivables 4.5%-5% 5.0% 5.5% 6.8% 7.3% 7.4% 7.4%

2005-2009 Target 2005 2006 2007 2008* 2009* Actual

Comparable store sales 3%-4% 3.0% 2.3% -0.6% 0.3% -2.6% 0.5%

ROIC 10% 9.3% 9.3% 10.5% 8.9% 7.7% 9.1%

Adj. EPS growth 12%-15% 16.2% 11.0% 18.1% -2.2% -12.4% 6.1%

Adj. EBITDA growth 10%-15% 14.6% 6.3% 9.7% 1.3% -2.0% 6.0%

*Aspirations were re-assessed due to the credit market disruption and subsequent economic downturn Source: Canadian Tire Corporation, Raymond James Ltd.

In order to better deliver against its financial aspirations, CTC is focused on making what, in our opinion, is a critical generational shift, centered around both the brand and the experience. The chosen cornerstone, upon which CTC has chosen to build its next generation brand, is the sporting goods category.

For CTR, this translates into acting less like a general merchant, and more like a specialty retailer with store-within-store and dedicated category-specific ProShops (currently led by Hunting and Fishing). The opportunity in Automotive (specifically in the growth of service and assortment) remains material, as are the stakes given the current (and expected) changes in the competitive landscape.

With sporting goods as the cornerstone, FGL mind and market share gains, and specifically the accelerated growth of the Sport Chek banner are strategic imperatives. The fight for increased relevance with younger consumers will not be fought (or won) in the aisles of either a CTR or Mark’s store. To win, CTC needs to deliver a knockout with Sport Chek, the halo effect of which will impact multiple banners.

Canadian Tire Corporation Canada Research | Page 7 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Investment Thesis

Perspective on Canadian Tire’s Business Model

It is impossible to do justice to a discussion of Canadian Tire without detailing (something of a misnomer given the very limited disclosure) the newly strengthened Associate Dealer Agreement. A new agreement (the culmination of a 2-year negotiation), which expires in 2024, was signed on April-17-13, and is expected to provide a framework for a new era of cooperation between Canadian Tire Corporation and its Associate Dealers. The Associate Dealer model is unique.

Canadian Tire stores are operated by independent third parties known as Associate Dealers. Canadian Tire’s relationship with each Dealer is governed by an individual Dealer contract pursuant to which each Dealer agrees to operate the retail business of a Canadian Tire store under the Canadian Tire name and to use his or her best efforts personally to manage his or her Canadian Tire store at its maximum capacity and efficiency. Each Dealer owns the fixtures, equipment and inventory of, and is responsible for the store staff and operating expenses for, the Canadian Tire store he or she operates. Each Dealer agrees to comply with the policies, marketing plans and operating standards prescribed by Canadian Tire, including purchasing merchandise primarily from Canadian Tire and offering merchandise for sale at prices not exceeding those set by Canadian Tire. In return, Canadian Tire supports Associate Dealers with marketing, supply chain management, purchasing, administrative, financial and information services. Except in limited circumstances, the premises on which the Canadian Tire stores are located are owned or leased by CTC and licensed to individual Associate Dealers. Individual Dealer contracts are all in a standard form, each of which generally expires on December 31, 2024.

Canadian Tire’s model, operated through its Associate Dealers, is a pull system. In Canadian Tire’s pull system, the Associate dealers determine what they want in the store, and corporate (CTC) does its best to meet the dealers’ requirements, versus in a push system where corporate makes the decisions and pushes inventory into the system. The primary benefit of a pull system is that it allows each Dealer to leverage local knowledge and expertise in determining preferred inventory. The offset is that a pull system is inherently inefficient (relative to a push system).

The pull system, in our opinion, plays to the Retail as Art model of yesterday, versus the Retail as Science model of the best-in-class global retailers of tomorrow. As such, the increased flexibility of the new dealer agreement is, we believe, less about a new era of cooperation, and more about the strategic imperative that is Retail as Science, Data as Art. While dealers are undoubtedly invaluable in determining timing on when to get snow shoes in stock up North, versus out West, the specific inventory levels and assortment are, in our opinion, best left to data-driven decisions by corporate.

The specifics on the road to a becoming a dealer are relatively scant; the process begins with an online application, followed by a pre-screen, and a three-stage interview (the final interview involves both senior management and representatives from the dealer network). The journey is also relatively (given the economics) capital light, with successful applicants required to cover up to 25% of the value of initial store inventory and fixed asset costs, or an estimated minimum of $125,000 in accessible capital (and additional $125,000 for dealer training and development).

An approved dealer enters a minimum 6-month (can be extended for another 6 months if warranted) dealer training program, which includes a number of store placements. In addition, new dealers receive an elevated level of support from CTC for the first 2 years. A key component of the dealer contract is upward mobility. While each Dealer receives training on store operations, performance, and inventory and staff management (after which they are placed in a pool and assigned a smaller store), the dealers laddered progression to larger and more profitable stores is dependent on meeting performance targets (most specifically, sales targets). In addition to improving dealer mobility (dealers are required to retire after 40 years in the system), the new contract brings an increased (and critical) focus on the relationship (versus the contract specifics), which allows for better flexibility in collaboratively working together to face the rapidly changing face of Canadian Retail.

While the change in tone in the relationship to conversations, versus finger pointing, is undeniably a critical (and positive) departure from the finger pointing of old, the billion dollar question in our opinion is whether the conversations translate into the requisite sense of urgency and alignment, under the CEO versus management by a committee of 493 CEOs.

Canada Research | Page 8 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

As previously noted, sport is both the cornerstone of the targeted generation shift and earnings growth. The reality is that sport is not only faster growing than core CTR categories, but it is also a higher margin business. Given Canadian Tire’s success as a hi-lo (versus every-day low price) retailer, and a growth strategy increasingly tied to all things automotive and sport, understanding the swings and roundabouts of the new agreement becomes all the more important.

A dealer’s upward mobility (and primary motivators) in the network are: (i) sales growth and, (ii) continuous engagement in personally running their store. The dealer of today whose average age is now believed to be in excess of 50 years of age, while undoubtedly a savvy retailer in core Canadian Tire categories, is likely significantly less experienced in the growth drivers of tomorrow. The risks of this new reality is that dealers who previously were poised for the next step up the ladder, are going to either have to hurry hard to stay on the ladder (a positive), or are simply going to tap out of the race and dedicate less time to the store, and more time to the sun (a negative). By its very nature, a pull-ordering system facilitates a mismatch of both strategic and economic imperatives between dealers and corporate, as a dealer’s orders do not need to match with the dealer’s retail sales. The dealer, as a rational individual (and business owner) acts in his own economic self-interest first, and in the interest of CTC second. With dealers controlling both what and how much inventory they order, and earning a spread between what they pay the corporation and receive from customers, the incentive to order excess inventory (when on promotion by the corporation) and sell (the excess) at regular prices when the promotion ends is real (and creates ripples through the system). Given that hockey is Canada’s Game, and that Canadian Tire was recently advertising a $99.99 (we’ll call it $100.00) Bauer Nexus 600 for $69.99 (we’ll call it $70.00), we decided to use a hockey stick to illustrate the above dynamic.

We assume that CTC’s COGS on the hockey stick is $40.00 with a retail price of $100.00 for total gross margin dollars of $60.00, of which we assume CTC takes $25.00 and the dealer takes $35.00, for CTC gross margins of 38.5% ($25.00/$65.00) and dealer gross margins of 35.0% ($35.00/$100.00). At full price, the margin dollars are split 41.6% CTC/58.3% Dealers.

If the dealer did not have an incentive (incremental risk for incremental dollars), then when the hockey stick is on promotion (assuming no excess inventory is ordered because of the promotion), the gross margin hit (of promotional prices) would be relatively balanced. However, if the dealer knowing their market, and loving the game purchases excess inventory on promotion from CTC, and sells it at regular prices, the implications are numerous.

The dealer over-purchases the promotion priced stick at $52.50 ($40.00 COGS plus $12.50 margin) in the belief that he can sell the excess inventory at $100.00, versus the promotional price of $70.00. In this scenario, CTC generates gross margin dollars of $12.50 and margins of 20.0% ($12.50/$62.50), while the dealer secures $37.50 and margins of 37.5% ($37.50/$100.00) on the excess inventory. The kicker however, is that this is not free money for the dealer, but rather a double-edged sword for both parties.

At the risk of stating the obvious, the supply chain inefficiencies the above scenario creates are manifold, and the ripple effect through the system profound. Not only is inventory risk higher (the dealer may not know their market as well as they like to think), but forecasting and replenishment are complicated (and inventory at corporate is necessarily higher than is ideal). In addition, consumers were too often met with sold out promotional products, which was often more a function of the model, than actually being sold out. We believe that the above dynamics were one of the drivers behind too much time spent on finger pointing and on the minutiae of previous contracts, versus the current contract, which according to management, is focused on the relationship and constructive dialogues about how to move forward together. A number of key differences highlighted include:

Flexibility to Face the Future (Evolution of Digital and Loyalty)

Sharing of the right costs in the business

Allows for increased collaboration

Contract is the longest ever secured

Canadian Tire Corporation Canada Research | Page 9 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Canadian Tire

Canadian Tire Retail’s (CTR) flagship banner, Canadian Tire, is one of the most shopped retailers in Canada with 493 dealer-owned Canadian Tire stores (complemented by 91 PartSource stores and 297 gas bars) at Dec-31-14. Canadian Tire represents 50% of CTC’s revenues and 60% of CTR’s retail sales. Canadian Tire is one of Canada’s most iconic brands, with commanding market share in most categories, and Canada’s most-read flyer. The average Canadian Tire bannered store is 41,580 square feet.

Automotive – The Heart and the Margin

Automotive and Living are the two largest categories for Canadian Tire. With the increase in the competitive intensity within these categories (and the imperative that is an acceleration of organic growth), CTC has allocated significant capital over the last 5-plus years to these categories. While the Automotive category represents approximately 34% of Canadian Tire’s Point of Sale (POS), versus the Living category at approximately 33%, Automotive is the heart (and margin). The reality of quite how appealing the economics of the Automotive (tires, accessories, parts, and service) business are, has not been lost on key competitors of all shapes and sizes (Walmart continues to accelerate the build out of its auto parts offering and has 1,000-plus SKUs available online, while Amazon Canada launched its auto parts push in October 2013).

As such, we believe that the capital deployed to the Automotive category has at best served to buttress the fortress, rather than expand the empire, leading to disappointing ROIC metrics from the category. The Living category is, to our mind, a traffic-driving investment in margin.

The Canadian automotive aftermarket is an approximately $23.1 bln business according to Statistics Canada. Sales in the Do-It-For-Me (DIFM) categories represent approximately 74% of the market, with the Do-It-Yourself (DIY) market the balance. As depicted in Exhibit 4, labour receipts make up the largest part of the aftermarket for auto parts, followed by installed parts and tires, accessories and DIY parts. Sales of DIY auto parts account for an estimated 13% of aftermarket retail sales, which according to Automotive Industries Association of Canada, Canadian Tire continues to lead with an estimated 46.7% market share in 2012 (its highest share in recent years).

The balance of auto parts is sold to dealerships and independent repair outlets that are supplied by Wholesale Distributors (WD). The WD channel is dominated by Uni-Select, NAPA, and Advance Auto Parts-owned CARQUEST. The commercial install market is necessarily dominated by new car dealerships with an estimated 36.6% share of the DIFM market, followed closely by independent repair shops at 32.2%. In our opinion, there are a number of tangible growth opportunities in the DIFM market upon which we expect Canadian Tire to capitalize. Exhibit 4 details the size and composition of the Canadian Automotive Aftermarket.

Exhibit 4: Size of Automotive Aftermarket – DIFM and DIY

Source: Canadian Tire Corporation, Statistics Canada, Raymond James Ltd.

Canada Research | Page 10 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Canadian Tire is the largest player in the aftermarket DIY auto parts industry in Canada, commanding an estimated 9.2% share of total auto aftermarket sales, and the leading online tire and wheels retailer. Canadian Tirebannered stores cater to the light to medium Do-It-Yourself (DIY) customers, while PartSource caters to the hard-core DIY and the previously untapped commercial installers markets. With the increase in the competitive intensity in the auto parts market, particularly on the expansion of AutoZone, Canadian Tire responded with the creation of PartSource, which caters to the hard-core DIY demographic. Additionally, Canadian Tire also addressed in-store availability of parts and faster and more efficient part delivery through the creation of a PartSource hub system. At approximately 15,000 square feet, a PartSource hub store is more than twice the size of a regular PartSource store, and carries a broader product assortment which enables better product availability and faster delivery to nearby Canadian Tire and PartSource locations. There are currently 91 PartSource locations.

While Canadian automotive aftermarket sales (according to Statistics Canada) have grown at a CAGR of 3.6% over the last decade, the pace of growth has moderated from a 4.9% CAGR in the 2005-2009 period to 2.3% in the 2010-2014 period. Factors influencing the automotive aftermarket include vehicle age and mix on the road, the number of kilometers driven, gasoline prices and, in the medium to long-term, new car sales. The DIY market benefits from older vehicles, mostly in the 10-year plus age group, while WDs primarily benefit from 6-10-year old vehicles. Exhibit 5 details the Canadian automotive aftermarket by category and growth.

Exhibit 5: Evolution of Canada’s Automotive Aftermarket Industry

Source: Canadian Tire Corporation, Statistics Canada, Raymond James Ltd.

The slower rate of growth is, in our opinion, due in large part to the decline in the average age of vehicles on Canadian roads, which is a function of the very aggressive financing offers from new car dealers. The low interest rate environment has made possible low-to-no interest financing for periods of up to 84 months which, in turn, has translated into strong new vehicle sales despite the restrained consumer spending (highlighting Canadian consumers’ preference for new vehicles over other big-ticket items). New light vehicle sales growth in Canada in the 2010-2014 period grew at a robust CAGR of 4.8% versus a decrease of 1.2% in the 2005-2009 period. With the interest rate environment expected to remain at historically low levels in the near-future, the strong growth in new vehicle sales is expected to continue through 2016E.

Automotive aftermarket retailers are direct beneficiaries of increased driving activity, as: (i) an increase in distance driven increases the necessary spending on maintenance on older vehicles, (ii) part failure rates inevitably rise with increased driving activity, particularly for categories like brakes; and, (iii) an increase in distance driven leads to quicker wear and tear for parts like tires. With the increasing complexity of modern vehicles and the expertise required for their maintenance and repair, the growth rate of the DIFM market is expected to outpace that of the DIY market.

Against this backdrop, Canadian Tire has implemented several initiatives to increase its presence in the commercial install market and improve its automotive business and service offerings, including the enhancement of customer-facing processes (in-store technology), upgrade of its IT infrastructure, supply chain capabilities, and expanded product assortment. Additionally, in March 2014 Canadian Tire brought in Michael Broderick, an industry veteran with over 20 years of automotive experience, to lead its Automotive business.

Canadian Tire Corporation Canada Research | Page 11 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Living the National Brand Life

The second largest component of CTR’s sales is the Living category, accounting for an estimated 33% of CTR’s revenues (approximately $2,069 mln business). The Living category comprises of home décor, home organization, and household essentials (cleaning supplies, personal hygiene products), in addition to kitchen appliances, gardening, outdoor tools, and seasonal items.

According to Statistics Canada, the retailing of indoor furniture, household appliances (two-thirds of which we moved to the Fixing market), home furnishings, housewares, lawn and garden equipment, and pet food was $40.2 bln in 2014 (which represents a 10-year CAGR of 2.8%). We estimate Canadian Tire’s 2014 market share at 5.1% (on revenues of approximately $2,069 mln) versus 3.9% in 2010. The increase in market share is primarily attributed to Canadian Tire’s expanded offering versus increased share in existing categories. Exhibit 6 details CTR’s Living category sales and market share in the period 2010-2014.

Exhibit 6: Evolution of Living Revenues and CTR’s Market Positioning

Source: Canadian Tire Corporation, Statistics Canada, Raymond James Ltd.

The marked deceleration of sales growth in the living category in the 5-year period through 2014 masked (relatively) solid continued growth of pet food and accessories. While living category sales growth decelerated from a 3.8% CAGR in the 5 years through 2009, to 1.8% through 2014, pet food (and accessories) and housewares sales CAGR were 3.4% and 3.1%, respectively.

The pet food market in Canada is a $3.5 bln industry, and accounts for approximately 8.7% of overall Living retail sales. Consumers are treating pets as members of the family and, as such, consumer demand for high-quality, natural and nutritious products, continues to grow. According to the Pet Industry Joint Advisory Council of Canada, approximately half of Canadian households own a pet. In addition, the pet food market appears to be less cyclical, which is evidenced by the reality that during the last economic downturn, pet-owners of all income levels cut back more on personal spending than on pet-related expenditures (according to Ibisworld).

As such, it does not come as a surprise that sales of pet food grew at the fastest rate in the 5 years to 2014, increasing at a CAGR of 3.4% versus the overall Living retail sales CAGR of 1.8%. Despite outpacing the overall industry, the 3.4% CAGR reflects a meaningful deceleration from the very robust 11.2% CAGR recorded in the 5 years through 2009. According to market research group Packaged Facts, the total pet-related market (food, accessories, veterinary) through 2018 is expected to grow at a 3.9% CAGR, led by growth in accessories.

The strong growth in the 2005-2009 period reflects both mass merchandizers and discounters meaningfully expanding their product assortment, with a broad price range of pet food and accessories, bringing premium offerings (we use the term loosely) to the mass channel. The increased competitive intensity in pet food and accessories that this expansion created necessarily resulted in increased bite in pet product pricing (driving prices and segment growth rates lower). We believe that the rebalancing (or shake out) of the pet product market has largely run its course given current share (and share trends in the last 5 years). Exhibit 7 details the evolution of pet-related spending and market share of the Retail Living category.

Canada Research | Page 12 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 7: Retail Sales Growth of Pet Food and Accessories

Source: Statistics Canada, Raymond James Ltd.

A decade ago, if looked hard you would find a shelf or two of canned pet food in CTR, whereas today, the pet product offering is on occasion a full aisle (or two). The push into expanded pet product offerings was particularly opportune, as it is both a traffic-driving and margin-expanding category with the best growth profile within CTR’s Living segment. We believe that pet product sales are positioned to, at a minimum, maintain their current growth trajectory, as even within the department and mass channels, there is a want for premium offerings (the mix impact of which offsets the ticket pressures on basics). Heaven forbid our four-legged fiends (sorry, friends) don’t get a new toy or Kong every second time we do a Canadian Tire (or dog food) run.

The $9.3 bln housewares segment’s 5-year CAGR of 3.1% through 2014 reflects a meaningful acceleration from the more modest 1.8% CAGR recorded in the preceding 5 years to 2009. The relative performance of housewares is all the more impressive, in the context of the paltry 1.2% CAGR through 2014 of the Living category excluding housewares and pets, versus 3.8% in the 2005-2009 period. We believe the acceleration in sales of housewares reflects the disruption driven merchandising innovation and new product introductions, necessitated by increased competitive intensity in the space.

CTR revamped its Living strategy to include a wider assortment of merchandize from prominent brands (such as KitchenAid, Lagostina, Cuisinart, and Miele), in addition to inspirational displays and improved product adjacencies in order to enhance Canadian Tire’s brand image as a destination for kitchen, home organization, and cleaning supplies. In fact, kitchen accounts for the largest part of CTR’s Living sales at an estimated $690 mln (approximately a third of Living sales), with kitchen appliances and cookware the two largest components. We estimate CTR had sales of kitchen appliances of approximately $310 mln, followed by cookware sales of approximately $276 mln. Exhibit 8 below illustrates the 5-year CAGR’s of the Living category.

Exhibit 8: Retail Sales CAGR’s of the Living Segment through 2014

Source: Statistics Canada, Raymond James Ltd.

Canadian Tire Corporation Canada Research | Page 13 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

CTR’s expanded Living strategy continues to resonate with consumers, with the performance in the kitchen category proving particularly robust. In addition, the sales performance of stores with the full living and associated merchandizing strategy is significantly better than CTR stores without the full living offering. Further underpinning the appeal of the strategy is the low capital intensity of the enhanced Living strategy. While the Living category (with exception of pet products) is largely an investment in margin (lower margin contributor), we believe that the low capital intensity and traffic-driving nature served to strengthen CTR’s business, and protect its market share in the face of increased competitive intensity.

Fixing to Play and Playing to Fix

Within CTR, the combined fixing and playing segments represent approximately 33% of revenues, with fixing edging playing on a percent of revenue basis. We estimate fixing represents 17% of revenues and playing 16%. While fixing is the slightly larger of the two segments, it is playing that is the higher margin business (and of particular import in terms of CTR’s strategy, brand image and repositioning).

CTR is a leading destination for the do-it-yourself home repairer, offering home renovation and repair tools, and paint and accessories. According to Statistics Canada, total home renovation spending (at Retail) was an estimated $29.0 bln in 2014, which grew at a 10-year CAGR of 3.1% through 2014. The market is dominated by The Home Depot (HD-N, RJA: Market Perform) with an estimated market share of 21.2%, followed by Home Hardware at 14.6%, Rona at 11.3%, Canadian Tire at 3.7%, and Lowe’s (LOW-N, RJA: Market Perform) a distant fifth at an estimated 2.4%. We estimate Canadian Tire’s Fixing revenues totaled approximately $1,066 mln in 2014 (17% of CTR’s revenues). With a four-firm concentration ratio of 50.5%, the fixing market is relatively concentrated.

At the risk of stating the obvious, the biggest differentiator is that the hardware stores (The Home Depot, Home Hardware, Rona, and Lowe’s) carry dry wall, lumber, heavy-duty repair materials (and a higher percentage of national brands), while CTR stores focus on the DIY customer demographic. We would not be surprised (given the scale of the addressable opportunity) to see CTR further up the ante in the Fixing segment with similar strategies to those effectively used in the expanded Living category offering.

The home improvement industry is highly correlated with the housing market. Sale of existing houses is one of the most important drivers of future home improvement spending. This is due to the reality that many homeowners now routinely undertake minor renovations prior to putting their homes on the market for sale, in addition to the future homeowners who generally embark on renovation projects following a home purchase. According to a CMHC survey, an estimated 40% of households were planning on making improvements to their homes in 2014 with an average project price tag of $20,000 (versus $15,000 in 2013). Exhibit 9 details actual and expected total renovation spending through 2016E. We expect renovation expenditures to increase 3.0% in 2015E, and 2.7% in 2016E.

Exhibit 9: Home Sales and Total Renovation Spending

Source: CREA, Statistics Canada, Raymond James Ltd.

Canada Research | Page 14 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

The Canadian housing market has experienced significant growth over the last decade, supported by an interest rate environment that has made home ownership (outside of Vancouver and Toronto) more feasible for a greater swathe of the population. In spite of the negative impact of declining oil on Canada’s economy, economic conditions appear to remain supportive of continued housing demand, which is a function of continued low mortgage rates (by historical standards) and demographic trends. Canada continues to attract a high level of immigrants, which has been the major driver of Canadian population growth.

Sharply higher housing prices are also forcing many home buyers, particularly the prime new household formation group of those aged between 25-34 years, to look for less expensive (read, fixer-upper) properties. In addition, Canada’s population is also aging – the proportion of Canadians aged 65-plus is expected to rise from 15% in 2013 to 23% by 2030. With an aging population that is more likely to stay put in their existing homes, combined with the reality that a rising proportion of homeowners are squeezed out of the red hot housing market in major Canadian cities, demand for renovation spending (despite the expected 1.1% dip in home sales in 2015) is likely to stay strong through our forecast window.

Total renovation spending at Retail, with the exception of modest decreases in 2009 and 2011, has increased every year over the last 10 years. During this 10-year period, the market grew at a CAGR of 3.1% to an estimated $29.0 bln. Sales in the last 5-year period through 2014, however, grew at a CAGR of 0.9% versus the preceding 5-year period CAGR of 5.4%. The more modest growth, in our opinion, largely reflects an increasingly stretched consumer (on an increasingly rich housing market buy-in), leaving less room for renovations.

Exhibit 10: Total Renovation Spending 2005-2016E ($ bln)

Source: Statistics Canada, Raymond James Ltd.

The growth in total renovation spending has, however, exceeded that of Canada’s GDP growth, which in the 10-year period through 2014, increased at a CAGR of 1.9%. Home improvement sales accounted for an estimated 1.8% of Canada’s GDP in 2014, up from an estimated 1.6% in 2005. In addition, renovation spending has been the fastest growing component of residential investments in Canada over the last 10-years, outstripping the growth in both new construction and home resale-related expenditures.

While part of the growth in renovation spending is attributed to the growth in Canada’s housing stock, the majority of the growth reflects increased expenditures per household. In fact, the average Canadian household now spends close to $4,600 on home renovation projects annually versus $2,500 in the 1994-1998 period. While the negative impact of lower oil prices will necessarily dampen renovation spending in Alberta, the reality that approximately two-thirds of renovation dollars are generated from Ontario and Quebec (where home sales are forecast to increase by low single digits in both 2015E and 2016E) is supportive of continued home improvement spending.

Canadian Tire Corporation Canada Research | Page 15 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

While an estimated 42% of Canadians identify CTR stores as their first choice for tools, this number drops significantly to 10% for small-home renovation and maintenance projects. Against this backdrop, CTR has revisited its Fixing business (with the same approach as in Automotive), with an emphasis on fundamentals such as optimizing product assortment, and introducing higher-quality brands, accompanied with marketing campaigns. By way of illustration, CTR’s wood stain TV commercial that aired during 2Q14 resonated particularly well with consumers, which is evidenced in the strong uplift in paint sales during the quarter.

As such, CTR’s product assortment is, we believe, sufficient to accommodate many small-home renovation and maintenance-related projects. The medium to longer-term outlook on home renovation spending is, we believe, more subdued. Housing affordability will necessarily decline as borrowing costs increase off their historic lows, and consumers find themselves more financially stretched. In the interim, Canadian households appear focused on managing down their mortgage debt.

The $8.7 bln Canadian sporting goods market is characterized by intense competition between existing retailers, exacerbated by increasing competition from online sales channels. The Playing segment accounts for an estimated 16% of CTR’s revenues. The approximately $1,003 mln Playing business has a strong focus on hardgoods, specifically sporting and recreational equipment, with leading market positions in several key categories including hockey, camping, hunting, fishing, and bicycles. Canadian Tire offers a broad range of sporting and recreational equipment, with a more limited footwear and apparel product mix.

The Canadian sporting goods industry is comprised of four primary channels:

Traditional Sport Stores;

Mass Merchandizers and Department Stores;

Canadian Tire/Costco/Other;

Athletic Footwear Retailers.

Sport stores represent the largest piece of the Canadian sporting goods pie, commanding a 65.4% share, followed by mass merchandizers (department stores and discount stores) in a distant second place. FGL Sports’ Sport Chek banner (owned by CTC) is not only the largest player in the Canadian sporting goods market, but it is also the only retailer among the top three players in all three segments (equipment, footwear, and apparel) of the sporting goods market.

Mass merchandizers and department stores account for 14.9% of the Canadian sporting goods market with Walmart Canada commanding a 9.6% market share, while other notable participants, such as Sears and The Bay, are significantly smaller.

The third-largest segment, which includes Canadian Tire and Costco, represents 12.9% of the Canadian sporting goods market.

The remainder of the market is serviced by the collection of athletic footwear stores, accounting for 6.8%, including the likes of Foot Locker, and The Running Room. Exhibit 11 depicts sales of Canadian sporting goods by retail channel.

Exhibit 11: Breakdown of the Canadian Sporting Goods Market – 2013

Source: Trendex North America, Raymond James Ltd.

Canada Research | Page 16 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

With an estimated 8.7% market share, Canadian Tire is the third-largest player in the approximately $8.7 bln Canadian sporting goods market. In the preceding decade, CTR was squeezed by Walmart, whose market share essentially doubled from 5.4% in 2003 to 9.6% in 2012, while CTR’s share decreased modestly from 9.1% to 8.7% according to Trendex data. While an estimated 57% of Canadian sporting goods buyers made a purchase at one of CTC’s banners in 2014, only 24% were made at CTR. In response, CTR made changes that included bringing in the top sporting goods merchant from FGL Sports (CTC acquired FGL in 2011) to run CTR’s Playing business. The focus and mandate were clear – increase CTR’s relevance as a sporting goods destination. Exhibit 12, below, highlights the evolution of the Canadian sporting goods industry and its largest players.

Exhibit 12: Evolution of Canadian Sporting Goods Market – 2012 versus 2003

Source: Trendex North America, Raymond James Ltd. (CTC banners marked in red)

The largest component of the Canadian sporting goods industry is equipment, which accounts for an estimated 53.2%, with athletic footwear at 27.1% and apparel at 19.8%. The mass merchandizers tend to compete most effectively at an entry level in the hardgoods market, given their souring reach and the reality that price tends to trump either service or the shopping experience at this end of the market. Canadian Tire is the largest player in the hardgoods (sports equipment) market with an estimated 14.9% market share. Exhibit 13 details CTR’s sporting goods market share.

Exhibit 13: Largest Canadian Sporting Goods Retailers – Market Share

Canadian Tire 14.9% Sport Chek 18.5% Lululemon 11.0%

Walmart 12.5% Foot Locker 6.2% Sport Chek 9.2%

Sport Chek 9.0% Running Room 6.1% Walmart 7.3%

Golf Town 6.6% Walmart 5.4% Sears 6.0%

MEC 3.9% Sports Experts 5.3% Sports Experts 5.9%

Sports Experts 3.3% Sears 1.7% Mark's 5.9%

Costco 3.0% Golf Town 1.7% Winners 5.1%

Sears 1.7% Athletes World 1.7% Costco 2.1%

Total CTC 27.2% 25.5% 21.0%

Equipment Footwear Apparel

Source: Trendex North America, Raymond James Ltd. (CTC banners marked in red)

Canadian Tire’s sporting goods selection is largely comprised of hardgoods (70% of assortment), with leading market positions in hunting, fishing, and camping, as well as strong market presence in hockey equipment, biking, and biking accessories. CTR’s 14.9% equipment market share imputes equipment sales of approximately $690.3 mln which, given market dynamics, was necessarily the most exposed market in the last 10 years to the mass merchants’ share grab. CTR has rolled out hunting and fishing store-within-store ProShops in key markets (following a successful test in 2011). CTR’s 30 Fishing ProShops, 62 Hunting ProShops, and 104 combined Fishing and Hunting ProShops, generated approximately 15% of Playing revenues in 2014, implying revenues of approximately $150.4 mln. While CTR leads the equipment market of the sporting goods industry, it does not have a meaningful footwear and apparel offering. CTC owned FGL Sports banner Sport Chek is the leading player in the Footwear Market (and number two in the Apparel Market).

Canadian Tire Corporation Canada Research | Page 17 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

FGL Sports

The Cornerstone of Growth

The Canadian sporting goods industry is relatively concentrated with the 10 largest sporting goods retailers commanding an estimated 54.2% of the market, versus the more competitive US sporting goods market, where the top 10 retailers represent approximately 40.6%. In addition, the sporting goods by retail channel in Canada differ from that of the US, with sport stores representing 65.4% of sales in Canada versus 51.2% in the US. Another striking difference between the two markets is the spend per capita on sporting goods, with the average Canadian spending 28% more annually at $240 versus the average American at $187. The higher spend per individual is most likely attributable to Canadians’ love for sports with higher capital intensity – specifically hockey, skiing, skating, and cycling. Exhibit 14 details the Canada versus US dynamic by channel and spend.

Exhibit 14: Canadian versus US Sporting Goods Distribution Channels

Source: Trendex North America, Raymond James Ltd.

With the August 2011 acquisition of the Forzani Group (FGL Sports), Canadian Tire emerged as the largest sporting goods retailer in Canada, commanding an approximate 31.5% of the sporting goods market. FGL Sports’ largest banner, Sport Chek, accounted for approximately 11.4% of the sporting goods market in Canada, followed by its Sports Experts banner at 4.3% at the end of 2012, both of which increased market share through 2014. The acquisition not only served to reinforce CTC’s leadership position within the Canadian sporting goods market, but to also stave off (or at a minimum materially delay) the entrance of US-based Dick’s Sporting Goods (which was rumoured to have been eyeing FGL as the preferred platform to build a Canadian footprint). Exhibit 15 details Sporting goods industry growth and FGL Sport market share growth.

Exhibit 15: FGL Market Share and Sporting Goods Industry Growth

Source: Forzani Group, Trendex North America, Statistics Canada, Raymond James Ltd.

Canada Research | Page 18 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

In addition to becoming the largest player in the sporting goods industry in Canada, FGL Sports was a complementary addition to the CTC family, with very minimal product overlap. When historically an FGL Sports store opened in the vicinity of a CTR store, the sales impact on CTR was (according to CTR management) negligible at 1%. Prior to the FGL Sports acquisition, CTR tended to play in price-driven entry level sport equipment categories, with very little to offer in terms of either sports apparel and footwear. The mix at FGL, with over 70% of revenues derived from softgoods and footwear (Exhibit 16), is essentially the opposite of CTR. In addition, FGL’s hardgoods offerings are tailored to the more serious athlete (higher price point, higher service expectation) as opposed to the typical recreational sport enthusiast at CTR. Exhibit 16 below highlights the complementary nature of the FGL Sports acquisition.

Exhibit 16: Comparison of Canadian Tire and FGL Sports, and FGL Sports’ Sales Mix

Source: Canadian Tire Corporation, Raymond James Ltd.

While CTR was historically strong in kid (recreational) and adult (recreational) segments, the offering struggled to resonate (due to its offering, experience, and location) with the critical 18-35 demographic. With FGL, it was essentially game on with CTC in the mall and finally able to target this demographic. Driving the appeal and brand resonance of FGL (and capitalizing on the halo effect for other CTC banners) is a critical element of CTC’s growth strategy. FGL Sports’ banners attract a relative young demographic (80% of Sport Chek’s customers are under the age of 40) and have above-average incomes.

CTR’s playing merchandize assortment now targets a wider range of sports enthusiasts and covers essentially all income and skill levels in the majority of key sports. We do believe that there remains an untapped opportunity for FGL (and by extension CTC) in the high (or rather higher end) of the cycling market, which continues to be serviced by the Independent Bike Dealer (IBD) network or brand-specific stores (TREK). While we think it a stretch for CTC to successfully retail the super-premium (Cervelo, Pinarello) end of the market, an opportunity exists in our opinion in premium brands (Cannondale, TREK). An increased share in this growing segment could necessarily be achieved in a number of ways. Exhibit 17 details the positioning of key players in the Canadian sporting goods market.

Exhibit 17: Canadian Sporting Goods Retail Positioning

Source: Trendex North America, Raymond James Ltd. (CTC banners marked in red)

Canadian Tire Corporation Canada Research | Page 19 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

The combination of the continuous update of retail store concepts, revamp of store aesthetics, and superior customer service, play a critical role in delivering a shopping environment that complements that of the products offered. In fact, FGL Sports only hires sports enthusiasts with thorough product knowledge. Additionally, it is necessary for retailers to cater to consumers’ constantly-evolving lifestyles and tastes. By way of illustration, sports apparel, including footwear and clothing, has become particularly fashionable over the last few years. Sport Chek stores, with their high proportion of athletic footwear, have been direct beneficiaries of this trend.

In May 2012, Canadian Tire announced an accelerated growth plan for FGL Sports, on the basis of three strategic pillars. The first pillar is the focus on strategic banners, with Sport Check as its super brand, and Atmosphere as its outdoor lifestyle banner. Sport Chek has been rolling out its new concept flagship stores across Canada, with the latest addition in Burnaby, B.C. The second pillar is the accelerated growth of FGL’s footprint, under which Sport Chek and Atmosphere will add approximately 50% more square feet to their existing footprint by 2017. The third pillar focuses on building customer connection and improving customer experiences.

As part of the accelerated growth plan, FGL Sports also embarked on a banner rationalization initiative, under which the number of banners were reduced to three main banners (with the latest acquisition of Pro Hockey Life the number of banners increased to four), and several underperforming banners were closed (e.g., Sports Mart and Athlete’s World). The August 2013 acquisition of Pro Hockey Life added 23 high-end specialty hockey stores to the FGL Sports umbrella. FGL’s Sports Experts banner (primarily located in Quebec) was unaffected by the restructuring. Exhibit 18, below, illustrates the evolution of FGL Sports’ banners.

Exhibit 18: Evolution of FGL Sports Banners

2010 2011 2012 2013 2014 2015E 2017E

Sport Chek 140 150 161 171 189 195 205

Sports Experts 72 70 72 72 73 74 76

Atmosphere 65 68 57 66 66 67 69

Pro Hockey Li fe - - - 23 14 14 14

L’Entrepôt du Hockey - - - - 9 9 9

Sport Mart 64 59 41 - - - -

Intersport 53 51 47 45 44 44 44

Hockey Experts 17 19 22 17 15 15 15

National 19 18 18 18 18 18 18

Athletes World 54 53 44 - - - -

Nevada Bob's Gol f 6 1 - - - - -

Fi tness Source 1 - 2 - - - -

S3 7 11 11 9 8 7 7

Tech Shop 3 - - - - - -

Other 15 15 - - - - -

Buying Members 18 19 20 - - - -

Total 534 534 495 421 436 443 457 Source: Forzani Group Ltd., Canadian Tire Corporation, Raymond James Ltd.

FGL will also invest in the creation of 12-14 HERO stores (and additional Sport Chek flagship stores) over the next several years. The HERO stores will incorporate the learnings from the existing flagship stores, in addition to ongoing digital enhancements, increased customization capabilities (e.g., personalized sneakers), and greater connection with the local community through event boards and mobile engagement.

The reality of how appealing the economics of the upgraded stores are is highlighted in the performance of the West Edmonton flagship store, which has seen a material 20% lift in average basket since its opening in January 2014. Exhibit 19 details FGL’s SSS performance through 2014.

Canada Research | Page 20 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 19: FGL Sports Same-store Sales Performance

Source: Canadian Tire Corporation, Raymond James Ltd.

In terms of the sporting goods market, sales growth has been muted relative to broader Retail sales. In 2014, the sporting goods industry is estimated to have grown 2.5% to $8.7 bln versus retail sales growth of 4.6%. Within the sporting goods market, the apparel and footwear segments are poised to see the fastest growth rate through 2017E.

According to estimates by Trendex North America, sales of sports apparel are expected to grow at an annual CAGR of 2.7%, followed by the sports footwear industry at a CAGR of 2.5%. Conversely, should sports participation rates for capital-intensive sports such as hockey and skiing continue to stagnate, sales of sports equipment are forecast to grow at a much slower 0.8% CAGR. CTC (through both CTR and FGL) is very actively involved in driving renewed growth in participation rates in sports (and key sports in particular). The key initiatives aimed at getting kids active are Canadian Tire Jumpstart, Active at School, and the announcement on Jan-23-13 that CTC had signed an 8-year deal as a premier partner of the Canadian Olympic Committee.

In addition, on Jan-23-13 CTC announced that it has inked a four-year partnership with the Canadian Paralympic Committee, a new partnership with Hockey Canada (including sponsorship of the World Juniors), the Canadian Soccer Association and Canada Snowboard. An expanded partnership with Alpine Canada was also announced, which compliments the recently announced partnership with Skate Canada.

Exhibit 20: Canadian Sporting Goods Market Outlook – 2012 through 2017E

Source: Trendex North America, Raymond James Ltd.

Canadian Tire Corporation Canada Research | Page 21 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Mark’s

Generational Shift Underway

Mark’s offers affordable industrial and casual apparel and accessories, and is one of the largest specialty retailers in Canada. The store network at the end of 2014 was 383 of which 348 were corporate stores (including 65 store-within-stores), and 35 were franchise stores. While Mark’s is generally associated with industrial wear, it also offers men and women’s business, casual, and active wear. In order to increase its appeal in the casual wear market, Canadian Tire launched a network refresh initiative, which included converting its Marks Work Wearhouse stores to Mark’s and offering an enhanced customer shopping experience with wider aisles, brighter interiors, interactive features in addition to revamped product assortment in its casual wear line.

Mark’s 2014 revenues were $1,122 mln (9.9% of CTC revenues). In pursuit of building out its brand, Mark’s key strategic initiatives since 2010 have been the rebranding of its stores, the expansion of Imagewear and the launch of improved e-commerce capabilities. The rebranding initiative involved new logos, taglines and an improved customer experience (underpinned by a new store format, improved product assortment, clear navigational signage, and wider and brighter aisles). The rebranding initiative saw Mark’s replacing Mark’s Work Wearhouse.

The end-game of the rebranding and store experience reset was to increase the appeal of the brand, such that it begins to resonate with a younger, more urban consumer in the 35-50 age group (as opposed to its current 50-year-old plus customer demographic). The tagline reset dovetailed with the rebranding, supporting both new marketing campaigns and the formation of a strategic partnership with Cineplex’s SCENE loyalty program, the membership base of which skews to young and urban (perhaps too young and too urban for Mark’s today, but invaluable in the longer term given the Scotiabank partnership). The average SCENE member is between the ages of 18 and 35, with the majority of the member base under 40.

Mark’s management has moved to capitalize on the SCENE partnership. As part of Mark’s Everything in Jeans campaign, SCENE members could earn 500 points with any jean purchase (the promotion ran through March-2015). The Everything in Jeans campaign kicked off on Aug-10-14, and drove double-digit jeans sales growth in the last two quarters of 2014 (jeans sales increased 38% in the August to October time frame). The campaign was the primary driver of Mark’s positive 4Q14 SSS growth surprise of 1.2% on a tough year ago comp of 5.2%. In addition, the growth of Mark’s assortment is being driven by National Brands, including, Helly Hansen, Merrell and Columbia (to name a few). While these brands resonate better with the target demographic, the challenge is to get the message to that demographic.

With the learnings from Sport Chek in mind, Canadian Tire has also been testing digital marketing at Mark’s. The increased digital prowess is best illustrated by a digital flyer that Mark’s ran for winter boots and jackets in response to an early snowstorm in September 2014 in Calgary. The flyer generated a comp sales increase of 403% on target items in the relevant market. On the heels of several successful pilots, Mark’s continues to ramp its digital marketing spend, and e-commerce capabilities, driving an expected lift in brand resonance. Exhibit 21 below details the evolution of Mark’s same-store sales performance overlaid with the strategic initiatives undertaken.

Exhibit 21: Mark’s Same-store Sales Performance

Source: Canadian Tire Corporation, Raymond James Ltd.

Canada Research | Page 22 of 48 Canadian Tire Corporation

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Petroleum

More Marketing than Margin Play

Canadian Tire Petroleum is one of Canada’s largest independent gasoline retailers, with 297 gas bar locations across the country. In the 5 years through 2014, Petroleum has opened 38 new gas bars, rebranded 20 competitor gas stations, and performed major rebuilds at 15 sites. The majority of the gas bar sites are located adjacent to a CTR store, which serves to drive increased traffic to these stores. Fuel is sourced from several Canadian suppliers, and all of the gas bars are operated by independent retailers.

While the Petroleum business is a traffic driver for CTR stores, it is not a material contributor to earnings, which given the vagaries (and volatility) of fuel retail is a positive for CTC. The fuel retail market is both price sensitive and highly competitive. Petroleum maintains tight controls over its cost structure and enters into long-term gasoline purchase agreements with integrated gasoline wholesalers. Petroleum also engages in a cross-marketing strategy with other Canadian Tire banners, in addition to cross-promotional activities with grocer(s).

The largest driver of profitability for Canadian Tire Petroleum is the margins of the attached convenience stores operations attached to the petroleum retail apron. The gross margin on gasoline of 7%-9% is significantly lower than on c-store sales of 30%-plus. As such, Petroleum continues to push sales of ancillary products and non-gasoline service offerings such as convenience store items and car washes.

Financial Services

Not All Credit Cards are Created Equal

The Financial Services segment or Canadian Tire Financial Services (CTFS), while a key driver of CTC’s profitability with a solid track record, has found driving growth relatively challenging in the 5 years through 2014. While Financial Services represents only 8.6% of total revenues, the segment generates much higher margins and, as such, accounts for approximately 39.3% of EBT. Canadian credit card purchase volumes increased by 7.9% to $387.4 bln in 2014, of which MasterCard represented approximately 31.7% (or $122.7 bln) according to Nilson data (VISA continues to dominate with an approximate 60.3% share). While based on purchase volumes, RBC with $77.7 bln would the largest issuer in Canada, applying the more widely used measure of Outstandings, TD is Canada’s largest card issuer. On total market Outstandings of $81.4 bln in 2014, TD’s market share was 19.5%. CTB’s market share, on Outstandings of $4.3 bln, was approximately 5.3% in 2014, ranking CTB as the eighth largest card issuer in Canada.

Through Canadian Tire Bank (CTB), the corporation has continued to strengthen its Canadian Tire branded credit card business, which now issues the co-branded (MasterCard) Options World Card and (MasterCard) Sport Chek card, in addition to expanded deferred and equal payment programs. On May-08-14, Canadian Tire announced that Financial Services has struck a strategic partnership deal with Scotiabank for a cash consideration of $500 mln. The agreement also includes a credit card funding facility, where Scotiabank will provide Financial Services with credit card receivable financing of up to $2.25 billion, and an option to sell an additional 29% of the portfolio to Scotiabank within the next 10 years, at fair market value. Scotiabank’s market share based on Outstandings of $11.7 bln was 13.9%, ranking it third behind TD and RBC.

As part of this transaction (which closed on Oct-01-14), CTC reorganized its Financial Services business by transferring substantially all of its domestic insurance, identity theft, and other optional products from CTFS to CTB. Scotiabank is now the exclusive partner for new financial products for CTB customers, such as mortgages, with both partners aggressively looking to monetize the opportunities for new products, services and improved customer loyalty (both Scotiabank and CTC are SCENE Loyalty partners) that the partnership is expected to generate. The SCENE Loyalty program is a good fit for Scotiabank and CTC, in our opinion, given who they bank today and the target demographic of tomorrow.

While the competitive intensity in the premium card market experienced a step-function change late in 2013, the competitive dynamics in the mass (or more specifically sub-prime as it relates to CTB) market were largely unchanged. We are not saying this market was not competitive, but rather that it was not subject to the same level of disruption as in the premium and super premium markets. We estimate (adjusted for the potential overlap in the Aerogold portfolio through the transition year that was 2014) that there were approximately 84 mln credit cards in circulation, of which CTB represents an estimated 4.2% or 3.5 mln cards (1.8 mln active accounts).

Canadian Tire Corporation Canada Research | Page 23 of 48

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2