canada’s competitive barrel: can canadian heavy barrels ... bbl competition_argus media … ·...

TRANSCRIPT

Canada’s Competitive Barrel: Can Canadian Heavy Barrels Compete in the

US Gulf?

Canadian Energy Research Institute

Dinara MillingtonCanadian Energy Research Institute

Argus Canadian Crude SummitMay 18-19, 2016

Relevant • Independent • Objectivewww.ceri.ca

Relevant • Independent • Objectivewww.ceri.ca2

Canadian Energy Research InstituteFounded in 1975, the Canadian Energy Research Institute (CERI) is an independent, non-profitresearch institute specializing in the analysis of energy economics and related environmentalpolicy issues in the energy production, transportation, and consumption sectors.

Our mission is to provide relevant, independent, and objective economic research of energyand environmental issues to benefit business, government, academia and the public.

Our core supporters include the Canadian Government (Natural Resources Canada), theGovernment of Alberta (Alberta Energy), and the Canadian Association of PetroleumProducers (CAPP), Chemistry Industry Association of Canada (CIAC), Alberta’s IndustrialHeartland Association (AIHA), and the University of Calgary. In-kind support is also providedby the Alberta Energy Regulator (AER) and Petroleum Services Association of Canada (PSAC).

All of CERI’s research is placed in the public domain and can be accessed via our website atwww.ceri.ca .

Relevant • Independent • Objectivewww.ceri.ca3

Agenda

• Crude Oil Prices: Canadian crude resiliency • Canadian Exports to the US• US Gulf Imports• Potential Netbacks for Canadian heavy

barrel producers

Relevant • Independent • Objectivewww.ceri.ca4

Crude Prices

Source: Argus Media

0.00

20.00

40.00

60.00

80.00

100.00

120.00

01 Ju

l 201

3

01 A

ug 2

013

01 S

ep 2

013

01 O

ct 2

013

01 N

ov 2

013

01 D

ec 2

013

01 Ja

n 20

14

01 F

eb 2

014

01 M

ar 2

014

01 A

pr 2

014

01 M

ay 2

014

01 Ju

n 20

14

01 Ju

l 201

4

01 A

ug 2

014

01 S

ep 2

014

01 O

ct 2

014

01 N

ov 2

014

01 D

ec 2

014

01 Ja

n 20

15

01 F

eb 2

015

01 M

ar 2

015

01 A

pr 2

015

01 M

ay 2

015

01 Ju

n 20

15

01 Ju

l 201

5

01 A

ug 2

015

01 S

ep 2

015

01 O

ct 2

015

01 N

ov 2

015

01 D

ec 2

015

01 Ja

n 20

16

01 F

eb 2

016

01 M

ar 2

016

01 A

pr 2

016

01 M

ay 2

016

(US$

/bbl

)

WTI month 1 - Exchange settlement Maya USGC - Houston close Castilla Blend - Houston close

Relevant • Independent • Objectivewww.ceri.ca5

Canadian Heavy Crude Exports to the US (2014-2015)

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

PADD I PADD II PADD III PADD IV PADD V

Thou

sand

bar

rels

per

day

Conventional Heavy Synthetic Bitumen and Blended Bitumen

East Coast Midwest US Gulf Coast Rocky Mountain West Coast

Source: National Energy Board

Relevant • Independent • Objectivewww.ceri.ca6

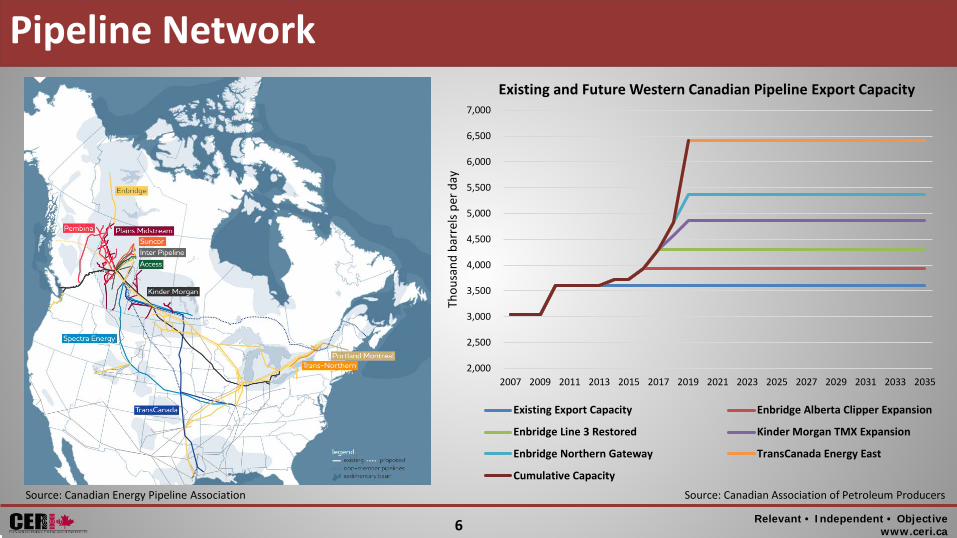

Pipeline Network

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

Thou

sand

bar

rels

per d

ay

Existing Export Capacity Enbridge Alberta Clipper Expansion

Enbridge Line 3 Restored Kinder Morgan TMX Expansion

Enbridge Northern Gateway TransCanada Energy East

Cumulative Capacity

Source: Canadian Energy Pipeline Association

Existing and Future Western Canadian Pipeline Export Capacity

Source: Canadian Association of Petroleum Producers

Relevant • Independent • Objectivewww.ceri.ca7

Rail Network

0

100

200

300

400

500

600

700

800

900

1,000

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

Thou

sand

bar

rels

per d

ay Future Rail Capacity Existing Rail Capacity

Source: Canadian Association of Petroleum Producers

Existing and Future Western Canadian Rail Export Capacity

Source: Canadian Association of Petroleum Producers

Relevant • Independent • Objectivewww.ceri.ca8

US Gulf Coast Refining Capacity

Source: US Energy Information Agency

Relevant • Independent • Objectivewww.ceri.ca9

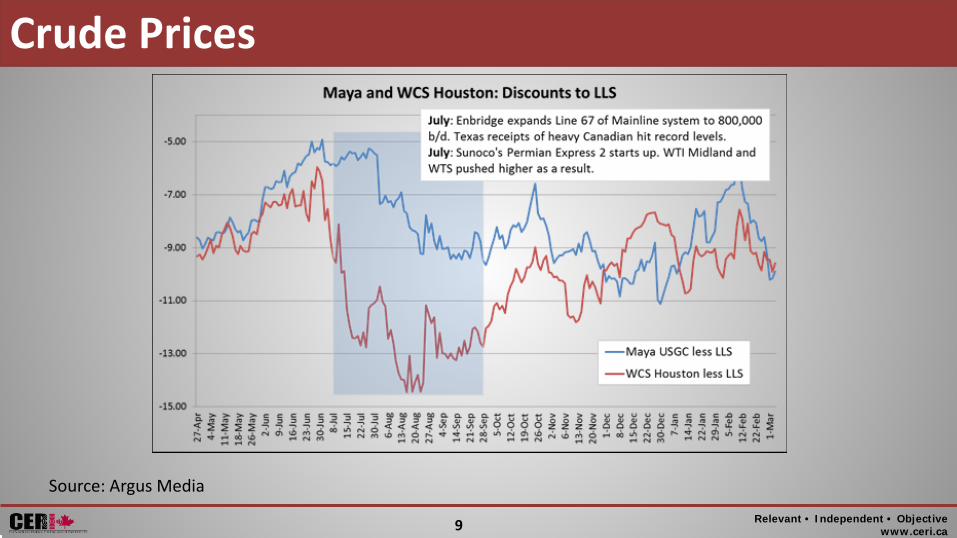

Crude Prices

Source: Argus Media

Relevant • Independent • Objectivewww.ceri.ca10

Crude Oil Quality

Source: BP, EIA, Genesis Capital, Oil &Gas Journal, Pemex, Statoil

Condensate BlendSuncor Synthetic A

Syncrude Synthertic

Western Candian SelectCold Lake Blend

Peace River Heavy

Wabasca Heavy

Albian Hvy. Syn.

Hibernia Blend

Monterey

Kern River

Mars

West Texas Intermediate

West Texas Sour

Alaska North Slope

Mexico - Maya

Venezuela -Merey

Venezuela - BCF-17Ecuador - Napo

Brazil - Marlim

Colombia - Castilla Blend

Brazil - PolvoColombia - Rubiales

Brent

Forties Blend

Algerian CondensateNigeria - Bonny Light

Kuwait - Kuwait

UAE - Dubai

Saudi Arabia - Arab Light

Iraq - Basra Light

Malaysia - TapisSumatra - Duri

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80

Sulfu

r Con

tent

wt.

% (Sw

eet -

> Sou

r)

API Gravity (Heavy -> Light)

Heavy Vs. Light

Sweet Vs. Sour

Canadian Crudes

US Crudes

Relevant • Independent • Objectivewww.ceri.ca11

US Gulf Coast Heavy Crude Imports

0

500

1,000

1,500

2,000

2,500

3,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Thou

sand

bar

rels

per d

ay

Canada Ecuador Brazil Colombia Venezuela Mexico

Source: US Energy Information Agency, 2015

Relevant • Independent • Objectivewww.ceri.ca12

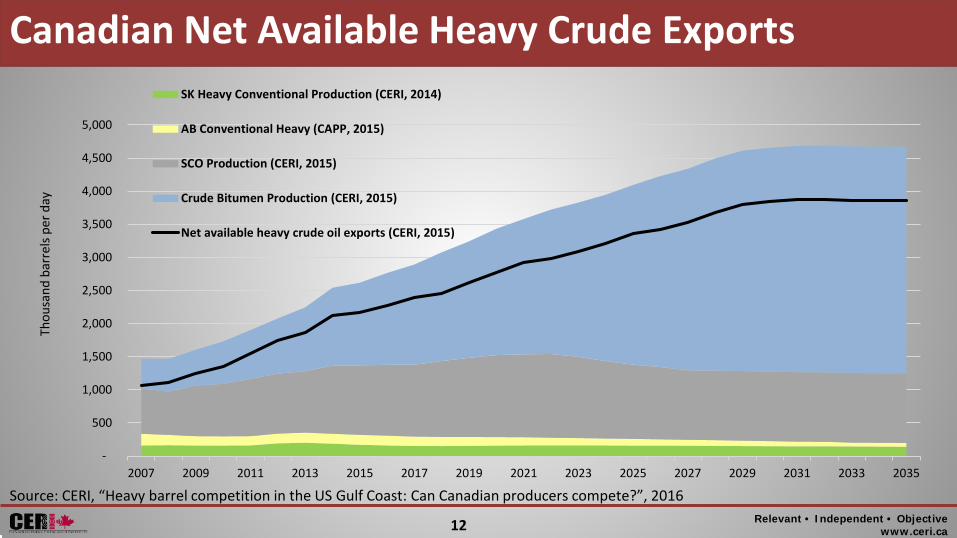

Canadian Net Available Heavy Crude Exports

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

Thou

sand

bar

rels

per d

ay

SK Heavy Conventional Production (CERI, 2014)

AB Conventional Heavy (CAPP, 2015)

SCO Production (CERI, 2015)

Crude Bitumen Production (CERI, 2015)

Net available heavy crude oil exports (CERI, 2015)

Source: CERI, “Heavy barrel competition in the US Gulf Coast: Can Canadian producers compete?”, 2016

Relevant • Independent • Objectivewww.ceri.ca13

Potential Heavy Crude Exports to the US Gulf Coast

-

200

400

600

800

1,000

1,200

1,400

1,600

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Thou

sand

bar

rels

per d

ay

Pipeline Capacity to the Gulf Coast Rail Capacity to the US Gulf Coast

Considering 50% capacity through EE & TMX Considering 75% capacity through EE & TMX

Considering 50% capacity through EE,TMX & NG Considering 75% capacity through EE,TMX & NG

No major coast export pipeline available

Source: CERI, “Heavy barrel competition in the US Gulf Coast: Can Canadian producers compete?”, 2016

Relevant • Independent • Objectivewww.ceri.ca14

Potential Netbacks for Canadian Heavy Barrel Producers

$30.43

$45.95

$8.79 $12.03

$15.50 $11.73 $12.50

$15.00

$13.02 $4.23 $0.99 $1.29 $0.52

$2.50

$-

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

WesternCanadian Select

@ Hardistry

Median HeavySour Crude

landed @USGC

USGC HeavySour Crude

QualityAdjustment

@USGC

WCS PriceUplift@USGC

(excludingtransportation

costs)

Pipeline(10-year

committed toll)

Pipeline(uncommited

tolls)

Rail Pipeline +Barge

Energy East +Tanker

TMX + Tanker

All values are 2015 average US$Source: CERI, “Heavy barrel competition in the US Gulf Coast: Can Canadian producers compete?”, 2016

Relevant • Independent • Objectivewww.ceri.ca15

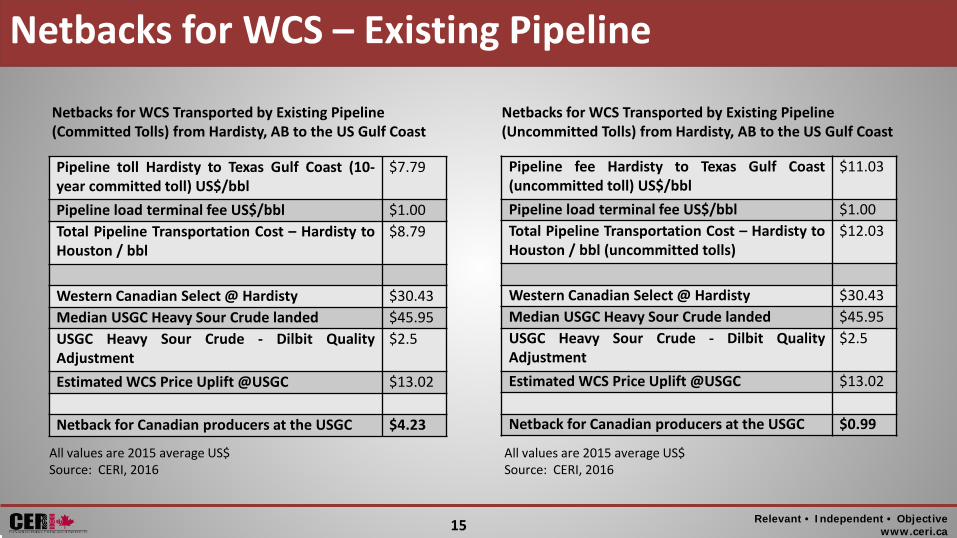

Pipeline toll Hardisty to Texas Gulf Coast (10-year committed toll) US$/bbl

$7.79

Pipeline load terminal fee US$/bbl $1.00Total Pipeline Transportation Cost – Hardisty toHouston / bbl

$8.79

Western Canadian Select @ Hardisty $30.43Median USGC Heavy Sour Crude landed $45.95USGC Heavy Sour Crude - Dilbit QualityAdjustment

$2.5

Estimated WCS Price Uplift @USGC $13.02

Netback for Canadian producers at the USGC $4.23

Netbacks for WCS Transported by Existing Pipeline (Committed Tolls) from Hardisty, AB to the US Gulf Coast

Pipeline fee Hardisty to Texas Gulf Coast(uncommitted toll) US$/bbl

$11.03

Pipeline load terminal fee US$/bbl $1.00Total Pipeline Transportation Cost – Hardisty toHouston / bbl (uncommitted tolls)

$12.03

Western Canadian Select @ Hardisty $30.43Median USGC Heavy Sour Crude landed $45.95USGC Heavy Sour Crude - Dilbit QualityAdjustment

$2.5

Estimated WCS Price Uplift @USGC $13.02

Netback for Canadian producers at the USGC $0.99

Netbacks for WCS Transported by Existing Pipeline (Uncommitted Tolls) from Hardisty, AB to the US Gulf Coast

Netbacks for WCS – Existing Pipeline

All values are 2015 average US$Source: CERI, 2016

All values are 2015 average US$Source: CERI, 2016

Relevant • Independent • Objectivewww.ceri.ca16

Netbacks for WCS Transported by Rail fromHardisty, AB to the US Gulf Coast

Netbacks for WCS – Existing Rail

Rail Tank Car (bbl) 600Rail Freight Hardisty to Texas Gulf Coast (HeavyCrude) US$/bbl Unit Train

$12.00

Rail Tank Car Lease / bbl ($600/month, 2 turns) $0.50Rail Car Load and Unload Terminal Fee / bbl ($1.50each)

$3.00

Total Rail Transportation Cost – Hardisty to Houston /bbl

$15.50

Western Canadian Select @ Hardisty $30.43Median USGC Heavy Sour Crude landed $45.95USGC Heavy Sour Crude - Dilbit Quality Adjustment $2.5

Estimated WCS Price Uplift @USGC $13.02

Netback for Canadian producers at the USGC $(-2.48)All values are 2015 average US$Source: CERI, 2016

Relevant • Independent • Objectivewww.ceri.ca17

Conclusions• Canadian heavy crude oil production is expected to grow from 2.6 MMbpd in 2015 to 4.7

MMbpd in 2035, more than a 2 MMbpd increase over the next twenty years.

• Canadian domestic demand for heavy crude oil is expected to increase by approximately50% and reach over 800,000 bpd by 2035.

• Net heavy Canadian available exports are expected to grow to volumes larger than 3.5MMbpd over the next decade.

• Heavy crude imports from Mexico and Venezuela have decreased by over 1 MMbpd overthe last 10 years.

• If Canadian heavies could displace most of the Mexican and Venezuelan imports, theopportunity for bitumen blends and heavy oil would be about 1.5 MMbpd.

Relevant • Independent • Objectivewww.ceri.ca18

Conclusions• Under current market conditions, rail access to the USGC would price Canadian producers

out of the market.

• Industry needs to consider how additional pipeline capacity can be developed, in order toconnect the Canadian heavy crude oil producers with US Gulf Coast.

• As Western Canadian crude oil production continues to grow, the leverage of theseresources for economic benefits to the nation will depend on the ability to connect thisgrowing supply with the demand.

• By allocating heavy production to other markets such as Asia and Europe, Canadianproducers are able to reduce their overland dependence on the US market, reduce theirsupply to that market, and overcome pipeline constraint issues on the US Gulf Coast.

Relevant • Independent • Objectivewww.ceri.ca19

Thank you!

www.ceri.ca