canfor corporation · pdf filecanfor corporation forward looking ... china • sichuan wood...

TRANSCRIPT

Canfor Corporation1

Canfor Corporation

June 2010

2Canfor Corporation

Forward Looking Statements

► The presentation and answers to questions today contain forward-looking statements which involve known and unknown risks, uncertainties and other factors that may cause actual results to be materially different from any future results, performance or achievements expressed or implied by such statements. Factors that could have a material impact on any future oriented statements made herein include, but are not limited to: general economic, market and business conditions, product selling prices, raw material and operating costs, foreign exchange rates, interest rates, changes in law and public policy, the outcome of trade disputes, and opportunities available to or pursued by the Company.

► For further details on these factors and our assumptions and applicable risks and uncertainties, please refer to Canfor Corporation’s Annual Report for the year ended December 31, 2009 available at www.canfor.com or www.sedar.com.

3Canfor Corporation

Canfor Overview► 15 sawmills in Canada

(Capacity – 4.3 Bfbm)

► 4 sawmills in the US(Capacity – 0.6 Bfbm)

► 50.2% interest in Canfor Pulp (3 BC interior pulp mills) (Capacity - 1 million admt)

Non Core Holdings► 50% interest in Peace Valley OSB plant ► 2 panel plants in BC – OSB & plywood ► 1 BCTMP pulp mill in BC ► 50% interest in Howe Sound Pulp LP

4Canfor Corporation

Canfor Overview2%

43%55%

LumberPulpUnallocated

20%

32%

48%LumberPulpUnallocated

0200400600800

1,0001,2001,4001,6001,8002,000

WFT CFP NBD CPLP IFP TMB

Market Capitalization (MM$) – at May 28/10

2009 Revenues ($2,100 million) 2009 Assets ($2,700 million)

5Canfor Corporation

The Downturn

► Reduced sawmill capacity to below 60%, idled OSB and plywood plants

► Reduced corporate and support staff levels by 25%

► Rolled back salaried staff wages 3-15%

► Rolled back contractor and supplier invoices by 10-15%

► Reduced peak working capital by approximately $100 million

► Reduced capital expenditures to minimal levels ($40 million)

0.0

0.5

1.0

1.5

2.0

2.5

J-04

M-04 M-04 J-04

S-04 N-04 J-05

M-05 M-05 J-05

S-05 N-05 J-06

M-06 M-06 J-06

S-06 N-06 J-07

M-07 M-07 J-07

S-07 N-07 J-08

M-08 M-08 J-08

S-08 N-08 J-09

M-09 M-09 J-09

S-09 N-09 J-10

M-10

0

50

100

150

200

250

300

350

400

450

500

US Housing Starts (millions) USD Lumber Price (right axis)

6Canfor Corporation

Improved Lumber Prices

(50)

(40)

(30)

(20)

(10)

0

10

20

Q1.09 Q2.09 Q3.09 Q4.09 Q1.10

Lumber EBITDA (MM$)

150

170

190

210

230

250

270

290

Q1.09 Q2.09 Q3.09 Q4.09 Q1.10 Current

SPF 2x4 (CAD)

Represents EBITDA adjusted for restructuring and inventory devaluation

7Canfor Corporation

Our Markets - Lumber

Market Focus► Grow high value customers

• Increase integration with US retail customers

• Key Asian customers

► Grow Asian markets

SPF

Offshore27%

Canada21%

US 52%

SPF88%

SYP 12%

SYP

Offshore1%

US 99%

Represents Q1 2010 volumes

8Canfor Corporation

U.S. Lumber Demand2009 – Repair & Remodelling - 40% of the total US Demand

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014

0

10

20

30

40

50

60

Single-Family Repair & Remod. Industrial Multifamily

Mobile Nonresid.Constr. US Consumption

Volume (Bfbm) Volume (Bfbm)

* Source - RISI(right axis)

9Canfor Corporation

Canfor’s Top 10 Global Customers

►Alpa Forest Products Inc.Pro Dealer

►Lowes CompaniesHome Center

►Millman Lumber CompanyPro Dealer

►Pro BuildPro Dealer

►Universal Forest ProductsHouse Components

►Home DepotHome Center

►LMCPro Dealer

►Mitsui Homes (Japan)Home Builder

►Stock Building SupplyPro Dealer

►Wing Corp (Japan)Industrial

These represent approximately 50% of total lumber revenues.

10Canfor Corporation

Developing Asia

► Japan• Further develop the DIY segment• Further develop Post & Beam / 2X4 hybrid market• Increase committed volumes to strategic customers

► China• Sichuan wood frame reconstruction• Infill partition walls, trusses / floor systems in concrete structures• Custom remanufacturing for Japan and other countries

► Korea• Increase market share of wood frame construction homes

Guangzhou, China

11Canfor Corporation

China

► Long term commitment to China

► Building codes are more conducive to wood frame construction

► Establishing 2 X 4 for the emerging housing sector

► Significant demand for low grade product

► Provincial and Federal government support for market development

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010F

Low Grade #2 & better

Lumber Volume - MMfbm

12Canfor Corporation

Margin FocusedMargin (% of Sales) – Lumber Segment

(25%)(20%)(15%)(10%)(5%)

0%5%

10%15%20%25%30%

Q4/

03

Q1/

04

Q2/

04

Q3/

04

Q4/

04

Q1/

05

Q2/

05

Q3/

05

Q4/

05

Q1/

06

Q2/

06

Q3/

06

Q4/

06

Q1/

07

Q2/

07

Q3/

07

Q1/

08

Q2/

08

Q3/

08

Q4/

08

Q1/

09

Q2/

09

Q3/

09

Q4/

09

Q1/

10

Canfor Competitor A Competitor B Competitor C Competitor D Competitor E

13Canfor Corporation

BC Interior Annual Allowable Cut

Source: Ministry of Forests

0

10

20

30

40

50

60

Historical 2006-2010 2011-2015 2016-2020

(millions of cubic metres)

14Canfor Corporation

BC Fibre Outlook – Production Capacity

Capacity = 1,200Mfbm

Capacity = 1,200Mfbm

Capacity = 1,400Mfbm

Capacity = 400Mfbm

0

20

40

60

80

100

2010 2020

Pine Spruce/Other Species

0

20

40

60

80

2010 2020

Pine Spruce/Other Species

0

20

40

60

80

2010 2020

Pine Spruce/Other Species

0

10

20

30

40

50

2010 2020

Pine Spruce/Other Species

15Canfor Corporation

Elements of a Lumber Supply Shortage

33European Imports

100%

78

8

10

60

78

2014F*

(2)(1)MPB/Canadian Cut Reduction

27

4

0

23

8

6

Change

7251Total Consumption (Bfbm)

94%73%Operating Rate

84Offshore

1010Canadian Consumption

5437US Consumption

7770Total Capacity (Bfbm)

6Capacity Growth (2.2%)

7070North American Capacity

Normalized2010F(in billions of fbm)

* Sources: Capacity as per USDA; Consumption as per FEA (except 2014 Offshore), company estimates

Normalized assumes 1.5 million housing starts

16Canfor Corporation

Lumber Price/Operating RateForecast operating rate is high by historic standards…

Sources: FEA, RISI, Company estimates

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

$- $100 $200 $300 $400 $500 $600

CAD 2x4 Price

N.A

. Ope

ratin

g R

ate

FEA Forecast (2010-2014)

1992-2009 Actual

Including Export Growth

2010

20142013

2012

2011

17Canfor Corporation

Capital Expenditures

► 2010 projected capital spend of $115 million:

Maintenance capital - $25 million

► 2011+ projected capital spend - $125 million annually

Mill modernization and reductions of fossil fuel usage

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010E 2011E

Capital Expenditures (MM$)

18Canfor Corporation

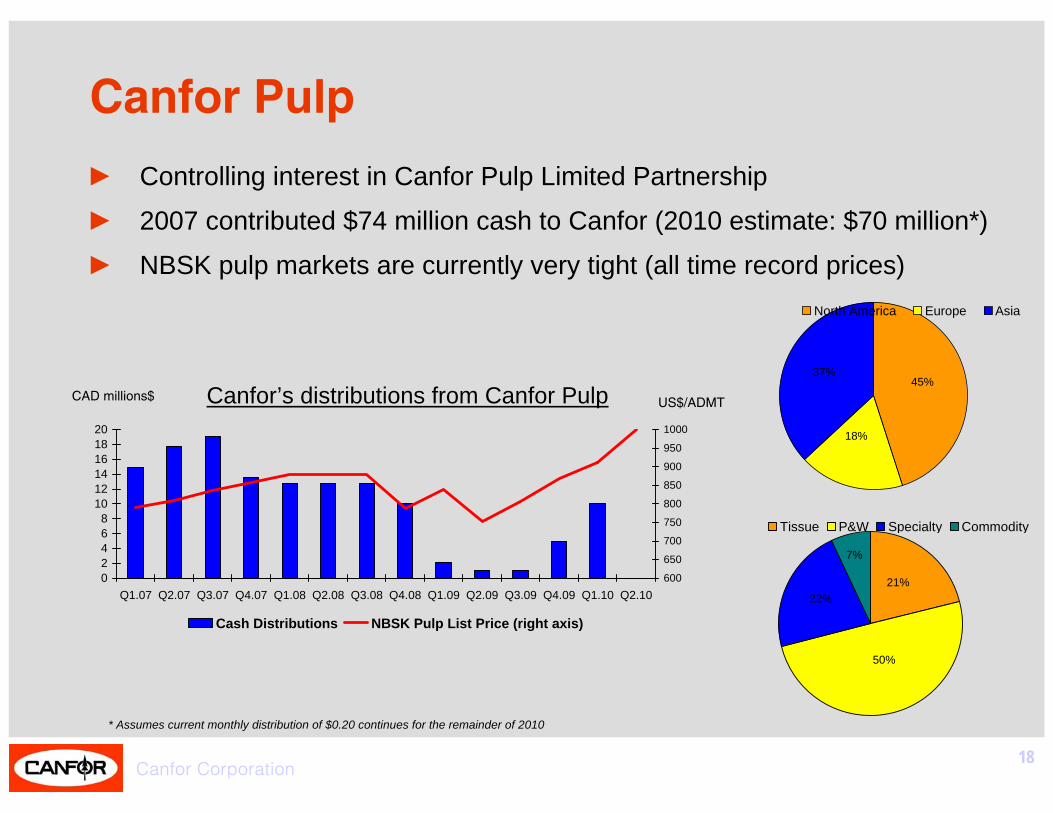

Canfor Pulp

► Controlling interest in Canfor Pulp Limited Partnership

► 2007 contributed $74 million cash to Canfor (2010 estimate: $70 million*)

► NBSK pulp markets are currently very tight (all time record prices)

02468

101214161820

Q1.07 Q2.07 Q3.07 Q4.07 Q1.08 Q2.08 Q3.08 Q4.08 Q1.09 Q2.09 Q3.09 Q4.09 Q1.10 Q2.10600

650

700

750

800

850

900

950

1000

Cash Distributions NBSK Pulp List Price (right axis)

Canfor’s distributions from Canfor PulpCAD millions$ US$/ADMT

37%

18%

45%

North America Europe Asia

7%

22%21%

50%

Tissue P&W Specialty Commodity

* Assumes current monthly distribution of $0.20 continues for the remainder of 2010

19Canfor Corporation

Leveraged to Lumber Market Recovery

0

100

200

300

400

500

600

700

800

2011 2012 2013

Current Production Full Capacity

$351$300RISI 2x4 (CAD) $275

201320122011

Change in EBITDA*(in millions $)

* Base year 2009

20Canfor Corporation

CFP Trading Liquidity

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010YTD

CFP WFT IFPAverage Daily Trading Volume

Source: Bloomberg

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

2006 2007 2008 2009 2010YTD

CFP WFT IFP

Average Daily Trading Value

Major Shareholders*The Pattison Group 31%

Mackenzie Cundill 15%

Jarislowsky Fraser 15%

* As per public filings

21Canfor Corporation

Canfor Corporation

TSX:CFP

www.canfor.com

Contacts:Thomas Sitar – VP Finance and CFO

604 661 [email protected]

Patrick Elliott – Treasurer604 661 5441

22Canfor Corporation

Appendix

23Canfor Corporation

Historic North American Capacity and Consumption

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Capacity Consumption

Source: USDA

Peak to Trough Annual Growth Rate: 2.2%

BFBM

CapacityBC Capacity - 15.8 Bfbm (22% vs. peak of 24%)Non-BC Canadian Capacity - 14.7 Bfbm (21% vs. peak of 25%)

ConsumptionOffshore Shipments - 3.7 Bfbm (8% of total)Projected Offshore Shipments - 7.7 Bfbm (11% of total compared to 4% in last peak)

24Canfor Corporation

US Housing Starts – What is Normalized Demand?

0.0

0.5

1.0

1.5

2.0

2.5

1970's 1980's 1990's 2000's

Household Formations House Removals Other

Source: RISI

Current HousingStarts Level

25Canfor Corporation

Impact of Normalized Housing Demand

12.421.99.5Total Consumption (Bfbm)

-6.356.35Board feet per Sq. Foot

-2,3002,300Square Feet per House

8501,500650Housing Starts (000’s)

ChangeNormalizedCurrent

Note: Increase to normalized level assumes all new starts are single family. At the peak another 3 Bfbm of consumption in multi-family and mobile home applications.

26Canfor Corporation

Capitalization and Liquidity (as at March 31, 2010)

Canfor Corp. Debt $ Millions

Senior Unsecured Notes 8.03% 2011 32

Senior Unsecured Notes 6.18% 2011 50

Senior Unsecured Notes 6.33% 2012 50

Senior Unsecured Notes 5.42% 2013 75

Total 207

Cash 53

Shareholders’ Equity 1,398

Net Debt to Total Capitalization 10%

Liquidity $ Millions

Syndicated operating facility 2011 355

Operating facility “A” & “B” 2011/12 49

Outstanding Letters of Credit (18)

Cash balance 53

Net Liquidity 439

(35)

(25)

(15)

(5)

5

15

2004 2005 2006 2007 2008 2009

Net Debt to Total Capitalization

All information below excludes CPLP