capital budgeting...sanjay saraf sir page 4 capital budgeting – challenger series question 2 the...

TRANSCRIPT

CHALLENGER SERIES

Capital

Budgeting

FOR

CA FINAL OLD SYLLABUS

CA INTER NEW

AND

OLD SYLLABUS

SANJAY SARAF SIR

Sanjay Saraf Sir Page 1

Capital Budgeting – Challenger Series

Question 1 :

A multinational company is planning to set up a subsidiary company in India (where hitherto

it was exporting) in view of growing demand for its product and competition from

other MNCs. The initial project cost (consisting of Plant and Machinery including installation)

is estimated to be US$ 500 million. The net working capital requirements are estimated at

US$ 50 million. The company follows straight line method of depreciation. Presently, the

company is exporting two million units every year at a unit price of US$ 80, its variable

cost per unit being US$ 40.

The Chief Financial Officer has estimated the following operating cost and other data in

respect of proposed project:

i. Variable operating cost will be US $ 20 per unit of production;

ii. Additional cash fixed cost will be US $ 30 million p.a. and project's share of allocated

fixed cost will be US $ 3 million p.a. based on principle of ability to share;

iii. Production capacity of the proposed project in India will be 5 million units;

iv. Expected useful life of the proposed plant is five years with no salvage value;

v. Existing working capital investment for production & sale of two million units through

exports was US $ 15 million;

vi. Export of the product in the coming year will decrease to 1.5 million units in case the

company does not open subsidiary company in India, in view of the presence of

competing MNCs that are in the process of setting up their subsidiaries in India;

vii. Applicable Corporate Income Tax rate is 35%, and

viii. Required rate of return for such project is 12%.

Calculate the Net Present Value (NPV) of the proposed project in India, assuming that:

a. there will be no variation in the exchange rate of two currencies and

b. all profits will be repatriated, as there will be no withholding tax.

Present Value Interest Factors (PVIF) @ 12% for five years is as below:

Year 1 2 3 4 5

PVIF 0.8929 0.7972 0.7118 0.6355 0.5674

Sanjay Saraf Sir Page 2

Capital Budgeting – Challenger Series

Answer :

Financial Analysis whether to set up the manufacturing units in India or not may be carried

using NPV technique as follows:

i. Incremental Cash Outflows

$ Million

Cost of Plant and Machinery 500.00

Working Capital 50.00

Release of existing Working Capital (15.00)

535.00

ii. Incremental Cash Inflow after Tax (CFAT)

a. Generated by investment in India for 5 years

$ Million

Sales Revenue (5 Million x $80) 400.00 Less: Costs

Variable Cost (5 Million x $20) 100.00 Fixed Cost 30.00

Depreciation ($500Million/5) 100.00

EBIT 170.00 Taxes@35% 59.50

EAT 110.50 Add: Depreciation 100.00

CFAT (1-5 years) 210.50 Cash flow at the end of the 5 years (Release of Working Capital) 35.00

b. Cash generation by exports

$ Million

Sales Revenue (1.5 Million x $80) 120.00

Less: Variable Cost (1.5 Million x $40) 60.00

Contribution before tax 60.00

Tax@35% 21.00

CFAT (1-5 years) 39.00

c. Additional CFAT attributable to Foreign Investment

$ Million

Through setting up subsidiary in India 210.50

Through Exports in India 39.00

CFAT (1-5 years) 171.50

Sanjay Saraf Sir Page 3

Capital Budgeting – Challenger Series

iii. Determination of NPV

Year CFAT ($ Million) PVF@12% PV($ Million) 1-5 171.50 3.6048 618.2232

5 35 0.5674 19.8590

638.0822 Less: Initial Outflow 535.0000

103.0822

Since NPV is positive the proposal should be accepted.

Sanjay Saraf Sir Page 4

Capital Budgeting – Challenger Series

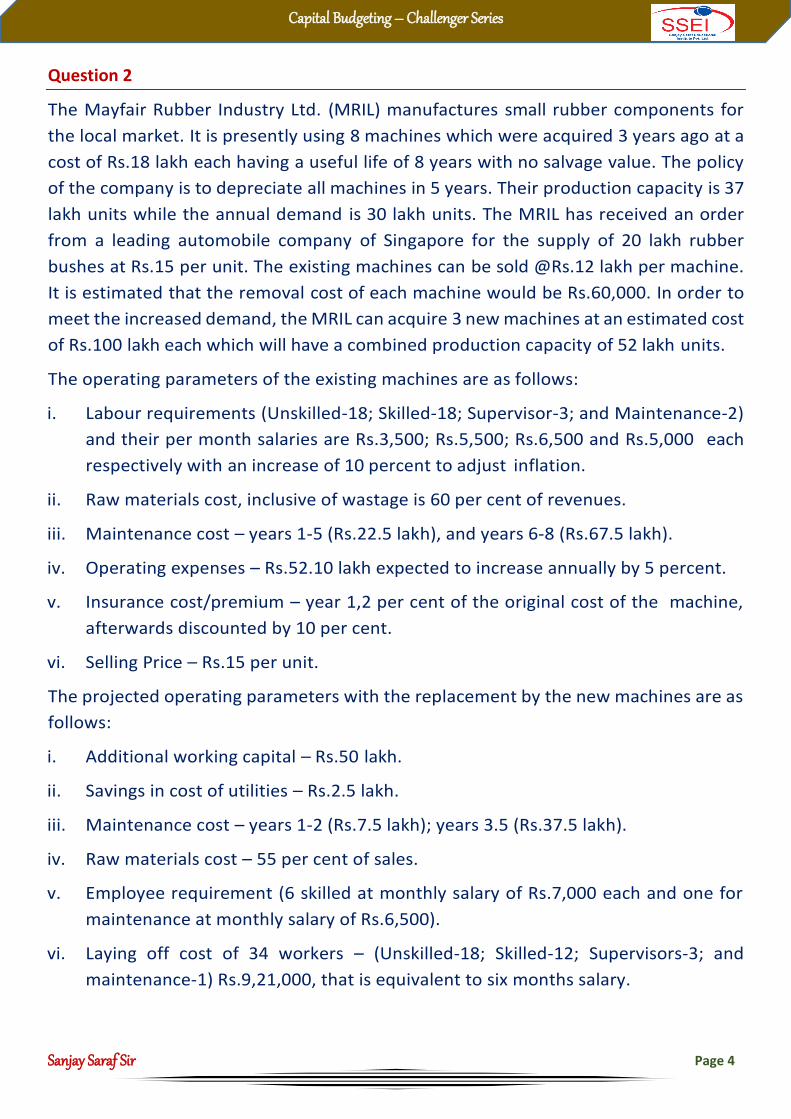

Question 2

The Mayfair Rubber Industry Ltd. (MRIL) manufactures small rubber components for

the local market. It is presently using 8 machines which were acquired 3 years ago at a

cost of Rs.18 lakh each having a useful life of 8 years with no salvage value. The policy

of the company is to depreciate all machines in 5 years. Their production capacity is 37

lakh units while the annual demand is 30 lakh units. The MRIL has received an order

from a leading automobile company of Singapore for the supply of 20 lakh rubber

bushes at Rs.15 per unit. The existing machines can be sold @Rs.12 lakh per machine.

It is estimated that the removal cost of each machine would be Rs.60,000. In order to

meet the increased demand, the MRIL can acquire 3 new machines at an estimated cost

of Rs.100 lakh each which will have a combined production capacity of 52 lakh units.

The operating parameters of the existing machines are as follows:

i. Labour requirements (Unskilled-18; Skilled-18; Supervisor-3; and Maintenance-2)

and their per month salaries are Rs.3,500; Rs.5,500; Rs.6,500 and Rs.5,000 each

respectively with an increase of 10 percent to adjust inflation.

ii. Raw materials cost, inclusive of wastage is 60 per cent of revenues.

iii. Maintenance cost – years 1-5 (Rs.22.5 lakh), and years 6-8 (Rs.67.5 lakh).

iv. Operating expenses – Rs.52.10 lakh expected to increase annually by 5 percent.

v. Insurance cost/premium – year 1,2 per cent of the original cost of the machine,

afterwards discounted by 10 per cent.

vi. Selling Price – Rs.15 per unit.

The projected operating parameters with the replacement by the new machines are as

follows:

i. Additional working capital – Rs.50 lakh.

ii. Savings in cost of utilities – Rs.2.5 lakh.

iii. Maintenance cost – years 1-2 (Rs.7.5 lakh); years 3.5 (Rs.37.5 lakh).

iv. Raw materials cost – 55 per cent of sales.

v. Employee requirement (6 skilled at monthly salary of Rs.7,000 each and one for

maintenance at monthly salary of Rs.6,500).

vi. Laying off cost of 34 workers – (Unskilled-18; Skilled-12; Supervisors-3; and

maintenance-1) Rs.9,21,000, that is equivalent to six months salary.

Sanjay Saraf Sir Page 5

Capital Budgeting – Challenger Series

vii. Insurance cost/premium-2 per cent of the Purchase cost of machine in the first

year and discounted by 10 percent in subsequent years.

viii. Life of machines – 5 years and salvage value – Rs.10 lakh per machine.

The company follows straight line method of depreciation and the same is accepted for

tax purposes. Corporate tax rate is 35 per cent and the cost of capital is 20 percent.

As the Finance Manager of MRIL, prepare a report for submission to the top

management with your recommendations about the financial viability of the

replacement of the existing machine.

Sanjay Saraf Sir Page 6

Capital Budgeting – Challenger Series

Answer :

Incremental CFAT and NPV

(Rs. in Lakhs)

Particulars 1 2 3 4 5

Sales 300 300 300 300 300

Add: Cost Savings:

Maintenance (note 2) 15 15 30 30 30

Cost of utilities 2.5 2.5 2.5 2.5 2.5

Labour Costs (note 3) 17.16 18.87 20.76 22.84 25.12

Less: Incremental cost

Raw materials (note 4) 142.5 142.5 142.5 142.5 142.5

Depreciation (note 5) 25.2 25.2 54 54 54

Insurance (note 6) 4.12 3.71 3.34 3 2.71

Earning before Tax 163.04 165.16 153.42 155.84 158.76

Less: Taxes (0.35) 57.064 57.806 53.607 54.544 55.426

Earning after taxes 105.976 107.354 99.723 101.296 102.934

CFAT (EAT + Depreciation) 130.976 132.354 153.723 155.296 156.934

Salvage Value 30

Release of working capital 50

(x) PV factor at .20 0.833 0.694 0.579 0.482 0.402

PV 109.10 91.85 89.01 74.85 95.25

Total present value (t = 1-5) 460.06

Less: cash Outflow 276.55

NPV 183.51

Comments: Since the NPV is positive, replacement of the exiting machines is financially

viable.

FINANCIAL ANALYSIS WHETHER TO REPLACE THE EXISTION MACHINES (USING NPV

METHOD)

Incremental cash outflows:

Cost of 3 new machines (Rs.100 lakh × 3) 300,00,000

Additional working capital 50,00,000

Less:Sale proceeds of existing machines 96,00,000

Sanjay Saraf Sir Page 7

Capital Budgeting – Challenger Series

Add: Removal cost of existing machines 4,80,000

Tax on profit on sale of machine (working note1) 11,76,000

Cost of layng off 34 workers (Rs.921000 tax advantage @ .35 i.e. to Rs.3,22,350) 5,98,650

Incremental cash outflows 2,76,54,650

Working Notes

1. Tax on profit on sale of existing machine:

Sale proceeds of existing

machine: (8 × 12,00,000) 96,00,000

Less: Book value (Rs.18 lakh × 8 – Original Cost

accumulated depreciation 28.80 × 3)

57,60,000

Gross profit 38,40,000

Less: Removal Cost (60,000 × 8) 4,80,000

Net Profit 33,60,000

Tax rate 0.35

Taxes payable on profit 11,76,000

2. Saving in Maintenance cost:

(Rs. in lakhs)

Year 1 2 3 4 5

Old Machine 22.5 22.5 67.5 67.5 67.5

New Machine 7.5 7.5 37.5 37.5 37.5

Saving in cost 15 15 30 30 30

3. Savings in Labour cost:

Existing labour cost

Unskilled (18 × Rs.3,500 × 12 months) 7,56,000

Skilled (18 × Rs.5,500 × 12 months) 11,88,000

Supervisor (3 × Rs.6,500 × 12 months) 2,34,000

Maintenance (2 × Rs.5,000 × 12 months) 1,20,000

22,98,000

Proposed labor cost

Skilled (6 × Rs.7,000 × 12 months) 5,04,000

Maintenance (1 × Rs.6,500 × 12 months) 78,000

Cost savings 17,16,000

Savings in subsequent years will increase by 10%

Sanjay Saraf Sir Page 8

Capital Budgeting – Challenger Series

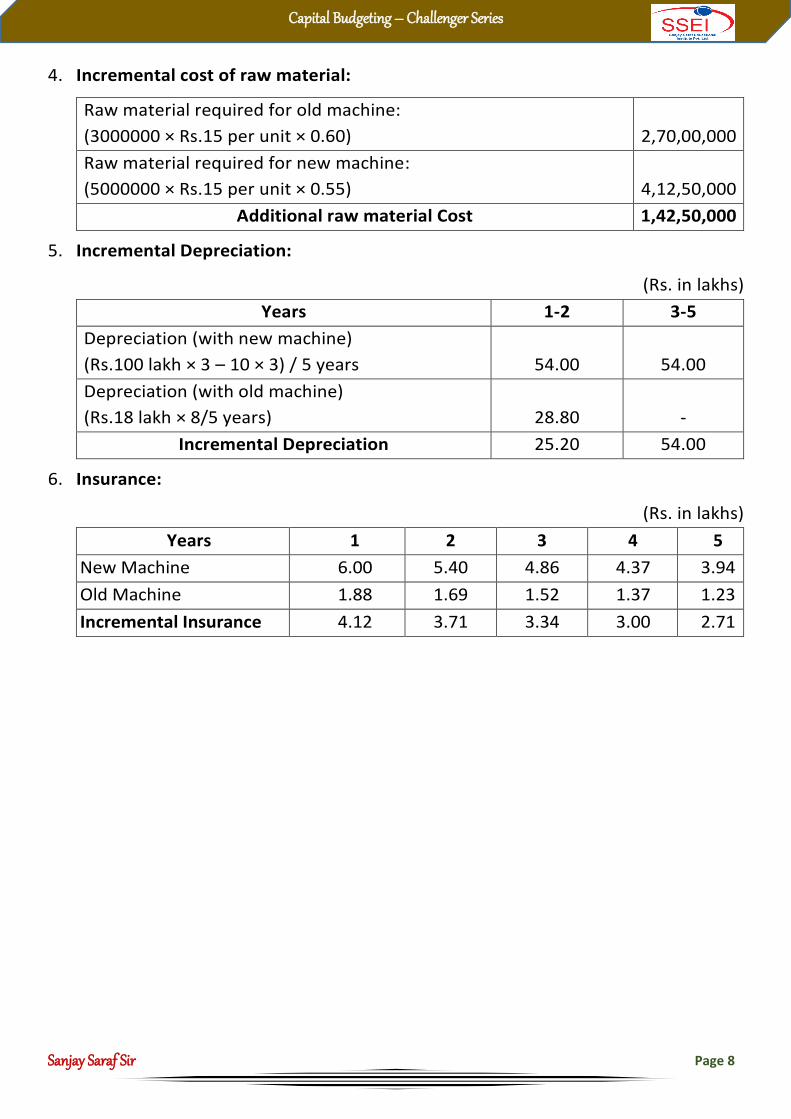

4. Incremental cost of raw material:

Raw material required for old machine:

(3000000 × Rs.15 per unit × 0.60)

2,70,00,000

Raw material required for new machine:

(5000000 × Rs.15 per unit × 0.55)

4,12,50,000

Additional raw material Cost 1,42,50,000

5. Incremental Depreciation:

(Rs. in lakhs)

Years 1-2 3-5

Depreciation (with new machine)

(Rs.100 lakh × 3 – 10 × 3) / 5 years

54.00

54.00

Depreciation (with old machine)

(Rs.18 lakh × 8/5 years)

28.80

-

Incremental Depreciation 25.20 54.00

6. Insurance:

(Rs. in lakhs)

Years 1 2 3 4 5

New Machine 6.00 5.40 4.86 4.37 3.94

Old Machine 1.88 1.69 1.52 1.37 1.23

Incremental Insurance 4.12 3.71 3.34 3.00 2.71

Sanjay Saraf Sir Page 9

Capital Budgeting – Challenger Series

Question 3

Jyoti Printers Pvt. Ltd. (JPPL) uses a printing machine which has a book value of Rs.5

lakh and a useful life of five years. It may be sold at present for Rs.4 lakh. After five

years the salvage value of the machine is expected to be Rs.1 lakh. The machine is

presently being depreciated on a straight line basis.

Pioneer Machine Tools Ltd. (PMTL) has recently offered to sell a new printing machine

to JPPL. The new machine will replace the old machine. The investment required on the

purchase and installation of the new machine is Rs.10 lakh. The new machine is

expected to reduce labour cost by Rs.50,000 per year and electricity costs by Rs.20,000

per year. Moreover, the new machine can also be productively used for other types of

printing works and it is expected to increase the profits by Rs.1,20,000 per year. After

five years the salvage value of the new machine is expected to be Rs.4 lakh. The new

machine will be depreciated on a straight line basis.

The cost of capital of JPPL is 12 percent. The tax rate applicable is 36 percent.

You are required to answer the following questions:

a. Derive the net cash flows associated with the replacement decision.

b. Appraise the replacement proposal using the net present value criterion and advise

accordingly.

Sanjay Saraf Sir Page 10

Capital Budgeting – Challenger Series

Answer :

a. The net cash flows associated with the replacement decision are given below:

(Rs. ‘000)

Year 0 1 2 3 4 5

A. Net investment (600)

B. Incremental cost savings (Rs.50,000 + Rs.20,000) 70 70 70 70 70

C. Incremental profits 120 120 120 120 120

D. Incremental depreciation1 40 40 40 40 40

E. Incremental pre-tax profits E = B + C – D 150 150 150 150 150

F. Taxes 54 54 54 54 54

G. Incremental post-tax profits 96 96 96 96 96

H. Initial flow (600)

I. Operating flow (G + D) 136 136 136 136 136

J. Terminal flow2 300

K. Net cash flow (H + I + J) (600) 136 136 136 136 436

Working notes:

1. Annual depreciation on old machine = 5,00,000 - 1,00,000

= Rs.80,000 5

Annual depreciation of new machine = 10,00,000 - 4,00,000

= Rs.1,20,000 5

Incremental depreciation per year on new machine

= 1,20,000 – 80,000 = Rs.40,000

2. Terminal flow = Incremental salvage value = 4,00,000 – 1,00,000 = Rs.3,00,000.

b. Net present value = 1,36,000 PVIFA (12%, 4) + 4,36,000 PVIF (12%,5) – 6,00,000

= 1,36,000 × 3.037 + 4,36,000 × 0.567 – 6,00,000 = Rs.60244

Since the NPV is positive the replacement should be done.

Sanjay Saraf Sir Page 11

Capital Budgeting – Challenger Series

Question 4

Modern Industries Ltd. (MIL) is considering to invest in a lathe machine. There are three

machines offered by three different manufacturers. The price quotations and

operational costs for the three machines are given below:

Manufacturers Western Engineering

Ltd. (WEL)

Jain Engineering

Ltd. (JEL)

Reddy Industries

Ltd. (RIL)

Cost of machine (Rs.) 8,00,000 12,00,000 18,00,000

Annual cost of

operations (Rs.) 1,60,000 1,20,000 1,00,000

Useful life (years) 5 8 10

The cost of capital for the company is 15%.

You are required to find out the machine that should be selected for investment by

MIL, using a suitable appraisal criterion.

Sanjay Saraf Sir Page 12

Capital Budgeting – Challenger Series

Answer :

Supplier: Western Engineering Ltd. (WEL)

Cost of the machine = Rs.8,00,000

Annual cost of operation = Rs.1,60,000

The present value of the annual cost of operation = Rs. 1,60,000 × PVIFA (15%, 5)

= Rs. 1,60,000 × 3.352

= Rs. 5,36,320

Hence the present value of costs = Rs. 8,00,000 + 5,36,320 = Rs.13,36,320

The annual capital change will be = 13,36,320

Rs.PVIFA(15%,5)

= 13,36,320

= Rs.3,98,663 (approx) 3.352

Supplier : Jain Engineering Ltd. (JEL)

Cost of the machine = Rs.12,00,000

Annual cost of operation = Rs. 1,20,000

The present value of the annual cost of operation = Rs. 1,20,000 × PVIFA (15%, 8years)

= Rs.1,20,000 × 4.487 = Rs.5,38,440

Hence, the present value of cost = Rs. 12,00,000 + Rs. 5,38,440 = Rs.17,38,440

The annual capital charge will be = 17,38,440

PVIFA(15%,8)

=Rs.17,38,440

Rs.3,87,439(approx)4.487

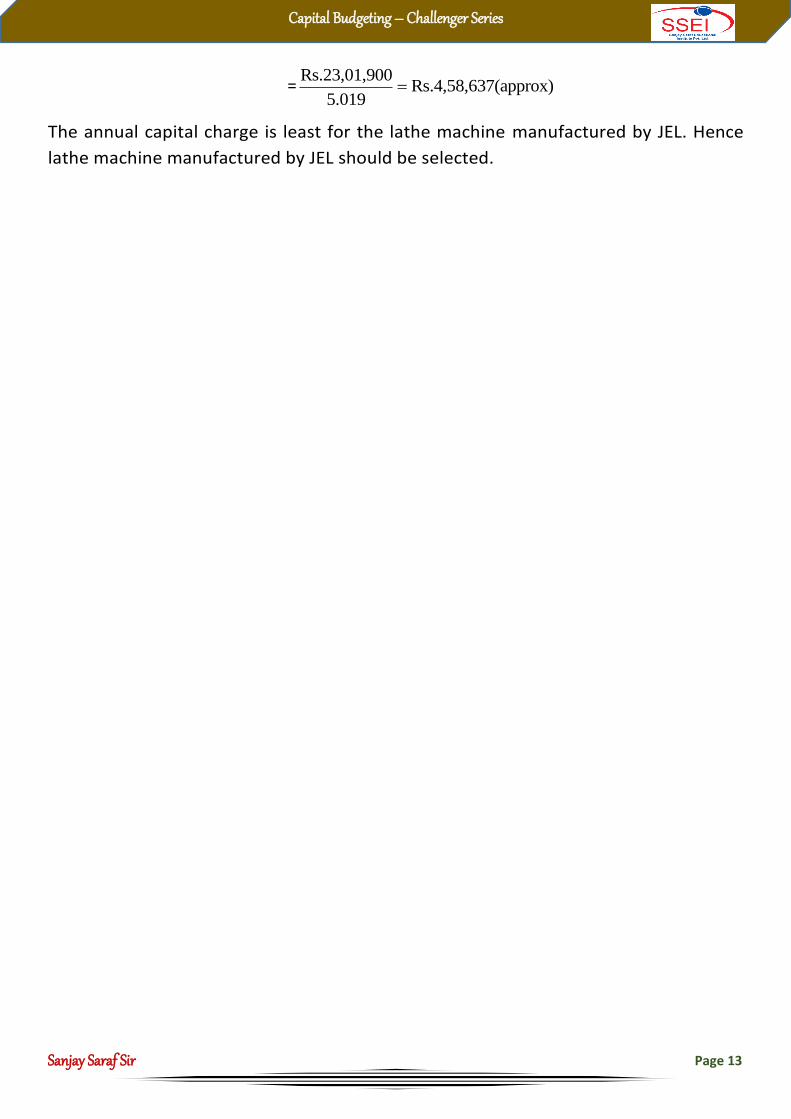

Supplier: Reddy Industries Ltd. (RIL)

Cost of the machine = Rs. 18,00,000

Annual cost of operation = Rs.1,00,000

The present value of the annual cost of operations = 1,00,000 × PVIFA (15%,10)

=1,00,000 × 5.019 = Rs. 5,01,900

Hence, the present value of Costs = 18,00,000 + 5,01,900 = 23,01,900

The annual capital charge = 23,01,900

PVIFA(15%,10)

Sanjay Saraf Sir Page 13

Capital Budgeting – Challenger Series

=Rs.23,01,900

Rs.4,58,637(approx)5.019

The annual capital charge is least for the lathe machine manufactured by JEL. Hence

lathe machine manufactured by JEL should be selected.

Sanjay Saraf Sir Page 14

Capital Budgeting – Challenger Series

Question 5

A large profit making company is considering the installation of a machine to process the

waste produced by one of its existing manufacturing process to be converted into a

marketable product. At present, the waste is removed by a contractor for disposal on

payment by the company of ` 150 lakh per annum for the next four years. The contract can

be terminated upon installation of the aforesaid machine on payment of a compensation of

` 90 lakh before the processing operation starts. This compensation is not allowed as

deduction for tax purposes.

The machine required for carrying out the processing will cost ` 600 lakh to be financed

by a loan repayable in 4 equal instalments commencing from end of the year 1. The

interest rate is 14% per annum. At the end of the 4th year, the machine can be sold for

` 60 lakh and the cost of dismantling and removal will be ` 45 lakh.

Sales and direct costs of the product emerging from waste processing for 4 years are estimated as under:

(` In lakh)

Year 1 2 3 4

Sales 966 966 1,254 1,254

Material consumption 90 120 255 255

Wages 225 225 255 300

Other expenses 120 135 162 210

Factory overheads 165 180 330 435

Depreciation (as per income tax rules) 150 114 84 63

Initial stock of materials required before commencement of the processing operations

is ` 60 lakh at the start of year 1. The stock levels of materials to be maintained at the

end of year 1, 2 and 3 will be ` 165 lakh and the stocks at the end of year 4 will be nil.

The storage of materials will utilise space which would otherwise have been rented out

for ` 30 lakh per annum. Labour costs include wages of 40 workers, whose transfer to

this process will reduce idle time payments of ` 45 lakh in the year - 1 and ` 30 lakh in

the year - 2. Factory overheads include apportionment of general factory overheads

except to the extent of insurance charges of ` 90 lakh per annum payable on this

venture. The company’s tax rate is 30%.

Present value factors for four years are as under:

Year 1 2 3 4

PV factors @14% 0.877 0.769 0.674 0.592

Advise the management on the desirability of installing the machine for processing the waste. All calculations should form part of the answer.

Sanjay Saraf Sir Page 15

Capital Budgeting – Challenger Series

Answer :

Statement of Operating Profit from processing of waste

(` in lakh)

Year 1 2 3 4

Sales :(A) 966 966 1,254 1,254

Material consumption 90 120 255 255

Wages 180 195 255 300

Other expenses 120 135 162 210

Factory overheads (insurance only) 90 90 90 90

Loss of rent on storage space (opportunity cost) 30 30 30 30

Interest @14% 84 63 42 21

Depreciation (as per income tax rules) 150 114 84 63

Total cost: (B) 744 747 918 969

Profit (C)=(A)-(B) 222 219 336 285

Tax (30%) 66.6 65.7 100.8 85.5

Profit after Tax (PAT) 155.4 153.3 235.2 199.5

Statement of Incremental Cash Flows

(` in lakh)

Year 0 1 2 3 4

Material stock (60) (105) - - 165

Compensation for contract (90) - - - -

Contract payment saved - 150 150 150 150

Tax on contract payment - (45) (45) (45) (45)

Incremental profit - 222 219 336 285

Depreciation added back - 150 114 84 63

Tax on profits - (66.6) (65.7) (100.8) (85.5)

Loan repayment - (150) (150) (150) (150)

Profit on sale of machinery (net) - - - - 15

Total incremental cash flows (150) 155.4 222.3 274.2 397.5

Present value factor 1.00 0.877 0.769 0.674 0.592

Present value of cash flows (150) 136.28 170.95 184.81 235.32

Net present value 577.36

Sanjay Saraf Sir Page 16

Capital Budgeting – Challenger Series

Advice: Since the net present value of cash flows is ` 577.36 lakh which is positive the

management should install the machine for processing the waste.

Notes:

i. Material stock increases are taken in cash flows.

ii. Idle time wages have also been considered.

iii. Apportioned factory overheads are not relevant only insurance charges of this

project are relevant.

iv. Interest calculated at 14% based on 4 equal instalments of loan repayment.

v. Sale of machinery- Net income after deducting removal expenses taken. Tax on

Capital gains ignored.

vi. Saving in contract payment and income tax thereon considered in the cash flows.