capital buffer and risk-taking in banks: islamic vs...

TRANSCRIPT

Capital Buffer and Risk-taking in Banks:

Islamic vs. Conventional Banks1

Eva Liljebloma, Sabur Mollahb2, and Omar Sikderc

aHanken School of Economics

Helsinki, Finland.

bStockholm Business School

Stockholm University, Sweden.

SE-10691, Stockholm, Sweden.

Email: [email protected]

cKungl Tekniska Högskolan

SE-100 44, Stockholm, Sweden.

Email: [email protected]

Abstract:

The Basel framework cannot address some specific risks inherent to Islamic banks’ activities, which go

beyond the traditional role of financial intermediation, due to dual banking systems in different countries

and difference composition of balance sheet of Islamic banks. This paper examines the difference in the

changes of capital buffer between Islamic and conventional banks and its endogenous relationship with

the difference in the changes of risk-taking behaviour between these two bank types. By employing

2SLS and 3SLS equations on a dataset of 701 banks for the period 2004-2013, we show that the

difference in the changes of capital buffer between IBs and CBs does not only influence the changes in

risk-taking between these banks, but also explains an endogenous relationship between changes in

capital buffer and the changes in risk-taking for these banks. Finally, the study underpins an important

policy implication for banks by examining buffer theory in a comparative framework.

1 We acknowledge financial support from JAK Medlemsbank, Sweden. 2 Corresponding Author: Sabur Mollah, Stockholm Business School, Sweden. Email:

Page 2 of 26

1. Introduction

Risk-taking behaviour in the inception of the recent global financial crisis renews the importance of

bank default and helps the regulators and shareholders pay attention to capital buffers3. However, capital

regulation is prioritized since the Basel accord has impelled aftermath of recent crisis (Basel III) with

more capital adjustment for controlling and absorbing shocks that evolves from financial and economic

stresses (Basel Committee on Banking Supervision (BCBS), 2011). However, European Central Bank

(ECB) capital requirement directive (2015) stresses that central banks have to review the capital buffer

requirements for world leading financial institutions due to the current risk appetite of financial system4.

Prior research stress that the cyclical behaviour of bank capital and risk adjustment is the major cause

for major banking crises (Chessen, 1987; Keeton, 1989; Avery and Berger, 1991; Berger, 1995; Jacques

and Nigro, 1997). As Tirole et al. (2010) demonstrate that, just before the recent crisis, substantial risks

are driven by transforming short-term borrowings into long-term loans in banks. However, highly

leveraged bank has the incentive to gamble at the cost creditors’ expense due to option features of bank

shares and hence, different risk apatite is influenced by market power and consequently make a bank

either winner or loser (Bebchuk and Spamann 2010).

Previous studies also observe that excessive risk-taking behaviour underpins financial crisis (Erkens et

al., 2012; Kirkpatrick, 2009; Sharfman, 2009). However, recent studies emphasize different structural

design between conventional banks (hereafter CBs) and Islamic banks (hereafter IBs). Thus, different

structural design between CBs and IBs cause different risk-taking behavior between these banks (Mollah

et al., 2016). Moreover, while CBs experience negative capital buffer due to its risk-taking behaviour

during crisis (Shim 2013), the IBs observe positive capital buffer (Hasan et al., 2015).

The main objective to adequate the capitalization level with risk exposure (Basel I to III) in order to

enhance the soundness of the banking industry around the world by protecting it from instability and

insolvency. However, the implementation of Basel faces challenges in some countries characterized by

the existence of a full-fledged Islamic banking system (like Iran) or a dual banking system (as the case

of the majority of Muslim countries and some non-Muslim countries). Indeed, the Basel framework,

namely Capital Adequacy Standard does not address some specific risks inherent to Islamic banks’

activities which go beyond the traditional role of financial intermediation. Due to the difference between

the composition of the balance sheet of Islamic banks and their conventional counterparts, the main

Islamic regulatory institutions, namely the Islamic Financial Services Board (IFSB) and the Accounting

3 See Shim J. (2013) and according to the failed bank list of the Federal Deposit Insurance Corporation

(FDIC), 414 banks have failed from January 2008 to December 2011, while only 27 banks failed between

October 2000 and December 2007. 4 ECB capital requirement directive Article 131. See https://www.eba.europa.eu/regulation-and-policy/single-

rulebook/interactive-single-rulebook/-/interactive-single-rulebook/article-id/298

Page 3 of 26

and Auditing Organization for Islamic Financial Institutions (AAOIFI) have devised appropriate capital

adequacy guidelines that take into account the specificity of the Islamic financial industry. The AAOIFI

proposal issued in March 1999 is based on Basel II with some modifications mainly the inclusion of the

assets financed by Profit-Sharing Investment Accounts (PSIA) in the calculation of the capital adequacy

ratio (CAR). The AAOIFI Standard maintains the same minimum CAR of 8%. The other proposal issued

by the IFSB in December 2005 tries to take into account the criticisms addressed to the AAOIFI proposal

by suggesting a new formula to compute the risk weighted assets. In this regard, Errico and Farahbaksh

(1998) note that Basel Committee on Banking Supervision (BCBS)’s adjusted recommendations have

relatively better impact on IBs. Archer, Karim and Sundararajan (2010) also stress that IBs mechanism

displaces commercial risks by reflection of their profit-sharing investment accounts (PSIA).

Nevertheless, a usual question arises whether there is any difference in capitalization between two bank

types (IBs vs. CBs). If any, does this difference explains the difference in risk-taking behaviour between

IBs and CBs?

The purpose of this paper is to examine the difference in the changes of capital buffer between IBs and

CBs and its endogenous relationship with the difference in the changes of risk-taking behaviour between

these two bank types. By using a dataset of 701 banks (123 IBs and 578 CBs) for the period 2004-2013,

we show that the difference in the changes of capital buffer between IBs and CBs does not only influence

the changes in risk-taking between these banks, but also explains an endogenous relationship between

changes in capital buffer and the changes in risk-taking for these banks. Our study differs from prior

research and contributes to the literature in a number of ways. First, to our knowledge, this is the first

comparative study to investigate the impact of the Islamic bank’s capital buffer and risk adjustments

between IBs and CBs. This paper looks into an important policy implication for banks by examining

buffer theory in a comparative framework. Jokipii et al. (2011) and Shim (2013) examine the

simultaneous relationship between capital buffer and risk-taking in the US context, whereas we look

into the simultaneous relationship in a comparative setting for global banks.

Second, as Shim (2013) provides an evidence that conventional banks have opposite relation between

capital buffers and default risks, that is, banks with lower default risks maintains higher capital buffers.

We complement Shim (2013) and other previous studies with regards to capital buffer and risk-taking

tendency (e.g. Tarazi et at., 2008; Stiroh and Rumble, 2006; Baele et al., 2004; Lepetit et al., 2008;

Stiroh, 2004; Ayuso et al., 2004; Crockett, 2001; and Gallo et al., 1996). These studies examine the

relationship between capital buffer and default risk for commercial banks and bank holding companies

(BHC), but our study includes commercial banks and bank holding companies (BHC) as well as IBs.

Third, our study sheds light on the simultaneous relationship between capital buffer risk-taking during,

pre, and post crisis periods. Since crisis is the fundamental element for both capital buffers and risk

Page 4 of 26

taking for banks. We split the sample into different economic cycles (e.g. pre, during, and post-crisis).

Our study underpins different behaviour for the simultaneous relationship between capital buffer risk-

taking among different sub-samples.

The rest of the paper is organized as follows. Section 2 outlines the theoretical motivation and

hypotheses development. Section 3 specifies the model applied and the description of the data used in

the paper. The empirical results are reported in section 4 and the concluding discussion remarks are in

section 5.

2. Previous Studies and hypothesis development

Regulators focus on banking capital structure to limit risk taking behaviour for securing financial

system. The literature emphasizes threshold of capital importance for controlling banks’ risk taking

behaviour. Unavoidable features of information asymmetries in banking industry at inappropriate

implementation of regulation gave banks to take excessive risks to maximize their benefits that

ultimately borne by deposit insurers and taxpayers (Dewatripont and Tirole 1994, 2010). Therefore,

Basel committee seldom propels the framework for stabilizing bank industry. In such a context, banking

risk taking behaviour depends on capital buffers. The literature of capital buffer and risk adjustment

practices were primarily examined on the European banks (Ayuso et al. (2004) and Heid et al. (2004))

and later on the US banks (Jokipii and Milne (2011) and Shim (2013)).

Sudrarajan (2005) explains that market force due to competition drives Islamic banks to arrange a

similar arrangement as conventional banks, but does not prevent Islamic banks their risks (Farook et

al., 2012). Cihak & Hesse (2007) demonstrate that profit-sharing arrangement in Islamic banks (IBs)

lowers credit risk and hence, some risk pass from bank to asset side. Mollah and Zaman (2015) and

Mollah et al. (2016) provide evidence that the governance structures under Shari’ah supervision of

Islamic banks help them undertake higher risks and achieve better performance. Hasan et al. (2015) and

Mollah et al. (2016) look into the effect of capital buffer on firm performance and value in Islamic banks.

In this connection, Archer el al. (2010) emphasize that displaced commercial risk resulted from

depositors’ profit-sharing investment accounts (PSIA) has exogenous effect on Islamic banks that is

insufficient to assess from bank perspective but rather to keep in supervisory inspection.

The literature often separates Islamic and conventional banks from addressing differences between

respective business models although they are significantly different (Beck et al. 2013). In principle, the

concept of Islamic financial products anchored in various religious scriptures (e.g. Qur’an, Bible and

Talmud). While conventional banks typically rely on time value returns of their leverage and capital,

the Islamic banks rely on more buy-sales products and services. In interest free profit-loss-risk sharing

arrangement, Islamic banks operate under the philosophy of depositor-bank-investor relationship. In

Page 5 of 26

general, depositors are the indirect investors who monitor Islamic banks as an ex-ante basis while

conventional banks borrow funds to pay interests independent to their returns (Hasan and Dridi, 2010).

Financial transactions in Islamic banks generate relatively better corporate governance with legitimate

profit and augmented economic social value (Mollah et al. 2016 and Siddiqi, 1999). Transparency

between buyer and seller contribute to address problems of adverse selection and moral hazard, but

Islamic banks operate equity-based financing and risk sharing where conventional banks engage in debt

financing and risk transference ((Beck et al., 2013; Hasan and Dridi, 2010).

Internal design of Islamic banks can be less vulnerable to risks as compared to conventional banks.

Likewise, depositors in Islamic banks invest via enriched Sharia-compliant channel while profit-loss

passes between traders and investors the bank intermediary serves provides another layer of protection

(Abedifar et al., 2013). In conventional banks, however, the obligation of predefined commitment of

interest payment, which is independent to their returns, put risks within the banks and may generate

information asymmetries as similar relationship happens with borrowers. At the same token, the profit-

loss sharing banking model generates gearing up trust between the clients and banks that stimulate

relationships among them that can minimize transaction costs. This relationship can minimize agency

conflicts through monitoring by depositors in ex-ante basis as a counter cycle protection layer rather

than government interventions. In consequence the risks can be bounded to business instead of to

security.

Islamic banks evolve mainly from safekeeping deposits and profit sharing investment accounts (Hasan

and Dridi, 2010) and from operations known as profit-loss sharing (Mudaraba) and nonprofit-loss

sharing (Murabaha and Ijara) (Khan and Ahmed 2001) as alternatives to time deposits, debt financing,

and lease financing in conventional banking, hence, Islamic banking products has been attracted by

major players, e.g. Citigroup, HSBC, Standard Chartered banks.

The banking operation, bank-clients relation vis-à-vis supervision of Islamic bank is significantly differs

from conventional banks. Specifically, the Sharia Supervisory Board (SSB) inspects each financial

transactions, contracts and future intermediary activities on the basis of Sharia (Hasan and Dridi 2010).

This supervision shields the banks as deposit insurance for equity-like investment (Warde, 2010,

Deloitte 2010). This requirement in Islamic bank limits negligence and misconduct for lesser operational

risks and difficulty in assessing liquidity put them to be more conservative. In additionally, the Islamic

banks traditionally keep relatively more capital reserves with central bank or in corresponding accounts

(Cihak and Hesse 2007, Ghosh 2014). However, empirical evidences show that more studies are needed

to decide whether higher capital encourage or dissuade risk-taking in Islamic banks and their strength

on the outreach of overall banking systems (Beck et al. 2013, Ghosh 2014). IBs have different

Page 6 of 26

mechanisms and corporate governance than CBs (see, e.g., Mollah and Zaman, 2015). This hypothesis

is never examined. Even if there exist any difference in between supervisory regulator for IBs and for

CBs, is there really any difference between IBs and CBs? Based on these arguments, we propose the

following hypothesis.

Hypothesis 1: Capital and risk taking in Islamic banks

𝐻01: The difference in capital buffer between Islamic and conventional banks does not distinguish risk

taking activities between these bank types.

A rejection of 𝐻01 implies the distinct properties in capital buffer of Islamic banks’ affect their risk

taking behaviour.

Sharia-compliant products prohibit excessive uncertain investment ‘gharar’. Higher performance is the

central to the excessive risk-taking. Safieddin (2009) noted that Sharia-compliant products and services

provide Islamic banks to form a unique structure because any exploitive contracts based on interest,

uncertain, excessive risky is not allowed in Islamic banking. Abedifar et al. (2013) exhibit that small

Islamic banks are more capitalized and are highly leveraged in Muslim majority countries while small

foreign and subsidiary CBs are highly leveraged in that countries. Prior research also stress that

religiosity impacts risk-taking behaviour of IBs (e.g. Miller and Hoffmann, 1995; Osoba, 2003; Hilary

and Hui, 2009; Abedifar et al., 2013). Based on the above discussions, we propose the following

hypothesis as follows.

Hypothesis 2: Risk taking and capital buffers in Islamic banks

𝐻02: The difference in risk taking behaviour between Islamic and conventional banks does not

distinguish the impact of capital buffer between these bank types.

A rejection of 𝐻02 implies risk taking mechanism in Islamic banks drive capital buffer. This notion also

indicates the governance structure in Islamic banks plays a crucial role in higher risk taking and

enhanced performance both for banks and clients that have impact to overall banking strong and better

withstand periods of stress, which is distinct from conventional banks (Mollah et al., 2016).

Shari’ah-compliant products of Islamic banks allow risk sharing and not risk transferring (Hasan and

Dridi 2010). Mollah et al. (2016) finds IBs governance structure enhance better risk-taking performance.

Risk sharing model in Islamic banking products improves relationship banking that can help banking

performance and in presence of appropriate Sharia Board (Alman 2012). On the other hand, due to fixed

interest in conventional banking and its risk transferring systems directs banks to vulnerable.

Page 7 of 26

Further, Basel III recognizes the importance of substantial improvement in banks’ overall stability.

During financial recession Islamic banks performed better than their counterparts in terms of credit and

asset growth (Hasan and Dridi 2010), higher intermediation ratio, asset quality, capitalization and better

performance in stock market (Beck et al. 2013). The current financial literature often separates the

statusability of conventional banks from Islamic banks. While the Sharia compliance induces capital

buffer and mitigates risk-taking in Islamic bank compares to the conventional banks. Thus, our study

extends the literature on Islamic banks’ capital-risk-security relation.

3. Data and Method

We use Bankscope’s database to form our primary sample from for all Islamic banks during the period

from 2004 to 2013. We explore for Islamic banks and filter them by keeping only those having codes

C1, C2, and C* because banks with these codes publish consolidated financial statements. We then filter

the remaining banks with an independence indicator defined by Bureau van Dijk (BvD) as equal to A

or B.7 Next, by following Beck et al. (2013), Mollah and Zaman (2015), and Mollah et al. (2016), we

filter the remaining banks based on three principles: (1) countries having both Islamic and conventional

banks; (2) countries with at least four banks; and (3) banks with at least 3 years of data. After the filtering

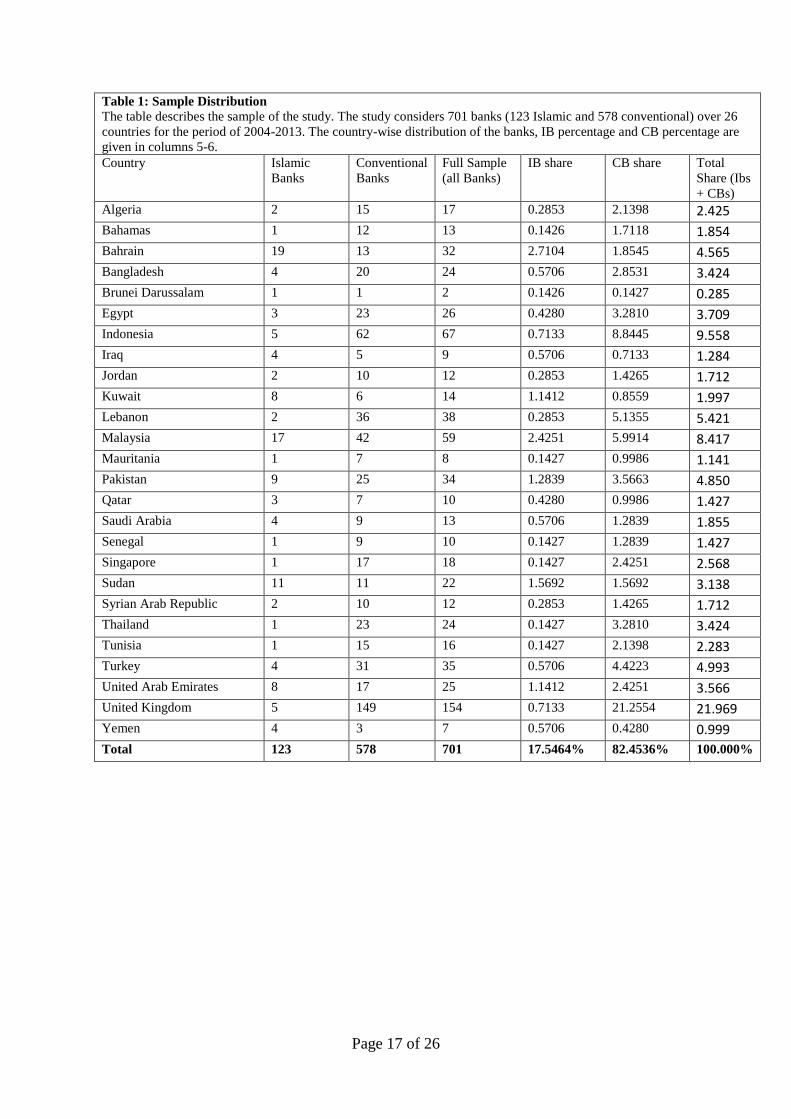

process, the final sample has 123 Islamic banks and 578 conventional banks in 26 countries. The banks

in our sample come from Algeria, Bahamas, Bahrain, Bangladesh, Brunei Darussalam, Egypt,

Indonesia, Iraq, Jordan, Kuwait, Lebanon, Malaysia, Mauritania, Pakistan, Qatar, Saudi Arabia,

Senegal, Singapore, Sudan, Syria, Thailand, Tunisia, Turkey, United Arab Emirates, United Kingdom

and Yemen. Table 1 reports the country-wise distribution of the sample. The final sample giving us 7010

bank-year observations in each sub-sample. The sample distribution is presented in following table and

figures.

[Insert Table 1 about here]

In the line with previous research of Shrieves and Dahl (1992), Jacques and Nigro (1997), Aggarwal

and Jacques (2001), Rime (2001), Jokipii and Milne (2011) and Shim (2013), our model, with

simultaneously determined variables, can be written as follows:

𝛥𝑏𝑢𝑓𝑖𝑡 = Δ𝑟𝑖𝑠𝑘𝑖𝑡𝑖𝑠𝑙𝑎𝑚𝑖𝑐 + 𝜖𝑖𝑡 .............. ................. ................. (1)

Δ𝑟𝑖𝑠𝑘𝑖𝑡 = Δ𝑏𝑢𝑓𝑖𝑡𝑖𝑠𝑙𝑎𝑚𝑖𝑐 + 𝜇𝑖𝑡 .............. ................. ................. (2)

where itbuf and itrisk are the observed changes in the capital buffer and risk, respectively.

Δ𝑏𝑢𝑓𝑖𝑡𝑖𝑠𝑙𝑎𝑚𝑖𝑐 and Δ𝑟𝑖𝑠𝑘𝑖𝑡

𝑖𝑠𝑙𝑎𝑚𝑖𝑐 are the changes in the capital buffer and risk that are managed internally

by the ‘Islamic’, 1 for IBs and 0 for CBs. it and it are the exogenously determined random shocks

Page 8 of 26

for bank i at time t.

3.2 Dependent and Explanatory variables

We have diagnosed for appropriate bank capital and risk-taking variables to test our hypotheses. After

adjusting minimum requirement, we defined our depended variable capital buffer (BUF) for Eq.(1). For

risk (RISK), we took well known insolvency risk proxy (Z-score) for Eq.(2) (see Pathan, 2009; Laeven

and Levine, 2009; Cihak and Hesse, 2010; Beltratti and Stulz, 2012; Beck et al. 2013; Abedifar et al.

2013; and Fu et al. 2014).

We also control for ROA, Bank supervisory, anti-director index, world-wide governance indicator

country-level governance (Kaufmann et al., 2009), and cross country differences. We include the

description of variables in Table 2.

[Insert Table 2 here]

3.3 Empirical Model

We use following models to test our hypotheses

∆𝑏𝑢𝑓𝑖,𝑡 = 𝛼0 + 𝛼1 ∗ 𝑖𝑠𝑙𝑎𝑚𝑖𝑐𝑖,𝑡 + 𝛽1 ∗ ∆𝑟𝑖𝑠𝑘𝑖,𝑡 + 𝛽2 ∗ 𝐵𝑆𝑖,𝑡 + 𝛾 ∗ 𝑋𝑖,𝑡 + 𝛿 ∗ 𝑀𝐸𝑖,𝑡 + 𝜖𝑖,𝑡 … … (3)

∆𝑟𝑖𝑠𝑘𝑖,𝑡 = 𝛼0 + 𝛼1 ∗ 𝑖𝑠𝑙𝑎𝑚𝑖𝑐𝑖,𝑡 + 𝛽1 ∗ ∆𝑏𝑢𝑓𝑖,𝑡 + 𝛽2 ∗ 𝐵𝑆𝑖,𝑡 + 𝛾 ∗ 𝑋𝑖,𝑡 + 𝛿 ∗ 𝑀𝐸𝑖,𝑡 + 𝜖𝑖,𝑡 … … (4)

We use the model to analyse the effect of (i) risk-taking (Δrisk), (ii) capital buffer (Δcap), and (iii)

relation for outcome impact between IBs and CBs through the simultaneous equations both two stage

and three stages. The choice of liquidity (NLTA), firm size (Log_TA), risk-taking (z) and country specific

variables GDP per capita (lnGDP_percapita), and an Islamic bank dummy (Islamic) are included in our

model. The description of the variables is elaborated in Table 2.

4. Empirical Findings

4.1) The determinants of Capital buffers and risks

Table 3 presents the regression results of simultaneous equations examining the determinants of capital

buffers and risk taking in IBs. With respect to 𝐻01, we find an insignificance positive relationship of

Islamic bank dummy with capital buffer and significance with negatively related to distance to default

indicating that IBs not only encourage high risk taking but also increase capital buffers. The results also

indicate that both capital buffer and distance to default are endogenously related because changes in

Page 9 of 26

distance to default is significantly positive to changes in capital buffer and vice versa. This finding is

consistent with prevailing literature for example, Ediz et al. (1998) UK banks and Rime (2001), Nocera

and Sironi (2007) for European banks and Berger (1995), Shrieves and Dahl (1992), while Jopikii and

Milne (2011) supports Shim (2013) for US banks.

Interestingly IB dummy interacts with distance to default indicating that secured operating systems in

IBs enhance capital buffers. On the other hand, the interaction between IB dummies and capital buffer

significantly mitigate risk taking. Specifically, both at firm level and country level the results indicate

IBs perform significantly lower default risks by 777.1%, 671.3% and 732.5%. These results reject 𝐻02.

[Insert Table 3 about here]

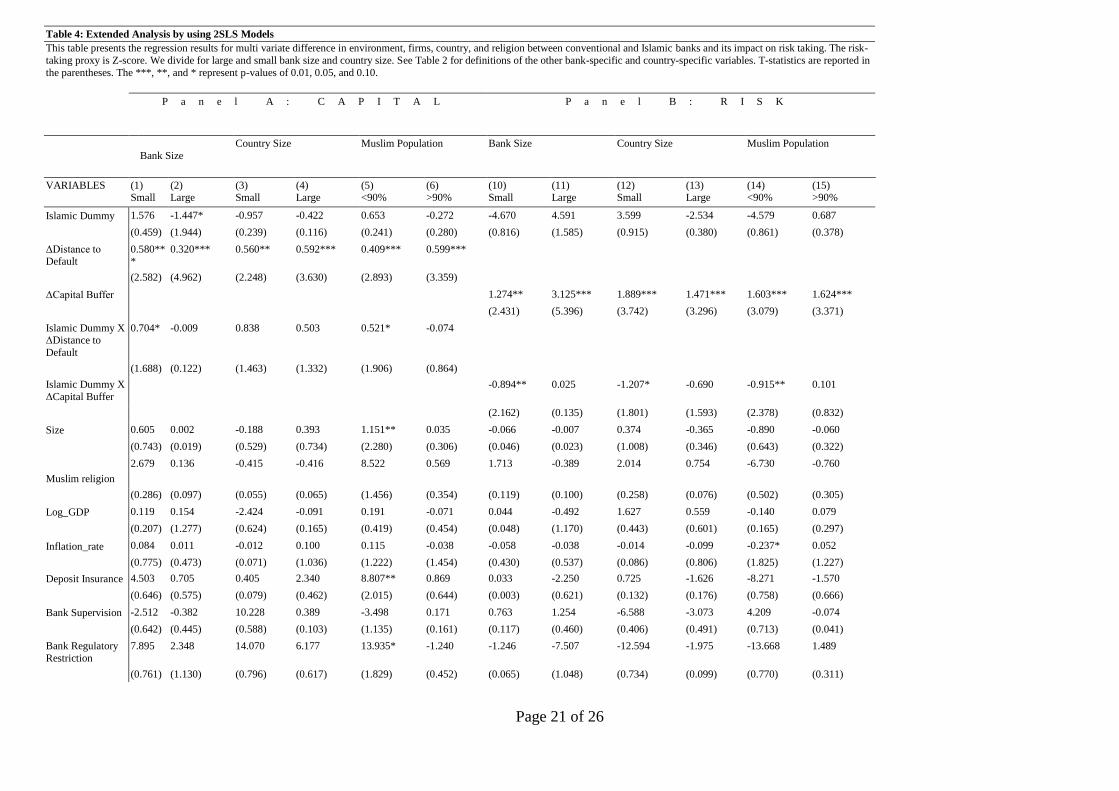

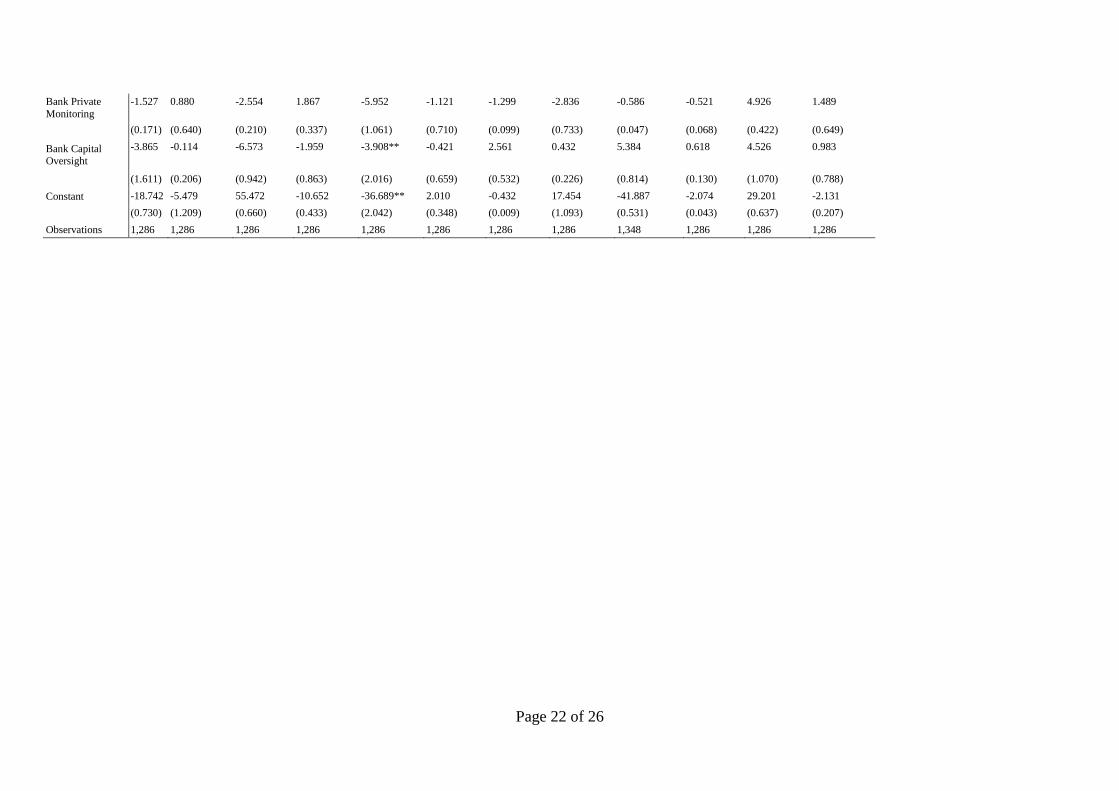

(i) Extended analysis and comparison

This section extends our base model to test how consistent the relationship of IBs between capital and

risk taking in different bank-level and country-level perspectives. Studies show that Islamic bank size

has negative impact on credit risk (Abedifar et al., 2013) and Mollah et al. (2016) finds only big IBs

are well equipped to keep risk taking under control. First, we review the results if bank size consistent

in explaining risk taking activities that determine banking capital. We find risk taking is negatively

related (in Panel A) with large IBs at insignificant level. However, the norm of significant dummy is in

model 2 and consistent with significant bank size in model 10. Second, in Panel B, for small economy,

according to model 12, we find risk taking shields the IBs’ client by enhancement safety of financial

structure. This may show the better corporate governance of Islamic banks’ impact noted in Mollah et

al. (2016) that ensures from more conservative operation as capital equation insignificant seen in model

3.

Third, in Table 4, for non-religiosity, capital index and intercept are negatively related in model 5 while

deposit insurance and restriction index are positively related in capital equation. The simultaneous risk

equation model 14 shows the notion differently as only consumer price index significant negatively

while deposit insurance display insignificance.

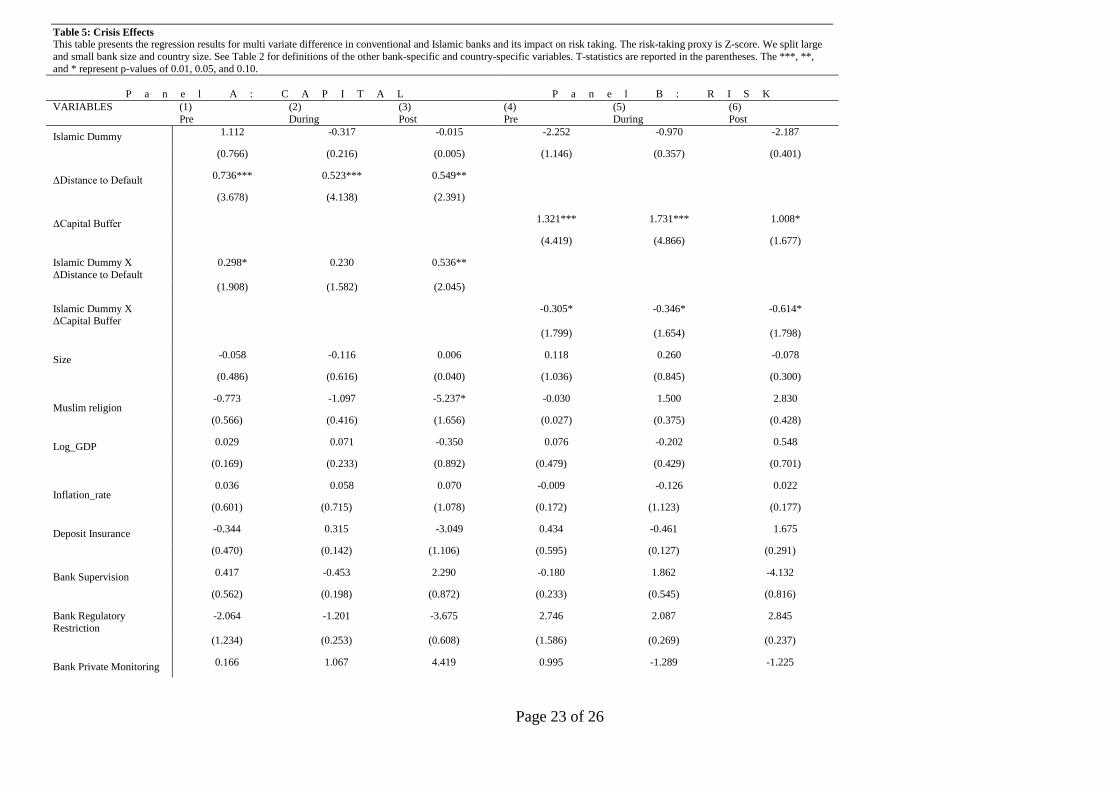

Finally, in Table 5, we examine the whole period impact on different economic situation: pre-crisis,

during-crisis and post-crisis. Here we find interesting result. The models 4, 5 and 6 provide consistent

evidence on risk taking tendencies in IBs are statistically strongly negative repeats our previous finding

in Table 3 that indicate that they reduce risk taking in response to their enhanced financial structure to

control risk adjustment at their desired level. In other words, Sharia-compliant product and services

direct risk taking behaviour to safeguard banking stability even in during financial stresses. The model

3 shows post-crisis capital is amplified at the cost of religiosity.

Page 10 of 26

Religiosity model 6 and 15 represent insignificant relationship for both equations in IBs. A similar

notion is explained in country size difference on models 3, 4 and 13. The small banks in non-religiosity

represents highest utility in both capital and risk models (1 and 14) in IBs.

[Insert Table 4 about here]

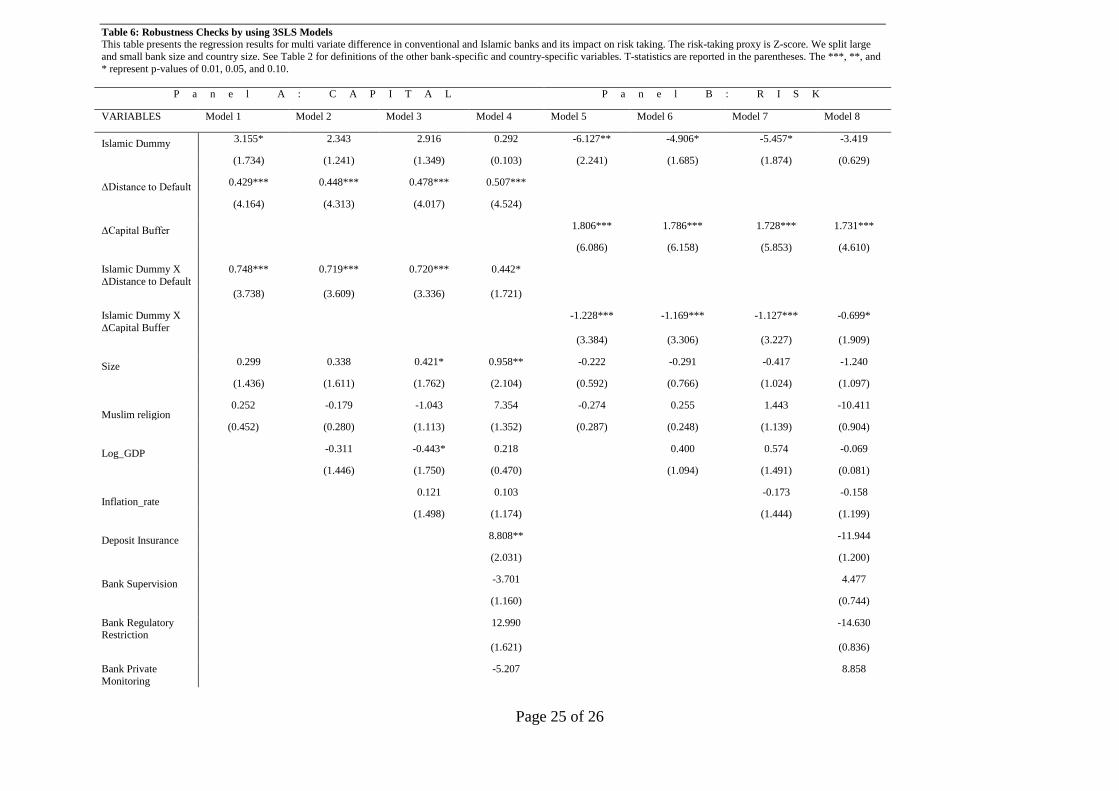

(ii) Robustness checks

The simultaneous framework is widely used in examining financial institutions’ capital and risk

decisions through 3SLS (Jacques and Nigro, 1997; Rime,2001; Shim, 2010). Wickens (1982) and Shim

(2013) notes that 3SLS estimation is asymptotically more efficient than 2SLS. The cross equation

correlation differs between the methods. We check the robustness to find any different results between

2SLS and 3SLS. We find the supporting results for the models.

[Insert Table 5 about here]

(iii) Additional analysis and discussion

We observe for capital (risk) equations insignificant results of large IBs negative (positive) and large

economy positive (negative) and with religiosity negative (positive). An economy with minor Muslim

religion reflects the most interesting interactions of supervisory and IBs’ behaviour (model 5). It shows

the highest coefficient in risk equation that may suggest the banks are top secured throw Sharia-

compliant products and services (model 14). Small IBs are relatively more efficient to adjust desired

risk level where both the bank and client is protected the most (model 1 and 10). Model comparison for

the whole period shows complete behaviour of IBs. During financial stress IBs risk taking was resilient

during crisis noted from insignificant determination of capital changes (in model 8) but significantly

and consistently have reduced bank default risks as seen in models 16, 17, 18.

Several authors noted religiosity of +90% Muslim countries being mostly risk averse clients in Islamic

banks (Miller and Hoffmann, 1995; Osoba, 2003; Hilary and Hui, 2009; Abedifar et al., 2013) model 6

and 15 supports the literature and we have extend the exploration if any other factor involve. In model

2 and 11 find such similarity for large Islamic banks. On the similar episode, the +90%GDP per capita

in models 4 and 13 reports the reverse intuition that imply clients are more sensitive in regards to Sharia-

compliant products and services. We find different results for -90%GDP per capita where risk

coefficient is significant in Islamic banks, possibly because clients in those countries are, on average,

more concerned about consequence of Sharia-compliant products and services. The results insignificant

(significant with negative sign) provides the ability to keep the risk adjustment at the desired level in

Islamic banks are relatively more successful than their counterparts. Finally, the significance Islamic-

dummy suggests banks those that have Sharia-compliant product and services would require 144.7%

lower capital changes.

Page 11 of 26

Beck et al. (2013) concluded IBs’ better asset quality and higher capitalized theoretical underpins to

expect for positive relation between capital and risk. We find this positive buffer relation that are

strongly significant with always more relative coefficients to determine risks in CBs. In IBs this

significance relation is always negative. Eventually, there evolves to evaluation between the banks

type’s theoretical frameworks deserves rethinking to understand the differences between the bank types.

5. Conclusion

The study aims to address Islamic bank different mechanism matters to enhance overall banking

services. Our empirical comparison suggests some similarity in Islamic and conventional banks in

capital buffer, but displays an opposite picture in case of risk-taking behaviour. This helps us to

understand risk taking and consequence as well as different bank structure between conventional and

Islamic banks. The practical lesson is IBs takes excessive risks that interacts with their capital and in

consequence significantly mitigate risk taking. We explore for risk aversion of Islamic Banks noted in

Beck et al. (2013) and Abdifar et al. (2013) and found significantly small IBs in less Muslim countries

are taking more risks to determine capital buffers while found some not significant positive and

relatively low coefficients in large IBs and countries of Muslim majority. Economic down turn during,

crisis and upper turn in pre and post crisis IBs are always significant negatively. These results add a new

dimension banking research for the economic stability. This study recommends better capital regulation

and bank supervision for monitoring risk-taking behaviour if banking system as a whole.

References

Abedifar P, Molyneux P, Tarazi, A., 2013. Risk in Islamic banking. Review of Finance 17, 2035–2096

Aggarwal, R., Jacques, K.T., 2001. The impact of FDICIA and prompt corrective action on bank

capital and risk: estimates using a simultaneous equations model. Journal of Banking and Finance 25,

1139–1160.

Alman, M. 2012. Shari’ah supervisory board composition effects on Islamic banks’ risk taking

behavior. European Financial Management Association meeting 2012

http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETING S/2013-

Reading/papers/EFMA2013_0082_fullpaper.pdf

Archer, S., Abdel Karim, R.A., and Sundararajan, V., 2010. Supervisory, regulatory, and capital

adequacy implications of profit-sharing investment accounts in Islamic finance. Journal of Islamic

Accounting and Business Research 1, 10-31.

Page 12 of 26

Archer, S. and Abdel -Karim, R.A., 2007. On capital structure, risk sharing and capital adequacy in

Islamic banks. International Journal of Theoretical and Applied Finance 9, 269-280.

Ariss R. T., 2010. Competitive conditions in Islamic and conventional banking: A global perspective.

Review of Financial Economics 19, 101–108.

Avery R., and Berger A., 1991. Risk-Based Capital and Deposit Insurance Reform. Journal of Banking

and Finance 15, 847-874.

Ayuso J., Pe´rez D., Saurnia J., 2004. Are capital buffers pro-cyclical? Evidence from Spanish panel

data. Journal of Financial Intermediation 13, 249–264

Beck, T., Demirguc-Kunt, A., Merrouche, O., 2013. Islamic vs. conventional banking: Business

model, efficiency, and stability. Journal of Banking and Finance 37, 433-447.

Berger, A.N., 1995. The relationship between capital and earnings in banking", Journal of Money,

Credit and Banking 432-456.

Baele L.M., Ferrando A., Hordahl P., Krylova E., Monnet C., 2004. Measuring financial integration in

the euro area. ECB Occasional Paper 14.

Bebchuk, L., and H. Spamann., 2010. Regulating Bankers’ Pay. Georgetown Law Journal 98, 247-

287.

Chessen, J., 1987. Feeling the heat of risk based capital: the case of off-balance-sheet activity.

Regulatory review. August 1-18. Washington DC: Federal Deposit Insurance Corporation, Office of

Research and Strategic Planning.

Čihák, M., Hesse, H., (2007). Cooperative banks and financial stability, IMF Working Paper No.

07/02, Washington D.C., I.M.F.

Cihak, M., Hesse H., 2010. Islamic banks and financial stability: an empirical analysis. Journal of

Financial Services Research 38, 95– 113

Crockett, A., 2001. The regulation of financial services: international principles and standards’.

Speech at the 17th International PROGRESS Conference, Geneva.

Page 13 of 26

Dewatripont, M., Tirole, J., Rochet, J., 2010. Balancing the Banks: Global Lessons from the Financial

Crisis, Princeton University Press.

Dewatripon, M, Tirole J., 1994. The prudential regulation of banks. MIT Press, Cambridge

Ediz, T., Michael, I., Perraudin, W., 1998. The Impact of Capital Requirements on U.K. Bank

Behaviour. Federal Reserve Bank of New York Economic Policy Review 4, 15-22.

Erkens, D. H., Hung, M., and Matos, P. P., 2012. Corporate Governance in the 2007-2008 Financial

Crisis: Evidence from Financial Institutions Worldwide. Journal of Corporate Finance, 18, 389-411.

Ediz, T., Michael, I. Perraudin, W., 1998. The Impact of Capital Requirements on U.K. Bank

Behaviour. Federal Reserve Bank of New York Economic Policy Review 4, 15-22.

Errico L., and Farahbaksh M., 1998. Islamic Banking: Issues in Prudential Regulations and

Supervision. IMF WP/98/30. https://www.imf.org/external/pubs/ft/wp/wp9830.pdf

Farook S., Hassan M. K., Clinchc G., 2012. Profit distribution management by Islamic banks: An

empirical investigation .The Quarterly Review of Economics and Finance 52, 333– 347.

Fu, X., Lin, Y., Molyneux, P., 2014. Bank competition and stability in Asia Pacific. Journal of

Banking and Finance 38, 64-77

Gallo J., Apilado V., Kolari J., 1996. Commercial bank mutual fund activities: Implications for bank

risk and profitability. Journal of Banking and Finance 10, 775-792

Ghosh S., 2014. Risk, Capital and Financial Crisis: Evidence for Gulf Cooperation Council (GCC)

Banks. Reserve Bank of India, MPRA Paper No. 65246. http://mpra.ub.uni-muenchen.de/65246/

Hassan D., Mansu M., Mansor I., 2015. The unique risk exposures of Islamic banks’ capital buffers:

A dynamic panel data analysis. Journal of International Financial Markets, Institutions and Money 36,

36-52.

Heid F., Porath D., Stolz S., 2004. Does capital regulation matter for bank behaviour? Evidence for

German savings banks. Deutsche Bundesbank, Discussion Paper 2, Frankfurt.

Page 14 of 26

Hilary, G. and Hui, K. W. (2009) Does religion matter in corporate decision making in America?,

Journal of Financial Economics 93, 455-473.

Jensen, M.C., Meckling, W.H., 1976. Theory of the Firm: Managerial Behavior, Agency Costs and

Ownership Structure. Journal of Financial Economics 3, 305-360.

Jacques, K., Nigro, P., 1997. Risk-based capital, portfolio risk, and bank capital: a simultaneous

equations approach. Journal of Economics and Business 49, 533–547.

Jokipii, T., Milne, A., 2011, Bank Capital Buffer and Risk Adjustment Decisions. Journal of

Financial Stability 7, 165-178.

Khan T, Ahmed, H., 2001. Risk management: an analysis of issues in Islamic financial industry,

Occasional Paper No. 5, IRTI, Islamic Development Bank, Jeddah

Keeton, W.R., 1989. The New Risk-Based Capital Plan for Commercial Banks. Federal Reserve Bank

of Kansas City Economic review 74, 40-60.

Kirkpatrick G., 2009. The corporate governance lessons from the financial crisis. OECD Journal:

Financial Market Trends 1, 61-87.

Lee C.C and Hsieh M.F., 2013. The impact of bank capital on profitability and risk in Asian banking.

Journal of International Money and Finance 32, 251–281.

Lepetit L., Bouvatier V., 2008. Banks’ procyclical behaviour: Does provisioning matter?. Journal of

International Financial Markets, Institutions and Money. 18, 513-526.

Laeven, L., Levine, R., 2009. Bank governance, regulation and risk taking. Journal of Financial

Economics 93, 259–275

Miller, A.S., Hoffmann, J.P., 1995. Risk and religion: An exploration of gender differences in

religiosity. Journal for the Scientific Study of Religion 34, 63-75.

Mollah S., Zaman, M., 2015. Shari’ah Supervision, Corporate Governance and Performance:

Conventional vs. Islamic Banks. Journal of Banking and Finance 58, 418-435.

Page 15 of 26

Mollah, S., Hassan, K., Al-Farooque, O., and Mobarek, A. (2016). The Governance, Risk-Taking, and

Performance of Islamic Banks. Journal of Financial Services Research, Forthcoming.

Osoba, B. (2003) Risk preferences and the practice of religion: Evidence from panel data,

Unpublished Working Paper, West Virginia University

Pathan, S., 2009. Strong boards, CEO power and bank risk-taking. Journal of Banking and Finance

33, 1340– 1350

Rime B., 2001. Capital requirements and bank behaviour: empirical evidence for Switzerland. Journal

of Banking and Finance 25, 789-805.

Siddiqi, A.M., 1999. The growing popularity of Islamic banking. Middle East Lond 291, 33–35

Sharfman, B.S., Toll, S.J., and Szydlowski, A., 2009. Wall Street's Corporate Governance Crisis.

Corporate Governance Advisor 17, 5-8.

Shim, J., 2013. Bank Capital Buffer and Portfolio Risk: The Influence of Business Cycle and Revenue

Diversification. Journal of Banking and Finance 37, 761-772.

Shim, J., 2010. Capital based regulation, portfolio risk and capital determination: empirical evidence

for Switzerland. Journal of Banking and Finance 25, 789-805

Shrieves, R., Dahl, D., 1992. The relationship between risk and capital in commercial

Banks. Journal of Banking and Finance 16, 439–457.

Stiroh K.J., 2004. Diversification in banking: is noninterest income the answer? Journal of Money

Credit and Banking 36, 853-882.

Stiroh J., and Rumble, A., 2006. The Dark side of Diversification: The case of US Financial Holding

Companies. Journal of Banking and Finance 30, 2131-2161.

Stulz, B., 2012. The credit crisis around the globe: Why did some banks perform better? Journal

Financial Economics 105, 1–17

Page 16 of 26

Sudrarajan, V., 2005. Riks Measurement and Disclosure in Islamic Finance and the implication of

Profit Sharing Investment Accounts. Sixth International Conference on Islamic Economics, Banking

and Finance, Jakarta, Indonesia.

Srairi, S., 2013. Ownership structure and risk-taking behaviour in conventional and Islamic banks:

Evidence for MENA countries. Borsa Istanbul Review 13, 115-127.

Tarazi, A., Lepetit, L., Nys, E., and Rous, P., 2008. Bank income structure and risk: An empirical

analysis of European banks. Journal of Banking and Finance 32, 1452–1467.

Warde I., 2010. Islamic Finance in the Global Economy (2nd edn). Edinburg: Edinburg University

Press.

Page 17 of 26

Table 1: Sample Distribution

The table describes the sample of the study. The study considers 701 banks (123 Islamic and 578 conventional) over 26

countries for the period of 2004-2013. The country-wise distribution of the banks, IB percentage and CB percentage are

given in columns 5-6.

Country Islamic

Banks

Conventional

Banks

Full Sample

(all Banks)

IB share CB share Total

Share (Ibs

+ CBs)

Algeria 2 15 17 0.2853 2.1398 2.425

Bahamas 1 12 13 0.1426 1.7118 1.854

Bahrain 19 13 32 2.7104 1.8545 4.565

Bangladesh 4 20 24 0.5706 2.8531 3.424

Brunei Darussalam 1 1 2 0.1426 0.1427 0.285

Egypt 3 23 26 0.4280 3.2810 3.709

Indonesia 5 62 67 0.7133 8.8445 9.558

Iraq 4 5 9 0.5706 0.7133 1.284

Jordan 2 10 12 0.2853 1.4265 1.712

Kuwait 8 6 14 1.1412 0.8559 1.997

Lebanon 2 36 38 0.2853 5.1355 5.421

Malaysia 17 42 59 2.4251 5.9914 8.417

Mauritania 1 7 8 0.1427 0.9986 1.141

Pakistan 9 25 34 1.2839 3.5663 4.850

Qatar 3 7 10 0.4280 0.9986 1.427

Saudi Arabia 4 9 13 0.5706 1.2839 1.855

Senegal 1 9 10 0.1427 1.2839 1.427

Singapore 1 17 18 0.1427 2.4251 2.568

Sudan 11 11 22 1.5692 1.5692 3.138

Syrian Arab Republic 2 10 12 0.2853 1.4265 1.712

Thailand 1 23 24 0.1427 3.2810 3.424

Tunisia 1 15 16 0.1427 2.1398 2.283

Turkey 4 31 35 0.5706 4.4223 4.993

United Arab Emirates 8 17 25 1.1412 2.4251 3.566

United Kingdom 5 149 154 0.7133 21.2554 21.969

Yemen 4 3 7 0.5706 0.4280 0.999

Total 123 578 701 17.5464% 82.4536% 100.000%

Page 18 of 26

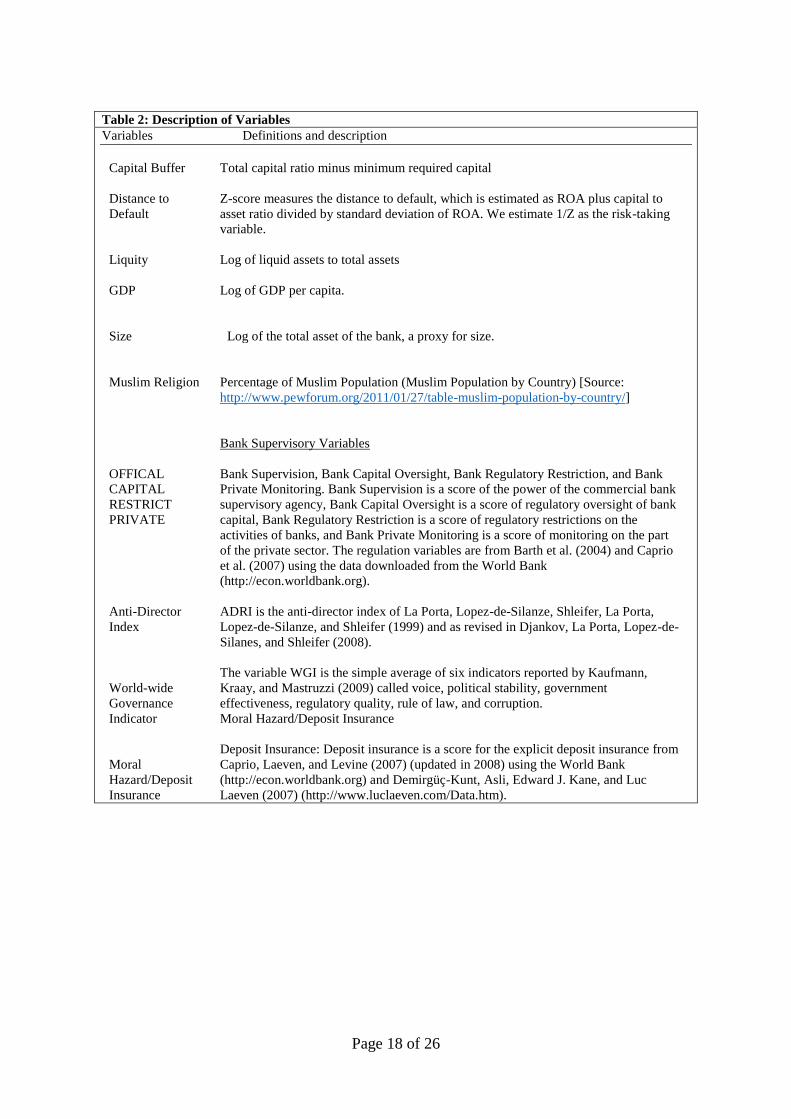

Table 2: Description of Variables

Variables Definitions and description

Capital Buffer

Distance to

Default

Liquity

GDP

Size

Muslim Religion

OFFICAL

CAPITAL

RESTRICT

PRIVATE

Anti-Director

Index

World-wide

Governance

Indicator

Moral

Hazard/Deposit

Insurance

Total capital ratio minus minimum required capital

Z-score measures the distance to default, which is estimated as ROA plus capital to

asset ratio divided by standard deviation of ROA. We estimate 1/Z as the risk-taking

variable.

Log of liquid assets to total assets

Log of GDP per capita.

Log of the total asset of the bank, a proxy for size.

Percentage of Muslim Population (Muslim Population by Country) [Source:

http://www.pewforum.org/2011/01/27/table-muslim-population-by-country/]

Bank Supervisory Variables

Bank Supervision, Bank Capital Oversight, Bank Regulatory Restriction, and Bank

Private Monitoring. Bank Supervision is a score of the power of the commercial bank

supervisory agency, Bank Capital Oversight is a score of regulatory oversight of bank

capital, Bank Regulatory Restriction is a score of regulatory restrictions on the

activities of banks, and Bank Private Monitoring is a score of monitoring on the part

of the private sector. The regulation variables are from Barth et al. (2004) and Caprio

et al. (2007) using the data downloaded from the World Bank

(http://econ.worldbank.org).

ADRI is the anti-director index of La Porta, Lopez-de-Silanze, Shleifer, La Porta,

Lopez-de-Silanze, and Shleifer (1999) and as revised in Djankov, La Porta, Lopez-de-

Silanes, and Shleifer (2008).

The variable WGI is the simple average of six indicators reported by Kaufmann,

Kraay, and Mastruzzi (2009) called voice, political stability, government

effectiveness, regulatory quality, rule of law, and corruption.

Moral Hazard/Deposit Insurance

Deposit Insurance: Deposit insurance is a score for the explicit deposit insurance from

Caprio, Laeven, and Levine (2007) (updated in 2008) using the World Bank

(http://econ.worldbank.org) and Demirgüç-Kunt, Asli, Edward J. Kane, and Luc

Laeven (2007) (http://www.luclaeven.com/Data.htm).

Table 3: Baseline Estimations by using 2SLS Models

This table presents the regression results for multi variate difference in conventional and Islamic banks and its impact on risk taking. The risk-taking proxy is Z-score. We split for large and small bank size and country size. See Table 2 for definitions of the other bank-specific and country-specific variables. T-statistics are reported in the parentheses. The ***,

**, and * represent p-values of 0.01, 0.05, and 0.10.

P a n e l A : C A P I T A L P a n e l B : R I S K

VARIABLES Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8

Islamic Dummy 3.300* 2.620 3.717 0.210 -7.771*** -6.713** -7.325** -4.505

(1.709) (1.311) (1.608) (0.073) (2.773) (2.236) (2.418) (0.808)

ΔDistance to Default 0.410*** 0.429*** 0.471*** 0.453***

(3.707) (3.834) (3.731) (3.498)

ΔCapital Buffer 1.507*** 1.532*** 1.556*** 1.577***

(4.634) (4.793) (4.865) (3.613)

Islamic Dummy X

ΔDistance to Default

0.807*** 0.798*** 0.879*** 0.477*

(3.718) (3.658) (3.571) (1.706)

Islamic Dummy X ΔCapital Buffer

-1.328*** -1.297*** -1.339*** -0.793**

(3.538) (3.515) (3.620) (2.021)

Size 0.317 0.350 0.410* 1.057** 0.124 0.028 -0.175 -0.746

(1.446) (1.579) (1.655) (2.104) (0.307) (0.068) (0.407) (0.587)

Muslim religion 0.253 -0.192 -1.226 7.940 0.414 0.761 1.858 -5.818

(0.436) (0.289) (1.256) (1.358) (0.416) (0.723) (1.440) (0.460)

Log_GDP -0.305 -0.449* 0.185

0.319 0.498 0.031

(1.413) (1.761) (0.397)

(0.867) (1.285) (0.036)

Inflation_rate 0.131 0.093

-0.177 -0.183

(1.601) (1.003)

(1.470) (1.353)

Deposit Insurance 9.065**

-8.173

(1.998)

(0.757)

Bank Supervision -3.605

3.395

Page 20 of 26

(1.123)

(0.552)

Bank Regulatory

Restriction

13.135

-8.843

(1.596)

(0.476)

Bank Private

Monitoring

-5.748

5.461

(1.058)

(0.507)

Bank Capital

Oversight

-4.423**

4.712

(2.195)

(1.055)

Constant -7.923 -0.322 1.642 -33.534* -1.750 -8.290 -7.771 18.820

(1.592) (0.044) (0.200) (1.726) (0.188) (0.701) (0.658) (0.408)

Observations 1,288 1,288 1,288 1,287 1,288 1,288 1,288 1,287

Page 21 of 26

Table 4: Extended Analysis by using 2SLS Models

This table presents the regression results for multi variate difference in environment, firms, country, and religion between conventional and Islamic banks and its impact on risk taking. The risk-

taking proxy is Z-score. We divide for large and small bank size and country size. See Table 2 for definitions of the other bank-specific and country-specific variables. T-statistics are reported in

the parentheses. The ***, **, and * represent p-values of 0.01, 0.05, and 0.10.

P a n e l A : C A P I T A L P a n e l B : R I S K

Bank Size

Country Size Muslim Population Bank Size Country Size Muslim Population

VARIABLES (1) Small

(2) Large

(3) Small

(4) Large

(5) <90%

(6) >90%

(10) Small

(11) Large

(12) Small

(13) Large

(14) <90%

(15) >90%

Islamic Dummy 1.576 -1.447* -0.957 -0.422 0.653 -0.272 -4.670 4.591 3.599 -2.534 -4.579 0.687

(0.459) (1.944) (0.239) (0.116) (0.241) (0.280) (0.816) (1.585) (0.915) (0.380) (0.861) (0.378)

ΔDistance to Default

0.580***

0.320*** 0.560** 0.592*** 0.409*** 0.599***

(2.582) (4.962) (2.248) (3.630) (2.893) (3.359)

ΔCapital Buffer 1.274** 3.125*** 1.889*** 1.471*** 1.603*** 1.624***

(2.431) (5.396) (3.742) (3.296) (3.079) (3.371)

Islamic Dummy X ΔDistance to

Default

0.704* -0.009 0.838 0.503 0.521* -0.074

(1.688) (0.122) (1.463) (1.332) (1.906) (0.864)

Islamic Dummy X

ΔCapital Buffer

-0.894** 0.025 -1.207* -0.690 -0.915** 0.101

(2.162) (0.135) (1.801) (1.593) (2.378) (0.832)

Size 0.605 0.002 -0.188 0.393 1.151** 0.035 -0.066 -0.007 0.374 -0.365 -0.890 -0.060

(0.743) (0.019) (0.529) (0.734) (2.280) (0.306) (0.046) (0.023) (1.008) (0.346) (0.643) (0.322)

Muslim religion

2.679 0.136 -0.415 -0.416 8.522 0.569 1.713 -0.389 2.014 0.754 -6.730 -0.760

(0.286) (0.097) (0.055) (0.065) (1.456) (0.354) (0.119) (0.100) (0.258) (0.076) (0.502) (0.305)

Log_GDP 0.119 0.154 -2.424 -0.091 0.191 -0.071 0.044 -0.492 1.627 0.559 -0.140 0.079

(0.207) (1.277) (0.624) (0.165) (0.419) (0.454) (0.048) (1.170) (0.443) (0.601) (0.165) (0.297)

Inflation_rate 0.084 0.011 -0.012 0.100 0.115 -0.038 -0.058 -0.038 -0.014 -0.099 -0.237* 0.052

(0.775) (0.473) (0.071) (1.036) (1.222) (1.454) (0.430) (0.537) (0.086) (0.806) (1.825) (1.227)

Deposit Insurance 4.503 0.705 0.405 2.340 8.807** 0.869 0.033 -2.250 0.725 -1.626 -8.271 -1.570

(0.646) (0.575) (0.079) (0.462) (2.015) (0.644) (0.003) (0.621) (0.132) (0.176) (0.758) (0.666)

Bank Supervision -2.512 -0.382 10.228 0.389 -3.498 0.171 0.763 1.254 -6.588 -3.073 4.209 -0.074

(0.642) (0.445) (0.588) (0.103) (1.135) (0.161) (0.117) (0.460) (0.406) (0.491) (0.713) (0.041)

Bank Regulatory

Restriction

7.895 2.348 14.070 6.177 13.935* -1.240 -1.246 -7.507 -12.594 -1.975 -13.668 1.489

(0.761) (1.130) (0.796) (0.617) (1.829) (0.452) (0.065) (1.048) (0.734) (0.099) (0.770) (0.311)

Page 22 of 26

Bank Private

Monitoring

-1.527 0.880 -2.554 1.867 -5.952 -1.121 -1.299 -2.836 -0.586 -0.521 4.926 1.489

(0.171) (0.640) (0.210) (0.337) (1.061) (0.710) (0.099) (0.733) (0.047) (0.068) (0.422) (0.649)

Bank Capital Oversight

-3.865 -0.114 -6.573 -1.959 -3.908** -0.421 2.561 0.432 5.384 0.618 4.526 0.983

(1.611) (0.206) (0.942) (0.863) (2.016) (0.659) (0.532) (0.226) (0.814) (0.130) (1.070) (0.788)

Constant -18.742 -5.479 55.472 -10.652 -36.689** 2.010 -0.432 17.454 -41.887 -2.074 29.201 -2.131

(0.730) (1.209) (0.660) (0.433) (2.042) (0.348) (0.009) (1.093) (0.531) (0.043) (0.637) (0.207)

Observations 1,286 1,286 1,286 1,286 1,286 1,286 1,286 1,286 1,348 1,286 1,286 1,286

Page 23 of 26

Table 5: Crisis Effects

This table presents the regression results for multi variate difference in conventional and Islamic banks and its impact on risk taking. The risk-taking proxy is Z-score. We split large

and small bank size and country size. See Table 2 for definitions of the other bank-specific and country-specific variables. T-statistics are reported in the parentheses. The ***, **,

and * represent p-values of 0.01, 0.05, and 0.10.

P a n e l A : C A P I T A L

P a n e l B : R I S K

VARIABLES (1)

Pre

(2)

During

(3)

Post

(4)

Pre

(5)

During

(6)

Post

Islamic Dummy 1.112 -0.317 -0.015 -2.252 -0.970 -2.187

(0.766) (0.216) (0.005) (1.146) (0.357) (0.401)

ΔDistance to Default 0.736*** 0.523*** 0.549**

(3.678) (4.138) (2.391)

ΔCapital Buffer 1.321*** 1.731*** 1.008*

(4.419) (4.866) (1.677)

Islamic Dummy X

ΔDistance to Default

0.298* 0.230 0.536**

(1.908) (1.582) (2.045)

Islamic Dummy X ΔCapital Buffer

-0.305* -0.346* -0.614*

(1.799) (1.654) (1.798)

Size -0.058 -0.116 0.006 0.118 0.260 -0.078

(0.486) (0.616) (0.040) (1.036) (0.845) (0.300)

Muslim religion -0.773 -1.097 -5.237* -0.030 1.500 2.830

(0.566) (0.416) (1.656) (0.027) (0.375) (0.428)

Log_GDP 0.029 0.071 -0.350 0.076 -0.202 0.548

(0.169) (0.233) (0.892) (0.479) (0.429) (0.701)

Inflation_rate 0.036 0.058 0.070 -0.009 -0.126 0.022

(0.601) (0.715) (1.078) (0.172) (1.123) (0.177)

Deposit Insurance -0.344 0.315 -3.049 0.434 -0.461 1.675

(0.470) (0.142) (1.106) (0.595) (0.127) (0.291)

Bank Supervision 0.417 -0.453 2.290 -0.180 1.862 -4.132

(0.562) (0.198) (0.872) (0.233) (0.545) (0.816)

Bank Regulatory

Restriction

-2.064 -1.201 -3.675 2.746 2.087 2.845

(1.234) (0.253) (0.608) (1.586) (0.269) (0.237)

Bank Private Monitoring 0.166 1.067 4.419 0.995 -1.289 -1.225

Page 24 of 26

(0.123) (0.448) (1.165) (0.765) (0.356) (0.174)

Bank Capital Oversight -0.258 -0.613 0.901 -0.588 1.134 -0.975

(0.283) (0.424) (0.549) (0.797) (0.506) (0.295)

Constant 1.372 1.531 8.920 -5.837 -2.615 -11.125

(0.344) (0.145) (0.828) (1.486) (0.153) (0.498)

Observations 1,591 1,286 1,654 1,591 1,286 1,654

Page 25 of 26

Table 6: Robustness Checks by using 3SLS Models

This table presents the regression results for multi variate difference in conventional and Islamic banks and its impact on risk taking. The risk-taking proxy is Z-score. We split large

and small bank size and country size. See Table 2 for definitions of the other bank-specific and country-specific variables. T-statistics are reported in the parentheses. The ***, **, and

* represent p-values of 0.01, 0.05, and 0.10.

P a n e l A : C A P I T A L P a n e l B : R I S K

VARIABLES Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8

Islamic Dummy 3.155* 2.343 2.916 0.292 -6.127** -4.906* -5.457* -3.419

(1.734) (1.241) (1.349) (0.103) (2.241) (1.685) (1.874) (0.629)

ΔDistance to Default 0.429*** 0.448*** 0.478*** 0.507***

(4.164) (4.313) (4.017) (4.524)

ΔCapital Buffer 1.806*** 1.786*** 1.728*** 1.731***

(6.086) (6.158) (5.853) (4.610)

Islamic Dummy X

ΔDistance to Default

0.748*** 0.719*** 0.720*** 0.442*

(3.738) (3.609) (3.336) (1.721)

Islamic Dummy X

ΔCapital Buffer

-1.228*** -1.169*** -1.127*** -0.699*

(3.384) (3.306) (3.227) (1.909)

Size 0.299 0.338 0.421* 0.958** -0.222 -0.291 -0.417 -1.240

(1.436) (1.611) (1.762) (2.104) (0.592) (0.766) (1.024) (1.097)

Muslim religion 0.252 -0.179 -1.043 7.354 -0.274 0.255 1.443 -10.411

(0.452) (0.280) (1.113) (1.352) (0.287) (0.248) (1.139) (0.904)

Log_GDP -0.311 -0.443* 0.218

0.400 0.574 -0.069

(1.446) (1.750) (0.470)

(1.094) (1.491) (0.081)

Inflation_rate 0.121 0.103

-0.173 -0.158

(1.498) (1.174)

(1.444) (1.199)

Deposit Insurance 8.808**

-11.944

(2.031)

(1.200)

Bank Supervision -3.701

4.477

(1.160)

(0.744)

Bank Regulatory Restriction

12.990

-14.630

(1.621)

(0.836)

Bank Private

Monitoring

-5.207

8.858

Page 26 of 26

(1.014)

(0.888)

Bank Capital

Oversight

-4.649**

5.922

(2.333)

(1.385)

Constant -7.504 0.108 1.280 -31.896* 6.292 -3.111 -4.259 35.007

(1.590) (0.015) (0.161) (1.723) (0.725) (0.271) (0.370) (0.822)

Observations 1,288 1,288 1,288

1,287 1,288

1,288 1,288

1,287