capital flows to emerging markets under the flexible dollar standart: a critical view based on...

TRANSCRIPT

218

11. Capitalflowstoemergingmarketsundertheflexibledollarstandard:acriticalviewbasedontheBrazilianexperience

Carlos Medeiros and Franklin Serrano1*

IntroduCtIon

thepurposeofthischapteristocontributetothediscussionofanumberofis-sues concerning macroeconomic policies that should be appropriate fordevelopingcountries.Weshalltakeintoaccountthebroaderpoliticalpictureofchangesintheinternationaleconomy,reflectedobjectivelyintermsofthenatureofthebalanceofpaymentsconstraintsfacingthe‘emergingmarkets’andspe-ciallytheLatinAmericaneconomiessincetheearly1990s.ItiswithinthiswidercontextthatwepresentouraccountoftheparticularcaseofBrazil. theBrazilianexperiencehassomepeculiaritiesthatmakeitaninterestingtestinggroundforthepresumedbenefitsoftheprocessoffinancialglobalizationandthepoliciesoftradeandfinancialopening. Manywillagreethattheslowgrowthandextremelyhighinflationexperi-encedinBrazilinthe1980shadmuchtodowithdebtcrisisandthesubsequentinterruptionofcapitalflowstowardsLatinAmerica.Indeed,inwhatbecameknownasthe‘lostdecade’Brazilexperiencedaseverebalanceofpaymentsconstraintthatslowedgrowthandtriggeredtheaccelerationofinflation.Sincetheearly1990s,foreigncapitalstartedagainflowingtowardsBrazilinlargequantities,firstmainlyasportfoliocapitalbuttowardstheendofthedecademoreandmoreasforeigndirectinvestment.onecouldwellhaveexpectedthatthislargeamountofforeigncapitalwouldimprove‘quality’(presumablyin-creasingly ‘cold’ rather than ‘hot’ money), by alleviating the balance ofpaymentsconstraint,andwouldhavehadabigeffectonbothinflationstabiliza-tionandintheresumptionoffasteconomicgrowth. However,whattheactualrecordshowsisthattheimpactoninflationstabili-zation,althoughstartingabitlate,onlybymid-1994,wasinfactmoredrasticthananybodycouldhavereasonablyexpected.Inflationfellspectacularlyand

Capital flows to emerging markets: the Brazilian experience 219

hasremainedextremelyloweversince.ontheotherhand,thegrowthperform-ancewas,tosaytheveryleast,extremelydisappointing.thischapterwilltrytomakesenseofthisexperienceusingacombinationofsomefeaturesoftheinternational situation and of particular policies followed by the Brazilianstate. MostLatinAmericaneconomiesfollowedmoreorlessthesamebroadpatternoffastdisinflationandslowgrowthwiththenotableexceptionofChileandpartialexceptionofArgentina.thereforetheBrazilianstory,inspiteofitspe-culiarities,mayarguablybeseentoreflectamoregeneralpattern. Weshallbeginourdiscussioninthefollowingsectionwithabriefaccountoftheoperationofthecurrentinternationalmonetarysystem,asystemthatwecallthe‘floatingdollarstandard’,andofothersalientfeaturesoftheinterna-tional trade and financial environment faced by the ‘emerging’ developingeconomiessincetheearly1990s.thethirdsectionshowshowthisnewinter-nationalenvironmentaffectsandchangesthenatureofthebalanceofpaymentsconstraint facing the developing countries.the fourth section discusses theBrazilianexperiencewithinthecontextoftheresumptionoflargecapitalflowstowardsLatinAmericasincetheearly1990s.thelastsectioncontainsafewconcludingremarks.

tHeFLoAtIngdoLLArStAndArd,FInAnCIALgLoBALISAtIonAndtHeeMergIngMArketS

The Floating Dollar Standard

Attheendof1979therewasamajorchangeinAmericanmonetarypolicy,withtheVolckerinterestrateshock.thedollarinterestrateinbothnominalandrealtermsreachedunprecedentedlevelsandthiswasfollowedbyawaveoffinancialinnovationsandpoliciesoffinancialderegulation,whichhaseversincebeenspreadingacombinationoflargeandincreasinglyunregulatedshort-termcapitalflowsandvolatileexchangeratesallovertheworld. thispolicychangequicklybroughtdowninternationalcommoditypricesand slowed down international inflation. the uSA has since then regainedcompletecontrolovertheinternationalmonetaryandfinancialsystem.theotherdevelopedcountries,finallyconvincedofthefutilityoftryingtoquestionthecentralityofthedollar(astheyhadbeendoinginthe1970),increasinglyaccepttherealityofthenewsystem:thefloatingdollarstandard. Inthissystem,thedollarisstillthekeyinternationalcurrency.thedifferencenowisthattheuSAisfreefromthetwolimitationsthatthepreviousgold–dollarstandardimposedonitspolicies,namely,theneedtokeepafixednominalex-changerate(topreventaruntowardsgold)andtheneedtoavoidrunningcurrent

220 Emerging markets and the financial architecture

accountdeficits(inordertopreventadecreaseintheuSgoldreserves)(Serrano,1999;MedeirosandSerrano,1999). Inthecurrentfloatingdollarstandard,theuSAcanincuroverallbalanceofpaymentsdeficitsandfinancethembygivingassetsdenominatedinitsowncurrencyasinthegold–dollarstandardthatendedin1971.However,thelackofconvertibilityingoldallowstheuSAtochangebyitsowninitiativetheex-changeparityagainstothercurrencies,mainlythroughchangesindollarinterestrates.thisoccurredwhenitengineeredtrendsbothofdollarappreciation(asin1980–5and1995–2001)andofdepreciation(in1986–94).Inthelattercasethereisnobigdirectinflationaryeffectsinceinternationalcommodityandoilpricesaresetindollarsandthereisalsonoreasontofearagoldrunanymorebecausethecurrentstandardisthedollaritself.thedollaristheinternationalmeansofpaymentandthemainstandardincontractsandpricequotesintheinternationalmarkets(asithappens,forinstance,eveninAsiantradewhichismainlyinvoicedinuSdollars),propertiesthatmakeitanimportantstoreofvalue(becauseofitssuperiorliquidity). themainadvantageofthecurrentfloatingdollarstandardfortheuSAisthereforethecompleteeliminationofitsexternalorbalanceofpaymentscon-straint.nowtheuSAcananddoesruncurrentaccountdeficitswithoutworryingmuchabouttheincreaseinitsnetexternalliabilitiesbecausethese‘external’liabilitiesaremainlydenominatedindollarsanyway(withoutgoldconvertibilitytheproblemoflosinggoldreserveswhenacurrentaccountdeficithappenshassimplybeeneliminated,seeSerrano,1999). thisfloatingdollarstandard,whichnixonandkissingertriedtoimposeintheturbulent1970andwhichbecameafactinthe1980s,allowstheuSAtorunpermanentcurrentaccountdeficits,ashasbeenhappeningalmosteverysingleyearsince1971(exceptin1973–6and1980–81).Inthecurrentsystem,thetotalvalueofAmericandeficitsinthebalanceofpaymentsasawholeisautomaticallyfinancedbyanidenticalcapitalinflowcorrespondingtothein-creaseofothercountries’reserves.thesecountries,iftheywanttoparticipatein the internationaleconomy,simplymustagree toaccumulatedollarassets(oftenintheforofuSpublicdebt).Infact,thedollaristhereserveassetofthewholeinternationalfinancialsystem,asitisclearbothfromthecentralroleofAmericaninterestratesandfromthe‘flighttoquality’movementsintimesofturbulence,where‘quality’alwaysmeansuSgovernmentbonds.1

ItisveryimportanttostressthesecharacteristicsofthecurrentinternationalmonetaryandfinancialsystemandtheextremeextenttowhichtheybenefituSinterests.thatmayperhapstemperabitthewell-meantcallsformajorchangesinthe‘internationalfinancialarchitecture’,whichoftendonotspecifyhoworwhytheuSAwillacceptthosechanges,asmalldetailthatmakessuchproposalssoundratherutopian.

Capital flows to emerging markets: the Brazilian experience 221

Financial Globalization and Emerging Markets

Curiouslyenough,inspiteoftheabsenceofoverallbalanceofpaymentsprob-lems,Americantradepolicyduringthe1990sturnedprogressivelytougher,bothdirectlyandindirectly,throughitsoverwhelminginfluenceininternationalor-ganizationssuchastheWto,theWorldBankandtheIMF.uStradepolicyhassystematicallyattemptedtoreducebilateraltradedeficitswithmostcountriesandtoprotectits‘old’industries(suchas,steel,orangejuice,andsoon)andatthesametimetoopenforeignmarketsinsectors(suchasservices)wheretheuS has a clear competitive edge (software, entertainment services, and soon). the1990swascharacterizedbyrelativelylowgrowthoftheworldeconomyas whole, unfavourable terms of trade for the developing countries and thehardeningofthetradepoliciesoftheuSA,eurolandandoftheinternationalorganizations.WorldtradestillgrewbymorethanworldgdPbuttheexportmarketsfordevelopingcountriesgrewrelativelyslowlyandunderanincreas-inglyfiercecompetition.thiscompetitionhasbeenaggravatedbytherepeatedcompetitiveexchangeratedevaluationsofanumberofdevelopingcountriesrelativetothedollar,whichcreatesproblemsfordevelopingcountriesthatadoptfixedexchangerateregimes. Foreigndirectinvestmentsincethe1980hasgrownatveryhighrates,pre-dominantlybetweenindustrialcountries(forexample,Japaneseandeuropeaninvestment in theuSA, investmentbetweeneuropeanunioncountries)andalsoinanumberofdevelopingcountriesinAsiaandincreasinginChina.InLatinAmerica,Mexico(becauseofnAFtA)andmorerecentlyBrazilhavere-ceivedlargeflowsofFdI. Asfarasdevelopingcountriesareconcerned,theseflowshavebeensubstan-tialonlyforaselectedgroupofthem.Furthermore,asaruletheseflowstowardsdevelopingcountrieshavenotalwaysbeengearedtowardsimportsubstitutingorexportsectors,sincemanyemergingcountriesareattractingFdIthroughprivatizationofnon-tradableutilitiesandservicesand/orbymakinglocalfirmsacheapbuyduetothearbitragegainallowedbykeepinglargeinterestratedif-ferentials(faraboveexpectedexchangeratedevaluation).onlyunderveryfewspecificcircumstancessuchasintheeastAsianeconomiesinthe1980s,wereFdIflowsstronglyconnectedwithanaccelerationofexportsandastructuralimprovementinthebalanceofpaymentsposition.2Moreover,theseflows,par-tially because of these attraction policies and in part because of the veryonce-and-for-allnatureofalotofFdIflows,havenotbeenverystableorregularovertime. overthisperiod,increasingfinancialderegulationmadeitdeceptivelyeasyformostdevelopingcountries,evenmanyofthosewhohadbeencutofffromthecircuitofinternationalfinancesincethedebtcrisisintheearly1980s,tofi-

222 Emerging markets and the financial architecture

nance current account deficits through private international capital markets(mainlythroughshort-termportfolioinvestmentsbutalsothroughbankloans).Inthe1990stherewasamarkedexpansionofthesegrosscapitalflowstowardsthedevelopingcountries,flowswhichinspiteofnumerouscriseshavecontin-ued,albeitwithlargefluctuations,eversince. Inthelastfiveyears,theglobaltrendofcapitalflowstowardsdevelopingcountrieshasshiftedagaintowardsafastergrowthofFdIrelativetodebtorportfolioflows.thishasledinmanyplacestoarenewedoptimismabout‘glo-balization’ and development since the ‘quality’ of the flows seems to beimproving,butthisoptimism,atleastinwhatregardsgrowthperformance,ap-pearsasweshallpresentlyseetoberatherexaggerated.

LArgeCAPItALFLoWSAndtHeexternALConStrAIntFortHedeVeLoPIngCountrIeS

Capital Flows to ‘Emerging Markets’

thebalanceofpaymentssituationinthe‘emerging’developingcountrieswiththecurrentfloatingdollarstandardseemsquitepeculiar.Forontheonehand,intermsofthebalanceoftradeandgrowthofexports,thetrendsingeneralarequiteunfavourable(incomparisonwiththe1970forinstance)sincenowthegrowthofexportvolumesarelower,thetermsoftradeworseandthepressurefromtherichcountriesonthosecountriestoincreaseimportsisratherstrong.3ontheotherhand,ithasbecomeeveneasierthanitwasinthe1970fordevel-opingcountriestoattractlargeflowsofforeigncapital. thiscontradictionisaggravatedbythefactthat,ingeneral,itbecomeseasiertoattractlargercapitalinflowsthemorean‘emerging’economyfollowspoliciesoffinancialderegulationandopeningitsmarkets:policiesthatinvariablyleadtoexchangerateappreciationandlossofcompetitiveness.thisincreasesthegapbetweenthelargeaccumulationofforeignliabilitiesandtherealpossibilityofservicingtheseliabilitiesthatrequiresarapidincreaseinexportearnings. Itisimportanttonotethatthisproblemcannotbesolvedbychangingtheformofthecapitalinflows.Itistruethatthemoreafinanciallyopeneconomyattractsandreliesonshort-termspeculativecapitalthemoreitwillbepronetoforeign-exchange and liquidity crises.4 However, even when capital inflowsconsistmainlyofFdIthelonger-termstructuralexternalfragilityisnotreduced.AsithasbeenpointedoutbyPrebisch(1950),kalecki([1972]1982)andmorerecentlybykregel(1996)amongothers,unlessFdIiscontinuouslyandsteadilyexpandingand isdirectlyconnected to theexpansionofexportcapacity (orimportsubstitution),itdoesnotgeneratelong-runpositiveeffectsonthebalanceofpaymentspositionofrecipientcountries(seebelow).

Capital flows to emerging markets: the Brazilian experience 223

In this very unstable international environment, we observe that the bestperformanceintermsofeconomicgrowthhasoccurredinthedevelopingcoun-triesthathavemanaged(inmanycountriesforaslongastheyhavemanaged)toresistthetemptationof(andthepressuresfor)uncontrolledfinancialopeningderegulation,andhavekeptsomesortofcontrolespeciallyoverthecapitalin-flows;thishaskeptexchangerateandindustrialpoliciesgearedtowardsexportpromotion.Inotherwords,thegrowthperformancehasbeenmuchbetterincountriesinwhichfinancialglobalizationdidnotlead(orforaslongasitdidnotlead)totheabandonmentofstate-leddevelopmentstrategies(suchasChilefromthe1980s,andChina,IndiaandAsiancountriesuntilthelate1980s).

Long-term Sustainability and Growth

Whendiscussingcapitalflowsandthebalanceofpaymentssituationwemustbeclearaboutwhatarethelimitsonthepossibilityofeconomiesgrowingwhileincurringcurrentaccountdeficits. Inthefirstplaceitisimportanttolookatthequestionofthesustainability(orsolvency)ofthistypeofgrowthtrajectory.Wemustexamineunderwhatconditionsthegrowthofnetforeignliabilitiesintheeconomywillremainundercontrolandnotfollowanexplosivepath.thiscaninitiallybethoughtofinde-pendently of the specific manner in which the current account is financed,whetheritisintermsofexternaldebtorforeigndirectinvestment. thecentralelement,asfarasthesustainabilityofastrategyofgrowingwithcurrentaccountdeficitsisconcerned,isgivenbytherelativeevolutionofthenetexternalliabilitiesandexports,sincethelatterarenecessarilytheultimatesourceofthecashflowinforeignexchangethatallowstheservicingoftheseliabilities. thenetexternalliabilities,likeanydebtthatisrolledover,growatarateequaltotheeffectiveinterestratepaidontheseliabilities.thecrucialrelation-shipregardingthesustainabilityofthisgrowthwithdebtisthusgivenbythedifferencebetweentherateofgrowthofthevalueofexportsandthatoftheef-fectiveinterestrate. Asdemonstratedoriginallybydomar(1950),iftherateofgrowthofexportsissystematicallybelowthatinterestrate,evenasmalltradedeficitwillmaketheratiobetweennetexternalliabilitiesandexportsgrowwithoutlimitandatsomepointitwillbeinevitablethattheeconomywillhavetogenerateatradesurplusinordertostabilizethegrowthofitsexternalliabilities.Itisthereforeextremelyimportant,forcountriesthataregrowingandexperiencecurrentac-countdeficits,thattherateofgrowthoftheirexportsshouldbesufficientlyhightosatisfythedomarstabilitycondition. Consideringthisdiscussionofthesustainabilityofexternalliability,theonlyrelevantdifferencebetweenforeigndirectinvestmentandexternaldebt,whether

224 Emerging markets and the financial architecture

thelatterisshort-termorlong-term,istheirrelativecostsintermsofpaymentsofforeignexchange. Althoughforeigndirectinvestmentisconsideredthecheapestformofexter-nalfinancebecausesomeoftheirprofitsarereinvested,someauthorssuchaskregel(1996)claimthatthecostofthisalternativemayinfactwellbehigherthanlong-termexternaldebt.kregelclaimsthatthisisbecausetherateofprofittendstobehigherthantherateofinterest.Inthatcasethe‘reinvestment’ofprofitsshouldbeseenasanewgrossforeigndirectinvestmentflow(implyingnewrightstofuturerepatriationofprofits)andshouldthisnotbedeductedfromthecostofpreviousflows. Anotherproblemisthatthecostofattractingcapitalthroughalargediffer-encebetweendomesticandforeigninterestratesisveryprobablymuchclosertothecurrentdollarvalueofthedomesticrateofinterestratherthantherateatwhichthecountrygetscreditintheinternationalmarket.thishappensbecausethesecapitalflowsarenormallyinvestedinfundsthatare,inonewayoranother,linkedtotheinternaldebtofthecountry(seeSerrano,1998). giventhesepossibilitiesandthenotoriouspracticaldifficultyofmeasuringaccuratelyandseparatelytheratesofreturnofalltypesofforeignliabilities–in-cludingthepaymentsforroyalties,licenses,patentsandsoon–agoodempiricalindicatorthatcanbeconsideredareasonablemeasureofthesustainabilityofthecountry’sexternalpositionistheratiobetweenitscurrentaccountdeficitanditsexports. thissimpleindicatorhasthefurtheradvantageofreflectingwelltheimpactoftheincreasesintheimportcoefficientsandthevolumeofimportsthathasbeensuchamarkedfeatureoftheexperiencesoftradeandfinancialopeningoftheso-called‘emergingmarkets’inthe1990s.

Short Term Liquidity and Crises

notethatwhileanunsustainabletrajectoryofnetforeignliabilitieswillsoonerorlaterleadtosomeslowdowningrowth,itwillnotnecessarilyleadtoafinan-cial or foreign exchange crisis. An external liquidity crisis generally onlyhappenswhenthecreditorssuddenlyrefusetorolloverdebtsthataredueinaparticularperiod.this,eveninasituationwherethecurrentaccountdeficit(thenetinflowofcapitaloveragivenperiod)isnotverybig,maymakethetotalstockofnon-renewedcreditlinesappearasaratherlargegrossoutflowofcapitalwhichcanquicklydepletethecountry’sforeignexchangereservesandtriggeraseriouscrisis. theconditionsthatwilltriggeranexternalliquidityorforeignexchangecrisisdependonthemagnitudeoftheforeignliabilitiesthatarematuringinrelationtothecountry’sreservesofforeignexchange.Itisinregardtothelatterrelation-shipthatthedistinctionbetweenshort-termdebt,long-termdebtandforeign

Capital flows to emerging markets: the Brazilian experience 225

directinvestmentacquiresgreatimportance.Itisclearthatthegreaterthema-turityofexternaldebtandthemorethecurrentaccountdeficithasbeenfinancedwithforeigndirectinvestment,thesmallerwillbethevalueofforeignliabilitiesthataredueinaparticularperiod.ontheotherhand,themoreurgenttheservic-ing of short-term external debt the greater will be the country’s external‘financialfragility’andtheriskofaliquiditycrisis. Wecansaythenthatagoodindicatoroftheexternalfinancialfragilityofacountryandevenoftheprobabilityofaforeignexchangecrisisisgivenbytheratiobetweenthecountry’sshort-termexternal liabilitiesand its foreignex-changereserves. Whenthisratiobecomesveryhigh,anyinterruptionofcapitalflowscausedbyadecisionnottorenewthecreditlinesthatareduecantrigger,andoftendoestrigger,aspeculativeprocess.thisprocessismagnifiedbytheexpectationsofdefaultorofexchangeratedevaluationsasthemagnitudeofthegrosscapitaloutflowsinvolvedaresuchthattheycanquicklywipeoutthecountry’sforeignexchangereserves. Indeed,ifweexaminethecircumstancesoftheforeignexchangeandliquiditycrisesthathavehappenedinvarious‘emerging’economiesinLatinAmerica,eastAsiaandeasterneuropewecandistinguishclearlybetweentheproblemsofforeigndebtsustainabilityandthatofexternalliquiditywiththehelpofthetwoindicatorsdiscussedabove. Somebasiccommonfeaturesofalloftheseexperiencescaneasilybeenu-merated.Firstofall, factorsexogenous to thedevelopingcountries,suchasfinancialinnovationsandderegulation,togetherwithareductioninuSinterestratesintheearly1990s,playedacentralroleinoriginatingcapitalflowstowardstheseeconomies.5

Asecondfeatureisthatcrises,(i.e.suddenreversalsofcapitalflowstogetherwithacollapseofassetpricesandoftheexchangerate)havealwaysbeenpre-cededbyasignificantincreaseintheratiobetweenshort-termexternalliabilitiesand foreign exchange reserves and alsoby an appreciationof the exchangerate.6

Athirdsalientfeatureisthattheimpositionofcontrolsonshort-termcapitalflows,whetheroftheinflowsasinChileinthefirsthalfofthe1990sorevenofoutflowsasinMalaysiaafter1997,haveworkedwellintermsofreducingthevolumeandincreasingthematurityoftheexternalliabilitiesofthesecountries.7

Basedontheliquidityindicatordiscussedabove,table11.1belowranksafew‘emergingmarket’countriesintermsoftheirshort-termexternalfinancialfragility. thesefactsandfiguresindicatethatamidsttheabundanceofforeignshort-termcapitalflows,theaccumulationofshort-termliabilitiesrelativetoavailablereserves(ashappenedinMexicoin1994,thailand,Malaysia,Indonesiaandkoreain1997,russiain1998,Brazilin1999andArgentinain2000),hasal-

226 Emerging markets and the financial architecture

Table 11.1 External short-term bank liabilities relative to official forex in selected countries (stocks in December 1998)

ShorttermCountry debt/reservestaiwan 0.18China 0.21India 0.28Malaysia 0.36Southkorea 0.57Chile 0.57thailand 0.83Mexico 0.92Brazil 0.93Indonesia 1.04Argentina 1.37russia 2.26

Source: (downloadedfromwww.oecd.org/dac/debt),oeCddatafromtheWorldBank,IMFandBIS.CalculatedbytheBIS.

ways led to a situation of worsening financial fragility and, with differentnationalvariations,toaforeignexchangecrisis. theinternationalevidenceshowsalsothatspeculativebetsagainstcountriesinwhichtheratiobetweenshort-termforeignliabilitiesandreservesissmallsimplydonotwork(seethecaseofHongkongin1997).thisdoesnotseemtodependverymuchonthetypeofexchangerateregimeorthe‘credibility’ofthefinanceministersoftheseeconomies,noronanygenericfiscalfundamentalsfavouredbytheorthodoxview. Althoughtheinstabilityoffinancialmarketsanduncertaintyaboutshort-termmovementsofassetpricesseemtohaveincreasedinthe1990s,thefinancialcrisisthathappenedinthesecountrieswasbasedonanobjectivecondition:theaccumulation of short-term foreign liabilities relative to foreign exchangereserves. thisaccumulationofshort-termdebtwasnotinevitableanditshowsthatthebehaviourofcentralbanksandfinanceministriesoftheemergingmarketsandtheirattitudesintermsofcontrollingtheprocessoffinancialliberalizationandtheconductofmonetaryandexchangeratepolicyingeneralisakeydeterminantofthepossibilityofcrisis. Weobservefromtheseexperiencesthatthereisnostrongcorrelationbetweentheexpansionofforeigntradeandtheincreaseinshort-termcapitalflows.Both

Capital flows to emerging markets: the Brazilian experience 227

theverydynamic,export-ledeastAsianeconomiesandtheslower-growingandlessopenLatinAmericaneconomieshavebeenhurtbyliquiditycrises.thusitseemsthatitisnotnecessarilythesizeofthecurrentaccountdeficitpersethatexplainstheliquiditycrisis.

Exports, the Current Account and Growth

turningnowtothequestionofthelongtermsustainabilityoftheforeignliabili-ties/exportrelationship,wemaynotethat,exceptunderextremecircumstances,asthisratiograduallydeteriorates,itcanbeandoftenisimprovedbydevalua-tionand/orbyslowingthegrowthofaggregatedemandandtheeconomy,andthusthecontainingthegrowthofimports.thusaneconomywhichhassustain-abilityproblemswithitsexternaldebtorpositiontendstobesloweddown.Fromthisslowdownaforeignexchangecrisismayormaynot‘emerge’dependingonthematuritystructureofthecountry’sforeignliabilitiesandthesizeofitscentralbankforeignexchangereserves. Forinstance,overthefirsthalfofthe1990theslowdownofthegrowthrateofkoreanexportsandtheincreaseinitsimportcoefficientsclearlysignalledthatgrowthcouldnotcontinueattheveryfastratesofthe1980s.that,however,wasnotthereasonforthecollapseofthewonin1997,whichwasduetoexces-sive short-term borrowing following the financial opening of the economy(ChangandYoo,1999;Medeiros,1998). thereissignificantautonomybetweentheproblemsoflonger-termsustaina-bilityandthatofshort-termliquidityalthoughonecananddoesaffecttheother.themainconnectionsbetweenthenaretransmittedthroughtherateofinterestandtheexchangerate.Short-termcapitalinflowsincreasewhenthedifferencebetweendomesticandinternationalinterestratesisbigenoughtocompensatefortheexpecteddevaluationofthecurrencyandthecountry’ssovereignriskpremium.Capitalflowstendtohurtthecompetitivenessofexportsandcheapenimportstotheextentthatwhenlarge,theytendtoleadtoexchangerateapprecia-tion.thisendsupaffectingnegativelythecurrentaccounttoexportsratio.this,byitsturn,maywellleadtodeflationarydemandpoliciesthatfurtherincreasethedomesticinterestrateandattractevenmoreshort-termcapitalinflows,in-creasingtheexternalfinancialliabilities.theresultmaybeacrisis,orelsea‘stop-and-go’patternofgrowthwithatendencytowardsovervaluation. Whiletheviewthatsustaininggrowingcurrentaccountdeficits(eveninrela-tiontoexports)ispossibleaslongastheyarefinancedby‘cold’ratherthan‘hot’moneyisstillthedominantone,weobservenoempiricalevidenceinthecurrentconditionsof theinternationaleconomythatpreviousgrossflowsofforeigndirectinvestmentwillsignalthefuturepersistenceofthoseflows,aswepointedoutabove.thatresultputsinquestiontheideathatforeigndirectinvest-mentisinherentlystable(Claessensetal.,1995,kregel,1996).

228 Emerging markets and the financial architecture

thehistoricalrecordandtheproblemsmentionedaboveshowthatlargein-flowsofforeigndirectinvestmentdonotseemtoconstituteastablesolutionforthesustainabilityproblem,unlessitgeneratesinthehosteconomyasufficientaccelerationofexportsthatcanfinancetheexpansionofimportsandotherout-flowsofdividends,royaltiesandsoonwhicharetraditionallyassociatedwiththistypeofinvestment.

CAPItALFLoWStoLAtInAMerICAAndtHeCASeoFBrAzIL

Latin America: from the Export Drive to the Import Boom

Afterthe1982Mexicandefault,mostofLatinAmericafounditselfwithoutfreshexternalsourcesoffinanceinaperiodwhenthetermsoftradehadwors-ened;thedemandforitsexportshadfallenwiththerecentworldrecessionandinternational interest rateswereat record levels.thiscombinationofeventsimposedasevereandprolongedbalanceofpaymentscrisisontheregion. thiscrisisresultedinaninterruptiontotheState-ledindustrialdevelopmentstrategyincountriessuchasBrazilandMexico. Ingeneraltheregionalreactiontothecrisiswasbasedonthecontrolofim-portsboththroughpolicy-inducedrecessionsandadministrativecontrolsandby the promotion of net exports through exchange rate devaluations.thesepoliciesledtoanincreaseinexportsandatthesametimetoeconomicstagna-tionandanexplosiveaccelerationofinflation.Astheeuropeaneconomywasinrecessionintheearly1980,thecounterpartofincreasedfactorservicepay-mentsandcapitaloutflowsof theregionwasanincreaseofLatinAmericantradesurpluswiththeuSA.However,sinceitsmainpurposewastoservicethedebtratherthanincreasingthecapacitytoimport(thathadbeenconstrainedthroughoutthedecadeintheregion)theLatinAmericanexportdriveingeneralcametogetherwithslowgrowthandhighinflation. Withtheabundanceofinternationalliquidityandafterthe‘securitization’oftheexternaldebtintheearly1990s,theexternalfinancingconditionsofLatinAmericachangeddrastically.Fromastrategyofpromotingexports,exchangeratedevaluationandrigidcontrolofimports(responsibleforthestagnationandhighinflation)theLatinAmericaneconomiesingeneralturnedtoastrategygearedtowardsattractinggrowingexternalcapitalinflowsinordertoremovetheexternalconstraintandresumesomegrowth,controllinginflationthroughcontrolofnominalexchangerateandintegratingdomesticfinancialmarketswiththeinternationalfinancialcircuit. WiththeexceptionofChile(whichdidnotallowexcessiverealexchangeraterevaluationorimposecapitalcontrolsontheinflows)andofColombia,the

Capital flows to emerging markets: the Brazilian experience 229

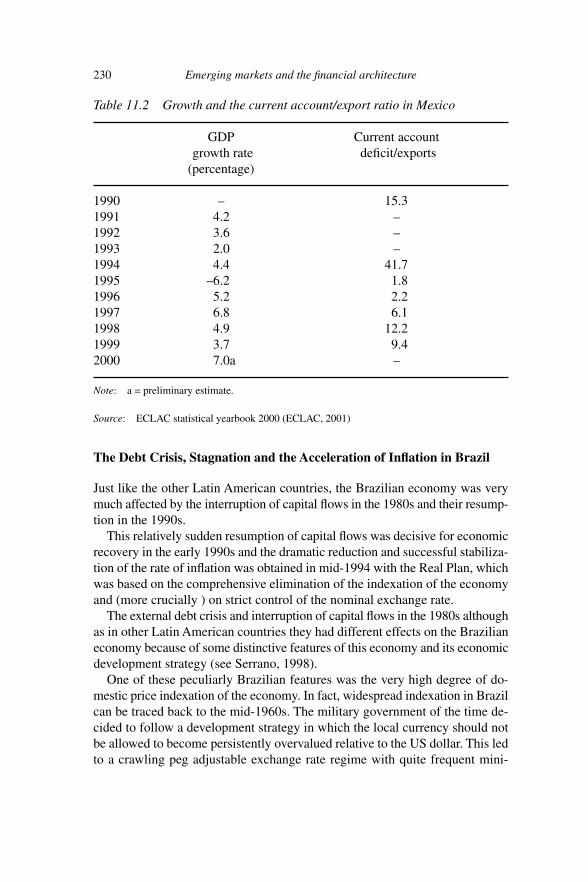

biggesteconomiesintheregionfollowedthe‘southerncone’strategythathadbeentriedandhadfailedinthelate1970sinArgentinaandChile.8Followingtradeandfinancialliberalization,countrieslikeArgentina,MexicoandBrazilstarted to receive large inflowsof international speculativecapital.Manyofthemseizedthisopportunityandappliedinflationstabilizationplansbasedontherelativestabilizationofnominalexchangerates(thistimeaccompaniedwithmeasurestodrasticallyreduceoreliminateinflationindexingofcontracts). thiswasonthewholequitesuccessfulinbringinginflationdown.thecom-binationoflargecapitalinflowsinacontextofeconomicrecovery,dismantlingofimportcontrolsandovervaluedrealexchangerates(duetothestabilizationplans)ledtoalargeincreaseinimportsacrossthewholeregion,particularlyfromtheuSA(Medeiros,1997,MedeirosandSerrano,1999). thecaseofMexico,oneoftheveryfewcountriesoftheregionthat,becauseofnAFtA,actuallysawahighrateofgrowthofexports,isaverygoodexampleofhowthedeteriorationofthecurrentaccountdeficittoexportsratio,duetotheimportboom,leadstoasituationofconstrainedgrowthevenwhentheinflowofFdIisquitelarge.Infact,in1990,MexicanexportsreacheduS$40.7billion,whichwasabout28percentofallLatinAmericanexports.In1998MexicoexporteduS$117.5billiondollarsincreasingitsshareofLatinAmericanex-portsto46percent. However,ratherthanbringingfastgrowth,theMexicanexportscametogetherwithanevenmorespectacularexpansionofimports.Sincethe1994crisisthatledtoa6percentfallingdPin1995,thetradebalanceshiftedbackintosur-plus.onaverage,theMexicaneconomygrewmodestlyinthe1990s,inspiteofhavinghadanabove-averageperformancecomparedwiththerestofLatinAmerica.WhathappenedinMexicowasaveryfastincreaseintheimportcoef-ficientandoftheremittancesassociatedwiththeforeigndirectinvestmentsthatelevatedtheratioofcurrentaccountdeficittoexportsfrom15.3percentin1990to41.7percentin1994.WithanincreasingshareofMexicanexportsbeingconcentratedinthemaquiladoraswherethecreationofdomesticvalueaddedisverylowandwiththenon-tradablesectorconstrainedbyarelativelybyarelativelyrestrictivemacroeconomicpolicy,theMexicaneconomydidnotman-agetotransformitsexportgrowthintoanengineforoveralleconomicgrowth.When,after1994therealexchangeratewasdevaluedandkeptlow,andparticu-larlyinthelastfewyearswhenoilpricesincreasedsharply,thecurrentaccountwasstabilizedandtheexpansionofexportsdidcometogetherwithahigherrate of economic growth. these years of faster expansion however merelycompensatedforthebig1995recessionandintheendinbothhalvesofthe1990sMexico(aftergrowingonaverageonly1.9percentinthe1980s)keptthedisappointingaveragerateofgrowth,foracountrywithsomuchcatchinguptodo,ofaround3.5percentascanbeseenintable11.2below.

230 Emerging markets and the financial architecture

Table 11.2 Growth and the current account/export ratio in Mexico

gdP Currentaccount growthrate deficit/exports (percentage)

1990 – 15.31991 4.2 –1992 3.6 –1993 2.0 –1994 4.4 41.71995 –6.2 1.81996 5.2 2.21997 6.8 6.11998 4.9 12.21999 3.7 9.42000 7.0a –

Note: a=preliminaryestimate.

Source: eCLACstatisticalyearbook2000(eCLAC,2001)

The Debt Crisis, Stagnation and the Acceleration of Inflation in Brazil

JustliketheotherLatinAmericancountries,theBrazilianeconomywasverymuchaffectedbytheinterruptionofcapitalflowsinthe1980sandtheirresump-tioninthe1990s. thisrelativelysuddenresumptionofcapitalflowswasdecisiveforeconomicrecoveryintheearly1990sandthedramaticreductionandsuccessfulstabiliza-tionoftherateofinflationwasobtainedinmid-1994withtherealPlan,whichwasbasedonthecomprehensiveeliminationoftheindexationoftheeconomyand(morecrucially)onstrictcontrolofthenominalexchangerate. theexternaldebtcrisisandinterruptionofcapitalflowsinthe1980salthoughasinotherLatinAmericancountriestheyhaddifferenteffectsontheBrazilianeconomybecauseofsomedistinctivefeaturesofthiseconomyanditseconomicdevelopmentstrategy(seeSerrano,1998). oneofthesepeculiarlyBrazilianfeatureswastheveryhighdegreeofdo-mesticpriceindexationoftheeconomy.Infact,widespreadindexationinBrazilcanbetracedbacktothemid-1960s.themilitarygovernmentofthetimede-cidedtofollowadevelopmentstrategyinwhichthelocalcurrencyshouldnotbeallowedtobecomepersistentlyovervaluedrelativetotheuSdollar.thisledtoacrawlingpegadjustableexchangerateregimewithquitefrequentmini-

Capital flows to emerging markets: the Brazilian experience 231

devaluations.thiscontinuousnominaldevaluationofthecurrencybyitsturnledtotheneedtoformallyindexinterestratesongovernmentbonds(thesocalled‘monetarycorrection’mechanism)inordertopreventcapitalflight.In-dexationthenspreadtoallfinancialcontractsandalsototaxesandtariffsonpublicutilitiesandintroducedanelementofinertiaininflationwhichatthesametimemadenecessaryorperhapsinevitable(eveninapoliticallyrepressiveregime)apartialbutlaterincreasingindexationofnominalwages.thelatterby its turn reinforced the inflationary inertia in inflation ratesgiving furtherstimulustowidespreadindexationofallcontracts. therefore,whentheexternalshocksoftheearly1980sandthedebtcrisishitBrazil,theeconomyalreadyhadaveryhighdegreeofindexationandarela-tivelyhighpersistentrateofinflation.thisexplainswhyinflationacceleratedsomuchandreachedsuchhighandpersistentlevelsinBrazilduringthe1980s.the debt crisis led to the so called ‘maxi-devaluations’ over and above thecrawlingpegasanattempttoaltertherealexchangerate,topromoteexportsandcutimportsinordertoobtainatradesurpluslargeenoughtoservicethedebtandmakeupforcapitalflight(thelatterbeingalessseriousprobleminBrazilbecauseofcapitalcontrolsandtheindexed,andontheaveragequitepositiveinrealterms,interestrate).thosemaxi-devaluationsledtoanaccelera-tionofinflationandledtofurtherincreasesininterestratesandthenwages.ontheotherhand,thesystemofgeneralizedindexedcontractsallowedtheeconomytooperatenormallyinspiteofrecordhighratesofinflation.thus,indexationatthesametimemadeinflationratesmuchhigherandmorepersistentthaninothercountriesoftheregionbutatthesametimepreventedthedisorganizationoftheeconomythathappensunderopenuncontrolledhyperinflation. Intheperiodbetween1982and1994manydifferenttypesofinflationstabi-lizationplanswereattempted.But,regardlessofsuchefforts,untiltherealPlantheBrazilianeconomylivedunderpermanentinflationaryconditionswithstrongtrendstowardshyperinflation,brieflycontainedbyincreasinglyineffectivesta-bilizationattempts.Bytheendofthedecadeannualinflationratesreachedfourdigits. AnotherfeatureofBraziliandevelopmentstrategythatwascrucialinexplain-ingthepeculiarperformanceoftheeconomyinthe1980swasthat,inmarkedcontrastwithmanyotherLatinAmericancountries(wheretheexternaldebtfi-nancedcapitalflight)fromthemid-1970sagoodpartoftheBrazilianexternaldebtwasusedtofinancetheSecondnationaldevelopmentPlanwhichinvestedheavilyinthecapitalgoodssectorandinfrastructure.thoseinvestmentswereinstrumentalinreducingthedependencyoftheeconomyonsomeimports(suchasoil,forinstance)andmoreimportantly,servedtocompletethelocalindustrialbase(includingsomeindigenoustechnologicalcapacity)andprovidedthecostexternalities(intransportation,energyandbasicinputs)thatallowedthecountrytobecomeamajorexporterofindustrialcommoditieswithinashortspaceof

232 Emerging markets and the financial architecture

time. this successful export performance coupled with the policy-inducedstagnationoftheeconomyandothermeasurestorationimports,allowedthecountrytoproducelargetradesurplusesafter1983fortenyears.Brazilianex-ports increased from uS$ 15 billion in 1979 to around uS$ 34 billion in1989. AlthoughrelativelysuccessfulinservicingthedebtandpreventingeconomiccollapsethisexportperformanceappearsdifferentlywhencomparedwithotherdevelopingcountriesoutsideLatinAmerica.Indeed,theaveragerateofgrowthofexportsinthe1980s,ofabout4.5percentayearwasbelowthegrowthofworldtradeandaroundonlyone-thirdthatofcountriessuchasChinaorkoreaoverthesameperiod. underthesecircumstancesthecontrolofimportswasmadeinevitableandeven then foreignexchange reserveswerenot stabilized.By1990Brazilianimportsincurrentdollarswerestillbelowthe1980levels(seetable11.4be-low).thewholeexportexpansionwasabsorbedbythedebtserviceanddidnotimprovethecapacitytoimport.WhentheBrazilianeconomyreturnedtotheinternationalfinancialcircuitintheearly1990s,itsindustryanditsoverallin-ternationalcompetitivenessweresignificantlyinferior,relativetotherestoftheworldthanatthebeginningofthe1980s. thiswholeprocessmadeBrazilachieveanaveragegdPgrowthrateofonly1.6percentinthe1980s.thiswasalittleworsethanMexico,substantiallylowerthanChile(3percent)andColombia(3percent),countrieswherethecapitalflowswherenotcutoffsodrasticallyandwereresumedearlier,butstillmuchbetterthanArgentina(–0.7percent)andmanyoftheothersmallercoun-triesintheregion.9

The Resumption of Capital Flows, the New Exchange Rate Policy and the End of Inflation

Import liberalization started inBrazil in1990when, followingverycloselyWorldBankadvice,Brazildismantledanumberofnon-priceimportrestrictionsandstartedreducingtariffs.However,sincetheeconomywasinrecessionatthebeginningof thedecadethevalueof importsonlystartedgrowingmoresubstantiallyafter1993whenamoresustainedeconomicrecoverybegan. InMay1991,animportantregulatorychangeinBrazil(thesocalled‘AnnexIV’), which allowed foreign ownership of domestic portfolio investmentsmarkedthebeginningofalargeinflowofcapital,afteralmosttenyearsofverysmallflows.10Inthatsameyearthecentralbankstartedthepolicyofcreatinganinterestratedifferentialbetweeninternalandexternalrateswaybeyondanypossibleexpectationofdevaluationoftheexchangerate(whichwasstillin-dexedtoinflationtoavoidovervaluation).thispolicystartedattractinglargecapitalinflows.giventhatthevalueofexportswasgrowingatarelativelyhigh

Capital flows to emerging markets: the Brazilian experience 233

rateintheperiod1992–4,thatimportshadnotyetstartedgrowingandthattherehadbeencutsintheinternationalinterestratethateasedtheservicingofthe‘old’externaldebt,theresultoftheseinitialsurgesofcapitalinflowswasafastaccumulationofreserves,whichmorethandoubledbetween1991and1992. theseeventsshowclearlytheexogenouscharacteroftheseinflows.Whentheybegantomount,theeconomywasstagnated,inflationwasmorethan400percentayear,andtheso-calledfundamentalswerefarfromright. Indeed,capitalinflowspickedupsomuchmomentumthatinspiteofthesubsequentimportboomandslowdownofexportsandmoregenerallyoftheincreaseinthecurrentaccountdeficit,thegrowthofforeignexchangereservesbetween1991and1996wasof539percent. Foranumberofreasons,mostlyrelatedtothedomesticpoliticalsituationandtheelectioncalendar,itwasonlyin1994thatthegovernmenttookfullad-vantageofthisnewexternalsituationtolaunchanew(andthissuccessful)radicalstabilizationplan,therealPlan. thisplan,likethefailed1986CruzadoPlan,wasbasedonstabilizingthenominalexchangerateandeliminatingindexationofwages,pricesandfinancialcontracts. themaindifferenceswereacertainlackofpreoccupationwithpossiblerealwagelosses,alongpreparatoryphasetosynchronizerelativepricesandothercontracts11andthemaintenanceofrecordhighinterestratesinordertoensureacontinuationoftheinflowofforeigncapital. Interest ratesweresetsohighwhenthemonetaryreformbeganthat theyquicklyledtoanominalappreciationofthenewcurrency,whichwassupposedtobepeggedonaone-to-onebasistotheuSdollarbuteventuallywentashighas85centsofrealtothedollarforashortwhile.theBraziliancentralbankthenfollowedapolicyoffrequentlyandgraduallymakingsmalldevaluations.thispolicywasrununtilearly1999but,assubsequenteventshaveshown,wasnotenoughtocorrectthechronicovervaluation.theplanwasextremelysuc-cessfulinbringinginflationdownandkeepingitlow.Inflationratesof43.1percentamonthinthefirsthalfof1994,fellto3.1percentinthesecondhalfofthatyearandto1.7percentinthefirsthalfof1995(CalcagnoandSainz,1999,p.13).Annualinflationwasbroughtdowntolessthan5percentin1998and1999,inspiteofthelargedevaluationinthelatteryear,showingthatthegovern-mentdidreallysucceedineliminatingindexationand‘realwageresistance.’12thebehaviourof therateof inflationandthenominalexchangeratecanbegaugedfromtable11.3below. therealPlanrepresentsacompletebreakwiththemacroeconomicpolicyofrelativerealexchangeratestabilitywhichhadbeenmaintainedmoreorlessconsistently(inspiteofeverything)sincethe1960sinordertoavoidcompro-misingtheexportperformanceoftheeconomy.

234 Emerging markets and the financial architecture

Table 11.3 Yearly rates of inflation and nominal exchange rate devaluation

Implicit real/uS$ gdPdeflator averageexchangerate 1991 416.7 497.91992 969.0 1011.41993 1996.1 1853.91994 2240.2 1888.91995 77.5 43.61996 17.4 9.61997 8.2 7.31998 4.7 7.71999 4.3 56.42000 8.6 –

Source: IPeAdAtAdatabase(www.ipeadata.gov.br).

thegovernmentshiftedtoapolicyoftryingtoachievethemaximumpossiblestabilityofthenominalexchangerateinordertocontrolinflationandpreventthereturnofindexation.thispolicyseemedalsotobestrictlynecessaryforthestrategyoffinancinggrowingtradeandcurrentaccountdeficits.

The Unsustainable Current Account and Slow Growth

thecombinationofanappreciatedcurrencyinanewenvironmentofliberalizedimports(whichwerefurtherliberalizedinthefirstmonthsaftermonetaryre-form) with a credit boom that followed the stabilizationnaturally led to anexplosionofimports. Veryquickly,monthlyfiguresforthegrowthofimportsmorethandoubled.Asexportscouldnotanddidnotfollowsuit,Brazilranatradedeficitin1995,aftermorethanadecadeofsurpluses.thefearofaMexican-stylebalanceofpaymentcrisisquicklymadetheauthoritiesputbrakesintheeconomymainlythroughmonetarypolicy(creditcontrolsandstratosphericinterestrates),butalso by attempts at controlling the growth of public expenditure and taxincreases. Indeed,inspitegrowinginterestpayments(reaching7.5percentofgdPin1998)thatseemtohavehadlittleifanyeffectonaggregatedemand,thehighestprimarydeficit in theperiodwas aroundoneper cent ofgdP in1996 and1997. thesepoliciesofcontainingthetrendgrowthofaggregatedemandhavebeenfollowedmoreorlessconsistentlyfrom1995tothebeginningof1999,avow-

Capital flows to emerging markets: the Brazilian experience 235

edlytocontroldemandinflationbutinfactdictatedmainlybythesurprisingandunexpectedever-worseningcurrentaccountfigures,anddoubtsabouttheirabilitytofinanceitadequately. duringthisperiodgdPgrowthwasbroughtdownfrom5.8percentin1994toameagre0.2percentin1998.eventhenthecurrentaccountdeficitasapro-portionofthegdPmeasuredincurrentdollarsswungfrompracticallyzeroin1994to4.3percentin1998. remittancesforpaymentsofprofitsandinterestsgrewfrom23percentofexportsin1994to39.9percentin1998,reflectingthehighdollarinterestratespaidtoforeigninvestorsinBrazilianassetsandalsoincreasingpaymentsofroyalties,patentsandlicenses,asBrazilprogressivelyabandoneditspolicyofcreatinglocal technologyandtheshift in itsdiplomaticpositionin termsofpaymentsfor‘intellectualpropertyrights’. Ifwelookatourfavouritemeasureofthesustainabilityofthecurrentaccount,whichisachangeintheratioofthecurrentaccountdeficittoexports,weseethatintheperiod1994–8thisindicatorshiftedfrom3.9to65.8,adeteriorationofapproximately1580percent.thishadtheinevitableconsequenceofincreas-ingthegrowthofBrazil’snetexternalliabilityposition,i.e.thesumofforeigndebtplusaccumulatedFdI.thisposition,accordingtosomeestimatesincreasedfromapproximatelyuS$165billionin1994toarounduS$303billionin1998.thecountry’snetexternalposition,calculatedasaratiotoexports,shiftedfrom3.8to5.9overthatsameperiod. table11.4belowcontainsdataforthemanyoftheindicatorsdiscussedaboveforBrazilinthe1990s. given the overvaluation and the misguided industrial policy strategy, thecurrentaccountwasclearlyonanunsustainablepath,evenwithever-slowinggrowth.tomakemattersworse,theincreaseinreservesandlargeandgrowingcurrentaccountdeficitswereoriginallyfinancedthroughtheaccumulationofahighlevelofshort-termdebtandportfolioinvestments. Aftertherussiancrisisofmid-1998thatledtoafallininternationalcom-moditypricesofmanyBrazilianexportsandtothedowngradingofBrazilbythe credit ratingagencies, the situationbecamecritical.A ‘preventive’ IMFagreementwasmadeand itwasmeant toavoidamajordevaluation. In themonthsthatfollowed,short-termcapitalquicklyflowedoutofBrazil,andthecountrylostalargeamountofforeignexchangereservesinafewmonths.Amajordevaluationbecameincreasinglyexpectedbythemarketinspiteofre-peateddenialsbybothgovernmentandIMFofficials. BanksstartedreducingtheirexposuretoBrazil.AccordingtoBaigandgold-fajn’s(2000)estimates,internationalbanksreducedtheiroverallexposuretoBrazilfromuS$84.6to62.3billionduring1998.thenetoutflowofshort-termcapitalwhichstartedin1997wasofmorethanuS$30billionduring1998(seetable11.4).

236

Tabl

e 11

.4

Mac

roec

onom

ic in

dica

tors

for

Bra

zil

exp

orts

Im

port

sg

dP

(gro

wth

)r

atio

of

netf

acto

rpa

ymen

ts

abro

adto

ex

port

s

rat

ioo

fcu

rren

tac

coun

tde

ficit

to

expo

rts

rat

ioo

fcu

rren

tac

coun

tde

ficit

to

gd

P*

rat

ioo

fne

tfor

eign

lia

bilit

ies

toe

xpor

ts

Fore

ign

dire

ct

inve

stm

ent

Inte

rnat

iona

lr

eser

ves

(mill

ion

uS$

)

Shor

t-te

rm

capi

tal

flow

s

1991

0.6

1.8

1.0

––4

.40.

04.

73–

94

06.4

–740

619

9213

.2–2

.3–0

.5–

17.2

1.5

4.15

19

2423

754

.3–2

844

1993

7.7

22.9

4.9

––1

.50.

04.

09

801

322

11.2

–443

219

9412

.931

.05.

823

.0–3

.90.

03.

812

035

388

06.2

–382

419

956.

850

.74.

227

.7–3

8.6

2.5

3.64

34

7551

840

.315

523

1996

2.6

7.0

2.7

33.4

–484

–3.0

4.15

116

6660

110

.148

5719

9711

.012

.03.

336

.6–5

8.1

–3.8

4.70

186

0852

172

.7–1

5517

1998

–3.5

–3.3

0.2

39.9

–65.

7–4

.35.

9328

541

445

56.4

–300

3219

99–6

.1–1

4.7

0.8

41.2

–52.

2–4

.57.

0230

254

363

42.3

–194

3**

2000

14.0

13.2

4.5

––4

4.7

–4.2

6.68

––

–

Not

es:

*g

dP

inu

S$;*

*u

pun

tiln

ovem

ber

1999

.

Sour

ces:

IP

eA

dA

tA(

ww

w.ip

eada

ta.g

ov.b

r/),

eC

LA

C(

2001

),M

igue

land

Cun

ha(

2001

;Bai

gan

dg

oldf

ajn

(200

0).

Capital flows to emerging markets: the Brazilian experience 237

thedebtrolloverrateforshort-termloansfellto0.62between1octoberand31december1998.InJanuary1999anewdirectorwasappointedtotheBrazil-iancentralbankwhotriedtoacceleratethedevaluationsgraduallyaccordingtoanewformula.thedecisionseemstohavetakentheIMFbysurprise.ItledtoalotofconfusionandapparentlytheBraziliancentralbankwasnotallowedtointervenetosupportthenewregimeusingfundswhichweredefactounderIMFcontrol.that,amidstintensespeculation,ledtothequickcollapseofthenewscheme.thecurrencywasallowedtofloat,andthenewcentralbankerwasdulyremovedandreplaced.theexchangeratesufferedwildgyrationsforsometime,andonlywhenyetanothercentralbankerwithtacitIMFpermissiontointervenewasappointeddidthemarketcalmdown. AfterthatBrazilofficiallyadheredtoa‘free’floatingexchangerateregimeandtoamonetarypolicyof‘inflationtargeting’mainlythroughnominalinterestratechanges.thefloatinghoweverwasfarfrom‘clean’andinterestratemanage-mentwasnotindependentofbalanceofpaymentsconsiderations.Interventionswerefrequentandsomeoftheinterestratechangeswereclearlymadewiththeexchangerateinmind.Inanycase,thefactthatformalindexationofinterestrates,exchangeratesandwageswereeliminatedpreventedtheexchangeratesupplyshockturningintoanacceleratinginflationspiral.thecrisis,andaverytightfiscalpolicyaimedatstabilizingtheinternaldebt-to-gdPratioinasituationofveryhighrealinterestrates,broughttheeconomytoastandstill. However,fromthesecondsemesterof1999arecoverybeganandtheecon-omyactuallygrew0.7percentinthatyear.Afterthesituationwasnormalized,capitalflowswereresumed.BanksreopenedcreditlinesalthoughnowwithapermanentlyreducedexposuretoBrazil.13thisturnedoutnotbeapressingproblemsincebythenforeigndirectinvestment,whichwasalreadyfollowingaveryfastrisingtrendsince1994,increasedevenfurthertorecordlevelsforafewyears.FdIflowsincreasedfromlittlemorethanuS$2billionin1994tomorethanuS$30billionin1999.Afterpeakingin2000,theFdIflowstarteddecreasingagainin2001raisingnewfearsabouttheexternalfinancingofthecountry. themainfeatureofthisFdIboomisthepredominanceofacquisitionsofexistinglocalfirms,whetheralreadyintheprivatesectororthroughprivatiza-tion,insteadoftheinstallationandexpansionoftheoperationsofforeignfirmsinthecountryasinthe1970s.Alsothesecapitalflows,contrarytonaiveofficialexpectations,havenothadamajorpositiveimpactonexportperformance,noraretheinvestmentsgearedtoimportsubstitution.onthecontrary,giventheconcentrationoftheseflowsonlargelynon-tradablesectors(especiallyservicessuchastelecommunications)andthenaturaltendencyofmultinationals(whenallowedbypolicy)toimportalargefractionoftheirinputsandcomponentstheFdIhashelpedtoincreasetheimportcoefficientsofanumberofsectorsoftheBrazilianeconomythathaveveryhighincomeelasticity.

238 Emerging markets and the financial architecture

Beforelookingatthedataonewouldhaveexpectedthatafterthe‘preventive’IMFagreement in1998and thedevaluationandcrisis inearly1999, thingswouldhavechangedandtheBrazilianeconomyandinparticularitscurrentaccountwouldbynowbeonasustainablegrowthpath.thatunfortunatelydoesnotseemtohavebeenthecase.Inspiteoftheveryslowgrowthin1999andthelargerealdevaluation,thecurrentaccountdeficitfellbyaboutuS$8.5bil-lion,alittlemorethanthefallinimports.exportsactuallyfellin1999becauseofthefallininternationalcommoditypricesandhadnotrecoveredtheircurrentdollarvalueof1998bytheendof2000. thechangeintheexchangerateregimeledtoasubstantialreductionininter-estratesandeasingofcredit,whichtogetherwithsomespontaneousimportsubstitutioninducedbythedevaluationmadetheeconomygrow4.4percentintheyear2000inspiteofthetightfiscalpolicy.However,thecurrentaccountdeficitseemstobestuckataround4percentofgdP.recentstudiesshowthatsuchdeficitswouldrequireveryhighaverageratesofexportgrowth,inexcessof10percentayear,almosttwicethehistoricalaverage,inordertobesustain-able(MiguelandCunha,2001). ontheotherhand,aseconomicgrowthrecoversimportsarebeginningtogrowfastagain.Moreovertherecent(2001)fallinflowsofFdI,preciselyastheglobalmarketsaregettingturbulentoverthetroublesofArgentina,hasmadetheBraziliancentralbankabandonitsforecastof4.5percentgrowthin2001andemitsomesigns,byraisinginterestrates,thatitmightbegettingreadytoslowtheeconomydownrevertingtoitsmoderatelymoreexpansionistpolicystanceadoptedafterthedustofthebigdevaluationsettled. Intheend,whatBrazilhastoshowforthisimmenseaccumulationofforeignliabilitiesisanaveragegrowthrateofgdPinthe1990sofmerely2.6percent,asinglepercentagepointmorethanintheso-called‘lostdecade’ofthe1980sandalmostawholepointlessthanthe3.3percentaveragegrowthrateforLatinAmericafrom1991to2000(eCLAC,2001).14

thestructuralreasonsbehindthiscontinuingexternalfragilityarerelatedtoanumberoffactors.First,tothesizeofthealreadyaccumulatednetforeignli-ability position and the associated remittances of factor services’ income.Anotherproblemistheveryhighincomeelasticityofindustrialimportsandtheratherlowincomeelasticityofexportsthatisbeingobservedevenafterthebigdevaluation.theseveryunfavourableelasticitiesaremainlytheresultofthere-specializationoftheBrazilianindustryandinparticularofthecapitalgoodsandintermediategoodsandcomponentssectors.thisre-specializationofBra-zilianindustrywasinducedbypoliciesanddisincentivesthatwereexplicitlymeantasanabandonmentofthestate-leddevelopmentstrategy,astrategythatmadeBraziloneofthefastestgrowingeconomiesintheworlduntiltheearly1980sbutthatwasseenbytheCollor(1990)andlatertheCardosoadministra-tions(1995–2002)ashavingproducedaninefficientandoutdatedmanufacturing

Capital flows to emerging markets: the Brazilian experience 239

sectorthatwouldbemodernizedwithouttheneedoftraditionalindustrialpolicymerelybyexposingthesystemtostrongforeigncompetition. thecurrentdifficultiesthatBrazilfacesarethedirectresultofthesepolicies.Facingthelossofsubsidiesandincentives,thedismantlingofalargepartoftheincipienttechnologicaleffortsofnationalresearchinstitutes,state-ownedenterprisesanduniversities,thedisorganizationofamessilyprivatizedinfra-structure,15anunfavourableexchangerate,amuchhighercostofcapitalandaslow-growing domestic market (that did not help in terms of economies ofscale),itisnotverysurprisingtofindthatsincetheearly1990thestructureofBrazilianindustrialexportshaschangedbackabit towardsmorenaturalre-source-basedgoodsandstandardizedindustrialcommodities.16

ontheotherhand,manyofthesamefactors,andtheopeningoftheeconomytoforeigncompetition,havegivenastrongimpetustothegrowinguseofim-portedcapitalgoodscomponentsandinputs(Brazilisnowanetimporterofrawcottonandthereisnotasinglemicrochipfactoryinthecountry)evenoftheproductsthatarestillbeingproducedinthecountry.the‘competitive’re-specialization of the Brazilian economy has resulted in a reduction of itsindustrialdiversification, inexportsmoreconcentratedinsectorswithlowertechnologicalcontentand lower internationaldemandgrowth rates.17At thesametimethisre-specializationbroughtwithalargeincreaseinimportcoeffi-cients,18creatinganinherenttendencytowardsgrowingdeficits.Itseemsthatthereversalofthissituationwilltakemuchmorethanasensibleexchangeratepolicy(althoughthatdoesreallyhelp)andwouldrequirerestartingthestate-leddevelopmentstrategywhichwouldentailrebuildingthestate’sregulatoryandincentivesframeworkandamajornewindustrialpolicyeffort.thatisasdifficulttodoasitsoundsevenifthereisthepoliticalwill(sinceithasbeendoneinthepast)butitisextremelyunlikelytohappeninthenearfuture.

ConCLudIngreMArkS

Inthischapterwehavearguedthatinthecurrentfloatingdollarstandardthebalanceofpaymentssituationfacingtheemergingmarketsischaracterizedbyabasiccontradiction.ononehand,itisextremelyeasytoattractlargeamountsofforeigncapital.ontheotherhand,itbecomesmoreandmoredifficulttode-liverthefastgrowthofexportsthatisanecessaryconditionforthefinancialservicingoftheseinflows. thisbasiccontradictionisgreatlystrengthenedincountriesthathavefol-lowedmorecloselythe‘Washington-consensus’fashionablepackageoftradeandfinancialliberalizationtogetherwiththecontrolofnominalexchangerates.Inthesecases,theamountsofcapitalattractedareevenbiggerbutatthesametimethetendencytowardsovervaluation,deindustrializationanddismalexport

240 Emerging markets and the financial architecture

performancearemuchstronger.Moreover,therelativelackofcontrolofshort-term capital movements does add to the unsustainable trend of that currentaccountalargeprobabilityofanexchangeratecollapseandanexternalfinancialcrisis. Inourview thecaseofBrazil in the1990 illustratesverywell thesedangers.

noteS

* AssociateprofessorsattheInstitutodeeconomia,universidadeFederaldoriodeJaneiro(uFrJ),Brazil.e-mailaddresses:[email protected]@openlink.com.br.

1. InwhatwastobehislastbookHicks(1989)noticedthatfromthebeginningofthe1980s,theuSAhadtakenforitselftheresponsibilityofmakingtheuSdollartheinternationalcur-rencyandthuscorrectlyadopteda‘passive’attitudetowardsitsbalanceofpaymentsresults.However,Hicksaskedhimselfifthisrolecouldbeperformedbya‘weak’currencylikethedollar.By‘weak’Hicksmeansthecurrencyofacountrythattendstoruncurrentaccountdeficits.Morethantenyearslater,theanswerseemstobeyes,itcananditdoes.

2. Medeiros(1997)showedhowtheFdIexportconnectionfoundinAsiainthe1980swasaproductofparticularcircumstancesinvolvinguStradepolicies,theJapanesereactiontoyenrevaluationandlocalstatedevelopmentpoliciesandcouldnotbegeneralizedtoLatinAmerica.MorerecentlyAgosinandMayer(2000)haveconfirmedeconometricallythatFdIdidseemto‘crowdin’investmentinAsiawhileitseemsto‘crowdout’investmentinLatinAmerica.

3. Indeed,formostdevelopingcountries thesameratesofgrowthareassociatedwithmuchbiggertradedeficitsthaninthepast.

4. Asshowbykregel(1996),ifthecapitalaccountisreallyopen,eventhecapitalthatcameinasFdImayquicklyandeasilytransformitselfintospeculativecapital,somethingthatweak-enssomewhat the idea thatexternalfinancingviaFdIwouldexpose theeconomyless toexchangeratespeculationandexternalliquiditycrises.

5. SeeamongothersCalvoetal.(1993).thecapitalflowstowardLatinAmericaintheearly1990sdependedheavilyontheloweringofinterestratesandregulatorychangesintheuSA:‘themostsalientchangesweretheapprovalofregulationS.andrule144awhichreducedtransactionandliquiditycostsfacedbydevelopingcountriesinapproachingcapitalmarketsthere’p.128.

6. SeerodrikandVelasco(1999)andkaminskietal.(1998). 7. SeeFfrench-davisandreisen(1997). 8. InitiallyChileandArgentinafollowedapolicyofpeggingthenominalexchangeratebetween

1978and1982(withouteliminatingdomesticindexingclausesinwagesandcontracts),pre-cededbywide-rangingtradeandfinancialliberalization.Capitalflightplusthefastgrowthofexternalliabilities,atamomentwheninternationalinterestrateswhereatrecordhighlevels,ledtoaseriouscrisisandtheinsolvencyofthedomesticfinancialsystem.InbothcountriesthisledtheStatetotakeovertheprivatesectorexternaldebt,tonationalisemanybanksandcontrolimportsagain.

9. datafromeCLAC(2001).10. SeeCarneiro(1997)11. Synchronizationwasachievedthroughaspecialtransitoryunitofaccount,theurV(unitof

realValue)bywhichwageswerecompulsorilyconvertedattheiraverageleveloveraperiod,whileotherpriceswerefreelyandvoluntarilyconvertedatanydesiredrate.

12. Inthisthegovernmentwashelpednotonlybyweakenedunionsandhighunemploymentbutalsoby thefavourable trendofrelativepricesoffoodstuffs,whichhavebeenfollowingalonger-rundownwardtrendduetothemodernizationoflarge-scaleBrazilianagriculturesincethe1980sandbytheresumptionofeasy(butnotcheap)consumercredit,whichgavetoalargenumberofpoorerBrazilianstheopportunitytobuyconsumerdurables.

13. notethatinthecaseofBrazil,thedevaluationdidnotcausebankingcrises.domesticbanks

Capital flows to emerging markets: the Brazilian experience 241

werenotmuchindebtinforeigncurrencyandhadbeen‘strengthened’byamajorcentralbankprogramme,Proer,justafterthe1994stabilisation.SeeCalcagnoandSainz(1999).

14. Brazilwhichgrewaround7percentayearfrom1945untilthelate1970sbecamealow-growth country. In the 1990s it grew less thanArgentina, Bolivia, Chile, Costa rica, elSalvador,guatemala,Honduras,Mexico,nicaragua,Panama,Peruandthedominicanre-public(eCLAC,2001).

15. themostglaringcaseisthatofelectricity.thepartialprivatizationlackofanadequateregula-tory framework, together with the government not allowing the still state-owned powergeneratorstoinvesthavemadeinvestmentinthatsectorfallfromarounduS$8billionayearinthe1980stoarounduS$3billioninthe1990s.notsurprisinglyenergyrationingschemesareprobablygoingtobeintroducedinthenextfewmonths.

16. Asaresultofthisanti-exportpolicybiasin1998theBrazilianshareofworldexportsin1998was lower than 1980 while over the same period korea’s share doubled and China’strebled.

17. Accordingtoarecentstudy,theBrazil’sshareinexportmarketsclassifiedas‘verydynamic’fellfrom20percentto13percentduringthetwohalvesofthe1990s.thesechangeshap-pened in thecompositionofexportsnotof imports that remainconcentrated in the ‘verydynamic’sectors.SeeIedI(2000).

18. AccordingtoMesquita(2000)theshareofimportsonthevalueofgrossoutputinBrazilianmanufacturingindustryincreasedfrom5.7in1990to20.3in1998.overthesameperiodtheratioofexportstogrossoutputincreasedfrom9.4percentto14.8percent.

reFerenCeS

Agosin,randr.Mayer(2000),‘FdIindevelopingcountries:doesitcrowdindomesticinvestment’,unCtAddiscussionPaperno.196,February.

Baig,t.andI.goldfajn(2000),‘therussiandefaultandthecontagiontoBrazil’,textoparadiscussãono420,departamentodeeconomia,PuC-rio,May.

CalgagnoA.andP.Sainz(1999),‘LaeconomiaBrasilenaanteelPlanrealesucrisis’,temasdeCoyunturano.4,CePAL,Santiago,July.

Calvo,g.,L.LeidermanandC.reinhart(1993)‘CapitalInflowsandrealexchangerateAppreciationinLatinAmerica’,IMF,staffpapers,40(1).

Carneiro, d. (1997), ‘Flujos de Capital y desempeño económico en Brasil’, in r.Ffrench-davisandH.reisen(eds),Flujos de Capital e Inversion Productiva,Santia-go:CePAL,McgrawHill.

Chang,H.-J.andYoo,C.-g.(1999),‘thetriumphoftherentiers?the1997koreancrisisinahistoricalperspective’,CenterforeconomicPolicyAnalysis,newSchool,newYork.

Claessens,S.;M.dooleyandA.Warnes(1995),‘Portfoliocapitalflows:hotorcold?’,World Bank Economic Review,9(1),January.

domar,e.(1950),‘theeffectofforeigninvestmentonthebalanceofpayments’,Ameri-can Economic Review.

eCLAC(2001),Statistical Yearbook 2000,Santiago.Ffrench-davis, r. and H. reisen (1997), Flujos de Capital e Inversion Productiva,

Santiago:CePAL,McgrawHill.Hicks,J.(1989),A Market Theory of Money,oxford:Clarendon.IedI,(2000),‘Abertura,PolíticaCambialeComércioexteriorBrasileiro–Liçõesdos

Anos90ePontosdeumaAgendaparaaPróximadécada’,athttp://www.iedi.org.br/.

kaminsky,g.,S.LizondoandC.reinhart(1998),‘Leadingindicatorsofcurrencycrises,’IMF,staffpapers,45(1),March.

242 Emerging markets and the financial architecture

kalecki,M.([1972]1982),‘FormasdeAjudaexterna:umaAnáliseeconômica’,inJ.Miglioli(ed.),Kalecki,SãoPaulo:Ática.

kregel,J.(1996),‘riscoseImplicaçõesdaglobalizaçãoFinanceiraparaaAutonomiadasPolíticasnacionais’,Economia e Sociedade,7,december.

Medeiros,C.(1997),‘globalizaçãoeInserçãoInternacionaldiferenciadadaÁsiaedaAmericaLatina’,inM.tavaresandJ.Fiori(eds),Poder e Dinheiro,riodeJaneiro:Vozes.

Medeiros,C.A.(1998),‘raizesestruturaisdaCriseFinanceiraAsiáticaeoenquadra-mentodaCoréia’,economiaeSociedade,11,Campinas.

Medeiros,C.A.andF.Serrano(1999), ‘PadrõesMonetários InternacionaiseCresci-mento’, in J.LuísFiori (ed.)estadoseMoedasnodesenvolvimentodasnações,Vozes.riodeJaneiro.

Mesquita,M.(2000),‘AIndústriaBrasileiranosAnos90.oquejásepodedizer?’,uSP,IPe,textoparadiscussão.

Miguel P. and J. Cunha (2001), ‘AVulnerabilidade externa do Brasil’, República ,April.

Prebisch,r.(1950),‘estudoeconômicodaAméricaLatina’,inr.Bielschowsky(ed.)(2000),Cincuenta Anos de Pensamento na CEPAL:riodeJaneiro,record.

rodrik,d.andA.Velasco(1999),‘Short-termcapitalflows’,WorldBank,processed.Serrano,F.(1998)‘tequilaoutortilla:notassobreaeconomiabrasileiranosnoventa’,

Archetypon,6,(18)September–december.Serrano,F.(1999),‘doouroImóvelaodólarFlexível’,Ie-uFrJ,processed.