capital market assumptions - health | aon rest of the market has been a net seller in aggregate ......

TRANSCRIPT

Capital Market AssumptionsAs of September 30, 2014

Aon HewittConsulting | Investment Consulting Practice

Risk. Reinsurance. Human Resources.

2 Capital Market Assumptions

Buyback bonanza – short term gain for longer term pain? . . . . . . . . . . . 3

Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Government bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Inflation-linked government bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Investment grade corporate bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

US high yield debt and emerging market debt . . . . . . . . . . . . . . . . . . . 9

Equities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Private equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Hedge funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Correlations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Capital market assumptions methodology . . . . . . . . . . . . . . . . . . . . . . 14

Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Table of contents

Aon Hewitt 3

Buyback bonanza – short term gain for longer term pain?

Economic growth has been weak, corporate revenue

growth nowhere to be found and earnings per share

growth has ticked along gradually yet US equities have

shot the lights out in terms of returns. How to make

sense of it all? Well, one explanation lies in corporate

buybacks – the act of companies repurchasing their

own shares in the market. These have become a really

important feature of the equity market environment

with wide ranging implications for both the near

term and long term prospects for equity markets.

This article is an abbreviated version of a recent research

note written by Aon Hewitt’s Global Asset Allocation team

which has been adapted for the purposes of this quarter’s

Capital Market Assumptions publication. Attention here

is focused on the US equity market where buybacks

have always been more common than elsewhere. If

you would like a copy of the original longer research

note then please contact your Aon Hewitt consultant.

A historic perspective

Dividends have traditionally represented the method

used by companies to return cash to shareholders and,

on the face of it, companies appear to have become less

generous over time. So far this millennium, dividend

payout ratios (the proportion of earnings that are paid

out in dividends) have averaged only around 35%, well

below the 50% average of the previous three decades.

However, this is because dividends are no longer the

only game in town when it comes to cash distributions.

Companies have increasingly turned to share buybacks

as an alternative means of returning cash to shareholders.

According to Standard & Poors (‘S&P’), over 80% of S&P

500 companies bought back shares during the second

quarter of 2014 and buybacks have been significantly

outstripping dividends for most of the past 10 years.

Consequently, though dividend payout ratios

have been low, when buybacks are included,

payout ratios have, in fact, been much higher.

Companies have been using around 85% of their

earnings to pay dividends and buy back stock.

Source: S&P

Dollar value of dividends and buybacks: S&P 500 ($bn)

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

200

180

160

140

120

100

80

60

40

20

0

Dividends Buybacks

4 Capital Market Assumptions

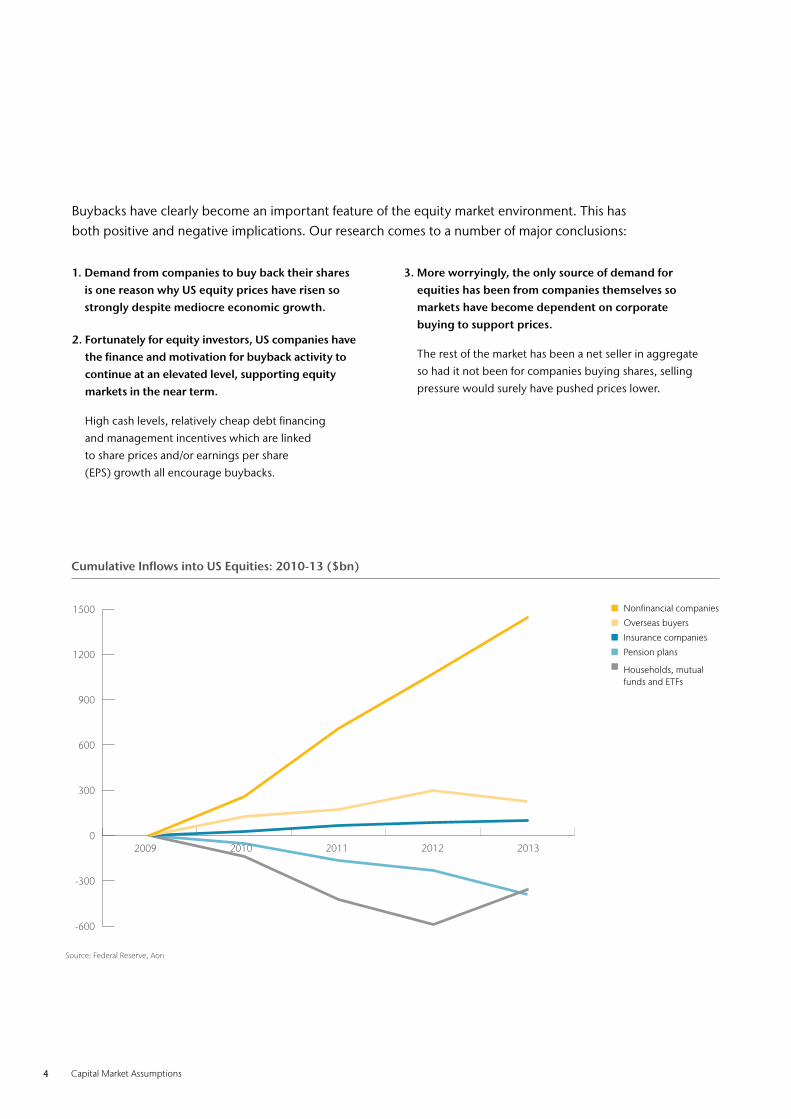

Buybacks have clearly become an important feature of the equity market environment. This has both positive and negative implications. Our research comes to a number of major conclusions:

1. Demand from companies to buy back their shares is one reason why US equity prices have risen so strongly despite mediocre economic growth.

2. Fortunately for equity investors, US companies have the finance and motivation for buyback activity to continue at an elevated level, supporting equity markets in the near term.

High cash levels, relatively cheap debt financing

and management incentives which are linked

to share prices and/or earnings per share

(EPS) growth all encourage buybacks.

3. More worryingly, the only source of demand for equities has been from companies themselves so markets have become dependent on corporate buying to support prices.

The rest of the market has been a net seller in aggregate

so had it not been for companies buying shares, selling

pressure would surely have pushed prices lower.

Source: Federal Reserve, Aon

Cumulative Inflows into US Equities: 2010-13 ($bn)

-600

-300

0

300

600

900

1200

1500

2009 2010 2011 2012 2013

Nonfinancial companies

Overseas buyers

Insurance companies

Pension plans

Households, mutual funds and ETFs

Aon Hewitt 5

4. Further buybacks may support share prices or even push them higher but buying back shares when valuations are expensive is value-destructive in the long run.

Buybacks are value-accretive for a company when they

are bought back for below their ‘fair value’. They are

effectively buying them back on the cheap. However,

the opposite is also true and buybacks can have a

negative long term impact if they take place when

shares are overvalued. Current equity markets remain

fully valued on most measures and expensive on others

so although high levels of buybacks should continue

to support prices in the near term, the longer term

impact of buying back shares at current levels will be

at best neutral, and at worst, value-destructive.

5. Headline EPS growth figures overstate underlying earnings growth due to the impact of buybacks. Buybacks which reduce the number of shares outstanding

will lead to EPS growth outpacing overall earnings growth.

Across the S&P 500 overall, Barclays estimate that, on

average, companies have benefitted from a 1-2% EPS

growth boost as a result of buyback activity but in some

cases the impact has been much larger. For example,

Apple’s Q2 earnings increased by around 12% but EPS

grew by almost 20%. This is not genuine growth but

instead has been manufactured by Apple’s buyback

program! Higher EPS figures can lead to higher share

prices as analysts often value companies based on their

EPS. By buying back shares, a company could potentially

inflate both its EPS and, as a consequence, its share price.

There is an argument that one reason for the popularity

of buybacks is that management remuneration packages

are often linked to EPS growth and this could help explain

the upsurge in buyback activity in the 2000s. Unless there

is a dramatic change to remuneration practices, which

there is no reason to expect without regulatory change,

management will continue to be incentivized to utilize

buybacks as a means of boosting their take-home pay.

6. If sustained, current levels of buybacks could do long term damage to the earnings capacity of listed companies, and with it, long term prospects for economic growth and equity market returns.

By choosing to pay out the vast majority of their profits

through a combination of buybacks and dividends,

companies are retaining only a small proportion of their

profits within the business to generate future growth.

If current profitability and payout ratios were to be

maintained then our calculations suggest that companies

would struggle to generate much more than 2% nominal

earnings growth on a sustainable basis. This would have

a disastrous impact on economic growth and longer term

equity market prospects. Current buyback policies may lead

to near term gains but at the expense of longer term pain.

Implications for our Capital Market Assumptions

Our expectation is that as the economic recovery

progresses and companies grow more confident regarding

the outlook, they will divert cash away from buybacks

and towards profitable investment opportunities.

Indeed, when looking through the long term lens of our

Capital Market Assumptions, we look past the current

high payout ratio and instead assume that in the long

run, companies pay out the proportion of their earnings

(through dividends and/or buybacks) that allows them to

maintain their growth at sustainable levels. This payout

ratio is significantly below current levels. Current high

payout ratios are unsustainable in the long run.

When setting our Capital Market Assumptions, we make the

simplifying assumption that long term sustainable payout

ratios are broadly comparable across the developed world.

However, we assume that emerging market companies pay out

a smaller proportion of their earnings as a greater proportion

must be retained in order to finance their faster growth rates.

EPS=Earnings

Number of shares oustanding

6 Capital Market Assumptions

Inflation

Realized inflation has been falling on a global basis but

despite the concern that has been raised over the

potential for very low inflation or deflation across many

countries, consensus expectations for longer term

inflation remain relatively well grounded. CPI inflation

expectations have been downgraded slightly but inflation

is expected to be relatively close to central banks’ 2%

target level over the next 10 years in the US, UK and

Canada. Nearer term expectations for European inflation

have fallen further but inflation is expected to pick up in

later years, raising the 10 year assumption to 1.7%.

The Japanese authorities have undertaken huge amounts

of monetary stimulus with an objective to generate growth

and break the hold deflation has had over the economy,

attaining a new higher inflation target of 2%. The consensus

has consequently been revising up inflation expectations

for Japan but remains unconvinced that the 2% inflation

target will be achieved on a sustainable basis. Japanese

inflation is expected to be around 1.6% per annum over the

next 10 years in Japan. Though below the 2% target, this is

significantly higher than the experience of the past decade.

USD GBP EUR CHF CAD JPY

CPI Inflation (10yr assumption) 2.2% 2.1% 1.7% 1.1% 1.9% 1.6%

RPI Inflation (10yr assumption) – 3.1% – – – –

Aon Hewitt 7

Government bonds

We take French bonds to represent Eurozone bonds, as there is a

reasonably liquid market in French inflation-linked bonds and we

want to ensure consistency between the nominal and inflation-

linked government bond returns. Our calculation of a weighted

average Eurozone government bond yield leads to a figure which

is slightly higher than the yield on French government bonds.

Our analysis therefore supports the use of French bonds as a

proxy for Eurozone bond portfolios, where these portfolios do

not have a large exposure to the higher yielding periphery.

Bond markets had a ‘taper tantrum’ in May/June 2013 when

the US Federal Reserve suggested that it was ready to consider

tapering its quantitative easing program. Yields moved sharply

upwards and ended the year much higher than before the

Federal Reserve had spoken. However, experience in 2014 so

far has been counter to what was very much a consensus view

at the start of the year. Rather than continuing to move higher,

yields have fallen back quite markedly and yield curves have

flattened – long duration yields have fallen by more than short

duration yields. Key reasons for this lie in the deterioration

in the European situation and also falling inflation rates.

The European recovery has gone into reverse during 2014.

Economic weakness and deflationary concerns mean that the

European Central Bank (‘ECB’) has eased monetary policy further,

cutting interest rates and making cheap funds available to the

banking sector. This has pushed European yields down sharply

and further than elsewhere, particularly at short durations.

Europe is a large part of the global economy and the

deterioration in the European situation has raised concerns

over the impact on growth prospects for other economies.

Inflation has also been on a declining trend on a global basis

and could fall further in the near term given falling commodity

prices. Both a weaker growth environment and declining

inflationary pressures mean that central banks are under less

pressure to raise interest rates and a slower more gradual

approach is likely thereafter. For example, at one stage markets

were pricing in a strong likelihood that the Bank of England

would raise interest rates before 2014 was over. Things have

changed however and expectations for the first rate rise

have since been pushed back towards the end of 2015.

These factors have been major contributors to lower fixed

income yields and flatter yield curves. As a result of this, our

return assumptions for government bonds are now lower than

at the start of the year in local currency terms, with assumptions

for short duration bonds falling by more than long duration

bonds. The short duration assumptions have fallen by more

because the flattening in yield curves means that the average

yield on these bonds over the projection period is a lot lower

than at the start of the year. The larger downward moves in

European bond yields lead to relatively large reductions in

European fixed income bond assumptions during 2014.

Significantly lower yields lead to much lower return

assumptions for Swiss and Japanese government bonds

in local currency terms.

USD GBP EUR CHF CAD JPY

US 5yr 2.5% 2.4% 2.0% 1.4% 2.2% 1.9%

15yr 3.4% 3.3% 2.9% 2.3% 3.1% 2.8%

UK 5yr 2.4% 2.3% 1.9% 1.3% 2.1% 1.9%

15yr 3.4% 3.3% 2.9% 2.3% 3.1% 2.9%

Eurozone 5yr 1.6% 1.5% 1.1% 0.6% 1.3% 1.1%

15yr 2.8% 2.8% 2.3% 1.8% 2.6% 2.3%

Switzerland 5yr 1.5% 1.4% 1.0% 0.5% 1.2% 1.0%

15yr 2.3% 2.2% 1.8% 1.3% 2.0% 1.8%

Canada 5yr 2.3% 2.2% 1.8% 1.3% 2.0% 1.8%

15yr 3.1% 3.1% 2.6% 2.1% 2.9% 2.6%

Japan 5yr 1.0% 0.9% 0.5% -0.1% 0.7% 0.4%

15yr 1.7% 1.6% 1.2% 0.6% 1.4% 1.2%

10yr Annualized Nominal Return Assumptions

8 Capital Market Assumptions

Inflation-linked government bonds

We have taken French bonds to represent Eurozone

bonds, partly because there is a reasonably liquid market

in French inflation-linked bonds. Our analysis of nominal

government bonds also suggests that French bonds are

a reasonable proxy for Eurozone government bonds so

we make the same assumption here for consistency. The

bonds represented are linked to Eurozone inflation.

We formulate return assumptions for 10 year US and

Eurozone inflation-linked government bonds rather than

15 year bonds. This is because we think that the absence

of inflation-linked bonds at the longest durations in these

markets can lead to misleading 15 year bond return

assumptions. We also no longer publish a 5 year duration

Canadian inflation-linked government bond assumption

due to the lack of short duration bonds in this market.

A similar story holds for inflation-linked as for nominal

government bonds when, after the large rises seen in

2013, real yields have fallen back in 2014. Short duration

real yields are in negative territory for all of the markets

covered in our Capital Market Assumptions and are even

negative at long durations in the UK and Europe. Low real

yields lead to low return assumptions for these bonds.

A second factor influencing inflation-linked bond return

assumptions is inflation expectations. In this respect, returns

from UK index-linked gilts benefit in relative terms compared

with the other markets by virtue of the fact that returns on

these bonds are linked to UK RPI inflation. This has an impact

because other regional inflation-linked bond returns are

linked to CPI inflation and this is assumed to be much lower

than UK RPI inflation. UK real yields remain well below the

level of the other markets so if it were not for the difference

between RPI and CPI inflation, the return assumption for

UK index-linked gilts would be much lower compared

with the other regions than shown in the table above.

USD GBP EUR CHF CAD JPY

US 5yr 2.9% 2.8% 2.4% 1.8% 2.6% 2.4%

10yr 2.9% 2.8% 2.4% 1.8% 2.6% 2.4%

UK 5yr 2.6% 2.6% 2.1% 1.6% 2.4% 2.1%

15yr 2.3% 2.2% 1.8% 1.2% 2.0% 1.7%

Eurozone 5yr 2.1% 2.0% 1.6% 1.0% 1.8% 1.5%

10 yr 2.0% 2.0% 1.5% 1.0% 1.8% 1.5%

Canada 5yr - - - - - -

15yr 2.4% 2.4% 1.9% 1.4% 2.2% 1.9%

10yr Annualized Nominal Return Assumptions

Aon Hewitt 9

Investment grade corporate bonds

Corporate bond returns depend on both a government yield

component and a credit spread component but also take account

of losses arising from defaults and bonds being downgraded.

As with all fixed income assets, the decline in government

yields during 2014 has put downward pressure on our

corporate bond assumptions. However, in addition, credit

spreads in many regions have declined and this means that

corporate bond return assumptions have generally fallen by

a larger amount than the government bond assumptions.

USD GBP EUR CHF CAD JPY

US 5yr 3.2% 3.1% 2.7% 2.1% 2.9% 2.6%

10yr 4.4% 4.4% 3.9% 3.4% 4.2% 3.9%

UK 5yr 3.2% 3.2% 2.7% 2.2% 3.0% 2.7%

10yr 3.8% 3.8% 3.3% 2.8% 3.6% 3.3%

Eurozone 5yr 1.9% 1.8% 1.4% 0.8% 1.6% 1.3%

10yr 2.6% 2.6% 2.1% 1.6% 2.4% 2.1%

Switzerland 5yr 1.8% 1.7% 1.3% 0.7% 1.5% 1.2%

10yr 2.2% 2.1% 1.7% 1.1% 1.9% 1.6%

Canada 5yr 3.3% 3.3% 2.8% 2.3% 3.1% 2.8%

10yr 4.2% 4.1% 3.7% 3.1% 3.9% 3.6%

Japan 5yr 1.1% 1.1% 0.6% 0.1% 0.9% 0.6%

10yr 1.3% 1.2% 0.8% 0.3% 1.0% 0.8%

After having fallen to very low level, the high yield debt credit

spread increased by a large 0.9% during the third quarter.

This benefits future return expectations for high yield debt

although low government yields continue to be a drag on

long term prospects. Taking these points together as well as

allowing for average default experience, US high yield debt is

now assumed to return 4.2% a year over the next 10 years.

When the US first mentioned that it may be ready to consider

tapering, emerging market assets were among the worst

affected, suffering very poor performance.

This raised the credit spread that could be earned on US

dollar denominated debt. This credit spread subsequently

declined but remains elevated relative to US high yield debt.

The differing movements in these credit spreads mean that a

credit return premium has opened up for emerging market

debt relative to high yield debt. As with high yield debt,

lower Treasury yields have put downward pressure on the

US dollar denominated emerging market debt assumption,

which stands at 4.7% a year as at 30 September.

US high yield debt and emerging market debt

10yr Annualized Nominal Return Assumptions

10 Capital Market Assumptions

Equities

Our equity return assumptions are driven by market valuations,

earnings growth expectations and assumed payouts to

investors. The price you pay is one of the single biggest

drivers of returns, even over the long term. Looking back over

recent experience, strong equity market performance has

been driven more by increasing valuations than increasing

profits. Therefore, as markets have become more expensive,

our equity return assumptions have consequently fallen.

UK equities have a higher return assumption than the other

developed markets. The main reason for this is that this equity

market is currently the ‘cheapest’ of the developed markets in

valuation terms. As at 30 September, UK equities were trading

on a multiple of around 14 times our 2014 earnings assumption.

In contrast, US equities were valued at over 17 times our 2014

earnings assumption. Investors in UK equities are therefore

paying less for expected future earnings, which raises the

return assumption for the UK market relative to elsewhere.

Emerging market equities have significantly underperformed

developed markets over the past few years for a variety of

reasons including a reduction in emerging market growth

prospects and more recently, concerns over the impact of

less accommodative US monetary policy. This cheapened

the relative valuation of emerging market equities and, even

after allowing for a reduction in emerging market growth

prospects, has led to an increased return premium opening

up for emerging market equities over developed markets.

The earnings growth component of our equity return

assumptions comprises both near term and longer

term elements. While our Capital Market Assumptions

process typically involves using consensus inputs, for

some time we have believed that the consensus of

analysts’ forecasts has been unrealistically optimistic

regarding near term earnings growth prospects.

Unlike analysts, against a backdrop of weak global growth we

do not expect company profit margins to increase from their

already elevated levels. For this reason, we have developed

our own in-house corporate earnings paths which have led

to lower growth assumptions than forecast by the consensus.

For the major developed markets, we assume low single digit

earnings growth over the next few years. Not being influenced

by short-term market sentiment, our near term earnings growth

assumptions have been relatively stable overall, in contrast

to consensus expectations which have varied far more.

In the long term, we assume that companies’ earnings growth

is related to GDP growth. Crucially, we do not assume a one-

to-one relationship between a country’s growth rate and the

long term earnings growth potential of companies listed on

the stock market within that country. We do this because many

companies are international in nature and derive earnings

from regions outside of where they have a stock market

listing. An implication is that European company earnings

have only about a 50% direct exposure to developments in

the Eurozone and similarly, investors in non-European equity

markets should not consider themselves insulated from events

there either. It is also notable that emerging markets are an

important driver of profits earned in the developed world.

USD GBP EUR CHF CAD JPY

US 6.7% 6.6% 6.1% 5.6% 6.4% 6.1%

UK 7.4% 7.4% 6.9% 6.3% 7.2% 6.9%

Europe ex UK 6.9% 6.8% 6.4% 5.8% 6.6% 6.3%

Switzerland 6.6% 6.6% 6.1% 5.5% 6.4% 6.1%

Canada 7.0% 6.9% 6.4% 5.9% 6.7% 6.4%

Japan 6.5% 6.4% 5.9% 5.4% 6.2% 5.9%

Emerging Markets 8.4% 8.3% 7.9% 7.3% 8.1% 7.8%

10yr Annualized Nominal Return Assumptions

Aon Hewitt 11

Private equity

Real estate

We assume that global private equity will return 9.0%

per annum over the next 10 years in US dollar terms. The

assumption represents a diversified private equity portfolio

with allocations to leveraged buyouts (LBOs), venture capital,

mezzanine and distressed investments. Return expectations

for these different strategies depend on different market

factors. For example, distressed investments are influenced

by the outlook for high yield debt. Similarly, LBO returns

are influenced by the outlook for equity markets as well as

the cost of the debt used to finance these LBOs. The current

low interest rate environment is therefore beneficial for LBO

investors. Notwithstanding this, whereas in the past leverage

has been a big driver of private equity returns, particularly for

LBOs, in future the ability of managers to add value through

operational improvements will become more important.

On our analysis, the median private equity fund manager has

historically performed in line with the median public equity

manager, but high performing private equity managers have

performed significantly better. Our assumption incorporates

the level of manager skill (‘alpha’) associated with such a high

performing manager. This contrasts with our other equity

return assumptions where no manager alpha is assumed.

The US currently offers the highest real estate return

assumption of all of the markets covered in our Capital

Market Assumptions. Although capital values have been

rising, this market continues to benefit from a healthy rental

yield and a relatively robust outlook for rental growth.

In Europe, signs of stabilization have provided some support

to real estate capital values and they have been rising in

parts of the region. This has put some downward pressure

on rental yields although they have been more stable

than in the other major markets. This region continues to

offer a weak rental growth outlook because, unlike equity

markets which benefit from their international exposure,

real estate is much more closely tied to the fortunes of

the region in question. A weak rental outlook acts as a

drag on the return prospects for European real estate.

Our assumptions here are in respect of a large fund

which is capable of investing directly in real estate. The

assumptions relate to the broad real estate market in each

region rather than any particular market segment. Our

analysis allows for the fact that real estate is an illiquid

asset class and revaluations can be infrequent, leading

to lags in valuations compared with trends in underlying

market values. While our real estate assumptions do not

include any allowance for active management alpha or

active management fees, there is an allowance for the

unavoidable costs associated with investing in a real estate

portfolio. These include real estate management costs,

trading costs and investment management expenses.

USD GBP EUR CHF CAD JPY

US 7.0% 6.9% 6.5% 5.9% 6.7% 6.4%

UK 6.7% 6.6% 6.1% 5.6% 6.4% 6.1%

Europe ex UK 6.4% 6.4% 5.9% 5.3% 6.2% 5.9%

Canadian 5.8% 5.7% 5.3% 4.7% 5.5% 5.2%

10yr Annualized Nominal Return Assumptions

12 Capital Market Assumptions

Hedge funds

Our fund of hedge funds return assumption is 5.0% a year in

US dollar terms. We formulate this by combining the return

assumptions for a number of representative hedge fund

strategies. As with private equity, this assumption includes

allowances for manager skill and related fees (including

the extra layer of fees at the fund of funds level), but unlike

private equity, this is for the average fund of funds in the

hedge fund universe rather than for a high performing

manager. Our analysis allows for the fact that hedge fund

managers have been unable to deliver the high levels of

‘alpha’ that they did in the more distant past and that alpha

generation is likely to remain challenging moving forwards.

The individual hedge fund strategies we model as

components of our fund of hedge funds’ assumption are

equity long/short, equity market neutral, fixed income

arbitrage, event driven, distressed debt, global macro and

managed futures. Our modelling of these strategies includes an

analysis of the underlying building blocks of these strategies.

For example, we take into account the fact that equity long/

short funds are sensitive to equity market movements. In

practice the sensitivity of equity long/short funds to equity

markets can vary substantially by fund with some behaving

almost like substitutes for long only equity managers, while

others retain a much lower exposure. Our assumptions are

based on our assessment of the average sensitivity across

the entire universe of equity long/short managers.

Given the nature of the asset class, our hedge fund return

assumptions are more stable than, for example, our US equity

return assumption. Nonetheless, the strategies are impacted

by changes to the other asset class assumptions. For example,

most hedge funds are ‘cash+’ type investments to a greater or

lesser extent so the rise in cash return expectations during 2013

raised the hedge fund assumptions and the decline during 2014

has lowered the hedge fund assumptions. Similarly, changes

to our equity and high yield return assumptions influence

assumptions for those strategies which are related to these

markets, such as equity long-short and distressed debt.

As set out in the lead article to our 30 June 2013 Capital

Market Assumptions publication, history, forward looking

indicators and our view on the economic cycle all enter our

volatility assumption setting process and the volatilities in

the table above are representative for each asset class over

the next 10 years overall. For illiquid asset classes, such as

real estate, de-smoothing techniques are employed. All

volatilities shown above are in local currency terms. For

emerging market equities, global private equity and global

fund of hedge funds the local currency is taken to be USD.

Volatility in asset markets has fallen to unusually low levels

given the uncertainties facing financial markets and the global

economy. To a large extent this has been driven by the backstop

that central banks have been providing to markets. One example

concerns the statement by the President of the European Central

Bank, Mario Draghi, that the central bank would do “whatever

it takes” to save the euro. This reassured markets and brought

about a period of relative calm when before there had been

stress. When the US Federal Reserve stated in May 2013 that it

may soon start to reduce some of the support that it has been

providing to markets, volatility was reignited before falling back

once again. Volatility again spiked more recently but only for a

short period. Throughout, our assumptions have looked through

this recent period of low volatility and instead have been and

continue to be at a somewhat elevated level relative to history.

Please note that due to the level of yields and shape of

the yield curve in Japan and Switzerland, lower volatility

assumptions apply to bond investments in these markets.

Volatility

15yr Inflation-Linked Government Bonds 9.0%

15yr Government bonds 11.0%

10yr Investment Grade Corporate Bonds 9.0%

Real Estate 14.5%

US High Yield 14.0%

Emerging Market Debt (USD denominated) 12.0%

UK Equities 20.0%

US Equities 19.0%

Europe ex UK Equities 20.0%

Japan Equities 20.0%

Canada Equities 20.0%

Switzerland Equities 20.0%

Emerging Market Equities 28.5%

Global Private Equity 26.0%

Global Fund of Hedge Funds 8.0%

Aon Hewitt 13

Correlations

IL FI CB RE UK Eq US Eq Eur Eq Jap Eq Can Eq CHF Eq EM Eq Gbl PE Gbl FoHF

IL 1 0.5 0.4 0.1 -0.1 -0.1 -0.1 0 -0.1 -0.1 0 0 0

FI 1 0.8 0.1 -0.2 -0.2 -0.2 -0.1 -0.2 -0.2 -0.1 0 0

CB 1 0.1 0.1 0.1 0.1 0 0.1 0.1 0 0.1 0

RE 1 0.4 0.4 0.4 0.3 0.4 0.4 0.3 0.3 0.3

UK Eq 1 0.85 0.85 0.7 0.85 0.85 0.8 0.6 0.6

US Eq 1 0.85 0.7 0.85 0.85 0.8 0.7 0.6

Eur Eq 1 0.7 0.85 0.85 0.8 0.6 0.6

Jap Eq 1 0.7 0.7 0.6 0.4 0.5

Can Eq 1 0.8 0.8 0.6 0.6

CHF Eq 1 0.8 0.6 0.6

EM Eq 1 0.6 0.5

Gbl PE 1 0.4

Gbl FoHF 1

Domestic Inflation-Linked Government Bonds

Eurozone Equities

Domestic Government bonds

Japan Equities

Domestic Investment Grade Corporate Bonds

Canada Equities Global Fund of Hedge Funds

US Equities

Global Private EquityDomestic Real Estate

Switzerland Equities

UK Equities

Emerging Market Equities

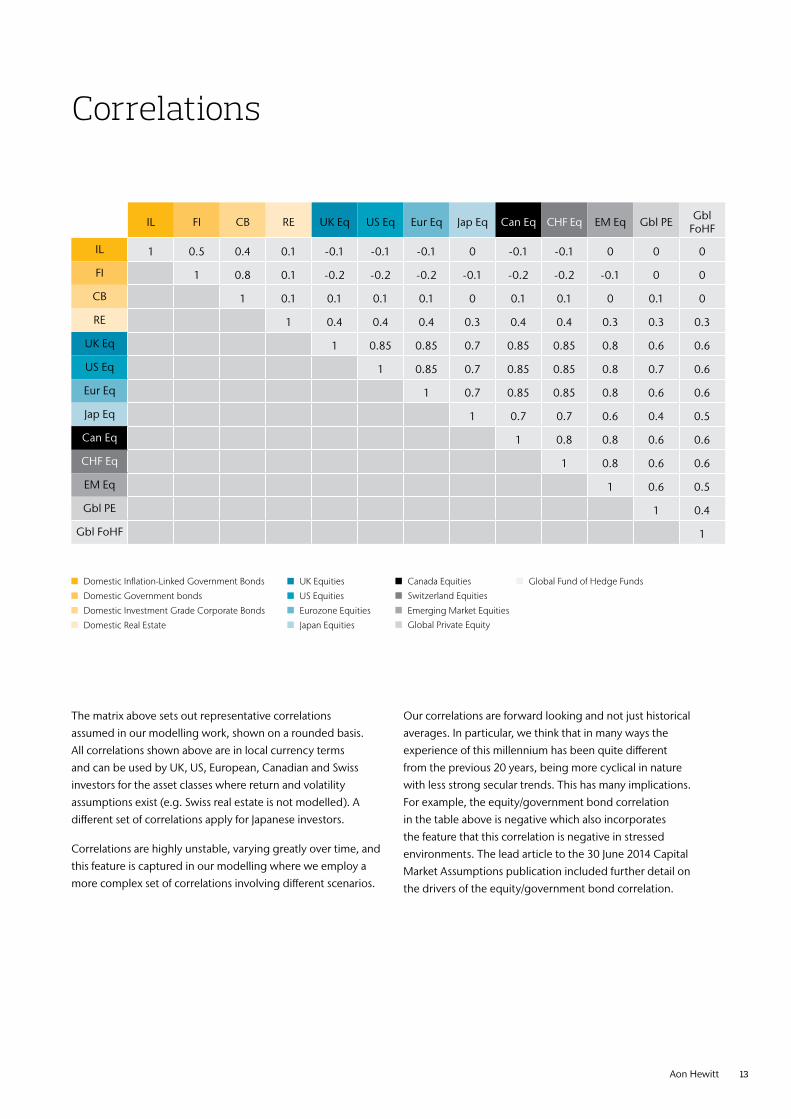

The matrix above sets out representative correlations

assumed in our modelling work, shown on a rounded basis.

All correlations shown above are in local currency terms

and can be used by UK, US, European, Canadian and Swiss

investors for the asset classes where return and volatility

assumptions exist (e.g. Swiss real estate is not modelled). A

different set of correlations apply for Japanese investors.

Correlations are highly unstable, varying greatly over time, and

this feature is captured in our modelling where we employ a

more complex set of correlations involving different scenarios.

Our correlations are forward looking and not just historical

averages. In particular, we think that in many ways the

experience of this millennium has been quite different

from the previous 20 years, being more cyclical in nature

with less strong secular trends. This has many implications.

For example, the equity/government bond correlation

in the table above is negative which also incorporates

the feature that this correlation is negative in stressed

environments. The lead article to the 30 June 2014 Capital

Market Assumptions publication included further detail on

the drivers of the equity/government bond correlation.

14 Capital Market Assumptions

Capital market assumptions methodology

Overview

Aon Hewitt’s Capital Market Assumptions are our asset class return, volatility and correlation assumptions. The return assumptions are ‘best estimates’ of annualized returns. By this we mean median annualized returns – that is, there is a 50/50 chance that actual returns will be above or below the assumptions. The assumptions are long term assumptions, based on a 10 year projection period and are updated on a quarterly basis.

Material uncertainty

Given that the future is uncertain, there is material uncertainty in all aspects of the Capital Market Assumptions and the use of judgment is required at all stages in both their formulation and application.

Allowance for active management

The asset class assumptions are assumptions for market returns, that is we make no allowance for managers outperforming the market. The exceptions to this are the private equity and hedge fund assumptions where, due to the nature of the asset classes, manager performance needs to be incorporated in our Capital Market Assumptions. In the case of hedge funds we assume average manager performance and for private equity we assume a high performing manager.

Inflation

When formulating assumptions for inflation, we consider consensus forecasts as well as the inflation risk premium implied by market break-even inflation rates.

Government bonds

The government bond assumptions are for portfolios of bonds which are annually rebalanced (to maintain constant duration). This is formulated by stochastic modelling of future yield curves.

Inflation-linked government bonds

We follow a similar process to that for nominal government bonds, but with projected real (after inflation) yields. We incorporate our inflation profiles to construct nominal returns for inflation-linked government bonds.

Corporate bonds

Corporate bonds are modelled in a similar manner to government bonds but with additional modelling of credit spreads and projected losses from defaults and downgrades.

Other fixed income

Emerging market debt and high yield debt are modelled in a similar fashion to corporate bonds by considering expected returns after allowing for losses from defaults and downgrades.

Equities

Equity return assumptions are built using a discounted cashflow analysis. Forecast real (after inflation) cashflows payable to investors are discounted and their aggregated value is equated to the current level of each equity market to give forecast real (after inflation) returns. These returns are then converted to nominal returns using our 10 year inflation assumptions.

Private equity

We model a diversified private equity portfolio with allocations to leveraged buyouts, venture capital, and mezzanine and distressed investments. Return assumptions are formulated for each strategy based on an analysis of the exposure of each strategy to various market factors with associated risk premia.

Real estate

Real estate returns are constructed using a discounted cashflow analysis similar to that used for equities, but allowing for the specific features of these investments such as rental growth.

Hedge funds

We construct assumptions for a range of hedge fund strategies (e.g. equity long/short, equity market neutral, fixed income arbitrage, event driven, distressed debt, global macro, managed futures) based on an analysis of the underlying building blocks of these strategies.

We use these individual strategies to formulate a fund of hedge funds’ assumption which is quoted in the Capital Market Assumptions.

Currency movements

Assumptions regarding currency movements are related to inflation differentials.

VolatilityAssumed volatilities are formulated with reference to implied volatilities priced into option contracts of various terms, historical volatility levels and expected volatility trends in future.

Correlations

Our correlation assumptions are forward looking and result from in-house research which looks at historical correlations over different time periods and during differing economic/investment conditions, including periods of market stress. Correlations are highly unstable, varying greatly over time. This feature is captured in our modelling.

ContactsDuncan Lamont T: +44 (0)20 7086 [email protected]

Disclaimer

This document has been produced by Global Investment Consulting of Aon Corporation. Nothing in this document should be treated as an authoritative statement of the law on any particular aspect or in any specific case. It should not be taken as financial advice and action should not be taken as a result of this document alone. Consultants will be pleased to answer questions on its contents but cannot give individual financial advice. Individuals are recommended to seek independent financial advice in respect of their own personal circumstances.

Aon Corporation 200 E. Randolph Street Chicago Illinois 60601, USA

Copyright © 2014 Aon Corporation

Risk. Reinsurance. Human Resources.

About Aon HewittAon Hewitt is the global leader in human resource

consulting and outsourcing solutions. The company

partners with organizations to solve their most

complex benefits, talent and related financial

challenges, and improve business performance.

Aon Hewitt designs, implements, communicates

and administers a wide range of human capital,

retirement, investment management, health

care, compensation and talent management

strategies. With more than 29,000 professionals in

90 countries, Aon Hewitt makes the world a better

place to work for clients and their employees.

For more information on Aon Hewitt,

please visit www.aonhewitt.com

© Aon plc 2014. All rights reserved.The information contained herein and the statements expressed

are of a general nature and are not intended to address the

circumstances of any particular individual or entity. Although we

endeavor to provide accurate and timely information and use

sources we consider reliable, there can be no guarantee that

such information is accurate as of the date it is received or that it

will continue to be accurate in the future. No one should act on

such information without appropriate professional advice after a

thorough examination of the particular situation.

Aon Hewitt Limited is authorised and regulated by the Financial

Conduct Authority. Registered in England & Wales.

Registered No: 4396810.