capital market research forum capital market research

TRANSCRIPT

Capital Market Research Forum Capital Market Research Forum 66//22011011

Corporate bond markets: a spare tire for AsiaCorporate bond markets: a spare tire for Asia

By

Dr. Eli Remolona

Regional Head for Asia and the Pacific

Bank of International Settlements

23 May 2011

Corporate bond markets:

a spare tire for Asia

Eli RemolonaEli Remolona

2

All views expressed here are our own and do not necessarily

reflect those of the Bank for International Settlements.

Capital Markets Research Forum

Stock Exchange of Thailand

Bangkok, 23 May 2011

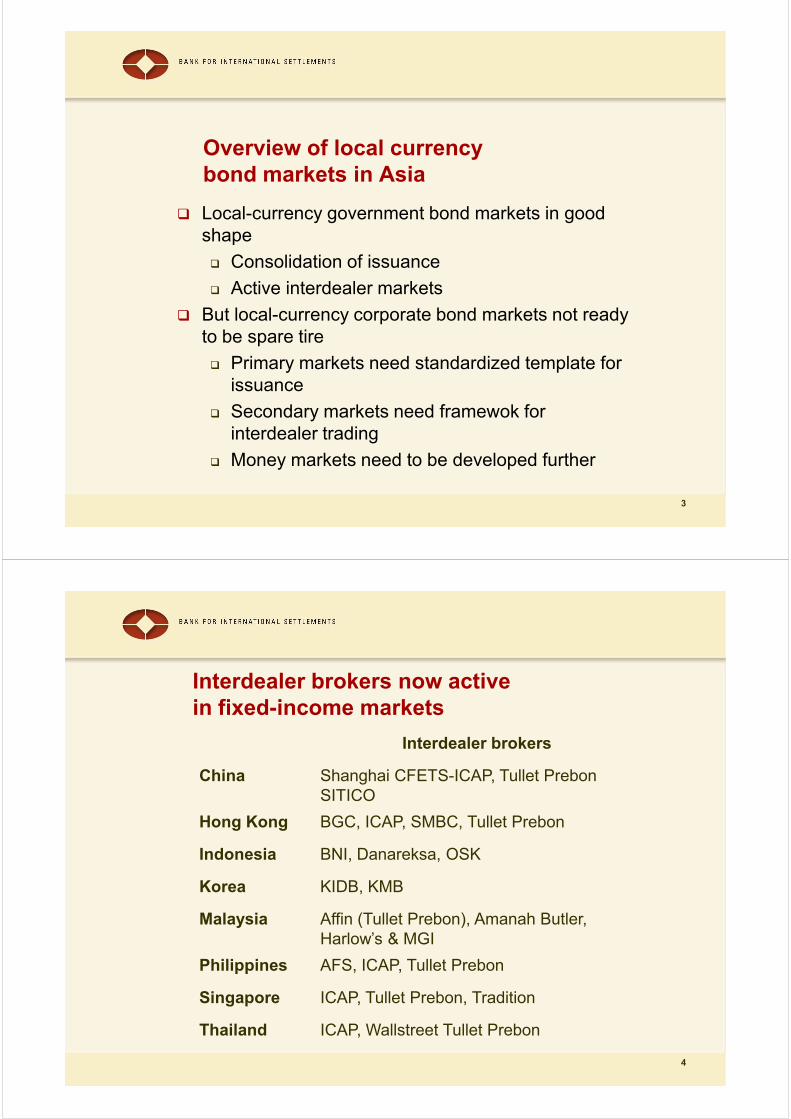

Overview of local currency

bond markets in Asia

� Local-currency government bond markets in good

shape

� Consolidation of issuance

Active interdealer markets

3

� Active interdealer markets

� But local-currency corporate bond markets not ready

to be spare tire

� Primary markets need standardized template for

issuance

� Secondary markets need framewok for

interdealer trading

� Money markets need to be developed further

Interdealer brokers now active

in fixed-income markets

Interdealer brokers

China Shanghai CFETS-ICAP, Tullet Prebon

SITICO

Hong Kong BGC, ICAP, SMBC, Tullet Prebon

4

Indonesia BNI, Danareksa, OSK

Korea KIDB, KMB

Malaysia Affin (Tullet Prebon), Amanah Butler,

Harlow’s & MGI

Philippines AFS, ICAP, Tullet Prebon

Singapore ICAP, Tullet Prebon, Tradition

Thailand ICAP, Wallstreet Tullet Prebon

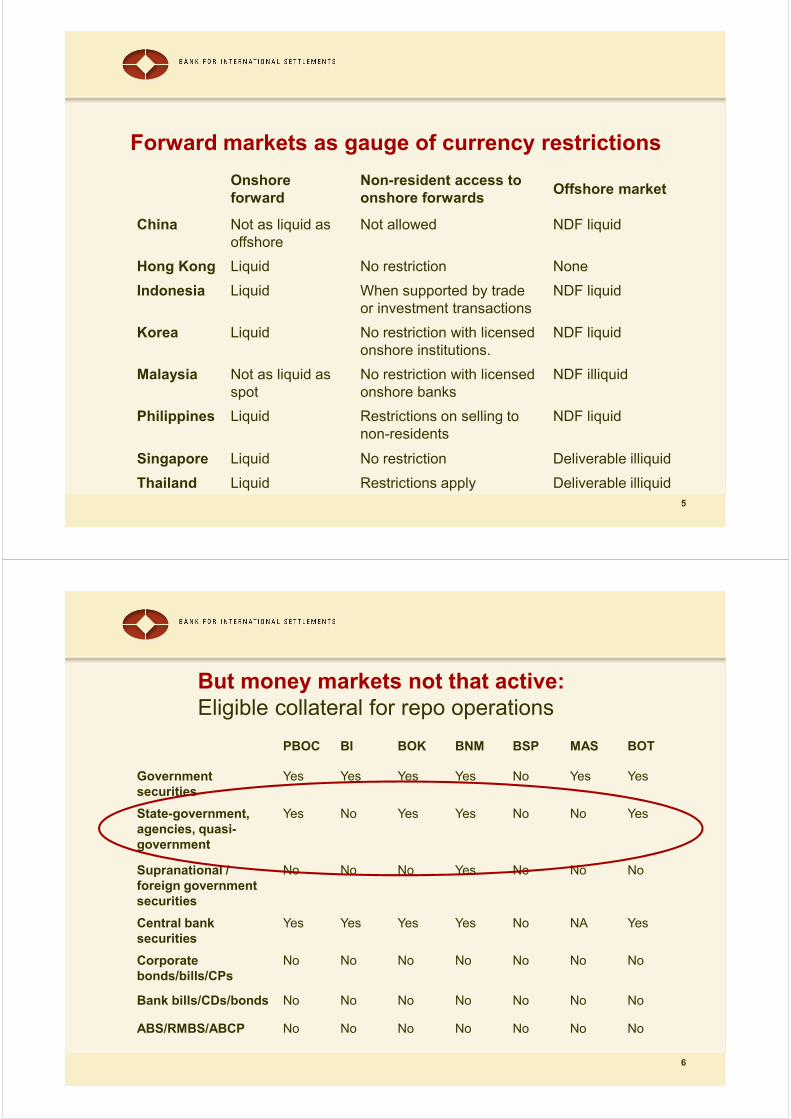

Forward markets as gauge of currency restrictions

Onshore

forward

Non-resident access to

onshore forwardsOffshore market

China Not as liquid as

offshore

Not allowed NDF liquid

Hong Kong Liquid No restriction None

5

Indonesia Liquid When supported by trade

or investment transactions

NDF liquid

Korea Liquid No restriction with licensed

onshore institutions.

NDF liquid

Malaysia Not as liquid as

spot

No restriction with licensed

onshore banks

NDF illiquid

Philippines Liquid Restrictions on selling to

non-residents

NDF liquid

Singapore Liquid No restriction Deliverable illiquid

Thailand Liquid Restrictions apply Deliverable illiquid

But money markets not that active:

Eligible collateral for repo operations

PBOC BI BOK BNM BSP MAS BOT

Government

securities

Yes Yes Yes Yes No Yes Yes

State-government,

agencies, quasi-

government

Yes No Yes Yes No No Yes

6

government

Supranational /

foreign government

securities

No No No Yes No No No

Central bank

securities

Yes Yes Yes Yes No NA Yes

Corporate

bonds/bills/CPs

No No No No No No No

Bank bills/CDs/bonds No No No No No No No

ABS/RMBS/ABCP No No No No No No No

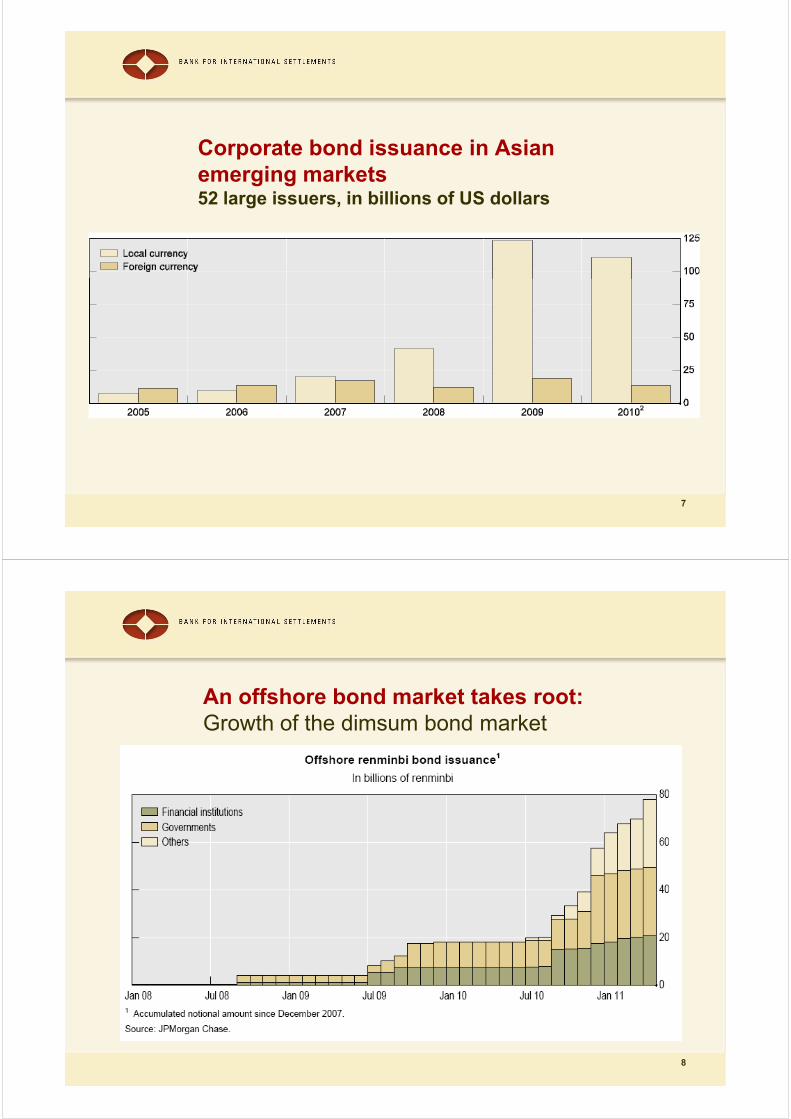

Corporate bond issuance in Asian

emerging markets52 large issuers, in billions of US dollars

7

An offshore bond market takes root:

Growth of the dimsum bond market

8

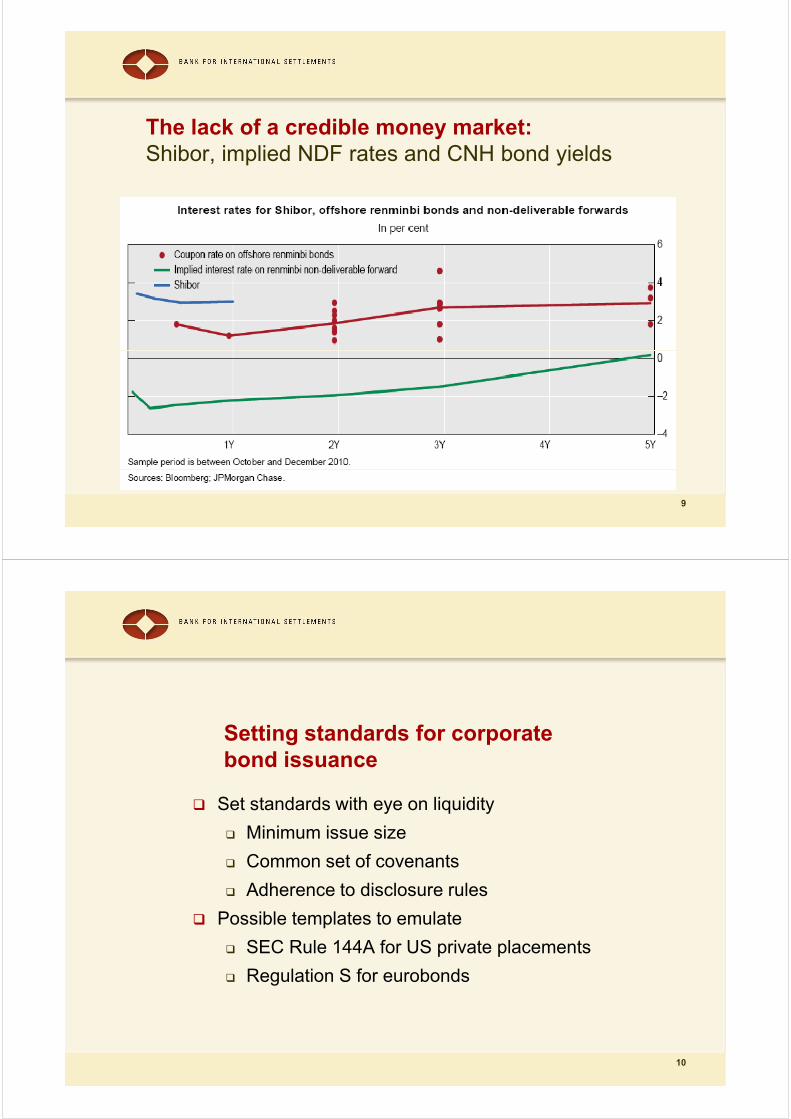

The lack of a credible money market:

Shibor, implied NDF rates and CNH bond yields

9

Setting standards for corporate

bond issuance

� Set standards with eye on liquidity

� Minimum issue size

10

� Minimum issue size

� Common set of covenants

� Adherence to disclosure rules

� Possible templates to emulate

� SEC Rule 144A for US private placements

� Regulation S for eurobonds

Setting up a framework for

interdealer trading

� Liquidity in fixed-income markets requires active

interdealer market:

� Pre-trade anonymity

11

� Pre-trade anonymity

� Post-trade transparency

� Asian markets could use interdealer trading platform

for corporate bonds

� Dealers commit to make markets

� Issuers commit to list large issues

� Links to clearing and settlement facilities

� Possible model: EuroCredit MTS

Developing Asia’s money markets

� Weak link in money markets is repo markets

� Introduce tri-party repos

� Clearing bank stands between lender and

borrower

12

borrower

� It also manages custody and transfer of

collateral

� Safeguards against runs

� Robust rules on collateral eligibility

� Set haircuts at stress levels even in normal

times