capital one southcoast 4th annual energy conference

TRANSCRIPT

Sue Carter – Senior Vice President and CFO

John Rose, President – Hydrocarbons Group

December 9, 2009

Capital One Southcoast4th Annual Energy Conference

Forward Looking StatementsThis presentation contains “forward-looking statements.” All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements include statements about the benefits of the split-off, the discussions of KBR’s business strategies and KBR’s expectations concerning future operations, profitability, liquidity and capital resources. You can generally identify forward-looking statements by terminology such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,”“forecast,” “goal,” “intend,” “may,” “objective,” “plan,” “potential,” “predict,” “projection,” “should” or other similar words. These statements relate to future events or future financial performance and involve known and unknown risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to differ materially from those in the future that are implied by these forward-looking statements. Many of these factors cannot be controlled or predicted. These risks and other factors include those described under “Risk Factors” in KBR’s Annual Report on Form 10-K dated February 25, 2009, Forms 10-Q, recent Current Reports on Forms 8-K, and other Securities and Exchange Commission filings. Those factors, among others, could cause KBR’s actual results and performance to differ materially from the results and performance projected in, or implied by, the forward-looking statements. As you read and consider this presentation, you should carefully understand that the forward-looking statements are not guarantees of performance or results. KBR cautions you that assumptions, beliefs, expectations, intentions and projections about future events may and often do vary materially from actual results. Therefore, KBR cannot assure you that actual results will not differ materially from those expressed or implied by forward-looking statements.

The forward-looking statements included in this presentation are made only as of the date of this document. New risks and uncertainties arise from time to time, and KBR cannot predict those events or their impact. KBR assumes no obligation to update any forward-looking statements after the date of this presentation as a result of new information, future events or developments, except as required by the federal securities laws.

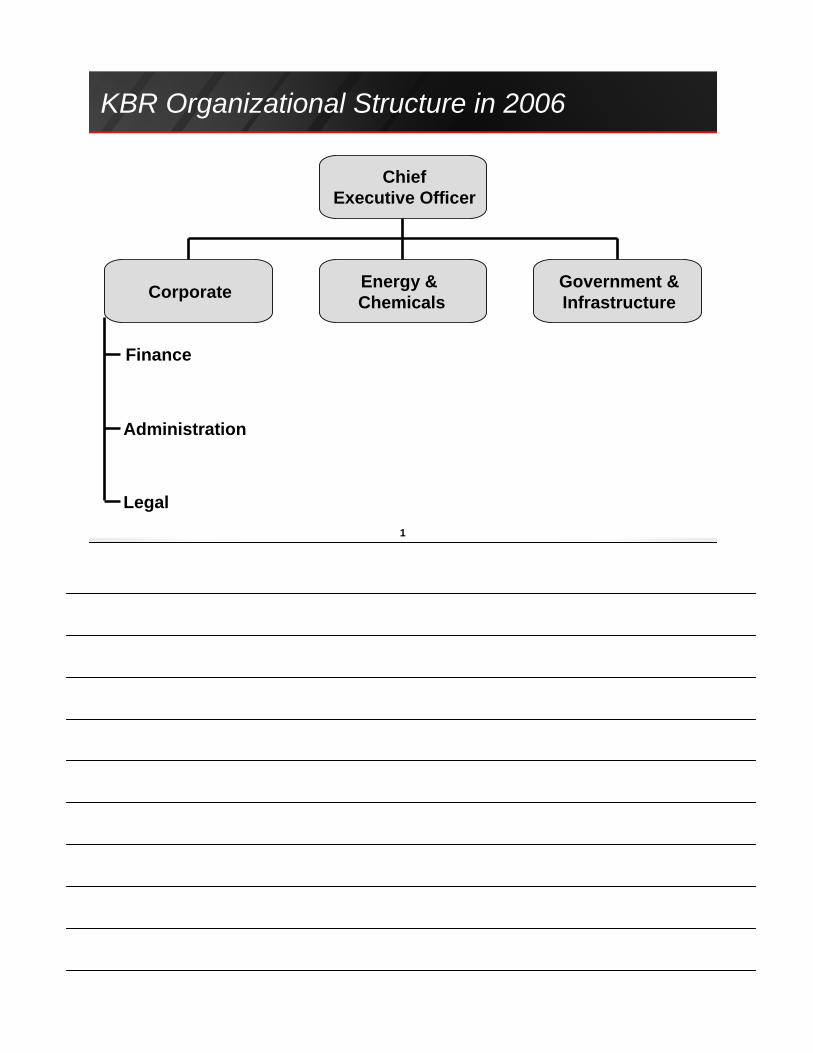

KBR Organizational Structure in 2006

1

ChiefExecutive Officer

Corporate Energy & Chemicals

Government &Infrastructure

Finance

Administration

Legal

KBR Proposed Organizational Structure in 2010

2

Chief Executive Officer

Corporate ServicesGovernment, Defense,

& Infrastructure; Power & Industrial

Finance

Legal

Commercial

Hydrocarbons

Administration

Operations

Ventures

Buildings Group N. America G&D

Oil & Gas Canada Operations International G&D

Downstream Construction Infrastructure &Minerals

Technology O&M Power & Industrial

Gas Monetization

Fabrication

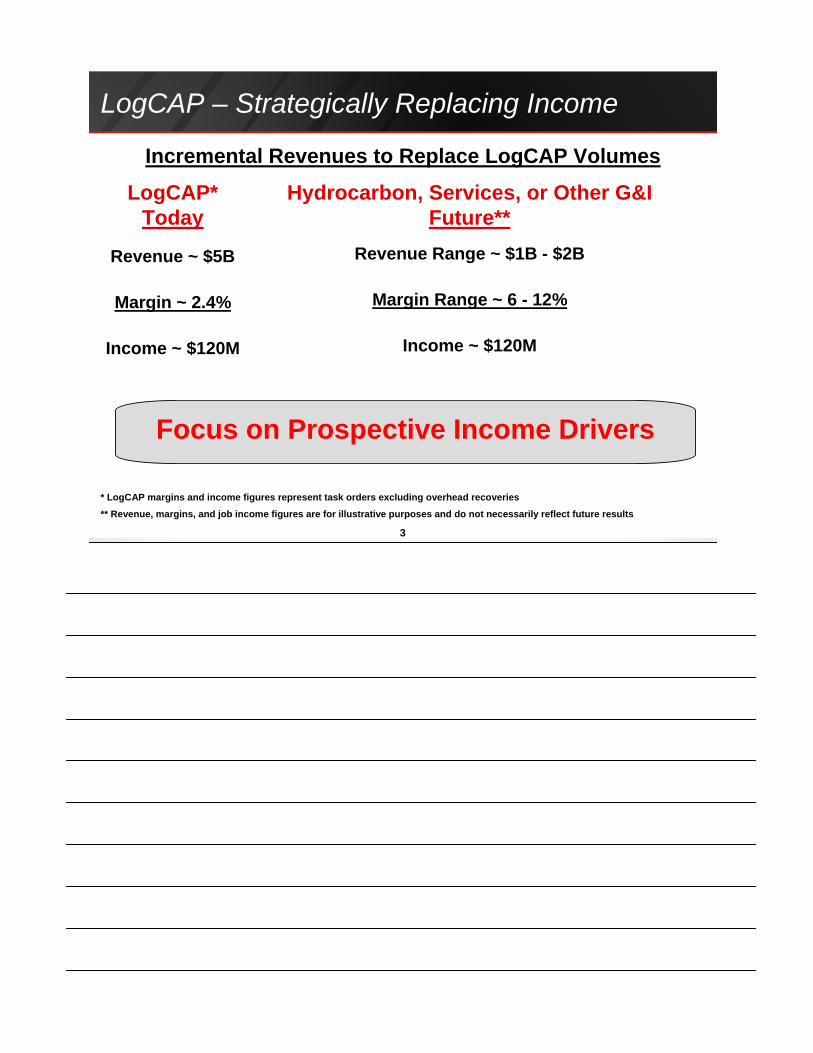

LogCAP – Strategically Replacing Income

Revenue ~ $5B

Margin ~ 2.4%

Income ~ $120M

3

Hydrocarbon, Services, or Other G&IFuture**

** Revenue, margins, and job income figures are for illustrative purposes and do not necessarily reflect future results

LogCAP*Today

Revenue Range ~ $1B - $2B

Margin Range ~ 6 - 12%

Income ~ $120M

Focus on Prospective Income Drivers

Incremental Revenues to Replace LogCAP Volumes

* LogCAP margins and income figures represent task orders excluding overhead recoveries

Growing KBR’s Prospects to Projects

4

Gas Monetization• Gorgon LNG EPCm

• Skikda LNG EPC

• Tangguh LNG EPC

• Inpex Ichthys LNG FEED

• Pluto 2/3 LNG FEED

Oil & Gas• Big Foot Offshore FEED

• West of Shetlands FEED

• Jack/St. Malo Pre-FEED

• Chirag Platform FEED

• Various FPSO projects

Expansion trains at existing or ongoing projects

EPC/EPCm after FEED work

Australian LNG opportunities

Expanded work from FEEDs

PMC opportunities

Geographical expansion

Expand capabilities to procurement services and construction management

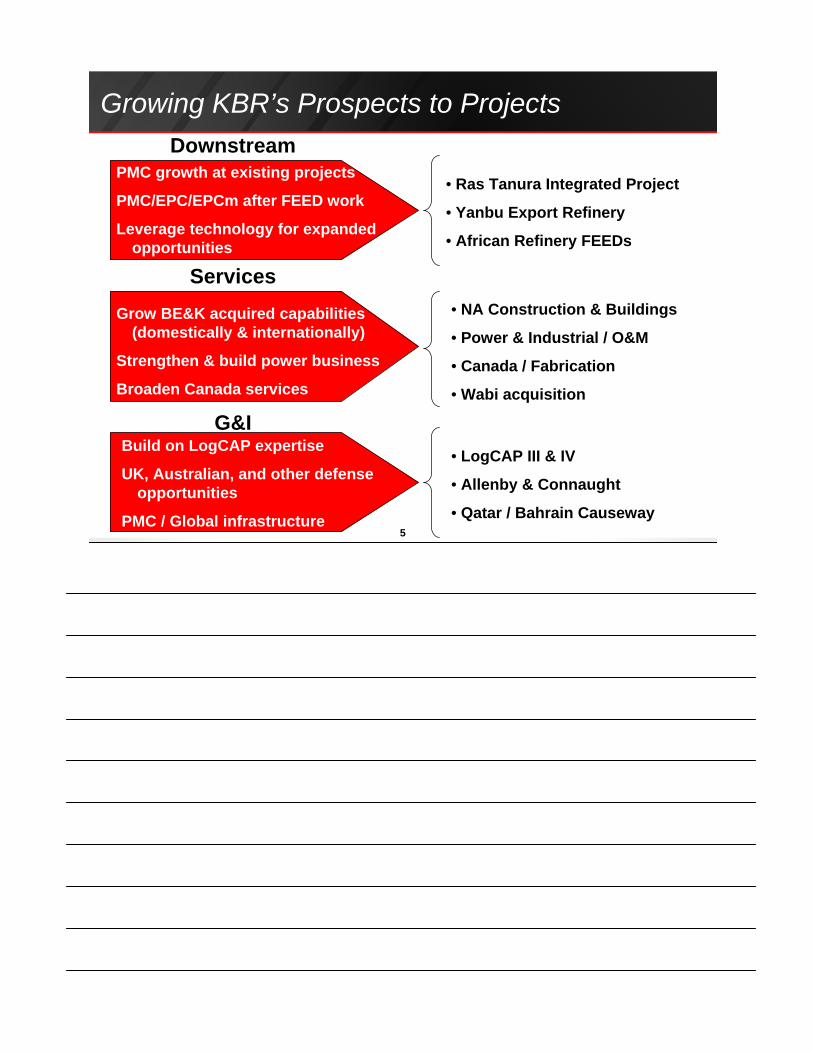

Growing KBR’s Prospects to Projects

5

Downstream

• Ras Tanura Integrated Project

• Yanbu Export Refinery

• African Refinery FEEDs

Services• NA Construction & Buildings

• Power & Industrial / O&M

• Canada / Fabrication

• Wabi acquisition

PMC growth at existing projects

PMC/EPC/EPCm after FEED work

Leverage technology for expanded opportunities

G&I• LogCAP III & IV

• Allenby & Connaught

• Qatar / Bahrain Causeway

Grow BE&K acquired capabilities (domestically & internationally)

Strengthen & build power business

Broaden Canada services

Build on LogCAP expertise

UK, Australian, and other defense opportunities

PMC / Global infrastructure

Job Income Growth Excluding LogCAP

6

2007

$379M

Nine Months Ended September 30,2007 2008 2009

+44%

+15%

$193M $193M$183M

$546M

$627M

ME Operations Job Income KBR excluding ME Operations Job Income

KBR Corporate

Strong Balance Supports Functional Options

8

DividendsAcquisitions Share Repurchases

Reinvest in Existing Business

Capitalization @ 9/30/09 ($ in millions)

Available Cash 1,020$

Cash Associated with JVs & Projects 205

Discretionary Cash 815$

Working Capital Management

9

Focused on reducing general business accounts receivable

Managing accounts payable

Resolution of unbilled receivables on uncompleted contracts

Collecting on past disputes (EPC 1)

Government Business

As LogCAP work declines, less working capital requirements

Diligently working to resolve disputed withhold amounts

“Best in Class” Risk Management & Awareness

10

Identification AnalysisMeasurement Pricing Management Reporting

Business Development Oversight

Commercial Technical Execution

Risk Management & ReportingLegal Financial

Prudent Financial Management & Focus

11

** KBR SG&A represents corporate general and administrative expenses and all Business Unit overheads;

14%

44%

2007 – 2009 Growth*

KBR SG&A**

* Compares growth from first nine months ended 2007 compared to first nine months ended 2009

4.8%

6.4%

KBR Revenue

SG&A Comparison

KBR SG&A**

Peer Average SG&A***

*** Peer group consists of JEC, FWLT, MDR, CBI, and SHAW, as these firms report SG&A and not G&A only

Presentation Summary

12

• Greater transparency into the KBR organization for stakeholders

• Strategically replacing declining LogCAP work with other business opportunities

• Strong balance sheet with emphasis on cash management

• Prudent management focus on risk management and controlling overhead costs

We Deliver