capital one southcoast energy conference...

TRANSCRIPT

Capital One SouthcoastEnergy Conference 2006

December 4, 2006

1

Forward-looking Statements

This presentation will contain "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements, which include any statement that does not relate strictly to historical facts, use terms such as “anticipate,” “assume,” “believe,” “estimate,” “expect,” “forecast,” “intend,”“plan,” “position,” “predict,” “project,” or “strategy” or the negative connotation or other variations of such terms or other similar terminology. In particular, statements, express or implied, regarding future results of operations or ability to generate revenues, income or cash flow or to make acquisitions are forward-looking statements. These forward-looking statements are based on management’s current plans, expectations, estimates, assumptions and beliefs concerning future events impacting Hercules Offshore, Inc. (“Hercules”) and therefore involve a number of risks and uncertainties, many of which are beyond management’s control. These risks and uncertainties are further described in Hercules’ annual report on Form 10-K and its most recent periodic reports and other documents filed with the Securities and Exchange Commission which are available free of charge at the SEC’s website at www.sec.gov or the company’s website at www.herculesoffshore.com.

The forward-looking statements involve risks and uncertainties that affect Hercules’ operations and financial performance. All forward-looking statements attributable to Hercules’ representatives are expressly qualified in their entirety by this cautionary statement.

2

Management Representatives

Participants

• Randall Stilley Chief Executive Officer and President

• Steven Manz Chief Financial Officer

• John Rynd President, Hercules Drilling Company

• Stephen Butz Vice President and Treasurer

Company Overview

4

Hercules Offshore Overview

• Unique business mix within the oil services industry – Industry leading liftboat business – currently 64 liftboats, including 47 in the U.S.

Gulf of Mexico (“GOM”) and 17 in West Africa– Expanding contract drilling business - nine jackup rigs, six operating in the GOM

and three focused internationally• Market capitalization of approximately $1 billion

Note: See Explanatory Information slide. Division Adjusted EBITDA does not include corporate G&A and other income/expenses.

Quarterly Revenue Quarterly Adjusted EBITDA($ in millions)

$7.7 $9.2 $10.8 $13.9$24.0 $29.1 $33.7 $42.9

$15.6$24.9 $26.3 $28.2

$24.0$27.0

$42.6

$54.3

Liftboats Drilling

4Q 04 1Q 05 2Q 05 3Q 05 4Q 05 1Q 06 2Q 06 3Q 06$3.0 $4.2 $4.6 $5.8

$11.7 $16.8 $20.7$26.7

$6.1$12.5 $12.6 $13.8

$11.3$14.1

$26.8

$33.7

Liftboats Drilling

4Q 04 1Q 05 2Q 05 3Q 05 4Q 05 1Q 06 2Q 06 3Q 06

($ in millions)

5

Investment Highlights

• Consolidator of shallow water assets through prudent acquisitionstrategy

• Conservative capital structure and strong liquidity provide foundation for further growth

• Proven track record of maximizing return on capital and profitability

• Strong industry fundamentals

• Experienced management team

6

• Completed 12 asset acquisitions in last two years

• Opportunistic acquisition strategy– Non-core assets from larger organizations– Consolidate fragmented market segments

• Focus on return on capital employed

Successful Acquisition Execution Track Record

February2006

Acquired Rig 26 from Aries Offshore

Partners Ltd.

November 2005

Acquired seven liftboats from

Danos & Curole

September2005

Acquired Rig 31 from Hydrocarbon

Capital II LLC

(1) Received insurance proceeds of $48.8 million as the rig was severely damaged in Hurricane Katrina. The rig has since been retired.(2) Includes one shallow water liftboat which was subsequently sold and one that was retired.

June2006

Acquired six liftboats from

Laborde Marine Lifts

November2006

Acquired eight liftboats and

assumed rights to operate five

additional liftboats from Halliburton

August2004

Acquired five jackup rigs from Parker Drilling

January2005

Acquired Rig 25 (1)

from Parker Drilling and Rig 30 from

Porterhouse Offshore, L.P.

August2005

Acquired the Whale Sharkliftboat from CS Liftboats

June2005

Acquired Rig 16 from Transoceanand 17 liftboats from Superior

Energy(2)

October2004

Acquired 22 liftboats from

Global Industries

7

Halliburton Liftboat Acquisition

• On November 7, 2006 Hercules acquired Halliburton’s West African liftboat fleet for $50 million, plus amounts payable under an earn-out agreement(1)

• The fleet consists of eight wholly-owned liftboats and rights to operate five non-owned liftboats subject to bareboat charters

(1) The Company agrees to make additional payments over a three-year period up to an aggregate amount of $10 million, based on achieving certain financial targets.

Fleet Summary

Vessel ClassLowell Granstaff 215Malcolm Kinnaird 150F.J. Leleux* 150James Choat* 120Durwood Speed* 120Charlie Cobb* 120Zoal Albrecht* 120Leon Grigsby 120Glenn Craig 120A.B. Crutchfield 105C.C. Whittington 105Jack Huffman 105Mene-Afejuku (A. Brady) 105

* Owned by Meridien Maritime and Offshore Services Limited and previously operated by Halliburton.

Lowell GranstaffClass 215 Liftboat

• The liftboats range from 105’ to 215’ class size and are currently operating in the coastal waters of Nigeria and Cameroon

• The fleet adds significant economies of scale to Hercules operations, making it the largest and most diversified fleet in West Africa

8

Additional Opportunities for Consolidation Still Exist

Aries 14

HERO 47

Seven remaining owners 25

SPN 27

• The top ten jackup owners control 67% of the current global fleet

• The remaining 33%, or 130 jackups, are controlled by 50 different companies

• With the exception of Hercules and Superior Energy Services, the other liftboat operators in the GOM are private companies

• There are 62 jackups on order by 30 industry participants, including 13 new players(1)

• There are 13 liftboats on order by 4 industry participants, including 2 new players(1)

DO 13 ESV 43

GSF 45

NBR 16

NE 40PDE 27RDC 20THE 24

RIG 25

COSL 11Fifty

remaining owners 130

(1) As of November 1, 2006.(2) Source: Company estimates based on publicly available disclosure made by listed companies and Company-developed information. (3) Source: ODS-Petrodata as November 27, 2006.

GOM Liftboat Ownership (113)(2) Total Jackups Worldwide (394)(3)

9

Increasing Geographic Diversity

India

Rig 31 contracted with Cairn for 7 wells at

$110,000 escalating to $140,000

Middle East

Rig 16contracted with Occidental for two years at

$69,500

West Africa

17 liftboats in operation. Recently

acquired eight liftboats and

assumed rights to operate five

additional liftboats from Halliburton

Other International Opportunities

Rig 26 - exclusively being marketed internationally

Liftboats - actively marketing several liftboats in West Africa, Middle East and North Sea

Marine Services Segment Overview

11

Hercules: Marine Services Segment Overview

• 64 vessels worldwide– Hercules operates the largest liftboat

fleet in the GOM with 47 vessels– Largest liftboat fleet in West Africa with

17 vessels

• Recently closed acquisition of Halliburton’s West African liftboat fleet consisting of eight wholly-owned liftboats and rights to operate five additional liftboats

• Liftboats are self-propelled, self-elevating vessels with large open deck space from which to perform maintenance and construction activities

• Liftboat utilization and dayrates tend to be more stable than that of jackups given their use throughout the life of a well

Swordfish Class 200 Liftboat

Marlin Class 105 Liftboat

12

0 5 10 15 20 25 30 35 40 45 50

CS Liftboats

Seahorse

OMC

AMC

Laredo

OL

Montco

Aries

Superior

Hercules

105 - 130' 131 - 190' 190'+

Largest Liftboat Operator in the U.S. Gulf of Mexico

Source: Company estimates based on publicly available disclosure made by listed companies and Company-developed information.Note: Excludes Hercules’ 17 liftboats operating in West Africa.

• We believe there are 13 newbuilds on order or under construction that may be operated in the U.S. GOM.

Liftboat Class (ft.):

47

14

6

6

4

3

3

2

1

27

13

West African Competitive Landscape

Source: Company estimates based on publicly available disclosure made by listed companies and Company-developed information.Note: Hercules’ fleet includes five non-owned liftboats subject to bareboat charters.*The three vessels owned by Zumax are currently cold-stacked and the two vessels owned by Zukus have been abandoned.

0 5 10 15 20

Shoreline

NV De Brandt

Zukus

Zumax

100-130' 131-190' 190'+Liftboat Class (ft.):

1

1

3*

17

2*

14

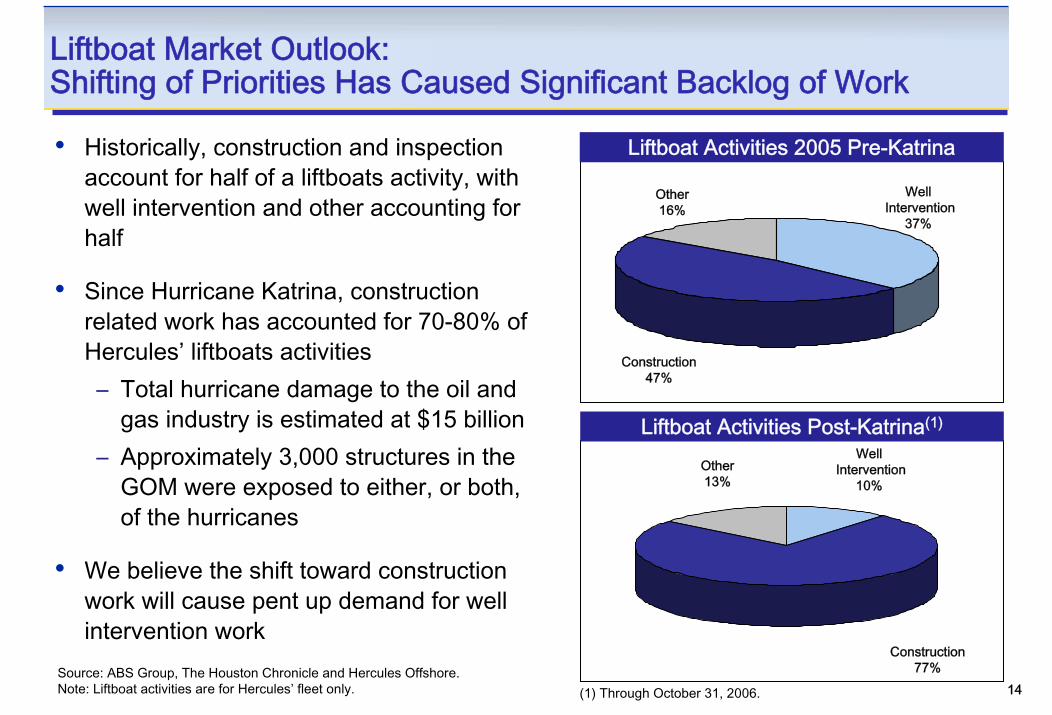

Liftboat Market Outlook:Shifting of Priorities Has Caused Significant Backlog of Work

• Historically, construction and inspection account for half of a liftboats activity, with well intervention and other accounting for half

• Since Hurricane Katrina, construction related work has accounted for 70-80% of Hercules’ liftboats activities– Total hurricane damage to the oil and

gas industry is estimated at $15 billion – Approximately 3,000 structures in the

GOM were exposed to either, or both, of the hurricanes

• We believe the shift toward construction work will cause pent up demand for well intervention work

Source: ABS Group, The Houston Chronicle and Hercules Offshore. Note: Liftboat activities are for Hercules’ fleet only. (1) Through October 31, 2006.

Construction77%

Construction47%

WellIntervention

37%

WellIntervention

10%

Other16%

Other13%

Liftboat Activities 2005 Pre-Katrina

Liftboat Activities Post-Katrina(1)

15

Hercules’ Liftboat Fleet

StarfishClass 140’ Liftboat

SwordfishClass 200’ Liftboat

(1) Within the liftboat industry, the terms leg-length and liftboat class are used interchangeably.(2) Leg-length, dayrate and utilization amounts are based on the four liftboats Hercules owned in West Africa as of October 31, 2006.Note: Utilization is defined as the total number of operating days in the period as a percentage of the total number of calendar days in the period our

liftboats were actively marketed. YTD is as of October 31, 2006. Dayrates include reimbursements from customers under relevant contracts.

79%

Leg - Length /Liftboat Class(1) Number of Oct-05 Oct-06 Y-o-Y YTD 2006

(Feet) Vessels Dayrate Dayrate % Change UtilizationGulf of Mexico260' 1 NA $33,611 NA 97% 0230' 3 $13,842 27,224 97% 77% 0190-215' 6 14,385 22,221 54% 76% 0170' 2 NA 16,090 NA 94% 0140-150' 6 8,289 9,953 20% 68% 0120-130' 14 6,448 8,491 32% 86% 0105' 15 4,146 7,178 73% 72% 0

Domestic Total 47 $6,557 $12,086 84% 78%West Africa130-170' 17 NA $13,085 NA 87%(2)(2)(2)

Contract Drilling Segment Overview

17

Hercules: Contract Drilling Segment Overview

• Hercules owns a fleet of nine jackup rigs

– Six currently operating in U.S. GOM

– One operating in Qatar

– One operating in India

– One currently in a shipyard being upgraded to a 250’IC for international operations

• Specialized design features of three of Hercules’ rigs contribute to high utilization of the Company’s fleet

Source: ODS-Petrodata as of 11/27/06.(1) Excludes cold-stacked rigs, rigs that have announced mobilization

out of the GOM, and rigs expected to be permanently out of service due to recent Hurricanes.

Rig 22GOM Market Share: Jackups <= 250’(1)

1312

76

54

2 21

0

2

4

6

8

10

12

14

THE PDE ESV HERO NBR DO Blake RDC GSF

18

Hercules Drilling Fleet Status

Upgrading to 250’IC

FY 2006 FY 2007Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Location

GOM Rig 11 $61,914 $64,871 $65,976

GOM Rig 15 $52,692 $78,540 $95,487

GOM Rig 20 $73,499 $84,886 $100,781

GOM Rig 21 $79,925 $82,443

GOM Rig 22 $67,826 $83,899 $82,497

GOM Rig 30 $69,162 $67,933 $71,443

International Rig 16

International Rig 26

International Rig 31

Average Dayrate $69,534 $76,129 $81,283

Note: Q1, Q2 and Q3 2006 dayrates are based on actual results. Subsequent quarters represent estimates based on current backlog.

Contracted Dayrate TBD Available Shipyard

$64-66,000

$94-96,000

$114K-116K

$79-81,000

$84-86,000

$79-81,000

Through May 2008 @ $69-70,000

$84-86,000

$79-81,000

$79-81,000

$114K-116K

$89-91,000

$110-140K $140,000 $140,000

$69,860

19

0

50

100

150

200

250

300

350

400

450

500

Feb-

99

Nov

-99

Aug

-00

May

-01

Feb-

02

Nov

-02

Aug

-03

May

-04

Feb-

05

Nov

-05

Aug

-06

$-

$25

$50

$75

$100

$125

$150

$175

$200

0

50

100

150

200

250

300

Feb-

99

Nov

-99

Aug

-00

May

-01

Feb-

02

Nov

-02

Aug

-03

May

-04

Feb-

05

Nov

-05

Aug

-06

$-

$25

$50

$75

$100

$125

Source: ODS-Petrodata. West Africa dayrates are used to approximate average market rates for worldwide jackup rigs.

Increasing Backlog of Work

Business visibility has increased substantially over the past six years, both internationally and in the U.S. Gulf of Mexico.

Current Worldwide Jackup Backlog Current GOM Jackup Backlog

West Africa 300’ IC

Jan 1999187 Days

200’ MC Jackups in GOM

Jan 200432 Days

Oct 2006457 Days

Oct 2006245 Days

Aver

age

Rig

Day

s / M

arke

ted

Rig

Dayrate (in thousands)

Dayrate (in thousands)

Aver

age

Rig

Day

s / M

arke

ted

Rig

20

GOM Jackup Market Update

• A mixed bag – Since May 2006, there has been no clear trend in the U.S. GOM jackup market with a mix of increasing, flat and declining fixtures

• Departing rigs are creating contract gaps – 9 high-specification jackups in the GOM have announced contracts in other markets, leaving short-term work windows

• High-specification rigs competing for standard shelf work – Many of the rigs with reduced dayrates have been independent leg cantilevered jackups suggesting much of the pricing pressure is coming from higher specification rigs

• Move to the shallower water – the number of jackups drilling in 200’ or greater in the GOM declined from 16 in August 2005 to only 5 in November 2006

Source: ODS-Petrodata.

21

0

30

60

90

120

150

180

(# o

f Rig

s)

??? ??? ???

June 2001 Jackup Supply

Less: Cold Stacked/

Shipyard(1)

Marketed Supply

Less: Jackups Leaving

GOM

Plus Jackups

Reactivated (non-

contracted)

Visible Marketed

Supply

Less: Future Jackup

DeploymentsPlus:

NewbuildsPlus:

Reactivation of Cold

Stacked (9)

(19)

156

94

7510

(9)

76

Current Jackup Supply

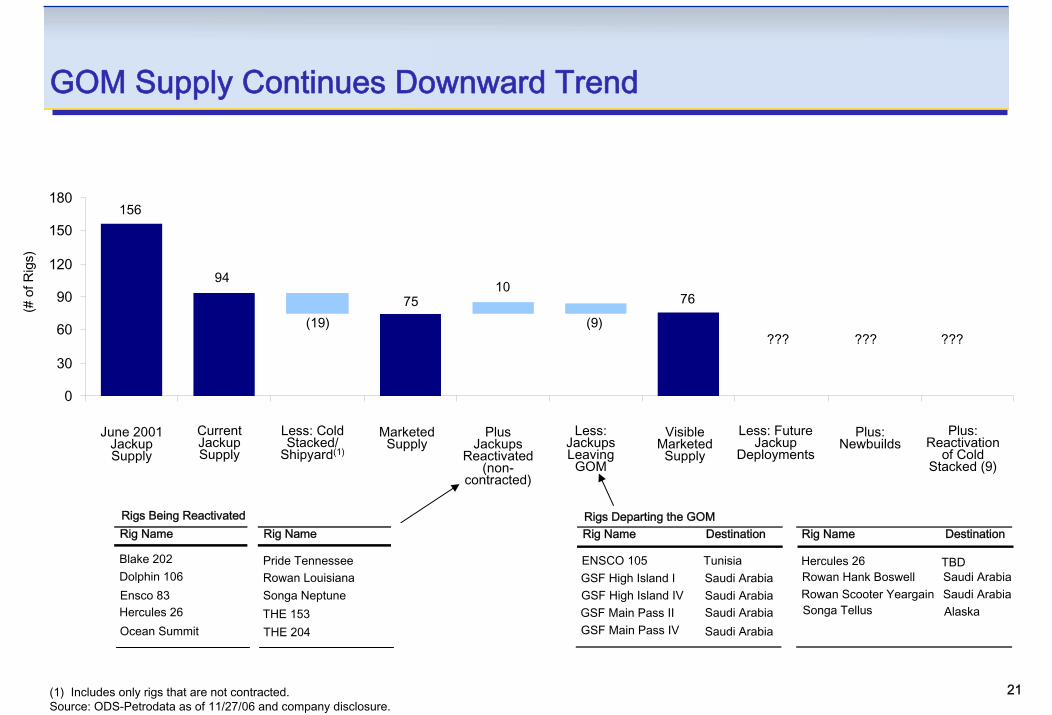

GOM Supply Continues Downward Trend

Rigs Being Reactivated Rig Name

Blake 202Rowan LouisianaDolphin 106

Ocean SummitTHE 153Songa Neptune

Pride Tennessee

Hercules 26THE 204

Rig Name

Ensco 83

Rigs Departing the GOMRig Name Destination Rig Name Destination

ENSCO 105 TunisiaGSF High Island I Saudi ArabiaGSF High Island IV

Saudi ArabiaGSF Main Pass IISaudi Arabia

Rowan Hank Boswell Saudi Arabia

GSF Main Pass IV Saudi Arabia

Hercules 26 TBD

Rowan Scooter Yeargain Saudi ArabiaSonga Tellus Alaska

(1) Includes only rigs that are not contracted.Source: ODS-Petrodata as of 11/27/06 and company disclosure.

22

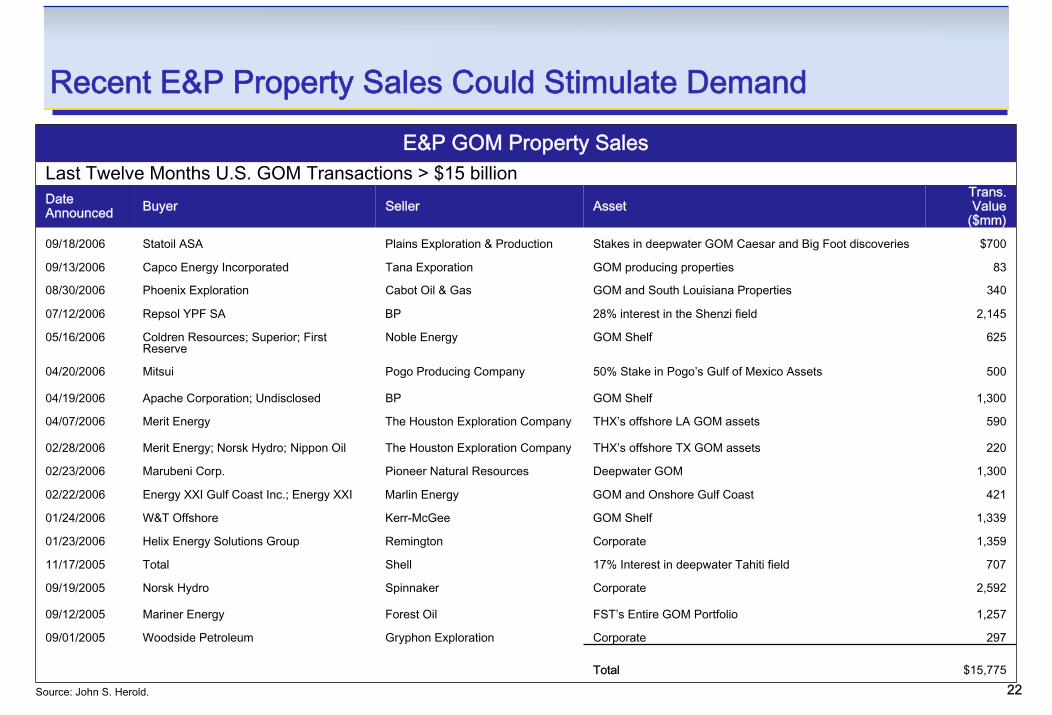

Recent E&P Property Sales Could Stimulate Demand

E&P GOM Property SalesLast Twelve Months U.S. GOM Transactions > $15 billionDateAnnounced Buyer Seller Asset

Trans.Value

($mm)09/18/2006 Statoil ASA Plains Exploration & Production Stakes in deepwater GOM Caesar and Big Foot discoveries $700

09/13/2006

08/30/2006

Capco Energy Incorporated

Phoenix Exploration

Tana Exporation

Cabot Oil & Gas

GOM producing properties

GOM and South Louisiana Properties

83

340

07/12/2006 Repsol YPF SA BP 28% interest in the Shenzi field 2,145

05/16/2006 Coldren Resources; Superior; First Reserve

Noble Energy GOM Shelf 625

04/20/2006 Mitsui Pogo Producing Company 50% Stake in Pogo’s Gulf of Mexico Assets 500

04/19/2006 Apache Corporation; Undisclosed BP GOM Shelf 1,300

04/07/2006 Merit Energy The Houston Exploration Company THX’s offshore LA GOM assets 590

02/28/2006 Merit Energy; Norsk Hydro; Nippon Oil The Houston Exploration Company THX’s offshore TX GOM assets 220

02/23/2006 Marubeni Corp. Pioneer Natural Resources Deepwater GOM 1,300

02/22/2006 Energy XXI Gulf Coast Inc.; Energy XXI Marlin Energy GOM and Onshore Gulf Coast 421

01/24/2006 W&T Offshore Kerr-McGee GOM Shelf 1,339

01/23/2006 Helix Energy Solutions Group Remington Corporate 1,359

11/17/2005 Total Shell 17% Interest in deepwater Tahiti field 707

09/19/2005 Norsk Hydro Spinnaker Corporate 2,592

09/12/2005 Mariner Energy Forest Oil FST’s Entire GOM Portfolio 1,257

09/01/2005 Woodside Petroleum Gryphon Exploration Corporate 297

Total $15,775

Source: John S. Herold.

Financial Overview

24

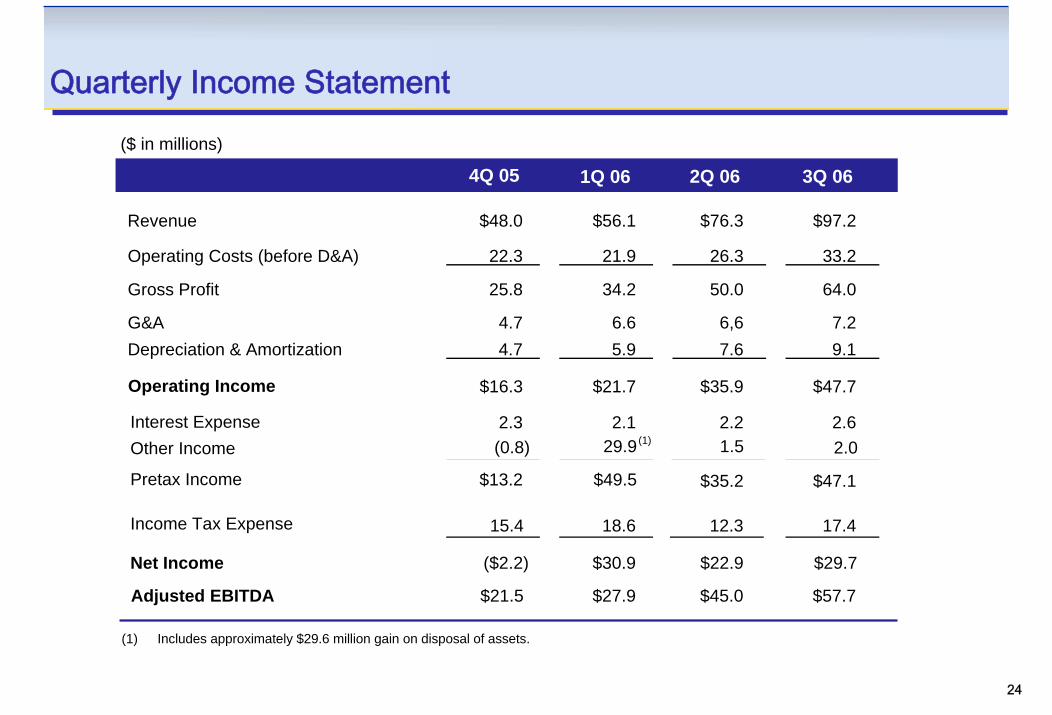

Quarterly Income Statement

(1) Includes approximately $29.6 million gain on disposal of assets.

(1)

4Q 05 2Q 061Q 06 3Q 06

($ in millions)

Revenue $48.0 $56.1 $76.3 $97.2

Operating Costs (before D&A) 22.3 21.9 26.3 33.2

Gross Profit 25.8 34.2 50.0 64.0

G&ADepreciation & Amortization

4.74.7

6.65.9

6,67.6

7.29.1

Interest Expense 2.3 2.1 2.2 2.6

Operating Income $16.3 $21.7 $35.9 $47.7

Other Income

Pretax Income

Income Tax Expense

Net Income

(0.8)

$13.2

15.4

($2.2)

29.9 1.5 2.0

$49.5 $35.2 $47.1

18.6 12.3 17.4

$30.9 $22.9 $29.7

Adjusted EBITDA $21.5 $27.9 $45.0 $57.7

25

Drivers of Financial Performance

Quarter Ending,12/31/05 3/31/06 6/30/06 9/30/06

Domestic Contract Drilling Services Segment:Operating Days 409 382 494 548# of Rigs (as of end of period) 9 6 6 6Average Dayrate $58,611 $70,673 $77,513 $84,776Average Utilization 88.9% 84.9% 94.3% 99.3%

International Contract Drilling Services Segment:Operating Days -- -- 33 100# of Rigs (as of end of period) -- 3 3 3Average Dayrate -- -- $129,577 $78,825Average Utilization -- -- 89.2% 100.0%

Domestic Marine Services Segment:Operating Days 2,999 2,850 2,802 3,171# of Liftboats (as of end of period) 46 42 47 47Average Dayrate $8,010 $8,981 $10,765 $12,641Average Utilization 83.5% 82.4% 75.8% 77.0%

International Marine Services Segment:Operating Days -- 357 355 235# of Liftboats (as of end of period) -- 4 4 4Average Dayrate -- $9,913 $10,047 $12,050Average Utilization -- 99.0% 98.0% 63.9%

26

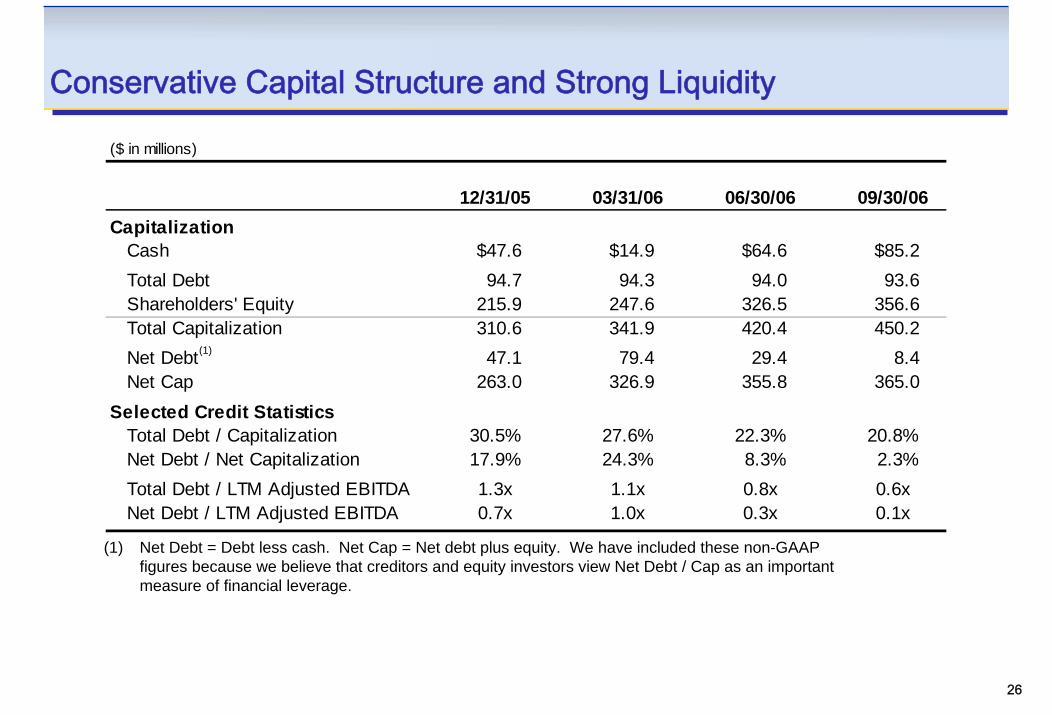

Conservative Capital Structure and Strong Liquidity

(1) Net Debt = Debt less cash. Net Cap = Net debt plus equity. We have included these non-GAAP figures because we believe that creditors and equity investors view Net Debt / Cap as an important measure of financial leverage.

($ in millions)

12/31/05 03/31/06 06/30/06 09/30/06Capitalization

Cash $47.6 $14.9 $64.6 $85.2Total Debt 94.7 94.3 94.0 93.6Shareholders' Equity 215.9 247.6 326.5 356.6Total Capitalization 310.6 341.9 420.4 450.2Net Debt 47.1 79.4 29.4 8.4Net Cap 263.0 326.9 355.8 365.0

Selected Credit StatisticsTotal Debt / Capitalization 30.5% 27.6% 22.3% 20.8%Net Debt / Net Capitalization 17.9% 24.3% 8.3% 2.3%Total Debt / LTM Adjusted EBITDA 1.3x 1.1x 0.8x 0.6xNet Debt / LTM Adjusted EBITDA 0.7x 1.0x 0.3x 0.1x

(1)

27

Gross Margin vs. PeersHigher Profitability Despite Lower Specification Assets

32%

39%

40%

41%

42%

44%

45%

45%

49%

52%

57%

0% 10% 20% 30% 40% 50% 60%

PDE

RDC

THE

RIG

ATW

GSF

DO

NE

SPN

HERO

ESV

Note: For purposes of this presentation, gross margin has been calculated by subtracting operating costs (excluding SG&A and depreciation and amortization) from revenues, and dividing by revenues, in each case as publicly reported by the listed companies. Analysis on GSF excludes its drilling management business as management believes this business is significantly less capital intensive than the drilling and other oilfield services businesses. ATW reflects nine months ended June 30, 2006, as September 30, 2006 numbers have not been published (as of November 29, 2006).

37%

41%

42%

43%

47%

49%

54%

57%

58%

65%

68%

0% 10% 20% 30% 40% 50% 60% 70%

PDE

RIG

THE

RDC

ATW

GSF

SPN

DO

NE

HERO

ESV

9 Months Ending 9/30/2006Year-end 2005

28

First Year Anniversary as a Public Company – Report CardGrow the Company

– Grew revenue and assets by 103% and 109%, respectively, during the 12 months ended September 30, 2006

Maintain Financial Discipline

– Generated a 33.9% ROCE(1) for the 12 months ended September 30, 2006

– Reduced total debt to cap from 57.1% at September 30, 2005 to 20.8% at September 30, 2006

Diversify Geographically

– At time of IPO, 100% of revenue was derived in GOM

– Today, 3 of our 9 jackups and 17 of our 64 liftboats are focused internationally

Generate Attractive Returns for Our Shareholders

– As of November 24th, the Company’s share price has appreciated by 44.7% since the IPO versus 24.4% for the OSX

(1) ROCE (Return on Capital Employed) – Defined as Adjusted EBIT divided by average total assets less average current liabilities.

29

Explanatory Information

Adjusted EBITDA is calculated as net income before interest expense, taxes, depreciation and amortization, gain on disposal of assets and loss on early retirement of debt. Adjusted EBITDA is included in this presentation because our management considers it an important supplemental measure of our performance and believes that it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry, some of which present EBITDA and Adjusted EBITDA when reporting their results. We regularly evaluate our performance as compared to other companies in our industry that have different financing and capital structures and/or tax rates by using Adjusted EBITDA. In addition, we utilize Adjusted EBITDA in evaluating acquisition targets. Management also believes that Adjusted EBITDA is a useful tool for measuring our ability to meet our future debt service, capital expenditures and working capital requirements, and Adjusted EBITDA is commonly used by us and our investors to measure our ability to service indebtedness. Adjusted EBITDA is not a substitute for the GAAP measures of earnings or of cash flow and is not necessarily a measure of our ability to fund our cash needs. In addition, it should be noted that companies calculate EBITDA and Adjusted EBITDA differently and, therefore, Adjusted EBITDA as presented for us may not be comparable to EBITDA and Adjusted EBITDA reported by other companies. Adjusted EBITDA has material limitations as a performance measure because it excludes interest expense, taxes, depreciation and amortization, gain on disposal of assets and loss on early retirement of debt. The following tables reconcile Adjusted EBITDA with net income.

EBITDA Reconciliation($ in millions)

Drilling Liftboats1Q 05 2Q 05 Q3 05 4Q 05 1Q 06 2Q 06 3Q 06 1Q 05 2Q 05 Q3 05 4Q 05 1Q 06 2Q 06 3Q 06

Net Income $9.5 $7.6 $10.5 $0.5 $25.6 $15.6 $19.1 $2.5 $1.5 $2.5 ($1.6) $7.5 $9.3 $12.6Plus: Interest Expense 1.8 1.8 1.9 1.5 1.3 1.4 1.7 0.5 0.6 0.9 0.8 0.7 0.8 0.9Plus: Income Tax Expense – – – 6.9 15.1 7.5 10.5 – – – 8.9 4.4 5.5 7.6Plus: Depreciation and Amortization 1.3 1.3 1.4 1.5 1.7 2.3 3.5 1.2 1.5 2.3 3.2 4.3 5.2 5.6Plus: Loss on Early Retirement of Debt – 1.8 – 0.8 – – – – 0.9 – 0.5 – – –Less: Gain on Disposal of Assets – – – – 29.6 – 1.1 – – – – – – –

Adjusted EBITDA $12.5 $12.6 $13.8 $11.3 $14.1 $26.8 $33.7 $4.2 $4.6 $5.8 $11.7 $16.8 $20.7 $26.7

Company EBITDA Reconciliation($ in millions)

Company1Q 05 2Q 05 Q3 05 4Q 05 1Q 06 2Q 06 3Q 06

Net Income $11.4 $8.2 $10.1 ($2.2) $30.9 $22.9 $29.7Plus: Interest Expense 2.3 2.5 2.7 2.3 2.1 2.2 2.6Plus: Income Tax Expense – – – 15.4 18.6 12.3 17.4Plus: Loss on Early Retirement of Debt – 2.8 – 1.3 – – –Less: Gain on Disposal of Assets – – – – 29.6 – 1.1

Adjusted EBIT $13.7 $13.5 $12.8 $16.8 $22.0 $37.4 $48.6Plus: Depreciation and Amortization 2.5 2.9 3.8 4.7 5.9 7.6 9.1

Adjusted EDITDA $16.2 $16.3 $16.6 $21.5 $27.9 $45.0 $57.7

Note: Reconciliations for Drilling and Liftboats do not include corporate adjustments.