carrefour hy2011 uk hy2011_uk_0.pdfcarrefour planet rollout underway: ... excluding logistic...

TRANSCRIPT

1

New game plan

2

Introduction & Summary – Lars Olofsson• First‐Half Highlights• Midway through the Transformation Plan: Achievements • H1 2011: Lessons Learned• New Game Plan, New Team

Results Review – Pierre Bouchut

New game plan, pursuing our strategic priorities – Lars Olofsson• FRANCE ‘RESET’ – New Commercial Strategy and Action Plan – Noël Prioux• PLANET – Progress Update• ADJUSTING – to new context in Southern Europe• GROWTH MARKETS – Brazil and China Update

Conclusion – Lars Olofsson

3

Introduction & SummaryLars Olofsson

4

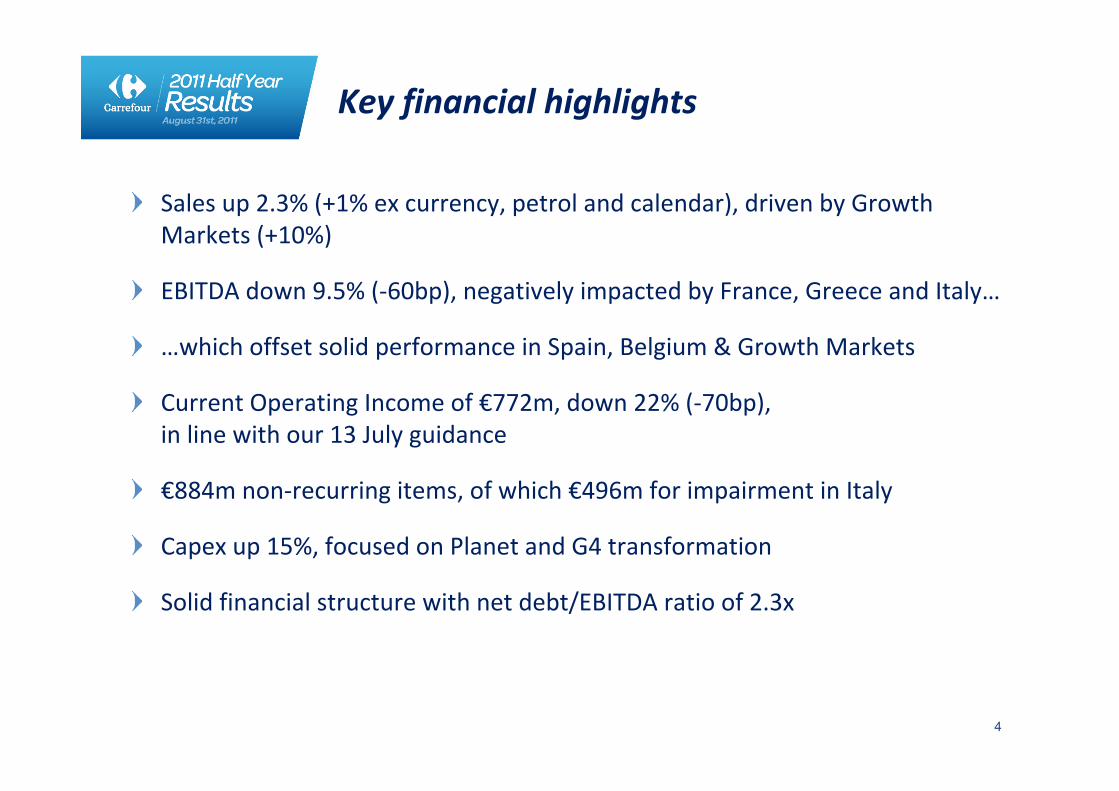

Key financial highlights

Sales up 2.3% (+1% ex currency, petrol and calendar), driven by Growth Markets (+10%)

EBITDA down 9.5% (‐60bp), negatively impacted by France, Greece and Italy…

…which offset solid performance in Spain, Belgium & Growth Markets

Current Operating Income of €772m, down 22% (‐70bp), in line with our 13 July guidance

€884m non‐recurring items, of which €496m for impairment in Italy

Capex up 15%, focused on Planet and G4 transformation

Solid financial structure with net debt/EBITDA ratio of 2.3x

5

Overall environment characterized by major price hikes from suppliers and worsening economic environment in Southern Europe during Q2

Unsatisfactory execution of Group strategy in France

Disappointing performance in Italy and Greece

Resilient performance in Spain

Encouraging recovery in Brazilian hypermarkets

Confirmed turnaround in Belgium, Poland and Taiwan

Carrefour Planet rollout underway: 13 stores across Europe in Q2

Spin‐off of DIA completed

Key business highlights

6

Mid‐way through the Transformation Plan: Achievements

HYPERMARKET REINVENTION: ROLLING OUTPlanet: from 6 pilot stores to the launch of industrial roll out

COST SAVINGS: DELIVERED€1.3bn of cost reductions achieved since launch of Plan

BRAND REVITALIZATION: ON TRACKCarrefour branded offer repositioned and enriched assortment

BEST PRACTICE SHARING: UNDERWAYCompetence centers created to share best practices throughout the group

7

H1 2011: Lessons learned

FRANCE

Too much, too quickly

Unsatisfactory execution of strategy

Intensifying price competition due to commodity price hikes

Over‐focus on market share

● New head for France in place

● Action plan implemented to regain momentum

● New commercial strategy focused on enhanced price competitiveness and sustainable traffic gains

8

H1 2011: Lessons learned

Built‐in rigidities in our processes and complexity of our organization

ORGANIZATION

Duration and depth of downturn in Europe and commodity price hikes severely affecting consumption

ENVIRONMENT •Slower GDP forecast in Europe•Adjusted Capex and further cost savings in Europe

•Timeline on purchasing savings and inventory reduction revised

•Reinforced executive team •Better coordinate plans, processesand people

•Adjust speed of implementation•Enhance predictability through improved internal controls

9

Decisive actions to regain momentum

• New game plan

France “Reset”

Adapting to the new context in Europe

• New Team

• Pursuing strategic priorities Continue delivering on Transformation Plan

Focus on growth levers:Emerging Markets

Planet

Carrefour brand

Step change to meet our Strategic Goal: Sustainable, Profitable Growth

10

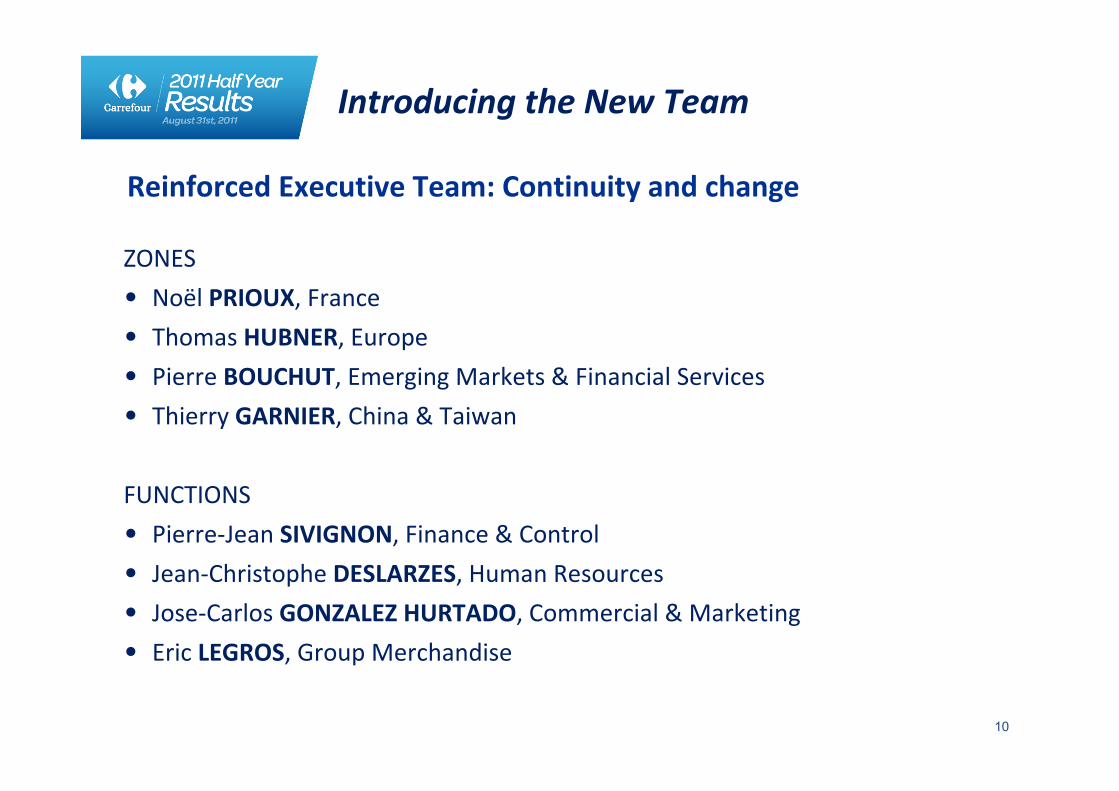

ZONES

• Noël PRIOUX, France

• Thomas HUBNER, Europe

• Pierre BOUCHUT, Emerging Markets & Financial Services

• Thierry GARNIER, China & Taiwan

FUNCTIONS

• Pierre‐Jean SIVIGNON, Finance & Control

• Jean‐Christophe DESLARZES, Human Resources

• Jose‐Carlos GONZALEZ HURTADO, Commercial & Marketing

• Eric LEGROS, Group Merchandise

Reinforced Executive Team: Continuity and change

Introducing the New Team

11

Pierre Bouchut

12

Summarized H1 P&L

(1) Adjusted as per DIA deconsolidation, Thailand deconsolidation and restated as per Brazil(2) Excluding the depreciation of the assets of our integrated supply chain operations (€50m in H1 2011 and €37m in H1 2010)

Net Sales 38,710 39,607 2.3%

H1 2011 Var.H1 2010 (1)

Non‐recurring items (353) (884) 150.1%

Net financial expenses (349) (342) (2.2%)

Income tax (238) (490) 105.8%

Net income, Group share

€m

Interest expenses (270) (258) (4.4%)Other financial expenses (79) (84) 6.3%

97 (249) na

Current operating income 989 772 (22.0%)

Net income from disc. operations 85 680

EBITDA (2) 1,855 1,679 (9.5%)

Operating income 636 (112) (117.5%)

302 153 (49.3%)Net income, Group share, Adjusted for exceptional items

13

Sales growth in a challenging environment

€38,710m

102.3

H1 2010 sales Petrol impactOrganic expansion

& acquisitions (2)

Like for likeEx petrol

Fx Impact H1 2011 salesH1 2011 sales at constant

exchange rates ex petrol

ex calendar impact

(1) Adjusted as per IFRS 5, Thailand and DIA have been retroactively deconsolidated

(2) The variation between the reported 2.7% increase in H1 sales including VAT is mainly explained by an increase in the value added tax in several European countries: Spain, Greece, Poland and Romania. This 0.4% difference has been included in the “Organic expansion & acquisitions” column.

Change in net sales (1) (2)

(in %)

+0.1 +0.9

101.0 +1.1

+0.2

€39,607m

14

Sales growth driven by emerging markets

€m

France

Europe

Latin America

Asia

16,806

H1 2010

11,989

6,463

3,452

38,710

17,073

H1 2011

11,517

7,298

3,719

39,607

1.6%

Evolution

‐3.9%

12.9%

7.7%

2.3%Total

‐0.2%

Evolution at constant exch. rates ex petrol

‐4.6%

11.6%

6.7%

1.0%

15

Decrease in commercial margin in a tougher competitive environment

20 bp decrease in commercial margin as a % of sales ex petrol (‐40bp inc. petrol)

Tough competitive environment in Europe, notably in France

Strong rise in commodity prices

Positive impact of €42m from logistics gains

8,494

8,428

21.4%

21.8%

23.4%

23.6%

Commercialincome

(€m)

Commercialmargin

as a % of sales

Ex petrolCommercial margin

as a % of sales

H1 2010 H1 2011

16

Stable underlying SG&A as a percentage of sales

€m H1 2010 ChangeH1 2011

SG&A (excluding asset costs) (6,149) +3.8%

As a % of sales 15.9%

(6,381)

16.1% +20bp

Asset costs (rents & depreciation) (1,290) +3.9%

As a % of sales 3.3%

(1,341)

3.4% +10bp

As a % of sales 19.2%

SG&A including asset costs (7,439) +3.8%(7,722)

19.5% +30bp

Adjusted for the end of the Loi Fillon benefits and other non‐recurring elements, underlying SG&A costs as a % of sales are stable

17

SG&A (ex. asset costs) up despite significant cost savings

(1) The incidence of foreign exchange differences was neutral on H1 SG&A costs

158

75

169

SG&A ex. asset costsH1 2010

Cost savingsCost inflation (salaries, “LoiFillon”, etc.)

SG&A ex. asset costsH1 2011

Additional operating taxes

Expansion and transformation

Other & Forex (1)

(195)25

Change in SG&A excluding asset costs(€m)

€6,149m

€6,381m

18

Efficiency gains on all fronts

Store operations

Support functions

Other SG&A

Total cost reductions

51

33

86

236

H1 2011

Cost reductions 66Of which

Rest of the World

Of which G4

Operating cost savings

Logistics cost savings

195

42

€m

Total cost reductions 236

19

EBITDA (1)(2)(€m and % of sales)

Net sales(€m)

Current OperatingIncomebefore

Group overhead(€m and % of sales)

CAPEX(€m)

France: unsatisfactory sales and EBITDA performance

Net sales broadly stable ex petrol (+1.6% inc. petrol)

EBITDA down 17.4% reflecting: • A decrease in commercial margin due to rise in supplier tariffs

• Impact of operational issues (out‐of‐stock, textile, fresh food pricing)

• Increase in operating costs in French hypermarkets

Current Operating Income down 37%

CAPEX up 22% mainly focused on IT and start‐up phase of Planet23,000 gross new sqm, 12,000 net sqm

(1) Unallocated headquarter costs of €76 m in H1 2010 and €73m in H1 2011 (2) excluding logistic depreciation of €12m in H1 2010 and €36 m in H1 2011

8815.2%

728 4.3%

16,806

17,073

5473.3%

3442.0%

239

292

‐17.4%

+1.6%

‐37.1%

+22%

H1 2010 H1 2011

20

Europe: EBITDA weighed down by Greece and Italy

5354.5%

4353.8%

11,989

11,517

2432.0%

1681.5%

166

246

‐18.8%

‐3.9%

‐30.7%

+48%

(1) Unallocated headquarter costs of €76m in H1 2010 and €73m in H1 2011 (2) excluding logistic depreciation of €22m in H1 2010 and €11m in H1 2011

Net sales down 4.6% ex petrol at constant exchange rates (‐3.9% including petrol and currency)

EBITDA margin down 70bp reflecting: • decline in sales of €472m • decrease in commercial margin• strong grip on operating costs overall• deteriorating profitability in Greece and Italy

Current Operating Income margin down 50bp

Ex. Greece and Italy, broadly flat EBITDA and Current Operating Income up 6%

CAPEX up 48%, boosted by Carrefour planet rollout145,000 gross new sqm, 46,000 net sqm

EBITDA (1)(2)(€m and % of sales)

Net sales(€m)

Current OperatingIncomebefore

Group overhead(€m and % of sales)

CAPEX(€m)

H1 2010 H1 2011

21

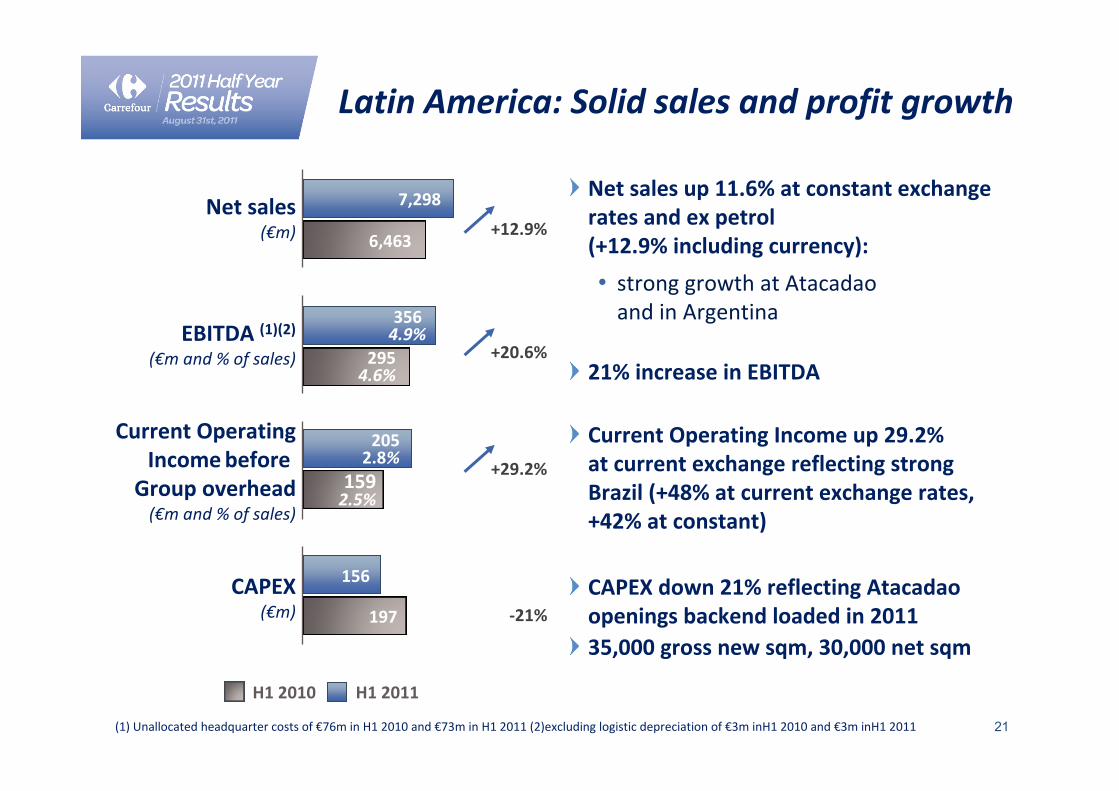

Latin America: Solid sales and profit growth

1592.5%

Net sales up 11.6% at constant exchange rates and ex petrol (+12.9% including currency):

• strong growth at Atacadao and in Argentina

21% increase in EBITDA

Current Operating Income up 29.2% at current exchange reflecting strong Brazil (+48% at current exchange rates, +42% at constant)

CAPEX down 21% reflecting Atacadao openings backend loaded in 201135,000 gross new sqm, 30,000 net sqm

2954.6%

356 4.9%

6,463

7,298

2052.8%

156

(1) Unallocated headquarter costs of €76m in H1 2010 and €73m in H1 2011 (2)excluding logistic depreciation of €3m inH1 2010 and €3m inH1 2011

197

+20.6%

+12.9%

‐21%

+29.2%

EBITDA (1)(2)(€m and % of sales)

Net sales(€m)

Current OperatingIncomebefore

Group overhead(€m and % of sales)

CAPEX(€m)

H1 2010 H1 2011

22

Asia: Rise in sales and EBITDA

2206.4%

2336.3%

3,452

3,719

1183.4%

1283.4%

56

67

(1) Unallocated headquarter costs of €76m in H1 2010 and €73m in H1 2011

+6.2%

+7.7%

+8.7%

+19%

Net sales up 6.7% ex petrol and at constant exchange rates(+7.7% including petrol and currency)

EBITDA up 6.2% reflecting:

• Resilient performance in China with an increase of 2.7% at current exch. rates

• Confirmed turnaround in Taiwan

CAPEX up 19%35,000 gross new sqm; 3,000 net sqm

EBITDA (1)(€m and % of sales)

Net sales(€m)

Current OperatingIncomebefore

Group overhead(€m and % of sales)

CAPEX(€m)

H1 2010 H1 2011

23

Transformation Plan: cost reduction on track

1,065

570485

860

1,135

2009 – 2012 targets and achievements for operating cost savings, ex DIA (€m)

1,300

1,870

Targeted Achieved

2009 2010 H1 2011 2012

On track on operating cost savings:• €236m achieved in H1 2011

• Target of €480m for 2011

Main cost reduction drivers• Logistics savings

• Contract renegotiation with third parties

• Energy, recycling and other SG&A reduction

24

Transformation Plan: on track on cumulative purchasing gains despite lost momentum in H1

No further purchasing savings booked in H1 2011 in a context of:

• Tough negotiations

• Tough price competition

• Strong rises in commodity prices335

4040

250

356

335

850

2009 – 2012 targets and achievements for purchasing gains, ex DIA (€m)

Targeted Achieved

2009 2010 H1 2011 2012

25

Personal Financial Services: Continued solid growth of all KPIs

Savings accounts (€m)

Consumer Credit Outstanding (€m) Insurance premiums (€m)

+2.8%5,708

5,551 +4.0%133

128

Number of cards (millions)

+2.5%1,824

1,779+3.7%

14.2

13.7

Launch of “Carrefour Banque” brand in H1

Brazil: New partnership agreement with Itau Unibanco

H1 2010 H1 2011

26

Europe (mainly Spain & Belgium)

Rest of the World (mainly Brazil, Colombia

and Argentina)France

Geographical breakdown (%)

Other contribution

InsuranceBanking

Breakdown of Personal Finance Services contribution (%)

18%

5%77%

30%

37%

33%

(1) Before unallocated headquarter costs and including financial services commissions, warrantee revenues and cost saving generated by the reduction in fees as compared to competing payment cards

Personal Financial Services: +15.5% in Current Operating Income (1)

Current Operating Income (1) (€m)Net Banking income evolution (€m)

H1 2010 H1 2011

532

473 +12.5%

181

157 +15.5%

27 (1) Current Operating Income pre‐group overhead

Net rents ‐ Total

Of which Carrefour tenants

Of which external tenants

EBITDA

Current Operating Income (1)

France, Spain, Italy, and HO (€m)

Carrefour Property: Downward adjustment in rents to be in line with market practice

‐5.7%

‐4.9%

‐5.7%

5.9%

‐3.4%

Var.

160

362

336

25

337

H1 2010

151

H1 2011

344

317

27

325

28

€884m non‐recurring charges

Restructuring OtherNet capital gains / losses

Transformation (3)

(1) Impairment: mainly linked to Italy(2) Allowances for tax litigation in France, Brazil and equity tax in Colombia(3) Transformation: mainly linked to the implementation of our cost cutting measures

(516)

16

Impairment (1)

(39)

(244)

Operating tax expense (2)

(22)

(79)

Total

(884)

29

Slight improvement in inventory turn

H1 2011 inventories up €48mvs. H1 2010 (€m)

Improvement in inventory turn(days of COGS down 0.7)

H1 2010 H1 2011H1 2010 H1 2011

6,494

6,447 37.037.7

30

17%

32%

51%

19%

42%

39%

CAPEX up with focus on Planet and remodelling

New space

Remodelling /Maintenance

France

Europe

Latin America

Asia

659 761

9% 9%

25%

36%

30%20%

32%

38%

H1 2011 CAPEX (€m) up 15% vs. H1 2010

More CAPEX allocated to Carrefour Planet in Europe and IT in France

H1 2010 H1 2011

659 761

IT

H1 2010 H1 2011

31

Net debt reduced by €770m

(1) Restated in accordance with IAS 8 for Brazil

Opening net debt (11,424)

Gross Cash flow 3,405

Change in WCR and others (363)

Expansion capex (629)

Free cash flow 1,108

Acquisitions (178)

Disposals 222

Thailand cash‐in 808

Dividends & Treasury shares (2) (895)

Net debt at close (10,654)

Consumer credit impact (98)

(2) Including €778m share buy‐back

(€m) 12 months to June 2011 (1)

Remodelling and maintenance capex (1,306)

Operating Free cash flow 1,736

Others (197)

32

Key cash flow figures proforma ex‐DIA

Reported Proforma ex‐DIA12 months to June 2011 (€m)

Operating free cash flow 1,736 1,573

Gross cash Flow 3,405 2,974

Free cash flow 1,108 944

Net debt at close 10,654 9,798

33

Sound financial structure

EBITDA / Interest expenses 9.1x 8.5x

Rating agenciesS&PMoodysFitch

A stable outlookA3 negative outlookA‐ stable outlook

BBB+ stable outlookBaa1 negative outlookBBB+ negative outlook

Net debt at close 11,424 9,798

Gross cash flow / net debt at close 29.1% 30.4%

12 months to 30 June 2010(with Dia)

12 months to 30 June 2011(excl. Dia)

Net debt at close / EBITDA 2.4x 2.3x

Gearing 103.6% 110.7%

34

Sound liquidity position

Thanks to an excellent liquidity position, no transactions necessary in debt capital markets

Short‐term liquidity ensured through low levels of French commercial paper (c. €621m)

Commercial paper program backed‐up by two undrawn syndicated credit facilities totaling €3.25bn and maturing in 2012 and 2015 with no financial covenants

Well diversified bond redemption profile, no refinancing concentrations

Next bond redemption due in April 2012 (€264m)

2012 1,260

Debt redemption schedule (€m)

1,4502013

1,5002014

1,3512015

6002016

2502017

2018

2019

1,0002020

1,0002021

35

New game plan,pursuing strategic priorities

Lars Olofsson

36

France ‘‘Reset’’: New commercial strategy and action plan

Lars Olofsson – Noël Prioux

37

Diagnosis: Too much, too quickly

Change in category and pricing management

Change in commercial dynamics

New IT systems for stores and merchandise

Head‐office move and rationalization

Planet concept launch and implementation

France

Unwanted side‐effectsUnsatisfactory execution

Many critical steps in our Transformation…

38

3.Accelerate

2.Rebuild

• Hypermarket commercial mix (price ‐ promotion ‐loyalty)

• Carrefour branded products

• Expansion / Carrefour Drive

• E‐commerce

• Cost savings

1.Adjust

• Organization and IT Systems

• Out‐of‐stocks

• Planet deployment

Our 3‐pillar action plan to rebuild momentum

France

39

Simplify head office systems and processes

Intensify focus on non‐food assortment &

profitability

Adjust Hypermarket organization

Differentiated organization depending on store size and requirements.

More responsibility for the store manager

Creation of a dedicated non‐food merchandise department

Focus on merchandise and supply chain

Simplified interaction between head‐office and stores

France 1 ‐ Adjust organization

40

Objectives

Excessive level of out‐of‐stocks•7% in food•18% in non food

Diagnosis

Dedicated task force•Reduce in‐store IT glitches•Improve inventory management in intermediate warehouses

•Better coordination between merchandise and store management

Action Plan

30% decrease in out‐of‐stocks by September 201150% decrease in out‐of‐stocks by end 2011

France 1 ‐ Adjust out‐of‐stocks

41

• Significant outperformance compared to non converted stores…

• …despite suboptimal execution

• Concept not fully implemented

• Absence of specific commercial program

• Overly drastic reduction in some product categories

• Priority in H1 to IT deployment before store rollout

Diagnosis

Improved execution, new timeline

•Full deployment by 2013 as planned

•First wave moved from June to September to benefit from adjustments

•26 stores instead of 40 initially planned in 2011, 14 moved back to early 2012

•Specific Carrefour Planet event and seasonal commercial program

Action Plan

France 1 ‐ Adjust Planet deployment

42

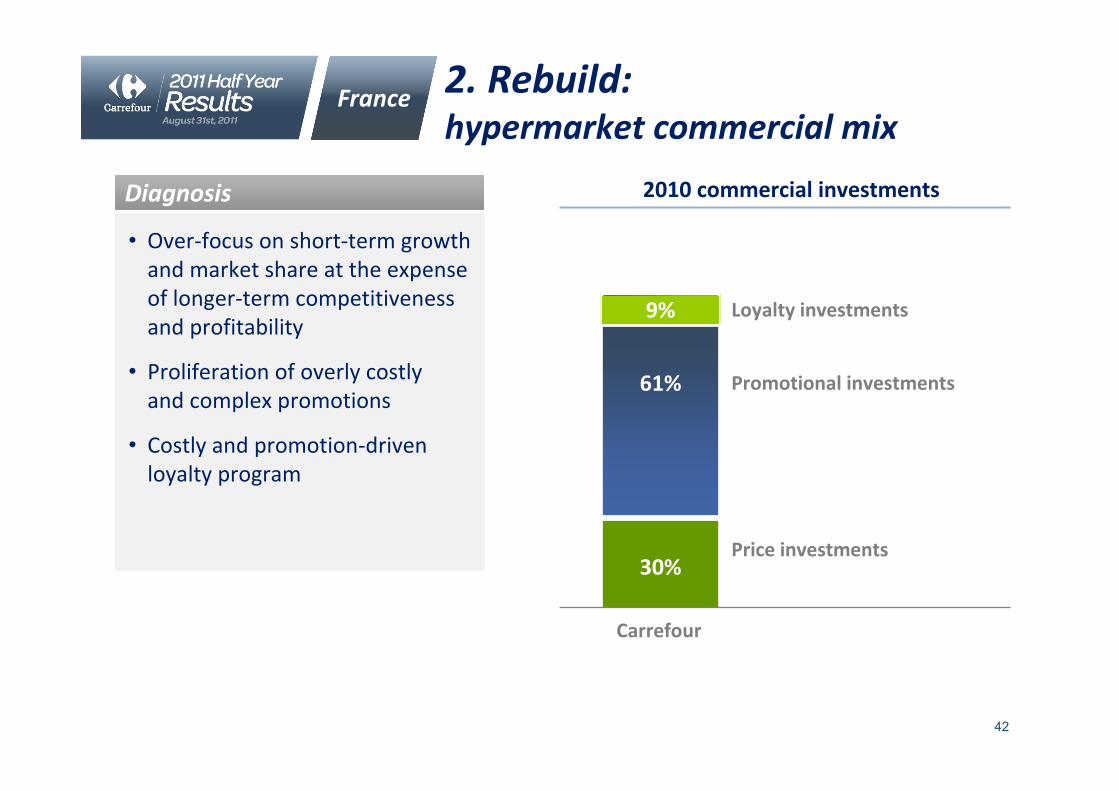

• Over‐focus on short‐term growth and market share at the expense of longer‐term competitiveness and profitability

• Proliferation of overly costly and complex promotions

• Costly and promotion‐driven loyalty program

Diagnosis

France

2010 commercial investments

Carrefour

Loyalty investments

Promotional investments

Price investments

2. Rebuild: hypermarket commercial mix

9%

61%

30%

43

A step change in execution

•Targeted price investment to improve price competitiveness in dry grocery

•Drive Carrefour branded growth

•Reinforce customer communication

• Price • Carrefour brand

•Financed by • rebuilt loyalty program• fewer but more impactful promotions• gains on non‐food

Short term negative impact on sales to gain a sustainable profitable growthplatform

Action Plan

France 2. Rebuild: hypermarket commercial mix

Non food

Promotions

Food pricing

Targetedloyalty

Carrefour brand

Source Investment

44

France 2. Rebuild: hypermarket commercial mix

45

France2. Rebuild: hypermarket commercial mix

46

France3. Accelerate: Carrefour‐branded products

• Carrefour brand relaunch beginning in September 2011

• Innovations• Renovations• Price realignment• New visual identity

• Specific communication plan

• Targeting 40% Carrefour brand participation (vs. 25% in 2011)

Action Plan

47

3. Accelerate: Expansion, Drive, Internet

France

• Expansion:

• Boost smaller formats’ expansion• Grow selling space in line with market mainly through franchise and convenience

• Drives at year‐end:

• 22 hypermarkets • 24 supermarkets

• Internet:

• Launch of the Carrefour/Pixmania website in November

Action Plan

48

Conclusion

•A decisive step change:Consistent implementation of new commercial strategy

Priority to rigorous execution over speed

•A comprehensive action plan to:

Unleash the full potential of Carrefour Planet

Reap benefits of Non‐Food strategy implementation

Simplify processes and systems

Enhance competitiveness

Regain lost ground on drives and e‐business

Short term negative sales impact on the way to profitable growth

France

France ‘Reset’

49

Planet deployment update

50

Sinceopening

H1 2011

Sales growth Traffic evolution Market share evolution

Sharply improved performance in the 4 Planet model stores

17%

18.8%

+180bp

10.9%

14.3%

Since opening

H1 2011

+9.7%

13.3%

Strong sales and traffic growth in four model stores*

• Encouraging profitability improvement driven by:Volume growthLower labor costs as a % of sales despite additional services

• Further upside through: Non‐food gains New store operating model

Planet

Before opening After opening

* Four model stores FRANCE ‐ Venissieux – SPAIN ‐ El Pinar – Mostolles – BELGIUM ‐ Mont St Jean.

51

Rollout of Carrefour Planet: slight adjustment in phasing

Fine tuning and optimization of the concept

Rollout from April

2010 2011

98 Carrefour Planet in G4 and Greece

82 Carrefour Planet: 27 in France – 43 in Spain –9 in Belgium‐ 2 in Italy –1 in Greece

6 Carrefour Planet pilot stores in G3

4 model stores

Initial plan

Upd

ated

plan

Planet

52

CompletionCompletion

2010 2011

98 Carrefour Planet in G4 and Greece

82 Carrefour Planet: 27 in France – 43 in Spain –9 in Belgium‐ 2 in Italy –1 in Greece

6 Carrefour Planet pilot stores in G3

4 model stores

Initial plan

Upd

ated

plan

2013

Total 503 hypermarkets:241 Carrefour Planet262 renovated hypermarkets

Total 464 hypermarkets:221 Carrefour Planet243 renovated hypermarkets

Completion

Planet

Fine tuning and optimization of the concept

Rollout from April

Carrefour Planet rollout: pragmatic adjustments

53

Adapting to newcontext: Southern Europe

54

Adapting to new context

•Greece:Conversion of remaining DIA stores to Carrefour banner

Freeze on further expansion

Capex reduction with conversion of 10 Planet (vs. 14 initially planned) and no investment in remodelling (vs. 23 initially planned) by 2013

• Italy:Adapted commercial strategy, price repositioning underway

Ongoing banner conversion for convenience

Capex reduction with 43 hypermarkets converted/ remodelled (vs 53 initially planned) by 2013

• Spain:Ongoing cost optimization

Capex optimization with 103 stores remodelled rather than converted to Planet (vs 89 initially planned) by 2013

Southern Europe

55

Pursuing our leadership ambition in Growth Markets

56

Reinforcing leadership in key countries

•Reinforcing leadership in growth markets with:

475 new stores to be opened in 2011, for total of c. 583 000 new gross sqm

Planned FY Capex of €900m, up 20% vs. 2010

Development of new formats (e‐commerce, Carrefour Express)

Expand Atacadao throughout Latin America

Growth Markets

New stores under banners 2011 Hypers Atacadao Supers Convenience Cash & Carry Total

Latin America 2 22 3 69 96

Asia 31 1 32

Eastern Europe 9 58 246 313

Franchise (ME, Dom Tom) 9 20 3 2 34

Total 51 22 81 318 3 475

57

Brazil: Strong commitment, strong performance

• 2nd largest country for the Group, representing 14% of Group sales

• Carrefour No1 food retailer

• Continued strong growth at AtacadaoNear double digit LfL growth in H1 2011

17 new stores planned in 2011

• Positive results from hypermarket turnaround plan

Growth Markets

Net sales (€m)

4,6955,455

+16.2%

Current Operating Income (€m)

+48.2% (+60bp)

H1 2010 H1 2011 H1 2010 H1 2011

58

Brazil : A positive turnaround in hypermarkets

•Return to Lfl growth thanks to:Commercial dynamicsStore renovationsFixing the basics

• Strong rebound in profitability thanks to:Head‐office downsizingNew store operating modelPurchasing improvementsStore closures & Transformations to Atacadao

Growth Markets

Hypermarket turnaround plan drives sales and profit growth in 2011

59

2,044

2,251

+10.1%

Growth Markets China: Consolidate our leadership

• 5th‐largest country for the Group, representing 6% of Group sales

•No1 international banner

• Solid growth in H1 2011 supported by ongoing expansion

• Simplified partnership structure

• Pursuing sustained and profitable expansion: 23 new stores in 2011

• Inflationary pressure on consumption likely to continue in H2

Net sales (€m)

H1 2010 H1 2011

60

61

New game plan to rebuild momentum

• Implementing a new game plan…

France “Reset”

Adapting to the new context in Europe

• …While pursuing our strategic priorities

Pursue Transformation Plan

Focus on growth levers: Emerging Markets, Planet, Carrefour brand

“Biting the bullet” in 2011: Group Current Operating Income ‐15% ex DIA

Rebuilding momentum in 2012 to deliver long term sustainable profitable growth

62

APPENDICES

63

Restatement of HY 2010 Current Operating Income

(98)

989

20

Reported H1 2010 Current

Op.Income

H1 2010Brazil

restatem.

Thailandrestatem.

Hard discount restatem.

Restated H1 2010 Current

Op.Income

1,096

(28)

(€m)

64

Summary income statement

€m H1 2011 H1 2010 Change

Sales excl. VAT 39,607 38,710 2.3%

Loyalty impact (451) (377) 19.5%

Sales excl. VAT without fidelity impact 39,156 38,333 2.1%

Other income 1,100 1,020

Cost of goods sold (31,763) (30,925)

Gross margin from current operations 8,494 8,428 0.8%

S&GA (6,869) (6,605)

Current Operating Income before D&A and provis. 1,625 1,823 (10.9)%

Current Operating Income 772 989 (22.0)%

Current Operating Income as a % of sales excl.VAT 1.9% 2.6%

Non‐recurring income (expenses) (884) (353)

Operating income (112) 636

Financial expense (342) (349)

Income Tax (490) (238)

Net income from recurring operations – Group share (927) 63

Impact of discontinued operations– Group share 679 84

Net income – Group share (249) 97

65

Key operating ratios

€m H1 2011 H1 2010 Change

Sales excl. VAT 39,607 38,710 2.3%

Other income 1,100 1,020 7.9%

Gross margin from current operations as a % of sales

21.4% 21.8%

SG&A as a % of sales (17.3%) (17.1%)

D&A / provisions as a % of sales (2.2%) (2.2%)

Current Operating Incomeas a % of sales

1.9% 2.6%

Operating Income as a % of sales (0.3)% 1.6%

Actual tax rate (108.0)% 82.9%

Current Operating Income before D&A andprovisions as a % of sales

4.1% 4.7%

66

Summary cash flow statement

€m 30 June 2010 (12 months)

Net debt, beginning of period (11,424)

Gross cash flow from operating activities 3,405

Change in working capital (272)

Others and Impact of discontinued operations 57

Cash flow from operating activities 3,190

Capital expenditures (1,935)(148)

Free cash flow 1,108

Financial investments (178)Disposals 222

297

Cash flow after investing activities 1,450

Dividends (117)Treasury shares (778)

(98)

Net debt, end of period (10,654)

313

Consumer credit companies

Others and Impact of discontinued operations

Others and Impact of discontinued operations

Others and Impact of discontinued operations

67

Current Operating Incomeper region

H1 2010 % changeH1 2011€m

FranceAC margin

3021.8%

5033.0%

(40.0)%

EuropeAC margin

1421.2%

2131.8%

(33.3)%

Latin AmericaAC margin

1932.6%

1522.3%

27.4%

AsiaAC margin

1353.6%

1223.5%

10.8%

TotalAC margin

7721.9%

9892.6%

(22.0)%

68

Growth in sales, EBITDA, and Current Operating Income

% growth – H1 2011 vs. H1 2010 Sales EBITDA Current Operating Income

France 1.6% (21.2)% (40.0)%

Europe excl. France (3.9)% (18.5)% (33.3)%

Latin America 12.9% 17.0% 27.4%

Asia 7.7% 7.3% 10.8%

Total 2.3% (10.9)% (22.0)%

69

EPS calculation

H1 2010 EPS H1 2011 EPS

EPS before discontinued activities

EPS from discontinued activities

EPS including discontinued activities

EPS is based on the net result before discontinued activities (group share)

To calculate EPS, we have used the weighted average number of shares: 684,200,616 in H1 2010 and 659,181,759 in H1 2011

0.02

0.12

0.14

(1.41)

1.03

(0.38)

€

70

Consolidated store network June 2011

CONVENIENCE CASH & CARRY TOTAL

205 573 6 784166 108 8 28246 41 8739 227 224 49058 215 166 12 45184 186 27027 212 23923 35 58

443 1,024 398 12 1,877

72 109 227187 49 8 24473 77332 158 58 548

185 18560 3 6367 14 8124 242 2

1338 17 0 356

1,318 1,772 456 19 3,565

FRANCESpain

BelgiumGreece + CyprusItalyPolandTurkeyRomania

EUROPE

ArgentinaBrazilColombiaLATIN AMERICA

ChinaTaiwanIndonesia

MalaysiaSingapore

ASIA

TOTAL

HYPER SUPER

46

India 1

1

4

71

Stores under Group banners (incl. franchisees and partners) June 2011

15

HYPER SUPER CONVENIENCE CASH & CARRY TOTAL

FRANCE 232 974 3,244 137 4,587Spain 172 113 42 327Belgium 46 439 213 698Greece + Cyprus 39 255 572 866Italy 61 433 812 13 1,319Poland 84 186 97 367

Turkey 27 212 229Romania 23 35 58Others 61 127 68 256

EUROPE 513 1,800 1,804 4,132

Argentina 72 109 227Brazil 187 49 8 244Colombia 73 77LATIN AMERICA 332 158 58 548

China 185 185Taiwan 60 3 63Indonesia 67 14 91

Malaysia 24 32Singapore 2 2

ASIA 338 17 8 364

TOTAL 1,415 2,949 5,114 153 9,631

46

8

India 11

1

2

4

72