carsten klapproth and alex gonzalez,...

TRANSCRIPT

14-15 September 2016

Lisbon, Portugal

#DeloitteSharedServices

Deloitte Shared Services, GBS & BPO Conference

Breakout 5: KWS - Seeding the future

Carsten Klapproth and Alex Gonzalez, KWS

Deloitte Annual Shared Services Conference 2016

Seeding the FutureThe Service Center Structure in the KWS Group

Carsten Klapproth, Alex Gonzalez

Lisbon, September 2016

Source: DBV

48%

usable harvest

Source: FAO

42% pre-

harvest losses

10% post-

harvest losses

R&D intensity of approx. 17% of consolidated net sales

1% to 2% progress in yields p.a. and

development of tolerances and resistances

Per capita cropland

(in ha)

20001950 2050

0.50.3

0.2

Harvest losses

(worldwide)

Climate change°C

Plant breeding & seed businessFundamentals

Global importance of agricultural crops

Wheat

Corn

Barley

Sorghum

Rapeseed

Sunflower

Potato

Rye

Sugar-

beet

Catch

cropsSource: faostat.fao.org, January 2016 *raw sugar value, source: zuckerverbaende.de, January 2016

2014 Acreage in mn ha

2014 World production in mn tonnes

not part of the KWS product portfolio

729

1,018

741

308

144

67 71140

41

385

15 40

222

183

163

118

5044

3627 25

195 4

0.3

0.6

0.6

0.7

0.7

1.0

0.9

1.3

1.3

2.6

6.1

8.1

TOP 6 Global agricultural seed companiesSales of agricultural crops

Global sales in € bn

1.19 USD/EUR

1 FY 2014/2015 (1.9. to 31.8.; 1.16 USD/EUR); „Seeds & Genomics“ w/o

vegetables. 2 FY 2015 (1.1. to 31.12.; 1.11 USD/EUR); „Agricultural Sciences-Seeds“. 3 FY 2015 (1.1. to 31.12.; 1.11 USD/EUR); „Seeds“.4 FY 2014/2015 (1.7. to 30.6.); Sales incl. 50:50 JV.5 FY 2015 (1.1. to 31.12.; 1.11 USD/EUR); „Agriculture-Seeds“.6 FY 2014/2015 (1.7. to 30.6.); „Field Seeds“-Sales incl. 50:50 JV.

Monsanto1

DuPont/Pioneer2

Syngenta3

Dow5

Vilmorin6

4

DuPont/Pioneer

Syngenta

Monsanto

DLF Trifolium

Sales* in Europe in € bn

* Estimated sales for calendar year 2014,;1.19 USD/EUR.* Source: Phillips McDougall Consultants; own estimates KWS

Vilmorin

0.9

1.3

2.2

1.3

1.0

6.1

8.1

TOP 5 Global Agricultural Seed CompaniesSales of Agricultural Crops

Global sales in € bn

Bayer: FY 2015; “Seeds” w/o vegetables

Monsanto: FY 2014/2015 (1.9. to 31.8.); 1.16 USD/EUR; „Seeds & Genomics“ w/o vegetables.

Dow: FY 2015; 1.11 USD/EUR; “Agricultural Seeds”

DuPont: FY 2015; 1.11 USD/EUR; “Seeds”

Syngenta: FY 2015; 1.11 USD/EUR; “Seeds” w/o vegetables

KWS: FY 2014/2015 (1.7. to 30.6.); incl. 50:50 JV

Vilmorin: FY 2014/2015 (1.7. to 30.6.); incl. 50:50 JV; “Field Seeds”

Sources: Annual Reports, own estimates KWS.

Sales* in Europe in € bn

+

0.5

0.7

0.7

0.3

0.2

1.0

1.3+

KWS Track Record according to segment reporting*

Net sales development* in € mn

* Including 50:50-Joint Ventures

0

200

400

600

800

1,000

1,200

1,400

03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/1503/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Fit 4 Growth

KWS currently within a process of dynamic growth facing three typical challenges

What happens in a growing company?

Currently these three effects overlay each other at KWS

What is the typical reaction?

1

Due to the growth of the company the number of legal

entities increases

The complexity to steer these legal entities centrally

from HQ increases

An intermediate level, the regional headquarter, is installed

2

Along the growing complexity the heterogeneity

increases (acquisitions etc.)

The need for corporate guidance and standardization

increases

Corporate governance is extended (compliance, procurement

rules, IT standards etc.)

3

Due to the growth regional transactional services reach

a critical mass

Increased corporate standards (see 2) require more

process standardization

Regional shared service centers for transactional services are

set up

Company Board

of a Subsidiary

in Europe

Management of a

Subsidiary

One or several Country Managers are appointed as Managing Directors

Country

Manager

Cereals

Station

Manager

Country

Manager

Sugarbeet

Country

Manager

Corn

Division

Cereals

Research &

Development

Division

Sugarbeet

Division

Corn

Chairman

(Head of the

Service Company)

KWS EXECUTIVE BOARD

Global

Business

Services

Regional

Director

Sugarbeet

Regional

Director

Cereals

Station Manager

or Representative

R&D

Regional

Director

Corn

• This is the creation of the

regional hubs with

administration “managers”.

• Service Center Manager is

Chairman of the Company

Board as neutral party.

• Tasks of the Company Boards

are the steering and

monitoring of the management

as well as the cooperation with

the Service Center.

• KWS subsidiaries fully focused

on production, sales of seeds

and breeding of varieties.

• Country managers are

operational only.

• All administration duties were

carved out to the Service

Centers.

Organizational structure

GSC Scope

KWS

Divisions

R&D

Tasks:

• Breeding

• Production

• Seed sales

Tasks:

• HR

• Finance

• IT

• Controlling

• Legal Services

• Procurement

Service Centers

Service

Request

Services

The KWS Global Services scope

includes traditional activities (i.e.

Accounts Payable, Fixed Assets,

Payroll, T&E) as well as complex

/ non-traditional activities such as

Controlling and Legal.

Seeding the Future: Service Center Diagnostic

In 2015, KWS GSC worked with the CEB to provide an evaluation of our current maturity level. While our

scope is that of a “Progressive” SSO, we are still lacking in crucial areas such as GPOs and organizational

capacity.

Stages:

• Early

• Maturing

• Mature

• Very Mature

• Progressive

Service Center Regional Locations

Sao Paulo

Minneapolis

Barcelona

Einbeck

Vienna

Lessons Learned: People

Mandate to use existing staff from BU

No one left in the Business Units

Missing definition of roles and responsibilities

No top management support after go live

No stakeholder management approach

Lessons Learned: Processes

GSC concept designed from:

A consultant with no intensive SSO expertise

Only with the Executive Board

No involvement of organization

No additional budget for redesigning organization after kick-off:

“Political” decisions:

Lack of change management after go live

Centralized versus decentralized:

Lessons Learned: Technology

Lack of decision making power on systems to support service center processes

Lack of global system strategy:

Very hard to standardize even within regions

Existing systems were different (SAP)

No state-of-the-art technology (OCR scanning, electronic invoices, travel)

Seeding the Future: Stakeholder Feedback

Three drivers for change

Consistency across services

Cost and quality transparency

Closer to the business

The “3 Cs” leading to a shift in the GSC…

Core Changes:

GBC creation

Harmonized processes

CoEs for certain functions

Competency model

Governance structure

Global process owners

Seeding the Future: GBS Roadmap

Strategy 1Significantly improve the quality and efficiency of

services provided to BUs by upgrading expertise

in regional hubs to offer value-added services in

BU priority areas

Strategy 2Significantly improve the quality and efficiency of

services provided to BUs by bundling, outsourcing

and extending process automation of transactional

processes

2016

2017

2018

2019

2020

Upgrade staffing talent

Implement value-added services Design “fix and shift” model (To Be)

Determine KPIs on agreed upon activities

Re-assess activities and KPIs

Implement new value-added activities

Complete location business case / selection

Transfer processes into GBC / identify KPIs

Transfer processes into GBC / identify KPIs

Continuous improvements

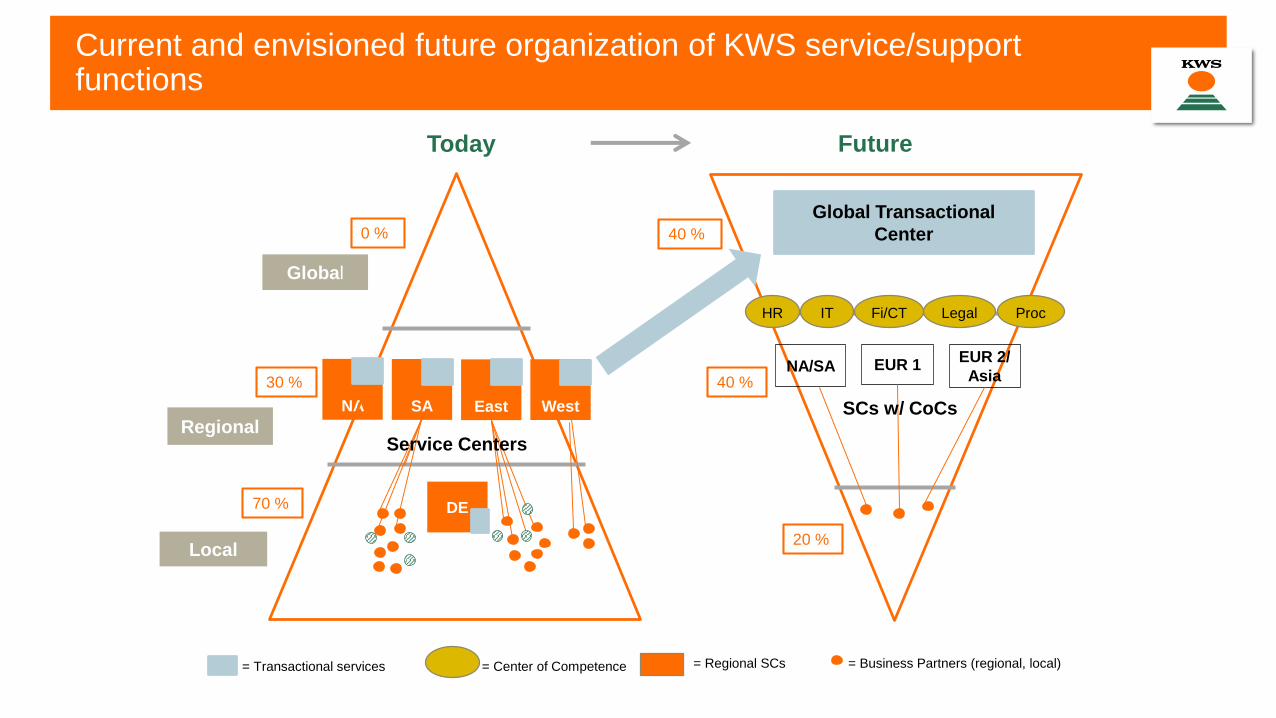

Current and envisioned future organization of KWS service/support functions

EUR 1

NA

Today

SA East West

DE

Global

Regional

Local

Future

0 %

30 %

70 %

Global Transactional

Center

40 %

40 %

20 %

= Transactional services

NA/SAEUR 2/

Asia

SCs w/ CoCs

Fi/CTHR IT Legal

= Center of Competence = Regional SCs = Business Partners (regional, local)

Proc

Service Centers

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally

separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte MCS Limited is a subsidiary of Deloitte LLP, the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular

circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte MCS Limited

would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte MCS Limited accepts no duty of care or liability for

any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2016 Deloitte MCS Limited. All rights reserved.

Registered office: Hill House, 1 Little New Street, London EC4A 3TR, United Kingdom. Registered in England No 3311052.