case no. 18-0018 - petitioner's brief - murray energy

TRANSCRIPT

FILE COpy DO NOT REMOVE

IN THE SUPREME COURT OF APPEALS OF WEST VIRGINIA FROM FILE

No. 18-0018 Marshall County Case No. 16-P-16

MURRAY ENERGY CORPORATION and CONSOLIDATION COAL COMPANY,

Petitioners below, Petitioners,

v.

DALE W. STEAGER, WEST VIRGINIA STATE TAX COMMISSIONER; THE COUNTY COMMISSION OF MARSHALL COUNTY, and

CHRISTOPHER J. KESSLER, ASSESSOR OF MARSHALL COUNTY,

Respondents below, Respondents.

APPEAL FROM THE FINAL ORDER OF THE CIRCUIT COURT OF MARSHALL COUNTY

PETITIONERS' BRIEF

Mark Gaydos, Esq. W. Va. State Bar # 4252 Buddy Turner, Esq. (Counsel of Record) W. Va. State Bar No. 9725 [email protected]

McNeer, Highland, McMunn, and Varner, L.C. 107 W. Court Street P.O. Box 585 Kingwood, WV 26537 Phone: (304) 329-0773 Fax: (304) 329-0595

TABLE OF CONTENTS

ASSIGNMENTS OF ERROR ......................................................................................................... 1

STATEMENT OF THE CASE ........................................................................................................ 1

SUMMARY OF ARGUMENT ....................................................................................................... 5

STATEMENT REGARDING ORAL ARGUMENT AND DECISION ........................................ 7

ARGUMENT ................................................................................................................................... 7

A. Standard of Review .................................................................................................. 7

B. The Circuit Court erred in finding that the Petitioner's Assessments were based upon the real property's true and actual value as required by West Virginia Code section 11-6K-1(a) and 11-3-1(a) ..................................................... 8

C. The Circuit Court erred in finding that the Assessments were not clearly wTong in light of the evidence presented ............................................................... 13

D. The Circuit Court erred in finding that the Assessments did not violate the Equal and Uniform Clause contained in Article X, Section 1 of the West Virginia Constitution ............................................................................................. 17

E. The Circuit Court erred in finding that the Assessments did not violate the Equal Protection Clauses of the United States and West Virginia Constitutions .......................................................................................................... 21

CONCLUSION .............................................................................................................................. 27

11

T ABLE OF AUTHORITIES

CASES

Allegheny Pittsburgh Coal Co. v. Cty. Comm 'n of Webster County, 488 U.S. 336 (1989) ............................................................................................... 10,22-26

Appalachian Power Co. v. State Tax Dep't of West Virginia, 195 W.Va. 573,466 S.E.2d 424 (1995) ............................................................................... 8

Arkansas Public Service Commission v. Pulaski County Board of Education, 582 S.W.2d 942 (Ark. 1979) ........................................................................................ 11-12

Cumberland Coal Co. v. Board of Revision, 284 U.S. 23 (1931) ....................................................................................................... 23-25

Greene v. Louisville & Interurban R. Co., 244 U.S. 499 (1917) ........................................................................................................... 19

Hillsborough v. Cromwell, 326 U.S. 620 (1946) .......................................................................................................... 22

In re 1975 Tax Assessments Against Oneida Coal Co., 178 W. Va. 485, 360 S.E.2d 560 (1987), rev'd sub nom. Allegheny Pittsburgh Coal Co. v. Cty. Comm'n of Webster Cty., W Va., 488 U.S. 336,109 S. Ct. 633,102 L. Ed. 2d 688 (1989) ................................................... 10

In re Assessment of Kanawha Valley Bank, 144 W. Va. 346,109 S.E.2d 649 (1959) ............................................................................ 18

In re Petition of Maple Meadow Mining Co. for Relief fi'om Real Prop. Assessmentfor the Tax Year 1992, 191 W.Va. 519,446 S.E.2d 912 (1994) ......................................................................... 8, 15

In re Tax Assessment Against Am. Bituminous Power Partners, L.P., 208 W.Va. 250, 539 S.E.2d 757 (2000) ............................................................................... 8

In re Tax Assessments Against Pocahontas Land Co., 172 W. Va. 53,303 S.E.2d 691 (1983) .............................................................................. 16

In re Tax Assessment of Foster Found. 's Woodlands Ret. Cmty., 223 W.Va. 14,672 S.E.2d 150 (2008) .................................................................... 7, 10, 15

Israel v. West Virginia Secondary Schools Activities Committee, 182 W. Va. 454, 388 S.E.2d 480 (1989) ............................................................................ 21

111

Killen v. Logan Cty. Comm 'n., 170 W. Va. 602, 295 S.E.2d 689 (1982), overruled on other grounds by In re Tax Assessment of Foster Found. IS Woodlands Ret. Cmty., 223 W. Va. 14,672 S.E.2d 150 (2008) ..................................................................... passim

Louis K. Liggett Co. v. Lee, 288 U.S. 517 (1933) ........................................................................................................... 24

Matter of us. Steel Corp., 165 W. Va. 373, 268 S.E.2d 128 (1980) ...................................................................... 18-19

Mountain Am., LLC v. Huffman, 224 W. Va. 669,687 S.E.2d 785 (2009) ........................................................................... .16

Robertson v. Goldman, 179 W. Va. 453, 369 S.E.2d 888 (1988) ............................................................................ 21

State ex rei. Rose v. Fewell, 170 W. Va. 447, 294 S.E.2d 434 (1982) ............................................................................ 10

Sunday Lake Iron Co. v. Wakefield Twp., 247 U.S. 350 (1918) ........................................................................................................... 22

Walker v. West Virginia Ethics Comm'n, 201 W.Va. 108,492 S.E.2d 167 (1997) ............................................................................... 7

White River Lumber Co. v. State, 2 S.W.2d 25 (Ark. 1928) .................................................................................................... 19

STATUTES

U.S. Const., amend. XIV, § 1 ........................................................................................................ 21

W . Va. Code § 11-1 C-1 ................................................................................................................... 9

W. Va. Code § 11-3-1 .................................................................................................... 9, 14, 17,25

W. Va. Code § 11-3-1(a) ...................................................................................................... 9, 10, 12

W. Va. Code § 11-3-1(£)(1) ............................................................................................................. 9

W. Va. Code § 11-3-24 .................................................................................................................... 2

W. Va. Code § 11-3-25(c) ................................................................................................................ 4

IV

W. Va. Code § 11-6K-l ......................................................................................................... passim

W. Va. Code § 11-6K-l(a) ............................................................................................................. 10

W. Va. Const., art. III, § 10 ...................................................................................................... 21, 26

W. Va. Const., art. X, § 1 ....................................................................................................... passim

W. Va. Const., art. X, § 1 b ..................................................................................................... passim

RULES

110 W. Va. C.S.R. 11-3.59 ............................................................................................................... 3

110 W. Va. C.S.R. 11-4.1.6.4 ........................................................................................................... 2

West Virginia Rule of Appellate Procedure 20 ............................................................................... 7

OTHER AUTHORITIES

R. Blakey, Report on Taxation in West Virginia 107 (1930) ................................................................ 6

William C. Peper, Proposition 13 Under an Updated Equal Protection Analysis: Unlucky at Last? 42 Wash. U. J. Urb. & Contemp. L. 433 (1992) ................................................................ 22

v

ASSIGNMENTS OF ERROR

I. The Circuit Court erred in finding that the Petitioner's Assessments were based upon the real property's true and actual value as required by West Virginia Code section 11-6K-1(a) and 11-3-1(a).

II. The Circuit Court erred in finding that the Assessments were not clearly wrong in light of the evidence presented.

III. The Circuit Court erred in finding that the Assessments did not violate the Equal and Uniform Clause contained in Article X, Section 1 of the West Virginia Constitution.

IV. The Circuit Court erred in finding that the Assessments did not violate the Equal Protection Clauses of the United States and West Virginia Constitutions.

ST ATEMENT OF THE CASE

Petitioners ask this Court to reverse the Circuit Court of Marshall County's ("Circuit

Court") December 7, 2017 "Final Order Dismissing Petition for Appeal and Affirming the Board

of Equalization and Review" (A.R. 816-41 ).1 The Circuit Court ruled therein that that the

methodology used by the West Virginia State Tax Department to value Petitioner's coal was

constitutional and affirmed the valuation by the Marshall County Board of Equalization and

Review. The Petitioners request this Honorable Court to rule that the West Virginia State Tax

Department's methodology for the valuation of coal is unconstitutional, and to assess Petitioners'

coal properties according to their true and actual value.

The Petitioners, Consolidation Coal Company and Murray Energy Corporation,

(hereinafter, collectively, "Petitioner"), are aggrieved by the assessment of certain real property

situated in Marshall County, West Virginia for tax year 2016.2 Petitioner Consolidation Coal

Company ("CCC") is a wholly owned subsidiary of Murray Energy Corporation ("MEC"). AR 1

References to the Appendix Record will be noted as (A.R. ~.

The Petitioners have also appealed assessments for the 2017 and 2018 tax years. These appeals are in various stages of review.

at ~ 1. Petitioner is the owner of numerous steam coal properties in Marshall County of which

188 are listed in Paragraph 2 of the Petition. See id. at ~ 2.

On August 27, 2015, the West Virginia State Tax Commissioner filed natural resource

property valuation variables for the 2016 Tax Year. See AR 150. Included within the August 27,

2015 filing by the West Virginia State Tax Commissioner was a State-Wide Steam Coal Price of

$60.35 per ton (hereinafter, "SCPPT"). See id. This is the number used to appraise and assess

coal properties in West Virginia. See 110 W. Va. C.S.R. 11-4.1.6.4. ("In order to convert decimal

royalty rates into specific dollars per ton rates, the Tax Commissioner shall separately conduct a

review of West Virginia coal selling prices, and select specific selling price rates based on prices

best typifying activity in each appraisal year. The selected selling prices per ton when multiplied

by the decimal royalty shall result in the specific dollar per ton royalty.").

The coal market has been declining since at least 2011 and the market value of steam coal

per ton as of July 1,2015 is significantly below the SCPPT set by the West Virginia State Tax

Commissioner. The average market value per ton of Pitt-8 steam coal in West Virginia as of July

1,2015 was $41.08 per ton. See AR 121 (Feb. 18,2016 Testimony ofJohn L. Weiss) (hereinafter

"Weiss Testimony"); see also AR 197.

On January 22, 2016, Petitioner filed a protest with the Marshall County Commission

pursuant to West Virginia Code section 11-3-24. On February 18,2016, Petitioner appeared before

the Marshall County Commission, which was sitting as a Board of Equalization and Review

pursuant to West Virginia Code section 11-3-24. See generally AR 91-408. During this hearing,

the County Commission heard arguments from Petitioner detailing two specific intentional

systemic constitutional deficiencies with the current state valuation model for coal properties. See

generally id.

2

First, for taxation purposes, the State of West Virginia sets forth in Administrative Notice

2016-03 a calculation for the specific gravity of coal which calculation is solved therein as

1,793.97 tons per acre foot. See AR 143-44. The State of West Virginia State Tax Department

then "rounds" this number up to 1800 tons per acre foot. See id.3 This "rounding up" grossly

increases the total number of tons per acre foot of coal and overtaxes Petitioner on over a million

tons of coal in Marshall County alone that, by the West Virginia State Tax Department's own

formula, do not exist.

Second, the SCPPT value selected and used by the West Virginia State Tax Commissioner

and shown in AR 150 (August 27, 105 Letter from State Tax Commissioner to Natalie Tennant)

is not accurate, is grossly overstated, and does not reflect the true value of the coal. The use of

this inaccurate value violates the United States Constitution, the West Virginia Constitution and

West Virginia Code.

At the hearing before the Marshall County Board of Equalization and Review held on

February 18,2016, Petitioner presented expert testimony from John L. Weiss, Vice-President of

John T. Boyd Company, Mining and Geological Consultants, who opined to a reasonable degree

of certainty in his field, that the average price per ton for the Pitt-8 steam coal owned by Petitioners

was $41.08 per ton as of July 1,2015. See AR 121; see also AR 197. Moreover, John L. Weiss

provided graphical representations of historical prices from 2012 through 2014. See AR 198.

These are the years averaged together and relied upon by the West Virginia State Tax

Commissioner in deriving the SCPPT value of $60.35 contained in the State Tax Commissioner's

August 27, 2015 letter to Natalie Tennant. The average price per ton of steam coal from

110 W. Va. C.S.R. 11-3.59 utilizes 1800 tons per acre foot instead of the calculation contained in Administrative Notice 2016-03.

3

commercially available records for this three-year period reveals an average price of $51.50 per

ton. See AR 197.

The County Commission denied Petitioner's protests. See AR 89-90. On or about March

16, 2016, Petitioner filed a Petition for Appeal on Behalf of Consolidation Coal Company

challenging the methodology by which the State Tax Department valued the Petitioner's coal

resources. By Order entered June 21, 2016, the Circuit Court of Marshall County remanded this

action back to the Marshall County Board of Equalization and Review pursuant to West Virginia

Code section 11-3-25(c). AR 428-34.

On August 25,2016, the remand hearing was held before the Marshall County Board of

Equalization and Review. One witness, Jeffrey Kern, was called by the West Virginia State Tax

Department. He testified in pertinent part as follows:

•

•

•

•

•

•

•

•

West Virginia uses a "mass appraisal system." AR 449;

It was the intent to create a mass appraisal system that would be market responsive, that would go with the market as it changed up and down. See AR 450/5-16;

System was designed to take out peaks and valleys. See AR 501:

Coal industry in huge depression right now. See AR 501;

The price of coal is in a valley right now. See AR 501;

The system Mr. Kern helped design is trying to average out the valley we are in right now. See AR 501;

When you average out the valley [low coal prices], the price of coal [used by the WVSTD] is higher than what it [market value of coal prices] actually is. See AR 501;

The data used to calculate the SCPPT of $60.35 is artificially higher than what the market was in 2015 by design. See AR 502;

The SCPPT of $60.35 is artificially higher than what the actual value of the coal was in 2015 by design. See AR 502.

4

As a result of this testimony, it is undisputed that the State of West Virginia is intentionally

overstating the value of the coal owned by the Petitioner and thus overtaxing it.4

On September 15, 2016, the Circuit Court entered an order establishing a briefing schedule.

After the filings of briefs by both the Petitioner and the WVSTD, the Court, on December 7, 2017

entered a "Final Order Dismissing Petition for Appeal and Affirming the Board of Equalization

and Review". A.R. 816-41. It is from this Order that Petitioner seeks relief.

SUMMARY OF ARGUMENT

Petitioner contends that the lower court erred in affirming the valuations placed upon the

Petitioner's coal properties. Inherently, the system is broken. The coal market has been declining

since at least 2011 and the true and accurate value of steam coal per ton is significantly below the

SCPPT set and utilized by the West Virginia State Tax Commissioner to calculate the Petitioner's

taxes. The WVSTD's own witness recognized this anomaly and recognized that it was intentional

and systematic. As a result, the WVSTD is unconstitutionally, knowingly and intentionally

overvaluing coal reserves in Marshall County and the entire State. This continues year after year

with no end.

Petitioners presented clear and convincing evidence that the SCPPT value is clearly wTong

and that the data utilized by the WVSTD to value and assess Petitioner's coal properties in

Marshall County is clearly wrong. In fact, the only testimony from the two experts that presented

testimony on this issue was that the $60.35 per ton figure is intentionally and knowingly "clearly

wTong".

4 See AR 502 (stating, "Q. But, Ijust want to make sure that it's artificially higher than what the actual value of the property was for 2015, by design? A. Yes."); see also AR 507 (stating, "A. ... There's no - - there's no question here that the instant data from 2015 was significantly lower than the statewide average. There's no doubt - - there's no doubt whatsoever. Q. Undisputed? A. Undisputed.").

5

Because the data being utilized in the calculation by the WVSTD is "clearly wrong," the

end result of the calculation is "clearly wrong." The Petitioner's coal is being grossly overvalued

and is being assessed at a greater percent of its' "true and actual value" in contravention of the

West Virginia Constitution, United States Constitution, and West Virginia statutory law.

Erroneous valuations and unequal assessments have been age-old problems 111 West

Virginia. As early as 1930, the Report on Taxation in West Virginia recognized,

The success of the general property tax depends upon the quality of the assessments. If assessments are very unequal the foundation of the entire tax structure is unsound. Inequality of assessments means that those underassessed pay less than their fair share of public expenses and those overassessed pay their full share and, in addition, they have to make up for what the underassessed fail to pay. The greater the inequalities of assessment the greater the inequalities of the taxes and the more grievous the burdens upon those who find it most difficult to meet their obligations.

R. Blakey, Report on Taxation in West Virginia 107 (1930).

Because the SCPPT value proscribed by the WVSTD is erroneous, the subsequent

assessments issued by the WVSTD violate the West Virginia Constitution's equal and uniform

taxation clause which states "taxation shall be equal and uniform throughout the state, and all

property, both real and personal, shall be taxed in proportion to its value to be ascertained as

directed by law." W. Va. Const. art. X, § 1. By knowingly and intentionally overvaluing the price

per ton of coal, the WVSTD fails to meet this constitutional requirement as some owners of coal

are being overtaxed while others are being undertaxed. Similarly, the methodology and value

adopted by the WVSTD does not ensure that the Petitioner's property is assessed at 60 percent of

its value as required by Article X, Section 1 b of the West Virginia Constitution.

Finally, the Equal Protection Clauses of the United States and West Virginia Constitutions

prohibits the SCPPT value utilized by the WVSTD. By utilizing a price per ton for coal that is

artificially higher than what the actual value of the steam coal per ton was for 2015, the WVSTD

6

deliberately and systematically disregards the true and accurate value of coal in West Virginia and

has forced the Petitioner to pay tax at a higher proportion of the coal's true and accurate value than

other property owners.

ST ATEMENT REGARDING ORAL ARGUMENT AND DECISION

Petitioner respectfully requests that oral argument be granted in this case pursuant to Rule

20 of the West Virginia Rules of Appellate Procedure. The issues presented in this case involve

issues of fundamental public importance and raise constitutional questions regarding the validity

of a statute.

ARGUMENT

A. Standard of Review

This is an appeal from a Circuit Court's order reviewing a decision of the Marshall County

Board of Equalization and Review.

When evaluating a circuit court's order reviewing a decision of a Board of Equalization

and Review, this Court applies a multifaceted standard of review:

"This Court reviews the circuit court's final order and ultimate disposition under an abuse of discretion standard. We review challenges to findings of fact under a clearly erroneous standard; conclusions of law are reviewed de novo." Syllabus point 4, Burgess v. Porterfield, 196 W.Va. 178,469 S.E.2d 114 (1996).

Syl. pt. 1, In re Tax Assessment of Foster Found.'s Woodlands Ret. Cmty., 223 W.Va. 14, 672

S.E.2d 150 (2008). Accord Syl. pt. 2, Walker v. West Virginia Ethics Comm'n, 201 W.Va. 108,

492 S.E.2d 167 (1997) ("In review-ing challenges to the findings and conclusions of the circuit

court, we apply a two-prong deferential standard of review. We review the final order and the

ultimate disposition under an abuse of discretion standard, and we review the circuit court's

underlying factual findings under a clearly erroneous standard. Questions of law are subject to a

de novo review.").

7

When assessing the constitutionality of governing statutes of legislative rules, this Court

will similarly employ a de novo standard of review. Syl. pt. 1, Appalachian Power Co. v. State

Tax Dep't of West Virginia, 195 W.Va. 573,466 S.E.2d 424 (1995). Challenges to assessed values

are viewed under a plainly wrong standard. Syl. pt. 4, In re Petition of Maple A1eadmv Mining Co.

for Relieffi·om Real Prop. Assessmentfor the Tax Year 1992,191 W.Va. 519,446 S.E.2d 912

(1994). But see In re Tax Assessment Against Am. Bituminous PO'wer Partners, L.P., 208 W.Va.

250, 255, 539 S.E.2d 757, 762 (2000) ("[J]udicial review of a decision of a board of equalization

and review regarding a challenged tax-assessment valuation is limited to roughly the same scope

permitted under the West Virginia Administrative Procedures Act, W. Va. Code. ch. 29A. In such

circumstances, a circuit court is primarily discharging an appellate function little different from

that undertaken by this Court; consequently, our review of a circuit court's ruling in proceedings

under [W. Va. Code] § 11-3-25 is de novo.") (footnote and citation omitted).

B. The Circuit Court erred in finding that the Petitioner's Assessments were based upon the real property's true and actual value as required by West Virginia Code section 11-6K-l(a) and 11-3-1(a).

This case boils down to the seminal question of whether the Petitioner's real estate was

taxed on its value or not. All Petitioner is seeking is to be taxed on the value of its' real estate.

The Circuit Court recognized that "[t]he seminal issue in every ad valorem property tax case is the

value of property." AR 836. Despite this recognition and the dispositive admissions by the

WVSTD's expert witness, Jeff Kerns, see generally AR 446-523, the Circuit Court affirmed the

erroneous valuations promulgated by the WVSTD. AR 816-41.

Initially, West Virginia constitutional and statutory provisions set forth a detailed system

for the appraisal and assessment of real property for purposes of local taxation. The keystone of

the West Virginia property tax system is contained in Article X, section 1 of the West Virginia

8

Constitution, which provides in pertinent part that "taxation shall be equal and uniform throughout

the state, and all property, both real and personal, shall be taxed in proportion to its value to be

ascertained as directed by law." W. Va. Const. art. X, § 1.

In addition to dictating that property must be assessed according to its "value", the West

Virginia legislature set a specific date for determining this value. West Virginia Code section

11-3-1(a) provides,

All property, except public service businesses assessed pursuant to article six of this chapter, shall be assessed annually as of July 1 at sixty percent of its true and actual value; that is to say, at the price for which the property would sell if voluntarily offered for sale by the owner thereof, upon the terms as the property, the value of which is sought to be ascertained, is usually sold, and not the price which might be realized if the property were sold at a forced sale.

W. Va. Code § 11-3-1(a). See also W. Va. Code § 11-3-1(£)(1) ("Assessment date" means July 1

of the year preceding the tax year.).5 Finally, West Virginia Code section 11-1 C-l implements

West Virginia Constitution Article X, Section 1 's requirement of equal and uniform taxation

stating:

The Legislature hereby finds and declares that all property in this state should be fairly and equitably valued wherever it is situated so that all citizens will be treated fairly and no individual species or class of property will be overvalued or undervalued in relation to all other similar property within each county and throughout the state.

ld. at § 11-1 C-l. Thus, as a result of these provisions, taxpayers know that their property should

not be over or under valued and should be assessed according to its worth in money, or value, as

of July 1 of the preceding tax year. See W. Va. Const., art. X, § 1; id. at § Ib; W. Va. Code § 11-

3-1; id. at § ll-IC-l; id. at § 11-6K-1.

Notably, although West Virginia Code Section 11-6K-I proscribes that "natural resources property shall be assessed annually as of the assessment date at sixty percent of its true and actual value," West Virginia Code Section 11-6K-I et seq. does not set forth a specific assessment date or a date other than July 1 of the preceding tax year.

9

The question presented in this appeal is twofold. First, did the SCPPT value variable

proscribed by the WVSTD accurately reflect the "true and actual value" of Petitioner's properties;

and, second, does the methodology employed by the WVSTD in determining the "true and actual

value" of the coal owned by the Petitioner pass constitutional evaluation.

Much of the briefing before the Circuit Court was devoted to what "true and actual value"

IS. Compare AR 676-99 'with AR 703-25. The Circuit Court recognized that both West Virginia

Code section 11-3-1(a) and section 11-6K-1 require that property be assessed at its true and actual

value. AR 824. Despite this acknowledgment and West Virginia law proscribing "value" as

market value,6 the Circuit Court ignored Jeffrey Kern's testimony that Petitioner's property was

not being assessed on its value and instead implicitly found that "value" for purposes of assessing

coal properties was a three-year rolling average from the years 2012,2013, and 2014, AR 838, of

a "survey of numerous sources including confidential data .... ". AR 832.

In juxtaposition to the WVSTD's contrived and confidential methodology to determine the

value of a ton of coal, West Virginia Code and case law on the term "value" is clear. This Court

has examined this issue before and, fortunately, exhaustively examined what "value" means.

Value means exactly what common sense dictates - "'worth of money' of a piece of property-its

market value." In re 1975 Tax Assessments Against Oneida Coal Co., 178 W. Va. 485, 487-88,

360 S.E.2d 560, 562-63 (1987). See also Killen v. Logan Cty. Comm'n, 170 W. Va. 602, 611, 295

See In re 1975 TeL. Assessments Against Oneida Coal Co., 178 W. Va. 485, 487-88, 360 S.E.2d 560, 562-63 (1987) ("[t]he tenn 'value,' as used in article 10, section I of the West Virginia Constitution, means the 'worth of money' of a piece of property-its market value."), rev'd sub nom. Allegheny Pittsburgh Coal Co. v. Cly. Comm'n of Webster Cly., W. Va., 488 U.S. 336,109 S. Ct. 633,102 L. Ed. 2d 688 (1989); see also Syl. pt. 3, in part, Killen v. Logan Cly. C0111111'n, 170 W. Va. 602, 295 S.E.2d 689 (1982), overruled on other grounds by In re TeL. Assessment of Foster Found.'s Woodlands Ret. CJnly., 223 W. Va. 14,672 S.E.2d 150 (2008); State ex reI. Rose v. Fewell, 170 W. Va. 447, 449, 294 S.E.2d 434, 436 (1982); W. Va. Code § 11-3-1(a); W. Va. Code § 11-6K-I(a).

10

S.E.2d 689, 698 (1982), overruled on other grounds by In re Tax Assessment 0/ Foster Found.'s

Woodlands Ret. Onty., 223 W. Va. 14,672 S.E.2d 150 (2008).

In Killen, the West Virginia Supreme Court of Appeals wrote:

We have consulted numerous dictionaries with regard to the meaning of "value." The result is unanimous. From the time of Dr. Samuel Johnson and his first English language dictionary, value has meant the property's "worth" in terms of what sale of the property would bring on an open market.

170 W. Va. at 611,295 S.E.2d at 698. The Killen Court examined early Virginia and West Virginia

statutes that defined "value" as market value and cited an 1866 West Virginia statute directing

property to be assessed at "the fair cash value thereof in current money." 170 W. Va. at 612, 295

S.E.2d at 699 (emphasis added).

Early case law from this Court defined taxable value as "fair cash value." 170 W. Va. at

612,295 S.E.2d at 699 (citing State v. LOvll, 46 W. Va. 451, 458,33 S.E. 271, 274 (1899)). Case

law from other jurisdictions supported the logical conclusion that value meant market value. 170

W. Va. at 612, 295 S.E.2d at 700 (citing Arkansas Public Service Commission v. Pulaski County

Board o/Equalization, 266 Ark. 64, 582 S.W.2d 942 (1979)).

The inherent and undeniable problem with the SCPPT value and resultant methodology

adopted by the WVSTD is that it fails to appropriately assess coal property on its "value" as

required by the West Virginia Constitution and West Virginia Code. The system designed by the

WVSTD attributes a historical value on coal properties by design. Jeffrey Kern testified, and the

Circuit Court adopted, a variable used to value Petitioner's coal properties that relied upon stale

and, to an extent, confidential, data. AR 502; id. at 832.

Arkansas addressed a similar challenge in Arkansas Public Service Commission v. Pulaski

County Board 0/ Education, 582 S.W.2d 942 (Ark. 1979). In that case, the legislative act required

the county assessors to utilize a manual at that "froze" residential values as of 1956 and timber and

11

farm values as of 1961. Id. at 944. Examining similar language in the Arkansas Constitution that

required property to be taxed according to it "value", the Arkansas Supreme Court quickly rejected

the idea of using historical values to value real estate for taxation purposes writing,

But the larger question relates to the meaning of the word "value," Article 16, s 5, requiring that "(a)ll property subject to taxation shall be taxed according to its value." An illustration which is perhaps overly simple serves to drive home the meaning of the word "value." Ifan individual displays an article, be it an article of jewelry, an automobile, or even if a house is being sold, and is asked the question, "What is its value?", the answer, of course, is the value of that property today not what it was worth in 1956 or 1961 or any other year. The constitutional requirement, it would appear, undoubtedly means "present value," because its value in some other year would almost certainly not be the same as the current value, and accordingly, if some other basis is used, would not be its true value at all. In addition, the failure to use present market value, but instead to use 1956 and 1961 values, likewise violates the provision that the same shall be "equal and uniform throughout the state," for the reason that the value of properties in some counties since those years has greatly increased, while in others there has been an increase, but not so great, and in still others, the increase in value has only been minimal. In other words, the ratio of increase in property values has been far from the same in all 75 counties.

Id. at 945 (emphasis added).

In contrast to the plain meaning of "value" proscribed by our history, our Constitution, and

our Code, the stale value unilaterally prescribed by the WVSTD can never meet Constitutional and

statutory requirements that taxes be levied on a uniform assessment percentage of the "true and

actual value" of property. W. Va. Const. art. X, § 1b; W. Va. Code § 11-3-1(a); W. Va. Code

§ 11-6K-1.

As shown below, in adopting the WVSTD's SCPPT value variable for coal assessments,

the Circuit Court committed error by not ensuring that Petitioner's property was assessed

according to its "value" in violation of the West Virginia Constitution and West Virginia Code.

12

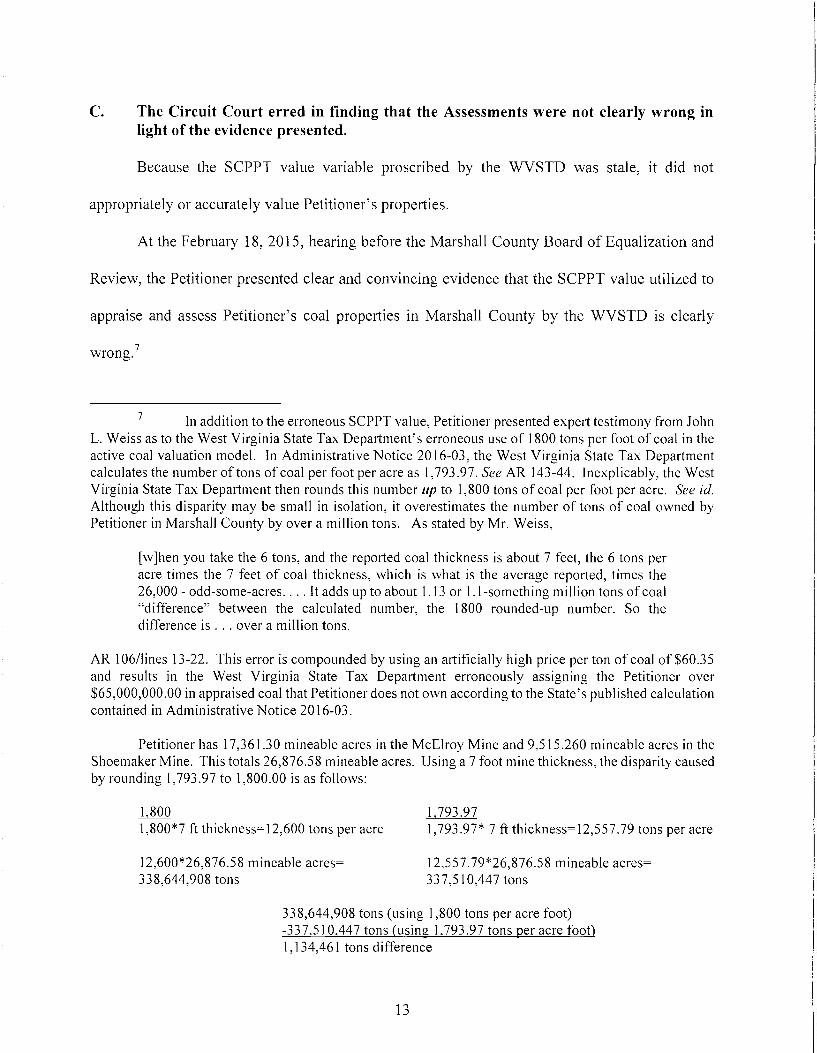

C. The Circuit Court erred in finding that the Assessments were not clearly wrong in light of the evidence presented.

Because the SCPPT value variable proscribed by the WVSTD was stale, it did not

appropriately or accurately value Petitioner's properties.

At the February 18, 2015, hearing before the Marshall County Board of Equalization and

Review, the Petitioner presented clear and convincing evidence that the SCPPT value utilized to

appraise and assess Petitioner's coal properties in Marshall County by the WVSTD is clearly

wrong. 7

7 In addition to the erroneous SCPPT value, Petitioner presented expert testimony from John L. Weiss as to the West Virginia State Tax Department's erroneous use of 1800 tons per foot of coal in the active coal valuation model. In Administrative Notice 2016-03, the West Virginia State Tax Department calculates the number of tons of coal per foot per acre as 1,793.97. See AR 143-44. Inexplicably, the West Virginia State Tax Department then rounds this number lip to 1,800 tons of coal per foot per acre. See id. Although this disparity may be small in isolation, it overestimates the number of tons of coal owned by Petitioner in Marshall County by over a million tons. As stated by Mr. Weiss,

[w]hen you take the 6 tons, and the reported coal thickness is about 7 feet, the 6 tons per acre times the 7 feet of coal thickness, which is what is the average reported, times the 26,000 - odd-some-acres .... It adds up to about 1.13 or 1. I-something million tons of coal "difference" between the calculated number, the 1800 rounded-up number. So the difference is ... over a million tons.

AR 10611ines 13-22. This error is compounded by using an artificially high price per ton of coal of$60.35 and results in the West Virginia State Tax Department erroneously assigning the Petitioner over $65,000,000.00 in appraised coal that Petitioner does not own according to the State's published calculation contained in Administrative Notice 2016-03.

Petitioner has 17,361.30 mineable acres in the McElroy Mine and 9,515.260 mineable acres in the Shoemaker Mine. This totals 26,876.58 mineable acres. Using a 7 foot mine thickness, the disparity caused by rounding 1,793.97 to 1,800.00 is as follows:

1.800 1,800*7 ft thickness=12,600 tons per acre

12,600*26,876.58 mineable acres= 338,644,908 tons

1.793.97 1,793.97* 7 ft thickness=12,557.79 tons per acre

12,557.79*26,876.58 mineable acres= 337,510,447 tons

338,644,908 tons (using 1,800 tons per acre foot) -337.510.447 tons (usin!2. 1.793.97 tons per acre foot) 1,134,461 tons difference

13

As indicated above, the WVSTD arbitrarily and capriciously assigned a clearly wrong

dollar per ton of coal value for tax year 2016. For the tax year at issue, the WVSTD assigned a

value of $60.35 per ton of coal. See AR 150. This number was arrived at by purportedly using a

confidential combination of PSC prices per ton, FERC prices per ton, and a three (3) year average

of coal prices for calendar years 2012, 2013 and 2014. AR 463; id. at 83; id. at 511. There is no

dispute that the assigned value of $60.35 per ton was not excessive and not the true and accurate

value of coal as of July 1, 2015. In fact, the true value of coal as of that date was significantly less

per ton. See AR 512; id. at 507.

Jeffrey Kern, testifying on behalf of the West Virginia State Tax Department, expressly

admitted that the present West Virginia tax system was not designed to tax the "true and actual

value" of property. Compare AR 502 and id. at 511 with W. Va. Const. art. X, § Ib and W. Va.

Code § 11-3-1 and W. Va. Code § 11-6K -1. Instead, the intent was to devise and create a mass

appraisal system to take out peaks and valleys in coal values. See AR 500. To his credit, Mr. Kern

readily admitted that the $60.35 per ton value was not accurate. See AR 502.

In addition to Mr. Kern's testimony, the Petitioner presented clear and convincing evidence

of the market value of coal of the type mined by the Petitioner based on publicly available arm's

length transactions. John L. Weiss presented testimony regarding the price of coal per ton before

the Marshall County Board of Equalization and Review on February 18, 2016. Specifically, he

set forth that the Petitioner mines two types of coal in West Virginia: the 13,000 BTU/4-pound

sulfur dioxide quality mined in the Monongalia, Marion and Harrison County operations and

12,500 BTU coal, 6 pounds of sulfur dioxide quality for the river mines in Ohio and Marshall

county mines. AR 115. Mr. Weiss discussed the different values for these two types of coal. The

12,500 BTU coal from Marshall County is historically lower in value than the higher BTU coal

14

mined in Monongalia, Marion and Harrison Counties. See AR 116. Mr. Weiss further explained

that "[ c ]oal prices have declined considerably in the last five years, since kind of the 2011 period"

due to various factors effecting the market. AR 116. Mr. Weiss opined, relying upon publicly

available data and publications, that the average value per ton of coal for Petitioner's West Virginia

coal properties as of July 1,2015 was $41.08 per ton. AR 121.8

In addition, Mr. Weiss testified as to a multitude of reasons that the $60.35 per ton price

set by the West Virginia State Tax Department was clearly wrong. First, the West Virginia State

Tax Department relies upon a three-year average, in this case 2012, 2013, and 2014, of various

components to arrive at this price. 9 AR 108-09. Second, the components relied upon by the West

Virginia State Tax Department are erroneous in that they include non-comparable coal from

diverse locations other than West Virginia and include value added components such as the cost

of delivery. AR 108.

The SCPPT value of$60.35 is clearly wrong; as such, the appraisements of the Petitioner's

properties are clearly wrong and the Petitioner met their burden. The taxpayer's burden before the

Board of Review is to present "clear and convincing evidence" that the Tax Department's valuation

was wrong. Syl. Pt. 5, in part, In re Tax Assessment of Foster Found. 's Woodlands Ret. Cmty., 223

W. Va. 14,672 S.E.2d 150 (2008). Once a taxpayer has shown this, it becomes "incumbent upon

8 Mr. Weiss also opined that utilizing the publicly available data for Pittsburgh Seam Coal and the State Tax Department's three-year averaging methodology, the Petitioner's West Virginia coal properties have an average value of $51.50 per ton utilizing data from 2012, 2013 and 2014. AR 116.

9 Any argument that the methodology adopted by the West Virginia State Tax Department adjusts over a three-year period of time is without merit. See In re Petition of Maple Meadow Mining Co. for Relieffrom Real Prop. Assessmentfor the Ta.x Year 1992, 191 W. Va. 519, 446 S.E.2d 912 (1994). The system developed by the West Virginia State Tax Department is, by design, always wrong. It either overvalues the coal or undervalues the coal and never reflects the true and accurate value as required by the West Virginia Constitution and West Virginia law.

15

the [Tax Department] to place some evidence in the record to show why its assessment is correct."

In re Tax Assessments Against Pocahontas Land Co., 172 W. Va. 53, 61, 303 S.E.2d 691, 699

(1983) (emphasis added); Mountain Am., LLC v. Huffman, 224 W. Va. 669, 786 n. 23, 687 S.E.2d

785 n. 23 (2009) ("Once a taxpayer makes a showing that tax appraisals are erroneous, the Assessor

is then bound by law to rebut the taxpayer's evidence.").

No evidence was presented by the WVSTD to support the proposition that the SCPPT value

of $60.35 was the true and accurate value of coal in Marshall County or West Virginia as of July

1, 2015. The WVSTD failed to introduce a single sale of coal at this price, failed to introduce any

analysis to show why the $60.35 per ton figure was correct, and failed to show why Petitioner's

market value of coal was wrong. The WVSTD did not even contest the calculations or opinions

ofMr. Weiss. Nor did the WVSTD introduce the specific confidential data relied upon to arrive at

the SCPPT. Instead, the State Tax Department unapologetically argued that coal companies would

not be complaining if they were being undertaxed, see AR 504, and admitted that the price of coal

for the 2016 Tax Year is artificially higher than what the actual value of the coal property was for

2015 - by design. See AR 502.10

Accordingly, the Court should find that the methodology employed and SCPPT value

assigned per ton of coal by the West Virginia State Tax Department are clearly wrong and direct

that the West Virginia State Tax Department and Marshall County Commission, sitting as the

Board of Equalization and Review, reassess Petitioner's coal properties in Marshall County based

upon the true and actual value of Petitioner's property.

10 Mr. Kern also admitted that the $60.35 per ton of coal price used by the West Virginia State Tax Department was higher than the PSC and FERC price per ton reported for 2015. See AR 506.

16

D. The Circuit Court erred in finding that the Assessments did not violate the Equal and Uniform Clause contained in Article X, Section 1 of the West Virginia Constitution.

Article X, section 1 of the \Vest Virginia Constitution provides, in pertinent part, that

"taxation shall be equal and uniform throughout the state, and all property, both real and personal,

shall be taxed in proportion to its value to be ascertained as directed by law." W. Va. Const. art.

X, § 1.

Over thirty years ago, this Court was confronted with a similar argument as was advanced

in this case by the WVSTD before the Circuit Court. In rejecting an argument as to the meaning

of the equal and uniform taxation clause contained in the West Virginia Constitution, this Court

wTote:

We wish to dispose of one final contention made by the taxpayers. They argue that the constitutional phrase "equal and uniform taxation throughout the State" does not mean what it says. They interpret this phrase to require only uniformity of methodology in determining value within a county. As already demonstrated, the existing "uniformity" of methodology has not, and cannot result in uniform taxation, either within a county or within this state. Since article 10, section 1 of the West Virginia Constitution requires equal and uniform taxation in all areas of the state, both the method and the result of taxation are essential to compliance with the constitution.

Killen v. Logan Cty. Comm'n, 170 W. Va. 602, 619, 295 S.E.2d 689,707 (1982) (emphasis added),

overruled on other grounds by In re Tax Assessment of Foster Found.'s Woodlands Ret. Cmty.,

223 W. Va. 14, 672 S.E.2d 150 (2008).

The erroneous assessments in this case result from the insertion of a knowingly erroneous

SCPPT value into the mass appraisal system deliberately adopted by the West Virginia State Tax

Department. As stated by Jeffrey Kern, testifying on behalf of the West Virginia State Tax

Department, the present West Virginia tax system was not designed to tax the "true and actual

value" of property. Compare AR 502 and id. at 511 with W. Va. Const. art. X, § 1b, W. Va. Code

§ 11-3-1, W. Va. Code § 11-6K-1. Instead, it was the intent to devise and create a mass appraisal

17

system to take out peaks and valleys. See AR 500. The West Virginia State Tax Department's

witness admitted that the figure used for the price of coal per ton for the 2016 taxes is artificially

higher than what the actual value of the coal property was for 2015 and that this was done by

design. See AR 502. In fact, this is "[U]ndisputed". AR 507.

West Virginia has long recognized that the taxation of one species of property from which

a tax may be collected shall not be taxed higher than any other species of property of equal value.

See W. Va. Const. art. X, § 1. In In re Assessment of Kanawha Valley Bank, 144 W. Va. 346, 109

S.E.2d 649 (1959), the West Virginia Supreme Court of Appeals examined West Virginia

Constitution Article X, Section 1 in relation to a case where the Kanawha County Assessor fixed

the assessed value of bank stock at one hundred percent of its appraised value and other personal

property in Kanawha County was assessed at a lower rate. In determining that this factual scenario

violated the true and actual value provisions of the West Virginia Constitution, the West Virginia

Supreme Court of Appeals wrote:

Where there is a systematic plan to assess all property of a certain species at a particular per centum of its value, substantially less than actual value, a showing that there were sporadic variations to the plan of assessment will not deprive the owner of property of another species of his right to relief under the provisions of Section 1, Article X, of the Constitution of this State, where the property of the latter was assessed at a substantially higher per centum of actual value than the approximate level of valuation of the other species of property of equal value.

Syl. pt. 6, Kanawha Valley Bank, 144 W. Va. at 347,109 S.E.2d at 651.

This rule applies with "equal if not more force where the variation is among parcels of

property of the same species." Matter of us. Steel COlp., 165 W. Va. 373, 378, 268 S.E.2d 128,

131 (1980). In Matter of U S. Steel Corp., the West Virginia Supreme Court of Appeals found that

assessing a coal mining property at 108% of its true and actual value and assessing other coal

companies' property at below 70% of its true and actual value violated West Virginia

18

Constitutional provisions requiring equal and uniform assessments in the range allowed by the

Code. See u.s. Steel Corp., 165 W. Va. at 378; 268 S.E.2d at 132.11

A successful equal and uniform challenge was brought before the West Virginia Supreme

Court of Appeals in Killen v. Logan Cty. Comm'n, 170 W. Va. 602, 611,295 S.E.2d 689, 698

(1982), overruled on other grounds by In re Tax Assessment of Foster Found.'s Woodlands Ret.

Cmty., 223 W. Va. 14, 672 S.E.2d 150 (2008). The Killen case examined a challenge to

assessments in Logan County. Factually,

[t]he parties stipulated below that the total assessed valuations per class in Logan County met the minimum 50 percent ratio required by W.Va.Code § 18-9A-l1. The percentage was 61.56 for Class I property, 59.16 for Class II property, 71.51 for Class III property and 57.99 for Class IV property. These figures do not represent the ratio that anyone property owner may have, but merely the aggregate total of all taxpayers with property of a certain category. Thus, as the parties stipulated below, some taxpayers' assessed values exceed the aggregate percentage and others fall below that figure. Consequently, some individual taxpayers are paying higher taxes because their property is valued at a higher percentage "of true and actual value," while their neighbors evade their civic duty.

This is true within a class of property and among the four classes in Logan County. For example, there exists almost a 14 percent difference between the aggregate assessment ratios for Class IV property and Class III property. With such disparity, equal and uniform taxation is an impossibility. Such a difference also violates the prohibition against taxation of property of equal value at a higher rate contained in article 10, section 1 of the state constitution. Class III property is currently valued at 71.51 percent of market value while Class IV property is valued at 57.99 percent. Items of property of the same value, but in different classes are being taxed at different levels because of the differences in classification and prevailing ratios.

II Other jurisdictions have examined this issue and found that assessing one taxpayer's property at a higher percentage of its value and other taxpayer's properties at a lower percentage of its value violates similar state constitutional provisions requiring equal and uniform taxation. For example, in White River Lumber Co. v. State, 2 S.W.2d 25 (Ark. 1928) the Arkansas Supreme Court held that to assess a taxpayer's property at 50% of its market value and other property in the same county at only 30% of its value was a violation of the similar provisions of the Arkansas Constitution. Id. at 29. Similarly, the Supreme Court of the United States construed a provision of the Constitution of Kentucky requiring that all property shall be taxed in proportion to its value. See Greene v. Louisville & Interurban R. Co., 244 U.S. 499 (1917). The United States Supreme Court found that assessing the property of a taxpayer at 75% of its actual value while other taxable property in general was assessed systematically and intentionally at not more than 52% of its actual value violated the Kentucky Constitution. Id. at 515-16.

19

While Class IV property owners in Logan County may be happy with this system, Class III property owners are being treated inequitably.

170 W. Va. at 614-15, 295 S.E.2d at 702.

In response to Killen's requirement that all property in the state be assessed at full value,

West Virginia passed the Property Tax Limitation and Homestead Exemption Amendment of 1982

which provides, in pertinent part, that "all property subject to ad valorem taxation shall be assessed

at sixty percent of its value." W. Va. Const. art. X, § lb. Thus, taxes must be equal and uniform,

W. Va. Const. art. X, § 1, and must be assessed at sixty percent of the property's value. W. Va.

Const. art. X, § 1 b. Taxing property at a rate higher than 60 percent of its assessed value is thus

constitutionally prohibited.

In this case, umefuted expert testimony was presented that the average value of coal per

ton as of July 2015 was $41.08. See AR 12; see also AR 197. Utilizing the WVSTD's value of

$60.35 appraises the coal property of Petitioner at 146.9 percent of its true and actual market value

as of July 1,2015. Coal companies selling coal on long term contacts at a price per ton of over

$60.35 are assessed at some percentage less than 100 percent of its actual value. 12 Similarly, coal

companies like Petitioner that are selling coal at less than $60.35 per ton are being assessed at

some percentage over 100 percent of its actual value. Although the WVSTD has adopted a uniform

method, it has failed to achieve an equal and uniform result of taxation as required by West

Virginia Constitution Article X, Section 1.

Accordingly, the Court should find that the methodology employed and SCPPT value

assigned per ton of coal by the West Virginia State Tax Department violates West Virginia

12 The West Virginia State Tax Department did not introduce evidence of a single sale at a price of or above $60.35 in 2015. See generally AR 673. Instead, the West Virginia State Tax Department relied upon historical reports and data from various sources for the years 2012, 2013 and 2014. See 449-64.

20

Constitution Article X, Section 1 and Section 1 b. The West Virginia State Tax Department and

Marshall County Commission, sitting as the Board of Equalization and Review, should be directed

to reassess Petitioner's coal properties in Marshall County based upon its true and actual value.

E. The Circuit Court erred in finding that the Assessments did not violate the Equal Protection Clauses of the United States and West Virginia Constitutions.

The Equal Protection Clause of the Fourteenth Amendment to the United States

Constitution provides "No State shall * * * deny to any person within its jurisdiction the equal

protection of the laws." U.S. Const. amend. XIV, § 1, cl. 4. West Virginia'S equal protection

clause is found in Article III, Section 10 of the West Virginia Constitution. See Israel v. West

Virginia Secondmy Schools Activities Committee, 182 W. Va. 454, 388 S.E.2d 480 (1989).

Moreover, the West Virginia Constitution's equal protection clause "is coextensive or broader"

than its federal counterpart. See Robertson v. Goldman, 179 W. Va. 453,369 S.E.2d 888(1988).13

13 The equal protection analysis contained herein is not the traditional equal protection analysis involving strict scrutiny or rational basis review. The Supreme Court of the United States

has formulated three situations by which a state's property tax can constitutionally run aground against Fourteenth Amendment protections.

First, a state's choice of classifications requires application of a fairly lenient arbitrary and capricious standard. States can and often do choose to divide property types into different classes and apply varying tax rates. The Clause permits resultant inequities where those divisions and burdens attain reasonableness. Typically, the state proffers a rational basis for the classification based on a policy or a difference between classifications. For example, a state may distinguish property held by a corporation from property held by an individual and apply different tax rates. Tax classifications supported by reasonable distinctions rarely fail to meet the generous arbitrary and capricious standard.

Second, the Fourteenth Amendment requires that states avoid intentional and systematic discrimination within a given classification. Ongoing, inequitable taxation imposed discriminately within a classification raises the specter of an equal protection violation. Not all discrepancies in tax treatment evoke equal protection problems. Discrimination reSUlting from occasional errors or mistakes in judgment is constitutionally permissible. Whether a claim survives depends on whether the state has attained some seasonable equality in the treatment of similarly situated taxpayers.

(footnote cant 'd on next page)

21

The Supreme Court of the United States has long held that "the equal protection clause of

the Fourteenth Amendment protects the individual from state action which selects him out for

discriminatory treatment by subjecting him to taxes not imposed on others of the same class."

Hillsborough v. Crom'well, 326 U.S. 620,623 (1946). As such,

The purpose of the equal protection clause of the Fourteenth Amendment is to secure every person within the state's jurisdiction against intentional and arbitrary discrimination, whether occasioned by express terms of a statute or by its improper execution through duly constituted agents. And it must be regarded as settled that intentional systematic undervaluation by state officials of other taxable property in the same class contravenes the constitutional right of one taxed upon the full value of his property.

Sunday Lake Iron Co. v. Wakefield Twp., 247 U.S. 350, 352-53 (1918). Thus, improper execution

of taxation that intentionally and systematically undervalues or overvalues real estate in

comparison to other taxable properties is constitutionally infirm and violates federal and state equal

protection guarantees.

The Supreme Court of the United States examined a variation of "welcome stranger"

taxation in in Allegheny Pittsburgh Coal Co. v. Cty. Comm 'n of Webster County. 488 U.S. 336,

345-46 (1989). In this case, the Webster County tax assessor valued recently sold properties on

the purchase price but failed to make appropriate modifications to the assessments of land that had

not been recently sold. Id. at 338. The Supreme Court overturned the ruling of the West Virginia

Supreme Court of Appeals upholding this practice and found:

Finally, a state's tax scheme must avoid impermissible interference with the right to interstate travel. This Fourteenth Amendment stipulation applies to statutes that discriminate between in-state residents and non-residents.

William C. Peper, Proposition 13 Under an Updated Equal Protection Analysis: Unlucky at Last?, 42 Wash. U. J. Urb. & Contemp. L. 433, 437-39 (1992) (internal footnotes omitted). The WVSTD's methodology of assigning an arbitrary coal value [the SCPPT] far above the real market value of coal to determine the Petitioner's assessments/tax burden results in intentional and systematic discrimination under the second analysis discussed in the law review article quoted above.

22

"[I]ntentional systematic undervaluation by state officials of other taxable property in the same class contravenes the constitutional right of one taxed upon the full value of his property." ... "The equal protection clause ... protects the individual from state action which selects him out for discriminatory treatment by subjecting him to taxes not imposed on others of the same class." .... We have no doubt that petitioners have suffered from such "intentional systematic undervaluation by state officials" of comparable property in Webster County. Viewed in isolation, the assessments for petitioners' property may fully comply with West Virginia law. But the fairness of one's allocable share of the total property tax burden can only be meaningfully evaluated by comparison with the share of others similarly situated relative to their property holdings. The relative undervaluation of comparable property in Webster County over time therefore denies petitioners the equal protection of the law.

Jd. at 345--46 (internal citations omitted).

Specifically, in a coal taxation case, the Supreme Court of the United States found that

deliberately and systematically ignoring the actual value of property violated the equal protection

provisions of the United States Constitution. Cumberland Coal Co. v. Board o/Revision, 284 U.S.

23, 29-30 (1931). Moreover, application of a uniform rate of taxation to the erroneous assigned

values of the property did not save the challenged methodology. See id. In Cumberland Coal, the

assessor for Greene County, Pennsylvania, appraised all coal properties at the same rate per acre

[much like the current West Virginia SCPPT value] and applied a uniform rate of 50 percent to

the appraised value to set the assessed value. See id. at 28. Cumberland Coal Company challenged

the assessments on the basis that coal closer to transportation sources, such as rail or river, was

more valuable than inaccessible coal properties. See id. The Cumberland Coal Court wrote:

In applying this principle, the fact that a uniform percentage of assigned values is used, cannot be regarded as important, if, in assigning the values to which the percentage is applied, a system is deliberately adopted which ignores differences in actual values so that property in the same class as that of the complaining taxpayer is valued at the same figure (according to the unit of valuation, as, for example, an acre) as the property of other owners which has an actual value admittedly higher. Applying the same ratio to the same assigned values, when the actual values differ, creates the same disparity in effect as applying a different ratio to actual values when the latter are the same .... The discrimination is essentially the same, and is equally repugnant to constitutional right, when both assessments are made on the

23

basis of 50 per cent. of assigned values and differences in actual values are deliberately and systematically disregarded.

Id. at 29-30. See also Louis K. Liggett Co. v. Lee, 288 U.S. 517,539-40 (1933) ("where a statute

lays a tax upon property ad valorem at an even and equal rate, discrimination may result from the

fact that the assessing officials systematically and intentionally value some property subject to the

tax at a proportion of its true value different from that fixed with respect to other like property.").

In accordance with these decisions, any system of assessment which subjects one owner to

taxation upon a substantially higher proportion of the full value of his property than other owners,

is unconstitutional. As such, taxing two $20,000.00 pieces of property comparable in every respect

at two different tax rates is unconstitutionally infirm. See, e.g., W. Va. Const. art. X, § 1 (requiring

equal and uniform taxation). See also Allegheny Pittsburgh Coal Co. v. Cty. Comm 'n of Webster

County. 488 U.S. 336, 345-46 (1989). However, this is not the only method by which taxation

systems can violate constitutional provisions for equal protection.

Unconstitutional discriminatory treatment can arise not only from discriminatory rates of

taxation, but in the application of knowingly erroneous values being assigned to the disparate

parcels of real estate. Given t\VO parcels of real estate, the market value of one of which is

$20,000.00 and the other with a market value of $10,000.00, knowingly assigning them both a

value of $15,000.00, and applying a uniform tax rate to each parcel creates two separate classes of

property - those that are overtaxed and those that are undertaxed in violation of constitutional

protections for equal protection.

The erroneous assessments in this case did not result from errors in judgment, the exercise

of discretion, or classification by State or County taxing authorities; instead, it resulted from an

unconstitutional and intentional calculation, deliberately adopted by the West Virginia State Tax

Department. As stated by Jeffrey Kern, testifying on behalf of the West Virginia State Tax

24

Department, the present West Virginia tax system was not designed to tax the "true and actual

value" of property. W. Va. Const. art. X, § 1b, W. Va. Code § 11-3-1, W. Va. Code § 11-6K-1.

By creating a mass appraisal system to level out the peaks and valleys, see AR 500, the West

Virginia State Tax Department, by design, uses a price per ton for coal that is artificially higher

than what the actual value of the steam coal per ton was for 2015. See AR 502. As such, this

system overtaxes all coal properties in excess of sixty percent of their value in violation of the

West Virginia Constitution. See W. Va. Const. art. X, § 1 b. Because West Virginia requires equal

and uniform taxation and some properties [coal properties] are being intentionally and

systematically overtaxed in comparison to other properties that are being assessed and taxed at

sixty percent of their value, the system violates federal and state equal protection clauses.

Moreover, there is little or no substantive difference in this case and the Cumberland Coal

case, supra. In both cases, the taxing authority is prescribing a uniform value [SCPPT value of

$60.35] to coal products with widely varying market values. Compounding this error is the use of

a SCPPT value that is intentionally and knowingly erroneous. In this case, umefuted expert

testimony was presented that the value of coal per ton as of July 2015 was $41.08. See AR 121;

see also id. at 197. Utilizing the West Virginia State Tax Department value of $60.35 overvalues

the coal property of Petitioner by 146.9 percent of its true and actual value as of July 1,2015. Coal

companies selling coal on long term contracts at a price per ton of over $60.35 are assessed as

some percentage less than 100 percent of its actual value. Similarly, coal companies like Petitioner

that are selling coal at less than $60.35 per ton are being assessed at some percentage over 100

percent of its actual value. This intentional and systematic methodology "deliberately and

systematically" disregards "differences in actual values" in contravention to the holdings of

Cumberland Coal Co. v. Ed. of Revision, 284 U.S. 23, 29-30 (1931) and Allegheny Pittsburgh

25

Coal Co. v. Cly. Comm'n of Webster Cly., 488 U.S. 336 (1989) and violates the United States

Constitution and the West Virginia Constitution.

Accordingly, the Court should find that the methodology employed and value assigned per

ton of coal by the West Virginia State Tax Department violates the Equal Protection Clause of the

Fourteenth Amendment to the United States Constitution and Article III, Section 10 of the West

Virginia Constitution and direct that the West Virginia State Tax Department and Marshall County

Commission, sitting as the Board of Equalization and Review, reassess Petitioner's coal properties

in Marshall County based upon the true and actual value of Petitioner's property.

26

CONCLUSION

WHEREFORE, Petitioners, Consolidation Coal Company and Murray Energy

Corporation, respectfully request that this Court find that the SCPPT value proscribed by the West

Virginia State Tax Department is erroneous and give "value" the meaning given by our founding

fathers at the West Virginia Constitutional Convention. Perhaps Delegate Sinsell said it best

during the West Virginia Constitution Convention when he stated,

I understand all property shall be taxed in proportion to its value. That is, if one horse is worth $5, tax it on $5, and if another is worth $125, tax it on $125.

Killen v. Logan Cty. Comm'n, 170 W. Va. 602, 613, 295 S.E.2d 689,700 (1982) (quoting 3

Debates, West Virginia Constitutional Convention, 1861-63 at 71 (remarks of Mr. Sinsell»,

overruled on other grounds by In re Tax Assessment of Foster Found.'s Woodlands Ret. Cmty.,

223 W. Va. 14,672 S.E.2d 150 (2008).

Petitioners further ask that this Court reverse the Circuit Court of Marshall County's

December 7, 2017 "Final Order Dismissing Petition for Appeal and Affirming the Board of

Equalization and Review", find that the methodology utilized by the West Virginia State Tax

Department is unconstitutional and remand this case to the Circuit Court of Marshall County for

further proceedings directing the Marshall County Board of Equalization and Review and the

Assessor to compute Petitioner's taxes based upon the true and accurate value of coal as of July 1,

2015.

27

Respectfully submitted the 5th day of April, 2018.

CONSOLIDATION COAL COMPANY and MURRAY ENERGY CORPORATION,

By Counsel,

W. Va. State Bar # 4252 Buddy Turner, Esq. W. Va. State Bar No. 9725 McNeer, Highland, McMunn, and Varner, L.c. 107 W. Court Street P. O. Box 585 Kingwood, WV 26537 Phone: (304) 329-0773 Fax: (304) 329-0595

28

CERTIFICATE OF SERVICE

This is to certify that on the 5th day of April, 2018, the undersigned counsel served the

foregoing "PETITIONERS' BRIEF' upon counsel of record by depositing a true copy in the

United States Mail, postage prepaid, in an envelope addressed as follows:

u.S. Mail Cassandra L. Means, Esq.

1900 Kanawha Boulevard, East Building 1, Room W-435

Charleston, West Virginia 25305

u.S. Mail Joseph R. Canestraro, APA

Marshall Co. Prosecutor's Office 600 7th Street

Moundsville, WV 26041

Buddy Turner, Esq. W. Va. State Bar No. 9725 McNeer, Highland, McMunn, and Varner, L.c. 107 W. Court Street P. O. Box 585 Kingwood, WV 26537 Phone: (304) 329-0773 Fax: (304) 329-0595

29