case no.2 of 2003 - infraline

TRANSCRIPT

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

1

Bef ore the MAHARASHTRA ELECTRICITY REGULATORY COMMISSION

World Trade Centre, Centre No.1, 13th Floor, Cuffe Parade, Mumbai – 400 005 Email: [email protected]

Website: www.mercindia.com

Case No.2 of 2003

IN THE MATTER OF Determination of Tariff [2003-04] applicable to various categories of consumers of the

Maharashtra State Electricity Board

Shri P.Subrahmanyam, Chairman Shri Jayant Deo, Member. Dr. Pramod Deo, Member

Date of Order: March 10, 2004

O R D E R

The Maharashtra Electricity Regulatory Commission, in exercise of the powers vested in it under Section 29 of the Electricity Regulatory Commissions Act, 1998 and all other powers enabling it in this behalf, and after taking into consideration all the objections, responses of the MSEB, issues raised during the Public Hearings, and all other relevant material, determines the tariff for supply of electricity by the Maharashtra State Electricity Board for retail distribution as under.

BRIEF HISTORY:

The Maharashtra State Electricity Board (MSEB) submitted a Petition for approval of the Annual Revenue Requirement for FY 2003-04 (ARR Petition)on April 7, 2003 under affidavit dated April 3, 2003 to the Maharashtra Electricity Regulatory Commission (Commission) for the revision of its Retail Distribution Tariff with effect from April 1, 2003, keeping in view the requirements of Section 59 of the Electricity (Supply) Act, 1948. The MSEB filed only the ARR Petition in April 2003 as against the Commission's directive to file the ARR and Tariff Petition for FY 2003-04 by December 2002. On receipt of the ARR Petition, the Commission held an admissibility hearing in the presence of S.26 Consumer Representatives on April 24, 2003. Although a specific Tariff Proposal was not submitted by the MSEB, the Commission admitted the Petition to avoid delay in processing of the Petition, with the following conditions:

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

2

(a) The Petition would be taken up for Technical Validation on May 13, 2003, subject to MSEB fulfilling data requirements; Consumer Representatives should submit their requirement of data by May 2, 2003 to MSEB through the Commission, for inclusion and submission by MSEB before May 9, 2003;

(b) MSEB should also prepare and submit a detailed Tariff Proposal taking into account, inter alia, the various directives and guidelines given by the Commission in earlier Orders, including the alternatives regarding T&D loss charges (Circle-wise and State-wide) as minuted in the Record of Proceedings held on October 7, 2002.

On receipt of the additional data and information and Tariff Petition from MSEB on June 30, 2003, the Commission held a Technical Validation Session in the presence of S.26 Consumer Representatives on July 1, 2003. During the Technical Validation Session held on July 1, 2003 at Mumbai, the following persons / officials were present: Sr. No. Name of person/ official

DESIGNATION AND INSTITUTION

MSEB Officials: - 1 Shri Asoke Basak Chairman, MSEB 2 Shri A.B. Shethji Technical Member (T&D), MSEB 3 Shri M.N. Bapat Technical Director (Distribution), MSEB 4 Shri G.P. Gunnapar Chief Engineer (Tariff Regulatory Cell),

MSEB 5 Shri V.L. Sonawane Superintending Engineer (Tariff Regulatory

Cell), MSEB 6 Shri M.R. Ambhore Technical Member (Generation), MSEB 7 Shri C.N. Gudap Chief Engineer (Distribution), MSEB 8 Shri Anil Deshkar Jt. Secretary, MSEB 9 Shri J.K. Shrinivasan Jt. Chief Accounts Officer, MSEB 10 Shri A.V. Deshpande Chief Accounts Officer, MSEB 11 Shri S.P. Vahalkar Dy Chief Accounts Officer, MSEB 12 Shri H.A. Patil Chief Engineer (Commercial), MSEB 13 Shri V.V. Kulkarni Accounts Officer, MSEB 14 Shri B.N. Farkade Chief Engineer (SLDC), Kalwa, MSEB 15 Shri S.S. Kulkarni Executive Engineer (SLDC), Kalwa, MSEB 16 Shri A. Krishna Rao Member (Accounts), MSEB 17 Shri P.V. Kulkarni Technical Director (EHVP), MSEB 18 Shri A.G. Khonde Executive Engineer, MSEB 19 Shri A.B. Chapalge Dy. Chief Engineer, (Generation

Works)MSEB

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

3

Sr. No. Name of person/ official

DESIGNATION AND INSTITUTION

20 Shri S.V. Ramakrishna Director (IT), MSEB 21 Shri B.M. Kumbhar Dy. Director, MSEB 22 Shri V.M. Baswante Executive Engineer, MSEB 23 Shri C.P. Katkuri Director of Accounts, MSEB 24 Shri R.N. Sonar Chief Accounts Officer (BA), MSEB 25 Shri S.J. Ambekar Dy Chief Accounts Officer (BA), MSEB 26 Shri U.S. Mane Addl. Director (IT) , MSEB 27 Shri V.W. Deshpande Jt. Director (IT) , MSEB 28 R.B. Kshirsagar Executive Engineer, MSEB 29 Shri P.H. Aher Executive Engineer, MSEB 30 Shri K.A. Sukumaran Steno, MSEB CONSUMER

REPRESENTATIVES: -

31 Shri R.B. Goenka President, Vidarbha Industries Association 32 Dr. Ashok Pendse Mumbai Grahak Panchayat 33 Dr. S.L. Patil Secretary General, Thane Belapur Industries

Association 34 Shri Shantanu Dixit Member, Energy Group, Prayas CONSULTANTS: -

35 Shri Sameer S. CRISIL 36 Shri B. Shesan CRISIL 37 Shri Palaniappan M. Manager, ICRA 38 Shri Suresh Gehani Manager, ICRA 39 Shri Ajit Pandit Manager, ICRA 40 Shri Anand Desai Manager, ICRA 41 Shri Jain Chirag A.F. Ferguson & Co. OTHER OFFICIALS: -

42 Shri M.S. Dave Assistant General Manager, Tata Power Company Ltd.

43 Shri T.P. Mohan Senior Manager, Tata Power Company Ltd. 44 Shri C.A. Colaco Tata Power Company Ltd. 45 Shri Vivek Kejriwal Manager, Tata Power Company Ltd.

During the Technical Validation session, the Commission and the Consumer Representatives identified several discrepancies and data gaps and directed MSEB to submit a consolidated ARR and Tariff Petition alongwith additional data and clarification. Subsequently, the MSEB, vide letter ref. TRC/TRP 03-04/24623, submitted the Revised ARR and Tariff Revision Petition (Petition) for FY 2003-04 on July 23, 2003 under affidavit dated July 21, 2003 in three volumes.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

4

In line with the Regulations and practice established by the Commission in previous tariff determination exercises, the Public Notice was issued in newspapers for inviting suggestions and objections from interested parties. The Public Notice was published in Asian Age, Economic Times, Financial Express, Maharashtra Times and Times of India in Mumbai; Indian Express, Dainik Samna, Gavkari, Kesari, Lok Mat, Lok Satta, Sakal, Tarun Bharat and Tudhari in all editions of Maharashtra and in leading local newspapers in each of the six Revenue Divisions of the State. The Public Notice appeared in most of the newspapers on August 4, 2003. Copies of the MSEB’s Petition and its summary were made available for inspection/purchase to members of the public throughout the State of Maharashtra in the MSEB's Executive Engineers' offices and on the MSEB’s website (www.msebindia.com). The last date for filing the written objections was fixed as September 3, 2003, which allowed a period of one month to the public to enable them to file their objections. The Public Notice specified that the suggestions/objections, either in English or Marathi, may be filed in the form of affidavits to the Commission along with proof of service on MSEB. It was specifically stated in the Public Notice that if any objector wanted to be heard in person, he would be invited to the Public Hearings. MSEB was given an opportunity to reply to the party's suggestion/objection by September 18, 2003. The concerned party was also allowed to submit a rejoinder to MSEB by October 3, 2003. By the above Public Notice, the Commission also admitted objections filed during the Public Hearing. To facilitate the interested objectors who find it difficult to submit their objections within the above stipulated time, it was also clarified that they were permitted to file their objections upto October 21, 2003 and could also participate in the Public Hearing at Mumbai. This was also announced during the Public Hearings held at various Divisional Headquarters. The Commission also made necessary arrangements to receive the affidavits and objections and to record all the oral submissions on audiotapes and videotapes at the Public Hearings.

The consumers, by a Public Notice, were also informed of the dates of the Public Hearings as follows:

Sl. Revenue Divisions Date of Public Hearing. 1 Amravati October 9, 2003 at 11.00 hrs 2 Nagpur October 10, 2003 at 10.00 hrs 3 Aurangabad October 13, 2003 at 10.00 hrs 4 Nashik October 15, 2003 at 10.00 hrs 5 Pune October 17, 2003 at 10.00 hrs 6 Mumbai October 20 and 21, 2003 at 11.30 hrs

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

5

The Commission received a large number of written objections expressing concern about the proposed upward revision in the Tariff charges, the working of the MSEB and a host of other issues. The Commission received a total of 792 objections, 628 on affidavit and 64 without affidavits. Those objectors who filed their affidavits and also indicated that they would like to be heard in person, were called for the Public Hearing at the respective headquarters of Revenue Divisions in which they were located.

The category-wise and revenue division-wise number of consumers/institutions who submitted their objections to the MSEB’s Tariff Revision for 2003-04 is detailed in the Table below:

Interest Groups Amra-vati

Aurang-abad

Konkan Nagpur Nashik Pune Total

Consumer

1 3 8 3 10 14 39

Consumer Association 1 2 8 1 8 7 27

Consumer Representative

3 1 1 5

Industry

2 3 10 2 7 11 35

Industry Association 3 2 14 2 4 8 33 Railway

2 2

Lift Irrigation Society 1 602 16 19

Political Party

2 3 4 2 11

Trade Union

1 1 2 1 1 6

Panchayat, Nagar Palika, Nagar Parishad, Municipality

1 1 5 7

Others

5 2 1 8

Total

8 13 56 11 643 61 792

The Commission, vide letter dated September 29, 2003, separately requested the Government of Maharashtra to indicate its commitment regarding subsidy with respect to Maharashtra

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

6

State Electricity Board's tariff. The GoM’s response, through its Industries, Energy & Labour Department, vide letter No. RCA, 2003/CR 174/NRG-3, is quoted below:

“Under Section 65 of the Electricity Act, 2003, it is stated that, "If the State Government requires the grant of any subsidy to any consumer or class of consumers in the tariff determined by the State Commission under section 62, the State Government shall notwithstanding any direction which may be given under section 108, pay, in advance and in such manner as may be specified, the amount to compensate the person affected by the grant of subsidy in the manner the State Commission may direct, as a condition for the licence or any other person concerned to implement the subsidy provided for by the State Government."

It is clear from the above that the sequence as intended by the Act is that the Commission first determines the tariff under section 62 after which the State Government would decide about the grant of subsidy.

At the moment, the issue of granting subsidy for the year 2003-04 based on the existing rates is under consideration of Government. Before the issue is decided, it is very difficult for Government to take a view as to the subsidy it would like to give after revision of rates by the Commission. Usually Government would be anxious to know the net tariff payable by the subsidized consumers after accounting for the subsidy and hence would find it difficult to commit subsidy amount without knowing the tariff fixed by the Commission”.

The Commission has ensured that the due process contemplated under the law has been followed at every stage meticulously and an adequate opportunity was given to all the persons concerned to file their say in the matter. The Commission, after taking into consideration all the objections, including the submission of the Government of Maharashtra, responses of the MSEB, issues raised during the public hearings, and all other relevant material, has issued the Operative part of the Order on December 1, 2003. The Commission hereby makes the following Tariff Order. 1. The revised tariffs will be applicable from December 1, 2003, and will continue to be in

force till further revision in tariffs. The net increase in revenue to the MSEB from the revised tariffs is Rs. 186 crore, if the revised tariffs had been made applicable from April 1, 2003, which amounts to an average tariff increase of around 1.5%.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

7

2. The matter of specifying the ‘Terms and Conditions of Supply’ for the MSEB is before the Commission, which is being taken up separately.

3. The Commission had directed the MSEB to comply with its directives given in the earlier Tariff Orders and issued separately from time to time. However, the Commission is very unhappy with the performance of the MSEB in this regard. Despite the Commission’s strong warning that it would be constrained to take serious action if there was slippage in compliance with the directives, the MSEB has not shown its willingness to comply with these directives in the true spirit. The Commission expresses extreme displeasure with the MSEB’s non-compliance of its directives, despite several reminders in this regard. The top management of the MSEB is urged to take urgent steps to comply with these directives expeditiously.

4. The Commission also directs that henceforth, the Commission will conduct quarterly reviews of the MSEB’s compliance with the directives. The MSEB’s senior officers would be expected to attend these compliance review meetings. Further, in case the MSEB desires any clarification on any directive issued by the Commission, the MSEB should request such clarification within a month of the directive being issued, failing which it will be assumed that the MSEB does not require any clarifications, and the MSEB will be required to comply with the directives expeditiously, both in letter and in spirit.

5. Energy accounting by itself has no meaning, unless the MSEB analyses the energy accounting data and holds the concerned officers responsible for the excess losses in that zone/circle. The Commission has noted that there are several instances where the meters installed are not being read on a monthly basis. The Commission reiterates that the MSEB should hold the concerned employees responsible for the T&D losses in the respective circles/zones, and consider departmental proceedings against these employees after following due disciplinary procedure. The monitoring of the circle-level losses should continue and the MSEB should continue to submit the circle-level energy accounting data on a monthly basis, and circles should operate on ‘profit centre’ basis.

6. For projecting the energy requirement, the Commission has considered the T&D loss level of 36.62%, which is the T&D loss level proposed by the MSEB despite the uncertain quality of data in this regard, for want of a better alternative. With the sales during FY 2003-04 projected by the Commission at 39710 MU, the total energy requirement to be met through generation and power purchase is expected to be about 62652 MU. This is in line with the energy handled by the MSEB’s system in the recent past.

7. The net generation from MSEB’s own stations as projected by the Commission is 46470 MU as compared to 45983 MU projected by the MSEB. The Commission has considered

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

8

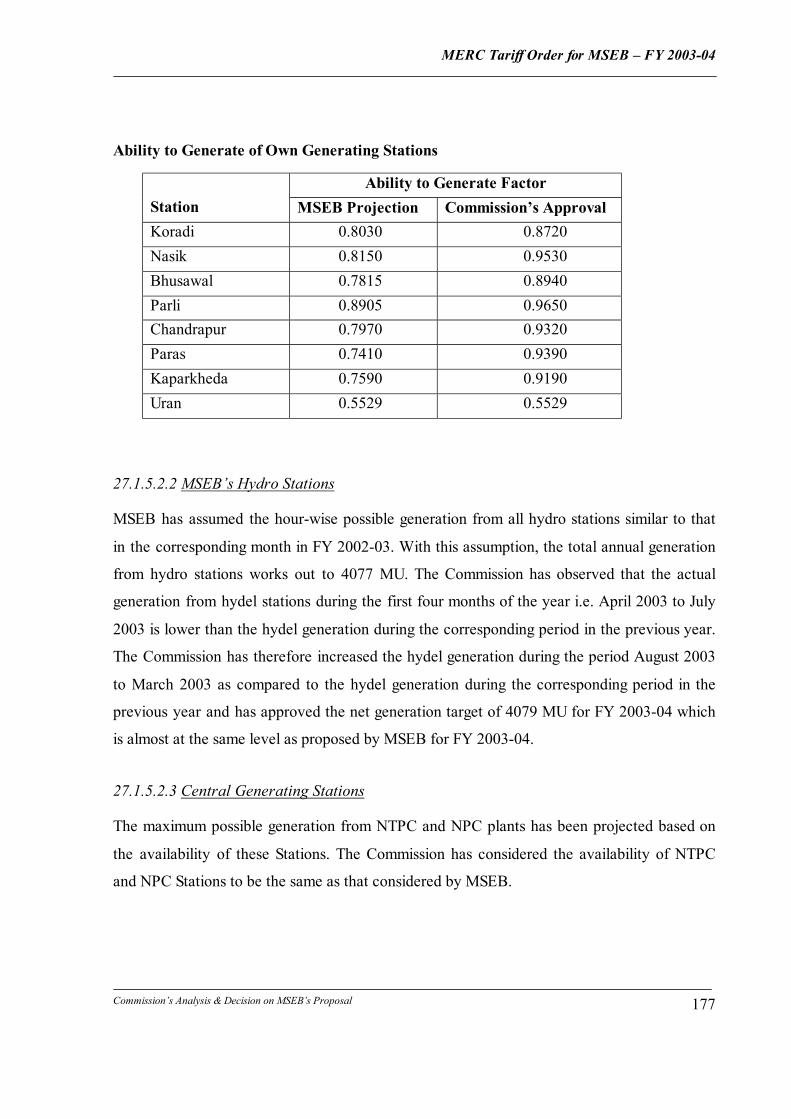

the generation from Hydel Stations at the same level achieved during FY 2002-03, and the generation from the thermal stations based on the ‘ability to generate’ factor.

8. Considering the actual power purchase from April to July 2003 and the month-wise purchase based on merit order scheduling, the total power purchase approved by the Commission for FY 2003-04 is 16182 MU.

9. Though the MSEB has projected load shedding of 1079 MU in FY 2003-04, the Commission is of the opinion that there is no need to resort to load shedding in FY 2003-04, as there is sufficient energy available through own generation and power purchase to meet the projected sales at the T&D loss levels considered by the MSEB.

10. The MSEB had considered a 5% increase in the fuel costs and power purchase costs over the actual costs incurred in FY 2002-03, while projecting the expenditure for FY 2003-04. The Commission has approved the total generation and power purchase costs for FY 2003-04 considering the quantum of actual generation and power purchase for the period of April to July 2003 and estimating the generation and power purchase costs from August 2003 to March 2004 based on a simulation of merit order dispatch and actual average generation and power purchase costs for the period of April to July 2003, subject to heat rate norms and transit loss component. As the actual costs have been considered, the Commission has not considered any escalation in the fuel prices and power purchase costs for the balance period. Further, if there is any change in the fuel prices and power purchase costs vis-à-vis the costs considered by the Commission, the MSEB will recover/refund the same through the FOCA mechanism.

11. The Commission has considered a reduction of 1% in the station heat rate over the levels considered in the Tariff Order for FY 2001-02, as it still continues to be above the norm.

12. In previous Tariff Orders, the Commission had disallowed the transit loss component as a legitimate expense while computing the generation cost. However, the Hon’ble High Court of Mumbai has held that transit losses are a legitimate expense, and the permissible level of transit losses should be determined by the Commission. The Commission has considered transit losses based on the actual level of station-wise transit losses and has assumed a trajectory for reduction in transit losses.

13. The Commission has considered drawal of additional long-term loans to the extent required for capital expenditure and to fund the shortfall in repayment obligations vis-à-vis the provision for depreciation, if any. The opening balance of long-term loans for FY 2003-04 has been computed accordingly, leading to a reduction in the interest costs. Further, the Commission has also disallowed the interest on bonds raised for investment in Dabhol Power Company (DPC), on principles consistent with those considered in the earlier Tariff Orders.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

9

14. The net working capital requirement has been estimated as Rs. 546 crore, by applying the

same principles as in the previous Tariff Order. Considering an average interest rate of 10% for working capital loan, which is the interest rate considered by the MSEB for such loans, the working capital interest allowable has been projected as Rs. 54.6 crore.

15. The Commission has considered provisioning for bad debts at the rate of 1.5% of the sales billed during FY 2003-04, in line with the principles considered in the past Tariff Orders.

16. The Commission has projected lower level of ‘Other expenses’ as compared to the MSEB’s projections, as it has considered interest on security deposit at the average of the past three years’ and lower level of miscellaneous expenses.

17. The Commission has considered the mandatory surplus at the rate of 4.5% of the Net Fixed Assets, at Rs. 433 crore.

18. The net revenue to be recovered through tariffs on sale of electricity have been projected after reducing the Annual Revenue Requirement, due to the following reasons: Revenue earned through FOCA for additional expenses in FY 2003-04 Other Income

19. The Commission has deducted the amount recovered through FOCA for additional expenses incurred in the months of April, May and June 2003 amounting to Rs. 135 crore, from the revenue requirement of FY 2003-04, as the actual generation and power purchase costs incurred during this period have been considered for projecting the total costs in FY 2003-04. Any additional amount recovered by the MSEB through the FOCA formula for increase in costs in FY 2003-04 after June 2003, if any, will be adjusted against the FOCA recoverable henceforth.

20. The Commission has considered a higher Other Income of Rs. 1067 crore as compared to the MSEB’s projection of Rs. 1022 crore, mainly on account of higher projection of interest on delayed payment and recovery from theft of power and wheeling charges.

21. All the directives issued by the Commission in the previous Tariff Orders issued in May 2000 and January 2002 are still applicable, and the MSEB is directed to comply with the same in letter and in spirit.

22. The net revenue requirement allowed by the Commission for FY 2003-04 to be recovered through tariffs is Rs. 12174 crore. The revenue from existing tariff works out to Rs. 12030 crore, leaving an uncovered gap of Rs. 144 crore, with the existing tariff. If the revised tariffs were to be charged for the entire year, then the additional revenue recovered through revised tariffs would be Rs. 144 crore. However, in the current year, the revised tariffs will be in force for only four months of FY 2003-04.

23. The Commission has introduced high load factor incentive and reclassified certain consumer categories, the impact of which cannot be assessed accurately at this point in

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

10

time with the available data. The Commission has hence determined the category-wise tariffs such that the additional revenue recoverable in the remaining four months of FY 2003-04 with revised tariffs is around 62 crore, as compared to the requirement of Rs. 48 crore. However, in case there is any revenue shortfall compared to the Commission’s projections due to the tariff classification changes and other rebates given in this Order, the Commission will consider it in the future.

24. The Commission has adopted certain principles, which are in continuation of the process of tariff rationalisation initiated in the previous Tariff Orders. In general, the movement of tariffs towards the average cost of supply has been maintained, such that inter-class cross-subsidy is reduced gradually, while at the same time ensuring that no consumer category is subject to a tariff shock. The Commission has also further reduced the intra-class cross-subsidy, by reducing the difference between the highest and lowest slab rates.

25. As all the hitherto un-metered consumer categories have been metered, except LT agriculture, the Commission has specified flat rate tariffs only for the un-metered LT agriculture category. The difference in metered tariff and the flat rate tariffs has been increased to incentivize un-metered consumers to opt for metering.

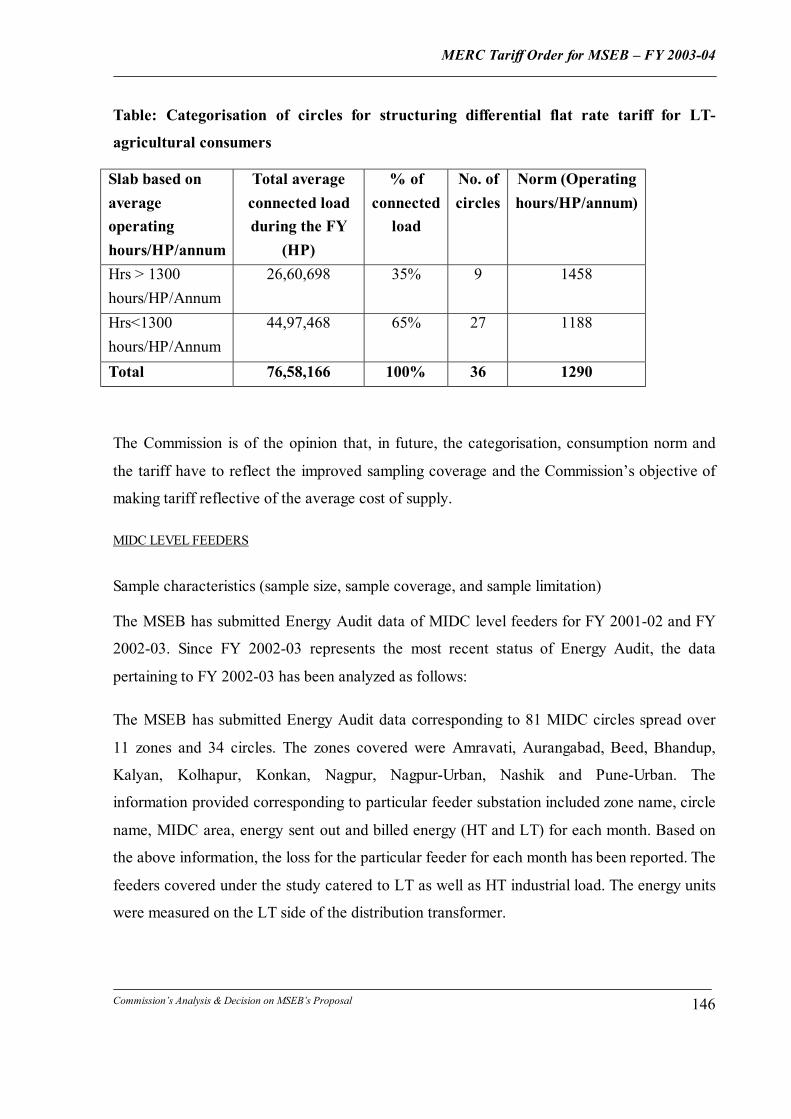

26. The Commission has considered an average consumption norm of 1300 hours/HP/year in case of flat rate LT agricultural consumers, based on the available sample energy audit data submitted by the MSEB. The Commission has attempted to determine the flat rate tariffs for agriculture category such that the tariffs reflect the actual consumption pattern. This has been done by specifying circle-wise differential flat rate tariffs linked to the agriculture consumption norm as established by the energy audit data for that circle. To start with, the Commission has specified two tariff levels, viz. lower tariff for circles with consumption norm lower than the average consumption norm of 1300 hours/HP/year, and higher tariffs for circles with consumption norm higher than the average consumption norm of 1300 hours/HP/year. The Commission hopes that this will incentivize the shift to metered consumption at a faster rate.

27. In the Tariff Order issued in January 2002, the Commission had initiated the process of levying the ‘T & D loss Charge’ for all consumers, in proportion to the average realisation from that category. By introducing this charge, the Commission intended to create awareness among the consumers regarding the additional cost of the excess T&D losses by levying this charge in an explicit manner. Hence, a more or less uniform T & D loss charge had been levied to start with. Moreover, the Commission had declared its intent to differentiate between the various circles/zones for the levy of the T & D loss charge, based on the T & D losses exhibited by the circle/zone in question. As an interim measure, in January 2003, the Commission had declared that 11 circles with T&D loss levels lower than the target loss level of 26.87% would be exempted from payment of

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

11

T&D loss charges. It should be noted that T&D loss charge was not an additional charge and was a part of the regular tariff, which the consumers were always paying though the separation of tariff due to excess T&D losses was not indicated explicitly earlier.

28. The Commission is of the view that the T&D loss charge concept has achieved a certain level of success in that the stakeholders are certainly much more aware of the extent of the problem, and atleast some circles have shown some improvement in the T&D loss levels. However, the Commission is of the view that the T&D loss charge concept cannot be a long-term solution and the problem has to be addressed in some other manner, and hence the T&D loss charge has been withdrawn for all consumer categories in all circles, with effect from December 1, 2003.

29. The problem arises in the assessment of the losses itself. Even if the Commission were to take a strict view that only the technical losses should be allowed and all the commercial losses should be to the MSEB’s account, the problem remains with the assessment of the technical losses. Though the MSEB has submitted in the past that the technical losses could be in the range of around 21%, this number has to be verified through load flow studies. In the absence of any certainty on this issue, the Commission is constrained to accept the target loss level at 26.87% for the purposes of this Order.

30. If the cost of all the excess losses were disallowed, then it is most likely that the MSEB will be unable to meet its daily requirements and will be unable to supply power to its consumers. This is not in the consumers’ interest, and till a viable alternative emerges, the MSEB has to continue to supply electricity to the consumers in the State. The Commission is of the opinion that a pragmatic decision has to be taken in the best long-term interest of the electricity consumers in the State as well as the MSEB. Moreover, this is a transition period and the MSEB is likely to be restructured in line with the principles enunciated in the EA 2003.

31. In this context, the Mumbai Grahak Panchayat (MGP), a S.26 consumer representative has suggested that if the MSEB needed ‘Oxygen’ in the form of tariffs to recover the cost of the excess losses, the consumers would be willing to contribute the same, provided the Commission treated this contribution as a Regulatory Liability owed by the MSEB to the consumers, as this was not part of the MSEB’s rightful revenue requirement. The Commission has given serious thought to this suggestion, and is of the opinion that this may solve the current predicament.

32. The Commission is of the opinion that only subsidizing consumers should contribute to the Regulatory Liability, which would have to be returned by the MSEB in future. Hence, the Regulatory Liability Charge (RLC) has been designed such that all the subsidizing categories contribute the same amount of RLC to keep the MSEB afloat. Subsidized categories cannot be expected to contribute to the Regulatory Liability as they have yet to

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

12

move towards the average cost of supply. Thus, for subsidizing categories, a separate component of tariff has been shown as ‘Regulatory Liability Charge’ which will be used by the MSEB for funding the cost of the excess T&D losses, which will be returned to these consumer categories in future through tariffs.

33. The Regulatory Liability requirement is equal to the cost of the excess losses, i.e. the cost of additional power purchase required on account of the higher energy input requirement. The T & D loss level proposed by the MSEB for FY 2003-04 is 36.62%, as compared to the target of 26.87% set by the Commission. The balance losses of 9.75% equivalent to 6107 MU are thus excess losses vis-à-vis the targets.

34. The net cost of the excess energy input requirement is Rs.947 crore (6107 MU at an average rate of Rs. 1.55 per unit). Thus, there is a need to contribute Rs. 947 crore towards the Regulatory Liability over a period of one year. The average rate of contribution works out to 50 paise per unit for the subsidizing categories, viz. LT commercial, LTPG, HTP I, HTP II and Railways.

35. In future, when the T&D losses are reduced, then the RLC will be returned to these consumer categories through reduction in tariffs. The Commission clarifies that the contribution through RLC will not be recorded and maintained separately for each individual consumer and the category as a whole is expected to get the contribution back.

36. The average cost of supply for FY 2003-04 works out to Rs. 2.83 per unit, which is lower than the average cost of supply considered in FY 2001-02, on account of the lower level of T&D losses considered for tariff determination, as well as the removal of the cost of excess losses while computing the average cost of supply.

37. The Commission has reduced the cross-subsidy between different consumer categories and tariff for all subsidised categories has been specified at least equal to 50% of the average cost of supply.

38. The Commission has attempted to increase the recovery from fixed charges, which ranged around 35% of the fixed costs in the existing tariffs, to around 40% in the revised tariffs. The energy charges have been adjusted in such a way that the average realisation from each consumer category approaches the average cost of supply, while at the same time ensuring that no consumer category faces a tariff shock.

39. The energy charge to be levied for net sale to the TPC has been increased to match the highest cost of power purchase, i.e. 299 p/u.

40. The tariff applicable for sale to Mula Pravara Electric Co-operative Society (MPECS) has been retained at the existing levels. The Commission is separately forwarding a Report on the viability of the MPECS to the Government of Maharashtra (GoM).

41. The rebates/incentives such as power factor incentive, bulk discount and prompt payment incentive have been retained at the existing levels. The power factor penalty has been

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

13

modified such that the penalty is levied in a graded manner similar to the power factor incentive.

42. The Commission is of the opinion that the MSEB faces a threat from movement of consumers having very high consumption to captive generation, under the provisions of the Electricity Act, 2003 (EA 2003). In order to incentivize such high consumption consumers who also contribute a steady load to the MSEB system, the Commission has introduced a Load factor incentive for consumers having Load Factor above 75% based on contract demand. Consumers having load factor over 75% upto 85% will be entitled to a rebate of 0.75% on the energy charges for every percentage point increase in load factor from 75% to 85%. Consumers having a load factor over 85 % will be entitled to rebate of 1% on the energy charges for every percentage point increase in load factor from 85%. The total rebate under this head will be subject to a ceiling of 15% of the energy charges for that consumer. Further, the load factor rebate will be available only if the consumer has no arrears with the MSEB, and payment is made within seven days from the date of the bill or within 5 days of the receipt of the bill, whichever is later.

43. The Commission directs the MSEB to compile data on reactive power consumption by all consumer categories where electronic meters are already installed, as the Commission intends to introduce kVARh tariffs in the subsequent Order. The kVARh consumption data for each billing cycle should be submitted alongwith the next ARR and Tariff Petition.

44. The Commission has increased the differential between tariff applicable for peak hour consumption and off-peak hour consumption by 20 paise per unit, respectively, and off-peak times for the HTP-I and HTP-II categories by 10 paise per unit for peak. The Commission also directs that MSEB should install ToD meters for all consumers with a connected load of over 20 kW, so that ToD tariffs can be availed by these consumers at their option.

45. In the FY 2000-01 Tariff Order, the Commission has directed the MSEB to charge domestic tariffs from certain professional categories if these professionals were using part of their residences for professional work. The Commission clarifies that the domestic tariffs will be applicable only to residential premises used by professionals like Lawyers, Doctors, Chartered Accountants, etc. except for nursing homes and surgical wards/clinics, in furtherance of their professional activity in their residences.

46. The Commission has reclassified the HTP I category to include only those HT industrial and other HT consumers situated in the Mumbai Metropolitan Region (MMR) and Pune Metropolitan Region (PMR), as defined by the State Government. The balance HT industrial and other HT consumers would be classified under HTP II category.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

14

47. In line with the recently announced IT and ITES Policy announced by the GoM and the stated philosophy of the Commission in previous Orders, the Commission has included the Low Tension IT industry and IT enabled services (as defined in the GoM Policy) in the LTPG category, for purposes of tariff.

48. The seasonal category will include all consumers who opt for a seasonal pattern of consumption, without the need for further approval from the Commission. The consumers should approach the MSEB for classification under the seasonal category if their business is such that electricity requirement is seasonal in nature. The shift from seasonal to normal connection and vice-versa can be done only once each year, at the beginning of the year.

49. The additional standby charges of Rs. 20 per kVA per month will be applicable to HT industrial consumers with captive generating units synchronized with the MSEB grid, only on the extent of standby demand, and not the entire contract demand as prevalent currently.

50. The Commission had initiated the process of levying a ‘Reliability Charge’ to begin with, on HTP-I and HTP-II consumers who have been provided with ToD meters, within urban agglomerations in the State, on consumers receiving power supply through Express Feeders and also those within MIDC areas. The MSEB was allowed to impose an additional charge of 25 paise per kWh to these consumers and ensure that they get uninterrupted power supply. However, the MSEB has not progressed very far in implementing the Reliability Charge, even though it would have resulted in additional revenue, which could have been gainfully employed in strengthening/augmenting the system to improve the quality of supply to consumers. MSEB should use the revenue realised from the Reliability Charge to create a fund which can be used to improving the voltage profile and reliability of supply.

51. Conservation of energy through energy efficiency is very essential, to bridge the gap between demand and supply. The objective of energy efficiency is two fold, viz. to increase the generation through energy efficiency at the generation level, and to manage the demand through Demand Side Management (DSM) techniques, which include load shaping as well as reduction in the consumption levels through use of energy efficient devices. The detailed plan should be submitted to the Commission within three months of this Order.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

15

Table 1: Tariff Hike for FY 2003-04

Description MSEB Proposal MERC Approval

Tariff Increase in Rs. Crore* 1462 186

Overall Tariff Increase in %* 12.5% 1.5%

* - if revised tariffs were applicable for the entire year

Table 2: Energy Input Requirement (MU)

MSEB Commission

Sales

Metered 32112 32818

Unmetered 8403 6893

Total Sales 40515 39710

T&D Losses 23407 22942

Energy Input Requirement 63922 62652

T&D loss as a % of energy requirement 36.62% 36.62%$

$ - Based on MSEB’s submission, against target level of 26.87%

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

16

Table 3: Annual Revenue Requirement for FY 2003-04

Sr No

Expense Head MSEB Proposal

(Rs. Crore)

MERC Approval (Rs.Crore)

Remarks

1 Generation 4243 4104 MSEB has considered higher than normative heat rate, transit losses, and escalation in fuel costs

2 Power Purchase 3493 3132 MSEB has considered higher power purchase quantum and escalation in power purchase costs

3 Employee Costs 1695 1655 MSEB has projected higher employee costs despite reducing trend

4 Administration & General expenses

145 139

5 Operation & Maintenance 738 737 6 Depreciation 1585 1578 MSEB has considered a higher

weighted average rate 7 Interest cost 1308 1126 MSEB has considered higher loans

and higher interest on working capital 8 Lease Rental 85 85 9 Provision for doubtful debts 250 181 MSEB has considered provisioning at

the rate of 2% of revenue from sale of electricity

10 Other Expenses 248 206 MSEB has considered higher interest expenditure on consumers’ security deposit

Total Expenses 13790 12943 Add: Surplus 433 433 Total Revenue Requirement 14223 13376 Reduction in Revenue Requirement Revenue earned through

FOCA for FY 2003-04 135 April to June 2003

Other Income 1022 1067 MSEB has projected lower income from interest on delayed payment

Net Revenue Requirement to be recovered through tariffs

13201 12174

Revenue from Existing tariff

12030

Tariff Increase Required 144 Cost of excess T&D losses 947 Average Cost of Supply –

excluding cost of excess T&D losses (Rs./unit)

2.83

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

17

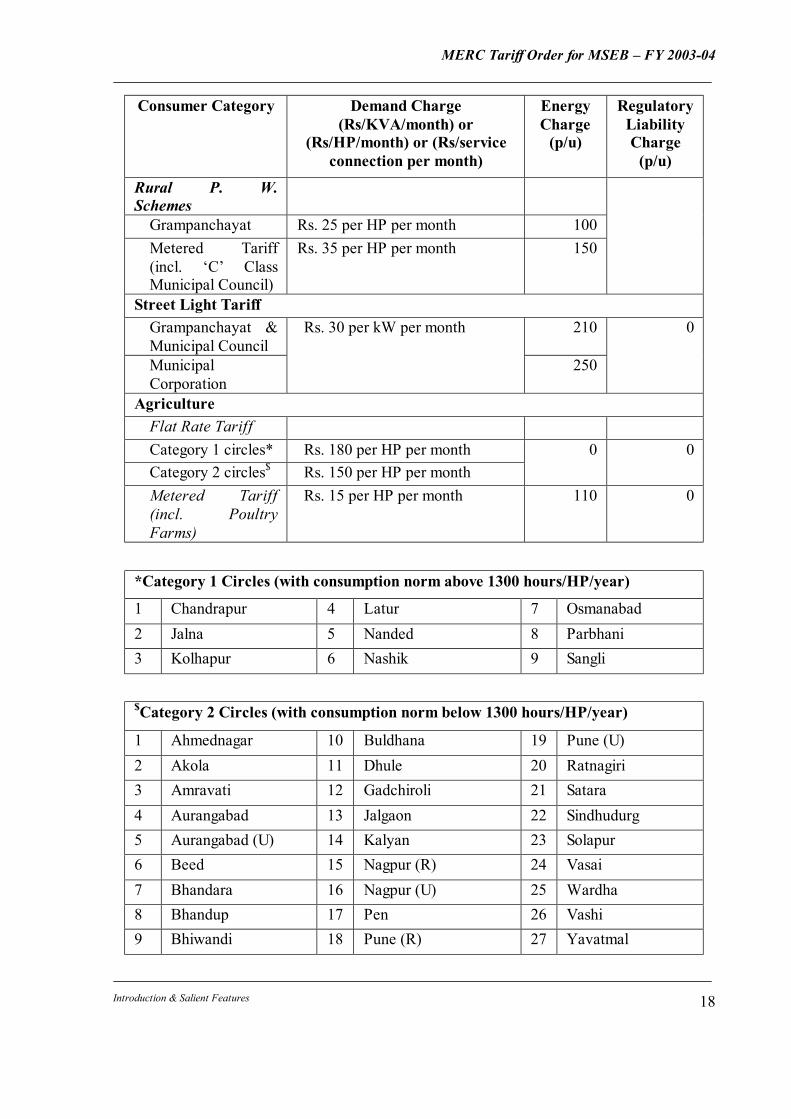

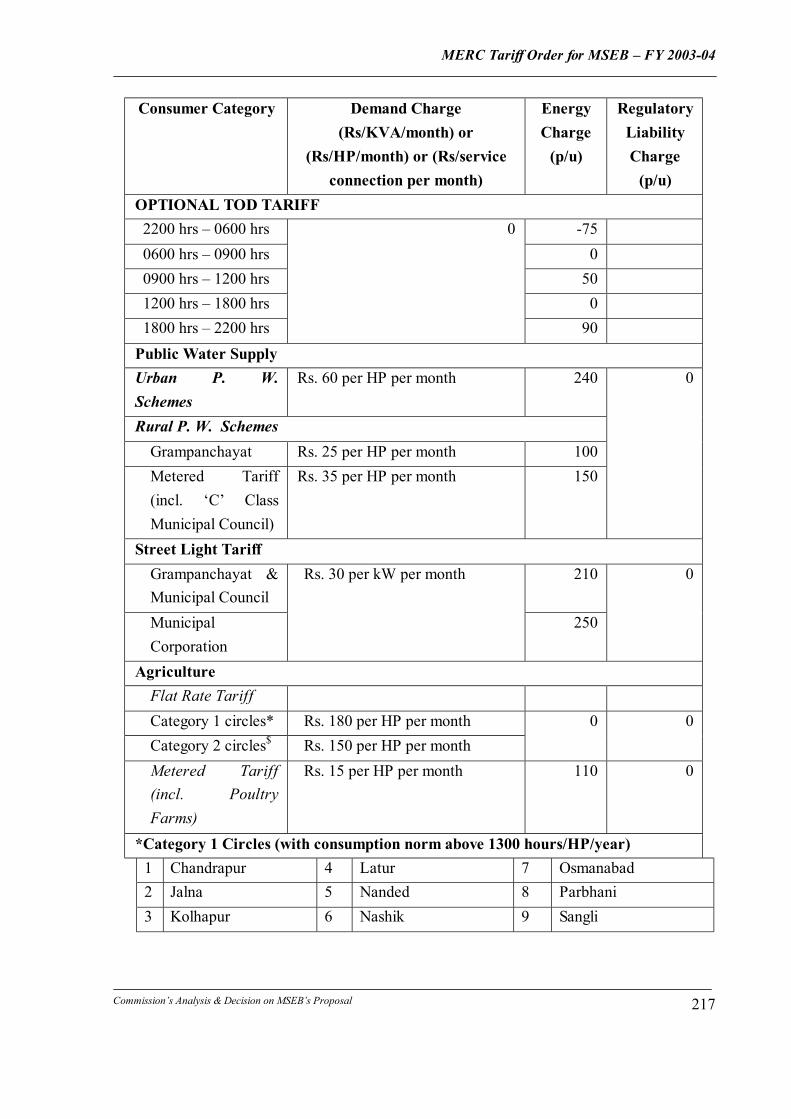

Table 4: Summary of LT Tariff (Effective from December 1, 2003)

Consumer Category Demand Charge (Rs/KVA/month) or

(Rs/HP/month) or (Rs/service connection per month)

Energy Charge

(p/u)

Regulatory Liability Charge

(p/u)

Domestic (LD 1) 0-30 Units Rs. 20 per service connection 125 31-300 Units 290 Above 300 units (only balance Units)

Single Phase: Rs. 40 per service connection; Three Phase: Rs. 100 per service connection; Additional Fixed charge of Rs. 100 per 10 KW load or part thereof above 10 KW load shall be payable.

400

0

Non Domestic (LD2) 0-100 Units 240 101-200 Units 315 Above 200 units (only balance Units)

Single Phase: Rs. 100 per service connection; Three Phase: Rs. 150 per service connection; Additional Fixed Charge of Rs. 150 per 10 KW load or part thereof above 10 KW load shall be payable. Optional LTMD based Tariff will be available for all consumers.

410

50

General Motive Power (LTP-G) – Base Tariff 0-1000 Units 230 Above 1000 Units (only balance Units)

Rs. 60 per HP (Rs. 80.5 per kW) per month for 50% of sanctioned load; Optional MD based tariff will be available for all consumers, irrespective of Contract demand, at Rs. 220/kVA/month

250 50

OPTIONAL TOD TARIFF

2200 hrs – 0600 hrs -75 0600 hrs – 0900 hrs 0 0900 hrs – 1200 hrs 50 1200 hrs – 1800 hrs 0 1800 hrs – 2200 hrs

0

90 Public Water Supply Urban P. W. Schemes

Rs. 60 per HP per month 240 0

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

18

Consumer Category Demand Charge (Rs/KVA/month) or

(Rs/HP/month) or (Rs/service connection per month)

Energy Charge

(p/u)

Regulatory Liability Charge

(p/u)

Rural P. W. Schemes

Grampanchayat Rs. 25 per HP per month 100 Metered Tariff (incl. ‘C’ Class Municipal Council)

Rs. 35 per HP per month 150

Street Light Tariff Grampanchayat & Municipal Council

210

Municipal Corporation

Rs. 30 per kW per month

250

0

Agriculture Flat Rate Tariff Category 1 circles* Rs. 180 per HP per month Category 2 circles$ Rs. 150 per HP per month

0 0

Metered Tariff (incl. Poultry Farms)

Rs. 15 per HP per month 110 0

*Category 1 Circles (with consumption norm above 1300 hours/HP/year)

1 Chandrapur 4 Latur 7 Osmanabad 2 Jalna 5 Nanded 8 Parbhani 3 Kolhapur 6 Nashik 9 Sangli

$Category 2 Circles (with consumption norm below 1300 hours/HP/year)

1 Ahmednagar 10 Buldhana 19 Pune (U) 2 Akola 11 Dhule 20 Ratnagiri 3 Amravati 12 Gadchiroli 21 Satara 4 Aurangabad 13 Jalgaon 22 Sindhudurg 5 Aurangabad (U) 14 Kalyan 23 Solapur 6 Beed 15 Nagpur (R) 24 Vasai 7 Bhandara 16 Nagpur (U) 25 Wardha 8 Bhandup 17 Pen 26 Vashi 9 Bhiwandi 18 Pune (R) 27 Yavatmal

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

19

Notes: FOCA shall be applicable to all categories of consumers. FOCA will be determined

monthly based on the FOCA Formula approved by the Commission. Billing Demand for LTPG and other LT categories opting for MD based tariff :

Monthly Billing Demand will be the higher of the following:

i. Actual Maximum Demand recorded in the month during 0600 hours to 2200 hours ii. 75% of the highest billing demand recorded during preceding eleven months

iii. 50% of the Contract Demand.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

20

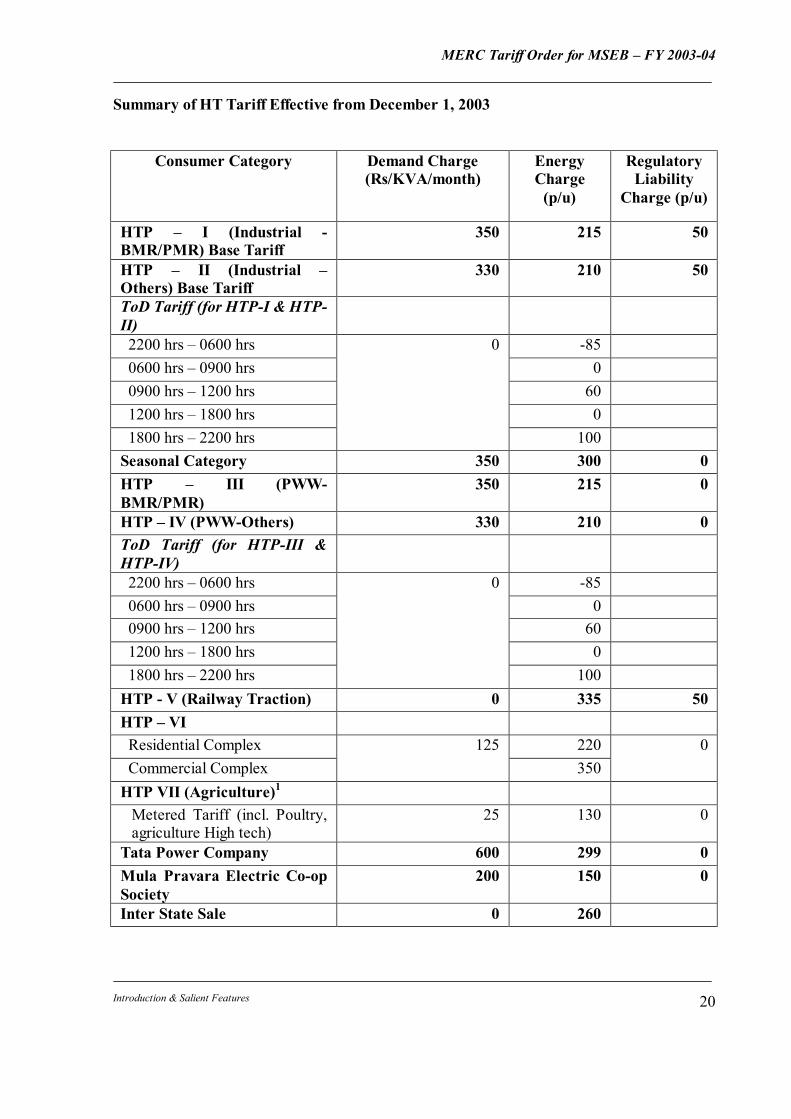

Summary of HT Tariff Effective from December 1, 2003

Consumer Category Demand Charge (Rs/KVA/month)

Energy Charge

(p/u)

Regulatory Liability

Charge (p/u)

HTP – I (Industrial - BMR/PMR) Base Tariff

350 215 50

HTP – II (Industrial – Others) Base Tariff

330 210 50

ToD Tariff (for HTP-I & HTP-II)

2200 hrs – 0600 hrs -85 0600 hrs – 0900 hrs 0 0900 hrs – 1200 hrs 60 1200 hrs – 1800 hrs 0 1800 hrs – 2200 hrs

0

100 Seasonal Category 350 300 0 HTP – III (PWW-BMR/PMR)

350 215 0

HTP – IV (PWW-Others) 330 210 0 ToD Tariff (for HTP-III & HTP-IV)

2200 hrs – 0600 hrs -85 0600 hrs – 0900 hrs 0 0900 hrs – 1200 hrs 60 1200 hrs – 1800 hrs 0 1800 hrs – 2200 hrs

0

100 HTP - V (Railway Traction) 0 335 50 HTP – VI Residential Complex 220 Commercial Complex

125 350

0

HTP VII (Agriculture)1 Metered Tariff (incl. Poultry, agriculture High tech)

25 130 0

Tata Power Company 600 299 0 Mula Pravara Electric Co-op Society

200 150 0

Inter State Sale 0 260

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

21

Notes:

1. HTP VII category includes HT Lift Irrigation Schemes irrespective of ownership 2. FOCA shall be applicable to all categories of consumers. FOCA will be determined

monthly based on the FOCA Formula approved by the Commission 3. Billing Demand definitions:

HT Categories (HTP-I, HTP-II, HTP-III, HTP-IV) Monthly Billing Demand will be the higher of the following: i) Actual Maximum Demand recorded in the month during 0600 hours to 2200 hours

ii) 75% of the highest billing demand recorded during preceding eleven months

iii) 50% of the Contract Demand.

Seasonal Category

During Declared Season

Monthly Billing Demand will be the higher of the following:

i) Actual Maximum Demand recorded in the month during 0600 hours to 2200 hours

ii) 75% of the Contract Demand

iii)50 kVA.

During Declared Off-season

Monthly Billing Demand will be the following:

i) Actual Maximum Demand recorded in the month during 0600 hours to 2200 hours

4. HT Industrial consumers having captive generation facilities synchronized with the grid will pay additional demand charges of Rs. 20 per kVA per month only for the standby contract demand component.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

22

5. Incentives

5.1.2 a) Power Factor Incentive

Whenever the average power factor is more than 0.95, an incentive shall be given at the rate of 1% (one percent) of the amount of the monthly energy bill (excluding FOCA charge, demand charge, electricity duty and regulatory liability charge) for every 1% (one percent) improvement in the power factor above 0.95. For PF of 0.99, the effective incentive will amount to 5% (five percent) reduction in the energy bill and for unity PF, the effective incentive will amount to 7% (seven percent) reduction in the energy bill. The power factor incentive is also applicable for LTP-G consumers who opt for LTMD tariff. Such incentives shall not be applicable for the Railways.

5.1.2 b) Bulk discount

If the consumption of any industrial consumer (availing TOD tariff and having no arrears with the MSEB) exceeds one million units per month, the consumer will get a rebate of 1% on his energy bill (excluding FOCA charge, demand charge, electricity duty and regulatory liability charge) for every one million unit consumption above one million unit subject to a maximum of 5%. The rebate will, however, be allowed only if the bill is paid within seven days from the date of the bill or within 5 days of the receipt of the bill, whichever is later.

6. Disincentives

6.1.1 a) Power factor Penalty

Whenever the average power factor is less than 0.9, penal charges shall be levied at the rate of 2% (two percent) of the amount of the monthly energy bill (excluding FOCA charge, demand charge, electricity duty and regulatory liability charge) for first 1% (one percentage point) fall in the power factor below 0.9, beyond which the penal charges shall be levied at the rate of 1% (one percent) for each percentage point fall in the power factor below 0.89. Such disincentives shall not be applicable for the Railways. The power factor penalty is also applicable for LTP-G consumers who opt for LTMD tariff.

After issue of the Operative Order, the Commission issued a Clarificatory Order on the newly introduced Load Factor Surcharge, in response to queries raised by the MSEB and certain consumers, the details of which have been reproduced below:

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

23

The Load Factor incentive is limited to HTP-I and HTP-II categories only. Further, the load factor rebate will be available only if the consumer has no arrears with the MSEB, and payment is made within seven days from the date of the bill or within 5 days of the receipt of the bill, whichever is later. However, this incentive will be applicable to consumers where payment of arrears in instalments has been granted by the MSEB, and the same being made as scheduled. The MSEB has to take a commercial decision on the issue of how to determine the time frame for which the payments should have been made as scheduled, in order to be eligible for the Load Factor incentive. The Load Factor has been defined below:

Load Factor = Consumption during the month in MU___________

Maximum Consumption Possible during the month in MU

Maximum consumption possible = Contract Demand (kVA) x Actual Power Factor

x (Total no. of hrs during the month less planned load shedding

hours*)

- Interruption/non-supply to the extent of 60 hours in a 30 day month has been built in the scheme.

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

24

OBJECTIONS ON POINTS OF LAW AND PROCEDURE AND THE FINDINGS OF THE COMMISSION

Acceptance of Petition in the context of Pending Public Interest Litigation

N.N.Kale and Associates have requested the Commission not to accept the present Proposal until Public Interest Litigation (PIL) dated March 15, 2003 and application for rejecting the Proposal dated May 5, 2003 have been disposed off. The Commission appreciates the points made by N. N. Kale and Associates regarding the acceptability of the Tariff Petition in the background of the pending PIL and also because of the fact that the MSEB’s Tariff Petition has not been certified by a Cost Accountant. However, the Commission is of the opinion that the mere fact that there is a pending litigation is not sufficient reason for not accepting the Tariff Petition. Moreover, the High Court has not granted any stay on the filing of the Tariff Petition by the MSEB. Approval of Terms and Conditions of Supply Several consumer associations have pointed out that the Proposal has been submitted before approval of the Terms and Conditions of Supply. They have highlighted that MSEB has not submitted the Terms and Conditions of Supply before August 30, 2003 for approval of the Commission. They have pointed out that the Mumbai High Court has ordered the State Commission to necessarily take into consideration the Terms and Conditions of Supply of electricity in so far as they add to the cost of electricity. They have stated that the Terms and Conditions of Supply cannot be separated from the tariff determination process as SLC charges, service connection charges, supervision charges would have an impact on revenue requirement. Various remedies suggested by consumers to deal with the situation are - reject the Tariff Proposal, consider existing "Terms and Conditions of Supply" while approving tariff, carry out public hearing for both the Proposal and the Terms and Conditions of Supply and Commercial Circulars together. The MSEB has submitted that a proposal in respect of the ‘Conditions and Miscellaneous Charges for Supply of Electrical Energy’ as well as Commercial Circulars as prescribed in previous Tariff Order shall be submitted to the Commission in due course. As regards the Terms and Conditions of Supply, the Commission has been of the view that any delay in the issue of the Tariff Order by the Commission would make the implementation

MERC Tariff Order for MSEB – FY 2003-04

Introduction & Salient Features

25

of the Tariff Order difficult, as only 4 months of the current year are remaining. Thus, the Commission is severely constrained to consider this Tariff Order without processing the Terms and Conditions of Supply. The Commission will approve the Terms and Conditions of Supply separately.

ORGANISATION OF THE ORDER

The Order of the Commission regarding the determination of tariff is broadly divided into three parts. The first part consists of a brief history of the tariff determination process and the subsequent quasi-judicial process that it underwent and the operative Order of the Commission passed on December 1, 2003, and the clarifications thereon issued by the Commission. It also gives the framework used by the Commission in evolving the tariff policy, Order and the schedule. It also contains the various objections raised on points of law and procedure during both the phases of public hearings before the Commission and the Commission’s findings thereon. For the sake of convenience, a list of abbreviations with their expanded forms is appended. The second part of the Order lists out the various objections raised by the Objectors in writing as well as during the Public Hearings before the Commission. They have been broadly categorized into seventeen issues and, for the sake of convenience, the various points have been classified under an index, along with page numbers, where the relevant objections have been dealt with. The various objections have been stated briefly, the response of the MSEB has also been stated and the findings of the Commission on each of these points have also been given. The third part of the Order comprises the Commission’s analysis and its decisions on the MSEB’s proposal for revision of Retail Distribution Tariff for FY 2003-04. It briefly enumerates the tariff issues involved, examines the revenue projections of the MSEB, the various cost estimates for the year 2003-04 and the Commission’s reasoning for arriving at acceptable figures with reference to the figures given by the MSEB. Part three also comprises various annexures to this order, comprising of Annexure-I and Annexure-II. Lastly, the philosophy of the determination of domestic tariff, LT tariff and HT tariff has been specified to estimate the income of the MSEB.

MERC Tariff Order for MSEB – FY 2003-04

Abbreviations 26

List of Abbreviations used in the Tariff Order

A&G Administration & General ABT Availability Based Tariff AP Andhra Pradesh APDRP Accelerated Power Development and Reform Programme APERC Andhra Pradesh Electricity Regulatory Commission ARR Annual Revenue Requirement BEE Bureau of Energy Efficiency BSES Bombay Suburban Electric Supply CAG Comptroller And Auditor General CAGR Compounded Annual Growth Rate CBR Conduct of Business Regulations CEA Central Electricity Authority CERC Central Electricity Regulatory Commission CII Confederation Of Indian Industry CIL Coal India Ltd. CPP Captive Power Plant CPSU Central Public Sector Units DPC Dabhol Power Company DPS Delayed Payment Surcharge E(S) Act or ESA Electricity (Supply) Act, 1948 EA 2003 The Electricity Act, 2003 EDP Electronic Data Processing EHV Extra High Voltage ERC Act Electricity Regulatory Commissions Act, 1998 FC Fixed Cost FCA Fuel Cost Adjustment FOCA Fuel and Other Cost Adjustment FY Financial Year GFA Gross Fixed Assets GoM Government of Maharashtra HP Horse Power HT High Tension (or High Voltage) HTP High Tension Power Hz Hertz

MERC Tariff Order for MSEB – FY 2003-04

Abbreviations 27

ICWAI The Institute of Cost and Works Accounts of India IEGC Indian Electricity Grid Code IPP Independent Power Producer IREDA Indian Renewable Energy Development Agency IT Information Technology Section IT & ITES Policy, 2003 IT & ITES Policy, 2003 issued by Energy & Labour Department of the

Government of Maharashtra vide Resolution No. ITP-2003/CR-3311/IND-7, Mantralaya, Mumbai - 400 032 dated July 12, 2003.

IWEA Indian Wind Energy Association kcal Kilo Calories kg Kilograms kV Kilo Volt kVA Kilo Volt Ampere kW Kilo Watt kwh Kilo Watt Hour LD1 Residential or Domestic LT category LD2 Non-Domestic LT category LDC Load Despatch Centre LIS Lift Irrigation System LNG Liquefied Natural Gas LS Load Shedding LT Low Tension (or Low Voltage) LTP-G Low Tension Motive Power Group – General Motive Power MD Maximum Demand MEDA Maharashtra Energy Development Agency MES Military Engineering Services MGP Mumbai Grahak Panchayat MIDC Maharashtra Industrial Development Corporation MkCal Million Kilo Calories MMP Master Metering Plan MMR Mumbai Metropolitan Region MOD Merit Order Dispatch MPECS/Mula Pravara Mula Pravara Electricity Co-operative Society MSEB Maharashtra State Electricity Board MU Million Units (million kWh)

MERC Tariff Order for MSEB – FY 2003-04

Abbreviations 28

MVA Mega Volt Ampere MW Mega Watts NFA Net Fixed Assets NGO Non Government Organisation NPC Nuclear Power Corporation NTC National Textile Corporation NTPC National Thermal Power Corporation O&M Operation & Maintenance OLC On Line Capacity PD Permanently Disconnected PF Power Factor PFC Power Finance Corporation PLF Plant Load Factor PMR Pune Metropolitan Region PPA Power Purchase Agreement PWW Public Water Works REC Rural Electrification Corporation, New Delhi REDAM Renewable Energy Developers Association of Maharashtra RLC Regulatory Liability Charge ROR Rate of Return RR Revenue Requirement SD Security Deposit SERC State Electricity Regulatory Commission SLC Service Line Charges SSI Small Scale Industry STP Software Technology Park T&D Transmission & Distribution TDL charge T&D Loss charge ToD Time-Of-Day TPC Tata Power Company TPS Thermal Power Station UI Unscheduled Interchange VC Variable Cost WTO World Trade Organisation

MERC Tariff Order for MSEB – FY 2003-04

Index 29

PART II: OBJECTIONS RECEIVED, MSEB’s RESPONSE AND THE

COMMISSION’S RULING

1 TARIFF CATEGORY-WISE REPRESENTATIONS .............................................. 32

1.1 INDUSTRY................................................................................................................... 32

1.2 SEASONAL CONSUMERS ............................................................................................. 35

1.3 DIFFERENTIATION BASED ON LOCATION .................................................................... 36

1.4 POWER LOOM............................................................................................................. 38

1.5 AGRICULTURE............................................................................................................ 39

1.6 RAILWAY TRACTION .................................................................................................. 42

1.7 DOMESTIC POWER SUPPLY TO RAILWAYS................................................................... 44

1.8 HTP-VI CATEGORY................................................................................................... 45

1.9 MULA PRAVARA ELECTRIC CO-OPERATIVE SOCIETY (MPECS) ................................ 47

1.10 OTHER CATEGORIES ................................................................................................ 48

1.11 CONSUMER CATEGORIZATION ................................................................................ 50

2 TARIFF DESIGN AND RATES .................................................................................. 54

2.1 GUIDELINES, COST OF SUPPLY/CROSS SUBSIDY, SUBSIDY......................................... 54

2.2 LEVY OF FIXED CHARGES .......................................................................................... 57

2.3 FUEL AND OTHER COSTS ADJUSTMENT (FOCA) ....................................................... 62

2.4 TIME OF DAY (TOD) TARIFF ...................................................................................... 63

2.5 BULK DISCOUNT ........................................................................................................ 65

2.6 POWER FACTOR (PF) INCENTIVE/PENALTY CHARGE ................................................. 67

2.7 RELIABILITY CHARGE ................................................................................................ 68

2.8 OTHERS ...................................................................................................................... 69

3 TARIFF SETTING PROCEDURE............................................................................. 70

4 TRANSMISSION AND DISTRIBUTION LOSSES .................................................. 73

5 REVENUE/REVENUE ARREARS ............................................................................. 78

6 QUALITY OF SUPPLY/SERVICE............................................................................. 83

7 GENERATION AND POWER PURCHASE ............................................................. 88

MERC Tariff Order for MSEB – FY 2003-04

Index 30

8 EXPENDITURE ............................................................................................................ 93

9 INFORMATION SYSTEMS AND METERING ....................................................... 98

10 T&D LOSS CHARGE (TDL).................................................................................. 101

11 SECURITY DEPOSIT (SD) .................................................................................... 103

12 SERVICE LINE CHARGES (SLC) ....................................................................... 104

13 CAPITAL INVESTMENT ...................................................................................... 105

14 ENERGY CONSERVATION AND DEMAND SIDE MANAGEMENT(DSM) 106

15 TRIFURCATION OF MSEB.................................................................................. 108

16 DATA DISCREPANCY/INSUFFICIENCY.......................................................... 109

17 NON-COMPLIANCE WITH COMMISSION DIRECTIVES............................ 110

PART III: COMMISSION’S ANALYSIS AND DECISION ON THE MSEB’S

PROPOSAL

18 APPLICABILITY OF TARIFF REVISION FOR REMAINING PART OF THE

YEAR................................................................................................................................... 114

19 AVERAGE COST OF SUPPLY ............................................................................. 115

20 GOVERNMENT OF MAHARASHTRA SUBSIDY............................................. 115

21 CROSS-SUBSIDY REDUCTION........................................................................... 116

22 RATIONALIZATION OF CATEGORIES ........................................................... 117

23 TIME OF THE DAY TARIFF ................................................................................ 117

24 METERING .............................................................................................................. 119

25 COMPLIANCE WITH COMMISSION’S DIRECTIVES BY MSEB................ 120

MERC Tariff Order for MSEB – FY 2003-04

Index 31

26 PROJECTED ENERGY INPUT REQUIREMENT............................................. 124

26.1 SALES PROJECTIONS ............................................................................................. 124

26.2 ENERGY AUDIT ANALYSIS AND T&D LOSSES ...................................................... 131

26.3 ENERGY INPUT REQUIREMENT.............................................................................. 168

27 EXPENDITURE PROJECTIONS.......................................................................... 169

27.1 GENERATION AND POWER PURCHASE COSTS........................................................ 169

27.2 OTHER HEADS OF EXPENDITURE........................................................................... 193

27.3 ANNUAL REVENUE REQUIREMENT ....................................................................... 200

28 REDUCTION IN ANNUAL REVENUE REQUIREMENT................................ 202

28.1 REVENUE EARNED THROUGH FOCA .................................................................... 202

28.2 OTHER INCOME..................................................................................................... 202

28.3 NET REVENUE REQUIREMENT............................................................................... 202

29 TARIFF DESIGN PRINCIPLES............................................................................ 203

29.1 TREATMENT OF EXCESS T&D LOSSES .................................................................. 204

29.2 GENERAL TARIFF DESIGN PRINCIPLES .................................................................. 207

29.3 ENERGY CONSERVATION ...................................................................................... 213

29.4 RELIABILITY CHARGE ................................................................................... 214

30 REVENUE PROJECTIONS ................................................................................... 221

31 TARIFF HIKE FOR FY 2003-04............................................................................ 221

32 INCENTIVES AND DISINCENTIVES ................................................................. 222

32.1 INCENTIVES........................................................................................................... 222

32.2 DISINCENTIVES ..................................................................................................... 223

32.3 OTHER CHARGES .................................................................................................. 224

33 APPENDIX I 34 APPENDIX II 35 APPENDIX III 36 APPENDIX IV 37 APPENDIX V 37 ANNEXURES

MERC Tariff Order for MSEB – FY 2003-04

Objections Received, Mseb’s Response And The Commission’s Ruling 32

PART II: OBJECTIONS RECEIVED, MSEB’s RESPONSE AND THE

COMMISSION’S RULING

1. TARIFF CATEGORY-WISE REPRESENTATIONS

1.1 Industry

1.1.1 Objections

The industrial sector has strongly objected to the tariff increase proposal of MSEB on the

grounds that the Proposal is against the basic principles of cost reflective tariff and

progressive elimination of cross subsidy established by the Commission in its past Tariff

Orders.

They have contended that the current tariff has been restricting their ability to compete in the

domestic as well as global market. Captive Power Producers Association has pointed out that

the HT consumption has declined by 2.8% during the past year as industry has been moving

through recession and being forced to pay above the average cost of supply. Several small-

scale industry associations have also brought out that the present tariff is affecting their

viability and existence of their units. Pimpri Chinchwad Small Industries Association has

mentioned that 4,000 out of 7,000 SSIs within Pimpri Chinchwad have closed down. The

objectors have submitted that the MSEB, like any other industrial organisation, must accord

the highest priority to cost reduction and productivity improvement to enable reduction in the

tariffs which would help industries in Maharashtra to remain economically viable.

Mahratta Chamber of Commerce and Industry, Finolex Industries Limited and several others

have pointed out that the effective tariff increase proposed by the MSEB for HT industrial

category works out to 23-26%, considering increase in MD charges and energy charges, as

against the average tariff increase of 12.5% projected by MSEB. They have added that if the

proposed increase in HT industrial tariff is accepted, then the tariff to HT industrial

consumers would move further away from the average cost of supply.

The Indian Ferro Alloy Producers’ Association has represented that Ferro Alloy industry

should be accorded a separate category with a special tariff considering high cost of power in

total cost of finished product. Presently, the industry has been operating at 50% of its total

MERC Tariff Order for MSEB – FY 2003-04

Objections Received, Mseb’s Response And The Commission’s Ruling 33

capacity, mainly due to rock bottom prices in international market and high power tariff

prevailing in India. The Association has submitted that to be competitive in the international

and domestic markets, the industry requires power at competitive prices. Power cost in

Maharashtra, at equivalent rate of 8 -10 cents, has been 3-4 times that of Europe, South

Africa, Australia, USA and Canada. Power cost in Maharashtra has to be also competitive

vis – à - vis other States such as Andhra Pradesh, Orissa, West Bengal, Chhattisgarh,

Meghalaya, etc., which have implemented special tariffs for the ferro alloy industry. The

Association has suggested that industry should be offered tariffs such that it is the lower of

international tariffs and NTPC rates. The tariff should be based on actual T&D losses incurred

by MSEB in supplying power to these industries and should not account for any cross

subsidies.

R L Steels Limited has brought out that the steel industry, whose major inputs are steel and

electricity, is faced with severe competition from China, whose end product price is at the

same level as the raw material cost in India, and has hence been facing a survival problem. If

the industry has to close down on account of higher tariff, MSEB would lose paying

consumers.

Maharashtra Elektrosmelt Limited has requested the Commission to consider telescopic

incentive for maintaining high load factor. They have proposed a discount of 40% for a load

factor range of 50 to 60%, and 50% for load factor greater than 60%.

Maharashtra State Coop Textile Federation Limited has also represented that under the

Agreement on Textile and Clothing (ATC), all quotas restricting textile trade are going to be

eliminated by December 31, 2004 with one global market. To compete effectively, they

would need electricity at internationally competitive rates.

Century Enka Limited, Garware Polyester Ltd, R L Steels Limited and several other

industrial consumers have requested for a separate tariff category for EHV consumers, with

lower tariff as compared to tariff of other industrial consumers supplied at 11kV and 33kV

connection. Lower tariff to EHV consumers is justified on account of lower investments in

infrastructure, lower cost of maintenance and substantially lower transmission and

distribution losses.

MERC Tariff Order for MSEB – FY 2003-04

Objections Received, Mseb’s Response And The Commission’s Ruling 34

Industry has also brought out that any further increase in tariff may force them to opt for

cheaper sources of power such as CPP or other sources in pursuit of competitiveness.

1.1.2 MSEB’s Response

MSEB has responded that the Tariff Proposal has been used as a means of informing the

Commission and the public as to how the MSEB intends to improve its financial viability

through tariffs. The MSEB has added that the Tariff Proposal has detailed the reasons that

have compelled it to propose the tariff hike.

On the issue of separate tariff category for ferro-alloy industries, MSEB has pointed out that

such a move is against the principles of tariff rationalization established by the Commission

in its earlier Tariff Orders.

1.1.3 Commission’s Ruling

The Commission is aware of the problems faced by the industrial consumers and has taken

due care while framing the tariffs. The Commission has rejected MSEB’s Proposal for

increasing tariff for subsidizing categories and has continued the process of gradually

reducing the cross-subsidy burden on subsidizing consumers, including industrial consumers.

The aim of the Commission, while determining the tariffs, has been to ensure that the overall

tariff for the subsidizing consumers is reduced in relation to the average cost of supply.

The Commission is of the opinion that the MSEB faces a threat from movement of

consumers, having very high consumption, to captive generation, under the provisions of the

Electricity Act, 2003 (EA 2003). In order to incentivize such consumers with high level of

steady consumption to remain with the MSEB, the Commission has introduced a Load factor

incentive for consumers having Load Factor above 75% based on contract demand. The

details of the Load factor incentive have been elaborated in the Section on General Tariff

Design Principles, subsequently.

As regards determination of separate tariffs for the EHV and HV category, the Commission

earlier had commissioned a study to determine the voltage-level wise cost of supply. The

MERC Tariff Order for MSEB – FY 2003-04

Objections Received, Mseb’s Response And The Commission’s Ruling 35

study has remained inconclusive on account of data inadequacy. Hence, the Commission has

been constrained to continue, except for rationalising definition, the present tariff

categorisation for HT consumers. However, the Commission would progressively work

towards determining voltage-wise cost to serve and subsequently consumer-wise cost to

serve. The Commission hereby directs MSEB to start maintaining Voltage-level wise asset

classification.

1.2 Seasonal Consumers

1.2.1 Objections

Freshtop Fruits Limited has requested to categorize themselves as HTP-II Seasonal Consumer

Category as their export activity is limited to grape season which lasts for a period of 60 days

in a year. Several other consumers have also approached the Commission to categorise them

as Seasonal Consumers and approve the same status.

1.2.2 MSEB’s Response

MSEB has refrained from responding on this issue, stating that no specific objection has been

raised with reference to the Tariff Proposal.

1.2.3 Commission’s Ruling

The Commission clarifies that the seasonal category will include all such manufacturers /

processors who opt for a seasonal pattern of consumption, including but not restricted to those

as defined by the Commission earlier, without the need for further approval from the

Commission. The consumers should approach the MSEB for classification under the seasonal

category if their business is such that electricity requirement is seasonal in nature. The shift

from seasonal to normal connection and vice-versa can be done only once each year, at the

beginning of the year. Further for a seasonal consumer during Declared Off-season.

MERC Tariff Order for MSEB – FY 2003-04

Objections Received, Mseb’s Response And The Commission’s Ruling 36

1.3 Differentiation based on Location

1.3.1 Objections

Adv. M. G. Kimmatkar of Vidarbha Statutory Development Board (VSDB) has suggested

that the ‘tariff’ should not be uniform across the MSEB’s license area. The consumers in

regions away from the generating stations must pay the transmission and distribution

expenses. Vidarbha Iron and Steel Corporation Limited has pointed out that industry in their

region have been incurring cost of transportation on its inputs and outputs as it is away from

source and market. However, they do not get any compensating benefit for being closer to

electricity generating units. The principle of “User Pays” should be rigidly applied to ensure

financial and economic justice to Vidarbha. Further, VSDB has pointed out that the tariff

should be structured to compensate the Vidarbha Region for the economic loss and

environmental degradation arising out of generation of power. Industries in Vidarbha region

have sought relief to boost their commercial viability on the grounds that the generation assets

of the MSEB are primarily concentrated in the Vidarbha region, while the load centres are

located in Western Maharashtra. Thus, consumers of Vidarbha region should not be required

to bear the cost of T&D losses sustained in the transport of energy to Western Maharashtra.

Other consumers in the region have requested to extend this concept to categories other than

industrial HT tariff category as well.

VSDB has pointed out that the large cross-subsidies to specific sections such as, power loom

industries and lift irrigation schemes, which are located in Western Maharashtra, directly or

indirectly results in cross-subsidy by underdeveloped region to developed regions of Western

Maharashtra. To prevent such a situation, the different cross-subsidy should be calculated for

each region separately and the tariff increase for each region should be made proportional to

the subsidy level received by the region.

Chamber of Marathwada Industries and Agriculture has requested the Commission to clarify

applicability of HTP-I category to Nashik, Aurangabad, Waluj, Chikalthana, Chitegaon in

light of the Commission’s Order to consider all industrial consumers even above 500 kVA

outside Mumbai and Pune under HTP-II Category.

MERC Tariff Order for MSEB – FY 2003-04

Objections Received, Mseb’s Response And The Commission’s Ruling 37

Citizens Forum has represented that reducing the difference in tariff between HTP-I and HTP-

II category would have an adverse impact on backward areas. Several objectors have also

complained about the acute discrimination in load shedding practiced by the MSEB between

Mumbai/Pune and other less-developed areas, despite the same tariffs being proposed for the

two regions.

1.3.2 MSEB’s Response

The MSEB has submitted that it has adhered to the stand taken by the Commission in its

previous Tariff Orders that the consumers located near pit head sites should not be charged

lower rates than those situated farther away. The MSEB has added that the Generating

Stations happen to be in the eastern part of the State, as the fuel source is available there

locally, while the generation is done for the benefit of the entire State and should be made

available on equitable basis without any preferential treatment to any of the grid constituents.

Further, the Maharashtra State grid is being treated as a single unit with pooled resources.

MSEB has submitted that the current classification of HTP-1 and HTP-II has been based on

classification as per tariff circular approved by the Commission. MSEB has further clarified

that narrowing gap in fixed charges for HTP I and II is essential to facilitate tariff

rationalisation and reduction of categories in near future.

1.3.3 Commission’s Ruling

As discussed in the earlier Orders, the Commission is of the opinion that differential tariffs

for selected regions is not advisable, as this can give rise to similar demands from other

regions as well. The Commission is of the opinion that VSDB’s suggestion that the tariff for

each region should be computed separately based on the cross - subsidy given by that region

is not practical, as each region has a different consumer mix, and the inter-region cross-

subsidy is difficult to assess. However, the Commission has decided to retain the HTP-I and

HTP-II categories, with higher tariffs for HTP-I category. The Commission has also

reclassified the HTP I category to include only those HT industrial and other HT consumers